Market news

-

20:00

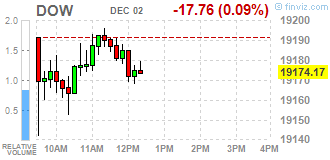

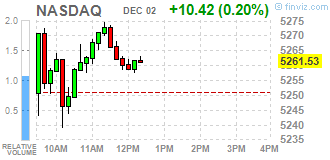

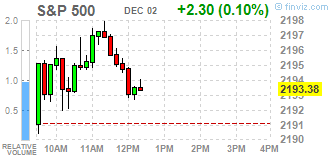

DJIA 19156.71 -35.22 -0.18%, NASDAQ 5252.33 1.22 0.02%, S&P 500 2189.98 -1.10 -0.05%

-

17:26

Wall Street. Major U.S. stock-indexes little changed

Major U.S. stock-indexes little changed. Industrial and banks stocks have been the biggest gainers of a post-election rally as investors expect these sectors to benefit the most from President-elect Donald Trump's policies. U.S. employers boosted hiring in November and the unemployment rate dropped to a more than nine-year low of 4.6 percent, making it almost certain that the Federal Reserve will raise interest rates later this month. Nonfarm payrolls increased by 178,000 jobs last month after increasing by 142,000 in October, the Labor Department said on Friday.

Most of Dow stocks in positive area (19 of 30). Top gainer - Merck & Co., Inc. (MRK, +1.04%). Top loser - The Goldman Sachs Group, Inc. (GS, -1.93%).

Most S&P sectors also in positive area. Top gainer - Healthcare (+1.1%). Top loser - Conglomerates (-0.5%).

At the moment:

Dow 19165.00 -32.00 -0.17%

S&P 500 2192.00 0.00 0.00%

Nasdaq 100 4742.25 +5.75 +0.12%

Oil 51.37 +0.31 +0.61%

Gold 1178.40 +9.00 +0.77%

U.S. 10yr 2.36 -0.06

-

17:00

European stocks closed: FTSE 6730.72 -22.21 -0.33%, DAX 10513.35 -20.70 -0.20%, CAC 4528.82 -31.79 -0.70%

-

16:30

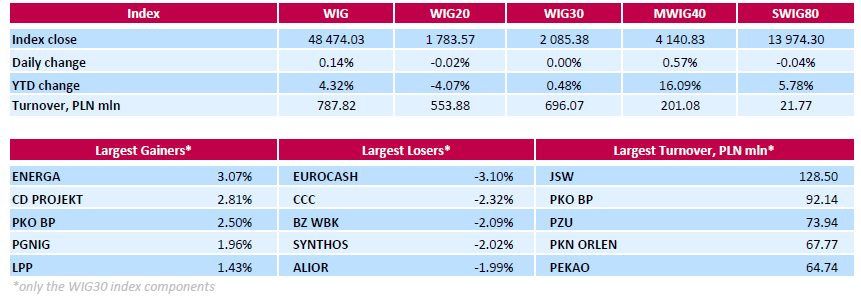

WSE: Session Results

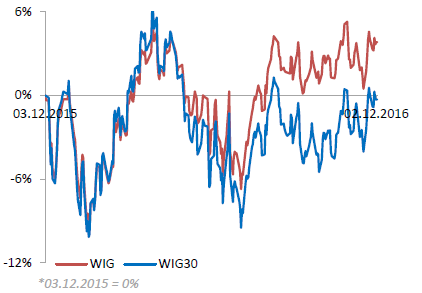

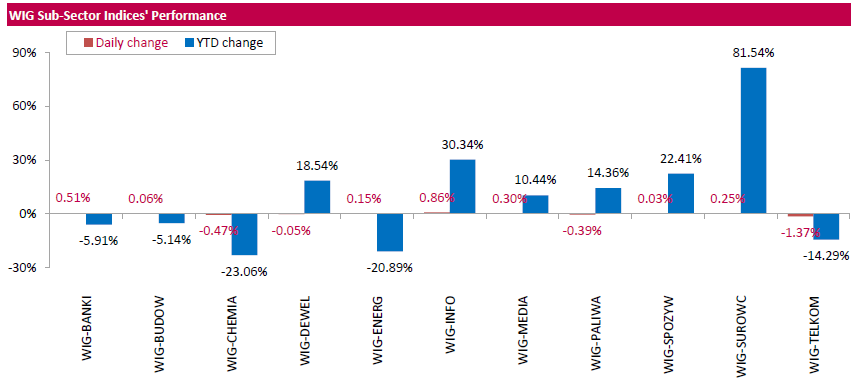

Polish equity market closed higher on Friday. The broad market measure, the WIG Index, added 0.14%. Sector performance within the WIG Index was mixed. Informational technology (+0.86%) outperformed, while telecoms (-1.37%) lagged behind.

