Notícias do Mercado

-

20:36

Australia CFTC AUD NC Net Positions up to $-40.6K from previous $-44.6K

-

20:36

European Monetary Union CFTC EUR NC Net Positions increased to €124.9K from previous €122.2K

-

20:35

Japan CFTC JPY NC Net Positions increased to ¥-66K from previous ¥-67.4K

-

20:34

United Kingdom CFTC GBP NC Net Positions climbed from previous £-36.6K to £-28.2K

-

20:33

United States CFTC S&P 500 NC Net Positions up to $-203.7K from previous $-204.2K

-

20:32

United States CFTC Oil NC Net Positions fell from previous 239.7K to 231.7K

-

20:32

United States CFTC Gold NC Net Positions climbed from previous $110K to $115.1K

-

18:53

GBP/USD: Flirting with 1.2300 ahead of the Bank of England’s decision

- Bank of England to hike rates by 50 bps, fresh forecasts coming up.

- Concerns about a global economic setback weighed on US indexes.

- GBP/USD trades near its recent multi-month high of 1.2343.

The GBP/USD pair peaked at 1.2321 after Wall Street’s opening but trimmed intraday gains and hovers at around 1.2280. The pair ends the week flat, as demand for the US Dollar remained subdued.

At the time being, US indexes trade mixed, with the Dow Jones Industrial Average and the S&P 500 in the red, but the Nasdaq Composite up measly 12 points. Generally better-than-anticipated US macroeconomic data has lifted concerns the US Federal Reserve will go for an aggressive 75 bps hike, which will end up raising the risk of a longer and steeper recession in 2023.

The week ahead will bring the monetary policy decisions of the US Federal Reserve, the European Central Bank, and more relevantly for the British Pound, the Bank of England. Market participants have fully priced in a 50 bps, and little surprises are expected there. However, investors are unaware of what English policymakers have on the docket for 2023.

The Bank of England acknowledged the country is in a recession and expects the setback to extend well into 2023. Fresh forecasts on growth and inflation will be key for the Pound’s direction.

-

18:06

United States Baker Hughes US Oil Rig Count down to 625 from previous 627

-

17:17

WTI Price Analysis: Crude Oil sits at its lowest for the year

Europe and the G-7 started applying a price cap to oil prices, crude plunged.

EU Commission President Von der Leyen anticipated more sanctions ahead.

WTI trades near a weekly low of $71.11 a barrel, the lowest since December 2021.

The barrel of West Texas Intermediate Crude Oil plummeted this week and trades at levels that were last seen in December 2021. The black gold stands just above $70 a barrel, after peaking at $81.71 a barrel on Monday. The weekly drop came after the European Council, alongside the G-7, agreed on a price cap on Russian oil applicable as of December 5.

EU cap on Russian oil

“The price cap on Russian oil will limit price surges driven by extraordinary market conditions and drastically reduce the revenues Russia has earned from oil after it unleashed its illegal war of aggression against Ukraine. It will also serve to stabilise global energy prices while mitigating adverse consequences on energy supply to third countries,” reads the European Commission press release from December 3.

It is worth adding that, despite not directly referring to oil prices, European Commission President Ursula von der Leyen announced she will propose a ninth package of sanctions against Russia.

-

16:20

Fed's Powell to push back against rate cuts in 2023 – Rabobank

Previewing the FOMC's December policy meeting, Rabobank analysts said they expect the US central bank to hike the policy rate by 50 basis points and see policymakers revising the terminal rate projection to the neighbourhood of 5%.

Dot plot to show disagreement about terminal rate

"We expect that Powell will continue to push back against rate cuts in 2023, repeating that restoring price stability will require holding policy at a restrictive level for some time and that history cautions strongly against prematurely loosening policy."

"Meanwhile, obscured by Powell’s hawkish consensus view, the dot plot is likely to show considerable disagreement about the terminal rate. This could become more prominent in 2023 when the subset of voters becomes more dovish."

-

16:00

Russia Consumer Price Index (MoM) increased to 0.4% in November from previous 0.18%

-

16:00

Gold Price Forecast: XAU/USD could find support on reduced rate hike expectations – Commerzbank

Gold trades flat when compared to Monday’s opening. US inflation data and/or the Fed and ECB could give new impetus to the Gold market next week, economists at Commerzbank report.

Gold will be affected by three major events next week

“First, the US inflation data will be published – they could turn out to be more moderate than the market envisages. Though this may not have any impact on the Fed’s interest rate decision the day after, it could influence the tone taken at the press conference. If the market scales back its expectations with respect to the rate hike cycle, this is likely to lend buoyancy to Gold.”

“Whether the third major event, the ECB’s meeting on Thursday, will then have any serious effect on prices, is somewhat doubtful.”

-

15:49

EUR/USD Price Analysis: Buyers maintain the pressure ahead of the weekly close

- The US Michigan Consumer Confidence Index improved to 59.1 in December.

- The uncertainty surrounding the US Federal Reserve’s decision weighs on mood.

- EUR/USD eases following upbeat US data but holds above 1.0500.

Despite a knee-jerk mid-week, the EUR/USD pair is comfortably trading above the 1.0500 threshold, seesawing around 1.0530 following the release of the December University of Michigan's (UoM) Consumer Confidence Index, which rose by more than anticipated, to 59.1 from 56.8 in November. Market players had anticipated a setback to 53.3

Upbeat US data helped the US Dollar by the end of the week amid a deteriorating market sentiment. US indexes turned lower with the release, as speculative interest anticipates a potentially aggressive US Federal Reserve. The central bank has anticipated it would slow the pace of quantitative tightening, and Chair Jerome Powell hinted it could happen as soon as this month.

However, resilient macroeconomic data leaves the door open for yet another 75 bps hike, ahead of a smaller one. Recession concerns add to the dismal mood, as the higher rate goes, the higher are the chances of an economic setback.

EUR/USD technical perspective

According to Valeria Bednarik, FXStreet.com chief analyst, “The EUR/USD pair weekly chart shows that the pair posted a higher high and a higher low, maintaining the risk skewed to the upside. The same chart shows that the 20 Simple Moving Average (SMA) advances far below the current level, at around 1.0080, while technical indicators consolidate near overbought readings, all of which favors a bullish continuation. Finally, the 100 SMA is crossing below the 200 SMA, both far above the current level, losing relevance as a bearish signal.”

She also added that “ EUR/USD needs to break above 1.0580 to be able to extend its gains towards 1.0620 first, and 1.0700 later. A break above the latter should bring the 1.1000 figure to the table. Buyers stand at around 1.0490, while the next support level is 1.0420. An unlikely slide below the latter could favor a downward extension towards 1.0300.”

-

15:43

Gold Price Forecast: XAU/USD's technical outlook suggests a bullish bias remains intact

Gold has extended its rebound toward $1,800. A look at XAU/USD’s technical picture confirms the bullish bias, FXStreet’s Eren Sengezer reports.

Failure to defend $1,792 could trigger additional losses

“The Relative Strength Index (RSI) indicator on the daily chart climbed above 60 on Friday, pointing to a buildup of bullish momentum. Additionally, XAU/USD climbed above the 200-day Simple Moving Average, which is currently located at $1,792.”

“On the upside, $1,800 (psychological level, static level) aligns as initial resistance before $1,830 (Fibonacci 50% retracement of the long-term downtrend) and $1,860 (static level) next.”

“In case buyers fail to defend $1,792, additional losses toward $1,780 (Fibonacci 38.2% retracement) and $1,770 (static level, 20-day SMA) could be witnessed.”

-

15:35

GBP/USD to see a correction lower rather than a fresh collapse – HSBC

Economists at HSBC expect the GBP/USD pair to head gradually lower but a big collapse is unlikely.

Some near-term downside for the GBP

“We look for some near-term downside for the GBP, amid vulnerable risk appetite and a dovish 50 bps hike by the Bank of England (BoE) at its 15 December meeting.”

“The structural concerns which drove October’s lurch lower in GBP/USD are less evident. The UK’s fiscal confidence has been regained with the Autumn budget, and the UK’s external imbalance is also showing some signs of improvement, notably for visible trade.”

“With all factors being considered, we are looking at a correction lower in GBP/USD, rather than a fresh collapse, over the near term.”

-

15:06

Four key differences between Gold and Silver – Morgan Stanley

To varying degrees, both Gold and Silver may provide a hedge in a potential economic or market downturn, as well as during sustained periods of rising inflation. Here are four factors to consider when deciding to invest in Gold or Silver, according to economists at Morgan Stanley.

