Notícias do Mercado

-

23:32

Commodities. Daily history for Dec 17’2014:

(raw materials / closing price /% change)

Light Crude 55.81 -1.17%

Gold 1,189.70 -0.40%

-

23:31

Currencies. Daily history for Dec 17’2014:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,2341 -1,37%

GBP/USD $1,5573 -1,14%

USD/CHF Chf0,9728 +1,35%

USD/JPY Y118,65 +1,90%

EUR/JPY Y146,41 +0,53%

GBP/JPY Y184,74 +0,78%

AUD/USD $0,8120 -1,19%

NZD/USD $0,7703 -1,21%

USD/CAD C$1,1632 +0,07%

-

23:31

Stocks. Daily history for Dec 17’2014:

(index / closing price / change items /% change)

Nikkei 225 16,819.73 +64.41 +0.38%

Hang Seng 22,585.84 -84.66 -0.37%

Shanghai Composite 3,061.02 +39.50 +1.31%

FTSE 100 6,336.48 +4.65 +0.07%

CAC 40 4,111.91 +18.71 +0.46%

Xetra DAX 9,544.43 -19.46 -0.20%

S&P 500 2,012.89 +40.15 +2.04%

NASDAQ Composite 4,644.31 +96.48 +2.12%

Dow Jones 17,356.87 +288.00 +1.69%

-

23:00

Schedule for today, Thursday, Dec 18’2014:

(time / country / index / period / previous value / forecast)

00:30 Australia RBA Bulletin

06:45 Switzerland SECO Economic Forecasts

07:00 Switzerland Trade Balance November 3.23 2.41

09:00 Eurozone EU Economic Summit

09:00 Germany IFO - Business Climate December 104.7 105.6

09:00 Germany IFO - Current Assessment December 110.0 110.3

09:00 Germany IFO - Expectations December 99.7 100.9

09:30 United Kingdom Retail Sales (MoM) November +0.8% +0.3%

09:30 United Kingdom Retail Sales (YoY) November +4.3% +4.5%

13:30 U.S. Initial Jobless Claims December 294 297

14:45 U.S. Services PMI (Preliminary) December 56.2 57.1

15:00 U.S. Leading Indicators November +0.9% +0.6%

15:00 U.S. Philadelphia Fed Manufacturing Survey December 40.8 26.3

21:45 New Zealand Visitor Arrivals November +3.3%

-

20:00

Dow +223.83 17,292.70 +1.31% Nasdaq +73.79 4,621.62 +1.62% S&P +29.24 2,001.98 +1.48%

-

19:00

U.S.: Fed Interest Rate Decision , 0.25% (forecast 0.25%)

-

17:32

The ECB board member Benoit Coeure said the sovereign bond purchases are the "baseline option".

-

17:08

European stocks close: most stocks closed slightly higher on higher energy and mining stocks

Most stock indices closed slightly higher on higher energy and mining stocks.

Investors are awaiting a parliamentary vote for president. The Greek presidency candidate is Stavros Dimas. There are three possible votes in parliament. If the candidate isn't elected in three possible votes, the parliament will be dissolved.

The Fed's interest rate decision is also expected. Investors expect that the Fed will keep its low interest rate for a longer period. They are awaiting new signs for further monetary policy in the U.S.

Eurozone's consumer price index dropped 0.2% in November, in line with expectations, after a flat reading in October.

On a yearly basis, Eurozone's consumer price inflation remained unchanged at 0.3% in November, in line with expectations.

Eurozone's consumer price inflation excluding food, energy, alcohol and tobacco remained unchanged at an annual rate of 0.7% in November, in line with expectations.

Indexes on the close:

Name Price Change Change %

FTSE 100 6,336.48 +4.65 +0.07%

DAX 9,544.43 -19.46 -0.20%

CAC 40 4,111.91 +18.71 +0.46%

-

17:00

European stocks closed: FTSE 100 6,336.48 +4.65 +0.07% CAC 40 4,111.91 +18.71 +0.46% DAX 9,544.43 -19.46 -0.20%

-

16:41

Foreign exchange market. American session: the U.S. dollar traded mixed to higher against the most major currencies ahead of the Fed's interest rate decision

The U.S. dollar traded mixed to higher against the most major currencies ahead of the Fed's interest rate decision. Investors expect that the Fed will keep its low interest rate for a longer period. They are awaiting new signs for further monetary policy in the U.S.

The U.S. consumer price inflation fell 0.3% in November, missing expectations for a 0.1% decrease, after a flat reading in October. That was largest decline since December 2008.

The declines was driven by lower gas prices. Gas prices slid 10.5% in November, the largest decline in nearly six years.

On a yearly basis, the U.S. consumer price index fell to 1.3% in November from 1.7% in October.

The U.S. consumer price inflation excluding food and energy climbed 0.1% in November, in line with expectations, after a 0.2% rise in October.

On a yearly basis, the U.S. consumer price index excluding food and energy decreased to 1.7% in November from a

The euro traded lower against the U.S. dollar. Eurozone's consumer price index dropped 0.2% in November, in line with expectations, after a flat reading in October.

