Notícias do Mercado

-

23:29

Commodities. Daily history for March 19’2014:

(raw materials / closing price /% change)Gold $1,341.4 -16.60 -1.22%

ICE Brent Crude Oil $105.85 -0.80 -0.75%

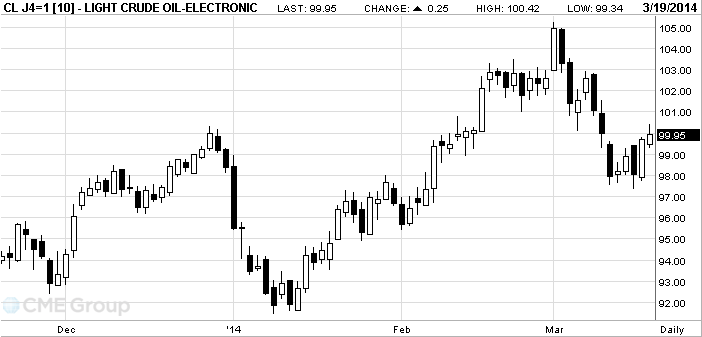

NYMEX Crude Oil $100.42 +0.95 +0.96%

-

23:29

Stocks. Daily history for March 19’2014:

(index / closing price / change items /% change)Nikkei 14,462.52 +51.25 +0.36%

Hang Seng 21,568.69 -14.81 -0.07%

Shanghai Composite 2,021.73 -3.46 -0.17%

S&P 1,860.77 -11.48 -0.61%

NASDAQ 4,307.6 -25.71 -0.59%

Dow 16,222.17 -114.02 -0.70%

FTSE 6,573.13 -32.15 -0.49%

CAC 4,308.06 -5.20 -0.12%

DAX 9,277.05 +34.50 +0.37%

-

23:29

Currencies. Daily history for March 19'2014:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,3817 -0,85%

GBP/USD $1,6530 -0,38%

USD/CHF Chf0,8818 +1,00%

USD/JPY Y102,38 +0,94%

EUR/JPY Y141,46 +0,11%

GBP/JPY Y169,24 +0,57%

AUD/USD $0,9032 -1,04%

NZD/USD $0,8537 -0,98%

-

23:01

Schedule for today, Thursday, March 20’2014:

(time / country / index / period / previous value / forecast)

00:30 Australia RBA Bulletin Quarter I

07:00 Germany Producer Price Index (MoM) February -0.1% +0.2%

07:00 Germany Producer Price Index (YoY) February -1.1% -0.9%

07:00 Switzerland Trade Balance February 2.59 2.47

07:15 Japan BOJ Governor Haruhiko Kuroda Speaks

08:30 Switzerland SNB Monetary Policy Assessment

08:30 Switzerland SNB Interest Rate Decision 0.25% 0.25%

10:00 Eurozone EU Economic Summit

10:00 Eurozone ECB President Mario Draghi Speaks

10:00 Eurozone European Council Meeting

11:00 United Kingdom CBI industrial order books balance March 3 5

12:30 U.S. Initial Jobless Claims March 315 327

14:00 U.S. Leading Indicators February +0.3% +0.3%

14:00 U.S. Existing Home Sales February 4.62 4.65

14:00 U.S. Philadelphia Fed Manufacturing Survey March -6.3 4.2

16:30 United Kingdom MPC Member Weale Speaks

20:00 U.S. Bank Stress Test Results

21:00 New Zealand ANZ Job Advertisements (MoM) February +2.8%

23:00 Australia Conference Board Australia Leading Index January +0.8% -

19:00

Dow 16,298.05 -38.14 -0.23%, Nasdaq 4,320.13 -13.18 -0.30%, S&P 500 1,867.94 -4.31 -0.23%

-

18:01

U.S.: Fed Interest Rate Decision , 0.25% (forecast 0.25%)

-

18:01

U.S.: FOMC QE Decision, 55 (forecast 55)

-

17:40

European stocks close

European stocks were little changed, following two days of gains, as investors awaited a speech by Federal Reserve Chair Janet Yellen to gauge the central bank’s views on its stimulus program and interest rates.