The large-cap WIG30 Index was unchanged. Within the index components, genco ENERGA (WSE: ENG) was the best-performing name, climbing by 3.07%. It was followed by videogame developer CD PROJEKT (WSE: CDR), bank PKO BP (WSE: PKO), oil and gas producer PGNIG (WSE: PGN) and clothing retailer LPP (WSE: LPP), advancing 1.43%-2.81%. On the other side of the ledger, FMCG-wholesaler EUROCASH (WSE: EUR) and footwear retailer CCC (WSE: CCC) fell the most, down 3.1% and 2.32% respectively. Among other noticeable underperformers were chemical producer SYNTHOS (WSE: SNS), telecommunication services provider ORANGE POLSKA (WSE: OPL) and two banking names ALIOR (WSE: ALR) and BZ WBK (WSE: BZW), which retreated by 1.9%-2.09%.

-

15:52

Gold little changed for the day

Gold prices pared gains Friday, after an on-target U.S. jobs report bolstered the case for the Federal Reserve to raise interest rates at a faster clip next year, Dow Jones says.

Gold for February delivery was recently unchanged at $1,169.30 a troy ounce on the Comex division of the New York Mercantile Exchange. Prices stood at around $1,173 a troy ounce before the report was released at 8:30 a.m. ET.

Nonfarm payrolls rose by a seasonally adjusted 178,000 in November from the prior month, the Labor Department said Friday. The unemployment rate dropped to 4.6% last month from 4.9% in October as some people found jobs while others dropped out of the workforce. At 4.6%, the headline figure is the lowest since August 2007.

Economists surveyed by The Wall Street Journal had expected 180,000 new jobs and a jobless rate of 4.9% in November.

-

14:38

WSE: After start on Wall Street

The afternoon data from the US labor market were consistent with expectations but disappointed investors who expect fireworks. Quiet market expectations, however, were higher than read 178 thousand. The data should not change market expectations against the December price of the loan increase, but will not be an element that eventually convince the market that the Fed will raise rates in mid-December.

The beginning of trading on Wall Street took place at neutral level, what was already heralded by previous behavior of futures on the US indices. Our the WIG20 index also does not leave today's volatility level and after entering the game by Americans was at the level of 1,784 points (+0,00%).

-

14:34

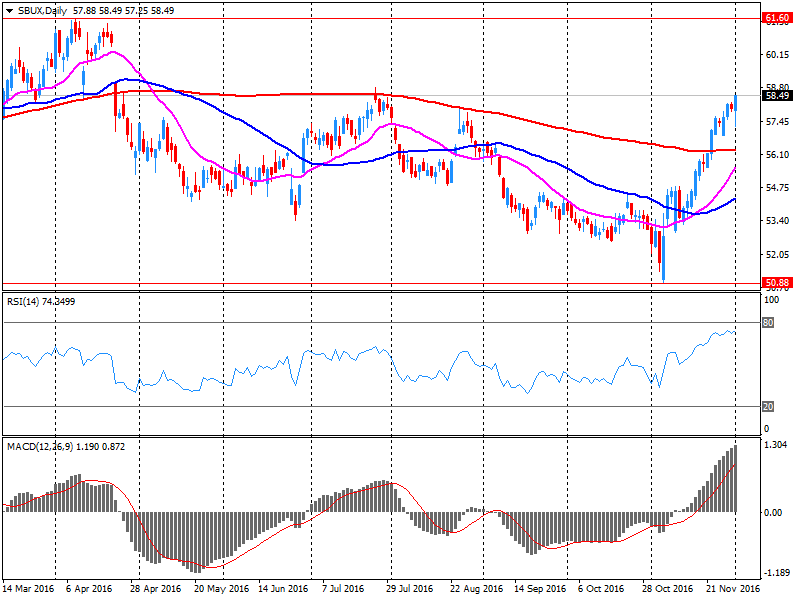

Starbucks CEO (SBUX) Howard Schultz to leave in April

Starbucks, confirmed the information that CEO Howard Schultz will leave on April 3, 2017. According to the report, Mr. Schultz will be appointed Chairman of the Board of Directors and will focus on innovation, design and Starbucks Reserve Roasteries development around the world, expanding the format of the retailer and the company's social initiatives.

SBUX shares fell in premarket trading to $ 56.85 (-2.84%).

-

14:33

U.S. Stocks open: Dow -0.11%, Nasdaq -0.08%, S&P 0.00%

-

14:12

Before the bell: S&P futures -0.19%, NASDAQ futures -0.25%

U.S. stock-index futures slipped after the latest jobs report delivered a mixed picture on the strength of the labor market as investors assess the Federal Reserve's plans to raise interest rates..

Global Stocks:

Nikkei 18,426.08 -87.04 -0.47%

Hang Seng 22,564.82 -313.41 -1.37%

Shanghai 3,244.48 -28.83 -0.88%

FTSE 6,699.25 -53.68 -0.79%

CAC 4,505.44 -55.17 -1.21%

DAX 10,449.58 -84.47 -0.80%

Crude $50.75 (-0.61%)

Gold $1,174.30 (+0.42%)

-

13:54

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

28.78

-0.10(-0.3463%)

2389

ALTRIA GROUP INC.

