Notícias do Mercado

-

23:53

Japan: Adjusted Merchandise Trade Balance, bln, February -1133.2 (forecast -893.6)

-

23:31

Australia: Leading Index, February -0.1%

-

23:29

Commodities. Daily history for March 18’2014:

(raw materials / closing price /% change)Gold $1,357.1 -2.60 -0.19%

ICE Brent Crude Oil $106.79 +0.40 +0.38%

NYMEX Crude Oil $99.48 +1.47 +1.50%

-

23:24

Stocks. Daily history for March 18’2014:

(index / closing price / change items /% change)Nikkei 14,411.27 +133.60 +0.94%

Hang Seng 21,583.5 +109.55 +0.51%

Shanghai Composite 2,025.2 +1.52 +0.08%

S&P 500 1,872.25 +13.42 +0.72%

NASDAQ 4,333.31 +53.36 +1.25%

Dow 16,336.19 +88.97 +0.55%

FTSE 6,605.28 +36.93 +0.56%

CAC 4,313.26 +41.30 +0.97%

DAX 9,242.55 +61.66 +0.67%

-

23:19

Currencies. Daily history for March 18'2014:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,3934 -0,09%

GBP/USD $1,6592 -0,24%

USD/CHF Chf0,8730 -0,03%

USD/JPY Y101,42 -0,36%

EUR/JPY Y141,31 -0,28%

GBP/JPY Y168,27 -0,61%

AUD/USD $0,9126 +0,45%

NZD/USD $0,8621 +0,65%

USD/CAD $1,1137 +0,71%

-

23:01

Schedule for today, Wednesday, March 19’2014:

(time / country / index / period / previous value / forecast)

04:30 Japan All Industry Activity Index, m/m January -0.1% +1.3%

05:00 Japan BOJ Governor Haruhiko Kuroda Speaks

09:30 United Kingdom Average earnings ex bonuses, 3 m/y January +1.0% +1.2%

09:30 United Kingdom Average Earnings, 3m/y January +1.1% +1.3%

09:30 United Kingdom Bank of England Minutes

09:30 United Kingdom Claimant count February -27.6 -23.3

09:30 United Kingdom Claimant Count Rate February 3.6% 3.5%

09:30 United Kingdom ILO Unemployment Rate January 7.2% 7.2%

10:00 Eurozone Construction Output, m/m January +0.9% +1.8%

10:00 Eurozone Construction Output, y/y January -0.2%

10:00 Switzerland Credit Suisse ZEW Survey (Expectations) March 28.7 25.0

12:30 United Kingdom Chancellor Osborne Speaks

12:30 United Kingdom Annual Budget Release 2014

12:30 Canada Wholesale Sales, m/m January -1.4% +1.2%

12:30 U.S. Current account, bln Quarter IV -94.87 -88.0

14:30 U.S. Crude Oil Inventories March +6.2

17:00 Switzerland SNB Chairman Jordan Speaks

18:00 U.S. Fed Interest Rate Decision 0.25% 0.25%

18:00 U.S. FOMC QE Decision 65 55

18:00 U.S. FOMC Economic Projections

18:00 U.S. FOMC Statement

18:30 U.S. Federal Reserve Press Conference

21:45 New Zealand GDP q/q Quarter IV +1.4% +1.0%

21:45 New Zealand GDP y/y Quarter IV +3.5% +3.1%

-

19:00

Dow 16,353.87 +106.65 +0.66%, Nasdaq 4,332.55 +52.60 +1.23%, S&P 500 1,872.83 +14.00 +0.75%

-

18:20

American focus : the euro fluctuates against the U.S. dollar

The euro rose sharply against the dollar, but could not resist the vicinity of achieved values , and fell to session lows , and then recovered . Initially influenced the course of trading weak data for the euro area and Germany, but active buying dips and words of Russian President Putin promoted a marked increase . Nevertheless , submitted after U.S. data back to previous levels euros . At the beginning of the American session EUR / USD updated session low , then bounced back and beyond the level of $ 1.3900 at the resumed concern about the situation in Crimea.