The Stoxx Europe 600 Index dropped 0.1 percent to 327.63 at the close of trading. The gauge slid 4.8 percent from Feb. 25 through the end of last week amid a standoff between Russia and the West over Crimea. It extended this week’s gain yesterday as Russian President Vladimir Putin said he isn’t seeking to annex other parts of Ukraine.

Fed officials today end a two-day policy meeting at which they will decide whether to slow the central bank’s monthly asset-purchase program. They will announce the outcome after European markets close, followed by Yellen’s speech.

The Federal Open Market Committee will cut its monthly bond buying by $10 billion to $55 billion and continue reductions at that pace at every meeting before announcing an end to the program at its Oct. 28-29 gathering, economists said in a survey. The Fed will also probably scrap its 6.5 percent jobless rate threshold to adopt qualitative guidance for signaling when it will consider raising the benchmark interest rate, according to the survey.

National benchmark indexes declined in 11 of the 18 western European markets. The U.K.’s FTSE 100 lost 0.5 percent, Germany’s DAX added 0.4 percent, and France’s CAC 40 slipped 0.1 percent.

Inditex climbed 4.9 percent to 108.10 euros after the owner of the Zara clothing chain said sales in local currencies rose 12 percent from Feb. 1 to March 15. Profit for 2013 totaled 2.38 billion euros ($3.31 billion), Inditex also said. That compared with the average analyst projection of 2.39 billion euros.

Brenntag AG gained 0.8 percent to 132 euros after recommending a payout of 2.60 euros per share, surpassing the Bloomberg Dividend estimate of 2.40 euros. The world’s largest distributor of chemicals also said it will propose a three-for-one stock split at its annual general meeting on June 17.

HeidelbergCement AG declined 1.8 percent to 60.22 euros after saying that net debt at Dec. 31, 2013 rose to 7.5 billion euros as it increased its stake in joint ventures and paid a fine for cartel infringements dating back to the 1990s. That exceeded the average analyst estimate of 7.2 billion euros.

-

17:21

American focus : the euro fell

The euro fell against the dollar today on the eve of publication of the two-day meeting of the Federal Open Market Committee, the Fed , followed by the first press conference Janet Yellen . It is expected that the Central Bank will continue to reduce the quantitative easing program . It is worth noting that in the last month , Fed Chairman Yellen has promised to continue to move in the direction of reduction of monetary stimulus . Positive economic statistics confirm this prediction . In addition , analysts expect the Fed to abandon the target level of unemployment, which tied terms of higher interest rates . Most experts expect that the Central Bank may move to a new practice notice of plans to raise the base interest rate and determine further action by a number of macroeconomic indicators .

Little influenced by the data for the euro area , which showed that the seasonally adjusted construction output rose in January by 1.5 per cent ( on a monthly basis ), which is followed by growth of 1.3 percent in December and fall by 0.1 percent in November . Experts predicted an increase of 1.8 percent. In annual terms, construction output rose by 8.8 percent in the beginning of the year , changing the downward trend , which was observed in recent months.

The dollar had evidence that the current account deficit the U.S. fell to a 14- year low in the fourth quarter , as the volume of exports reached record levels. This was stated in the report, which was submitted to the Ministry of Commerce . According to the negative balance of payments declined in the last quarter of 2013 to $ 81.12 billion , compared with a revised upward figure for the third quarter at $ 93.37 billion

The latter value was the lowest since the third quarter of 1999 , and represented 1.9 percent of gross domestic product ( the lowest proportion since the third quarter of 1997 ) , compared with 2.3 percent in the period from July to September. Economists forecast that the current account deficit will fall to $ 88 billion from $ 94.84 billion, which was originally reported.

For the full 2013 current account deficit was on average at 2.3 per cent of GDP , which is the lowest value since 1997.

