Notícias do Mercado

-

23:48

BlackRock: Fed might not need to hike rates in May as US economy slows

Rick Rieder, Chief Investment Officer of global fixed income at BlackRock, the world's largest asset manager, crossed wires via Reuters late Monday while saying, “The Federal Reserve may not need to raise interest rates further to fight inflation, as the fallout from last month's turmoil in the banking sector and a series of recent labor data point to a slowing US economy.”

Additional comments

Though Friday’s closely-followed Labor Department employment report showed that U.S. employers maintained a strong pace of hiring last month, it was also marked by slowing wage gains and jobs growth that was below the three, six and 12-month moving averages.

That data, together with labor market numbers released last week and expectations of tighter credit conditions after the failure of two US banks last month, paint a picture of a slowing economy.

Last Friday’s employment report, while clearly not alarming in any way, allows investors to see more clearly through to what should be a tangibly slower set of economic conditions.

Presumably, this will also see a cessation of Fed policy rate hikes after one more possible hike at the May meeting, although it’s also possible the Fed is done already.

Inflation should ease going forward, in line the economic slowing seen last month.

Hopefully ... markets can look forward to a more relaxed Fed from here.

EUR/USD remains pressured

EUR/USD pays little heed to the news as it holds lower grounds near 1.0860, despite recently bouncing off the lowest levels in a one-week.

Also read: EUR/USD scales above 1.0860 ahead of Eurozone Retail Sales and US Inflation

-

23:35

Silver Price Analysis: XAG/USD bulls run out of steam, sellers need validation from $24.30

- Silver price stays depressed after downbeat week-start, grinds near highest levels in a year.

- Overbought RSI conditions, receding bullish bias of MACD signals lure bears.

- Failure to cross ascending resistance line from late 2022 adds strength to bearish bias.

- Multiple support lines from March restrict immediate downside ahead of highlighting 100-DMA support.

Silver price (XAG/USD) makes rounds to $24.80-85 during the early hours of Tuesday’s Asian session, following a downbeat start of the week. Even so, the bright metal seesaws around the highest levels since late April 2022 marked in the last week.

That said, the commodity buyers appear running out of steam of late as the RSI (14) turns over overbought and the MACD signals also retreat within the bullish area.

Adding strength to the downside bias is the XAG/USD’s failure to cross an upward-sloping resistance line from late December 2022, close to $25.15 by the press time.

However, two ascending support lines from the previous month, respectively near $24.65 and $24.30, restrict the short-term downside of the Silver price.

Following that, the precious metal’s slump towards the $21.80-75 support zone comprising January’s low and the 100-DMA can’t be ruled out.

Meanwhile, an upside clearance of the aforementioned resistance line, close to $25.15, opens the door for the XAG/USD rally towards the April 2022 peak of $26.22.

In a case where the Silver buyers keep the reins past $26.22, the previous yearly high of around $26.95 and the $27.00 round figure will gain the market’s attention.

Silver price: Daily chart

Trend: Further downside expected

-

23:31

EUR/USD scales above 1.0860 ahead of Eurozone Retail Sales and US Inflation

- EUR/USD has jumped above the critical resistance of 1.0860 amid a correction in the USD Index.

- Fed Williams is anticipating inflation at 3.75% and a growth rate of less than 1% this year.

- A contraction in Eurozone Retail Sales is insufficient to back a neutral stance from the ECB.

The EUR/USD pair has climbed above the immediate resistance of 1.0860 in the early Asian session. The shared currency pair rebounded firmly after buying interest above 1.0830 in the early New York session. A corrective move in the US Dollar Index (DXY) resulted in a recovery in the Euro after a sheer sell-off.

The downside bias for the major currency pair has not been over yet as investors are anticipating a hawkish stance from the Federal Reserve (Fed) for its next month’s monetary policy.

S&P500 futures showed a stellar recovery on Monday after a gap-down opening despite anxiety among investors ahead of result season. The street is worried about the earnings of commercial banks after the banking fiasco due to the collapse of Silicon Valley Bank (SVB) and Signature Bank. Also, tight credit conditions by US banks must have impacted advances needed by firms for fixed capital working capital management.

The US Dollar Index (DXY) registered a gradual correction to near 102.54 as investors ignored China-Taiwan tensions despite the continuation of drilling by the Chinese military around Taiwan Island.

The major trigger that will keep investors busy ahead is the United States Consumer Price Index (CPI) data, which will release on Wednesday. Analysts at TD Securities expect the headline inflation to rise by 0.1% in March, and the core CPI by 0.4%. They see the CPI slowing to 3.6% by the fourth quarter.

Also, the commentary from New York Fed Bank president John C. Williams conveys, Inflation will be around 3.75% this year. He further added that the growth rate will be less than 1% and the Unemployment Rate will gradually rise to 4-4.5%. On banking turmoil, Fed Williams believes that higher rates by the Fed were not the cause of recent banking stress.

On the Eurozone front, investors are awaiting the Retail Sales data for fresh impetus. Monthly Retail Sales (March) are expected to contract by 0.8% vs. an expansion of 0.3% recorded in February. And annual Retail Sales would contract further to 3.5% from a prior contraction of 2.3%.

This might delight the European Central Bank (ECB) but is not sufficient to back a neutral stance for upcoming monetary policy meeting.

-

23:20

Fed’s Williams: Don’t think pace of rate hikes was behind the issues at two banks back in March

“Financial system troubles that drove the central bank to provide large amounts of credit to banks is not collateral damage from the Fed’s aggressive effort to lower inflation,” Federal Reserve (Fed) Bank of New York President, as well as Fed’s Vice Chairman of the rate-setting committee, John Williams said on Monday, per Reuters.

More comments

I personally don’t think the pace of rate increases was behind the issues at the two banks back in March.

Viewed the trouble at the two banks as unique in nature and unlikely to reflect broader trends in the financial system.

While past episodes of financial sector stress point to tightening credit, as it now stands, ‘we haven't seen clear signs yet of credit conditions tightening and we don't know how big this effect will be’ if it happens.

I don't really worry about the divergence.

I think part of it is because there is an expectation among many market participants and economists that the economy's going to slow even more than I expect.

Additional readables

- EUR/USD stabilizes near mid-1.0800s after setting weekly low

- NY Fed: Year-ahead expected inflation rises to 4.7% in March from 4.2% in February

-

23:10

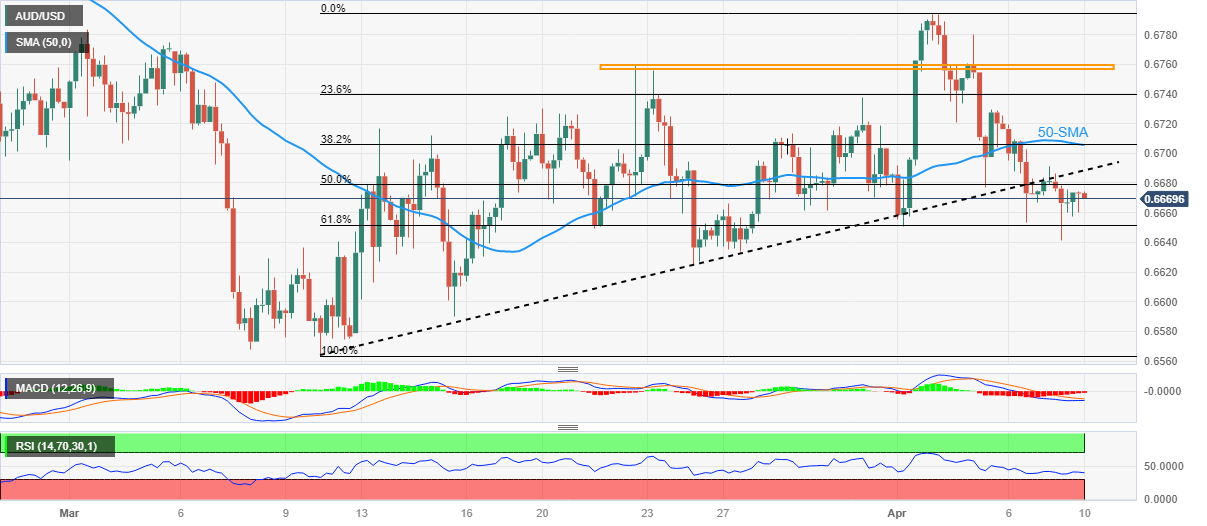

AUD/USD grinds lower towards 0.6600 amid firmer US Dollar, risk-off mood ahead of China inflation

- AUD/USD remains depressed around three-week low, stays bearish after five-day downtrend.

- Recovery in US Treasury bond yields joins US-China tension and RBA-inflicted bearish bias to weigh on Aussie prices.

- Australia Westpac Consumer Confidence, China inflation numbers eyed for fresh impulse.