As for the data , they showed that the economic expectations for Germany deteriorated significantly in March , beating forecasts while most experts . It became known from the results of recent studies that were presented today by the Centre for European Economic Research ZEW. According to the index of economic confidence fell this month to the level of 46.6 points, compared with 55.7 points in February . Many experts expect that this figure will drop 52.8 . Meanwhile, we note that the index of the current economic situation has improved to 51.3 points from 50 a month earlier. Nevertheless , it remained below the expected level of 52 points . Also, the data showed that economic expectations in the euro area declined by 7 points - to 61.5 points . In contrast, the current economic situation indicator increased by 3.5 points - to 36.7 points.

Meanwhile, U.S. data showed that consumer prices have not changed in February , which is a sign of restrained inflationary pressures in the economy. According to the report , the February consumer price index rose a seasonally adjusted 0.1 % compared with the previous month. Basic prices , which exclude volatile categories, namely, the price of food and energy , also rose by 0.1%. Last significance were in line with economists' forecasts . Meanwhile, it was reported that consumer prices rose by 1.1% compared to February last year. It was the weakest annual growth since October. Also figure was below 2 per cent target by the Federal Reserve System. Basic prices , meanwhile, rose by 1.6 % compared to last year. Economists were expecting an increase of 1.2% and 1.6% , respectively.

At the same time , housing data indicate that adverse weather conditions seem to restrain the pace of housing starts in February , but the basic figures showed that the sector may be ready for spring rebound . This in his report informed the Ministry of Commerce . According to the data , bookmarks new homes in the U.S. fell last month by 0.2% to a seasonally adjusted annual rate reached 907 thousand slight deterioration occurred after construction fell by 11.2 % in January , although the rate for this month were revised upwards ( up to 910 thousand from 880 thousand ) .

The yen is trading with a noticeable increase against the U.S. dollar . Markets continue to play up the theme of the Crimea, and according to recent reports , Russian President Vladimir Putin signed a decree recognizing the Republic of Crimea as a sovereign and independent state , which creates prerequisites for joining the peninsula to Russia . In light of the current situation, the EU and the United States imposed sanctions against certain officials of Russia and Ukraine , the number reached 21 people . According to Europe and America , these people are guilty of infringing on the sovereignty of Ukraine . In this list of Russian President Vladimir Putin did not hit, although it is expected the introduction of further sanctions in the event of further intervention by Russia . Markets remain relatively calm and safe-haven rally stopped . In general, the market situation in the Crimea scenario assumes preservation " wait and see ."

The Canadian dollar fell after comments from Bank of Canada Governor Steven runners pointed out the potential weakness of the Canadian economy in the first quarter of this year. Runner said that lag in real output in the economy from potential is unlikely to be closed for several years . Runner also noted that inflation in February was probably as weak GDP growth in the first quarter . Even so, he expects GDP growth this year and next above trend .

" On the inflation front , although we have in the past few months, core inflation slightly stronger, which is reassuring , most analysts expect weak inflation data later in the week because of a sharp change in February last year ", - said skid . Data on inflation in Canada go on Friday .

-

18:00

European stocks close

European stocks rose, extending their biggest gain in two weeks, after Russian President Vladimir Putin said he isn’t seeking to split up Ukraine.

The Stoxx Europe 600 Index gained 0.6 percent to 327.93 at the close in London, after earlier falling as much as 0.5 percent. The gauge climbed 1.1 percent yesterday, rebounding from its biggest weekly loss since January.

Putin signaled that his country isn’t about to occupy eastern Ukraine after a March 16 Crimean referendum backed joining Russia by almost 97 percent. The U.S. and European Union imposed sanctions on Russian and Crimean officials and threatened further measures.