Pound was up against the U.S. dollar , which was associated with the publication of minutes of meetings of the Bank of England and labor market data . Note that the minutes of the last meeting of the Bank of England from March 5-6, showed that members of the Central Bank were unanimous in their decision to maintain the status quo , leaving the rate at around 0.5% , and the size of its asset purchase program - at £ 375 billion MPC members noted that in the three months to December , employment growth slowed slightly in the UK , and the unemployment rate remained above the 7% mark target designated by the Bank in the past year . MPC members stressed that the recent appreciation of sterling puts downward pressure on inflation .

Meanwhile, data showed that the unemployment rate for three months ( December) compared with the previous three-month period remained unchanged - at 7.2 % , confirming the predictions of many experts. The number of applications for unemployment benefits fell by 34.6 million in February , after falling 33.9 thousand the previous month ( revised from -27.6 million). Economists were expecting a decrease only 23.3 thousand Moreover , it became known that the level of unemployment claims for employment fell in February to reach 3.5% from 3.6 % in January , showing the 16th consecutive monthly decline . The number of people in employment has reached a new record high - a little less than 30.2 million , driven by growth in self-employment.

The yen fell against the U.S. dollar . Impact on the dynamics of the data provided by Japan, as well as words BOJ board member Takahide Kiut . Report submitted to the Ministry of Finance of Japan, showed that the trade deficit declined in February to a level of 800.3 billion yen , compared with 2.8 trillion . yen in January. Deficit reduction occurred on the background of accelerating export growth and weakening imports. However, experts expect further reduction - up to 600 billion yen. Add that captures Japan 's trade deficit for 20 consecutive months ( the longest period since 1979 ) . Meanwhile, it became known that the growth rate of imports in the country in February slowed to 9% from 25.1 % in January , as export growth accelerated to 9.8% from 9.5% .

With regard to the Kiut , he warned that if the Central Bank will forever campaign to mitigate the monetary policy or to undertake additional mitigation measures , it can give rise to adverse effects on the markets .

-

17:00

European stocks closed in different ways: FTSE 100 6,573.13 -32.15 -0.49%, CAC 40 4,308.06 -5.20 -0.12%, DAX 9,277.05 +34.50 +0.37%

-

15:40

Oil rose

West Texas Intermediate rose after a government report showed that inventories at Cushing, Oklahoma, the delivery point for the contract, dropped a seventh week. Brent oil slid.

WTI rose as much as 0.7 percent. Supplies at Cushing fell 989,000 barrels to 29.8 million last week, the lowest level since January 2012, the Energy Information Administration said. Futures also climbed after Enterprise Products Partners LP said yesterday that operations on the expanded Seaway line to

WTI for April delivery advanced 58 cents, or 0.6 percent, to $100.28 a barrel at 10:43 a.m. on the New York Mercantile Exchange. The contract traded at $100.23 before the release of the report at 10:30 a.m. in

Brent for May settlement dropped 68 cents, or 0.6 percent, to $106.11 a barrel on the London-based ICE Futures Europe exchange. Trading volume was 13 percent lower than the 100-day average. The European benchmark’s premium to WTI for the same month slipped to $7.04 a barrel.

Cushing stockpiles have fallen since the southern portion of the Keystone XL pipeline began moving oil to the

Total crude inventories climbed by 5.85 million barrels to 375.9 million, the EIA said. A 2.75 million-barrel gain was projected, according to the median of 11 analyst responses in a Bloomberg survey.

Supplies of distillate fuel, a category that includes heating oil and diesel, fell 3.1 million barrels last week to 110.8 million, the lowest level since May 2008, according to the EIA, the Energy Department’s statistical arm. Gasoline stockpiles dropped 1.47 million barrels to 222.3 million.

-

15:21

Gold fell third consecutive session

The price of gold is reduced by the weakening of tension around the situation in the Crimea, and pending the outcome of the meeting of the Federal Open Market Committee Federal Reserve .

" Reducing the cost of gold continues from the beginning of the week. One of the reasons - is selling due to stabilization of the situation around the Crimea, which supports risk appetite . On the other hand , low inflation and positive statistics from the United States put pressure on prices , "- said Commerzbank analyst Daniel Brizmann .

