Notícias do Mercado

-

23:50

Japan: Monetary Base, y/y, February +55.7% (forecast +54.2%)

-

23:29

Commodities. Daily history for March 03’2014:

(raw materials / closing price /% change)

Gold $1,352.4 +9.90 +0.74%

ICE Brent Crude Oil $111.20 +2.13 +1.95%

NYMEX Crude Oil $104.86 +1.07 +1.03%

-

23:24

Stocks. Daily history for March 03’2014:

(index / closing price / change items /% change)Nikkei 14,652.23 -188.84 -1.27 %

Hang Seng 22,500.67 -336.2 -1.47 %

Shanghai Composite 2,075.23 +18.93 +0.92 %

S&P 1,845.73 -13.72 -0.74 %

NASDAQ Composite 4,277.3 -30.82 -0.72 %

Dow 16,168.03 -153.68 -0.94 %

FTSE 6,708.35 -101.35 -1.49 %

CAC 4,290.87 -117.21 -2.66 %

DAX 9,358.89 -333.19 -3.44 % -

23:19

Currencies. Daily history for March 03'2014:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,3834 +0,24%

GBP/USD $1,6765 +0,13%

USD/CHF Chf0,8732 -0,70%

USD/JPY Y101,44 -0,34%

EUR/JPY Y139,31 -0,84%

GBP/JPY Y169,04 -0,81%

AUD/USD $0,8935 +0,15%

NZD/USD $0,8370 -0,14%

USD/CAD C$1,1075 +0,04%

-

23:02

Schedule for today, Tuesday, March 04’2014:

(time / country / index / period / previous value / forecast)

00:30 Australia Building Permits, m/m January -2.9% +0.7%

00:30 Australia Building Permits, y/y January +21.8%

00:30 Australia Current Account, bln Quarter IV -12.7 -10.1

01:30 Japan Labor Cash Earnings, YoY January +0.8% +0.3%

03:30 Australia Announcement of the RBA decision on the discount rate 2.50% 2.50%

03:30 Australia RBA Rate Statement

03:30 United Kingdom Halifax house price index 3m Y/Y February +7.3%

08:00 United Kingdom Halifax house price index February +1.1% +0.6%

09:30 United Kingdom PMI Construction February 64.6 63.6

10:00 Eurozone Producer Price Index, MoM January +0.2% 0.0%

10:00 Eurozone Producer Price Index (YoY) January -0.8% -1.4%

10:30 United Kingdom BOE Deputy Governor for Financial Stability Jon Cunliffe speaks

21:30 U.S. API Crude Oil Inventories February +0.8

22:30 Australia AIG Services Index February 49.3 -

20:01

Dow 16,164.36 -157.35 -0.96%, Nasdaq 4,278.56 -29.56 -0.69%, S&P 500 1,846.26 -13.19 -0.71%

-

19:20

American focus : the dollar rose

The U.S. dollar strengthened against major currencies on the back of strong U.S. macro data . U.S. consumer spending rose in January, more than forecast , together with a sharp increase in income , which increases the likelihood that the biggest part of the economy can sustain growth in early 2014 . This was stated in the report, which was submitted to the Ministry of Commerce . According to consumer spending , which accounts for about 70 percent of the economy , rose in January by 0.4 percent after a 0.1 percent increase in the previous month , which was revised to 0.4 %. Experts predicted that the value of this index will rise by only 0.2 %. We also add that the amount of consumer income increased by 0.3 % , after a zero change in December. Expected that revenues will grow by 0.2%. Today's report confirms recent data that indicate that Americans are beginning to overcome the effect of the severe winter , and confidence in the world's largest economy will grow.

Manufacturing activity in the U.S. rebounded in February after its weakening due to the weather in January, although production decreased . This is according to the Institute for Supply Management (ISM). According to the report , the Purchasing Managers Index (PMI) for the manufacturing U.S. in February rose to 53.2 after an unexpected decline to a minimum of 51.3 in January. Index value above 50 indicates growth in the sector of activity . Economists had expected the index to rise in February to 52.3 .

In turn, the final data from Markit showed that business conditions in the U.S. manufacturing sector improved in February compared with the previous month , and were slightly higher than those reported in the initial assessment . Corresponding PMI rose to 57.1 points, compared with a final reading for January at 53.7 , and a preliminary estimate at around 56.7 .