National benchmark indexes advanced in all of the 18 western-European markets. Germany’s DAX gained 0.7 percent, while France’s CAC added 1 percent and the U.K.’s FTSE 100 rose 0.6 percent.

Kuoni climbed 8.2 percent to 409 Swiss francs. The company said 2013 earnings before interest and taxes rose to 154.2 million francs ($176.7 million), more than the 142.3 million francs analysts had projected. Kuoni added it plans to raise its dividend payout ratio to 40 percent to 45 percent from 30 percent to 35 percent.

Voestalpine AG gained 5.5 percent to 32.06 euros. The Austrian steelmaker said it will reduce costs by 900 million euros ($1.25 billion) in the next three years, adding it won’t cut jobs.

Cairn Energy slumped 14 percent to 168.2 pence, the lowest price since January 2004. The Scottish oil explorer said it is suspending its share repurchase program until an Indian tax issue is resolved. The company said in January authorities are auditing it for the year ended March 2007.

Scania fell 2.1 percent to 191.80 kronor. A board committee reviewing Volkswagen’s takeover offer said the bid was too low. The German company offered 6.7 billion euros for the Swedish truckmaker’s stock it doesn’t already own. The bid was 36 percent higher than Scania’s closing price on Feb. 21, when Volkswagen announced its plan for a full takeover. Volkswagen rose 0.1 percent to 180.40 euros.

-

17:00

European stocks closed in plus: FTSE 100 6,606.03 +37.68 +0.57%, CAC 40 4,315.13 +43.17 +1.01%, DAX 9,248.33 +67.44 +0.73%

-

15:42

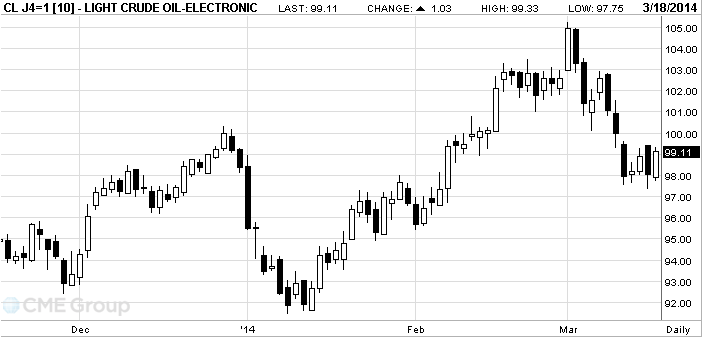

Oil rose

West Texas Intermediate rose for the third time in four days after data showed the

Prices increased as much as 0.6 percent in

“The market is a little optimistic about the

WTI for April delivery gained 24 cents to $98.32 a barrel at 9:32 a.m. on the New York Mercantile Exchange. The volume of all futures traded was near the 100-day average for this time of day.

Brent for May settlement slid 15 cents to $106.09 a barrel on the London-based ICE Futures Europe exchange. Volume was 22 percent below the 100-day average. The European benchmark crude settled at $106.24 a barrel yesterday, the lowest close since Feb. 4. Brent was at a premium of $8.31 to WTI for the same month. The spread closed at $8.62 yesterday.

-

15:21

Gold fell

The price of gold declines a second consecutive session on a stronger dollar due to political instability in the Crimea and the West's reaction .

Today in Parliament , Russian President Vladimir Putin said that now Sevastopol and Crimea are part of Russia , and the sanctions imposed by the EU and the U.S. , is an act of aggression , which will entail retaliatory measures. Moscow assured that an agreement to join the Crimea to Russia will be signed in the coming days .

Following comments by Putin acting president Alexander Turchinov reiterated that Kiev does not recognize Russia as part of the peninsula .

Meanwhile, French Foreign Minister L. Fabius wrote in his twitter account that the leaders of the G8 decided to exclude Russia from the block, adding that " all the other countries in the face of Seven leading nations will unite in its course of action is not Russia."