Silver may be more tied to the global economy

“Half of all Silver is used in heavy industry and high technology, according to the World Silver Survey. As a result, Silver is more sensitive to economic changes than Gold, which has limited uses beyond jewelry and investment purposes. When economies take off, demand tends to grow for Silver.”

Silver is more volatile than Gold

“The volatility in Silver prices can be two to three times greater than that of gold on a given day. While traders may benefit, such volatility can be challenging when managing portfolio risk.”

Gold has been a more powerful diversifier than Silver

“Silver can be considered a good portfolio diversifier with moderately weak positive correlation to stocks, bonds and commodities. However, Gold is considered a more powerful diversifier. It has been consistently uncorrelated to stocks and has had very low correlations with other major asset classes. Unlike Silver, Gold is less affected by economic declines because its industrial uses are fairly limited.”

Silver is currently cheaper than Gold

“Per ounce, Silver tends to be cheaper than Gold, making it more accessible to small retail investors who wish to own the precious metals as physical assets.”

-

15:04

US: UoM Consumer Confidence Index improves to 59.1 in December vs. 53.3 expected

- UoM Consumer Confidence Index rose modestly in early December.

- US Dollar Index holds steady slightly below 105.00.

Consumer sentiment improved in the US in early December with the University of Michigan's (UoM) Consumer Confidence Index rising to 59.1 from 56.8 in November. This reading came in better than the market expectation of 53.3.

"Year-ahead inflation expectations improved considerably but remained relatively high, falling from 4.9% to 4.6% in December, the lowest reading in 15 months but still well above 2 years ago," the UoM further noted in its publication. "At 3.0%, long run inflation expectations has stayed within the narrow (albeit elevated) 2.9-3.1% range for 16 of the last 17 months."

Market reaction

The US Dollar Index showed no immediate reaction to this report and was last seen staying flat on the day slightly below 105.00.

-

15:01

United States Wholesale Inventories: 0.5% (October) vs previous 0.8%

-

15:00

United States Michigan Consumer Sentiment Index registered at 59.1 above expectations (53.3) in December

-

15:00

United States UoM 5-year Consumer Inflation Expectation remains unchanged at 3% in December

-

14:35

USD/JPY could move higher alongside a hawkish Fed, should US yields rise – HSBC

USD/JPY could move higher alongside a hawkish Fed, should US yields move higher, in the view of economists at HSBC.

USD/JPY is likely to follow US yields higher

“USD/JPY is set to remain beholden to US-Japan yield differentials, particularly as the threat of FX intervention by Japan’s Ministry of Finance (MoF) feels distant at current levels. This means that, while risk appetite remains relevant for the JPY, it depends on what is driving that risk tone. “

“A hawkish Fed is likely to see the JPY lose ground against both the USD and EUR, while renewed concerns about China’s economic outlook would provide support for the JPY.”

-

14:25

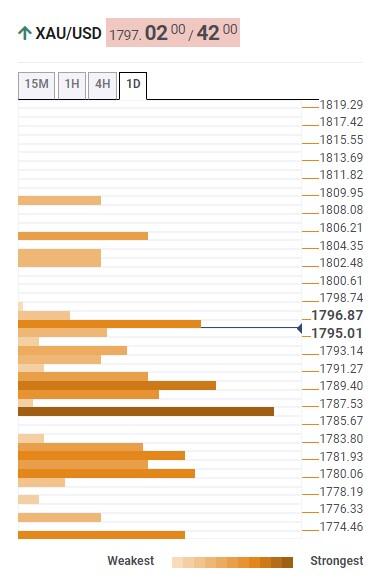

Gold Price Forecast: XAU/USD retreats from above $1,800

- The US Producer Price Index eased in November, but it was not enough.

- Market participants await the US Federal Reserve monetary policy decision next week.

- The XAU/USD pair maintains its bullish potential intact, despite the lack of follow-through.

Spot gold jumped to $1,804.43 ahead of the US opening but quickly retreated to currently trade at around $1,797 a troy ounce. The American Dollar remains on the back foot despite a dismal market mood, as the United States Producer Price Index (PPI) failed to impress. According to the US Bureau of Labor Statistics, inflation at wholesale levels rose at an annual pace of 7.4% in November, meeting market expectations. However, the core reading, which excludes volatile food and energy prices, was up by 6.2%, below the previous 6.7%, but above the 6% expected.

Demand for the US Dollar is limited ahead of the critical US Federal Reserve (Fed) monetary policy decision next week. The central bank may slow the pace of tightening and hike by 50 bps before pausing, ending the most aggressive cycle of its history. Nevertheless, speculative interest still sees a modest chance of another 75 bps hike amid resilient economic data.

XAU/USD technical perspective

XAU/USD trimmed its early weekly losses, and trades flat when compared to Monday’s opening. Still, it managed to post a higher low and a higher high, maintaining the bullish potential intact. The bright metal, however, is still unable to clear the psychological resistance at $1,800. Once above it, gold has the path clear towards the $1,850 price zone. A near-term support level comes at $1.780, while stronger buying interest is aligned at around $1,765.

-

14:17

GBP/USD: A push on to a 1.23 handle will underpin the positive tone – Scotiabank

GBP/USD’s bullish trend extends. Economists at Scotiabank expect the pair to remain well supported ahead of the weekend.

Weekly settings are turning mildly bullish

“The uptrend in the GBP/USD pair is well-established and enjoys the backing of solid trend momentum signals on the intraday and daily chart; weekly settings are turning mildly bullish as well.”

“The GBP retains a moderately firmer undertone into the end of the week; a push on to a 1.23 handle will underpin the positive tone ahead of the weekend.”

-

13:52

Silver Price Analysis: XAG/USD bulls retain control, multi-month top remains in sight

- Silver scales higher for the third successive day and inches back closer to the multi-month top.

- The technical setup favours bullish traders and supports prospects for a further positive move.

- A sustained break below the $22.00 mark is needed to negate the near-term bullish outlook.

Silver gains traction for the third successive day on Friday and sticks to its positive bias through the early North American session. The white metal is currently placed above the $23.00 mark and remains well within the striking distance of its highest level since late April touched on Monday.

From a technical perspective, this week's goodish rebound from the $22.00 round figure adds credence to the recent bullish breakout through the very important 200-day SMA. Furthermore, positive oscillators on the daily chart support prospects for a further near-term appreciating move for the XAG/USD.

That said, bulls might wait for a move beyond the multi-month top, near the mid-$23.00s, before placing fresh bets. The XAG/USD might then accelerate the upward trajectory and aim to reclaim the $24.00 round figure. The momentum could get extended towards the next relevant hurdle near the $24.50 area.

On the flip side, the daily swing low, just below the $23.00 mark, now seems to protect the immediate downside. This is followed by the 200-hour SMA, around the $22.40-$22.35 region. Any subsequent fall might continue to find decent support and attract fresh buyers near the $22.00 round-figure mark.

The latter should act as a pivotal point, which if broken decisively might negate the positive outlook and shift the bias in favour of bearish traders. The XAG/USD would then turn vulnerable to challenge the technical significant 200-day SMA support, currently pegged around the $21.25 area.

Silver 1-hour chart

Key levels to watch

-

13:51

Russian President Putin: We will not sell oil to those who proposed price caps

Russian President Vladimir Putin said on Friday that Russia will not sustain losses from oil price caps, as reported by Reuters.

Key takeaways

"If consumer defines oil prices, this will lead to a collapse of the oil industry."

"This will lead to rising prices, this proposal is stupid."

"Oil prices will skyrocket and hit those who propose price caps."

"We will think about oil output cuts."

"We will not sell oil to those who proposed price caps."

"Decision on oil output cuts is not taken yet."

"Decree responding to oil price cap will be announced in coming days."

Market reaction

Crude oil prices edged higher following these comments and the barrel of West Texas Intermediate was last seen trading at $72.65, where it was up 1.25% on a daily basis.

-

13:34

US: Annual PPI declines to 7.4% in November as expected

- Annual PPI in the US declined to 7.4% in November as expected.

- US Dollar Index gained traction and climbed to the 105.00 area.

The Producer Price Index (PPI) for final demand in the US declined to 7.4% on a yearly basis in November from 8.1% in October, the data published by the US Bureau of Labor Statistics revealed on Friday. This reading came in line with the market expectation.

The annual Core PPI edged lower to 6.2% in the same period from 6.7%, compared to analysts' estimate of 6%. On a monthly basis, the Core PPI came in at 0.4%.

Market reaction

The US Dollar gathered strength against its rivals with the initial reaction to the data. As of writing, the US Dollar Index was up 0.2% on the day at 105.02.