AUD/USD holds lower grounds near 0.6640 after declining in the last five consecutive days. In doing so, the Aussie pair not only justifies its risk barometer status but also respects the US Dollar’s broad recovery amid firmer yields, as well as the Reserve Bank of Australia (RBA) induced bearish bias.

That said, the previous Friday’s US employment numbers renew hawkish bets on the Federal Reserve’s (Fed) next rate hike of 0.25% in May and allowed the US Treasury yields to recover. As a result, the US 10-year and two-year Treasury bond yields rose to 3.41% and 4.0% at the latest.

US Dollar Index (DXY) traced yields towards the north and rose for the fourth day in a row while poking a one-week high on Monday, around 102.55 by the press time.

It’s worth noting that the receding fears of the banking crisis in the US and escalating US-China tension joined the firmer US Treasury bond yields to also propel the US Dollar Index, which in turn drowned AUD/USD prices. Furthermore, RBA’s pause to its rate hike trajectory in the last week also exerts downside pressure on the Aussie pair.

Amid these plays, Wall Street benchmarks closed mixed, with minor moves, whereas the other riskier assets like commodities and Antipodeans stay depressed of late.

Moving on, AUD/USD pair traders should watch Westpac Consumer Confidence for March ahead of China’s headline inflation numbers for the said month, namely the Consumer Price Index (CPI) and Producer Price Index (PPI). Given the dragon nation’s recent optimism, coupled with the downbeat mood in Australia, any disappointment from the inflation numbers of a major customer won’t be taken lightly by the Aussie pair traders. Above all, Wednesday’s US CPI and Fed Minutes will be crucial ahead of Thursday’s employment data from Canberra.

Technical analysis

A clear downside break of the one-month-old ascending support line, now immediate resistance around 0.6700, keeps AUD/USD bears hopeful of visiting the yearly low of around 0.6565.

-

22:53

Gold Price Forecast: XAU/USD extends recovery above $1,990 as USD Index corrects, US Inflation in spotlight

- Gold price has stretched its recovery above $1,990.00, however, the downside remains favored.

- US labor market conditions remained tight despite tight credit conditions from US banks and high rates from the Fed.

- A surprise rebound is expected in US core inflation as earnings data is still higher due to a shortage of labor.

Gold price (XAU/USD) showed a recovery move after printing a three-day low at $1,981.38 in the Asian session. The precious metal has stretched its recovery above $1,990.00 as the US Dollar Index (DXY) has witnessed a correction after a five-day high at 102.81. The recovery move in the Gold price could be a pullback move only and the downside journey would resume as investors are expected to remain anxious ahead of the United States inflation data, which is scheduled for Wednesday.

Meanwhile, S&P500 ended Monday’s session with nominal gains as the recovery move came post a gap-down opening due to volatility inspired by the extended weekend. The US Treasury Yields recovered losses and settled above 3.41% on Monday as the Federal Reserve (Fed) is expected to hike rates again next month.

Earlier, the street was anticipating that Fed chair Jerome Powell would consider an early pause in the policy-tightening spell as tight credit conditions and higher rates would slow down the economy dramatically. However, tight labor market conditions have confirmed that a shortage of labor would be there, which will be offset by higher offerings.

This week, the annual Average Hourly Earnings data softened further to 4.2% but is well above against consistency required to tame stubborn inflation.

Going forward, the US Consumer Price Index (CPI) data will remain in the spotlight. A surprise rebound in the US inflation would cement the need for one more rate hike from the Fed. As per the consensus, the headline inflation will soften to 5.2% from the former release of 6.0%. Also, monthly headline CPI would decelerate to 0.3% from 0.4% reported earlier. While annual core inflation that excludes oil and food prices could surprisingly jump to 5.6% from the former release of 5.5%.

Gold technical analysis

Gold price has corrected sharply to near $1,987.00 after a breakout move from the Symmetrical Triangle chart pattern formed on a two-hour scale. The precious metal is at a make-or-a-break level as a breakdown from this level would trigger further weakness in the Gold price.

The 100-period Exponential Moving Average (EMA) at $1,991.00 is providing a cushion to the Gold price.

Meanwhile, the Relative Strength Index (RSI) (14) is defending itself from shifting into the bearish range of 20.00-40.00.

Gold two-hour chart

-

21:38

Forex Today: US Dollar strengthens ahead of US Inflation

The US Dollar rose on Monday on holiday-thinned trading, amid higher US yields. On Tuesday, China will inform inflation figures, and Australia Consumer and Business Confidence. Eurozone Retail Sales are also due. Despite all those indicators, the focus is on Wednesday's US March Consumer Price Index.

Here is what you need to know on Tuesday, April 11:

The US Dollar Index (DXY) extended its recovery and rose on Easter Monday, hitting a weekly high at 102.82, boosted by higher US yields and as equity prices performed mixed in Wall Street. The US 10-year yield settled at 3.42% while the 2-year rose above 4%. The Dow Jones rose 0.3%, the S&P 500 0.10% but the Nasdaq lost 0.03%. It was a quiet trading session with European markets closed. The Q1 earnings season kick-offs.

Market participants continue to digest the latest US Employment numbers. On Tuesday, data to be released include March Chinese inflation (Consumer and Producer Price Index) awaiting the US CPI on Wednesday.

EUR/USD posted the lowest close since late April around 1.0860, after finding support at 1.0830. On Tuesday, Retail Sales data from the Eurozone is due.

GBP/USD dropped for the fourth consecutive day on Monday, extending its correction from above 1.2500. It bottomed at 1.2343 at the beginning of the American session and then trimmed losses.

USD/JPY jumped to the highest level in almost a month, near 134.00, boosted by higher US yields. Volatility in the bond market warrant action around the Japanese Yen. On his first day as the Bank of Japan Governor, Kazuo Ueda said they want to avoid a sudden normalisation in monetary policy as it would cause a big impact on markets.

The Canadian Dollar outperformed during the American session on Monday. USD/CAD pulled back from weekly highs at 1.3550 to end the day flat around 1.3500.

AUD/USD fell for the fifth consecutive day, posting the lowest daily close in two weeks, under 0.6650. Australia will release Consumer and Business Confidence on Tuesday, and the jobs report on Thursday.

NZD/USD slid to weekly lows on Dollar strength but managed to rise back above 0.6200.

Gold price fell again finding support at $1,980, and rebounded to $1,990. Silver continued to move sideways below $25.00. Bitcoin hit fresh cycle highs near $30,000 after rising more than 3% on the day. Ethereum climbed 1.60% to $1,886.

Like this article? Help us with some feedback by answering this survey:

Rate this content -

20:39

NZD/USD trading at its lowest in two weeks

- New Bank of Japan Governor Kazuo Ueda spurred US Dollar buying.

- Speculation that the tightening cycle is over weighed on investors' mood.

- NZD/USD is neutral-to-bearish around 0.6220, could extend its slump.

It was not a good start to the week for the New Zealand currency, as it weakened sharply against its American rival. NZD/USD fell to 0.6913 on Monday and trades at around 0.6220 ahead of Tuesday's opening. The Kiwi lost the most during European trading hours despite financial markets in the Old Continent remaining closed due to the Easter Monday Holiday.

The main market driver at the beginning of the week was the Japanese yen, which edged lower following comments from the new Bank of Japan Governor, Kazuo Ueda, replacing Haruhiko Kuroda.

Among other things, Ueda said that he has agreed with Prime Minister Fumio Kishida that there is no immediate need to change the 2013 joint statement with the government. Furthermore, he noted that a small rate hike would not be a big issue for the financial system, quite relevant after a decade of ultra-loose monetary tightening in the country.

The US Dollar benefited from JPY's broad weakness and speculation that most major central banks will soon hit the pause bottom amid the increased risk of a global recession. Central banks had started retrieving monetary support in 2022 to tame inflation, and most of them stand halfway towards their goals. Still, continued tightening has resulted in a banking crisis, while growth has turned sluggish.

Technical Outlook

NZD/USD daily chart offers a neutral stance, although the risk of a bearish continuation has increased. It trades between directionless moving averages, with the 100 SMA providing resistance around 0.6300 and the 200 SMA acting as dynamic support at 0.6160. At the same time, the pair seesaws around an also flat 20 SMA, aiming to end the day below it. Finally, technical indicators hover around their midlines with uneven downward strength, in line with another leg south.

-

19:28

GBP/USD stays below 1.2400 in a slow start to the week

- The United Kingdom will release relevant macroeconomic figures next Thursday.

- The American Dollar is rising on the back of a dismal market mood.

- GBP/USD is under selling pressure and could fall towards 1.2273.

GBP/USD bounced modestly from an intraday low of 1.2343, now changing hands at around 1.2380. The pair edged sharply lower ahead of the US opening, despite the Eurozone and the United Kingdom celebrating Easter Monday, which kept local markets closed.