On a yearly basis, Eurozone's consumer price inflation remained unchanged at 0.3% in November, in line with expectations.

Eurozone's consumer price inflation excluding food, energy, alcohol and tobacco remained unchanged at an annual rate of 0.7% in November, in line with expectations.

The British pound traded lower against the U.S. dollar despite the solid labour market data from the U.K. The U.K. unemployment rate remained uncaged at 6.0% in the August to October quarter, missing expectations for a decline to 5.9%.

The claimant count decreased by 26,900 people in November, exceeding expectations for a drop of 19,800 people, after a decrease of 25,100 people in October. October's figure was revised from a decline of 20,400.

Average weekly earnings, excluding bonuses, climbed by 1.6% in the August to October period, in line with expectations, up from a revised 1.2% rise in the previous three months.

Average weekly earnings, including bonuses, rose by 1.4% in the August to October period, beating expectations for a gain to 1.3%, after a 1.0% increase in the previous three months.

That was the first time for six years that earnings growth (both measures) has exceeded the inflation rate. The U.K. consumer price index declined to an annual rate of 1.0% in November from 1.3% in October.

The Bank of England (BoE) released its last meeting minutes. The BoE kept its monetary policy unchanged. Two members, Ian McCafferty and Martin Weale, voted for the fifth consecutive month to raise interest rates to 0.75% from 0.5%. The MPC members want to see further increases in wage growth before to raise interest rates.

The Canadian dollar traded mixed against the U.S. dollar after the weaker-than-expected Canadian wholesale sales. Wholesale sales increased 0.1% in October, missing expectations for a 0.9% gain, after a 1.8% rise in September.

The Swiss franc traded lower against the U.S. dollar. A survey by the ZEW Institute and Credit Suisse Group showed today that Switzerland's economic sentiment index rose to -4.9 points in December from -7.6 points in November.

The Swiss National Bank (SNB) released its quarterly bulletin on Wednesday. The SNB said that it will keep the exchange rate floor unchanged at 1.20 francs per euro. Switzerland's noted that deflation risks have increased that the Swiss franc is still high.

The New Zealand dollar traded lower against the U.S. dollar. In the overnight trading session, the kiwi declined against the greenback due after the current account data from New Zealand. New Zealand's current account deficit widened to NZ$5.01 billion in the third quarter from a deficit of NZ$1.08 billion in the second quarter. The second quarter's figure was revised down to a deficit of NZ$1.07 billion. Analysts had expected the current account deficit of NZ$5.32 billion.

The Australian dollar traded lower against the U.S. dollar. In the overnight trading session, the Aussie dropped against the greenback. The leading index for Australia fell 0.1% in November, down from a 0.1% rise in October. October's figure revised up from a flat reading.

The Japanese yen traded lower against the U.S. dollar in the absence of any major economic reports from Japan.

-

16:40

Oil: a review of the market situation

Oil prices rose moderately, departing from the five-year minimum, which was due to speculation that the recent drop is excessive.

Recall oil fell by almost half since June under pressure from concerns about forecasts slow recovery in global demand and oversupply of stocks. Last Friday, the International Energy Agency cut its forecast for global oil demand next year by 230,000 barrels per day to 900,000 barrels after similar cuts by OPEC and the Office of information in the field of Energy.

On the dynamics of trade have also influenced today's data on oil reserves in the United States. The Department of Energy said that the oil reserves in the US stores this week 6-12 December fell by 847,000 barrels to 379.9 million barrels, while the average forecast assumes a decrease of 1.9 million barrels. Gasoline inventories rose by 5.3 million barrels to 222 million barrels, the highest since March 14. Analysts had expected gasoline inventories increase compared to the previous week total of 2 million barrels. Distillate stocks fell by 207,000 barrels to 121.5 million barrels, while analysts had expected an increase of 1 million barrels. Utilization rate of refining capacity fell by 1.9 percentage points to 93.5%. Analysts expected a decrease of 0.1 percentage points. It is worth emphasizing that yesterday's report of the American Petroleum Institute showed an unexpected increase in US oil inventories to 1900000 barrels last week.

Market participants also drew attention to US CPI data. As it became known, the seasonally-weighted index of prices to consumers fell by 0.3% in November and increased by 1.3% per annum. As expected, the main driver of the decline in consumer prices was the drop in oil prices, the price index for gasoline fell to the lowest since December 2008 value. Indices of fuel and natural gas also showed decline, and the index of energy decreased by 3.8%.

In the center of attention - the announcement of the Fed's decision on interest rates. The Fed could delete the phrase about saving rates near zero "for an extended period of time," that would be a step toward raising rates in the middle of next year.

Cost of January futures for US light crude oil WTI (Light Sweet Crude Oil) rose to 56.48 dollars per barrel on the New York Mercantile Exchange.

January futures price for North Sea petroleum mix of Brent increased by $ 1.09 to $ 60.88 a barrel on the London Stock Exchange ICE Futures Europe.