-

13:31

United States Producer Price Index ex Food & Energy (MoM) above expectations (0.3%) in November: Actual (0.4%)

-

13:31

Canada Capacity Utilization below expectations (83%) in 3Q: Actual (82.6%)

-

13:30

United States Producer Price Index ex Food & Energy (YoY) registered at 6.2% above expectations (6%) in November

-

13:30

United States Producer Price Index (MoM) came in at 0.3%, above forecasts (0.1%) in November

-

13:30

United States Producer Price Index (YoY) meets expectations (7.4%) in November

-

13:20

USD/CAD Price Analysis: Holds steady above 1.3600, seems poised to appreciate further

- USD/CAD stages a modest intraday recovery move from the 50-day SMA support on Friday.

- Bearish oil prices undermine the Loonie and offer support, though weaker USD caps gains.

- The setup favours bullish traders and supports prospects for a further appreciating move.

The USD/CAD pair defends the 50-day SMA support and attracts some buyers near the 1.3570-1.3565 area on the last day of the week. Crude oil prices maintain the bearish bias near the YTD low, which is seen undermining the commodity-linked Loonie and lending some support to the major. However, the prevalent US Dollar selling bias, amid rising bets for less aggressive rate hikes by the Fed, caps the upside for the USD/CAD pair. Spot prices retreat a few pips from the daily low, though manage to hold above the 1.3600 mark through the early North American session.

From a technical perspective, the recent bounce from confluence support comprising of a nearly three-week-old ascending trend-line and the 100-period SMA on the 4-hour chart favours bullish traders. Moreover, oscillators on daily/4-hourly charts support prospects for additional gains. That said, this week's failure near the 1.3700 mark makes it prudent to wait for some follow-through strength beyond the said handle before placing fresh bullish bets. Nevertheless, the USD/CAD pair still seems poised to test the next relevant resistance near the 1.3745-1.3750 region.

Some follow-through buying has the potential to lift spot prices to the November monthly swing high, around the 1.3800 mark. The USD/CAD pair could eventually appreciate to the 1.3840-1.3850 region en route to the 1.3900 round figure and the YTD peak, around the 1.3975-1.3980 zone.

On the flip side, the 1.3570-1.3560 area (100 DMA) might continue to protect the immediate downside. A convincing break below could accelerate the fall towards the 1.3500 mark. Any subsequent slide, however, could get bought into near the 1.3460-1.3450 confluence support. The latter should act as a pivotal point, which if broken decisively will negate the positive outlook and shift the near-term bias in favour of bearish traders. The USD/CAD pair might then turn vulnerable to weaken below the 1.3400 mark and challenge the 100-day SMA support.

USD/CAD 4-hour chartg

Key levels to watch

-

13:17

EUR/USD: A weekly close above 1.0580 will be technically bullish – Scotiabank

EUR/USD retains a positive undertone. Economists at Scotiabank note that a weekly close above 1.0580 will be technically bullish.

EUR’s technical resilience looks impressive

“Minor dips are finding decent support near the mid 1.05 zone which may help revive spot gains for a retest of the upper 1.05s into the end of the week.”

“The EUR’s technical resilience looks impressive, from our point of view; it shrugged off a hefty (technically negative) loss earlier this week and remains within striking distance of 1.06.”

“A weekly close above 1.0580 will be technically bullish from a medium-term point of view.”

-

13:10

USD set for a cheery holiday season, 2023 to be a more challenging –HSBC

Economists at HSBC look for the US Dollar to strengthen into the holiday season. However, 2023 is likely to be a more challenging year for the greenback.

USD cheery, then bleary

“While we expect a weaker USD over the medium-term, the sharp recent decline in the currency appears to be overdone and the short-term risks are skewed towards a correction stronger in the USD into year-end 2022.”

“For the 13-14 December Federal Open Market Committee (FOMC) meeting it will be interesting to see where the ‘dots’ rate projections for year-end 2023 land. If it moves much above 5.00%, it might see further USD strength, given the market is eyeing a terminal rate around 4.60%. However, the FX market remains dominated by risk appetite, rather than rates.”

“Data will remain key to risk appetite and the USD with US inflation top of the list. Another lower-than-expected reading for US CPI (due 13 December) could provide further impetus to the ‘risk on’ USD weakness, for example, contrary to our view.”

-

12:36

AUD/USD sticks to modest intraday gains amid weaker USD, remains below 0.6800

- AUD/USD gains traction for the third successive day, though lacks follow-through buying.

- Bets for less aggressive Fed rate hikes weigh on the USD .and act as a tailwind for the pair.

- The upside seems capped as traders await the key US CPI and FOMC meeting next week.

The AUD/USD pair prolongs its positive trend for the third successive day and maintains its bid tone through the mid-European session. The pair, however, remains below its highest level since September 13 touched earlier this week and is currently placed just a few pips below the 0.6800 round-figure mark.

A combination of factors drags the US Dollar back closer to over a five-month low touched earlier this week, which, in turn, is seen offering support to the AUD/USD pair. Expectations that the Fed will slow the pace of its policy tightening and deliver a relatively smaller 50 bps rate hike in December keep the US Treasury bond yields depressed. This, along with a generally positive tone around the equity markets, undermines the safe-haven greenback and benefits the risk-sensitive Aussie.

The easing of COVID-19 restrictions in China remains supportive of the recent recovery in the global risk sentiment. Furthermore, a fresh leg up in commodity prices provides an additional lift to the resources-linked Australian Dollar. That said, growing worries about a deeper global economic downturn might keep a lid on any optimistic move and act as a headwind for the AUD/USD pair. Traders might also prefer to wait on the sidelines ahead of next week's key macro data/event risks from the US.

The latest US consumer inflation figures for November will be released on Tuesday. This will be followed by the highly-anticipated FOMC monetary policy meeting on December 13-14. The outcome should influence the near-term USD price dynamics and provide a fresh directional impetus to the AUD/USD pair. In the meantime, traders on Friday will look to the US economic docket, featuring the Producer Price Index (PPI) and the Prelim Michigan Consumer Sentiment Index, for short-term opportunities.

Technical levels to watch

-

12:29

Brent Crude Oil to average $104/bbl next year – ING

Crude oil prices fell below $79/bbl, erasing gains for this year. However, strategists at ING expect Brent Crude Oil to average $104/bbl in 2023.

Tighter oil market

“We believe that Russian supply will fall significantly early next year – in the region of 1.8MMbbls/d year-on-year in the first quarter. This supply loss coupled with continued OPEC+ supply cuts suggests that the oil market will tighten over the course of 2023. US supply growth will not be able to fill the gap, with US producers showing a lot more capital discipline.”

“We expect ICE Brent to average $104/bbl next year.”

-

12:00

Brazil IPCA Inflation came in at 0.41%, above expectations (0.15%) in November

-

11:51

The ‘safe-haven’ allure of the CHF may start to wane – HSBC

Diminishing 'safe haven’ allure alongside a dovish 50 bps hike by the Swiss National Bank (SNB) should see the CHF weaken over the near term, economists at HSBC report.

CHF’s ‘safe haven’ appeal may diminish

“The ‘safe haven’ allure of the CHF may start to wane, as many of the Eurocentric risks – most notably around periphery debt – appear to have topped out alongside the bottoming out of European data and a potential turn in European inflationary pressures.”

“The SNB is expected to deliver a 50 bps hike bringing the rate to 1.00% at its 15 December meeting. But inflation has never gotten as excessive in Switzerland as elsewhere, and we think that the SNB will leave rates flat at 1.00% after the December meeting. Any signal that the hiking cycle is close to its end will come as a disappointment to the rates market.”

“We expect the CHF to weaken against the USD over the near term.”

-

11:49

GBP/USD clings to gains above mid-1.2200s amid broad-based USD weakness

- GBP/USD edges higher for the third successive day amid the prevalent USD selling bias.

- Bets for less aggressive Fed rate hikes, depressed US bond yields undermine the buck.

- Traders now look to next week’s inflation data/central bank meetings for a fresh impetus.

The GBP/USD pair gains traction for the third successive day on Friday and sticks to the positive bias through the mid-European session. The pair is currently placed comfortably above the mid-1.2200s and remains well within the striking distance of its highest level since June 17 touched earlier this week.

A combination of factors keeps the US Dollar bulls on the defensive, which, in turn, is seen lending some support to the GBP/USD pair. The optimism over the easing of strict COVID-19 restrictions in China remains supportive of a generally positive tone around the equity markets. Furthermore, the uncertainty over the Fed’s rate-hike path is seen weighing on the safe-haven greenback.