Wall Street, on the other hand, normally operated with US indexes trading mixed around their opening levels. The Dow Jones Industrial Average is up 0.14%, while the S&P 500 and the Nasdaq Composite remain in the red. Treasury yields, on the other hand, ticked north, with the 10-year note currently offering 3.41% and the 2-year note 4.0%.

The US Dollar advanced amid a dismal market mood, as market players are once again focused on a potential recession in the United States, following aggressive monetary tightening from the Federal Reserve (Fed) and the banking crisis that started last month.

The British Pound may find firmer directional strength on Thursday when the UK will release updates on the Gross Domestic Product, Industrial and Manufacturing Production, and the Trade Balance.

Technical Outlook

The GBP/USD pair is posting lower lows on a daily basis, in line with a bearish extension in the upcoming sessions, moreover, if the aforementioned daily low is infringed. The pair may then slide towards 1.2273, April 3 daily low, en route to 1.2189, March 24 low. Immediate resistance could be found in the 1.2440 region, with gains beyond it exposing the multi-week high set in early April at 1.2524.

-

18:35

AUD/USD under pressure around 0.6640

- The United States monthly employment report revived growth concerns.

- Australia will return from a long weekend publishing Westpac Consumer Confidence.

- AUD/USD declines for a fifth consecutive day near the 0.6600 figure.

The AUD/USD pair extended its intraday slump to 0.6618 after Wall Street's opening, barely bouncing from the level and currently trading in the 0.6680 price zone. The pair fell alongside US indexes, which started the day on the wrong foot amid concerns about a potential recession in the United States.

The Nonfarm Payrolls (NFP) report released on Friday showed that the US added 236,000 new jobs in March, slightly lower than the market expectation of 240,000. In addition, the Unemployment Rate edged lower to 3.5% from 3.6% in the same period, while the Labor Force Participation Rate improved to 62.6% from 62.5%. Finally, annual wage inflation, as measured by the Average Hourly Earnings, declined to 4.2% from 4.6%.

The US Dollar surged following the news as it indicated the job sector remains resilient while inflation keeps easing at a slow pace. Indeed, the NFP report was insufficient to change the Federal Reserve's (Fed) newly adopted dovish stance. The central bank is expected to hike its benchmark rate by 25 bps in April and pause afterwards. The banking crisis that started with the collapse of two American regional banks accelerated the Fed's decision to put an end to the tightening cycle.

Australia will return from a long weekend after the Easter holidays and will publish early on Tuesday, April. Westpac Consumer Confidence foreseen at 0.8% after posting 0% in March.

Technical Outlook

The AUD/USD pair is down for a fifth consecutive day and poised to extend its slump, according to technical readings in the daily chart, as the pair develops below directionless moving averages. The 20 Simple Moving Average (SMA) provides dynamic resistance just above the daily high, at 0.6685. Technical indicators, in the meantime, stand below their midlines without enough directional strength to confirm a steeper extension coming up next. A break through the 0.6600 level should encourage sellers and push AUD/USD towards the 0.6530/40 support area.

-

18:33

US: Inflation likely cooled off modestly but still rising at a strong pace in March – TDS

The most important economic report of the week will be the US Consumer Price Index on Wednesday. Analysts at TD Securities expect the index to rise by 0.1% in March, and the core by 0.4%. They see the CPI slowing to 3.6% by the fourth quarter.

Key quotes:

“Our estimates for the CPI report are likely to show that core price inflation cooled off modestly to a still strong m/m pace in March: We forecast inflation to print 0.1%/0.4% m/m for headline/core CPI, respectively. Importantly, we expect the report to confirm that core goods prices have shifted from subtracting from inflation to adding decidedly to it.”

“We continue to expect core inflation to settle around a still uncomfortable 0.4% m/m pace through Q2 2023.”

“We look for headline CPI to slow to 3.6% y/y in 23Q4, after closing 2022 at a booming 7.1% y/y pace. For core CPI, we also project deceleration to 3.8% y/y in 23Q4 from 6.0% in 22Q4. Finally, for the core PCE index, we forecast inflation of 3.6% y/y in 23Q4 after 4.8% y/y in 22Q4.”

-

17:44

WTI Price Analysis: Testing the $80 level on broad US Dollar

- Crude oil prices retreat alongside equities at the beginning of the week.

- OPEC+'s decision to trim oil output in early April revived growth-related concerns.

- WTI is technically neutral in the near term but holding within a well-limited range.

Crude oil prices are down on Monday as a risk-off mood underpins the American currency. The black gold stands a few cents above an intraday low of $79.71 a barrel and is nearing its latest range's base.

OPEC+ oil output cut

Early April, the Organization of the Oil Exporting Countries and Allies (OPEC+) surprised market players by announcing a cut in their oil output of around 1.16 million barrels per day, pushing West Texas Intermediate (WTI) roughly 5.5% higher on April 3, leaving a $4 unfilled gap. WTI has been consolidating between $79 and $81.80 since the announcement, unable to find fresh directional impetus.

Higher energy prices have been partially responsible for skyrocketing inflation, and OPEC+'s decision came as a complete shock and revived concerns not only about price pressure but also about economic growth.

Technical Outlook

The United States crude oil consolidative phase gives no signs of changing in the near term. Technical indicators are flat in intraday charts, with modest downward slopes, which only reflect the absence of buying interest but fell short of supporting a steeper decline.

The base of the range comes as a strong static support level, with a break below $79.00 favoring a downward extension towards the $75.60 area, where the pair closed on March 31. On the other hand, the pair could accelerate its advance towards $82.65, this year's high, once above the aforementioned $81.80.

-

17:28

EUR/USD stabilizes near mid-1.0800s after setting weekly low

- EUR/USD has gone into a consolidation phase near 1.0850.

- The risk-averse market environment and rising bond yields help USD gather strength.

- March inflation data from the US will be the next market driver.

EUR/USD started the new week on the back foot and touched its lowest level in a week at 1.0830 in the American session. The pair was last seen trading a few pips below 1.0850, losing 0.5% on a daily basis.

Hawkish Fed bets lift USD

Following the three-day weekend, Wall Street's main indexes opened in negative territory on Monday and helped the US Dollar find demand as a safe haven.

The March jobs report from the US, which showed that the Unemployment Rate declined to 3.5% with an increase of 236,000 in Nonfarm Payrolls (NFP), seems to have brought back hawkish Fed bets, providing an additional boost to USD. According to the CME Group FedWatch Tool, markets are currently pricing in a 72% probability of the Fed raising its policy rate by 25 basis points in early May.

Furthermore, the Federal Reserve Bank of New York's monthly consumer survey revealed that the one-year inflation expectation climbed to 4.7% from 4.2% in March's survey.

Earlier in the day, European Central Bank (ECB) policymaker Pablo Hernandez de Cos said that core inflation in the Eurozone was expected to remain elevated in the rest of the year and added that they have "ground to cover" in terms of policy. These comments, however, failed to help the Euro stay resilient against the USD.

Eurostat will release March Retail Sales data on Tuesday. More importantly, the US Bureau of Labor Statistics will publish the Consumer Price Index (CPI) data on Wednesday, which could have significant implications on the Fed's rate outlook and the USD's valuation.

Technical levels to watch for

-

16:46

Gold Price Forecast: XAU/USD his fresh lows at the $1,980 zone

- US Dollar accelerates its recovery on Monday after a long weekend.

- US yields move higher following NFP, ahead of US CPI.

- XAU/USD fails to hold above $2,000; extends correction from monthly highs.

Gold price is falling by more than 1% on Monday following Friday’s NFP and ahead of crucial US consumer inflation numbers. XAU/USD printed a fresh six-day low near $1,980 and then trimmed losses.

A stronger US Dollar and higher US yield weigh on the yellow metal. The US Dollar Index is having the biggest daily gain in weeks and trades at 102.75. At the same time, the US 10-year bond yield is at 3.43%, and the 2-year is back at 4.00%.

XAU/USD bottomed at $1,981, the lowest level since last Tuesday. It is hovering below $1,990, with a bearish bias in the short term, extending the correction from the recent top at $2,031.

Gold price technical analysis

The metal remains depressed after breaking a relevant short-term uptrend line and also after pulling back under $2,000. The primary trend is bullish and the price holds above key moving averages in the daily chart. The 20-day Simple Moving Average awaits at $1,967.

If XAU/USD rises back above $2,000, it could recover momentum. The next resistance stands at $2,010, followed by $2,022.

Technical levels

-

16:13

NY Fed: Year-ahead expected inflation rises to 4.7% in March from 4.2% in February

The Federal Reserve Bank of New York's monthly Survey of Consumer Expectations showed on Monday that the US consumers' one-year inflation expectation rose to 4.7% compared to 4.2% in February, the lowest level since May 2021.

