Market news

-

22:28

Currencies. Daily history for Oct 20’2016:

(pare/closed(GMT +3)/change, %)

EUR/USD $1,0924 -0,45%

GBP/USD $1,2250 -0,29%

USD/CHF Chf0,9928 +0,40%

USD/JPY Y103,96 +0,56%

EUR/JPY Y113,57 +0,11%

GBP/JPY Y127,34 +0,27%

AUD/USD $0,7624 -1,22%

NZD/USD $0,7188 -0,54%

USD/CAD C$1,323 +0,82%

-

22:00

Schedule for today, Friday, Oct 21’2016

08:30 United Kingdom PSNB, bln September -10.05 -8.5

12:30 Canada Retail Sales, m/m August -0.1% 0.2%

12:30 Canada Retail Sales YoY August 2.3%

12:30 Canada Retail Sales ex Autos, m/m August -0.1% 0.3%

12:30 Canada Consumer Price Index m / m September -0.2% 0.2%

12:30 Canada Consumer price index, y/y September 1.1% 1.5%

12:30 Canada Bank of Canada Consumer Price Index Core, y/y September 1.8% 1.8%

14:00 Eurozone Consumer Confidence (Preliminary) October -8.2 -8

-

21:45

New Zealand: Visitor Arrivals, September 13%

-

14:29

US leading economic index resumed its increase in September

The index of leading economic indicators from the Conference Board increased by 0.2 percent in September to 124.4 (2010 = 100), after falling 0.2 percent in August, as well as increasing by 0.5 percent in July. Last change coincided with forecasts.

-

14:05

US Existing-home sales rebounded strongly in September

Existing-home sales rebounded strongly in September and were propelled by sales from first-time buyers reaching a 34 percent share, which is a high not seen in over four years, according to the National Association of Realtors. All major regions saw an increase in closings last month, and distressed sales fell to a new low of 4 percent of the market.

Total existing-home sales 1, which are completed transactions that include single-family homes, townhomes, condominiums and co-ops, hiked 3.2 percent to a seasonally adjusted annual rate of 5.47 million in September from a downwardly revised 5.30 million in August. After last month's gain, sales are at their highest pace since June (5.57 million) and are 0.6 percent above a year ago (5.44 million).

-

14:00

U.S.: Existing Home Sales , September 5.47 (forecast 5.35)

-

14:00

U.S.: Leading Indicators , September 0.2% (forecast 0.2%)

-

13:50

Option expiries for today's 10:00 ET NY cut

EURUSD 1.0900 (EUR 1.46bln) 1.0948-50 (438m) 1.0955 (476m) 1.1000 (1.21bln) 1.1050-53 (1.-6bln) 1.1155-60 (1.08bln)

GBPUSD 1.2235 (GBP 245m)

USDJPY 101.68-69 (USD 1.27bln) 103.00 (1.26bln) 103.50-55 (630m) 104.00 (930m)104.50 (1.13bln)

EURJPY: 113.45 ( EUR 235m)

EURGBP 0.8850 (EUR 201m)

EURCHF 1.0800 (EUR 370m)

AUDUSD 0.7400 (AUD 595m) 0.7500 (1.37bln) 0.7600 (429m) 0.7675 (347m) 0.7700 (457m)

USDCAD: 1.3100 (305m) 1.3150 (335m) 1.3200 (242m)

NZDUSD 0.7305-10 (NZD 565m)

EURAUD 1.4200 (EUR 345m) 1.4500 (245m)

-

13:28

-

12:52

-

12:51

Draghi: December Decisions Will Define Policy Environment for Coming Months

-

12:45

Draghi: No Discussion of Extending QE. EUR/USD moves higher

-

12:41

US unemployment claims below 300K but above expectations

In the week ending October 15, the advance figure for seasonally adjusted initial claims was 260,000, an increase of 13,000 from the previous week's revised level. The previous week's level was revised up by 1,000 from 246,000 to 247,000. The 4-week moving average was 251,750, an increase of 2,250 from the previous week's revised average. The previous week's average was revised up by 250 from 249,250 to 249,500.

There were no special factors impacting this week's initial claims. This marks 85 consecutive weeks of initial claims below 300,000, the longest streak since 1970.