Little support for the euro had earlier data on the index of manufacturing activity. Recall that the growth in the eurozone manufacturing sector weakened in February, but to a lesser extent than previously . This was stated in the final data , which were published today Markit Economics. According to the report , the seasonally adjusted purchasing managers' index for the manufacturing fell to 53.2 in February from 54 in January , the highest reading in 32 months . We add that the decline in February was the first in five months. Result was also slightly higher than previously estimated - at 53 points. The index currently remains above the mark of 50 points , which separates growth from contraction for the eighth consecutive month.

We also learned that the manufacturing sector continued to show growth in Germany in February , and has expanded more than initially expected. According to the report , the manufacturing purchasing managers index from Markit / BME fell to 54.8 points in February from January's 32-month high of 56.5 . Recall that originally reported on the significance of this indicator at the level of 54.7 points. The index remains above the neutral mark of 50 points for the eighth consecutive month.

The yen rose against the dollar as a result of increased demand for safe-haven currencies after entering the Russian armed forces on the territory of Ukraine. It was learned that U.S. Secretary of State tomorrow John Kerry will travel to Kiev to meet with Ukrainian leaders and likely offer support. Tension in the region has reached its peak since the " cold war ." In addition , the White House announced the termination of countries G7 ( Canada, France, Germany, Italy, Japan, the UK and the U.S.) up to the summit of "eight " in Sochi . G7 countries expressed their support for the sovereignty and territorial integrity of Ukraine and intend to support the country in dealing with the IMF to draw up a new lending program .

Pound hardly reacted to the British data , which showed that the UK manufacturing sector continued its expansion in February , registering with several large pace than in the previous month . It became known from the survey results , which were released Markit Economics and the Royal Institute of Purchasing and Supply (CIPS). According to the report , the seasonally adjusted purchasing managers' index for the manufacturing sector rose in February to a level of 56.9 , compared with 56.6 in January , the figure for which was revised down from 56.7 . A reading above 50 indicates an increase in activity, while a drop below indicates contraction. The index currently remains above the neutral point of the eleventh month in a row .

-

18:20

European stocks close

European stocks plunged the most in more than a month, retreating after reaching a six-year high last week, as investor concern increased that the escalating tension in Ukraine will hurt corporate earnings.

The Stoxx Europe 600 Index dropped 2.3 percent to 330.36 at the close of trading, its biggest decline since Jan. 24. Of the equity benchmark’s 600 members, 575 retreated, while 19 rose. The measure advanced 4.8 percent in February as Federal Reserve Chair Janet Yellen pledged to follow her predecessor’s policy on economic stimulus.

The standoff over Ukraine intensified over the weekend as Russian President Vladimir Putin got parliamentary approval to send troops into the country. The former Soviet state put its military on combat readiness as Russian-speaking forces arrived outside the Ukrainian infantry base at Privolnoye on the Crimean peninsula.

China’s Purchasing Managers’ Index for February fell to 50.2 from 50.5 in January, according to official data released on March 1. A number above 50 indicates expansion. A private PMI by HSBC Holdings Plc. and Markit Economics signaled contraction, slipping to 48.5 from 49.5.

An index of euro-area manufacturing output based on a survey of purchasing managers rose to 53.2 in February, compared with the preliminary estimate of 53, according to a final reading from Markit.

National benchmark indexes retreated in 17 of the 18 western-European markets today. The stock market in Athens was closed for a holiday. France’s CAC 40 lost 2.7 percent. Germany’s DAX slipped 3.4 percent, for its biggest drop since November 2011. The U.K.’s FTSE 100 declined 1.5 percent.

Carlsberg, which owns Russia’s Baltika Breweries, slid 5.3 percent to 540.50 euros.

Nokian Renkaat Oyj lost 6.6 percent to 30.35 euros. The Nordic region’s largest tiremaker got about 35 percent of its revenue from the Russian region in 2012, according to data compiled by Bloomberg.

Metro AG retreated 5.4 percent to 28.41 euros. Germany’s biggest retailer said on Jan. 20 that it plans to proceed with an initial public offering of its Russian cash and carry business to raise money for expansion.

Bouygues declined 1.8 percent to 28.70 euros. Chief Executive Officer Martin Bouygues met with French President Francois Hollande on Feb. 27 to seek government support for the purchase of SFR, Le Journal du Dimanche reported, citing people close to the CEO.

