Market news

-

23:50

Japan: Industrial Production (MoM) , December 0.5% (forecast 0.3%)

-

23:30

Japan: Household spending Y/Y, December -0.3% (forecast -0.6%)

-

23:30

Japan: Unemployment Rate, December 3.1% (forecast 3.1%)

-

23:24

Currencies. Daily history for Jan 30’2017:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,0693 -0,01%

GBP/USD $1,2483 -0,55%

USD/CHF Chf0,9951 -0,39%

USD/JPY Y113,77 -1,20%

EUR/JPY Y121,65 -1,22%

GBP/JPY Y142,01 -1,75%

AUD/USD $0,7553 +0,08%

NZD/USD $0,7284 +0,32%

USD/CAD C$1,3115 -0,16%

-

23:03

Schedule for today,Tuesday, Jan 31’2017 (GMT0)

00:05 United Kingdom Gfk Consumer Confidence January -7 -8

00:30 Australia National Australia Bank's Business Confidence December 5

00:30 Australia Private Sector Credit, m/m December 0.5%

00:30 Australia Private Sector Credit, y/y December 5.4%

03:00 Japan BoJ Interest Rate Decision -0.1% -0.1%

03:00 Japan BoJ Monetary Policy Statement

05:00 Japan Housing Starts, y/y December 6.7% 8.4%

05:00 Japan Construction Orders, y/y December -6.0%

06:30 France GDP, q/q (Preliminary) Quarter IV 0.2% 0.4%

06:30 France GDP, Y/Y (Preliminary) Quarter IV 1.0%

06:30 Japan BOJ Press Conference

07:00 Germany Retail sales, real adjusted December -1.8% 1%

07:00 Germany Retail sales, real unadjusted, y/y December 3.2%

08:00 Eurozone ECB President Mario Draghi Speaks

08:55 Germany Unemployment Rate s.a. January 6% 6%

08:55 Germany Unemployment Change January -17 -4

09:30 United Kingdom Consumer credit, mln December 1926 1700

09:30 United Kingdom Mortgage Approvals December 67.5 70

10:00 Eurozone GDP (QoQ) (Preliminary) Quarter IV 0.3% 0.5%

10:00 Eurozone GDP (YoY) (Preliminary) Quarter IV 1.7% 1.7%

10:00 Eurozone Harmonized CPI ex EFAT, Y/Y (Preliminary) January 0.9% 0.9%

10:00 Eurozone Harmonized CPI, Y/Y (Preliminary) January 1.1% 1.4%

10:00 Eurozone Unemployment Rate December 9.8% 9.8%

13:30 Canada Industrial Product Price Index, m/m December 0.3%

13:30 Canada Industrial Product Price Index, y/y December 1.4%

13:30 Canada GDP (m/m) November -0.3% 0.3%

14:00 U.S. S&P/Case-Shiller Home Price Indices, y/y November 5.1%

14:45 U.S. Chicago Purchasing Managers' Index January 54.6 55

15:00 U.S. Consumer confidence January 113.7 112.9

21:45 New Zealand Employment Change, q/q Quarter IV 1.4%

21:45 New Zealand Unemployment Rate Quarter IV 4.9%

22:35 Canada BOC Gov Stephen Poloz Speaks

-

21:45

New Zealand: Visitor Arrivals, December 11.1%

-

15:05

US pending home sales picked up in December

Pending home sales picked up in December as solid increases in the South and West offset weakening activity in the Northeast and Midwest.

The Pending Home Sales Index (PHS), a leading indicator of housing activity, measures housing contract activity, and is based on signed real estate contracts for existing single-family homes, condos and co-ops. Because a home goes under contract a month or two before it is sold, the Pending Home Sales Index generally leads Existing Home Sales by a month or two.

-

15:00

U.S.: Pending Home Sales (MoM) , December 1.6% (forecast 1.1%)

-

14:22

Belgian 4Q GDP +0.4% On Quarter, +1.2% On Year

-

13:53

Option expiries for today's 10:00 ET NY cut

EUR/USD 1.0500 (EUR 1.41bln) 1.0525 (313m) 1.0650 (754m)

USD/JPY 113.30-40 (USD 959m)

GBP/USD 1.2500 (GBP 370m)

EUR/GBP 0.8515 (EUR 526m)

AUD/USD 0.7575-85 (AUD 365m)

AUD/NZD 1.0450 (AUD 890m)

AUD/JPY 85.00 (AUD 491m)

-

13:48

I have made my decision on who I will nominate for The United States Supreme Court. It will be announced live on Tuesday at 8:00 P.M. (W.H.) @realDonaldTrump

-

13:48

US personal income increased $50.2 billion (0.3 percent) in December

Personal income increased $50.2 billion (0.3 percent) in December according to estimates released today by the Bureau of Economic Analysis. Disposable personal income (DPI) increased $43.6 billion (0.3 percent) and personal consumption expenditures (PCE) increased $63.1 billion (0.5 percent).

