Notícias do Mercado

-

23:30

Japan: National Consumer Price Index, y/y, October 1.4% (forecast 1.4%)

-

23:30

Japan: National CPI Ex-Fresh Food, y/y, October 1% (forecast 1%)

-

23:30

Schedule for today, Thursday, November 22, 2018

Time Country Event Period Previous value Forecast 00:00 U.S. Bank holiday 12:30 Eurozone ECB Monetary Policy Meeting Accounts 14:45 Canada Gov Council Member Wilkins Speaks 15:00 Eurozone Consumer Confidence November -2.7 -3.0 15:30 Canada Bank of Canada publishes financial system review 17:00 Eurozone ECB's Yves Mersch Speaks 20:55 United Kingdom MPC Member Saunders Speaks -

21:45

New Zealand: Visitor Arrivals, October 4.8%

-

21:17

Major US stock indexes finished trading mostly in positive territory

Major US stock indices predominantly rose after a two-day sell-off, as strong quarterly results from Foot Locker and growth in the commodity sector improved investor sentiment and compensated for the fall in the utility sector.

In addition, investors analyzed the US data block. The final results of the research, presented by Thomson-Reuters and the Michigan Institute, showed that in November, American consumers felt more pessimistic about the economy than last month. According to the data, in November, the consumer sentiment index fell to 97.5 points compared with the final reading for October of 98.6 points and a preliminary value for November of 98.3 points. Experts predicted that the index will be 98.3 points.

Meanwhile, the National Association of Realtors said that home sales in the secondary market increased by 1.4%, to a seasonally adjusted annual rate of 5.22 million units. Although the latter value was slightly higher than in September (5.15 million units), sales remained 5.1% lower than in October 2017, which is the sharpest 12-month decline since July 2014. Economists had expected home sales to grow to 5.2 million units in October.

Most of the components of DOW finished trading in positive territory (16 of 30). The growth leader was NIKE, Inc. (NKE, + 1.93%). Johnson & Johnson (JNJ, -3.06%) was an outsider.

Almost all sectors of the S & P recorded an increase. The commodity sector grew the most (+ 2.0%). Decline shows only the utilities sector (-0.9%)

Index Change, points Closed Change, % Dow Jones -0.95 24464.69 0 S&P 500 8.04 2649.93 0.3 NASDAQ Composite 63.43 6972.25 0.92 -

20:50

Schedule for tomorrow, Thursday, November 22, 2018

Time Country Event Period Previous value Forecast 00:00 U.S. Bank holiday 12:30 Eurozone ECB Monetary Policy Meeting Accounts 14:45 Canada Gov Council Member Wilkins Speaks 15:00 Eurozone Consumer Confidence November -2.7 -3.0 15:30 Canada Bank of Canada publishes financial system review 17:00 Eurozone ECB's Yves Mersch Speaks 20:55 United Kingdom MPC Member Saunders Speaks -

20:01

DJIA +0.58% 24,607.55 +141.91 Nasdaq +1.36% 7,002.95 +94.13 S&P +0.78% 2,662.46 +20.57

-

17:01

European stocks closed: FTSE 100 +102.31 7050.23 +1.47% DAX +177.76 11244.17 +1.61% CAC 40 +50.61 4975.50 +1.03%

-

15:30

U.S.: Crude Oil Inventories, November 4.851 (forecast 3.182)

-

15:00

U.S.: Leading Indicators , October 0.1% (forecast 0.1%)

-

15:00

U.S.: Reuters/Michigan Consumer Sentiment Index, November 97.5 (forecast 98.3)

-

15:00

U.S.: Existing Home Sales , October 5.22 (forecast 5.2)

-

14:34

U.S. Stocks open: Dow +0.63%, Nasdaq +1.43%, S&P +0.75%

-

14:23

Before the bell: S&P futures +0.73%, NASDAQ futures +1.18%

U.S. stock-index futures rose on Wednesday, correcting after a massive two-day selloff, which pushed the S&P 500 and the Dow Jones Industrial Average in the red for the year.