Kuehne & Nagel International AG lost 3.1 percent to 121.70 francs. The world’s biggest sea-freight forwarder reported 2013 earnings before interest and taxes rose 20 percent last year to 761 million francs ($865 million). Analysts had forecast 763.8 million francs.

-

17:00

European stocks closed in minus: FTSE 100 6,707.6 -102.10 -1.50 %, CAC 40 4,291.48 -116.60 -2.65 %, DAX 9,371.27 -320.81 -3.31 %

-

16:42

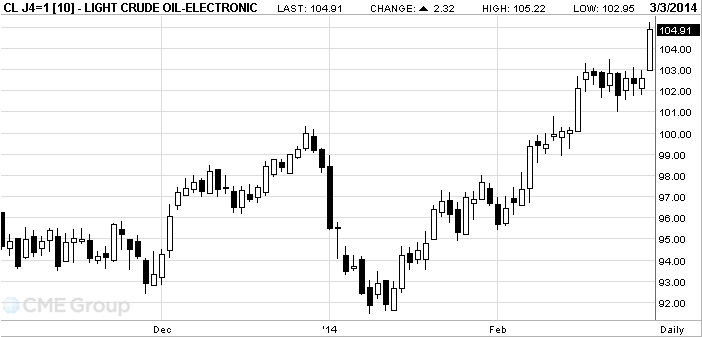

Oil rose

Brent crude surged to a two-month high amid escalating tension between

The European benchmark climbed as much as 3 percent, boosting its premium to WTI. Ukraine mobilized its army reserves as Russia seized control of the Black Sea region of Crimea. The U.S. is weighing sanctions against Moscow during the worst standoff between the West and Russia since the Cold War ended. WTI gained on speculation supplies at Cushing, Oklahoma, slid.

Brent for April settlement climbed $2.73, or 2.5 percent, to $111.80 a barrel at 11 a.m. New York time on the London-based ICE Futures Europe exchange. It rose to $112.39 earlier, the highest level since Dec. 30. Volume was double the 100-day average.

WTI for April delivery gained $2.51, or 2.4 percent, to $105.10 a barrel on the New York Mercantile Exchange. Earlier, it touched $105.22, the most since Sept. 20. Volume was 82 percent above the 100-day average. Brent’s premium over WTI was $6.70, up from $6.48 on Feb. 28, the narrowest level since October.

-

16:20

Gold rose to a four - month high

Gold prices rose more than 1 percent because of the worsening situation in the Crimea.

February price rose by 7 percent , the biggest increase since July , mainly due to slow economic growth in China and the U.S. and Ukrainian crisis.

The major industrialized countries of the " Big Seven " , condemned the invasion of Russian troops in Ukraine and suspended preparations for the summit " Big Eight ", which was to be held in Sochi in June.

European Commission President Jose Manuel Barroso said today that an emergency EU summit to assist Ukraine will be held in the shortest time. He assured that the rescue plan had already been developed in conjunction with the IMF. According to forecasts, Ukraine needs about $ 35 billion over the next two years.

German Chancellor Angela Merkel expressed concern over the events taking place in Ukraine, and noted that it is too late to resolve the situation through political means . French Foreign Minister Fabius suggested that Russia must conduct diplomatic negotiations .

" Obviously, if the situation is not resolved , it can cause economic disruption due to rising prices for oil and gas , trade sanctions and increased global tensions that may threaten the unstable global economic recovery ," - said analyst Edward Meir INTL FCStone .

On the physical market shows no signs of increasing demand from jewelers. Margins on bullion in Singapore remained at last week's $ 0.80 per ounce to the spot price in London.

Gold mining in Australia, occupying the second place in the world on this indicator in 2013 was the highest in 10 years due to improved ore.

The cost of the April gold futures on the COMEX today rose to $ 1354.30 per ounce.

-

15:01

U.S.: Construction Spending, m/m, January +0.1% (forecast 0.0%)

-

15:00

U.S.: ISM Manufacturing, February 53.2 (forecast 52.3)

-

14:36

U.S. Stocks open: Dow 16,258.58 -63.13 -0.39%, Nasdaq 4,260.07 -48.05 -1.12%, S&P 1,844.98 -14.47 -0.78%

-

14:29

Before the bell: S&P futures -0.81%, Nasdaq futures -0.84%

Global markets:

U.S. stock-index futures fell as Russia’s threat to invade Ukraine sent investors searching for havens.