The incoming positive US economic data has been fueling speculations that the Fed might lift interest rates more than estimated. That said, the recent comments by several FOMC members, including Fed Chair Jerome Powell, suggested that the US central bank will slow the pace of its policy tightening. In fact, the markets are pricing in a relatively smaller 50 bps lift-off by the Fed in December.

This leads to a further decline in the US Treasury bond yields and continues to weigh on the greenback. Hence, the market focus will remain glued to the upcoming FOMC meeting on December 13-14. The Bank of England is also scheduled to announce its policy decision next week. Apart from this, investors will confront the release of the latest consumer inflation figures from the US and the UK.

The combination of key central bank event risks and macro data should help determine the next leg of a directional move for the GBP/USD pair. In the meantime, traders on Friday will take cues from the US economic docket, featuring the release of the Producer Price Index (PP) and the Prelim Michigan Consumer Sentiment Index. This, along with the US bond yields and the broader risk sentiment, will influence the USD price dynamics and provide some impetus to the major.

Technical levels to watch

-

11:18

USD/JPY could trade well under 130 by late 2023 – ING

A weak growth environment and a clear drop in bond yields should lift the Japanese Yen. Thus, economists at ING expect the USD/JPY to drop under 130 by late 2023.

Too early to expect the CNY to lead the Asian FX complex substantially higher

“While it is tempting to argue that some heavily hit European or Asian currencies are due a substantial re-rating next year, we believe such a conclusion is premature.”

“European currencies will struggle with a German economy re-orienting itself to a new world order, while it also seems too early to expect the Chinese Renminbi to lead the Asian FX complex substantially higher. Instead, a weak growth environment and a clear drop in bond yields should see defensive currencies like the Japanese Yen start to outperform.”

“We could see USD/JPY trading well under 130 by late 2023.”

-

11:02

Portugal Global Trade Balance fell from previous €-8.305B to €-9.025B in October

-

10:54

Depressed economic outlook, cautious monetary policy and high inflation to put pressure on GBP – Commerzbank

Sterling has completely recovered from the mini-budget crisis. Nonetheless, economists at Commerzbank expect more pressure on the GBP.

Temporary breather for Sterling

“At present, the relief that the budget crisis has been brought under control is dominating and there is no evidence of the energy crisis escalating further. In our view that only provides a temporary breather for Sterling though.”

“The depressed economic outlook, the comparatively cautious monetary policy, which is likely to be confirmed by a return to a 50 bps rate step and the continued high levels of inflation continue to principally put pressure on Sterling.”

-

10:25

NZD/USD looks a better buy than AUD/USD – SocGen

Kit Juckes, Chief Global FX Strategist at Société Générale, believes that the New Zealand Dollar still looks a better buy than Aussie.

AUD and NOK may be the two G10 currencies most at risk of a New Year hangover

“The RBNZ is the only central bank that is more hawkish than the Fed, and rate differentials are much more friendly. Likewise, Australian/Kiwi rate differentials suggest there’s more downside to AUD/NZD, even now.”

“There is still one caveat, of course: If the global equity market bounce runs out of steam, then given the levels of correlations between risk sentiment and currency trends, I can’t see NZD (or AUD, NOK or SEK) completing bucking that trend.”

“Valuations in G10FX are however, still very friendly – AUD, NZD, CAD, JPY and SEK are all at very cheap levels. The conclusion – AUD and NOK may be the two G10 currencies most at risk of a New Year hangover.”

-

10:19

Gold Price Forecast: XAU/USD flirts with 200-day SMA, remains below $1,800 mark

- Gold price continues with its struggle to find acceptance above the 200-day SMA.

- A modest US Dollar bounce is seen as a key factor capping the upside for the metal.

- Rising bets for a smaller 50 bps rate hike by the Federal Reserve act as a tailwind.

- The focus remains on next week’s release of the US CPI and FOMC policy meeting.

Gold price extends its steady ascent for the fourth straight day and climbs back closer to the $1,800 mark on the last day of the week. The XAU/USD, however, struggles to find acceptance or capitalize on the move beyond a technically significant 200-day Simple Moving Average (SMA).

Modest US Dollar rebound caps Gold price

The US Dollar stages a modest intraday bounce from a multi-day low touched earlier this Friday, which, in turn, is seen as a key factor acting as a headwind for the Dollar-denominated Gold price. The USD uptick, meanwhile, lacks any obvious fundamental catalyst and runs the risk of fizzling out amid the uncertainty over the Federal Reserve's rate hike path.

Investors seek clarity on Federal Reserve’s rate hike path

The recent comments by several policymakers, including Federal Reserve Chair Jerome Powell, suggest that the US central bank will slow the pace of its policy tightening. In fact, the current market pricing indicates over a 90% chance of a relatively smaller 50 bps rate hike at the upcoming Federal Open Market Committee (FOMC) meeting on December 13-14.

Depressed US Treasury bond yields should lend support to Gold price

This is reinforced by the ongoing decline in the US Treasury bond yields, which should cap the upside for the US Dollar and lend support to the non-yielding Gold price. That said, the incoming stronger macro data from the United States fueled speculations that the Fed could lift interest rates more than estimated, which is acting as a headwind for the XAU/USD.

Consumer Price Index from the United States will also be in focus

Heading into the key central bank event risk, investors next week will also watch out for the latest consumer inflation figures from the United States. The crucial CPI report for November is due for release on Wednesday and will influence the Fed's policy outlook. This, in turn, will drive the US Dollar and provide a fresh directional impetus to Gold price.

Traders look to US macro data for short-term opportunities

In the meantime, traders on Friday will take cues from the US economic docket, featuring the release of the Producer Price Index (PPI) and the Prelim Michigan Consumer Sentiment Index. This, along with the US bond yields and the broader risk sentiment, should produce short-term trading opportunities around Gold price later during the early North American session.

Gold price technical outlook

From a technical perspective, Gold price, so far, has been struggling to find acceptance above the very important 200-day Simple Moving Average (SMA). This makes it prudent to wait for some follow-through buying beyond the $1,800 mark before confirming a fresh bullish breakout and positioning for any further appreciating move. The next relevant hurdle is pegged near the $1,809-$1,810 zone, above which the XAU/USD could climb to the $1,830 hurdle en route to the $1,843-$1,845 supply zone.

On the flip side, any meaningful pullback is likely to find some support near the $1,775-$1,774 area ahead of the weekly low, around the $1,765-$1,764 region. Some follow-through selling, leading to a subsequent break below the $1,761-$1,760 horizontal resistance breakpoint, will negate any near-term positive outlook. Gold price might then turn vulnerable to test the $1,738-$1,737 support zone before eventually dropping to the $1,725 level.

Key levels to watch

-

10:01

USD Index to stay around 104.50/105.00 as fights seasonal trends – ING

The US Dollar is still battling December seasonality, which is leading it to weaker levels. However, the market will mainly focus on next week rather than going in one direction, economists at ING report.

The Dollar’s fighting season

“The Dollar tends to be seasonally weak in December, so this is a month of damage limitation for Dollar bulls like ourselves.”

“The US calendar includes PPI and University of Michigan survey numbers today. With markets being focused on various gauges of inflation, expect Dollar sensitivity to these data releases.”

“The Dollar could stabilise around current levels as markets gear up for the last week of action (Fed, ECB and BoE meetings) of 2022.”

“DXY may stay around 104.50/105.00 today.”

-

10:00

Greece Industrial Production (YoY) down to -2.5% in October from previous -1.1%

-

10:00

Greece Consumer Price Index (YoY): 8.5% (November) vs previous 9.1%

-

10:00

Greece Consumer Price Index - Harmonized (YoY) dipped from previous 9.5% to 8.8% in November

-

09:34

BoE Survey: UK public inflation expectations for coming year ease to 4.8% in November

The quarterly survey conducted by the Bank of England (BoE)/ Ipsos showed on Friday that the public's expectations in Britain for inflation for the coming year inched a tad lower.

Key takeaways

Median public inflation expectation for the coming year is 4.8% in Nov vs 4.9% in Aug.

Median public inflation expectation for 1-2 years 3.4% in Nov vs 3.2% in Aug.

Median public inflation expectation for 5 years 3.3% in Nov vs 3.1% in Aug.

Net public satisfaction with BoE control of inflation -12 in nov vs -7 in Aug.

Market reaction

The Pound Sterling is unperturbed by the BOE survey findings, with GBP/USD keeping its range at around 1.2240, up 0.10% on the day.

-

09:32

EUR/USD will struggle to trade sustainably above 1.0600 – ING

EUR/USD continues to edge higher toward 1.0600. But in the view of economists at ING, a rally above 1.06 would be premature.