Global Stocks:

Index/commodity

Last

Today's Change, points

Today's Change, %

Nikkei

21,507.54

-75.58

-0.35%

Hang Seng

25,971.47

+131.13

+0.51%

Shanghai

2,651.51

+5.65

+0.21%

S&P/ASX

5,642.80

-29.00

-0.51%

FTSE

7,021.22

+73.30

+1.05%

CAC

4,947.85

+22.96

+0.47%

DAX

11,163.82

+97.41

+0.88%

Crude

$54.63

+2.25%

Gold

$1,226.50

+0.43%

-

13:46

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

3M Co

MMM

200.23

1.08(0.54%)

2911

ALCOA INC.

AA

33.25

0.57(1.74%)

2450

ALTRIA GROUP INC.

MO

55.89

0.26(0.47%)

578

Amazon.com Inc., NASDAQ

AMZN

1,530.00

34.54(2.31%)

73400

Apple Inc.

AAPL

178.93

1.95(1.10%)

656510

AT&T Inc

T

29.65

0.23(0.78%)

102397

Barrick Gold Corporation, NYSE

ABX

13.25

0.22(1.69%)

93109

Boeing Co

BA

323.89

6.19(1.95%)

28087

Caterpillar Inc

CAT

123.01

0.74(0.61%)

15909

Chevron Corp

CVX

117.1

1.00(0.86%)

9988

Cisco Systems Inc

CSCO

44.8

0.31(0.70%)

16920

Citigroup Inc., NYSE

C

63.15

0.62(0.99%)

50881

Deere & Company, NYSE

DE

134.34

-4.18(-3.02%)

39559

Exxon Mobil Corp

XOM

77.65

0.68(0.88%)

4827

Facebook, Inc.

FB

134.09

1.66(1.25%)

166329

Ford Motor Co.

F

9.15

0.09(0.99%)

11486

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

11.18

0.30(2.76%)

12593

General Electric Co

GE

7.78

0.13(1.70%)

954536

Goldman Sachs

GS

192

0.66(0.34%)

32812

Google Inc.

GOOG

1,035.00

9.24(0.90%)

6968

Home Depot Inc

HD

172

2.95(1.75%)

4214

Intel Corp

INTC

47.91

0.52(1.10%)

64023

International Business Machines Co...

IBM

117.75

0.55(0.47%)

10450

Johnson & Johnson

JNJ

145.85

-0.60(-0.41%)

2043

JPMorgan Chase and Co

JPM

109

0.55(0.51%)

18669

McDonald's Corp

MCD

184.22

0.51(0.28%)

3214

Merck & Co Inc

MRK

74.9

0.12(0.16%)

1447

Microsoft Corp

MSFT

102.95

1.24(1.22%)

136250

Nike

NKE

72.24

1.12(1.57%)

5823

Pfizer Inc

PFE

43.65

0.12(0.28%)

4748

Procter & Gamble Co

PG

91.65

-0.45(-0.49%)

3381

Starbucks Corporation, NASDAQ

SBUX

67.4

0.22(0.33%)

9423

Tesla Motors, Inc., NASDAQ

TSLA

352.49

5.00(1.44%)

59399

The Coca-Cola Co

KO

49.58

0.20(0.41%)

3212

Twitter, Inc., NYSE

TWTR

31.45

0.39(1.26%)

34812

UnitedHealth Group Inc

UNH

263.01

1.51(0.58%)

1701

Verizon Communications Inc

VZ

59.8

0.34(0.57%)

5418

Visa

V

135.09

1.72(1.29%)

18229

Wal-Mart Stores Inc

WMT

94.57

0.41(0.44%)

7903

Walt Disney Co

DIS

112.6

0.73(0.65%)

8199

Yandex N.V., NASDAQ

YNDX

28.84

0.99(3.55%)