Nikkei 14,652.23 -188.84 -1.27%

Hang Seng 22,500.67 -336.29 -1.47%

Shanghai Composite 2,075.23 +18.93 +0.92%

FTSE 6,700.72 -108.98 -1.60 %

CAC 4,307.67 -100.41 -2.28 %

DAX 9,410.28 -281.80 -2.91 %

Crude oil $104.07 (+1.44%)

Gold $1348.00 (+2.00%).

-

14:00

U.S.: Manufacturing PMI, February 57.1 (forecast 56.7)

-

13:45

Option expiries for today's 1400GMT cut

USD/JPY Y101.50, Y102.00, Y102.30, Y102.50, Y103.00, Y104.00

EUR/USD $1.3650, $1.3675, $1.3710, $1.3800, $1.3825

AUD/USD $0.8800, $0.8860, $0.8900, $0.8920, $0.9000, $0.9100

EUR/GBP stg0.8200, stg0.8250/55

USD/CAD Cad1.1100

GBP/USD $1.6575, $1.6600, $1.6625, $1.6650, $1.6700, $1.6900

EUR/JPY Y139.50

-

13:32

U.S.: PCE price index ex food, energy, m/m, January +0.1% (forecast +0.1%)

-

13:32

U.S.: PCE price index ex food, energy, Y/Y, January +1.2%

-

13:31

U.S.: Personal spending , January +0.4% (forecast +0.2%)

-

13:31

U.S.: Personal Income, m/m, January +0.3% (forecast +0.2%)

-

13:30

Canada: Industrial Product Prices, m/m, January +1.4% (forecast +0.9%)

-

13:30

Canada: Raw Material Price Index, January +2.6% (forecast +2.3%)

-

13:15

European session: The yen has risen considerably against the U.S. dollar

Data

00:00 Australia HIA New Home Sales, m/m January -0.4% +0.5%

00:30 Australia ANZ Job Advertisements (MoM) February -0.3% +5.1%

00:30 Australia Company Operating Profits Quarter IV +3.9% +2.3% +1.7%

01:00 China Non-Manufacturing PMI February 53.4 55.0

01:45 China HSBC Manufacturing PMI (Finally) February 48.3 48.5 48.5

05:30 Australia Commodity Prices, Y/Y February -9.9% -12.1%

08:30 Switzerland Manufacturing PMI February 56.1 57.2 57.6

08:48 France Manufacturing PMI (Finally) February 48.5 49.7

08:53 Germany Manufacturing PMI (Finally) February 54.7 54.8

08:58 Eurozone Manufacturing PMI (Finally) February 53.0 53.0 53.2

09:30 United Kingdom Purchasing Manager Index Manufacturing February 56.7 56.9 56.9

09:30 United Kingdom Net Lending to Individuals, bln January 2.3 2.5 2.1

09:30 United Kingdom Mortgage Approvals July 72.79 Revised From 71.64 72.00 76.94

Rate of the euro retreated from the maximum values against the dollar, while returning to the levels of the session. Little support was data on index of industrial activity , but interest in him was short-lived , and attention gradually began to switch to U.S. reports , which caused the fall of the euro currency . Recall that the growth in the eurozone manufacturing sector weakened in February, but to a lesser extent than previously . This was stated in the final data , which were published earlier today by Markit Economics. According to the report , the seasonally adjusted purchasing managers' index for the manufacturing fell to 53.2 in February from 54 in January , the highest reading in 32 months . We add that the decline in February was the first in five months. Result was also slightly higher than previously estimated - at 53 points. The index currently remains above the mark of 50 points , which separates growth from contraction for the eighth consecutive month.

We also learned that the manufacturing sector continued to show growth in Germany in February , and has expanded more than initially expected. According to the report , the manufacturing purchasing managers index from Markit / BME fell to 54.8 points in February from January's 32-month high of 56.5 . Recall that originally reported on the significance of this indicator at the level of 54.7 points. The index remains above the neutral mark of 50 points for the eighth consecutive month.

The yen rose against the dollar significantly as a result of increased demand for safe-haven currencies after entering the Russian armed forces on the territory of Ukraine. It was learned that U.S. Secretary of State tomorrow John Kerry will travel to Kiev to meet with Ukrainian leaders and likely offer support. Tension in the region has reached its peak since the " cold war ." In addition , the White House announced the termination of countries G7 ( Canada, France, Germany, Italy, Japan, the UK and the U.S.) up to the summit of "eight " in Sochi . G7 countries expressed their support for the sovereignty and territorial integrity of Ukraine and intend to support the country in dealing with the IMF to draw up a new lending program .