A day earlier, the U.S. Labor Department reported that annual inflation slowed in February to 1.1 % from 1.6 % in January , on a monthly basis , consumer prices increased by 0.1%. Analysts had expected a slowdown in consumer prices up 1.2% year on year and monthly inflation at 0.1% .

Brizmann also noted that currently market participants focused on the meeting of the U.S. Federal Reserve 's monetary policy , the results of which will be announced later on Wednesday .

It is expected that the U.S. Federal Reserve will continue to reduce the asset purchase program and slash it to $ 10 billion - to $ 55 billion

The Fed is expected to leave its key interest rate near zero , but the change may signal further action plan.

The cost of the April gold futures on the COMEX today dropped to $ 1338.10 per ounce.

-

14:30

U.S.: Crude Oil Inventories, March +5.9

-

13:45

Option expiries for today's 1400GMT cut

USD/JPY Y101.00, Y101.25, Y101.50, Y101.85, Y101.95, Y102.00, Y102.15-25, Y102.70, Y103.00

EUR/JPY Y142.00

EUR/USD $1.3790, $1.3800, $1.3815, $1.3860, $1.3900, $1.3915, $1.3920, $1.3960, $1.4010

GBP/USD $1.6650, $1.6675, $1.6695, $1.6700, $1.6900

EUR/GBP stg0.8300

AUD/USD $0.9000, $0.9050, $0.9100-10, $0.9150

NZD/USD $0.8350, $0.8400

USD/CAD C$1.1000, C$1.1025, C$1.1040, C$1.1070, C$1.1085, C$1.1125, C$1.1140, C$1.1150, C$1.1180, C$1.1200, C$1.1225, C$1.1235, C$1.1250

-

13:34

U.S. Stocks open: Dow 16,334.91 -1.28 -0.01%, Nasdaq 4,331.75 -1.56 -0.04%, S&P 1,871.89 -0.36 -0.02%

-

13:23

Before the bell: S&P futures +0.10%, Nasdaq futures +0.14%

U.S. stock-index futures rose as investors awaited a Federal Reserve decision that is forecast to cut monthly bond purchases by $10 billion.

Nikkei 14,462.52 +51.25 +0.36%

Hang Seng 21,568.69 -14.81 -0.07%

Shanghai Composite 2,021.73 -3.46 -0.17%

FTSE 6,599.6 -5.68 -0.09%

CAC 4,318.17 +4.91 +0.11%

DAX 9,297.81 +55.26 +0.60%

Crude oil $100.10 (+0.40%)

Gold $1345.90 (-0.96%).

-

13:17

European session: the pound rose substantially against the U.S. dollar

Data

04:30 Japan All Industry Activity Index, m/m January -0.1% +1.3% +1.0%

05:00 Japan BOJ Governor Haruhiko Kuroda Speaks

09:30 United Kingdom Average earnings ex bonuses, 3 m/y January +1.0% +1.2% +1.3%

09:30 United Kingdom Average Earnings, 3m/y January +1.1% +1.3% +1.4%

09:30 United Kingdom Bank of England Minutes

09:30 United Kingdom Claimant count February -27.6 -23.3 -34.6

09:30 United Kingdom Claimant Count Rate February 3.6% 3.5% 3.5%

09:30 United Kingdom ILO Unemployment Rate January 7.2% 7.2% 7.2%

10:00 Eurozone Construction Output, m/m January +0.9% +1.8% +1.5%

10:00 Eurozone Construction Output, y/y January -0.2% +8.8%

10:00 Switzerland Credit Suisse ZEW Survey (Expectations) March 28.7 25.0 19.0

12:30 United Kingdom Chancellor Osborne Speaks

12:30 United Kingdom Annual Budget Release 2014

12:30 Canada Wholesale Sales, m/m January -1.3% Revised From -1.4% +1.2% +0.8%

12:30 U.S. Current account, bln Quarter IV -96.37 Revised From -94.84 -88.0 -81.12

Euro traded slightly lower against the dollar today on the eve of publication of the two-day meeting of the Federal Open Market Committee, the Fed , followed by the first press conference Janet Yellen . It is expected that the Central Bank will continue to reduce the quantitative easing program . It is worth noting that in the last month , Fed Chairman Yellen, promised to continue to move in the direction of reduction of monetary stimulus . Positive economic statistics confirm this prediction . In addition, analysts expect the Fed to abandon the target level of unemployment, which tied terms of higher interest rates . Most experts expect that the Central Bank may move to a new practice notice of plans to raise the base interest rate and determine further action by a number of macroeconomic indicators .