Later this message denied German Chancellor Angela Merkel, who said that at the moment the status of Russia in the G8 remains the same.

U.S. President Barack Obama has invited the leaders of the G7 and EU officials for talks on Ukraine next week.

The cost of the April gold futures on the COMEX today dropped to $ 1351.10 per ounce.

-

13:45

Option expiries for today's 1400GMT cut

USD/JPY Y100.60, Y101.00, Y101.80, Y102.00, Y102.30, Y102.50/60, Y103.00, Y103.50

EUR/USD $1.3700, $1.3850, $1.3890, $1.3975

GBP/USD $1.6680

EUR/GBP stg0.8230, stg0.8240, stg0.8380

EUR/CHF Chf1.2125, Chf1.2250

AUD/USD $0.8865, $0.8885, $0.9000, $0.9025, $0.9050

USD/CAD C$1.0970/80, C$1.1010, C$1.1230

-

13:37

U.S. Stocks open: Dow 16,277.98 +30.76 +0.19%, Nasdaq 4,289.37 +9.42 +0.22%, S&P 1,862.45 +3.62 +0.19%

-

13:21

Before the bell: S&P futures +0.29%, Nasdaq futures +0.27%

U.S. stock-index futures climbed after Vladimir Putin said Russia isn’t seeking to split Ukraine and called for an end to Cold War rhetoric.

Global markets:

Nikkei 14,411.27 +133.60 +0.94%

Hang Seng 21,583.5 +109.55 +0.51%

Shanghai Composite 2,025.2 +1.52 +0.08%

FTSE 6,587.33 +18.98 +0.29 %

CAC 4,311.44 +39.48 +0.92 %

DAX 9,240.24 +59.35 +0.65 %

Crude oil $98.32 (+0.24%)

Gold $1354.30 (-1.35%).

-

13:15

European session: the euro declined significantly against the U.S. dollar

Data

00:30 Australia RBA Meeting's Minutes

01:30 China Property Prices, y/y February +9.6% +8.7%

06:45 Switzerland SECO Economic Forecasts Quarter II

10:00 Eurozone ZEW Economic Sentiment March 68.5 67.3 61.5

10:00 Eurozone Trade Balance s.a. January 13.7 13.9

10:00 Germany ZEW Survey - Economic Sentiment March 55.7 52.8 46.6

12:30 Canada Manufacturing Shipments (MoM) January -1.5% Revised From -0.9% +1.1% +1.5%

12:30 U.S. Building Permits, mln February 950 Revised From 937 960 1018

12:30 U.S. Housing Starts, mln February 910 Revised From 880 910 910

12:30 U.S. CPI, m/m February +0.1% +0.1% +0.1%

12:30 U.S. CPI, Y/Y February +1.6% +1.2% +1.1%

12:30 U.S. CPI excluding food and energy, m/m February +0.1% +0.1% +0.1%

12:30 U.S. CPI excluding food and energy, Y/Y February +1.6% +1.6% +1.6%

13:00 U.S. Net Long-term TIC Flows January -45.9 23.4 7.3

13:00 U.S. Total Net TIC Flows January -126.7 Revised From -119.6 83

The euro exchange rate rose sharply against the dollar, but could not resist the vicinity of achieved values , and fell to session lows . Initially influenced the course of trading weak data for the euro area and Germany, but active buying dips and words of Russian President Putin promoted a marked increase . Nevertheless , submitted after U.S. data back to previous levels euros .

As for the data , they showed that the economic expectations for Germany deteriorated significantly in March , beating forecasts while most experts . It became known from the results of recent studies that were presented today by the Centre for European Economic Research ZEW. According to the index of economic confidence fell this month to the level of 46.6 points, compared with 55.7 points in February . Many experts expect that this figure will drop 52.8 . Meanwhile, we note that the index of the current economic situation has improved to 51.3 points from 50 a month earlier. Nevertheless , it remained below the expected level of 52 points . Also, the data showed that economic expectations in the euro area declined by 7 points - to 61.5 points . In contrast, the current economic situation indicator increased by 3.5 points - to 36.7 points.