MO

62.8

-0.09(-0.1431%)

1608

Amazon.com Inc., NASDAQ

AMZN

743

-0.65(-0.0874%)

8739

Apple Inc.

AAPL

109.3

-0.19(-0.1735%)

48491

Barrick Gold Corporation, NYSE

ABX

15

-0.02(-0.1332%)

122097

Caterpillar Inc

CAT

95.74

-0.50(-0.5195%)

6397

Chevron Corp

CVX

113.39

0.10(0.0883%)

14910

Citigroup Inc., NYSE

C

57.05

-0.22(-0.3841%)

84017

Deere & Company, NYSE

DE

102.05

-0.65(-0.6329%)

2098

Exxon Mobil Corp

XOM

86.97

-0.27(-0.3095%)

23277

Facebook, Inc.

FB

115

-0.10(-0.0869%)

61512

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

14.76

-0.27(-1.7964%)

110847

General Electric Co

GE

31.28

-0.11(-0.3504%)

14678

General Motors Company, NYSE

GM

36.21

-0.22(-0.6039%)

11062

Goldman Sachs

GS

225.91

-0.72(-0.3177%)

43888

Google Inc.

GOOG

745.2

-2.72(-0.3637%)

3689

Home Depot Inc

HD

128.5

-0.97(-0.7492%)

3776

Intel Corp

INTC

33.73

-0.03(-0.0889%)

7182

International Business Machines Co...

IBM

158.9

-0.92(-0.5757%)

149

Johnson & Johnson

JNJ

111

-0.38(-0.3412%)

2097

JPMorgan Chase and Co

JPM

81.4

-0.39(-0.4768%)

40857

McDonald's Corp

MCD

118.42

-0.05(-0.0422%)

885

Merck & Co Inc

MRK

60.765

0.005(0.0082%)

446

Microsoft Corp

MSFT

59

-0.20(-0.3378%)

9485

Nike

NKE

50.59

-0.06(-0.1185%)

2024

Pfizer Inc

PFE

31.54

0.08(0.2543%)

5715

Procter & Gamble Co

PG

82.24

0.38(0.4642%)

296

Starbucks Corporation, NASDAQ

SBUX

56.68

-1.83(-3.1277%)

233133

Tesla Motors, Inc., NASDAQ

TSLA

182.15

0.27(0.1484%)

18325

The Coca-Cola Co

KO

40.18

0.01(0.0249%)

2601

Twitter, Inc., NYSE

TWTR

18.1

0.07(0.3882%)

31554

Verizon Communications Inc

VZ

49.93

0.06(0.1203%)

1464

Visa

V

75.4

-0.03(-0.0398%)

9108

Wal-Mart Stores Inc

WMT

70.83

0.16(0.2264%)

101

Walt Disney Co

DIS

98.74

-0.20(-0.2021%)

2787

Yahoo! Inc., NASDAQ

YHOO

39.68

0.05(0.1262%)

125

Yandex N.V., NASDAQ

YNDX

18.82

0.21(1.1284%)

18157

-

13:50

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Other:

Pfizer (PFE) initiated with a Neutral at Guggenheim

Exxon Mobil (XOM) initiated with a Market Perform at BMO Capital Mkts

-

13:50

Option expiries for today's 10:00 ET NY cut

EURUSD 1.0450 (EUR 2.38bln) 1.0500 (1.41bln) 1.0550 (1.86bln) 1.0600 (2.83bln) 1.0650 (2.23bln) 1.0700 (2.3bln) 1.0800 (1.48bln)

USDJPY 110.00 (USD 1.09bln) 111.50 (1.16bln) 111.75 500m) 112.00 (411m) 112.50 (1.6bln) 113.00-05 (422m) 115.00 (420m)

GBPUSD 1.2450 (GBP 531m) 1.2500 (788m) 1.2700 (497m)

AUDUSD 0.7320 (AUD 943m) 0.7425 (337m)

NZDUSD 0.7050 (NZD 834m)

USDCAD 1.3375-80 (USD 472m) 1.3500 (932m) 1.3600 (786m)

AUDNZD 1.0500 (AUD 1.15bln)

-

13:44

Labour productivity of Canadian businesses rose in the third quarter

Labour productivity of Canadian businesses rose 1.2% in the third quarter, after declining 0.2% in the second quarter.

Although this was the highest rate of growth since the second quarter of 2014 (+1.9%), the increase in productivity reflects a rebound in business output following a decline in the second quarter. Hours worked continued to decrease, but at a slower pace than in the previous quarter.

After decreasing 0.7% in the second quarter, real gross domestic product (GDP) of businesses rose 1.0% in the third quarter. Goods-producing businesses contributed the most to the gain, as mining and oil and gas extraction and manufacturing activities increased. In the second quarter, output was disrupted by the forest fires in northern Alberta and scheduled maintenance shutdowns in the oil and gas extraction industry.

-

13:41

Canadian employment beats expectations. USD/CAD tests major support at 1.3250

After two consecutive months of notable increases, employment was little changed in November (+11,000 or +0.1%). With fewer people searching for work, the unemployment rate fell by 0.2 percentage points to 6.8%.