Little influenced by the data for the euro area , which showed that the seasonally adjusted construction output rose in January by 1.5 per cent ( on a monthly basis ), which is followed by growth of 1.3 percent in December and fall by 0.1 percent in November . Experts predicted an increase of 1.8 percent. In annual terms, construction output rose by 8.8 percent in the beginning of the year , changing the downward trend , which was observed in recent months.

Pound was up against the U.S. dollar , which was associated with the publication of minutes of meetings of the Bank of England and labor market data . Note that the minutes of the last meeting of the Bank of England from March 5-6, showed that members of the Central Bank were unanimous in their decision to maintain the status quo , leaving the rate at around 0.5% , and the size of its asset purchase program - at £ 375 billion MPC members noted that in the three months to December , employment growth slowed slightly in the UK , and the unemployment rate remained above the 7% mark target designated by the Bank in the past year . MPC members stressed that the recent appreciation of sterling puts downward pressure on inflation .

Meanwhile, data showed that the unemployment rate for three months ( December) compared with the previous three-month period remained unchanged - at 7.2 % , confirming the predictions of many experts. The number of applications for unemployment benefits fell by 34.6 million in February , after falling 33.9 thousand the previous month ( revised from -27.6 million). Economists were expecting a decrease only 23.3 thousand Moreover , it became known that the level of unemployment claims for employment fell in February to reach 3.5% from 3.6 % in January , showing the 16th consecutive monthly decline . The number of people in employment has reached a new record high - a little less than 30.2 million , driven by growth in self-employment.

The yen fell against the U.S. dollar . Impact on the dynamics of the data provided by Japan, as well as words BOJ board member Takahide Kiut . Report submitted to the Ministry of Finance of Japan, showed that the trade deficit declined in February to a level of 800.3 billion yen , compared with 2.8 trillion . yen in January. Deficit reduction occurred on the background of accelerating export growth and weakening imports. However, experts expect further reduction - up to 600 billion yen. Add that captures Japan 's trade deficit for 20 consecutive months ( the longest period since 1979 ) . Meanwhile, it became known that the growth rate of imports in the country in February slowed to 9% from 25.1 % in January , as export growth accelerated to 9.8% from 9.5% .

With regard to the Kiut , he warned that if the Central Bank will forever campaign to mitigate the monetary policy or to undertake additional mitigation measures , it can give rise to adverse effects on the markets .

EUR / USD: during the European session, the pair fell to $ 1.3914 , after recovering slightly

GBP / USD: during the European session, the pair rose to $ 1.6640

USD / JPY: during the European session, the pair rose to Y101.70, but then declined slightly

At 18:00 GMT the economic outlook released on FOMC, and will be known FOMC decision on the basic interest rate. Also accompanying statement will be presented FOMC. At 18:30 GMT the United States will be a press conference FOMC. At 21:45 GMT New Zealand declares to the change in GDP for the 4th quarter.

-

12:59

Orders

EUR/USD

Offers $1.4000, $1.3967/75, $1.3945/50

Bids $1.3875/80, $1.3820/30, $1.3770/60, $1.3710/00

GBP/USD

Offers $1.6785, $1.6740, $1.6720/25, $1.6665/70

Bids $1.6545, $1.6510/00, $1.6485

AUD/USD

Offers $0.9200, $0.9165, $0.9150, $0.9140

Bids $0.9060/70, $0.9000/10, $0.8950, $0.8910/00

EUR/JPY

Offers Y142.90/00, Y142.50, Y142.00

Bids Y140.75 Y140.45/50, Y140.00, Y139.50

USD/JPY

Offers Y103.00, Y102.50/55, Y102.00

Bids Y101.20, Y101.00, Y100.50

EUR/GBP

Offers stg0.8470, stg0.8415/20, stg0.8405

Bids stg0.8360, stg0.8335/40, stg0.8320/15, stg0.8280/75

-

12:30

U.S.: Current account, bln, Quarter IV -81.12 (forecast -88.0)