Meanwhile, U.S. data showed that consumer price index rose by 0.1 % and building permits - to 1018 thousand units.

Pound weakened significantly against the U.S. dollar , updating intraday lows below $ 1.6600 . Many market participants are waiting for tonight's speech by Bank of England Governor Mark Carney . It is unlikely he will tell something new markets , but another piece of " dovish " statements may have a couple more substantial pressure . From the point of view of fundamental factors , this week promises to be very intense. Next report will be a key labor market indicators , the report and the Bank of England meeting FOMC.

The yen is trading with a noticeable increase against the U.S. dollar . Markets continue to play up the theme of the Crimea, and according to recent reports , Russian President Vladimir Putin signed a decree recognizing the Republic of Crimea as a sovereign and independent state , which creates prerequisites for joining the peninsula to Russia . In light of the current situation, the EU and the United States imposed sanctions against certain officials of Russia and Ukraine , the number reached 21 people . According to Europe and America , these people are guilty of infringing on the sovereignty of Ukraine . In this list of Russian President Vladimir Putin did not hit, although it is expected the introduction of further sanctions in the event of further intervention by Russia . Markets remain relatively calm and safe-haven rally stopped . In general, the market situation in the Crimea scenario assumes preservation " wait and see ."

EUR / USD: during the European session, the pair fell to $ 1.3889

GBP / USD: during the European session, the pair fell to $ 1.6572

USD / JPY: during the European session, the pair dropped to Y101.30

At 21:45 GMT New Zealand will report on the current account balance of the balance of payments for the 4th quarter . At 23:30 GMT Australia will index of leading indicators of economic activity from the Westpac-MI in February. At 23:50 GMT , Japan declares total foreign trade balance for February.

-

13:01

U.S.: Total Net TIC Flows, January 83

-

13:00

U.S.: Net Long-term TIC Flows , January 7.3 (forecast 23.4)

-

12:45

Orders

EUR/USD

Offers $1.4000, $1.3967/75, $1.3945/50

Bids $1.3870/75, $1.3820/30, $1.3770/60, $1.3710/00

GBP/USD

Offers $1.6720/25, $1.6665/70

Bids $1.6565/70, $1.6510/00

AUD/USD

Offers $0.9150, $0.9130, $0.9110

Bids $0.9000/10, $0.8950, $0.8910/00

EUR/JPY

Offers Y142.90/00, Y142.50, Y142.00

Bids Y140.55/50, Y140.00, Y139.50

USD/JPY

Offers Y103.00, Y102.50/55, Y102.00

Bids Y101.20, Y101.00, Y100.50

EUR/GBP

Offers stg0.8415/20, stg0.8405, stg0.8385/90

Bids stg0.8335/40, stg0.8320/15, stg0.8280/75

-

12:32

U.S.: CPI excluding food and energy, m/m, February +0.1% (forecast +0.1%)

-

12:32

U.S.: CPI, Y/Y, February +1.1% (forecast +1.2%)

-

12:32

U.S.: CPI excluding food and energy, Y/Y, February +1.6% (forecast +1.6%)

-

12:31

U.S.: Building Permits, mln, February 1018 (forecast 960)

-

12:31

U.S.: Housing Starts, mln, February 907 (forecast 910)

-

12:31

U.S.: CPI, m/m , February +0.1% (forecast +0.1%)

-

12:30

Canada: Manufacturing Shipments (MoM), January +1.5% (forecast +1.1%)

-

11:30

European stock fell

European stock indexes fell slightly , after fixing the biggest growth in the last two weeks , as investors continued to monitor developments in Ukraine. U.S. index futures are little changed , while Asian shares rose .