Compared with November 2015, overall employment rose by 183,000 (+1.0%), with the number of people working part time increasing by 214,000 (+6.4%). Over the same period, the total number of hours worked was up 1.1%.

More people were employed in the finance, insurance, real estate and leasing industry, in information, culture and recreation, in the "other services" industry and in agriculture. On the other hand, declines were observed in construction, in manufacturing, as well as in transportation and warehousing.

There were fewer self-employed workers in November, while the number of employees was little changed in both the public and private sectors.

-

13:39

US Non Farm Payrolls in line with estimates, poor average hourly earnings limit USD bids

Total nonfarm payroll employment rose by 178,000 in November. Thus far in 2016, employment growth has averaged 180,000 per month, compared with an average monthly increase of 229,000 in 2015. In November, employment gains occurred in professional and business services and in health care.

Employment in professional and business services rose by 63,000 in November and has risen by 571,000 over the year. Over the month, accounting and bookkeeping services added 18,000 jobs. Employment continued to trend up in administrative and support services (+36,000), computer systems design and related services (+5,000), and management and technical consulting services (+4,000).In November, average hourly earnings for all employees on private nonfarm payrolls declined by 3 cents to $25.89, following an 11-cent increase in October. Over the year, average hourly earnings have risen by 2.5 percent. Average hourly earnings of private-sector production and nonsupervisory employees edged up by 2 cents to $21.73 in November.

-

13:36

US unemployment rate declined to 4.6 percent in November

The unemployment rate declined to 4.6 percent in November, and total nonfarm payroll employment increased by 178,000, the U.S. Bureau of Labor Statistics reported today. Employment gains occurred in professional and business services and in health care.

The number of unemployed persons declined by 387,000 to 7.4 million. Both measures had shown little movement, on net, from August 2015 through October 2016.Among the major worker groups, the unemployment rate for adult men declined to 4.3 percent in November. The rates for adult women (4.2 percent), teenagers (15.2 percent), Whites (4.2 percent), Blacks (8.1 percent), Asians (3.0 percent), and Hispanics (5.7 percent) showed little or no change over the month.

-

13:30

U.S.: Unemployment Rate, November 4.6% (forecast 4.9%)

-

13:30

U.S.: Nonfarm Payrolls, November 178 (forecast 175)

-

13:30

U.S.: Average hourly earnings , November -0.1% (forecast 0.2%)

-

13:30

Canada: Employment , November 10.7 (forecast -20)

-

13:30

U.S.: Average workweek, November 34.4 (forecast 34.4)

-

13:30

Canada: Labor Productivity, Quarter III 1.2% (forecast 1%)

-

13:30

Canada: Unemployment rate, November 6.8% (forecast 7%)

-

13:09

Some upside risks for NFP as jobless claims dropped to a 43year low says UniCredit

US nonfarm payrolls likely rose another solid 175,000 in November. That is slightly faster than the 161,000 seen in October, but broadly in line with the average seen over the past three months. If anything, the most timely labor market indicator points to some upside risks, as jobless claims dropped to a 43year low in the middle of the month. In addition to very low layoffs, labor demand has remained strong with the number of jobs close to a record high. The jobless rate likely stayed at 4.9%, after declining in October. As the US economy approaches full employment, wage gains continue to rise, while payroll gains slow gradually towards the trend growth rate in the labor force.

-

13:05

BOE's Haldane: The Bank of England shouldn't be hasty about tightening

-

Risk Growth Could Underperform

-

Rise in Inflation Expectations Would Be Unhelpful

-

Comfortable With Stance of Policy

-

Sees Falling Pound Depressing Consumer Spending

-

-

13:00

Orders

EUR/USD

Offers 1.0685 1.0700 1.0730 1.0745-50 1.0780 1.0800 1.0820 1.0850

Bids 1.0650 1.0630 1.0600 1.0580 1.0550-55 1.0530

GBP/USD

Offers 1.2635 1.2650 1.2665 1.2680 1.2700 1.2725-30 1.2750 1.2780 1.2800

Bids 1.2600 1.2585 1.2560 1.2520-25 1.2500 1.2475-80 1.2455-60 1.2430 1.2400

EUR/GBP

Offers 0.8465 0.8480-85 0.8500 0.8525-30 0.8560 0.8575-80 0.8600

Bids 0.8420-25 0.8400 0.8370-75 0.8350 0.8330 0.8300

EUR/JPY

Offers 122.00 122.30 122.65-70 123.00 123.50 124.00

Bids 121.50 121.20 121.00 120.85 120.50 102.20 120.00 119.60 119.30 119.00

USD/JPY

Offers 114.20 114.35 114.50 114.80-85 115.00 115.25 115.45-50

Bids 113.80 113.50 113.20 113.00 112.85 112.50 112.20 112.00 111.80 111.50

AUD/USD

Offers 0.7425-30 0.7450 0.7485 0.7500-05 0.7520 0.7545-50

Bids 0.7400 0.7380 0.7355-60 0.7325-30 0.7300 0.7285 0.7250

-

12:34

Danske Sees EUR/NOK Up As "Oil Market Is Overreacting" to OPEC

-

12:11

WSE: Mid session comment

As expected and follow the usually played on the first Fridays of the month scenario, the WIG20 ended the first half of the session with modest change. The first three session hours were dominated by the consolidation, which the focal point was the region of 1,785 points. Entry into the afternoon phase brought withdrawal in the region of 1,780 pts., but the movement is in the range of today's volatility.