Further details of the publication showed that the three-year ahead expected inflation rose to 2.8% versus 2.7% of the previous month. The five-year ahead expected inflation edged lower to 2.5% from 2.6%.

"Credit access perceptions deteriorated, with the share of households reporting that it is harder to obtain credit than one year ago rising and reaching a series high", added the report.

-

15:23

ECB's de Cos: Core inflation in Eurozone to remain elevated

European Central Bank (ECB) policymaker Pablo Hernandez de Cos said on Monday that core inflation in the Eurozone is projected to remain elevated for the rest of the year, as reported by Reuters.

"If the baseline scenario published in March is confirmed, there is still ground to be covered in terms of monetary policy," de Cos added.

Market reaction

These comments don't seem to be helping the Euro find demand in the American session. As of writing, EUR/USD pair was trading at 1.0840, where it was down 0.5% on a daily basis.

-

15:00

United States Wholesale Inventories came in at 0.1%, below expectations (0.2%) in February

-

14:58

GBP/USD slides to one-week lows near 1.2340 as Dollar strengthens

- US Dollar gains momentum as stocks slide and Treasury yields rise.

- GBP/USD looks bearish, near the 1.2340 support.

The GBP/USD broke below 1.2380 and tumbled to 1.2342, reaching the lowest level in a week amid a stronger US Dollar across the board. The Greenback gained momentum during the American session as US yields moved to the upside.

From NFP to CPI

The US Dollar Index is rising for the fourth consecutive session. It is hovering around 102.65, up 0.57% for the day, at the highest level in a week as it continues to bounce from monthly lows.

Higher US yields are helping the Greenback on Monday following the latest US economic data. The US 10-year yield stands at 3.41%, a one-week high. After the release of the Nonfarm Payrolls report on Friday, market participants are turning their focus to the US Consumer Price Index number are out on Wednesday. After the NFP, the odds of another rate hike at the FOMC May meeting rose.

The US Dollar is driving price action on Monday. Most European markets were closed. In Wall Street, the Dow Jones is falling 0.20%, and the Nasdaq drops by 1.25% after the first minutes of trading.

Short-term outlook

Technical indicators favor the downside for the moment; however, after the sharp decline, some consolidation and a rebound seem likely. A recovery above 1.2395 would alleviate the bearish pressure, while above 1.2440 the outlook would change to bullish.

The immediate support is around the 1.2340 area. A break lower should point to further losses, targeting initially the 1.2290 support area followed by last week’s low at 1.2270.

Technical levels

-

14:51

USD/CAD touches over one-week high, around 1.3550-55 area amid stronger USD

- USD/CAD turns positive for the fifth straight day and rallies to over a one-week high.

- A combination of factors boosts the USD and remains supportive of the intraday rally.

- Subdued Oil prices fail to influence the Loonie or hinder the ongoing recovery move.

The USD/CAD pair attracts fresh buyers following an intraday dip to the 1.3485 region and turns positive for the fifth successive day on Monday. The intraday uptick is sponsored by the emergence of aggressive US Dollar (USD) buying and lifts spot prices to over a one-week high, around the 1.3555 region in the last hour.

Against the backdrop of reviving bets for further tightening by the Federal Reserve (Fed), the risk-off impulse boosts demand for the safe-haven USD and assists the USD/CAD pair to build on last week's rebound from the 1.3400 mark, or its lowest level since February 16. In fact, the markets are now pricing in a greater chance of a 25 bps lift-off at the next FOMC meeting in May and the bets were reaffirmed by the mostly upbeat US monthly jobs report (NFP) released on Friday.

The global risk sentiment, meanwhile, took a hit in the wake of heightening US-China tensions over Taiwan. This is evident from a fresh leg down in the equity markets, which, in turn, forces investors to take refuge in traditional safe-haven assets, including the Greenback. Furthermore, subdued action around Crude Oil prices, despite looming supply cuts from OPEC+, fails to benefit the commodity-linked Loonie. This supports prospects for a further appreciating move for the USD/CAD pair, though traders might refrain from placing fresh bets ahead of this week's key central bank event risks.

The Bank of Canada (BoC) is scheduled to announce its policy decision on Wednesday and will be accompanied by the latest US consumer inflation figures. This will be followed by the release of the FOMC meeting minutes, which will play a key role in influencing the USD price dynamics and provide a fresh directional impetus to the USD/CAD pair. Traders will further take cues from the release of the US monthly Retail Sales figures on Friday. In the meantime, expectations that the Fed is nearing the end of its rate-hiking cycle could cap the buck and act as a headwind for the major.

Technical levels to watch

-

14:18

USD/JPY jumps closer to 100 DMA barrier near mid-133.00s amid broad-based USD strength

- USD/JPY rallies to a one-week high and draws support from a combination of factors.

- Reviving bets for a 25 bps Fed rate hike in May boosts the USD and acts as a tailwind.

- Dovish remarks by the new BoJ Governor also contribute to the strong intraday rise.

The USD/JPY pair scales higher for the third successive day on Monday and touches a one-week high heading into the North American session. The pair is currently placed around the 133.30 mark, up nearly 0.90% for the day, with bulls now eyeing to challenge the 100-day Simple Moving Average (SMA) barrier amid broad-based US Dollar (USD) strength.

In fact, the USD Index, which tracks the Greenback against a basket of currencies, builds on last week's recovery move from over a two-month low and gains strong follow-through traction amid expectations for further rate hikes by the Federal Reserve (Fed). The markets are now pricing in a greater chance of a 25 bps lift-off at the next FOMC policy meeting in May and the bets were lifted by the mostly upbeat US monthly employment details released on Friday. This, in turn, continues to push the USD higher, which, along with dovish-sounding remarks by the new Bank of Japan (BoJ) Governor

Kazuo Ueda, prompt aggressive short-covering around the USD/JPY pair.During his inauguration speech, Ueda ruled out any major policy shift and said that they want to avoid a sudden normalisation in monetary policy as it would cause a big impact on markets. This, in turn, weighs heavily on the Japanese Yen (JPY) and provides an additional boost to the USD/JPY pair. That said, the risk-off impulse - as depicted by a fresh leg down in the equity markets - could lend some support to the safe-haven JPY and keep a lid on any further gains for the major, at least for the time being. Against the backdrop of worries about a deeper global economic downturn, heightened US-China tensions over Taiwan tempers investors' appetite for riskier assets.

This makes it prudent to wait for a sustained break through the 100-day SMA before positioning for any further appreciating move ahead of the US consumer inflation figures and the FOMC meeting minutes, due for release on Wednesday. Apart from this, traders will take cues from the US monthly Retail Sales figures on Friday. This will play a key role in influencing the near-term USD price dynamics and help determine the next leg of a directional move for the USD/JPY pair.

Technical levels to watch

-

13:30

Chile Trade Balance rose from previous $1999M to $2906M in March

-

13:29

EUR/USD drops to one-week low, closer to mid-1.0800s amid notable USD strength

- EUR/USD turns lower for the second successive day amid strong follow-through USD buying.

- Reviving bets for more rate hikes by the Fed and geopolitical tensions benefit the Greenback.

- The fundamental backdrop, however, warrants caution before placing aggressive bearish bets.

The EUR/USD pair attracts fresh sellers following an early uptick to the 1.0915 region and turns lower for the second successive day on Monday. This also marks the third day of a negative move in the previous four and drags spot prices to a one-week low, around the 1.0860-1.0855 region heading into the North American session.

A combination of supporting factors assists the US Dollar (USD) to gain strong follow-through traction on the first day of a new week, which, in turn, exerts downward pressure on the EUR/USD pair. In fact, the USD Index, which tracks the Greenback against a basket of currencies, spikes to a one-week high amid reviving bets for further policy tightening by the Federal Reserve (Fed). In fact, the markets are now pricing in a greater chance of a 25 bps lift-off at the next FOMC meeting in May and the bets were lifted by the mostly upbeat US employment details released on Friday. Apart from this, heightened US-China tensions over Taiwan and a generally weaker tone around the equity markets further lend support to the safe-haven buck.

Investors, however, seem convinced that the US central bank will cut rates in the second half of the year amid signs of slowing economic growth. This, along with the flight to safety, triggers a fresh leg down in the US Treasury bond yields and might hold back the USD bulls from placing aggressive bets. Furthermore, the growing acceptance of additional rate hikes by the European Central Bank (ECB) should continue to underpin the shared currency and limit the downside for the EUR/USD pair amid relatively light trading volumes. This warrants some caution before placing aggressive directional bets and positioning for an extension of the pair's recent pullback from over a two-month top, around the 1.0970-1.0975 area touched last week.