-

12:38

Draghi: Inflation to Pick Up Over Next Couple of Months

-

12:34

Draghi: Economy Has Shown Resilience

-

Data Point to Continued Growth

-

Low Oil Prices Provide Additional Support for Households

-

Domestic Demand Should be Supported by Policy

-

In Dec ECB will have new staff projections through to 2019

-

Council will review the committees work on QE in Dec

-

Data suggests Q3 will be similar to Q3

-

Investment should be supported by favourable financing conditions

-

EZ economy expected to be dampened by export demand

-

-

12:33

US regional manufacturing conditions continued to improve

Results from the October Manufacturing Business Outlook Survey suggest that regional manufacturing conditions continued to improve. Indexes for general activity, new orders, and shipments were all positive this month. But firms reported continued weakness in overall labor market conditions. Firms expect continued growth for manufacturing over the next six months and are becoming more optimistic about employment expansion.

The index for current manufacturing activity in the region edged down, from a reading of 12.8 in September to 9.7 this month. The index has now been positive for three consecutive months (see Chart 1). Other broad indicators showed notable improvement. The new orders index improved markedly this month, increasing from 1.4 in September to 16.3 in October. The percentage of firms reporting increases in new orders this month rose to 40 percent from 30 percent last month. The current shipments index also improved, rising 24 points to 15.3. The delivery times, unfilled orders, and inventories indexes remained weak, however, with all registering negative readings, although they were less negative than in September.

-

12:31

U.S.: Philadelphia Fed Manufacturing Survey, October 9.7 (forecast 5.3)

-

12:30

U.S.: Initial Jobless Claims, 260 (forecast 250)

-

12:30

U.S.: Continuing Jobless Claims, 2057 (forecast 2050)

-

12:02

Orders

EUR/USD

Offers 1.0980 1.1000 1.1025-30 1.1055 1.1070 1.1085 1.1100-05 1.1130 1.1150

Bids 1.0950 1.0920 1.0900 1.0880 1.0850 1.0830 1.0800

GBP/USD

Offers 1.2300 1.2325-30 1.2350 1.2380 1.2400 1.2430 1.2450

Bids 1.2250 1.2220 1.2200 1.2185 1.2165 1.2145-50 1.2130 1.2100

EUR/GBP

Offers 0.8955 0.8975-80 0.9000 0.9030-35 0.9050

Bids 0.8920 0.8900-05 0.8870 0.8850-55 0.8830 0.8800

EUR/JPY

Offers 114.00 114.20 114.70-75 115.00 115.50 115.80 116.00

Bids 113.50 113.00 112.60 112.00 111.85 111.50 111.00

USD/JPY

Offers 103.85 104.00 104.25-30 104.50 104.80 105.00

Bids 103.50 103.20-25 103.00 102.85 102.50 102.30 102.00

AUD/USD

Offers 0.7685 0.7700 0.7730-35 0.7755-60 0.7800

Bids 0.7650 0.7625-30 0.7600 0.7580 0.7550 0.7500

-

11:47

No change for ECB interest rates

"At today's meeting the Governing Council of the ECB decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council continues to expect the key ECB interest rates to remain at present or lower levels for an extended period of time, and well past the horizon of the net asset purchases.

Regarding non-standard monetary policy measures, the Governing Council confirms that the monthly asset purchases of €80 billion are intended to run until the end of March 2017, or beyond, if necessary, and in any case until it sees a sustained adjustment in the path of inflation consistent with its inflation aim.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:30 CET today".

-

11:45

Eurozone: ECB Interest Rate Decision, 0.0% (forecast 0.0%)

-

09:54

Bundesbank, Dombret: EU should not take a stance of punishing the UK in Brexit negotiations

-

09:29

Bundesbank Official Rebukes U.K. Government Over Central-Bank Meddling

-

08:32

UK retail sales flat in September

In September 2016, the quantity bought (volume) of retail sales is estimated to have increased by 4.1% compared with September 2015; all store types except textile, clothing and footwear stores showed growth with the largest contribution coming from non-store retailing.

There was no change in the quantity bought compared with August 2016; decreases in food stores, other stores and textile, clothing and footwear stores were offset by increases in department stores, household goods stores and non-store retailers.

The underlying pattern in the retail sector continues to show relatively strong growth with the 3 month on 3 month movement in the quantity bought increasing by 1.8%.