Stabilization is supported by the environment where the DAX drifting close to the opening level and by the currency market, where you may not see any major shifts.

Markets are waiting for the 14:30 (Warsaw time) when the data from the US should bring a little life to trade.

In the middle of today's session the WIG20 index was at the level of 1,781 points, and with the turnover of PLN 220 million.

-

11:40

Barclays see asymmetric risks to the USD before NFP

We see asymmetric risks to the USD this week as the employment report takes central stage. A number close to our expectation of 175k or even lower would keep the Fed on track as it is assumed that a deceleration in job creation is normal as the labour market is near full employment. On the other hand, a higher number (closer to 200k) would signal that the momentum is still strong, and that additional stimulus would probably lead the Fed to act faster, accelerating USD trend. We expect the unemployment rate to decline to 4.8% from 4.9%, average hourly earnings to rise 0.2% m/m and 2.8% y/y, and the average workweek to remain unchanged at 34.4 hours.

-

10:48

The dynamics of oil prices will continue to exert pressure on the Russian economy - Bank of Rusia’s Nabiullina

"The dynamics of oil prices will continue to be a major risk for the Russian economy that still low due to the diversification", - she said.

Since the beginning of this week, Brent crude oil has risen in price already 11%, and the day before rose above $ 54 a barrel for the first time since October 2015. The sharp rise in oil prices this week against the background of the OPEC deal to limit production.

-

10:34

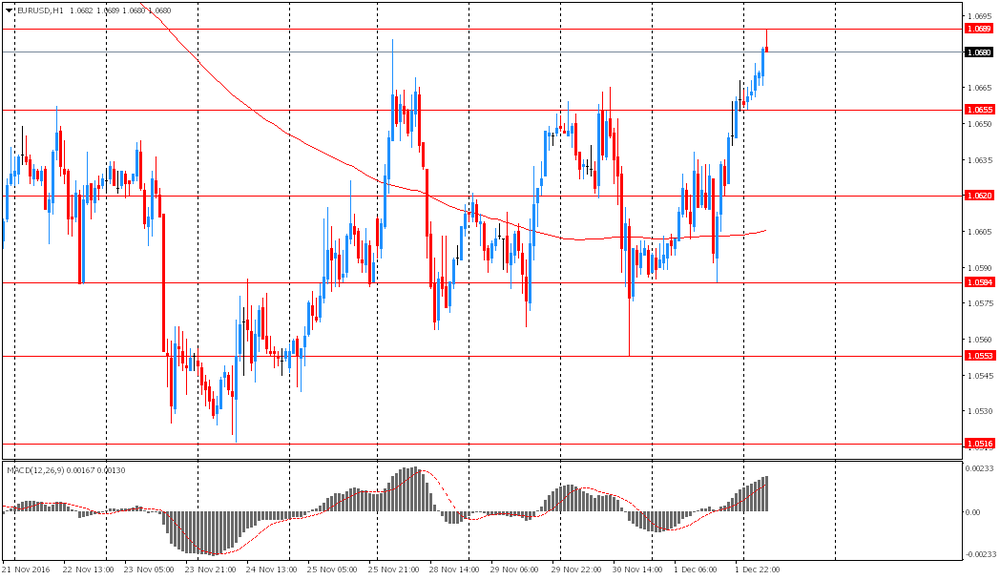

Euro fell significantly against the US dollar, under pressure from declining German bonds yields as well as increased demand for the dollar in anticipation of US labor market data. Currently EUR / USD traded at $ 1.0638, down 0.17%

The yield on German 10-year bond fell 4 basis points, or 10.65%, reaching 0.33%.

-

10:09

Euro area industrial producer prices rose mostly due to energy sector

In October 2016, compared with September 2016, industrial producer prices rose by 0.8% in the euro area (EA19) and by 1.0% in the EU28, according to estimates from Eurostat, the statistical office of the European Union. In September 2016 prices increased by 0.1% in both zones. In October 2016, compared with October 2015, industrial producer prices fell by 0.4% in the euro area, while it rose by 0.2% in the EU28.

The 0.8% increase in industrial producer prices in total industry in the euro area in October 2016, compared with September 2016, is due to rises of 2.6% in the energy sector, of 0.3% for non-durable consumer goods and of 0.1% for both intermediate goods and durable consumer goods, while prices remained stable for capital goods. Prices in total industry excluding energy rose by 0.1%.