1957

-

13:44

Analyst coverage resumption before the market open

Yandex N.V. (YNDX) initiated with a Buy at Jefferies

-

13:43

Downgrades before the market open

Goldman Sachs (GS) downgraded to Equal-Weight from Overweight at Morgan Stanley

-

13:39

U.S initial jobless claims higher than expected last week

In the week ending November 17, the advance figure for seasonally adjusted initial claims was 224,000, an increase of 3,000 from the previous week's revised level. The previous week's level was revised up by 5,000 from 216,000 to 221,000. The 4-week moving average was 218,500, an increase of 2,000 from the previous week's revised average. The previous week's average was revised up by 1,250 from 215,250 to 216,500.

-

13:37

Canadian wholesale sales declined for a second consecutive month, down 0.5% to $63.2 billion in September

Lower sales were recorded in five of seven subsectors, led by the machinery, equipment and supplies and the personal and household goods subsectors.

In volume terms, wholesale sales declined 0.7%.

In the third quarter, wholesale sales increased 0.6% in current dollars, while constant dollar sales were unchanged. This was the 10th consecutive quarterly increase in current dollars.

In September, lower sales were recorded in five of seven subsectors, which together accounted for 68% of total wholesale sales.

Following two consecutive monthly gains, sales in the machinery, equipment and supplies subsector declined for the second time in 2018, down 2.0% to $13.0 billion in September. Sales declined in three of the four industries, led by the computer and communication equipment and supplies (-3.3%) and the farm, lawn and garden machinery and equipment (-6.4%) industries.

-

13:35

U.S durable goods in October decreased $11.5 billion or 4.4 percent to $248.5 billion

New orders for manufactured durable goods in October decreased $11.5 billion or 4.4 percent to $248.5 billion, the U.S. Census Bureau announced today. This decrease, down three of the last four months, followed a 0.1 percent September decrease. Excluding transportation, new orders increased 0.1 percent. Excluding defense, new orders decreased 1.2 percent. Transportation equipment, down following two consecutive monthly increases, drove the decrease, $11.7 billion or 12.2 percent to $84.7 billion.

-

13:30

U.S.: Continuing Jobless Claims, November 1668 (forecast 1635)

-

13:30

U.S.: Initial Jobless Claims, November 224 (forecast 215)

-

13:30

U.S.: Durable goods orders ex defense, October -1.2% (forecast 0.1%)

-

13:30

U.S.: Durable Goods Orders ex Transportation , October 0.1% (forecast 0.4%)

-

13:30

U.S.: Durable Goods Orders , October -4.4% (forecast -2.5%)

-

13:30

Canada: Wholesale Sales, m/m, September -0.5% (forecast 0.3%)

-

12:37

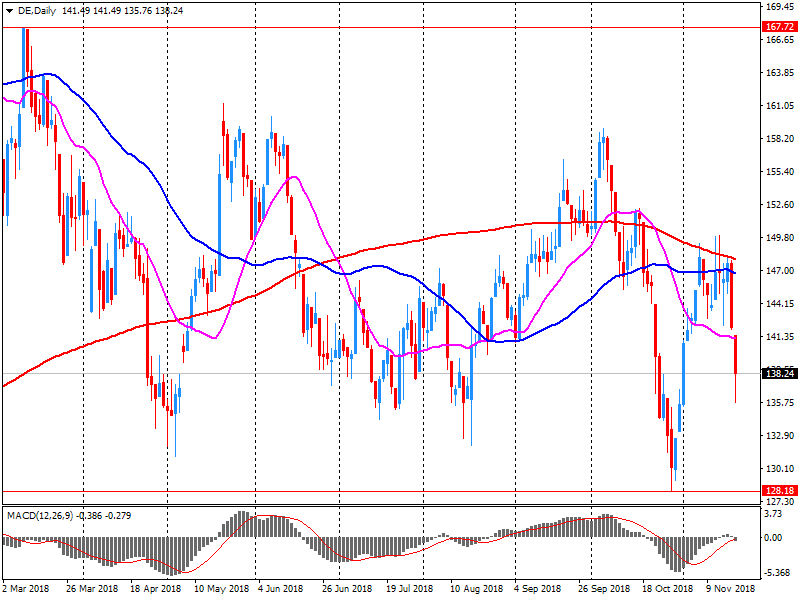

Company News: Deere (DE) quarterly results miss analysts’ forecasts

Deere (DE) reported Q4 FY 2018 earnings of $2.30 per share (versus $1.57 in Q4 FY 2017), missing analysts’ consensus estimate of $2.45.