-

16:20

Gold: a review of the market situation

Gold prices fell slightly, while entrenched below $ 1,200 per ounce, which is associated with the expectations of this year's last meeting of the Federal Reserve System. Little influenced by US data showing that the consumer price index fell to a seasonally adjusted 0.3% in October. This marked the largest monthly fall since December 2008, when the US was in a recession. Excluding food and energy, the so-called "core" prices rose by 0.1%. Economists had predicted a drop of 0.1% of the total price and the increase in basic prices by 0.1%. Compared with a year earlier, as a whole, prices rose by 1.3% in November and the basic prices rose by 1.7%. The Federal Reserve is focused on the annual inflation rate of 2%, as a sign of healthy economic growth and price stability. She prefers a separate measure, calculated the Ministry of Trade, which also shows that inflation remains below that purpose.

Investors remained cautious ahead of Fed statement after the constant speculation about the prospect of a rate hike in the US next year, raised expectations that the bank may change its forecast and mitigate the promise to keep interest rates near zero for "an extended period". In recent years, commodity markets benefit from a program of monetary easing by the Fed, on the other hand, are under pressure if the bank tightens its policy.

Pressure on prices had a significant drop in the ruble, which has led to speculation about the sale of the Central Bank of Russia's gold reserves. In this scenario, we can expect a significant drop in prices, in view of what we want to buy it at the existing levels, while a little.

Demand for physical gold in Asia remained weak as traders waited for the announcement of the results of the Fed meeting.

It also became known that the stocks of the world's largest gold exchange-traded fund SPDR Gold Trust fell at the end of Tuesday's 1.8 tons.

The cost of the December gold futures on the COMEX today fell to 1197.60 dollars per ounce.

-

15:54

Swiss National Bank’s Quarterly Bulletin: deflation risks have increased that the Swiss franc is still high

The Swiss National Bank (SNB) released its quarterly bulletin on Wednesday. The SNB said that it will keep the exchange rate floor unchanged at 1.20 francs per euro. Switzerland's noted that deflation risks have increased that the Swiss franc is still high.

Inflation forecast was revised down to 0.0% in 2014, to -0.1% in 2015 and to 0.3% in 2016. Falling oil prices weigh on inflation, so the central bank.

The SNB expects a moderate economic growth in the fourth quarter of 2014, driven by the services sector.

-

15:30

U.S.: Crude Oil Inventories, December -0.8

-

15:07

Canada’s wholesale sales climbed 0.1% in October

Statistics Canada released wholesale sales figures on Wednesday. Wholesale sales increased 0.1% in October, missing expectations for a 0.9% gain, after a 1.8% rise in September.

Lower sales volume weighed on wholesale sales. Sales volume declined 0.1% in October.

Building material and supplies rose 0.4%. Machinery, equipment and supplies climbed 0.4%.

-

14:47

U.S. consumer price inflation dropped 0.3% in November

The U.S. Labor Department released consumer price inflation data today. The U.S. consumer price inflation fell 0.3% in November, missing expectations for a 0.1% decrease, after a flat reading in October. That was largest decline since December 2008.

The declines was driven by lower gas prices. Gas prices slid 10.5% in November, the largest decline in nearly six years.

On a yearly basis, the U.S. consumer price index fell to 1.3% in November from 1.7% in October.

The U.S. consumer price inflation excluding food and energy climbed 0.1% in November, in line with expectations, after a 0.2% rise in October.

On a yearly basis, the U.S. consumer price index excluding food and energy decreased to 1.7% in November from a 1.8% gain in October.

Energy costs dropped 3.8% in November.

Gasoline prices declined 6.6% in November, while food prices rose 0.2%.

-

14:34

U.S. Stocks open: Dow 17,088.81 +19.94 +0.12%, Nasdaq 4,554.66 +6.83 +0.15%, S&P 1,974.99 +2.25 +0.11%

-

14:22

Before the bell: S&P futures +0.55%, Nasdaq futures +0.51%

U.S. stock futures advanced amid speculation the Federal Reserve will remain supportive of the economy even as policy makers gear up for an interest-rate increase.

Global markets:

FTSE 6,283.29 -48.54 -0.77%

CAC 4,063.69 -29.51 -0.72%

DAX 9,482.33 -81.56 -0.85%

Nikkei 16,819.73 +64.41 +0.38%

Hang Seng 22,585.84 -84.66 -0.37%

Shanghai Composite 3,060.26 +38.75 +1.28%

Crude oil $54.47 (-2.59%)

Gold $1196.70 (+0.18%)

-

14:07

Bank of England's Monetary Policy Committee minutes: further increases in wage growth needed before raising interest rate

The Bank of England's Monetary Policy Committee (MPC) released its latest minutes today. Two members, Ian McCafferty and Martin Weale, voted for the fifth consecutive month to raise interest rates to 0.75% from 0.5%.

Seven of the nine MPC members voted to keep interest rate at 0.5%.

The MPC members want to see further increases in wage growth before to raise interest rates.

The BoE expects that inflation will decline below 1% due to falling oil and food prices.