-

10:00

Eurozone: Producer Price Index, MoM , October 0.8% (forecast 0.2%)

-

10:00

Eurozone: Producer Price Index (YoY), October -0.4% (forecast -1%)

-

09:57

Oil is trading lower as the market digest the OPEC deal

This morning, the New York futures for Brent are down 0.71% to $ 50.72 and crude oil futures WTI fell 1.19% to $ 53.30 per barrel. Thus the black gold corrected after the recent rally associated with the OPEC agreement. On Wednesday OPEC and Russia agreed to reduce oil production by 1.5 million barrels per day. Now experts are focusing on the implementation of the measures. On the eve of the OPEC meeting the market saw a slight probability that the cartel will reach a significant agreement because of disputes between the de facto leader Saudi Arabia and the third-largest producer Iran.

-

09:35

November data indicated that the UK construction sector continued to rebound - Markit

November data indicated that the UK construction sector continued to rebound from the weak patch recorded on average during the third quarter of 2016. Business activity and incoming new work increased at the strongest pace since March, although both rates of expansion remained much softer than the peaks achieved at the start of 2014.

Greater workloads underpinned a further solid rise in employment levels and input buying among construction firms.

However, average cost burdens rose sharply, with the rate of inflation the steepest since April 2011.

The seasonally adjusted Markit/CIPS UK Construction Purchasing Managers' Index picked up slightly to 52.8 in November, from 52.6 in October, thereby signalling an expansion of total business activity for the third month running.

Reports from survey respondents cited improved order books, alongside resilient client confidence and strong demand for residential projects. There were again reports that heightened economic uncertainty was a key factor weighing on output growth across the construction sector.

-

09:30

United Kingdom: PMI Construction, November 52.8 (forecast 52.2)

-

09:01

Nomura: steady US employment activity expected

We forecast that nonfarm payrolls increased by 160k in November, comparable with the gains seen in October. We expect a modest rise of 5k in government payrolls, implying that private payrolls increased by 155k. Incoming data on the labor market, for the most part, imply steady employment activity with limited involuntary layoffs in NovemberWe expect the unemployment rate to decline further to 4.8% in November. On wages, we expect growth in average hourly earnings to slow to 0.1% m-o-m (2.7% y o-y) following a sharp increase of 0.4% m-o-m in the previous month. We think that the prior month's strong wage growth was artificially amplified by inclement weather holding down the average weekly hours worked during the survey reference period. To that end, we think that some payback is warranted in November as conditions returned back to normal.

-

08:58

Option expiries for today's 10:00 ET NY cut

EUR/USD 1.0450 (EUR 2.38bln) 1.0500 (1.41bln) 1.0550 (1.86bln) 1.0600 (2.83bln) 1.0650 (2.23bln) 1.0700 (2.3bln) 1.0800 (1.48bln)

USD/JPY 110.00 (USD 1.09bln) 111.50 (1.16bln) 111.75 500m) 112.00 (411m) 112.50 (1.6bln) 113.00-05 (422m) 115.00 (420m)

GBP/USD 1.2450 (GBP 531m) 1.2500 (788m) 1.2700 (497m)

AUD/USD 0.7320 (AUD 943m) 0.7425 (337m)

NZD/USD 0.7050 (NZD 834m)

USD/CAD 1.3375-80 (USD 472m) 1.3500 (932m) 1.3600 (786m)

AUD/NZD 1.0500 (AUD 1.15bln)

Информационно-аналитический отдел TeleTrade

-

08:31

Major stock markets trading in the red zone: FTSE -0.8%, DAX -0.9%, CAC40 -0.7%, FTMIB -0.6%, IBEX -0.6%

-

08:21

WSE: After opening

WIG20 index opened at 1787.79 points (+0.22%)*

WIG 48399.33 -0.01%

WIG30 2083.48 -0.09%

mWIG40 4132.80 0.37%

*/ - change to previous close

The future contracts December series (FW20Z1620) started the day from the decline of approx. 0.4%, roughly in line with a shift visible on major European stock exchanges.

The opening of the cash market (WIG20) was inscribed in sentiment in Europe and after the first transactions the market retreated in the region of 1,780 points and then rebounded to 1,789 points. From the standpoint of market activity the first minutes of trading may be considered as consolidation.

After fifteen minutes of trading, the WIG20 index was at the level of 1,789 points (+ 0.29%).

-

08:07

Spanish unemployment rises

The number of unemployed registered in the offices of Public Employment Services has increased in November by 24,841 people in relation to the previous month. In the last 8 years in the same month registered unemployment increased, on average, by 43,219 people In this way, the total number of registered unemployed reaches the figure of 3,789,823 and continues in the lowest levels of the last 7 years.

In seasonally adjusted terms, unemployment rose by 14,543 people in November. With respect to November 2015 unemployment has fallen by 359,475 people. The annual reduction rate of recorded unemployment is 8.66%.