Pound shows sharp fluctuations against the dollar, but in general , trading in a small range. On the dynamics of trade influenced the British data , which showed that the UK manufacturing sector continued its expansion in February , registering with several large pace than in the previous month . It became known from the survey results , which were released Markit Economics and the Royal Institute of Purchasing and Supply (CIPS). According to the report , the seasonally adjusted purchasing managers' index for the manufacturing sector rose in February to a level of 56.9 , compared with 56.6 in January , the figure for which was revised down from 56.7 . A reading above 50 indicates an increase in activity, while a drop below indicates contraction. The index currently remains above the neutral point of the eleventh month in a row .

EUR / USD: during the European session, the pair fell to $ 1.3758

GBP / USD: during the European session, the pair traded in the range of $ 1.6700 -$ 1.6750

USD / JPY: during the European session, the pair dropped to Y101.19

At 13:30 GMT , Canada will present the raw material price index for January, while the U.S. will release the main index for personal consumption expenditures for January and will report on changes in the level of expenses for January . At 14:30 GMT , Canada will release PMI index for the manufacturing of RBC in February. At 15:00 GMT the U.S. will release the ISM manufacturing index for February. At 23:50 GMT , Japan will announce to the change in the monetary base in February.

-

13:00

Orders

EUR/USD

Offers $1.3920, $1.3900, $1.3850/60

Bids $1.3755/40, $1.3710/00, $1.3645/40

GBP/USD

Offers $1.6880, $1.6840/50, $1.6795/800, $1.6770/80

Bids $1.6655/50, $1.6605/00, $1.6585/80, $1.6555/50

AUD/USD

Offers $0.9100, $0.9045/50, $0.9000, $0.8985/90

Bids $0.8850, $0.8800

EUR/GBP

Offers stg0.8300/05, stg0.8265/70

Bids stg0.8190-80, stg0.8150, stg0.8120, stg0.8100

EUR/JPY

Offers Y141.50, Y141.00, Y140.75/80, Y140.30

Bids Y139.00, Y138.75/80

USD/JPY

Offers Y102.90/00, Y102.65/70, Y102.45/50, Y102.20, Y102.00

Bids Y101.00, Y100.50, Y100.00

-

12:00

European stock markets mid-session: Indices turn negative after a moderately positive start

European stocks declined over the course of the day after a positive start. The FTSE and the DAX further retreated from all-time highs set yesterday. Investors now focus on the upcoming ECB meeting on Thursday.

Retail Sales in Europe's largest economy expanded in January far more than analysts had expected and fuelled bullish sentiment. The Federal statistics office Destatis stated the boost in sales comes amid lower consumer prices and strong consumption. Retailers profited from the high employment rate, the highest in Europe. Falling energy prices left consumers with more money to spend. Seasonally adjusted sales rose +2.9%, compared to revised +0.6% (previous +0.2%) in December. Analysts expected an increase of +0.6%.

On an annual basis Retail Sales rose +5.3%, the most since 2010. The previous reading was revised up from +4.0% to +4.8%.

The U.K. Construction sector expanded at a faster pace than expected. The Construction PMI rose from 59.1 points in January to 60.1 points in February, beating expectations of a decrease to 59.0. The increase was driven by a sharp rise in business volumes and an improving economy.

Eurozone's Producer Price Index fell more than expected in January with a reading of -0.9% compared to forecasts of -0.6%.

The FTSE 100 index is currently trading -0.11% quoted at 6,932.67. Germany's DAX 30 lost -0.06% trading at 11,403.42. France's CAC 40 is currently trading at 4,914.87 points, -0.05%.

-

11:46

European stock fell

European stocks declined the most in five weeks amid increasing geopolitical tension after Russia’s parliament authorized President Vladimir Putin to deploy troops in Ukraine. U.S. index futures and Asian shares also fell.

The Stoxx Europe 600 Index dropped 1.7 percent to 332.23 at 10:46 a.m. in London. Of the equity benchmark’s 600 members, 572 declined, while 22 advanced. The measure rose 4.8 percent in February as Federal Reserve Chair Janet Yellen pledged to follow her predecessor’s policy on economic stimulus.

The standoff over Ukraine intensified over the weekend as Putin got parliamentary approval to send troops into Ukraine. The former Soviet state put its military on combat readiness as Russian-speaking forces arrived outside the Ukrainian infantry base at Privolnoye on the Crimean peninsula.