-

14:02

DOW components before the bell

(company / ticker / price / change, % / volume)

Cisco Systems Inc

CSCO

26.59

+0.02%

0.3K

Johnson & Johnson

JNJ

102.93

+0.17%

0.2K

International Business Machines Co...

IBM

151.81

+0.26%

0.7K

Exxon Mobil Corp

XOM

86.70

+0.34%

24.4K

Pfizer Inc

PFE

30.78

+0.36%

0.7K

Intel Corp

INTC

35.75

+0.53%

0.7K

Home Depot Inc

HD

97.60

+0.56%

0.9K

JPMorgan Chase and Co

JPM

58.77

+0.58%

0.5K

Microsoft Corp

MSFT

45.42

+0.58%

8.8K

General Electric Co

GE

24.67

+0.73%

12.7K

Procter & Gamble Co

PG

90.02

+0.74%

0.2K

McDonald's Corp

MCD

88.72

0.00%

0.1K

Verizon Communications Inc

VZ

45.35

-0.40%

28.6K

-

13:58

Upgrades and downgrades before the market open

Upgrades:

Twitter (TWTR) upgraded to Buy from Hold at Pivotal Research Group, target $42

Google (GOOG) upgraded to Buy from Hold at Pivotal Research Group, target $610

Downgrades:

Verizon (VZ) downgraded to Neutral from Buy at Goldman, target lowered to $48 from $55

Other:

General Electric (GE) target lowered to $28 from $30 at RBC Capital Mkts

American Express (AXP) initiated with a Overweight at Morgan Stanley, target $110

3M (MMM) target raised to $190 from $164 at BofA/Merrill

-

13:50

Option expiries for today's 10:00 ET NY cut

EUR/USD: $1.2400(E750mn), $1.2450(E700mn), $1.2500(E2.7bn), $1.2575(E1.1bn), $1.2600(E1.3bn)

USD/JPY: Y115.00($500mn), Y116.20-25($600mn), Y116.50($1.6bn), Y116.75($410mn), Y117.00($603mn), Y117.20($560mn), Y118.25($1.4bn), Y119.50($4.8bn)

GBP/USD: $1.5630(gbp260mn)

EUR/GBP: stg0.7800(E308mn), stg0.7975(E230mn)

USD/CHF: Chf0.9390($550mn), Chf0.9500

AUD/USD: $0.8300(A$265mn)

USD/CAD: C$1.1400($1.0bn), C$1.1600($1.5bn)

-

13:31

U.S.: CPI excluding food and energy, Y/Y, November +1.7%

-

13:31

Canada: Wholesale Sales, m/m, October +0.1% (forecast +0.9%)

-

13:31

U.S.: Current account, bln, Quarter III -100 (forecast -98)

-

13:30

U.S.: CPI, m/m , November -0.3% (forecast -0.1%)

-

13:30

U.S.: CPI excluding food and energy, m/m, November +0.1% (forecast +0.1%)

-

13:30

U.S.: CPI, Y/Y, November +1.3%

-

13:05

Foreign exchange market. European session: the euro declined against the U.S. dollar after the consumer inflation data from the Eurozone

Economic calendar (GMT0):

(Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual)

09:30 United Kingdom Average Earnings, 3m/y October +1.0% +1.3% +1.4%

09:30 United Kingdom Average earnings ex bonuses, 3 m/y October +1.2% +1.6% +1.6%

09:30 United Kingdom ILO Unemployment Rate October 6.0% 5.9% 6.0%

09:30 United Kingdom Claimant count November -25.1 Revised From -20.4 -19.8 -26.9

09:30 United Kingdom Claimant Count Rate October 2.8% 2.7%

09:30 United Kingdom Bank of England Minutes

10:00 Eurozone Harmonized CPI November 0.0% -0.2% -0.2%

10:00 Eurozone Harmonized CPI, Y/Y (Finally) November +0.3% +0.3% +0.3%

10:00 Eurozone Harmonized CPI ex EFAT, Y/Y November +0.7% +0.7% +0.7%

10:00 Switzerland Credit Suisse ZEW Survey (Expectations) December -7.6 -4.9

The U.S. dollar traded mixed against the most major currencies ahead of the U.S. consumer inflation data and Fed's interest rate decision. The U.S. consumer price inflation is expected to decline 0.1% in November, after a flat reading in October.

The U.S. consumer price index excluding food and energy is expected to rise 0.1% in November, after a 0.2% gain in October.

The Fed will release its interest rate decision. Investors expect that the Fed will keep its low interest rate for a longer period. They are awaiting new signs for further monetary policy in the U.S.

The euro declined against the U.S. dollar after the consumer inflation data from the Eurozone. Eurozone's consumer price index dropped 0.2% in November, in line with expectations, after a flat reading in October.

On a yearly basis, Eurozone's consumer price inflation remained unchanged at 0.3% in November, in line with expectations.

Eurozone's consumer price inflation excluding food, energy, alcohol and tobacco remained unchanged at an annual rate of 0.7% in November, in line with expectations.