Traders might also prefer to move to the sidelines ahead of the release of the latest US consumer inflation figures and the FOMC monetary policy meeting minutes on Wednesday. This week's US economic docket also features the release of monthly Retail Sales figures, which will play a key role in influencing the near-term USD price dynamics and help determine the next leg of a directional move for the EUR/USD pair.

Technical levels to watch

-

12:19

BoJ's Ueda: Want to avoid sudden normalisation in policy

New Bank of Japan (BoJ) Governor, Kazuo Ueda, said on Monday that they want to avoid a sudden normalisation in monetary policy as it would cause a big impact on markets, as reported by Reuters.

Key takeaways

"We will debate all policy options at every monetary policy meeting."

"Fully aware that global economy is slowing and further slowdown is expected."

"Positive signs are emerging in prices."

"Very possible to reach sustainable price target as wage growth strengthens."

"Will do utmost to achieve inflation target during my term while paying attention to side effects."

"Will aim to explain each policy move in plain language."

"Need to make appropriate decision before reaching that stage."

Market reaction

USD/JPY edges higher following these comments and was last seen gaining 0.3% on the day at 132.55.

-

11:43

Silver Price Analysis: XAG/USD bulls retain control near $25.00 mark, just below YTD top

- Silver regains positive traction on Monday and climbs back closer to the YTD peak.

- The technical setup favours bullish traders and supports prospects for further gains.

- Overbought RSI on the daily chart warrants caution before placing aggressive bets.

Silver attracts some dip-buying on the first day of a new week and steadily climbs back closer to the $25.00 psychological mark during the first half of the European session. The white metal is currently placed just below a nearly one-year high touched on Friday and seems poised to prolong its recent upward trajectory witnessed over the past month or so.

Last week's sustained breakout through the $24.30-$24.40 strong horizontal barrier was seen as a fresh trigger for bullish traders. Furthermore, the emergence of fresh buying ahead of the said resistance breakpoint now turned support, adds credence to the positive outlook. That said, Relative Strength Index (RSI) on the daily chart is flashing overbought conditions and warrants some caution before positioning for any further appreciating move.

Hence, it will be prudent to wait for some near-term consolidation or a modest pullback before positioning for a fresh leg up. Nevertheless, the XAG/USD seems poised to surpass the $25.10-$25.15 area and climb further towards the $25.35-$25.40 region. The momentum could get extended towards the $26.00 mark en route to the next relevant hurdle near the $26.20 area, the $26.40-$26.50 zone and the 2022 high, just ahead of the $27.00 mark.

On the flip side, any meaningful pullback is likely to attract fresh buyers and remain limited near the $24.40-$24.30 resistance-turned-support. The said area should now act as a pivotal point, which if broken decisively might prompt some technical selling. The XAG/USD might then turn vulnerable to weaken below the $24.00 mark and test the $23.60-$23.55 support area before eventually dropping to the $23.15 zone en route to the $23.00 round figure.

Silver daily chart

Key levels to watch

-

11:26

BoJ's Ueda: BoJ faces task of making various efforts to sustain monetary easing

The new governor of Bank of Japan (BoJ), Kazuo Ueda, reiterated on Monday that they will do the utmost to achieve price stability and financial system stability, as reported by Reuters.

"It's very important for financial intermediation to smoothly play out in the economy," Ueda added and acknowledged that the BoJ faces the task of making various efforts to sustain monetary easing.

Ueda further noted that he wants to achieve the 2% inflation target during his 5-year term.

Market reaction

USD/JPY showed no immediate reaction to these comments and was last seen trading modestly higher on the day at 132.30.

-

11:02

Portugal Global Trade Balance climbed from previous €-7.269B to €-7.213B in February

-

10:48

AUD/USD recovers further from two-week low, climbs to 0.6675-80 area amid softer USD

- AUD/USD edges higher on Monday and snaps a four-day losing streak to a two-week low.

- Expectations for a dovish Fed pivot keep the USD bulls on the defensive and lend support.

- Geopolitical tensions and the RBA’s dovish tilt might keep a lid on any meaningful upside.

The AUD/USD pair attracts some buyers near the mid-0.6600s on the first day of a new week and moves away from a two-week low touched on Friday. Spot prices, however, lack follow-through and trade with a mild positive bias, around the 0.6675-0.6680 area during the first half of the European session.

The US Dollar (USD) struggles to preserve its modest intraday gains amid the uncertainty over the Federal Reserve's (Fed) rate-hike path and turns out to be a key factor lending some support to the AUD/USD pair. The mostly upbeat US NFP released on Friday revived bets for another 25 bps lift-off at the next FOMC meeting in May. Market participants, however, seem convinced that the Fed will cut rates in the second half of the year amid signs of slowing economic growth. This is reinforced by a fresh leg down in the US Treasury bond yields, which acts as a headwind for the Greenback.

The upside for the AUD/USD pair, however, seems capped amid the Reserve Bank of Australia's (RBA) dovish tilt last week, pausing its rate-hiking cycle following 10 consecutive raises and signalling that inflation had likely peaked. Apart from this, heightened US-China tensions over Taiwan might further contribute to keeping a lid on the risk-sensitive Aussie. This, in turn, makes it prudent to wait for strong follow-through buying before placing fresh bullish bets around the major confirming that the recent rejection slide from 100-day Simple Moving Average (SMA) has run its course.

Traders also seem reluctant and prefer to move to the sidelines ahead of the FOMC meeting minutes, due on Wednesday. This week's US economic docket also features the release of the latest consumer inflation figures and monthly retail sales data. This will play a key role in influencing the USD price dynamics and provide a fresh directional impetus to the AUD/USD pair. Nevertheless, the fundamental backdrop suggests that the path of least resistance for spot prices remains to the downside and any further move up might still be seen as an opportunity for bearish traders.

Technical levels to watch

-

10:29

New BoJ Governor Ueda: Discussed the need to guide policy flexibly given economic uncertainty

Following his meeting with Japanese Prime Minister Fumio Kishida on Monday, new Bank of Japan (BoJ) Governor Kazuo Ueda said that they discussed the need to guide policy flexibly given economic uncertainty.

Additional takeaways

“Agreed with PM Kishida that there is no immediate need to change the 2013 joint statement with the government.”

“When uncertainty is high, govt, BoJ must communicate closely.”

“BoJ’s monetary stimulus has helped pull japan out of deflation.”

-

10:20

United Kingdom: More hopes of stabilization – Societe Generale

Analysts at Societe Generale said in their latest client note, “in a light data week following Easter, the main focus will be on the monthly GDP data.”

Additional quotes

“It has been highly volatile over the turn of the year because of strikes and other influences on public sector activity but we think those effects will have faded in February to give a second successive month of growth.”

“This will raise hopes that the UK might be able to avoid a recession altogether as the Office for Budget Responsibility has recently forecast.“

“The RICS housing survey is likely to show further modest improvement.”

-

10:08

USD/CAD trades with modest losses below 1.3500 amid bullish Oil prices, subdued USD

- USD/CAD drifts lower on Monday and is weighed down by a combination of factors.

- Bullish Oil prices underpin the Loonie and exert pressure amid fresh USD selling.

- The downside seems cushioned ahead of this week’s key central bank event risks.

The USD/CAD pair attracts some sellers near the 1.3520 region on Monday and snaps a four-day winning streak. The pair is currently placed just below the 1.3500 psychological mark, down nearly 0.10% for the day, and is pressured by a combination of factors.

Crude Oil prices hold steady near a multi-month top touched last week in reaction to a new round of production cuts announced by the OPEC+, which, to a larger extent, overshadows concerns that weakening global growth may dent fuel demand. This, in turn, is seen underpinning the commodity-linked Loonie and exerting some downward pressure on the USD/CAD pair amid the emergence of some intraday selling around the US Dollar (USD).

In fact, the USD Index, which tracks the Greenback against a basket of currencies, surrenders its modest intraday gains amid the uncertainty over the Federal Reserve's (Fed) rate hike path. The mostly upbeat US NFP released on Friday revived bets for another 25 bps lift-off at the next FOMC meeting in May. Market participants, however, seem convinced that the Fed will cut rates in the second half of the year amid signs of slowing economic growth.

Expectations that the Fed is nearly done with its policy tightening lead to a fresh leg down in the US Treasury bond yields, which continue to act as a headwind for the buck and prompt fresh selling around the USD/CAD pair. The downside, however, seems cushioned as traders might refrain from placing aggressive bets ahead of the key central bank event risks - the Bank of Canada policy meeting and the release of the FOMC meeting minutes on Wednesday.

This week's US economic docket also features the release of the latest consumer inflation figures and monthly retail sales data, which will play a key role in influencing the USD and provide a fresh directional impetus to the USD/CAD pair. In the meantime, relatively thin liquidity conditions, in the wake of a holiday in most European markets, might hold back traders from placing aggressive bets and contributes to limiting losses for the major.