Real DPI increased 0.1 percent in December and Real PCE increased 0.3 percent. The PCE price index increased 0.2 percent. Excluding food and energy, the PCE price index increased 0.1 percent.

-

13:30

U.S.: Personal Income, m/m, December 0.3% (forecast 0.4%)

-

13:30

U.S.: Personal spending , December 0.5% (forecast 0.5%)

-

13:30

U.S.: PCE price index ex food, energy, m/m, December 0.1% (forecast 0.1%)

-

13:30

U.S.: PCE price index ex food, energy, Y/Y, December 1.7%

-

13:06

German CPI inflation moderately lower than expected

The inflation rate in Germany as measured by the consumer price index is expected to be +1.9% in January 2017. A similarly high rate of inflation was last measured in July 2013 (+1.9%). Based on the results available so far, the Federal Statistical Office (Destatis) also reports that the consumer prices are expected to decline by 0.6% on December 2016.

In January 2017, the harmonised index of consumer prices for Germany, which is calculated for European purposes, is expected to increase by 1.9% year on year and to decrease by 0.8% on December 2016.

-

13:01

Orders

EUR/USD

Offers: 1.0730 1.0750 1.0765 1.0780 1.0800 1.0830 1.0850-55

Bids: 1.0680 1.0655-60 1.0625-30 1.0600 1.0580 1.0565 1.0550 1.0520 1.0500

GBP/USD

Offers: 1.2560 1.2580 1.2600 1.2630 1.2660 1.2680 1.2700 1.2730 1.2750

Bids: 1.2525-30 1.2500 1.2480-85 1.2450 1.2430 1.2400

EUR/GBP

Offers: 0.8550-55 0.8580-85 0.8600 0.8620 0.8650

Bids: 0.8500 0.8470-75 0.8450 0.8430 0.8400

EUR/JPY

Offers: 123.00 123.30 123.50 123.80 124.00 124.20 124.50 124.80 125.00

Bids: 122.55-60 122.30 122.00 121.80 121.60 121.20 121.00

USD/JPY

Offers: 115.00 115.30-35 115.50 115.65 115.80 116.00 116.20 116.50

Bids: 114.50 114.30 114.00 113.80 113.50 113.30 113.00

AUD/USD

Offers: 0.7560 0.7580-85 0.7600 0.7630 0.7650

Bids: 0.7520 0.7500 0.7480-850.7450 0.7430 0.7400

Информационно-аналитический отдел TeleTrade

-

13:00

Germany: CPI, y/y , January 1.9% (forecast 2%)

-

13:00

Germany: CPI, m/m, January -0.6% (forecast -0.6%)

-

12:26

Nowotny: Can't Say Ii Taper Decision in Summer, Bbt Will Have Better Information to Make Decision. Eur/Usd down over 100 pips today

-

Would Be 'Suicide' for Italy to Leave Eurozone

-

In Interest of France and Italy to Remain in Eurozone

-

Trump Doesn't See That US Economic Priorities Require Cooperation

-

Will Discuss Future Policy Before End of 2017

-

ECB Can't React to Developments in One Country

-

-

11:29

UK private sector growth has slowed - CBI

The growth of the private sector fell in the three months through January, data from the Confederation of British Industry showed on Monday.

The growth rate dropped to 10 percent compared to 17 percent in December.

The picture was mixed between the various sectors during the period. Retailers reported decent growth in the previous three months, and the growth of production remained stable among producers, albeit at a slower pace. At the same time, the volume of the service sector has not changed.

In general, expectations have been growing at a level that will be maintained at the same rate over the next three months.

"While companies seek Brexit as a success, progress in improving the performance of the UK is the number one priority," said Rain Newton-Smith, chief economist at CBI.

-

10:49

Eurozone economic confidence strengthened in January

Eurozone economic confidence strengthened in January, monthly survey data from the European Commission showed, cited by rttnews.