The U.S. warned Russia not to intervene in the region and raised the possibility of imposing sanctions. Secretary of State John Kerry travels to Ukraine today to offer support as Russian troops occupy the Black Sea region of Crimea. European Union foreign ministers will hold an emergency meeting today, while the Group of Seven nations suspended planning for June’s Group of Eight summit in Russia.

China’s Purchasing Managers’ Index for February fell to 50.2 from 50.5 in January, according to official data released on March 1. A number above 50 indicates expansion. A private PMI by HSBC Holdings Plc. and Markit Economics signaled contraction, slipping to 48.5 from 49.5.

An index of euro-area manufacturing output based on a survey of purchasing managers rose to 53.2 in February, compared with the preliminary estimate of 53, according to a final reading from Markit.

Nokian Renkaat Oyj (NRE1V) lost 6.9 percent to 30.26 euros. The Nordic region’s largest tiremaker got about 35 percent of its revenue from the Russian region in 2012.

Metro AG retreated 6.6 percent to 28.08 euros. Germany’s biggest retailer said on Jan. 20 that it plans to proceed with an initial public offering of its Russian cash and carry business to raise money for expansion.

Roche slipped 2.5 percent to 264.70 Swiss francs. Genentech, a unit of the world’s largest maker of cancer drugs, said an independent data monitoring committee recommended that it halt the Phase III METLung study of the lung cancer treatment because it hasn’t shown any clinical benefits.

Bouygues declined 2.1 percent to 28.59 euros. Chief Executive Officer Martin Bouygues met with French President Francois Hollande on Feb. 27 to seek government support for the purchase of SFR, Le Journal du Dimanche reported, citing people close to the CEO.

Kuehne & Nagel International AG slipped 3.5 percent to 121.20 francs. The world’s biggest sea-freight forwarder reported 2013 earnings before interest and taxes rose 20 percent last year to 761 million francs ($865 million). Analysts had forecast 763.8 million francs.

FTSE 100 6,692.09 -117.61 -1.73%

CAC 40 4,304.53 -103.55 -2.35%

DAX 9,422.87 -269.21 -2.78%

-

10:20

Option expiries for today's 1400GMT cut

USD/JPY Y101.50, Y102.00, Y102.30, Y102.50, Y103.00, Y104.00

EUR/USD $1.3650, $1.3675, $1.3710, $1.3800, $1.3825

AUD/USD $0.8800, $0.8860, $0.8900, $0.8920, $0.9000, $0.9100

EUR/GBP stg0.8200, stg0.8250/55

USD/CAD Cad1.1100

GBP/USD $1.6575, $1.6600, $1.6625, $1.6650, $1.6700, $1.6900

EUR/JPY Y139.50

-

09:56

Asia Pacific stocks close

Asian stocks fell and measures of equity volatility surged amid escalating geopolitical tension over Ukraine and after an official gauge of Chinese manufacturing dropped to an eight-month low.

Nikkei 225 14,652.23 -188.84 -1.27%

S&P/ASX 200 5,384.33 -20.49 -0.38%

Shanghai Composite 2,075.23 +18.93 +0.92%

Rio Tinto Ltd., the world’s second-largest mining firm, lost 1.6 percent in Sydney with raw-materials shares among the largest decliners of the regional index’s 10 industry groups.

Mazda Motor Corp., an automaker that gets 73 percent of sales overseas, tumbled 3.5 percent in Tokyo as the yen touched an almost one-month high against the dollar.

China’s Shanghai Composite Index rose for a fourth day amid speculation lawmakers will announce measures to reform state-owned companies during an annual meeting this week.

-

09:32

United Kingdom: Net Lending to Individuals, bln, January 2.1 (forecast 2.5)

-

09:30

United Kingdom: Mortgage Approvals, July 76.94 (forecast 72.00)

-

09:28

United Kingdom: Purchasing Manager Index Manufacturing , February 56.9 (forecast 56.9)

-

08:58

Eurozone: Manufacturing PMI, February 53.2 (forecast 53.0)

-

08:53

Germany: Manufacturing PMI, February 54.8

-

08:48

France: Manufacturing PMI, February 49.7

-

08:38

FTSE 100 6,715.78 -93.92 -1.38%, CAC 40 4,330.93 -77.15 -1.75%, Xetra DAX 9,454.42 -237.66 -2.45%

-

06:44

European bourses are seen trading lower Monday, taking their lead from Asia: the FTSE, DAX and CAC down around 0.8%.