The British pound traded mixed against the U.S. dollar after the solid labour market data from the U.K. The U.K. unemployment rate remained uncaged at 6.0% in the August to October quarter, missing expectations for a decline to 5.9%.

The claimant count decreased by 26,900 people in November, exceeding expectations for a drop of 19,800 people, after a decrease of 25,100 people in October. October's figure was revised from a decline of 20,400.

Average weekly earnings, excluding bonuses, climbed by 1.6% in the August to October period, in line with expectations, up from a revised 1.2% rise in the previous three months.

Average weekly earnings, including bonuses, rose by 1.4% in the August to October period, beating expectations for a gain to 1.3%, after a 1.0% increase in the previous three months.

That was the first time for six years that earnings growth (both measures) has exceeded the inflation rate. The U.K. consumer price index declined to an annual rate of 1.0% in November from 1.3% in October.

The Bank of England (BoE) released its last meeting minutes. The BoE kept its monetary policy unchanged. Two members, Ian McCafferty and Martin Weale, voted for the fifth consecutive month to raise interest rates to 0.75% from 0.5%. The MPC members want to see further increases in wage growth before to raise interest rates.

The Canadian dollar traded mixed against the U.S. dollar ahead of the Canadian wholesale sales. Wholesale sales in Canada are expected to climb 0.9% in October, after a 1.8% rise in September.

The Swiss franc traded lower against the U.S. dollar despite the positive survey by the ZEW Institute and Credit Suisse Group. A survey by the ZEW Institute and Credit Suisse Group showed today that Switzerland's economic sentiment index rose to -4.9 points in December from -7.6 points in November.

EUR/USD: the currency pair fell to $1.2445

GBP/USD: the currency pair traded mixed

USD/JPY: the currency pair traded mixed

The most important news that are expected (GMT0):

13:30 Canada Wholesale Sales, m/m October +1.8% +0.9%

13:30 U.S. Current account, bln Quarter III -99 -98

13:30 U.S. CPI, m/m November 0.0% -0.1%

13:30 U.S. CPI, Y/Y November +1.7%

13:30 U.S. CPI excluding food and energy, m/m November +0.2% +0.1%

13:30 U.S. CPI excluding food and energy, Y/Y November +1.8%

14:00 Switzerland SNB Quarterly Bulletin

19:00 U.S. FOMC Economic Projections

19:00 U.S. FOMC Statement

19:00 U.S. Fed Interest Rate Decision 0.25% 0.25%

19:30 U.S. Federal Reserve Press Conference

21:45 New Zealand GDP q/q Quarter III +0.7% +0.7%

21:45 New Zealand GDP q/q Quarter III +3.9% +3.3%

-

12:50

Orders

EUR/USD

Offers $1.2600, $1.2550

Bids $1.2445/40, $1.2415/10, $1.2385-80

GBP/USD

Offers $1.5800, $1.5785

Bids $1.5650, $1.5600

AUD/USD

Offers $0.8250, $0.8200

Bids $0.8100, $0.8050, $0.8000

EUR/JPY

Offers Y147.80, Y147.50, Y146.80/00, Y146.50

Bids Y145.50, Y145.25/20, Y145.00, Y144.50

USD/JPY

Offers Y118.50, Y117.80/00

Bids Y117.00, Y116.50, Y116.05/00, Y115.50

EUR/GBP

Offers stg0.8066, stg0.8020

Bids stg0.7800

-

12:33

UK unemployment rate remained uncaged at 6.0% in the August to October quarter

The Office for National Statistics released the labour market data today. The U.K. unemployment rate remained uncaged at 6.0% in the August to October quarter, missing expectations for a decline to 5.9%.

The claimant count decreased by 26,900 people in November, exceeding expectations for a drop of 19,800 people, after a decrease of 25,100 people in October. October's figure was revised from a decline of 20,400.

Average weekly earnings, excluding bonuses, climbed by 1.6% in the August to October period, in line with expectations, up from a revised 1.2% rise in the previous three months.

Average weekly earnings, including bonuses, rose by 1.4% in the August to October period, beating expectations for a gain to 1.3%, after a 1.0% increase in the previous three months.

That was the first time for six years that earnings growth (both measures) has exceeded the inflation rate. The U.K. consumer price index declined to an annual rate of 1.0% in November from 1.3% in October.

-

12:00

European stock markets mid-session: European indices are trading lower before FED rate decision

In today's session the FTSE 100 index lost -0.73% quoted at 6,285.30 points, France's CAC 40 declined -0.45% trading at 4,074.77. Germany's DAX 30 is down -0.65% at 9,501.71 points.

The relentless drop in oil prices quoted near five-year lows and Russia's financial crisis weigh on European stocks. Investors are also focusing on developments in Greece where a parliamentary vote for president is scheduled for today. The Greek presidency candidate is Stavros Dimas. There are three possible votes in parliament. If the candidate isn't elected in three possible votes, the parliament will be dissolved.