The economic confidence index rose to 108.2 in January from 107.8 in December. The score was expected to remain unchanged at 107.8.

The mildly positive developments in euro-area sentiment resulted from improvements in industry, services and consumer confidence which outweighed decreases in retail trade and construction confidence.

-

10:31

Credit Agricole asks if Bank of Japan will announce a taper

"Despite JPY strengthening in the new year, our positioning indicator suggests the market's short JPY position remains at multi-year extremes.

While first-tier data on the labour market and industrial output will attract some attention from the JPY next week, the main local focus will be the BoJ meeting and the Board's Outlook Report.

Over the past year, the JPY TWI has strengthened in the week of all but one of the BoJ meetings. Admittedly, BoJ meetings have usually occurred the same week as FOMC meetings, and a stubbornly dovish FOMC has contributed to JPY strength during those weeks.

While the FOMC also meets next week, its members have been sounding more hawkish and so could contribute to a breaking of this pattern. But we also see a risk of a more upbeat BoJ in its first Outlook Report for the year. Indeed, the weaker JPY in Q4 will lead to stronger inflation and, to some extent, cyclical data readings in the coming months. And JPY depreciation has already helped push medium-term inflation expectations higher. BoJ Governor Haruhiko Kuroda recently said that Japan's economy has improved a lot and that it will grow well above expectations.

There is also some risk of the BoJ scrapping its guidance as when it comes to bond purchases. The central bank may have stepped up purchases in bonds due in 5-10 years, but the increase is not fully offsetting the reduction in shorter-term purchases. Our economists note that the net increment in JGB holding in 2017 will be way below the present guidance of JPY80trn.

As such, a formal taper announcement cannot be excluded. Any announcement of a formal taper would likely contain some sticker shock and strengthen the JPY, as it would lose some of its appeal as a funding currency.

We still significant risk of further downside in JPY crosses".

Copyright © 2017 Credit Agricole CIB, eFXnews™

-

10:00

Eurozone: Business climate indicator , January 0.77

-

10:00

Eurozone: Economic sentiment index , January 108.2 (forecast 107.9)

-

10:00

Eurozone: Consumer Confidence, January -4.7 (forecast -4.9)

-

10:00

Eurozone: Industrial confidence, January 0.8 (forecast 0.2)

-

09:50

Option expiries for today's 10:00 ET NY cut

EUR/USD 1.0500 (EUR 1.41bln) 1.0525 (313m) 1.0650 (754m)

USD/JPY 113.30-40 (USD 959m)

GBP/USD 1.2500 (GBP 370m)

EUR/GBP 0.8515 (EUR 526m)

AUD/USD 0.7575-85 (AUD 365m)

AUD/NZD 1.0450 (AUD 890m)

AUD/JPY 85.00 (AUD 491m)

Информационно-аналитический отдел TeleTrade

-

09:47

Germany's Hesse Jan CPI -0.5% On Mo; +2.4% On Year, Brandenburg Jan CPI -0.7% On Mo, +1.7% On Year, Bavaria Jan CPI -0.8% On Mo; +1.7% On Year

-

08:14

The Swiss KOF Economic Barometer dropped slightly in January

In January 2017, the Economic Barometer reached a score of 101.7 points. This relates to a slight downward revision by 0.4 points compared to its December value (102.1, revised from 102.2). Positive impulses to the Barometer came from the construction and the export sector.

Negative signals to the January standing came from indicators related to the financial sector, private consumption and, in particular, to the hotel and restaurant industry. The indicators from the manufacturing sector neutralized each other.

-

08:09

Spanish GDP in line with expectations in Q4

The Gross Domestic Product generated by the Spanish economy shows a variation of 0.7% in the fourth quarter of 2016 compared to the previous quarter, according to Estimation of quarterly GDP. This rate is similar to that recorded in the quarter previous.

The annual variation of GDP in the fourth quarter of 2016 stands at 3.0%, two tenths Lower than in the third quarter (3.2%). By the temporary aggregation of the four quarters, the growth in volume of GDP in the The year 2016 is estimated at 3.2%.

-

08:01

Switzerland: KOF Leading Indicator, January 101.7 (forecast 103.3)

-

07:58

USD will head back higher - Danske

"Year-to-date, the Dow Jones is up 1.71%, US 10Y yields are up 8bp and EUR/USD is 1 1/2 figure higher. Uncertainty is extraordinarily high given the lack of clarity on US economic policy, the risks of EU fragmentation with the near-term UK-EU Brexit negotiations, and the Dutch and French elections. Markets are struggling to grasp the policy uncertainties as the range of possible outcomes is so diverse. Hence, markets are trading sideways awaiting new information. Still, some markets are trending with German 10Y yields reaching the highest level in a year and bank stocks continuing their march higher.