Russian President Vladimir Putin ordered to approve the draft agreement on the adoption of the Crimea in the Russian Federation. March 16 in the Crimea at the military and political support of Russia held a referendum which resulted in power Peninsula proclaimed an independent republic and warned of the Russian Federation.

Yesterday, the EU and the U.S. have entered the first stage of sanctions in response to the Russian annexation of the Crimea . At a meeting of the Council of Europe was approved list of those banned from entry to the territory of the EU and freeze all assets located in their territory . Sanctions have also introduced Canada and Japan .

The Stoxx Europe 600 Index fell 0.1 percent. Yesterday gauge climbed 1.1 percent , recovering slightly after its biggest weekly decline since January.

"The situation in Russia and Ukraine is a source of danger for the market ," said Alessandro Fezii , an analyst at LGT Bank Schweiz AG. " While the international response is still quite muted , investors know that it can lead to an escalation , and cautious".

Many market participants also drew attention to the weak data on Germany. As it became known , the index of economic confidence fell this month to the level of 46.6 points, compared with 55.7 points in February . Many experts expect that this figure will drop 52.8 . Meanwhile, we note that the index of the current economic situation has improved to 51.3 points from 50 a month earlier. Nevertheless , it remained below the expected level of 52 points .

Also, the data showed that economic expectations in the euro area declined by 7 points - to 61.5 points . In contrast, the current economic situation indicator increased by 3.5 points - to 36.7 points.

Cost Cairn Energy fell 11 percent after the company Scottish oil producer said it would suspend its share buyback program until such time as the problem with the Indian tax is resolved.

Scania shares fell 4.2 percent . The Committee recommended that the Board of Directors to reject the proposal to increase the Volkswagen AG stake Scania by 6.7 billion euros. Against this background, the cost of Volkswagen fell 0.2 percent .

Cost of J Sainsbury Plc fell by 0.9 % , after it became known that comparable sales as a leading operator of supermarkets in the UK fell in the 10 weeks ended March 15 , 3.1%. Experts had expected a decline of 2.7%.

Royal Imtech NV capitalization decreased by 2.8 percent. The company reported that its net loss widened to 701 million euros in 2013 from 247 million euros a year earlier .

Kuoni cost rose by 6.2 percent , as it became known that in 2013 earnings before interest and taxes rose to 154.2 million francs , compared with a forecast of 142.3 million francs. Kuoni also added that they plan to increase its dividend payout ratio to 40-45 percent from 30-35 percent.

At the current moment

FTSE 100 6,552.6 -15.75 -0.24 %

CAC 40 4,268.86 -3.10 -0.07 %

DAX 9,129.64 -51.25 -0.56%

-

10:18

Option expiries for today's 1400GMT cut

USD/JPY Y100.60, Y101.00, Y101.80, Y102.00, Y102.30, Y102.50/60, Y103.00, Y103.50

EUR/USD $1.3700, $1.3850, $1.3890, $1.3975

GBP/USD $1.6680

EUR/GBP stg0.8230, stg0.8240, stg0.8380

EUR/CHF Chf1.2125, Chf1.2250

AUD/USD $0.8865, $0.8885, $0.9000, $0.9025, $0.9050

USD/CAD C$1.0970/80, C$1.1010, C$1.1230

-

10:01

Eurozone: ZEW Economic Sentiment, March 61.5 (forecast 67.3)

-

10:00

Germany: ZEW Survey - Economic Sentiment, March 46.6 (forecast 52.8)

-

09:39

Asia Pacific stocks close

Asian stocks rose, with the regional benchmark rebounding from a five-week low, as data showing improvement in U.S. factory output boosted optimism for the world’s biggest economy.

Nikkei 225 14,411.27 +133.60 +0.94%

S&P/ASX 200 5,344.56 +27.00 +0.51%

Shanghai Composite 2,025.2 +1.52 +0.08%

LG Electronics Inc., the world’s second-biggest maker of televisions, added 4.2 percent in Seoul.