Data on Eurozone's CPI was in line with expectations with a reading of -0.2% for November. Inflation is now at +0.3% on a yearly basis, far below the ECB's target of 2%. Now all eyes are on the FOMC meeting and the FED's interest rate decision due 19:00 GMT and U.S. CPI due 13:30 GMT.

-

11:20

Oil: prices decline after yesterday’s gains

Brent crude and West Texas Intermediate are trading lower today. Brent Crude lost -0.75%, currently trading at USD59.56 a barrel. Crude slipped below the 60 dollar mark yesterday, its lowest since May 2009. West Texas Intermediate declined -1.41% currently quoted at USD55.14, close to its five-year low. Neither Russia nor the OPEC are going to reduce output as reaction to falling prices and a supply glut as they are fighting for market shares and keeping the pressure on U.S. shale drillers. Market participants are now awaiting the FED's rate decision and key economic U.S. data later in the day.

-

11:00

Gold prices slightly recover after yesterday’s volatile trading

Gold further recovered and is currently trading just below the important key level of USD1,200 at USD1,197.60 a troy ounce quoted +0,10%. Market participants are awaiting the result of the FED's two-day meeting today to assess the timing of a benchmark interest rate hike. Talk about the fact that the central bank may abandon his former statement, which said that rates will remain near zero "for an extended period of time," on Wednesday, supported the US dollar and damaged precious metals in recent days. Gold, which does not bring interest income, can hardly compete with the assets generating interest income when interest rates rise. A stronger U.S. dollar makes gold more expensive to buy for holders of other currencies. Falling oil prices at five-year lows and potential Russian bullion sales to stabilize the slumping ruble weigh on the precious metal.

GOLD currently trading at USD1,197.60

-

10:20

Option expiries for today's 10:00 ET NY cut

EUR/USD: $1.2400(E750mn), $1.2450(E700mn), $1.2500(E2.7bn), $1.2575(E1.1bn), $1.2600(E1.3bn)

USD/JPY: Y115.00($500mn), Y116.20-25($600mn), Y116.50($1.6bn), Y116.75($410mn), Y117.00($603mn), Y117.20($560mn), Y118.25($1.4bn), Y119.50($4.8bn)

GBP/USD: $1.5630(gbp260mn)

EUR/GBP: stg0.7800(E308mn), stg0.7975(E230mn)

USD/CHF: Chf0.9390($550mn), Chf0.9500

AUD/USD: $0.8300(A$265mn)

USD/CAD: C$1.1400($1.0bn), C$1.1600($1.5bn)

-

10:01

Switzerland: Credit Suisse ZEW Survey (Expectations), December -4.9

-

10:00

Eurozone: Harmonized CPI ex EFAT, Y/Y, November +0.7% (forecast +0.7%)

-

10:00

Eurozone: Harmonized CPI, November -0.2% (forecast -0.2%)

-

10:00

Eurozone: Harmonized CPI, Y/Y, November +0.3% (forecast +0.3%)

-

09:31

United Kingdom: Claimant count , November -26.9 (forecast -19.8)

-

09:31

United Kingdom: Average Earnings, 3m/y , October +1.4% (forecast +1.3%)

-

09:31

United Kingdom: Average earnings ex bonuses, 3 m/y, October +1.6% (forecast +1.6%)

-

09:31

United Kingdom: Claimant Count Rate, October 2.7%

-

09:30

United Kingdom: ILO Unemployment Rate, October 6.0% (forecast 5.9%)

-

09:23

Press Review: Fed Won’t Stop Gold’s Recovery in ‘15, ANZ Says as Asia Buys

MARKETWATCH

What Wall Street's big-money managers predict for 2015

Buy Japan. Buy Europe. Buy technology. Avoid energy. Avoid Russia.

That's what the Big Money is saying as we get ready for the new year. This is according to the latest in-depth survey of institutional money managers conducted by Bank of America Merrill Lynch. In total, the poll-takers interviewed over 150 professional investment managers around the world with nearly $450 billion in assets under management.

Source:

BLOOMBERG

Fed Won't Stop Gold's Recovery in '15, ANZ Says as Asia Buys

Gold prices will recover next year as demand in China and India improves, according to Australia & New Zealand Banking Group Ltd., which forecast an advance for bullion even as the Federal Reserve raises interest rates.

BBC

Rouble regains ground as trading remains nervous

Russia's rouble has regained ground from Tuesday's all-time low, although trading remains edgy and volatile.

It opened 4% lower on Wednesday, but edged up. In early trading, one US dollar bought 66 roubles, far fewer than the record low of 79 on Tuesday.

Source:

BUSINESSSPECTATOR

Oil prices skid ahead of Fed meeting

US oil prices resumed their downward slide in Asian trade on Wednesday, and Brent crude stayed below the key $US60 mark, as markets braced for the outcome of the US Federal Reserve meeting later in the day.

The market expects the Fed to change some of the language in its policy statement, when it concludes its two-day meeting, to signal that a rate hike is likely in mid-2015. Commodity markets, which have benefited from the easing of US monetary policy in the last few years, could come under pressure if the Fed tightens its stance. Analysts also expect an upward revision to US GDP growth forecasts in response to the slump in oil prices.