Rate expectations unlikely to move much in the coming days

“Markets are pricing in around 55 bps of tightening ahead of the ECB meeting next week, and with no more speakers before the rate announcement and no key data releases except for the ZEW surveys on Tuesday, we doubt that rate expectations will move much in the coming days.”

“Our base case is still that EUR/USD will struggle to trade sustainably above 1.0600, and is mostly facing downside risks into year-end as the Dollar could regain some ground on global risk uncertainty and rebounding energy prices.”

-

09:31

United Kingdom Consumer Inflation Expectations fell from previous 4.9% to 4.8%

-

09:31

United Kingdom Consumer Inflation Expectations declined to 4% from previous 4.9%

-

09:25

OPEC+ crude oil output drops by 700K b/d in November – Platts survey

According to the latest Platts survey by S&P Global Commodity Insights, the oil output produced by OPEC and its allies (OPEC+) dropped by 700,000 b/d in November, the steepest monthly decrease since April when Russian production plunged due to sanctions.

Additional takeaways

OPEC's 13 countries produced 28.87 million b/d, a fall of 850,000 b/d from October, while Russia and eight other allies pumped 13.70 million b/d, up 150,000 b/d.

Gulf producers Saudi Arabia, the UAE, Kuwait and Iraq led the way, with all of them carrying out hefty cuts, as demand concerns have led to a very bearish sentiment in the oil markets.

These four producers cut a cumulative total of 780,000 b/d last month, accounting for almost all of the group's supply reduction.

Saudi Arabia cut output by a weighty 440,000 b/d, averaging 10.46 million b/d last month, its lowest since May.

Some of the cuts were offset by gains in Kazakhstan, Nigeria and Russia.

Market reaction

WTI has bounced from lows on the above report, trading at $71.76, up 0.25% on the day, at the time of writing.

-

09:22

EUR/USD surrenders modest intraday gains, once again fails ahead of 1.0600 mark

- EUR/USD moves back closer to a multi-month top, though lacks follow-through.

- A modest USD recovery is seen as a key factor acting as a headwind for the pair.

- Bets for less aggressive Fed rate hikes, a positive risk tone should cap the buck

- Traders also seem reluctant ahead of crucial central bank meetings next week.

The EUR/USD pair gains some follow-through traction on the last day of the week and inches back closer to a multi-month top set on Monday. The uptick, however, runs out of steam ahead of the 1.0600 mark, dragging spot prices to the lower end of the daily range, around the 1.0560-1.0555 area during the first half of the European session.

The US Dollar stages a modest recovery from a multi-day low touched earlier this Friday and turns out to be a key factor acting as a headwind for the EUR/USD pair. That said, the uncertainty over the Fed's rate-hike path should keep a lid on any meaningful upside for the greenback and continue lending some support to the major, at least for the time being.

The incoming positive macro data from the United States has been fueling speculations that the Federal Reserve might raise interest rates more than estimated. However, the recent comments by several FOMC members, including Fed Chair Jerome Powell, suggested that the US central bank will slow the pace of its policy tightening. In fact, the markets have been pricing in over a 90% chance of a relatively smaller 50 bps rate hike move by the Fed in December.

Apart from this, a generally positive tone around the equity markets could undermine the safe-haven greenback and contribute to limiting the downside for the EUR/USD pair. Despite the aforementioned supporting factors, any meaningful rally seems elusive amid diminishing odds for another supersized 75 bps rate hike by the European Central Bank (ECB). Hence, the focus will remain glued to next week's key central bank policy meetings.

In the meantime, traders on Friday will take cues from the US economic docket, featuring the release of the Producer Price Index (PPI) and the Prelim Michigan Consumer Sentiment Index. This, along with the US bond yields and the broader risk sentiment, might influence the USD price dynamics and provide some impetus to the EUR/USD pair. Nevertheless, spot prices remain on track to post modest gains for the third successive week.

Technical levels to watch

-

09:01

Gold Price Forecast: Lower interest rates environment is bullish for XAU/USD – SocGen

Gold gained 6.4% in November with the weakening US Dollar and declining yields. A lower interest rates environment supported the yellow metal, economists at Société Générale report.

A cheaper USD is bullish for Gold

“With 261K Nonfarm jobs added to the US economy, beating the consensus estimate of 193K, this is expected to ease pressure on the Fed to continue further interest rate tightening. A lower interest rates environment is bullish for the bullion since the latter is a non-yielding asset.”

“The US 10y real yield decreased 29.6 bps in November. Gold was further supported later in the month with the release of YoY US CPI figures for October. These were lower than the market had previously anticipated. Although lower inflation would traditionally be bearish for Gold, market sentiment seems to have focused on the prospect of slower interest rate hikes by the Fed or of an earlier pivot towards dovish policies which, if tamed faster than inflation decreases, would further lower real rates.”

“Gold was supported throughout the month by a weakening USD in a lower nominal rates environment, with the DXY down 5.0% in the month. A cheaper USD is bullish for the metal since it makes it relatively cheaper to foreign buyers.”

-

08:40

GBP/USD set to test the 200DMA at 1.2126 – ING

GBP/USD establishes above 1.2250. However, economists at ING expect the pair to test the 200-Day Moving Average (DMA) at 1.2126.

Keeping an eye on key technical levels

“GBP/USD could hover around 1.22 today, but risks are tilted to the 1.2126 200DMA being tested soon.”

“EUR/GBP is trading around the 0.8630 100DMA, and while we have less of a clear directional call on this pair in the short term, we see upside risks in the longer run.”

See: GBP/USD to spend much of next year below 1.20 – Rabobank

-

08:38

FX option expiries for Dec 9 NY cut

FX option expiries for Dec 9 NY cut at 10:00 Eastern Time, via DTCC, can be found below.

- EUR/USD: EUR amounts

- 1.0290-00 1.4b

- 1.0330 203m

- 1.0370 203m

- 1.0400 406m

- 1.0440-50 333m

- 1.0550 427m

- GBP/USD: GBP amounts

- 1.2200 211m

- 1.2400 291m

- USD/JPY: USD amounts

- 135.00 511m

- 135.25 305m

- 135.50 210m

- 136.00 623m

- 137.00 200m

- 138.00 395m

- AUD/USD: AUD amounts

- 0.6600 482m

- 0.6700 343m

- 0.6750 219m

- 0.6800 428m

- USD/CAD: USD amounts

- 1.3500 1.08b

- 1.3550-60 473m

- 1.3600 395m

- 1.3650 625m

- 1.3700 478m

- 1.3800 690m

- EUR/GBP: EUR amounts

- 0.8700 280m

-

08:33

USD/CAD rebounds from 50 DMA amid bearish oil prices, weaker USD might cap gains

- USD/CAD bounces off 50 DMA support and recovers a part of the overnight losses.

- Bearish crude oil prices undermine the Loonie and offer some support to the major.

- A combination of factors weighs on the USD and might cap the upside for the pair.

The USD/CAD pair manages to defend the 50-day SMA and attracts some buyers near the 1.3570-1.3565 area on the last day of the week. Spot prices move back above the 1.3600 mark during the first half of the European session and reverse a part of the previous day's retracement slide from a one-month high.

Crude oil prices languish near the YTD low amid worries that a deeper global economic downturn will dent fuel demand. Apart from this, a dovish 50 bps rate hike by the Bank of Canada earlier this week is seen undermining the commodity-linked Loonie and acting as a tailwind for the USD/CAD pair. The upside potential, meanwhile, seems limited amid the prevalent selling bias around the US Dollar.

In fact, the USD Index, which measures the greenback's performance against a basket of currencies, has now dropped back closer to a multi-month low and is pressured by a combination of factors. The latest optimism over the easing of COVID-19 curbs in China remains supportive of the recent recovery in the global risk sentiment. This, along with bets for less aggressive Fed rate hikes, weighs on the USD.

The markets seem convinced that the Fed will slow the pace of its policy tightening and are pricing in a relatively smaller 50 bps lift-off at next week's FOMC meeting. The expectations contribute to the ongoing decline in the US Treasury bond yields, which might hold back the USD bulls on the defensive. This, in turn, might keep a lid on any further gains for the USD/CAD pair, at least for the time being.

Moving ahead, Friday's US economic docket features the release of the Producer Price Index (PPI) and the Prelim Michigan Consumer Sentiment Index. This, along with the US bond yields and the broader risk sentiment, might influence the USD and provide some impetus to the USD/CAD pair. Apart from this, traders will take cues from oil price dynamics to grab short-term opportunities around the major.