The company’s quarterly revenues amounted to $8.343 bln (+17.6% y/y), missing analysts’ consensus estimate of $8.586 bln.

DE fell to $133.55 (-3.59%) in pre-market trading.

-

11:20

Growth forecasts for next year have been revised down for most of the world’s major economies - OECD

Global GDP is now expected to expand by 3.5% in 2019, compared with the 3.7% forecast in last May’s Outlook, and by 3.5% in 2020.

In many countries, unemployment is at record lows and labour shortages are beginning to emerge. But rising risks could undermine the projected soft landing from the slowdown. Trade growth and investment have been slackening on the back of tariff hikes. Higher interest rates and an appreciating US dollar have resulted in an outflow of capital from emerging economies and are weakening their currencies. Monetary and fiscal stimulus is being withdrawn progressively in the OECD area.

The shakier outlook in 2019 reflects deteriorating prospects, principally in emerging markets such as Turkey, Argentina and Brazil, while the further slowdown in 2020 is more a reflection of developments in advanced economies as slower trade and lower fiscal and monetary support take their toll.

-

11:19

German Federal Government Spokesman: Federal Government Sees No Possibility For New Negotiations Of Brexit Deal @LiveSquawk

-

11:19

EU commission says disciplinary procedure should be adopted against Italy for excessive debt - ANSA news agency

Italy’s Salvini: 2.4Pct Deficit Target Cannot Be Discussed

-

09:37

UK public sector net borrowing (excluding public sector banks) in October 2018 was £8.8 billion, £1.6 billion more than in October 2017

Borrowing (Public sector net borrowing excluding public sector banks) in October 2018 was £8.8 billion, £1.6 billion more than in October 2017; this was the highest October borrowing for three years (since 2015).

Borrowing in the current financial year-to-date (YTD) was £26.7 billion: £11.2 billion less than in the same period in 2017; the lowest year-to-date for 13 years (since 2005).

On 29 October 2018, the Office for Budget Responsibility (OBR) revised their official forecast of borrowing for the financial year ending (FYE) March 2019 down by £11.6 billion to £25.5 billion.

Borrowing in the FYE March 2018 was £40.1 billion: £5.5 billion less than in FYE March 2017; the lowest financial year for 11 years (since FYE 2007).

Debt (Public sector net debt excluding public sector banks) at the end of October 2018 was £1,791.6 billion (or 84.0% of gross domestic product (GDP)); an increase of £1.9 billion (or a decrease of 2.7 percentage points) on October 2017.

-

09:30

United Kingdom: PSNB, bln, October -7.956

-

08:50

FTSE +24.04 6971.96 +0.35% DAX +86.50 11152.91 +0.78% CAC +23.38 4948.27 +0.48%

-

08:35

The pound is likely to be volatile on Wednesday as U.K. Prime Minister Theresa May heads to Brussels says ING

The pound is likely to be volatile on Wednesday as U.K. Prime Minister Theresa May heads to Brussels. "More noise [is] expected," ING says. "Speculation that May can renegotiate her withdrawal agreement with Brussels looks misplaced and instead her trip today is all about writing the nonbinding political declaration that will accompany the exit," ING adds. Sterling is slightly higher at $1.2797, but EUR/GBP is up by 0.1% at 0.8899. "Slightly favor EUR/GBP lower on euro travails, but a very uncertain picture," says the Dutch bank - via WSJ