Source: https://www.businessspectator.com.au/news/2014/12/17/markets/oil-prices-skid-ahead-fed-meeting

-

09:11

European Stocks. First hour: stocks declined at the start

European stock indices declined at the start. UK's FTSE 100 index was down 0.57% to 6,295.82 points. Germany's DAX 30 fell 0.63% to 9,503.38 points, while France's CAC 40 decreased 0.40% to 4,076.97.

Lower energy and mining stocks weighed on markets.

Investors are awaiting the Fed' interest rate decision today. They expects new signs for further monetary policy.

The Greek parliament will elect a Greek president today. The Greek presidency candidate is Stavros Dimas. There are three possible votes in parliament. If the candidate isn't elected in three possible votes, the parliament will be dissolved.

-

08:00

Global Stocks: U.S indices trading lower, Asian indices book gains

U.S. markets were trading lower on Tuesday in a volatile session. The DOW JONES lost -0.65% shedding early gains closing at 17,068.87 points, the S&P 500 declined -0.85% as technology shares slumped, with a final quote of 1,972.74 points. Indices were weighed down by weak U.S. economic data as the U.S. preliminary manufacturing purchasing managers' index (PMI) fell to 53.7 in December from 55.8 in November, missing expectations for a rise to 56.1. That was the lowest level since January 2014. Soft U.S. housing data added to the concerns. Markets now await data on consumer inflation, the current account and the FED's interest rate decision.

Chinese stocks added gains while trading in Hong Kong was negative. Hong Kong's Hang Seng is trading -0.22% at 22,620.70. China's Shanghai Composite closed at 3,060.26 points, a gain of +1.28%.

Japan's Nikkei added +0.38% closing at 16,819.73 moving away from a 6-1/2 week low. Japanese exports rose less than analysts predicted in November whereas imports unexpectedly decreased.

-

07:30

Foreign exchange market. Asian session: U.S. dollar trading broadly stronger before FED

The greenback traded stronger against its major peers as the two day policy meeting of the FED started yesterday. U.S. policy makers could open the door for an interest rate hike in the middle of next year dropping its "considerable time" guidance from its minutes. Markets await data on U.S. CPI and the Current Account at 13:30 GMT and later in the session the FED's Interest Rate Decision and FOMC press conference.

The Australian dollar slumped and hit a new four year low. Yesterday the Reserve Bank of Australia (RBA) released its minutes from December's monetary policy meeting on Tuesday. The RBA said that gross domestic product growth will be below trend over 2014/15, but will pick up towards the end of 2016. The RBA noted that "very low interest rates had supported activity in the housing market". The central bank said that "subdued labour market conditions were likely to weigh on consumption growth and consumer confidence more generally". The RBA members pointed out that "further exchange rate depreciation was likely to be needed to achieve balanced growth in the economy". They noted that monetary policy easing is possible during 2015. Australia's central bank reiterated that "the most prudent course was likely to be a period of stability in interest rates". The Westpac Leading Index had a negative reading of -0.1% compared with +0.1% in October.

New Zealand's dollar traded negative against the greenback. New Zealand's Current Account for the third quarter was better than expected with a reading of -5.01 compared to forecasts of -5.32. Markets await data on GDP for the third quarter being published late in the day at 21:45 GMT.

The Japanese yen weakened in Asian trade retreating from a 1-month high despite a better-than-expected Merchandise Trade Balance with a reading of -925.0, compared to forecasts of -990.0. In previous sessions the Japanese currency was supported by weak economic data making the yen an attractive safe haven.

EUR/USD: the euro lost against the greenback

USD/JPY: the U.S. dollar traded stronger against the yen

GPB/USD: The British pound traded lost against the U.S. dollar

The most important news that are expected (GMT0):

(time / country / index / period / previous value / forecast)