-

08:30

United Kingdom: Retail Sales (MoM), September 0% (forecast 0.4%)

-

08:30

United Kingdom: Retail Sales (YoY) , September 4.1% (forecast 4.8%)

-

08:22

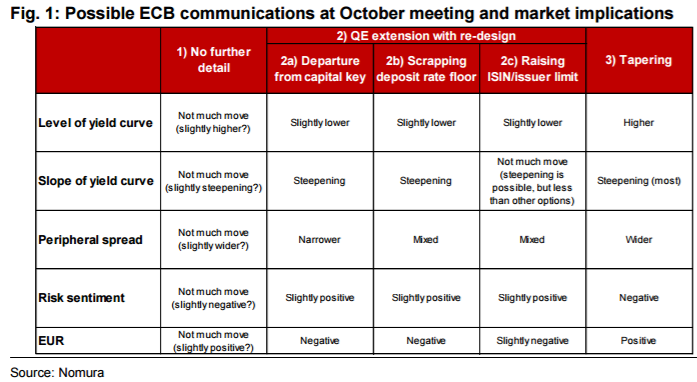

How Will EUR React at ECB? - Nomura

"Market expectations for an immediate policy change by the ECB are muted as we approach the meeting this week. Recent euro area economic data show the resilience of the economy, and a rate cut looks unlikely for now. Expectations of a rate cut into the meeting this week are fairly muted in the rates market.

The October meeting can be still important for the FX market, as markets are waiting for clarification on the future of the QE programme. We do not expect the ECB to make any final decisions on the QE programme this week, but any suggestions as to the likely path of the QE at the press conference could influence the euro area yield curve. FX market interest in the possibility of further bond sell-offs is rising, and the ECB's policy stance can influence the broader FX market, not only EUR.

Five possibilities: This week the ECB may communicate: 1) no details as to the future path of QE, 2) indications about extending QE further, or 3) indications of approaching tapering.

Then, if the ECB is inclined to extend the QE further, we see three likely options for the Bank to enable the extension: 2a)departure from the capital key, 2b) removal of the deposit rate floor, and 2c) increase in ISIN/issuer limits.

Conclusion: We believe the ECB's next step will be to extend its QE programme, not to taper it, and stronger indications of a QE extension would keep EUR/USD depreciating at its current pace.

Curve steepening is possible, but steepening owing to a QE extension would probably not cause a negative reaction in risk sentiment, which would enable USD/JPY to maintain its recent appreciation trend too. If ECB communication further increases market concerns about near-term tapering, the curve could steepen and risk sentiment deteriorate. This would challenge the recent trend of EUR/USD depreciation and USD/JPY appreciation. It is possible that the ECB does not offer any further details as to the future of QE, which would lead to muted reactions in the FX market. Under that scenario, comments by ECB officials and possible media leaks regarding the future of the QE programme, beyond the meeting next week, could increase EUR volatility into the December meeting.

As we expect the ECB to choose to extend the QE programme in the end, we judge EUR/USD downside risk is higher into the December ECB/Fed meetings".

Copyright © 2016 Nomura, eFXnews™

-

08:03

Euro Area current account improves in August

The current account of the euro area recorded a surplus of €29.7 billion in August 2016. This reflected surpluses for goods (€30.9 billion), services (€4.8 billion) and primary income (€6.6 billion), which were partly offset by a deficit in secondary income (€12.6 billion).

The 12-month cumulated current account for the period ending in August 2016 recorded a surplus of €350.0 billion (3.3% of euro area GDP), compared with one of €317.0 billion (3.1% of euro area GDP) for the 12 months to August 2015. This development was mostly due to an increase in the surplus for goods (from €327.7 billion to €372.7 billion), as well as a decrease in the deficit for secondary income (from €134.4 billion to €123.6 billion). These were partly offset by decreases in the surpluses for services (from €65.4 billion to €56.5 billion) and primary income (from €58.3 billion to €44.4 billion).