Technical levels to watch

-

10:00

Greece Consumer Price Index - Harmonized (YoY) down to 5.4% in March from previous 6.5%

-

10:00

Greece Consumer Price Index (YoY) declined to 4.6% in March from previous 6.1%

-

10:00

Greece Industrial Production (YoY): 5.2% (February) vs 0.5%

-

09:58

IMF’s Georgieva: India, China to account for 50% of global economic growth in 2023

International Monetary Fund’s (IMF) Managing Director Kristalina Georgieva said that “the global economy is estimated to grow less than 3 percent in 2023, with India and China expected to account for half of the global growth this year.

Key takeaways

“Some momentum comes from emerging economies -- Asia especially is a bright spot. India and China are expected to account for half of the global growth in 2023.”

“Despite surprisingly resilient labor markets and consumer spending in most advanced economies, and the uplift from China's reopening, we expect the world economy to grow less than 3 percent in 2023.”

“Economic activity is slowing in the US and the Eurozone because of the current higher interest rates regime, thereby weighing on the demand.”

“For low-income countries, higher borrowing costs come at a time of weakening demand for their exports. And we see their per-capita income growth staying below that of emerging economies. That is a severe blow, making it even harder for low-income nations to catch up.”

-

09:37

WTI: Oil looking up on inventory draws and OPEC+ cuts – TDS

Analysts at TD Securities offer a bullish outlook on WTI, in the wake of the OPEC and its allies (OPEC+) oil output cuts and US oil inventory drawdown and a potential increase in Chinese oil demand.

Key quotes

“Despite broad concerns surrounding global economic weakness and a lackluster risk appetite, crude oil continues to hold on to the strong gains made recently as the market focuses on the EIA data showing broad inventory draws and the unexpectedly large OPEC+ production cuts.”

“The crude complex is pricing a much tighter supply-demand environment for the rest of 2023, putting the previous OPEC statements suggesting a Q2 surplus, and demand concerns amid the evolving bank crisis, in the rearview mirror.”

“Notwithstanding pending economic weakness in the Western world, we judge that the combination of OPEC+ cuts, low US petroleum complex inventory levels and the upcoming sharp increase in Chinese demand will send WTI into $90+ territory in the second half of the year, with Brent not far off the triple digit mark.”

-

09:22

GBP/USD sticks to modest intraday gains above 1.2400, lacks follow-through

- GBP/USD attracts some dip-buying on Monday and snaps a three-day losing streak.

- The USD surrenders its modest intraday gains and lends some support to the major.

- Bulls lack conviction amid the uncertainty over the next move by the Fed and the BoE.

The GBP/USD pair reverses an intraday dip to sub-1.2400 levels and turns positive during the first half of the European session, though lacks follow-through. The pair currently trades around the 1.2420-1.2425 region, up less than 0.10%, and for now, seems to have snapped a three-day losing streak.

The US Dollar (USD) struggles to preserve its modest intraday gains amid the uncertainty over the Federal Reserve's (Fed) rate-hike path and turns out to be a key factor lending some support to the GBP/USD pair. The mostly upbeat US NFP released on Friday revived bets for another 25 bps lift-off at the next FOMC meeting in May. Market participants, however, seem convinced that the Fed will cut rates in the second half of the year amid signs of slowing economic growth. This is reinforced by a fresh leg down in the US Treasury bond yields, which acts as a headwind for the Greenback.

The upside for the GBP/USD pair, meanwhile, remains capped in the wake of the recent mixed signals from the Bank of England (BoE) members over the next policy move. It is worth recalling that the BoE MPC member Silvana Tenreyro advocated last Tuesday for the consideration of cutting rates sooner than thought as the absence of cost-push shocks would bring down inflation well below targets. In contrast, the BoE Chief Economist Huw Pill said that action is still needed in assessing inflation prospects and that the onus remains on ensuring enough policy tightening is delivered to see the job through.

Given that most European markets are closed in observance of Easter Monday, the aforementioned mixed fundamental backdrop is holding back traders from placing aggressive bullish bets around the GBP/USD pair amid relatively thin liquidity. Investors also seem reluctant and prefer to move to the sidelines ahead of the FOMC meeting minutes, due on Wednesday. This week's US economic docket also features the release of the latest consumer inflation figures and monthly retail sales data. This will play a key role in influencing the USD and provide a fresh directional impetus to the major.

Technical levels to watch

-

09:17

US: Inflation data take center stage this week – BBH

Economists at BBH offer a sneak peek at what to expect from the all-important United States Consumer Price Index (CPI) and Producer Price Index (PPI) data due for release this week on Wednesday and Thursday respectively.

Key quotes

“Inflation data take center stage this week. March CPI will be reported Wednesday.”

“Headline is expected at 0.2% m/m and 5.1% y/y vs. 0.4% m/m and 6.0% y/y in February. Core is expected at 0.4% m/m and 5.6% y/y vs. 0.5% m/m and 5.5% y/y in February.”

“Of note, the Cleveland Fed’s inflation nowcast model sees headline CPI at 0.30% m/m and 5.22% y/y and core CPI at 0.45% m/m and 5.66% y/y, both slightly above consensus.”

“PPI will be reported Thursday. Headline is expected at 0.0% m/m and 3.0% y/y vs. -0.1% m/m and 4.6% y/y in February. Core is expected at 0.3% m/m and 3.5% y/y vs. 0.0% m/m and 4.4% y/y in February. “

-

09:09

US labour market cooling, but still hot – ABN Amro

Economists at ABN Amro noted in their latest client note that the” US Payrolls growth slowed to 236k in March, down from 326k in February, and continuing the broad cooling trend in the labour market of the past year or so.”

Additional quotes

“The unemployment rate declined one tenth, to 3.5% – close to its all-time low. Wage growth remained benign at 0.3% m/m (4.2% y/y), though we must add the caveat here that productivity has been very weak of late, meaning that unit labour cost growth has surged (meaning that the labour market still poses upside risks to inflation). The overall message is that the labour market is loosening, but remains exceptionally tight. “

“Although markets reacted strongly to the steep drop in the JOLTS job vacancies on Wednesday, we interpret this data with caution given that similarly large declines in the past were subsequently revised away. The tendency for the JOLTS data to be revised may reflect that the survey response rate has fallen to a very low level of c.30% (i.e. the data is likely not as reliable as it used to be).”

“A more gradual slowing in the labour market is visible in other data, including continuing jobless claims, and challenger job cut announcements (both of which have been rising but remain historically low).”

-

08:45

USD/JPY trims a part of intraday gains to four-day high, holds above 132.00 mark

- USD/JPY gains traction for the third straight day amid a modest USD strength.

- The upbeat US NFP revives bets for more Fed rate hikes and underpins the buck.

- Sliding US bond yields cap gains for the USD and the pair amid geopolitical risks.

The USD/JPY pair scales higher for the third successive day on Monday and touched a four-day high, around the 132.80 region, albeit lacks follow-through. Spot prices trim a part of the intraday gains and trade around the 132.35 area during the early European session, up less than 0.15% for the day.

Reviving bets for further policy tightening by the Federal Reserve (Fed) push the US Dollar (USD) higher for the fourth straight day, which turns out to be a key factor acting as a tailwind for the USD/JPY pair. In fact, the markets are now pricing in a greater chance of a 25 bps lift-off at the next FOMC policy meeting in May and the bets were lifted by the mostly upbeat US employment details released on Friday. The intraday uptick, however, runs out to steam near the 132.80 region, warranting some caution for aggressive bullish traders.

Market participants still seem convinced that the Fed will cut rates in the second half of the year amid signs of slowing economic growth. This, along with a fresh leg down in the US Treasury bond yields, caps any meaningful upside for the buck. Apart from this, heightened US-China tensions over Taiwan drive some haven flows towards the Japanese Yen (JPY) and further contribute to keeping a lid on the USD/JPY pair. Traders also seem reluctant ahead of the new Bank of Japan (BoJ) Governor Kazuo Ueda's inauguration speech at 1030 GMT).

Moreover, most European markets are closed in observance of Easter Monday and relatively thin trading volumes might further hold back traders from placing fresh bets. The market focus, meanwhile, remains glued to the FOMC policy meeting minutes, due on Wednesday. This week's US economic docket also features the release of the latest consumer inflation figures and monthly retail sales data, which will play a key role in influencing the near-term USD price dynamics and determining the next leg of a directional move for the USD/JPY pair.

Technical levels to watch

-

08:01

Turkey Current Account Balance came in at $-8.783B below forecasts ($-8.5B) in February

-

08:00

Turkey Unemployment Rate climbed from previous 9.7% to 10% in February

-

07:57

Gold Price Forecast: XAU/USD bears seek re-entry near $1,990 as Easter Monday triggers USD rebound

- Gold price pares the first weekly gains in three, bounces off 200-EMA at the latest.