-

12:30

Canada: Wholesale Sales, m/m, January +0.8% (forecast +1.2%)

-

11:30

Major stock indexes in Europe grow

European stocks rose slightly , extending its two-day series , as investors awaited the statement from the Federal Reserve System. U.S. index futures were little changed , while Asian shares fell .

Note that today completed the first session of the U.S. Federal Reserve under the leadership of its new Chairman Janet Yellen . According to many forecasts , the March meeting should not bring surprises. Most investors and market participants are prepared for the next announcement of reductions of asset purchases by the U.S. Federal Reserve. It is expected that the Fed will lower the amount of incentive programs by $ 10 billion Thus , the total amount of monthly purchases of assets drop from $ 65 billion to $ 55 billion

In favor of further reducing incentives say the comments by officials of the Federal Open Market Committee , which have been made in advance of the two-day meeting . Fed satisfied with the current state of the U.S. economy. Moreover, Yellen hinted that will stay the course to reduce incentives.

Stoxx Europe 600 index rose 0.1 percent . Sensor decreased by 2.9 percent this month amid confrontation between Russia and the West over the Crimea.

Cost Inditex rose 4 percent after the owner of the Zara chain stores reported that the results of 2013 profit was 2.38 billion euros ($ 3310 million ) , compared with the average analyst forecast at 2.39 billion euros . The Spanish company also noted that net profit was in the amount of 703 million euros, compared with estimates at around 716.6 million euros.

Brenntag shares rose 1.5 percent , following a statement that will be invited to a stock split at the annual general meeting to be held on June 17. The world's largest distributor of chemicals also recommended a dividend of 2.60 euros per share, beating estimates at 2.40 euros.

Cost HeidelbergCement AG dropped 2.3 percent after saying its net debt by December 31, 2013 rose to 7.5 billion euros. The average analyst estimate was at 7.2 billion euros. We also add that the third -largest cement producer, forecast an increase in sales and operating profit in 2014.

At the current moment

FTSE 100 6,596.2 -9.08 -0.14%

CAC 40 4,314.08 +0.82 +0.02 %

DAX 9,279.72 +37.17 +0.40%

-

10:00

Eurozone: Construction Output, m/m, January +1.5% (forecast +1.8%)

-

10:00

Eurozone: Construction Output, y/y, January +8.8%

-

10:00

Switzerland: Credit Suisse ZEW Survey (Expectations), March 19.0 (forecast 25.0)

-

09:45

Option expiries for today's 1400GMT cut

USD/JPY Y101.00, Y101.25, Y101.50, Y101.85, Y101.95, Y102.00, Y102.15-25, Y102.70, Y103.00

EUR/JPY Y142.00

EUR/USD $1.3790, $1.3800, $1.3815, $1.3860, $1.3900, $1.3915, $1.3920, $1.3960, $1.4010

GBP/USD $1.6650, $1.6675, $1.6695, $1.6700, $1.6900

EUR/GBP stg0.8300

AUD/USD $0.9000, $0.9050, $0.9100-10, $0.9150

NZD/USD $0.8350, $0.8400

USD/CAD C$1.1000, C$1.1025, C$1.1040, C$1.1070, C$1.1085, C$1.1125, C$1.1140, C$1.1150, C$1.1180, C$1.1200, C$1.1225, C$1.1235,

C$1.1250

-

09:31

United Kingdom: Average Earnings, 3m/y , January +1.4% (forecast +1.3%)

-

09:30

United Kingdom: ILO Unemployment Rate, January 7.2% (forecast 7.2%)

-

09:30

United Kingdom: Claimant count , February -34.6 (forecast -23.3)

-

09:30

United Kingdom: Average earnings ex bonuses, 3 m/y, January +1.3% (forecast +1.2%)

-

09:23

Asia Pacific stocks close

Asia’s benchmark stock gauge fluctuated as investors weighed company earnings and awaited the Federal Reserve’s policy statement.