-

08:00

Eurozone: Current account, unadjusted, bln , August 23.6

-

07:44

Option expiries for today's 10:00 ET NY cut

EUR/USD 1.0900 (EUR 1.46bln) 1.0948-50 (438m) 1.0955 (476m) 1.1000 (1.21bln) 1.1050-53 (1.-6bln) 1.1155-60 (1.08bln)

GBP/USD 1.2235 (GBP 245m)

USD/JPY 101.68-69 (USD 1.27bln) 103.00 (1.26bln) 103.50-55 (630m) 104.00 (930m) 104.50 (1.13bln)

EUR/JPY: 113.45 ( EUR 235m)

EUR/GBP 0.8850 (EUR 201m)

EUR/CHF 1.0800 (EUR 370m)

AUD/USD 0.7400 (AUD 595m) 0.7500 (1.37bln) 0.7600 (429m) 0.7675 (347m) 0.7700 (457m)

USD/CAD: 1.3100 (305m) 1.3150 (335m) 1.3200 (242m)

NZD/USD 0.7305-10 (NZD 565m)

EUR/AUD 1.4200 (EUR 345m) 1.4500 (245m)

-

07:16

Today’s events

-

At 08:30 GMT Spain will hold an auction of 10-year bonds

-

At 11:45 GMT ECB's decision on interest rate

-

At 12:00 GMT Deputy Governor of the Bank of England Nemat Shafik will deliver a speech

- Day 1 of the EU Economic summit

-

-

06:45

Retail sales to continue better-than-expected UK data? Will it be enough to support the pound?

-

06:43

Asian Shares Rise as Clinton, Trump Largely Ignore Asia

-

06:28

Options levels on thursday, October 20, 2016:

EUR/USD

Resistance levels (open interest**, contracts)

$1.1170 (2474)

$1.1131 (1648)

$1.1070 (915)

Price at time of writing this review: $1.0961

Support levels (open interest**, contracts):

$1.0924 (7365)

$1.0896 (5200)

$1.0863 (2461)

Comments:

- Overall open interest on the CALL options with the expiration date November, 4 is 36344 contracts, with the maximum number of contracts with strike price $1,1300 (3790);

- Overall open interest on the PUT options with the expiration date November, 4 is 43655 contracts, with the maximum number of contracts with strike price $1,1000 (7365);

- The ratio of PUT/CALL was 1.20 versus 1.22 from the previous trading day according to data from October, 19

GBP/USD

Resistance levels (open interest**, contracts)

$1.2504 (1077)

$1.2407 (859)

$1.2312 (1360)

Price at time of writing this review: $1.2273

Support levels (open interest**, contracts):

$1.2191 (912)

$1.2094 (1433)

$1.1996 (684)

Comments:

- Overall open interest on the CALL options with the expiration date November, 4 is 29563 contracts, with the maximum number of contracts with strike price $1,2800 (2101);

- Overall open interest on the PUT options with the expiration date November, 4 is 29737 contracts, with the maximum number of contracts with strike price $1,2300 (1706);

- The ratio of PUT/CALL was 1.01 versus 1.01 from the previous trading day according to data from October, 19

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

06:26

Swiss trade balance surplus above expectations

Between July and September 2016, the exports grew corrected for working days by 8.1% (real terms: + 2.8%) and imports by 7.9% (real terms: + 4.7%). In both approaches, the chemical-pharmaceutical products dominated the development. So these were responsible export side for about 80% of the total additional revenue. The surplus in the trade balance exceeded the first time in a quarter the 10 billion-franc stamp.

-

06:07

Confidence in the business environment of Australia increased in the third quarter

Confidence in the business community of Australia, published by the National Bank of Australia, increased to a value of 5 from 2, after rising in the second quarter. NAB's business confidence report shows the dynamics of the Australian economy as a whole, in the short term. Positive economic growth is positive for the Australian currency.

-

06:03

German producer prices for industrial products fell by 1.4%

In September 2016 the index of producer prices for industrial products fell by 1.4% compared with the corresponding month of the preceding year. In August 2016 the annual rate of change all over had been -1.6%.

Compared with the preceding month August 2016 the overall index fell by 0.2% in September 2016 (-0.1% in August and +0.2% in July).

In September 2016 energy prices decreased by 5.2 % compared with September 2015, prices of intermediate goods fell by 1.2%. In contrast prices of non-durable consumer goods rose by 0.7%, prices of capital goods by 0.6% and prices of durable consumer goods by 1.2%.

The overall index disregarding energy decreased by 0.1% compared with September 2015 and rose by 0.1% compared with August 2016.