Technical levels to watch

-

08:02

Austria Industrial Production (YoY): 3.9% (October) vs previous 6.9%

-

08:02

Slovakia Industrial Output (YoY) fell from previous -1.9% to -2.6% in October

-

08:00

Spain Industrial Output Cal Adjusted (YoY) registered at 2.5%, below expectations (4.6%) in October

-

07:54

EUR/USD to see only temporary setbacks as inflation eases on sustainable basis – Commerzbank

A gap is increasingly emerging between the Fed's outlook and market expectations. A sustained decline of inflation will justify only temporary setbacks in EUR/USD, economists at Commerzbank report.

Dollar caught between market and Fed

“The Fed signalled that it is likely to adjust its rate outlook (the dots) to the upside at next week’s meeting and seemed anxious to invalidate market expectations for rate cuts next year.”

“The discrepancy between Fed and market expectations might widen further though, which also results in the potential for a temporary Dollar rally if new information were to cause the market to align itself more with the Fed’s outlook.”

“As we assume that inflation will now ease significantly and on a sustainable basis this is likely to justify only temporary setbacks in EUR/USD.”

-

07:50

USD/JPY bounces off multi-day low, keeps the red below mid-136.00s amid weaker USD

- USD/JPY drifts lower on Friday amid heavy follow-through selling around the USD.

- Bets for less aggressive Fed rate hikes, depressed US bond yields weigh on the buck.

- Traders, however, seem reluctant ahead of next week’s key US data/FOMC meeting.

The USD/JPY pair comes under fresh selling pressure on the last day of the week and drops to a multi-day low, albeit lacks follow-through. The pair trims a part of its intraday losses and trades around the 136.25-136.30 region during the early European session, still down over 0.25% for the day.

The US Dollar prolongs its steady descent for the third successive day amid firming expectations for a less aggressive policy tightening by the Fed, which, in turn, is seen weighing on the USD/JPY pair. In fact, the markets seem convinced that the US central bank will slow the pace of its rate-hiking cycle and have been pricing in a 50 bps lift-off in December.

The prospects for a relatively smaller rate hike contributes to the ongoing decline in the US Treasury bond yields. This, in turn, results in the narrowing of the US-Japan rate differential, which benefits the Japanese Yen and exerts additional downward pressure on the USD/JPY pair. The downside, meanwhile, seems limited, warranting caution for bearish traders.

The incoming positive economic data from the United States has been fueling speculations that the US central bank might lift interest rates more than estimates. This might hold back traders from placing aggressive bearish bets around the USD and offer some support to the USD/JPY pair ahead of next week's key US macro data and the central bank event risk.

The market focus remains on the highly-anticipated FOMC policy meeting on December 13-14. Moreover, the latest US consumer inflation figures are also scheduled for release next Wednesday, which will influence the Fed's policy outlook. This, in turn, will play a key role in driving the USD in the near term and provide a fresh directional impetus to the USD/JPY pair.

In the meantime, traders on Friday will take cues from the US economic docket, featuring the release of the Producer Price Index (PPI) and the Prelim Michigan Consumer Sentiment Index. This, along with the US bond yields, could provide some impetus to the USD. Apart from this, the broader risk sentiment might produce some trading opportunities around the USD/JPY pair.

Technical levels to watch

-

07:27

Lasting rise in equity markets no sooner than the first half of 2023 – Natixis

How long until US share prices can be expected to recover? As long as no end to the rise in interest rates is in sight, there can be no lasting equity market recovery, in the view of analysts at Natixis.

No lasting recovery in the share prices under threat of an uncertain rise in interest rates

“In the past, it was not until the Fed Funds rate had fallen for a year that share prices recovered in the United States.”

Given the impatience of equity investors and the good results of US companies, we can imagine that this time we will only have to wait until the confirmed stabilisation of the Fed Funds rate. Given the outlook for interest rates, this points to a lasting rise in share prices no sooner than the first half of 2023.”

-

07:23

Forex Today: US Dollar on the back foot, eyes on US PPI data

Here is what you need to know on Friday, December 9:

The US Dollar continues to have a hard time finding demand amid retreating US Treasury bond yields on Friday with the US Dollar Index edging lower toward 104.50 after having closed the last two days in negative territory. The market mood remains upbeat on the last trading day of the week and US stock index futures trade modestly higher. The Producer Price Index (PPI) data for November will be featured in the US economic docket alongside the University of Michigan's preliminary Consumer Sentiment Survey for December.

Earlier in the day, the data from China showed that inflation, as measured by the Consumer Price Index (CPI), declined to 1.6% on a yearly basis in November from 2.1% in December. This reading came in higher than the market expectation of 1%. Meanwhile, China’s Premier Li Keiang said that the risk of a global recession was increasing but added that the Chinese economy was currently in a 'stable state' after reversing the economic decline in the third quarter. Nevertheless, The Shanghai Composite Index and Hong Kong's Hang Seng Index both remain on track to post daily gains.

EUR/USD gained 50 pips on Thursday and preserved its bullish momentum early Friday. The pair continues to edge higher toward 1.0600, where it will set a fresh multi-month high. European Central Bank (ECB) Governing Council member and French central bank governor Francois Villeroy de Galhau warned on Friday, “a temporary recession cannot be excluded," but these comments had little to no impact on the Euro's performance against its rivals.

GBP/USD registered small daily gains on Thursday and was last seen trading modestly higher on the day above 1.2250. The Bank of England will release the Consumer Inflation Expectations data later in the session.

USD/JPY closed virtually unchanged on Thursday and started to stretch lower toward 136.00 early Friday.

Gold price gained traction during the Asian trading hours on Friday and started to climb higher toward $1,800. The benchmark 10-year US Treasury bond yield is down nearly 1% on the day below 3.5%, helping XAU/USD preserve its bullish momentum.

Bitcoin continues to fluctuate in its weekly range at around $17,000. Ethereum gained nearly 4% on Thursday and was last seen consolidating its gains slightly below $1,300.

-

07:07

NZD/USD retakes 0.6400 amid weaker USD, eyes multi-month top touched earlier this week

- NZD/USD gains traction for the fourth straight day on Friday amid the prevalent USD selling bias.

- Bets for less aggressive Fed rate hikes keep the US bond yields depressed and weigh on the buck.

- A positive risk tone further undermines the safe-haven buck and benefits the risk-sensitive Kiwi.

The NZD/USD pair edges higher for the fourth successive day on Friday and climbs back closer to the top end of its weekly trading range. The pair sticks to its modest gains through the early European session and is currently placed around the 0.6400 round-figure mark.

A combination of factors drags the US Dollar closer to a multi-month low set earlier this week, which, in turn, is seen acting as a tailwind for the NZD/USD pair. Rising bets for a less aggressive policy tightening by the Fed, along with a generally positive risk tone, continue to weigh on the safe-haven greenback.

The markets seem convinced that the US central bank will slow the pace of its rate-hiking cycle and have been pricing in a relatively smaller 50 bps lift-off in December. Furthermore, the optimism over the easing of strict COVID-19 restrictions in China remains supportive of a recovery in the global risk sentiment.

That said, the incoming positive US economic data fuels speculations that the US central bank might lift rates more than projected, which should limit losses for the USD. Moreover, worries about a deeper global economic downturn might further contribute to capping the upside for the growth-sensitive New Zealand Dollar.

Traders might also refrain from placing fresh bets ahead of next week's key data/event risks - the US consumer inflation figures and the FOMC meeting. The crucial US CPI report will influence the Fed's policy outlook, which, in turn, will drive the USD and provide a fresh directional impetus to the NZD/USD pair.

Hence, it remains to be seen if bulls are able to retain control or if the intraday move-up runs out of steam at higher levels. Nevertheless, the NZD/USD pair has reversed modest weekly losses and remains well within the striking distance of its highest level since mid-August, around the 0.6440-0.6445 area touched on Monday.

Market participants now look to the US economic docket, featuring the release of the Producer Price Index (PPI) and the Prelim Michigan Consumer Sentiment Index. This, along with the risk sentiment, could provide some impetus and allow traders to grab short-term opportunities around the NZD/USD pair on the last day of the week.

Technical levels to watch

-

07:01

Norway Core Inflation (YoY) below expectations (5.9%) in November: Actual (5.7%)

-

07:01

Denmark Trade Balance declined to 27.4B in October from previous 32.1B

-

07:00

Denmark Current Account dipped from previous 38.3B to 33.2B in October

-

07:00

Norway Producer Price Index (YoY) registered at 22.3% above expectations (5.4%) in November

-

07:00

Norway Consumer Price Index (MoM) below expectations (0.9%) in November: Actual (-0.2%)

-

07:00

Gold Price Forecast: XAU/USD targets multi-month highs above $1,800

Gold price recaptures a 200-Daily Moving Average on the road to recovery. XAU/USD is set to retest $1,810, FXStreet’s Dhwani Mehta reports.