- China-inflicted risk aversion, hawkish Fed bets underpin US Dollar’s corrective bounce after four-week downtrend.

- XAU/USD bears remain cautious ahead of key support.

- Easter Monday holidays, anxiety ahead of US inflation, Fed Minutes add filters to Gold price.

Gold price (XAU/USD) trims intraday losses around $1,995 amid the Easter Monday holiday in major bourses. In doing so, the bullion bounces off the 200-bar Exponential Moving Average (EMA) but remains mildly offered on a day, which in turn teases sellers after the bullion marked the first weekly gains in three at the last.

That said, the China-linked risk-off mood joins the US Dollar’s rebound to exert downside pressure on the Gold price. However, the market’s latest inaction limits the XAU/USD moves of late. Recently, South Korea joined the US in defending Taiwan as Beijing marks a heavy show of military drills. Even so, the terms of tension are still inexplicable as the US signals the latest moves of sending arms help to Taipei as precautionary and resists taking major steps.

Elsewhere, Friday’s better-than-forecast prints of the US Nonfarm Payrolls (NFP) renew hawkish Fed bets and suggest a 0.25% rate hike by the US central bank versus previously expected inaction.

It should be noted, however, that the downbeat US Treasury bond yields and the overall weak US statistics prod the US Dollar bulls and allow the Gold buyers to remain hopeful ahead of the US Consumer Price Index (CPI) data and the latest Federal Open Market Committee (FOMC) Monetary Policy Meeting Minutes.

While portraying the mood, the S&P 500 Futures print mild losses around 4,130, after a two-day uptrend, whereas the US 10-year and two-year Treasury bond yields remain pressured near 3.37% and 3.95% respectively. In doing so, the benchmark bond coupons extend the previous day’s losses and portray the market’s rush toward the risk-safety amid economic slowdown fears. Further, the US Dollar Index (DXY) prints mild gains around 102.20 while extending the last Tuesday’s rebound from a two-month low.

Moving on, Gold traders should pay attention to the geopolitical headlines for intraday directions while US inflation and Fed Minutes will be crucial for a clear guide afterward.

Gold price technical analysis

Gold price remains depressed as XAU/USD breaks the one-week-old ascending support line, now resistance, as well as the 50-bar Exponential Moving Average (EMA) surrounding $2,007, to lure Gold sellers.

Even so, the 200-EMA and previous resistance line from March 20, respectively near $1,990 and $1,982, can challenge the Gold price downside ahead of welcoming the bears.

In that case, an ascending support line from March 22, close to $1958, will be on the XAU/USD seller’s radar.

Meanwhile, recovery moves remain elusive unless crossing the 50-EMA hurdle of $2,007. Following that, the recent high near $2,035 and previous support line from April 03, now resistance around $2,040, can test the Gold buyers.

Should the precious metal remains firmer past $2,040, the previous yearly top surrounding $2,070 and the all-time high marked in 2020 around $2,075 will be in focus.

Gold price: Hourly chart

Trend: Further downside expected

-

07:54

US Dollar Index builds on the post-NFP positive move, lacks bullish conviction

- The US Dollar Index edges higher for the fourth straight day on Monday, though lacks follow-through.

- The upbeat US NFP report revives bets for additional Fed rate hikes and is seen underpinning the buck.

- Geopolitical tensions further benefit the safe-haven Greenback and remain supportive of the move up.

- Expectations that the Fed will cut rates during the second half of the year cap the upside for the USD.

The US Dollar Index (DXY), which tracks the Greenback against a basket of currencies, kicks off the new week on a positive note and builds on its recent bounce from the lowest level since early February touched last Wednesday. This marks the fourth successive day of a positive move for the buck, though lacks follow-through or bullish conviction amid the uncertainty over the Federal Reserve's (Fed) rate-hike path.

The mostly upbeat US monthly employment details released on Friday suggested that the US central bank may have to raise interest rates next month. In fact, the headline NFP showed that the US economy added 236K new jobs in March against market expectations for a reading of 240K. Furthermore, the jobless rate edged down to 3.5% from 3.6% the previous, while Average Hourly Earnings rose 0.3% during the reported month. The annual wage gains, meanwhile, slowed, though remain too high to be consistent with the Fed's 2% inflation target and support prospects for further policy tightening.

Apart from this, the risk of a further escalation in tensions between the US and China is seen as another factor benefitting the Greenback's relative safe-haven status. It is worth mentioning that China retaliated against Taiwan President Tsai Ing-wen’s US visit and carried out aggressive military drills around Taiwan on Monday. The de facto US embassy in Taiwan said on Sunday the US has sufficient resources and capabilities regionally to ensure peace and stability. This comes amid worries about a deeper global economic downturn, which continues to weigh on investors' sentiment and drives some haven flows.

Market participants, however, seem convinced that the Fed will cut rates in the second half of the year and the expectations were fueled by the recent US macro data, which has been pointing to slowing economic growth. This, in turn, might hold back the USD bulls from placing aggressive bets and cap the upside ahead of the FOMC meeting minutes, due on Wednesday. This week's US economic docket also features the release of the latest consumer inflation figures and monthly retail sales data, which if misses consensus estimates will take Fed rate-hike bets off the table and weigh on the USD.

Technical levels to watch

-

07:44

Forex Today: Market action remains subdued on Easter Monday

Here is what you need to know on Monday, April 10:

Following last Friday's quite trading, markets stay calm to start the week with most markets remaining closed on Easter Monday. In the second half of the day, US stock and bond markets will open at the usual time. February Wholesale Inventories will be the only data featured in the US economic docket and NY Fed President John Williams will be delivering a speech in the American trading hours.

On Friday, the US Bureau of Labor Statistics reported that Nonfarm Payrolls rose by 236,000 in March, slightly lower than the market expectation of 240,000. The Unemployment Rate edged lower to 3.5% from 3.6% in the same period and the Labor Force Participation Rate improved to 62.6% from 62.5%. Finally, annual wage inflation, as measured by the Average Hourly Earnings, declined to 4.2% from 4.6%.

Following the jobs report report, the benchmark 10-year US Treasury bond yield gained nearly 3% in the shortened session and snapped a seven-day losing streak. In turn, the US Dollar Index (DXY) registered modest daily gains. Early Monday, the DXY holds comfortably above 102.00 but the 10-year US yield stays in negative territory at around 3.35%. Meanwhile, US stock index futures trade mixed before Wall Street comes back from a long weekend.

Following Friday's pullback, EUR/USD trades within a very tight range at around 1.0900 in the European morning on Monday.

GBP/USD managed to close the previous week slightly above 1.2400 but struggled to gain traction early Monday.

USD/JPY edged higher during the Asian trading hours on Monday and was last seen trading in positive territory above 132.50. The data from Japan showed earlier in the day that the Consumer Confidence Index improved to 33.9 in March from 31.1 in February.

Gold price opened with a bearish gap following the sharp rebound witnessed in US yields on Friday. XAU/USD was last seen moving up and down in a range slightly below $2,000.

Bitcoin posted modest gains on Sunday but continues to fluctuate within its 10-day-old range at around $28,000. Ethereum is having a difficult time gathering bullish momentum and staying below $1,900 despite having snapped a three-day losing streak on Sunday.

-

07:14

EUR/USD Price Analysis: 10-DMA prods intraday sellers, 1.0850 is the last defense for bulls

- EUR/USD remains depressed around intraday low, snaps three-week uptrend.

- Downside break of three-week-old ascending trend line, receding bullish bias of MACD favor sellers.

- Fortnight-long support line acts as additional check for Euro bears.

- RSI retreat, multiple hurdles above 1.1000 keeps EUR/USD sellers hopeful.

EUR/USD remains indecisive around 1.0920, recently bouncing off the intraday low to pare the latest losses amid early Monday.

In doing so, the Euro pair portrays a U-turn from the 10-DMA support while defending the previous week’s hesitance in breaking the key horizontal hurdle from late January, around 1.0930. Even so, the EUR/USD pair remains sidelined after positing a three-week uptrend in the last.

Apart from the Euro pair’s inability to cross the 1.0930 hurdle, the receding bullish bias of the MACD and the RSI (14) line’s retreat also suggest a pullback in the EUR/USD price.

However, a daily closing below the 10-DMA support of 1.0890 becomes necessary for the intraday sellers of the pair. Following that, an upward-sloping support line from March 24, near 1.0850, becomes the last defense of the EUR/USD bulls.

Meanwhile, a daily closing beyond 1.0930 isn’t an open invitation to the EUR/USD bulls as the previous support line from mid-March, around 1.1015 by the press time, precedes the yearly high marked in January around 1.1035, to challenge further upside of the major currency pair.

In a case where EUR/USD remains firmer past 1.1035, the late March 2022 high near 1.1185 will be in focus.