-

06:01

Dudley: Government Bailouts of Banks Are No Longer Appropriate

-

There Is Huge Political Support to End Too Big to Fail

-

European, Japanese Banks Can Use Dollar Auctions, Swap Lines

-

European Banks Have Taken Down Their Dollar Books of Business

-

Squeeze on European, Japanese Banks in Dollar Funding Markets 'Not a Problem at This Juncture'

-

We're Making Progress on Insulating Banking System From Large Firm Failures

-

Probability of Big Bank Failure Is Much Lower Today Than It Was a Decade Ago

-

'I Don't Think We Have Any Problems Here in the U.S. in Terms of Monetary Policy Being Politicized'

-

Debate Over Central Bank Policy Being Politicized Is 'Non-Issue' in U.S.

-

Put More Weight On Fed Chair's Speeches Than Other Fed Speakers

-

Some Fed Speakers 'Are More Important Than Others,' Namely The Chair

-

Market Participants Need the Ability to 'Think Along With the Fed'

-

Monetary Policy Transparency Today Is a Lot Better Than it Used to Be

-

Wells Fargo Issues Underscore 'We Have a Lot More Work to Do'

-

-

06:01

Switzerland: Trade Balance, September 437 (forecast 3.27)

-

06:00

Germany: Producer Price Index (MoM), September -0.2% (forecast 0.2%)

-

06:00

Germany: Producer Price Index (YoY), September -1.4% (forecast -1.2%)

-

05:57

EUR/USD Into ECB: Targets For 3 Scenarios - Credit Suisse

"We see three scenarios for the ECB meeting as follows:

1. The ECB is clear and impressively decisive about its easing intentions: we suspect this would be enough to allow for a push towards EURUSD technical support levels around 1.09. If these do break then the natural extension would be to push on towards one-year lows around 1.06 in the weeks ahead, especially if the market is also prepared to price in a resumed Fed tightening cycle with more confidence.

2. The ECB is vague about its likely next actions - this would argue against a near-term range breakout lower for EURUSD, especially if there is any form of squeeze higher in euro area rates. We would expect a move back above 1.10 towards 1.12 in this scenario.

3. The ECB validates the recent speculation in the press about tapering by pointing towards this course of action for 2017: this would likely take EURUSD back towards 1.15 over coming weeks, especially if the market is unsure about the probability of a Fed hike in December. It could also create a virtuous cycle for the currency in that the market may suspect that the ECB anticipates better growth and inflation outcomes and would provide a boost to the many market participants who are looking at the glass as half full for euro area macro performance going into 2017. With oil prices and euro area marketbased inflation expectations on the rise anyway, all it would take would be a relatively positive reaction from European equity markets to more market participants that the worst may be over for the economy and that the need for still-looser monetary policy is much diminished".

Copyright © 2016 Credit Suisse, eFXnews™

-

05:54

Monthly trend employment in Australia increased slightly in September

Monthly trend employment in Australia increased slightly in September 2016, according to figures released by the Australian Bureau of Statistics (ABS) today.

In September 2016, trend employment increased by 3,900 persons to 11,959,500 persons - a monthly growth rate of 0.03 per cent. This is down from the monthly employment growth peak of 0.28 per cent in September 2015. Trend part-time employment growth continued, with an increase of 11,800 persons, while full-time employment decreased by 7,900 persons.

"The latest Labour Force release shows further increases in part-time employment. There are now 130,000 more persons working part-time than in December 2015, while the number working full-time has decreased by 54,100 persons," said the Program Manager of ABS' Labour and Income Branch, Jacqui Jones.

The trend monthly hours worked increased by 2.2 million hours (0.1 per cent), though it is still below the high in December 2015.

The trend unemployment rate decreased slightly (by less than 0.1 percentage points) to 5.6 per cent, and the participation rate decreased 0.1 percentage points but remained steady at 64.7 per cent in rounded terms.

Trend series smooth the more volatile seasonally adjusted estimates and provide the best measure of the underlying behaviour of the labour market.

-

05:52

Fed's Dudley: 25bps hike later this year 'not that big a deal' --Reuters

-

00:35

Australia: NAB Quarterly Business Confidence, Quarter III 5

-

00:30

Australia: Unemployment rate, September 5.6% (forecast 5.7%)

-

00:30

Australia: Changing the number of employed, September -9.8 (forecast 15)

-