We expected that there would be a market vacuum during H1 given the lofty expectations following Trump's win and the challenge he will face to enact fast fiscal stimulus. But it has surprised us how quickly the market vacuum arrived. This can be explained by positioning as the market was very short 10Y UST futures and long US dollars (USD) from the beginning of the year. The market is impatient and as the new US administration seems to have trade as its #1 priority we are not any wiser on fiscal policy (see Chart 1). However, during Trump's first 100 days in office we should know more about the new US government's fiscal policy plans. The market is likely to be significantly less short UST futures and long USDs than a couple of weeks back.

Where does this leave us in terms of markets? We see risks skewed towards higher US yields as positioning is probably cleaner now than a couple of weeks back and we will get more details on US fiscal stimulus plans during Trump's first 100 days in office. Due to the strong US economic data recently, we will look for signs in next week's FOMC statement on whether the next Fed rate hike could come as soon as March or May. Core European curves should continue to steepen from 5Y and beyond even though they are already at elevated levels (see Chart 2). A dovish ECB should help to reflate the European economy, driving longer-end yields higher.

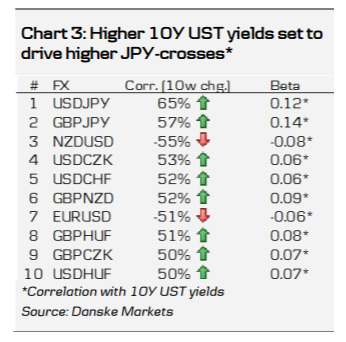

Over the coming 1-3 months, we expect the USD to strengthen in line with the receipt of more detail on the new US government's fiscal stimulus plans and probably other tariff and tax measures during Trump's first 100 day in office. We expect JPY-crosses to be the worst hit by reflation, with the USD/JPY likely to head up towards mid-December highs of 118/119".

Copyright © 2017 Danske, eFXnews™

-

07:30

Japanese retail sales fell more than expected

Retail sales in Japan fell a seasonally adjusted 1.7 percent on month in December, the Ministry of Economy, Trade and Industry said on Monday, cited by rttnews.

That missed expectations for a decline of 0.5 percent following the 0.2 percent increase in November.

On a yearly basis, retail sales added 0.6 percent - also shy of forecasts for a gain of 1.7 percent, which would have been unchanged from the November reading.

Large retailer sales dropped an annual 1.3 percent, missing forecasts for a fall of 1.0 percent following the 0.3 percent drop in the previous month.

-

07:29

Greece three weeks away from 'explosive' debt problems, says IMF

-

07:27

Japan FinMin Aso: Specific measures up to BoJ, hopes they make efforts to hit inflation target, with eye on economic developments - Reuters

-

06:05

Options levels on monday, January 30, 2017

EUR/USD

Resistance levels (open interest**, contracts)

$1.0781 (2520)

$1.0756 (2240)

$1.0740 (449)

Price at time of writing this review: $1.0720

Support levels (open interest**, contracts):

$1.0624 (1339)

$1.0598 (2083)

$1.0569 (1779)

Comments:

- Overall open interest on the CALL options with the expiration date March, 13 is 61138 contracts, with the maximum number of contracts with strike price $1,0800 (3829);

- Overall open interest on the PUT options with the expiration date March, 13 is 72094 contracts, with the maximum number of contracts with strike price $1,0000 (5013);

- The ratio of PUT/CALL was 1.18 versus 1.20 from the previous trading day according to data from January, 27

GBP/USD

Resistance levels (open interest**, contracts)

$1.2807 (1711)

$1.2710 (1629)

$1.2615 (1615)

Price at time of writing this review: $1.2567

Support levels (open interest**, contracts):

$1.2487 (1643)

$1.2390 (943)

$1.2293 (1747)

Comments:

- Overall open interest on the CALL options with the expiration date March, 13 is 23126 contracts, with the maximum number of contracts with strike price $1,2500 (2595);

- Overall open interest on the PUT options with the expiration date March, 13 is 26143 contracts, with the maximum number of contracts with strike price $1,1500 (3230);

- The ratio of PUT/CALL was 1.13 versus 1.12 from the previous trading day according to data from January, 27

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-