-

08:05

Brexit secretary suggests UK would consider paying for single market access - The Guardian

-

08:02

Today’s events

-

At 16:45 GMT FOMC member Lyell Braynard will deliver a speech

-

At 21:00 GMT FOMC Member Daniel Tarullo will deliver a speech

-

-

07:44

Negative start of trading expected on the major stock exchanges in Europe: DAX -0.3%, CAC40 -0.2%, FTSE -0.3%

-

07:43

Asian session review: USD weakness across the board

Australian dollar in the early session rose slightly on more positive than expected data on retail sales in Australia. As reported today by the Australian Bureau of Statistics, retail sales rose 0.5% in October, lower than the previous value of 0.6%, but higher than analysts' forecast of 0.3%. Previously, many analysts have expressed concerns about the growth of Australia's GDP in the third quarter, which will be published on December 7.

The US dollar is consolidating in anticipation of today's labor market data. Economists polled by Wall Street Journal, expects NFP at 175,000, and the unemployment rate stable at 4.9%. This report will be the last before the meeting of the Federal Reserve on 13-14 December. At this meeting, a decision with respect to interest rates will be made and it is expected (and probably priced in) that the Fed will raise its key interest rate for the first time for the year amid signs of improvement in the labor market and the continued growth of the economy.

EUR / USD: during the Asian session, the pair rose to $ 1.0690

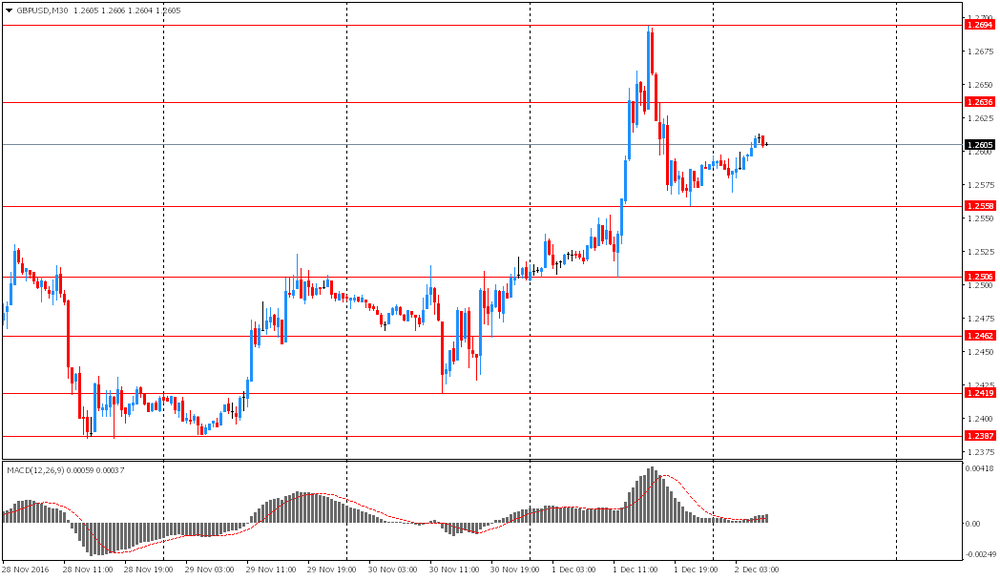

GBP / USD: during the Asian session, the pair was trading in the $ 1.2570-20 range

USD / JPY: fell to Y113.60

-

07:33

Options levels on friday, December 2, 2016:

EUR/USD

Resistance levels (open interest**, contracts)

$1.0932 (3503)

$1.0856 (4937)

$1.0793 (2938)

Price at time of writing this review: $1.0674

Support levels (open interest**, contracts):

$1.0597 (3329)

$1.0560 (2997)

$1.0509 (5172)

Comments:

- Overall open interest on the CALL options with the expiration date December, 9 is 87162 contracts, with the maximum number of contracts with strike price $1,1400 (6421);

- Overall open interest on the PUT options with the expiration date December, 9 is 72053 contracts, with the maximum number of contracts with strike price $1,0500 (6359);

- The ratio of PUT/CALL was 0.83 versus 0.82 from the previous trading day according to data from December, 1

GBP/USD

Resistance levels (open interest**, contracts)

$1.2901 (575)

$1.2802 (1181)

$1.2704 (1832)

Price at time of writing this review: $1.2633

Support levels (open interest**, contracts):

$1.2591 (1168)

$1.2495 (2487)

$1.2397 (1572)

Comments:

- Overall open interest on the CALL options with the expiration date December, 9 is 35672 contracts, with the maximum number of contracts with strike price $1,3400 (2561);

- Overall open interest on the PUT options with the expiration date December, 9 is 34792 contracts, with the maximum number of contracts with strike price $1,1750 (2539);

- The ratio of PUT/CALL was 0.98 versus 1.00 from the previous trading day according to data from December, 1

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

07:22

WSE: Before opening

Thursday's close on Wall Street took place in mixed moods - the Dow Jones index at the end of the day gained 0.36 percent, the S&P 500 fell by 0.35 percent, and the Nasdaq Comp. went down by 1.36 percent. Another day rise oil, after reaching the agreement by OPEC to reduce output.

The highest increases in the US were recorded by fuel companies and the financial sector, and strongest went down the computing enterprises.