Nikkei 225 14,462.52 +51.25 +0.36%

S&P/ASX 200 5,355.6 +11.03 +0.21%

Shanghai Composite 2,021.73 -3.46 -0.17%

Kingsoft Corp. jumped 7.6 percent to head for a record close in Hong Kong after the computer-software maker posted earnings that beat estimates, while instant noodle-maker Uni-President China Holdings Ltd. slumped 8 percent after its 2013 profit missed projections.

Country Garden Holdings Co. slid 3.4 percent in Hong Kong after the Chinese developer’s chief financial officer resigned.

Fanuc Corp. rose 3.2 percent in Tokyo after Credit Suisse Group AG said it’s a good time to buy the industrial-robot manufacturer’s shares.

-

08:42

FTSE 100 6,591.05 -14.23 -0.22%, CAC 40 4,306.52 -6.74 -0.16%, Xetra DAX 9,247.43 +4.88 +0.05%

-

06:40

European bourses are initially seen trading a narrowly mixed Wednesday: the FTSE is seen up 0.2%, the DAX flat and the CAC down 0.1%.

-

06:23

Asian session: The dollar was near a four-month low

04:30 Japan All Industry Activity Index, m/m January -0.1% +1.3% +1.0%

05:00 Japan BOJ Governor Haruhiko Kuroda Speaks

The dollar was near a four-month low against its peers amid bets the Federal Reserve will drop its jobless-rate threshold today and adopt qualitative guidance for signaling when it will raise interest rates. The Federal Open Market Committee will conclude its first meeting today after Janet Yellen succeeded Ben S. Bernanke as chair last month. The central bank will probably scrap its 6.5 percent jobless-rate threshold in favor of qualitative guidance for signaling when it will consider raising the benchmark interest rate, according to a Bloomberg News survey of economists. The unemployment rate was at 6.7 percent in February, near the lowest since October 2008.

Traders’ expectations of future currency swings remained near the lowest since 2012 after President Vladimir Putin said Russia isn’t seeking to split Ukraine further following the secession of its Crimea region. Putin yesterday told Russian lawmakers not to believe “those who scare you with Russia, who yell that Crimea will be followed by other regions.” While he said Russia doesn’t plan to further split up Ukraine, Putin underscored his right to defend Russian speakers in Ukraine’s east.

China’s currency completed the biggest three-day loss yesterday since at least 2007 amid concern financial risk is increasing.

EUR / USD: during the Asian session the pair fell to $ 1.3920

GBP / USD: during the Asian session, the pair traded in the range of $ 1.6585-05

USD / JPY: on Asian session the pair traded in the range of Y101.25-50

The European session could be dominated by the UK data calendar and the UK 2014/15 Budget statement. The European calendar gets underway at 0745GMT, with the release of the French current account balance for January. EMU data set for release at 1000GMT includes the fourth quarter labour costs and the January construction output data. At 1500GMT, German Chancellor Angela Merkel will deliver a speech and take part in a conference discussion in Berlin. At 1700GMT, SNB Chairman Thomas Jordan will deliver a speech on moral hazard, in Bern, Switzerland. Sovereign issuance on Wednesday sees Germany re-open its 10-year benchmark 1.75% Feb 2024 Bund for up to E4bln. Across the Atlantic, the US calendar gets underway at 1100GMT, with the release of the MBA Mortgage Index for the March 14 week. The fourth quarter US current account data will follow at 1230GMT. Canadian data due at 1230GMT includes the release of the January Wholesale sales numbers. The EIA Crude Oil Stocks for the March 14 week will be published at 1430GMT. The highlight of the day comes at 1800GMT, when the FOMC announces the latest policy announcement, to be followed at 1830GMT by Fed Chair Janet Yellen's first post meet press conference.

-