-

06:21

Asian session: The yen gained

00:00 Australia HIA New Home Sales, m/m January -0.4% +0.5%

00:30 Australia ANZ Job Advertisements (MoM) February -0.3% +5.1%

00:30 Australia Company Operating Profits Quarter IV +3.9% +2.3% +1.7%

01:00 China Non-Manufacturing PMI February 53.4 55.0

01:45 China HSBC Manufacturing PMI (Finally) February 48.3 48.5 48.5

05:30 Australia Commodity Prices, Y/Y February -9.9% -12.1%

The yen gained against all of its 16 major peers as Russian President Vladimir Putin’s threat to invade Ukraine intensified one of the most serious standoffs since the Cold War, boosting demand for haven assets. U.S. Secretary of State John Kerry will travel to Kiev to meet with Ukrainian leaders tomorrow to offer support as Russian troops occupy the nation’s Crimea region, U.S. officials said yesterday. President Barack Obama contacted overseas leaders on how to respond to the incursion, which prompted Ukraine to mobilize its army reserves as it seeks international economic aid. Ukraine said over the weekend an invasion would be “an act of war.”

The euro slid for a fifth day against the Swiss franc, after the Russian ruble and Ukraine’s hryvnia plunged to record lows last week.

Australia’s dollar held a four-day decline and the nation’s three-year bonds advanced on signs of a slowdown in China, the nation’s largest export market. China’s purchasing managers’ index of manufacturing released on March 1 dropped to 50.2 in February, the lowest since June. Analysts polled by Bloomberg News projected a reading of 50.1 with levels below 50 signaling shrinking output.

EUR / USD: during the Asian session, the pair traded in the range of $ 1.3755-90

GBP / USD: during the Asian session, the pair traded in the range of $ 1.6710-50

USD / JPY: on Asian session the pair fell to Y101.25

Events in the Ukraine - Crimea in particular - will continue to grab attention Monday, there will be plenty of interest in the full data calendar on both sides of the Atlantic. Later in the week, the policy decisions from the ECB and BOE will take centre stage. The ECB will be a closer call, but the recent inflation data could be enough to see them stand pat for now. The main releases set for Monday include the European and US manufacturing final PMI numbers. European data gets underway at 0813GMT, with the release of the Spanish Feb final manuf PMI. Italian PMI numbers will be released at 0843GMT, with French data at 0848GMT, Germany at 0853GMT and the amalgamated euro area numbers at 0858GMT. The data is seen in line with the recent flash numbers, but will be closely watched by the ECB ahead of Thursday's rate decision. At 0900GMT, Italy's final 2013 GDP data will be released. Analysts are looking for full year numbers to come in at -0.8%. Central bank speakers will be muted in the first part of the week as the BOE and ECB rate decisions approach. However, ECB Pres Draghi will appear at his quarterly hearing before the European Parliament, in Brussels. UK due due includes the February CIPS Manufacturing PMI at 0928GMT and the January BOE Money and Credit data at 0930GMT. Across the Atlantic, the US calendar gets underway at 1330GMT, with the release of the January personal income, expenditures and PCE data. Personal income is expected to rise 0.3% in January. Nonfarm payrolls rose a disappointing 113,000 in the month, while the average workweek was unchanged. At 1400GMT, the Feb Markit final manufacturing PMI data will be published. US data set for release at 1500GMT includes the January construction spending data and the February ISM index. Construction spending is expected to fall 0.1% in January. The ISM manufacturing index is expected to rebound slightly to a reading of 51.9 in February after falling sharply in January. Domestic-made light vehicle sales are set for release Monday and are expected to hold roughly steady in February near the 12.0 million annual rate posted in January. Seasonal adjustment factors expect another weak month for raw sales in February and will add to unadjusted sales, though not as much as in the previous month.

-

01:45

China: HSBC Manufacturing PMI, February 48.5 (forecast 48.5)

-

01:00

China: Non-Manufacturing PMI, February 55.0

-

00:32

Australia: ANZ Job Advertisements (MoM), February +5.1%

-

00:32

Australia: Company Operating Profits, Quarter IV +1.7% (forecast +2.3%)

-

00:01

Australia: HIA New Home Sales, m/m, January +0.5%

-