Renewed upside in the yellow metal is likely to gain momentum

“Gold remains on course to retest the five-month highs at $1,810. The next key resistance is seen at the upper boundary of the month-long rising wedge pattern, now placed at $1,816.”

“In case, the Gold price yields a weekly closing below the 200DMA at $1,792 on a renewed selling pressure, then the correction could resume toward the lower boundary of the wedge at $1,777.”

-

07:00

Norway Consumer Price Index (YoY) registered at 6.5%, below expectations (7%) in November

-

07:00

Norway Core Inflation (MoM) came in at -0.1%, below expectations (0.2%) in November

-

06:57

Silver Price Analysis: XAG/USD bulls occupy driver’s seat above $23.00

- Silver price remains firmer inside the four-day-old bullish channel.

- 200-HMA, weekly horizontal support zone challenge bears from retaking control.

- RSI conditions suggest further pullback but channel formation tests sellers.

Silver price (XAG/USD) pares intraday gains around the weekly top, also the highest level in seven months, as bulls take a breather during early Friday morning in Europe. Even so, the bullion price prints the third consecutive intraday gains by the press time.

In doing so, the bright metal retreats from the daily high as the RSI (14) takes a U-turn from the overbought territory, as well as breaks the short-term support line.

However, an ascending trend channel formation, established on Tuesday, restricts short-term XAG/USD moves between $23.45 and $23.00.

Even if the bright metal breaks the $23.00 support, the 200-HMA level surrounding $22.30 could challenge the bears.

It’s worth noting that the one-week-long horizontal area surrounding the $22.00 round figure appears the last defense of the silver buyers.

On the contrary, an upside break of the $23.45 hurdle needs validation from the multi-day high marked on Monday around $23.51 to convince Silver buyers of further advances.

Following that, March’s low near $24.00 and January’s high of $24.70 will gain the market’s attention.

To sum up, the Silver price remains on the buyer’s radar unless the quote drops below $22.00. However, the upside room appears limited below $23.51.

Silver: Hourly chart

Trend: Bullish

-

06:52

ECB’s Villeroy: A temporary recession cannot be excluded

European Central Bank (ECB) Governing Council member and French central bank governor Francois Villeroy de Galhau warned on Friday, “a temporary recession cannot be excluded.”

Additional quotes

“Growth for the whole of 2022 will be 2.6%.”

“In 2023, growth will be probably slightly positive. “

Market reaction

EUR/USD is consolidating gains above 1.0550 following the comments from the ECB policymaker. The currency pair is up 0.16% on the day.

-

06:30

USD/CHF bears approach 0.9325 support with eyes on central banks, inflation

- USD/CHF holds lower ground in the weekly low, down for the fourth consecutive day.

- Mixed sentiment, downbeat US Treasury yields weigh on US Dollar.

- Early signals for next week’s US inflation, monetary policy meetings of Fed, SNB will be in focus.

USD/CHF prints a four-day downtrend as sellers poke the lowest levels in eight months around 0.9325, marked the last Friday. That said, the Swiss Franc (CHF) pair remains pressured around 0.9335 during early the early Asian session.

The quote’s latest losses could be largely linked to the broad-based US Dollar weakness ahead of the next week’s busy schedule comprising the Federal Reserve (Fed) monetary policy meeting and the inflation data, not to forget today’s consumer-centric figures. In doing so, the major currency pair ignores challenges to the sentiment emanating from China and Russia, as well as fears of the global recession.

US Dollar Index (DXY) prints a three-day downtrend near 104.60, down 0.22% intraday while tracing downbeat US Treasury yields and justifying the softer US data printed of late. On Thursday, US Initial Jobless Claims matched 230K market consensus for the week ended on December 02, versus the upwardly revised 226K prior. Further, the four-week average also printed 230K figure compared to 229K in previous readings. Earlier in the week, the US Goods and Services Trade Balance deteriorated to $-78.2 billion versus $-79.1 billion expected and $-73.28 billion prior. Further, the final readings of the Unit Labour for Q3 eased to 2.4% QoQ versus 3.5% first estimations.

Talking about the risk catalysts, Organisation for Economic Co-operation and Development (OECD) Head Mathias Hubert Paul Cormann joined World Trade Organization (WTO) Director Dr. Ngozi Okonjo-Iweala to highlight the risk of the global recession. On the same line is China’s Premier Li Keqiang. However, US Treasury Secretary Janet Yellen’s rejection of recession woes and hawkish expectations from the Fed fails to underpin the DXY rebound. US Treasury Secretary Yellen said on Thursday night that "Recession is not inevitable," while also declining to say whether the dollar had peaked against other currencies.

Elsewhere, news from the Wall Street Journal (WSJ), suggesting the US readiness for human rights sanctions on Russia and China, recently weighed on the market’s risk appetite. However, the previous headlines signaling China’s interest in rebuilding ties with the US and easing the Zero-Covid policy tried to defend the optimists.

The mixed mood could be witnessed in mildly bid S&P 500 Futures and downbeat US Treasury yields, as well as slightly positive commodities, which in turn weigh on the US Dollar.

Moving on, the USD/CHF pair traders should pay attention to the preliminary readings of the Michigan Consumer Sentiment Index for December, expected 53.3 versus 56.8 prior, for fresh impulse. Also important to watch will be the University of Michigan’s (UoM) 5-year Consumer Inflation Expectations for the said month, 3.0% previous readings. Above all, next week’s monetary policy meeting by the Swiss National Bank (SNB) and the Federal Open Market Committee (FOMC) will be crucial for the pair traders to follow.

Technical analysis

A daily closing below the monthly bottom surrounding 0.9325 becomes necessary for the USD/CHF bears to keep the reins and approach March 2022 low near 0.9195.

-

06:10

GBP/USD establishes above 1.2250 amid cheerful market mood, UK/US Inflation eyed

- GBP/USD has shifted its business profile comfortably above 1.2250 as the risk-on mood has strengthened.

- Federal Reserve is set to calm down the pace of the interest rate hike next week.

- A hawkish policy stance is expected from the Bank of England despite the recession in the United Kingdom.

- GBP/USD is likely to accelerate its upside journey as the RSI (14) is looking to conquer the bullish range.

GBP/USD has comfortably shifted its auction profile above the crucial resistance of 1.2250 in the early European session. The Cable has climbed to near 1.2270 and is expected to extend its upside journey amid a stellar improvement in the risk appetite of the market participants. The risk aversion theme has lost its traction as investors are cheering expectations of a slowdown in the policy tightening pace by the Federal Reserve (Fed) rather than focusing on recession fears led by higher interest rate peak guidance belief.

Meanwhile, the US Dollar Index (DXY) has refreshed its four-day low at 104.50 and is expected to re-test the weekly low at 104.11 ahead. A significant recovery in S&P500 futures after a cautious start in early Tokyo is portraying an upbeat risk impulse. The alpha delivered by the US Treasury bonds has returned to a negative trajectory. The 10-year US Treasury yields have dropped to 3.46%.

Investors seek clarity on Federal Reserve’s policy outlook

Federal Open Market Committee (FOMC) in its October monetary policy meeting cleared that the Federal Reserve is actively discussing on slowing down the pace of policy tightening as escalating financial risks cannot be ignored now. Analysts at Danske Bank see a further hike in interest rates by 50 basis points (bps) and a hawkish message from Federal Reserve chair Jerome Powell for CY2023. Also, the neutral rate is expected at 5.00-5.25%.

The termination of the 75 basis points (bps) rate hike spell is going to provide a sigh of relief to the firms. No doubt, interest payment obligations after a 50 bps rate hike will escalate but signs of reaching to neutral rate will be cemented.

Bank of England needs to tight policy further despite a recession in the United Kingdom

The United Kingdom Consumer Price Index (CPI) is setting the bar higher with support from multiple tailwinds. Food price inflation soared to 12.4% in November led by accelerating prices of basic food items. Adding to that, the recent food supply crisis led by a shortage of labor and rising input cost has added fuel to the fire. The United Kingdom's economy is facing the heat of the recession, reporting a contraction in the growth rate. In spite of more downside risks to the economy, Bank of England (BOE) Governor Andrew Bailey is set to hike interest rates further.

A poll on Bank of England’s interest rate hike expectations taken by Reuters states that the central bank will add another 50 basis points (bps) next week and take borrowing costs to 3.50%, despite the economy falling into recession. The rampant inflation in the United Kingdom needs further policy tightening to bring exhaustion in the inflationary pressures.