09:30 United Kingdom Average Earnings, 3m/y October +1.0% +1.3%

09:30 United Kingdom Average earnings ex bonuses, 3 m/y October +1.3% +1.6%

09:30 United Kingdom ILO Unemployment Rate October 6.0% 5.9%

09:30 United Kingdom Claimant count November -20.4 -19.8

09:30 United Kingdom Claimant Count Rate October 2.8%

09:30 United Kingdom Bank of England Minutes

10:00 Eurozone Harmonized CPI November 0.0% -0.2%

10:00 Eurozone Harmonized CPI, Y/Y (Finally) November +0.3% +0.3%

10:00 Eurozone Harmonized CPI ex EFAT, Y/Y November +0.7% +0.7%

10:00 Switzerland Credit Suisse ZEW Survey (Expectations) December -7.6

13:30 Canada Wholesale Sales, m/m October +1.8% +0.9%

13:30 U.S. Current account, bln Quarter III -99 -98

13:30 U.S. CPI, m/m November 0.0% -0.1%

13:30 U.S. CPI, Y/Y November +1.7%

13:30 U.S. CPI excluding food and energy, m/m November +0.2% +0.1%

13:30 U.S. CPI excluding food and energy, Y/Y November +1.8%

14:00 Switzerland SNB Quarterly Bulletin

15:30 U.S. Crude Oil Inventories December +1.5

19:00 U.S. FOMC Economic Projections

19:00 U.S. FOMC Statement

19:00 U.S. Fed Interest Rate Decision 0.25% 0.25%

19:30 U.S. Federal Reserve Press Conference

21:45 New Zealand GDP q/q Quarter III +0.7% +0.7%

21:45 New Zealand GDP q/q Quarter III +3.9% +3.3%

-

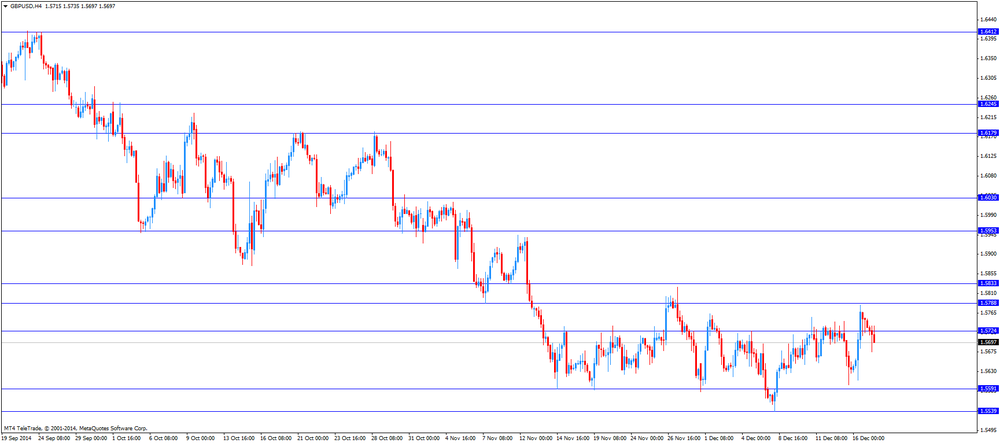

06:29

Options levels on wednesday, December 17, 2014:

EUR / USD

Resistance levels (open interest**, contracts)

$1.2590 (3390)

$1.2572 (2777)

$1.2543 (1502)

Price at time of writing this review: $ 1.2485

Support levels (open interest**, contracts):

$1.2444 (435)

$1.2407 (810)

$1.2355 (2150)

Comments:

- Overall open interest on the CALL options with the expiration date January, 9 is 50855 contracts, with the maximum number of contracts with strike price $1,2500 (6810);

- Overall open interest on the PUT options with the expiration date January, 9 is 59068 contracts, with the maximum number of contracts with strike price $1,2000 (7549);

- The ratio of PUT/CALL was 1.16 versus 1.09 from the previous trading day according to data from December, 16

GBP/USD

Resistance levels (open interest**, contracts)

$1.6002 (2720)

$1.5904 (1758)

$1.5807 (1842)

Price at time of writing this review: $1.5722

Support levels (open interest**, contracts):

$1.5690 (1312)

$1.5593 (1047)

$1.5496 (960)

Comments:

- Overall open interest on the CALL options with the expiration date January, 9 is 22243 contracts, with the maximum number of contracts with strike price $1,5850 (4142);

- Overall open interest on the PUT options with the expiration date January, 9 is 17562 contracts, with the maximum number of contracts with strike price $1,5550 (1722);

- The ratio of PUT/CALL was 0.79 versus 0.79 from the previous trading day according to data from December, 16

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

02:01

Nikkei 225 16,831.61 +76.29 +0.46%, Hang Seng 22,685.95 +15.45 +0.07%, Shanghai Composite 3,030.19+8.67 +0.29%

-

00:02

Commodities. Daily history for Dec 16’2014:

(raw materials / closing price /% change)

Light Crude 55.45 -0.86%

Gold 1,197.10 +0.23%

-

00:02

Stocks. Daily history for Dec 16’2014:

(index / closing price / change items /% change)

Nikkei 225 16,755.32 -344.08 -2.01%

Hang Seng 22,670.5 -357.35 -1.55%

Shanghai Composite 3,021.52 +68.10 +2.31%

FTSE 100 6,331.83 +149.11 +2.41%

CAC 40 4,093.2 +87.82 +2.19%

Xetra DAX 9,563.89 +229.88 +2.46%

S&P 500 1,972.74 -16.89 -0.85%

NASDAQ Composite 4,547.83 -57.32 -1.24%

Dow Jones 17,068.87 -111.97 -0.65%

-

00:01

Currencies. Daily history for Dec 16’2014:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,2510 +0,59%

GBP/USD $1,5750 +0,72%

USD/CHF Chf0,9597 -0,59%

USD/JPY Y116,39 -1,22%

EUR/JPY Y145,63 -0,60%

GBP/JPY Y183,3 -0,49%

AUD/USD $0,8217 +0,09%

NZD/USD $0,7796 +0,68%

USD/CAD C$1,1624-0,40%

-