Overall, EUR/USD is well-set for a pullback but the Easter Monday holiday restricts the pair’s moves.

EUR/USD: Daily chart

Trend: Further downside expected

-

07:09

USD/CAD attempts upside above 1.3520 ahead of US Inflation and Bank of Canada policy

- USD/CAD is putting efforts to shift the business above 1.3520 amid anxiety ahead of US Inflation.

- Federal Reserve is likely to consider one more rate hike in May amid tight labor market conditions.

- Bank of Canada would keep rates steady as Canada’s inflation is softening meaningfully.

- USD/CAD is auctioning in a Rising Channel, however, the upside momentum looks weak.

USD/CAD is making efforts in shifting business above the immediate resistance of 1.3520 in the Asian session. The Loonie asset is gaining traction as investors are awaiting the release of the United States inflation figures and the interest rate decision by the Bank of Canada (BoC), which will release on Wednesday.

S&P500 futures have turned negative after surrendering opening gains as geopolitical tension between China and Taiwan has underpinned the risk aversion theme. Also, investors are cautionary for US equities as the quarterly result season will kick off sooner.

Meanwhile, the US Dollar Index (DXY) is continuously refreshing day’s high as tight US labor market conditions have strengthened hopes of more rate hikes from the Federal Reserve (Fed). The USD Index has printed a high of 102.25. The US Treasury yields are showing a subdued performance despite rising odds of a hawkish Federal Reserve policy for May.

Federal Reserve to raise rates further as Unemployment Rate remains lower

Friday’s US Employment data has confirmed that higher rates by the Federal Reserve and tight credit conditions by commercial banks after the collapse of Silicon Valley Bank (SVB) and Signature Bank had a minimal impact on the US labor market. In March, the US economy added fresh 236K, marginally lower than the consensus of 240K but significantly lower than the former release of 326K. The Unemployment Rate dropped further to 3.5% from the consensus and the prior release of 3.6%.

Less impact of higher rates on the US labor market has strengthened the need for more hikes to arrest the stubborn US inflation. According to money market expectations, 64% of investors are supporting more rate hikes from the Federal Reserve.

US Inflation to provide clarity on Federal Reserve’s interest rate guidance

After the US Nonfarm Payrolls (NFP) data, investors are sticking to Consumer Price Index (CPI) data, which will provide extensive clarity on interest rate guidance. As per the consensus, the headline inflation will soften to 5.2% from the former release of 6.0%. Also, monthly headline CPI would decelerate to 0.3% from 0.4% reported earlier. Oil prices remained lower in March and its effect is expected to get visible in inflationary pressures.

However, the upward-rising US labor cost index due to a shortage of labor is keeping demand for core goods resilient. This might force Federal Reserve chair Jerome Powell to put the last nail in the coffin by pushing rates above 5% to intermediate pivotal.

Bank of Canada to keep rates unchanged

This week, the Canadian Dollar will dance to the tunes of the interest rate decision by the Bank of Canada. A continuation of a neutral policy stance is expected from Bank of Canada Governor Tiff Macklem as Canada’s inflation is softening consecutively. The inflation rate has already decelerated to 5.2% in February as the Bank of Canada monetary policy is restricted enough to tame inflationary pressures.

Last week, Canada’s employment data remained extremely tight. Demand for labor crossed expectations significantly and the Unemployment Rate was trimmed further to 5%. This could put some pressure on the Bank of Canada for reconsidering policy stance.

USD/CAD technical outlook

USD/CAD is auctioning in a Rising Channel chart pattern on an hourly scale in which corrections are considered buying opportunities by the market participants. However, the upside momentum looks weak amid an absence of any perpendicular move by the US Dollar.

The Relative Strength Index (RSI) (14) has been failing in climbing above the 60.00 level decisively, indicating missing upside momentum in the Loonie asset.

However, the 20-period Exponential Moving Average (EMA) at 1.3509 is continuously providing cushion to the US Dollar.

-

07:00

Japan Eco Watchers Survey: Outlook came in at 54.1, above forecasts (50.2) in March

-

07:00

Japan Eco Watchers Survey: Current registered at 53.3 above expectations (50.4) in March

-

06:42

WTI crude oil floats above $80.00 as US Dollar rebound jostles with supply crunch fears

- WTI remains sidelined inside a four-day-old trading range, retreats of late.

- Fears emanating from OPEC+ supply cuts, geopolitical fears underpin Oil price strength.

- US Dollar traces recently firmer odds of Fed’s 0.25% rate hike in May after upbeat US NFP.

- Risk catalysts, US inflation and Fed Minutes eyed for clear directions.

WTI crude oil buyers struggle to keep the reins around $80.70 during early Monday as risk-aversion joins hawkish Fed bets to underpin the US Dollar rebound. However, challenges to Oil supplies, mainly emanating from China and OPEC+, seem to keep the black gold buyers hopeful.

US Dollar Index (DXY) snaps a four-day downtrend around 102.25 even as the US Treasury bond yields fail to recover amid recession woes. That said, the US 10-year and two-year Treasury bond yields remain pressured near 3.37% and 3.95% respectively. In doing so, the benchmark bond coupons extend the previous day’s losses and portray the market’s rush toward the risk-safety amid economic slowdown fears.

That said, the recently downbeat US data renew fears of a recession in the world’s largest economy and challenge the energy optimists. However, the upbeat prints of the US Nonfarm Payrolls (NFP) allowed the Fed hawks to return to the table and new calls for the 0.25% rate hike in May. The same puts a floor under the US Dollar prices and prods WTI crude oil buyers.

On the other hand, geopolitical fears surrounding China, mainly after the dragon nation’s military drills near Taiwan, join the last week’s surprise OPEC+ output cut to keep the Oil buyers hopeful.

Elsewhere, China’s readiness to defend the global economy via strong monetary and fiscal easing at home also allows the Oil buyers to remain hopeful amid optimism at the world’s biggest Oil consumers.

Moving on, the Easter Monday holidays in spot markets may restrict Oil moves but the bulls appear to run out of fuel and hence US inflation and Fed Minutes will be watched carefully for the signals of a pullback.

Technical analysis

Despite the latest inaction, the WTI crude oil remains firmer past the 100-DMA support near $76.80. However, a downward-sloping resistance line from December 2022, around $81.70, appears a tough nut to crack for the WTI crude oil buyers.

-

06:14

USD/CHF Price Analysis: Pares recent losses, stays on bear’s radar unless crossing 0.9160

- USD/CHF picks up bids to refresh intraday high, extend previous week’s rebound from 22-month low.

- Bullish MACD signals allow USD/CHF to consolidate recent losses but March’s low guards immediate upside.

- Multiple resistance lines, 100-SMA stand tall to challenge USD/CHF bulls.

- Sellers need validation from 0.9035 to aim for fresh multi-month low.

USD/CHF renews its intraday high near 0.9065 during early Easter Monday in Europe. In doing so, the Swiss Franc (CHF) pair extends the previous day’s recovery from a 22-month low while approaching a one-month-old support-turned-resistance surrounding 0.9075.

It’s worth noting that the bullish MACD signals join the corrective bounce off the multi-day low to lure USD/CHF buyers as they approach the previous support near 0.9075.

Even if the quote manages to stay firmer past 0.9075, downward-sloping resistance lines from March 26 and 15, respectively near 0.9095 and 0.9145, can check the USD/CHF buyers.

Even so, the Swiss currency pair buyers need to portray a successful upside break of the 100-bar Simple Moving Average (SMA), around 0.9160, to please the USD/CHF buyers.

Following that, 0.9225 and a late March swing high of around 0.9345 will be in focus.

On the flip side, multiple lows around 0.9035-30 can test the USD/CHF bears before recalling them to the driver’s seat. However, the 0.9000 psychological magnet may challenge the sellers afterward.

In a case where USD/CHF remains bearish past 0.9000, June 2021 low near 0.8925 may lure the sellers.

USD/CHF: Four-hour chart

Trend: Limited recovery expected

-

06:08

USD/MXN Price Analysis: Downside looks solid below 18.10 as USD Index loses upside momentum

- USD/MXN is eyeing more weakness below 18.10 as USD Index has witnessed exhaustion in the upside momentum.

- The USD Index is struggling to expand gains further as investors are ignoring volatility ahead of US inflation data.

- USD/MXN is expected to continue further downside amid Darvas Box formation.

The USD/MXN pair has gauged an intermediate cushion after a sheer downside around 18.10 in the Asian session. The asset is hovering near the aforementioned support but is likely to face selling pressure as the US Dollar Index (DXY) has witnessed exhaustion in its upside journey.

The USD Index is struggling to expand gains further as investors are ignoring volatility ahead of US inflation data. Topsy-turvy moves are expected from the USD Index as the US inflation is expected to display some surprises.