-

07:55

Options levels on wednesday, November 21, 2018

EUR/USD

Resistance levels (open interest**, contracts)

$1.1470 (2292)

$1.1448 (2528)

$1.1431 (920)

Price at time of writing this review: $1.1396

Support levels (open interest**, contracts):

$1.1359 (4458)

$1.1343 (3431)

$1.1330 (2292)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date December, 7 is 125279 contracts (according to data from November, 20) with the maximum number of contracts with strike price $1,1200 (5896);

GBP/USD

Resistance levels (open interest**, contracts)

$1.2970 (1255)

$1.2946 (579)

$1.2925 (647)

Price at time of writing this review: $1.2809

Support levels (open interest**, contracts):

$1.2764 (1820)

$1.2740 (2505)

$1.2723 (2836)

Comments:

- Overall open interest on the CALL options with the expiration date December, 7 is 58132 contracts, with the maximum number of contracts with strike price $1,3500 (4790);

- Overall open interest on the PUT options with the expiration date December, 7 is 48338 contracts, with the maximum number of contracts with strike price $1,2500 (4397);

- The ratio of PUT/CALL was 0.83 versus 0.83 from the previous trading day according to data from November, 20

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

07:33

German Bund yields trade slightly higher early Wednesday, indicating an ease in risk aversion, but sentiment remains shaky ahead of the European Commission's opinion on member states' budget plans - ING

"All eyes obviously are on the opinion on Italy, with a likely negative verdict seen as paving the way for the launch of an excessive deficit procedure".

-

07:31

Futures: DAX + 0.6% FTSE + 0.2% CAC + 0.5%

A positive start to trading on the stock markets in Europe is expected, due to a rebound in Asian trading and a positive start to the day seen in US stock futures. The improvement in risk sentiment observed in stock markets push the dollar lower.

-

07:18

Treasury yields held their ground on Tuesday eve as stocks across the world came under pressure, prompted by concerns over a persistent decline in once-highflying U.S. tech companies and waning global growth

The 10-year Treasury note yield was down 0.9 basis point to 3.050%, after it touched a six-week low on Monday. The 30-year bond yield fell 1.2 basis point to 3.305%, while the 2-year note yield was up 1.2 basis points to 2.798%

-

07:14

Facebook CEO Zuckerberg: Stepping Down as Chairman Is 'Not the Plan'

I Hope to Work With Sheryl Sandberg for Decades More to Come

-

07:13

Trump says United States intends to remain steadfast partner of Saudi Arabia to ensure interests of US, Israel and regional partners - statement: RTRS

-

07:10

Italy's Salvini May Be Open To Budget Revisions - Stampa

Italy's Tria Said He's 'Concerned' About Bond Spread

-

04:31

Japan: All Industry Activity Index, m/m, September -0.9% (forecast -0.8%)

-

00:45

Commodities. Daily history for Tuesday, November 20, 2018:

Raw materials Closed Change, % Brent 62.58 -6.65 -

00:30

Stocks. Daily history for Tuesday, November 20, 2018:

Index Change, points Closed Change, % NIKKEI 225 -238.04 21583.12 -1.09 Hang Seng -531.66 25840.34 -2.02 KOSPI -17.98 2082.58 -0.86 ASX 200 -21.9 5671.8 -0.38 DAX -178.13 11066.41 -1.58 Dow Jones -551.8 24465.64 -2.21 S&P 500 -48.84 2641.89 -1.82 NASDAQ Composite -119.66 6908.82 -1.7 -

00:15

Currencies. Daily history for Tuesday, November 20, 2018:

Pare Closed Change, % AUDUSD 0.7214 -1.08 EURJPY 128.219 -0.53 EURUSD 1.13701 -0.72 GBPJPY 144.169 -0.32 GBPUSD 1.27856 -0.5 NZDUSD 0.67906 -0.67 USDCAD 1.33075 1.05 USDCHF 0.99481 0.13 USDJPY 112.738 0.18 -