The US economy released further data that reinforces expectations of a rise in interest rates in the US. At the same time, the prospect of higher oil prices next year in connection with the OPEC agreement affects the strengthening of inflation expectations in the United States.

Today is the first Friday of the month and a traditional meeting of the market with the monthly data from the US Department of Labor. The macro calendar today has no other report of a comparable impact on the market. This data also carry a risk of a strong reaction in the currency market, so the Warsaw market will depend on the relationship of the zloty to the dollar.

Today, the S&P Agency will revise the rating for Poland. The reduction in the retirement age, weaker economic data (disappointing GDP figures for the third quarter 2016 and the most recent data on industrial production and retail sales) - can be essential factors for the agency, at least as an excuse. It is doubtful, however, that S&P will lower the rating for the second time, when Moody's and Fitch have not done it yet, even for the first time. The decision probably will be announced in the evening.

-

07:20

Bank of America Merrill expects NFP at 170K

Recent labor market data has continued to show solid improvement. We expect the trend to continue in November with 170,000 in nonfarm payroll growth, a slight deceleration from the 176,000 average over the prior three months. We expect 165,000 in private payroll growth, with a modest 5,000 expansion in government payrolls.

We expect the labor force participation rate to remain at 62.8% and the unemployment rate to also remain unchanged at 4.9%. We expect a softer 0.2% mom gain in average hourly earnings after the strong 0.4% mom pop last month, leaving the year-over-year rate at 2.8%.

This shows continued improvement in wage growth, but still a less-thanhealthy 3%-4% pace of growth. Remember that the strong gain in average hourly earnings last month was concentrated in three categories: mining, utilities and information technology. We think that there is propensity for a modest reversal given the magnitude of the increase in all three. There are some risks of a weaker print and/or a downward revision to September wage growth. We expect average weekly hours to remain unchanged at 34.4.

-

07:17

USD / RUR recovers losses

USD / RUR fell sharply at the opening of trading to around 62.80, however, soon recovered and is now trading around 63.04. The pair is currently committed to the nearest resistance that is 63.19 (1 December high).

-

07:15

Reuters: The Reserve Bank of Australia will keep policy unchanged

According to a survey conducted by Reuters, the Reserve Bank of Australia will keep interest rates at a record low 1.5% on 6 December. 17 of 29 respondents forecast a loose RBA policy by mid-2017. 20 predict a rate hike in the 1st quarter of 2018.

-

07:13

U.S. Jobs Report in focus. EUR/USD up for the week, USD/JPY in distribution phase?

-

07:09

French President Francois Hollande will not run for another term in May

The current French President Francois Hollande announced his intention not to run for another term. This was seen as an unexpected solution for market participants, which enhances the risk of uncertainty on the European political scene, and the markets in general.

-

07:07

Australian retail sales rose more than expected in October

Australian retail turnover rose 0.5 per cent in October 2016, seasonally adjusted, according to the latest Australian Bureau of Statistics (ABS) Retail Trade figures.

This follows a 0.6 per cent rise in September 2016.

In seasonally adjusted terms, there were rises in food retailing (0.6 per cent), household goods retailing (0.7 per cent), other retailing (0.8 per cent) and cafes, restaurants and takeaway food services (0.4 per cent). There were falls in clothing, footwear and personal accessory retailing (-0.4 per cent) and department stores (-0.4 per cent) in October 2016.

-

07:04

Swiss GDP flat in Q3

Switzerland's real gross domestic product (GDP) has remained almost unchanged in the 3rd quarter of 2016 (+0.0%).* Consumption has contributed very little to growth. Investment in construction and equipment has supported GDP growth, while the trade balance in goods and services had a negative effect.

On the production side, the growth of value added has been below its historical mean in most sectors, with trade as well as health and social work activities having a negative impact. Manufacturing and the accommodation and food service industry have made positive contributions. Real GDP has grown by 1.3% in comparison to the 3rd quarter of 2015.

-

06:45

Switzerland: Gross Domestic Product (QoQ) , Quarter III 0.0% (forecast 0.3%)

-

06:45

Switzerland: Gross Domestic Product (YoY), Quarter III 1.3% (forecast 1.8%)

-

06:16

Global Stocks

European stocks ended lower for the first time in three days Thursday as investors opted for caution ahead of Italy's weekend referendum, which is feared to spark a political crisis in the eurozone.

The Dow Jones Industrial Average bucked the broader market's weakness on Thursday to close at a record high, even as large-cap technology stocks weighed down the Nasdaq Composite index for a second straight session.

The significant international exposure among tech companies makes them more vulnerable given the recent rise in the U.S. dollar, said Karyn Cavanaugh, senior market strategist at Voya Financial.

Asian shares were broadly lower Friday, tracking losses on Wall Street, as equity markets indicate the " Trump trade" could be overdone. Some traders have started asking if the market has overestimated U.S. president-elect Donald Trump's impact on inflation and U.S. growth.

-

00:30

Australia: Retail Sales, M/M, October 0.5% (forecast 0.3%)

-