United Kingdom/United States Consumer Price Index eyed

Next week, the release of the inflation figures will remain in the spotlight. In the United States economy, the headline CPI is expected to remain unchanged at 7.7% while the core inflation might inch higher to 6.4%. As payroll data and demand in the service sector have remained upbeat in November, the United States inflation could display a surprise rise, which could trigger volatility in the global market.

In the United Kingdom, rampant food price inflation could trigger upside momentum in overall inflation. Therefore, investors should brace for an upside release in inflation. As per the consensus, the headline inflation is expected to climb to 11.5% vs. the prior release of 11.1%. While the core inflation is seen higher at 6.6%. Higher consensus for headline inflation seems supported by bumper food price inflation.

Before US inflation data, investors will keep an eye on Producer Price Index (PPI) numbers. The headline factory-rate price index is seen at 7.4% from the prior release of 8.0% on an annual basis. Also, the core PPI is seen lower at 6.0% vs. the former figure of 6.7% in a similar period.

GBP/USD technical outlook

GBP/USD has recovered sharply after testing the horizontal support placed from November 24 high at 1.2153 on a four-hour scale. The secular and secondary upward-slopping trendlines plotted from September 26 low at 1.0339 and November 9 low at 1.1334 respectively will continue to support Pound Sterling.

Advancing 20-and 50-period Exponential Moving Averages (EMAs) at 1.2211 and 1.2263 respectively adds to the upside filters.

Meanwhile, the Relative Strength Index (RSI) (14) is looking forward to conquering the bullish range of 60.00-80.00, which will activate the upside momentum.

-

05:49

EUR/USD Price Analysis: Prints three-day uptrend near 1.0600 inside bullish triangle

- EUR/USD grinds higher inside a one-month-old bullish triangle.

- Nearly overbought RSI, sluggish MACD signals hint at limited upside room.

- Convergence of the key EMAs restricts short-term downside of the EUR/USD pair.

EUR/USD picks up bids to 1.0580 as buyers approach the weekly top, also the highest levels since late June, during early Friday morning in Europe.

The major currency pair’s run-up could be well-linked to the bull cross on the Daily chart as the 50-day Exponential Moving Average (EMA) crosses the 100-day EMA from below. Also favoring the buyers is the firmer RSI (14) and the absence of the bearish MACD signals. That said, the EUR/USD pair stays firmer inside a one-month-old ascending triangle.

However, sluggish MACD and the nearly overbought RSI conditions highlight the likely pullback of the major currency pair from the monthly triangle’s resistance line, close to 1.0630 by the press time.

In a case where the EUR/USD bulls cross the 1.0630 hurdle, the 1.0700 threshold and June’s peak surrounding 1.0775 should return to the chart.

On the contrary, a downside break of the stated triangle’s support line, near 1.0465 at the latest, could quickly drag the quote toward the 200-day EMA level of 1.0395.

However, the 50-day EMA and the 100-day EMA could challenge the EUR/USD bears afterward, around 1.0215 and 1.0190 in that order.

EUR/USD: Daily chart

Trend: Limited upside expected

-

05:34

USD/CAD Price Analysis: Bulls have a bumpy road ahead

- USD/CAD fades bounce off intraday low, struggles to reject two-day downtrend.

- Multiple hurdles to the north join downbeat RSI conditions to challenge bulls.

- Sellers have comparatively smoother roads to travel on breaking 1.3560.

USD/CAD retreats to 1.3588 as bulls struggle to defend the first daily gains in three heading into Friday’s European session. In doing so, the Loonie pair justifies downbeat RSI (14), as well as failures to cross the near-term key hurdles, in teasing the bears.

That said, the latest lows surrounding 1.3560 holds the key for the USD/CAD seller’s entry, a break of which could quickly drag the quote towards the December 02 swing high near 1.3520.

Following that, the 1.3500 round figure may act as an intermediate halt before highlighting the two-week-old support line, close to 1.3435 at the latest, for the pair bears.

In a case where USD/CAD bears dominate past 1.3435, the odds of witnessing a fresh monthly low, currently around 1.3385, can’t be ruled out.

On the flip side, a one-week-old horizontal resistance area near 1.3600 restricts the immediate upside of the USD/CAD pair.

Also acting as the key barrier for the pair buyers is the 1.3640-45 area that encompasses multiple levels marked since November 29.

Overall, USD/CAD remains pressured unless the quote successfully breaks the 1.3645 hurdle.

USD/CAD: Hourly chart

Trend: Further downside expected

-

05:30

Netherlands, The Manufacturing Output (MoM) declined to -0.4% in October from previous 0.5%

-

05:21

Australia’s PM Albanese announces price cap for gas and coal on Friday

Australian Prime Minister Anthony Albanese announced on Friday, a A$1.5 bln bill relief support for businesses and households on energy.

Additional takeaways

Announces price cap for gas at A$12 per gigajoule for 12 months.

Parliament to be recalled next week.

Australia to set price cap for coal at A$125 per tonne.

Bill relief to begin Q2 2023.

Price caps on coal and gas to apply for 12 months.

Market reaction

The fiscal announcement by the Australian Prime Minister fails to impress the AUD bulls, as AUD/USD keeps its range close to 0.6800, adding 0.35% so far.

-

04:56

Gold Price Forecast: $1,785 puts a floor under XAU/USD as Fed meeting, US inflation loom – Confluence Detector

- Gold price renews four-day high, approaches six-month-old resistance.

- US Dollar weakness joins China-linked optimism to favor XAU/USD bulls.

- Convergence of previous monthly high, golden ratio restricts downside ahead of US CPI, FOMC.

Gold price (XAU/USD) stays on the front foot for the fourth consecutive day as it cheers the broad-based US Dollar weakness to poke $1,800. Further, optimism surrounding China adds strength to the bullion’s run-up as traders await early signals for US inflation. It’s worth noting, however, that the cautious optimism ahead of next week’s Federal Open Market Committee (FOMC) meeting and the US Consumer Price Index (CPI) for November appears to challenge the Gold price. Considering the early signals, the Fed is likely to defend the policy hawks, despite suggesting a 0.50% rate hike, which in turn could keep the XAU/USD on the dicey floor and may allow the Gold buyers to retreat in case of US Dollar positive outcomes.

Also read: Since the Gold rally has stopped, can a reversal be expected?

Gold Price: Key levels to watch

The Technical Confluence Detector shows that the Gold price has fewer hurdles towards the north as it stays beyond the key $1,785 support comprising the previous month's high and Fibonacci 61.8% on daily formation, also known as the golden ratio.

That said, a convergence of the Fibonacci 23.6% on weekly and 38.2% on one day, around $1,791, also acts as short-term key support for XAU/USD.

It should be noted that a clear downside break of the $1,785 support confluence could quickly drag the quote toward the $1,780 mark encompassing 5-DMA and 38.2% on weekly formation.

In a case where the Gold price drops below $1,780, the 10-DMA and Fibonacci 161.8% on the one-day act as the last defense of buyers.

Alternatively, the previous weekly high surrounding $1,806 could test the Gold buyers, for now, before directing them to the Pivot Point one-day R3 near $1,810.

Following that, tops marked during the mid-June around $1,857 and June's monthly peak near $1,880 will be in focus.

Here is how it looks on the tool

About Technical Confluences Detector

The TCD (Technical Confluences Detector) is a tool to locate and point out those price levels where there is a congestion of indicators, moving averages, Fibonacci levels, Pivot Points, etc. If you are a short-term trader, you will find entry points for counter-trend strategies and hunt a few points at a time. If you are a medium-to-long-term trader, this tool will allow you to know in advance the price levels where a medium-to-long-term trend may stop and rest, where to unwind positions, or where to increase your position size.

-

04:55

AUD/USD sets to break 0.6800 as risk-on profile firms, US PPI hogs limelight

- AUD/USD is aiming to surpass 0.6800 as the market sentiment has become extremely bullish.

- China’s factory-gate price deflation has cemented a dovish commentary from the PBOC.

- A decline in the US PPI data is going to delight the Fed as expectations for a drop in inflation will get strengthened.

The AUD/USD pair is gathering momentum to surpass the immediate resistance of 0.6800 in the Tokyo session. The Aussie asset has gained strength as investors have underpinned the risk appetite theme. The major is holding its morning gains amid an intense sell-off in the US Dollar Index (DXY). The USD Index is hovering around 104.50 and is expected to re-test weekly lows around 104.10.

Meanwhile, S&P500 futures have recovered morning losses and have resumed their upside journey. The 500-united States stock basket futures are looking to extend their gains as a slowdown in the interest rate hike pace looks imminent. While the 10-year US Treasury yields have dropped to near 3.46%.