Lippo Ltd., founded by Indonesian tycoon Mochtar Riady, surged by a record in Hong Kong after South Korea approved a proposal by the company and Las Vegas-based partner Caesars Entertainment Corp. to build a casino.

Tencent Holdings Ltd., Asia’s biggest Internet company, jumped 5.8 percent, snapping a four-day decline, before releasing earnings tomorrow.

-

08:42

FTSE 100 6,542.19 -26.16 -0.40%, CAC 40 4,261.79 -10.17 -0.24%, Xetra DAX 9,148.86 -32.03 -0.35%

-

06:44

European bourses are seen trading flat to modestly higher Tuesday: the FTSE is seen up 0.2%, the DAX unchanged and the CAC up 0.1%

-

06:26

Asian session: The dollar held a gain from yesterday

00:30 Australia RBA Meeting's Minutes

01:30 China Property Prices, y/y February +9.6% +8.7%

The dollar held a gain from yesterday versus the yen before the Federal Reserve starts a two-day meeting at which policy makers are expected to trim asset purchases that tend to debase the greenback. U.S. policy makers will meet today and tomorrow in the Federal Open Market Committee’s first gathering led by Fed Chair Janet Yellen since she succeeded Ben S. Bernanke last month. The central bank has cut monthly bond purchases to $65 billion this year, from $85 billion in 2013. Yellen last month pledged further “measured” steps to slow the buying if improvement continues.

The yen remained lower against most of its 16 major peers as concern eased that Crimea’s vote to secede from Ukraine would spur turmoil in the region. The European Union and the U.S. imposed sanctions on individuals in Russia and Crimea amid the standoff. Crimean lawmakers set in motion measures for the Black Sea peninsula to leave Ukraine and join Russia after a March 16 plebiscite, which EU and U.S. leaders have condemned as illegal. Russia has deployed about 60,000 troops along the Ukrainian border, according to the government in Kiev.

The Australian dollar gained briefly after minutes of the Reserve Bank meeting this month reiterated a period of interest-rate stability was likely. The central bank said it saw more signs record-low interest rates were boosting growth, and reiterated a period of steady borrowing costs was likely.

EUR / USD: during the Asian session, the pair traded in the range of $ 1.3920-40

GBP / USD: during the Asian session, the pair traded in the range of $ 1.6630-45

USD / JPY: on Asian session the pair traded in the range of Y101.65-95

The European calendar starts at 0700GMT, when the German Feb wholesale prices data will be published. At the same time, the EMU February ACEA car registrations data will cross the wires. At 0800GMT, Spanish fourth quarter labour costs will be released. However, at the same time, much of the market's attention will be focused on Karlsruhe in Germany, where the German Constitutional Court will give its final ruling on the European Stability Mechanism. The Court has already made a provisional ruling in favour of the ESM - with some caveats - and is not expected to deviate from that ruling. At 1000GMT, the EMU January trade balance data will be released, although the German March ZEW survey will be the most watched. At the same time, ECB Supervisory Board Chair Daniele Nouy will appear before the European Parliament's Economic and Monetary Affairs Committee. At 1300GMT, German Chancellor Angela Merkel and Portuguese PM Pedro Passos Coelho hold a press conference after a meeting in Berlin. Across the Atlantic, the US calendar gets underway at 1145GMT, when the ICSC-Goldman Store Sales for the March 15 week will be released. The main US data will be published at 1230GMT, when the February housing starts and building permits data is released, along with the February CPI. The core CPI is also expected to be up 0.1%. Also due for release at 1230GMT is the Canadian January manufacturing survey. The US Redbook Average for the March 15 week are due for release at 1255GMT. At 1300GMT, German Chancellor Angela Merkel and Portuguese PM Pedro Passos Coelho hold a press conference after a meeting in Berlin. -