Market news

-

23:32

Commodities. Daily history for Jan 10’2017:

(raw materials / closing price /% change)

Oil 50.89 +0.14%

Gold 1,186.00 +0.04%

-

23:31

Stocks. Daily history for Jan 10’2017:

(index / closing price / change items /% change)

Nikkei -152.89 19301.44 -0.79%

TOPIX -11.01 1542.31 -0.71%

Hang Seng +186.16 22744.85 +0.83%

CSI 300 -5.63 3358.27 -0.17%

Euro Stoxx 50 -2.76 3306.21 -0.08%

FTSE 100 +37.70 7275.47 +0.52%

DAX +19.31 11583.30 +0.17%

CAC 40 +0.66 4888.23 +0.01%

DJIA -31.85 19855.53 -0.16%

NASDAQ +20.00 5551.82 +0.36%

S&P/TSX +37.33 15426.28 +0.24%

-

23:29

Currencies. Daily history for Jan 10’2017:

(pare/closed(GMT +3)/change, %)

EUR/USD $1,0553 -0,19%

GBP/USD $1,2173 +0,11%

USD/CHF Chf1,0167 +0,15%

USD/JPY Y115,75 -0,22%

EUR/JPY Y122,17 -0,40%

GBP/JPY Y140,92 -0,11%

AUD/USD $0,7367 +0,20%

NZD/USD $0,6988 -0,37%

USD/CAD C$1,323 +0,12%

-

23:01

Schedule for today, Wednesday, Jan 11’2017 (GMT0)

05:00 Japan Coincident Index (Preliminary) November 113.5

05:00 Japan Leading Economic Index (Preliminary) November 100.8 102.6

09:30 United Kingdom Total Trade Balance November -1.97

09:30 United Kingdom Industrial Production (MoM) November -1.3% 0.8%

09:30 United Kingdom Industrial Production (YoY) November -1.1% 0.6%

09:30 United Kingdom Manufacturing Production (MoM) November -0.9% 0.5%

09:30 United Kingdom Manufacturing Production (YoY) November -0.4% 0.4%

15:30 U.S. Crude Oil Inventories January -7.051 0.620

23:50 Japan Current Account, bln November 1720 1500

-

20:00

DJIA 19877.18 -10.20 -0.05%, NASDAQ 5550.50 18.68 0.34%, S&P 500 2270.91 2.01 0.09%

-

17:00

European stocks closed: FTSE 7275.47 37.70 0.52%, DAX 11583.30 19.31 0.17%, CAC 4888.23 0.66 0.01%

-

16:29

WSE: Session Results

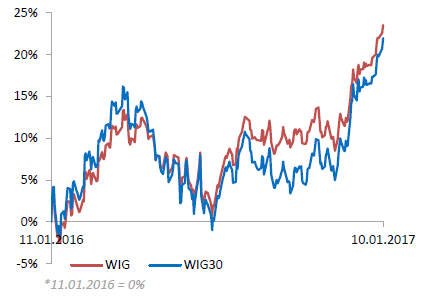

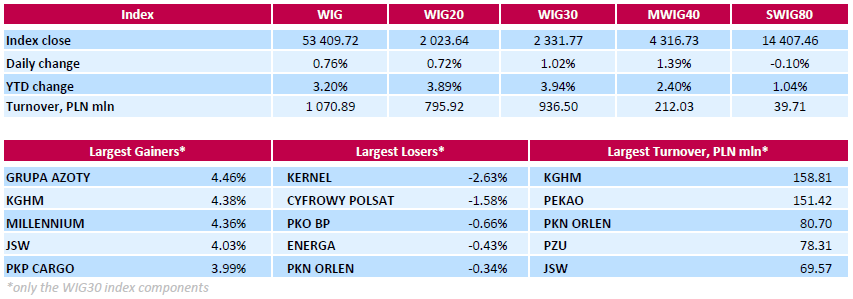

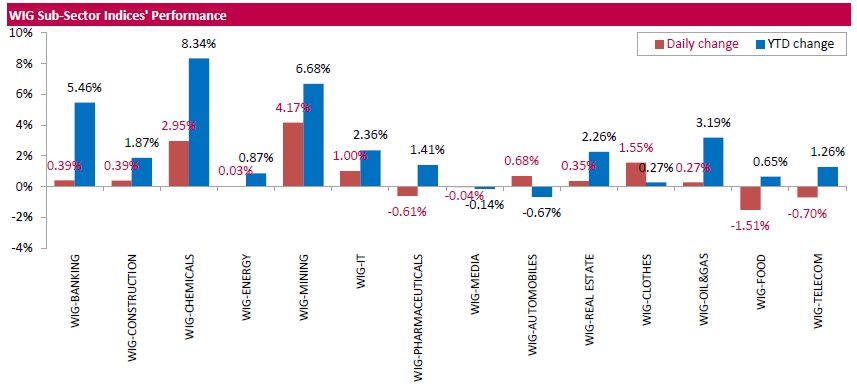

Polish equity market continued its upward trajectory on Tuesday. The broad market measure, the WIG Index, added 0.76%. The WIG sub-sector indices were mainly higher with mining stock gauge (+4.17%) outperforming.

The large-cap companies' measure, the WIG30 Index, recorded a 1.02% gain. A majority of the index components generated positive returns. The exception were agricultural producer KERNEL (WSE: KER), media group CYFROWY POLSAT (WSE: CPS), bank PKO BP (WSE: PKO), oil refiner PKN ORLEN (WSE: PKN) and three utilities names ENERGA (WSE: ENG), PGE (WSE: PGE) and ENEA (WSE: ENA), declining between 0.1% and 2.63%. At the same time, chemical producer GRUPA AZOTY (WSE: ATT) was the strongest performer with a 4.46% advance, followed by copper producer KGHM (WSE: KGH), bank MILLENNIUM (WSE: MIL) and coking coal miner JSW (WSE: JSW)), which quotations went up by 4.38%, 4.36% and 4.03% respectively.

-

16:14

Wall Street. Major U.S. stock-indexes slightly rose

Major U.S. stock indexes slightly rose on Tuesday. Banks have led a record-breaking run in U.S. equities since Donald Trump's election on Nov 8. But the rally's momentum has stalled of late as investors now wait to see if he can deliver on his promises of fiscal stimulus. The U.S. President-elect will hold a news conference on Wednesday, his first since his election.

Most of Dow stocks in positive area (19 of 30). Top gainer - Caterpillar Inc. (CAT, +1.56%). Top loser - International Business Machines Corporation (IBM, -0.72%).

Most of S&P sectors also in positive area. Top gainer - Basic Materials (+0.6%). Top loser - Utilities (-0.1%).

At the moment:

Dow 19837.00 +9.00 +0.05%

S&P 500 2267.00 +2.00 +0.09%

Nasdaq 100 5027.75 +5.75 +0.11%

Oil 51.27 -0.69 -1.33%

Gold 1188.60 +3.70 +0.31%

U.S. 10yr 2.37 0.00

-

15:53

ING sees weaker GBP as markets price Brexit risk

-

15:41

Long HUF/PLN on political risks, says Nordea

-

15:17

US wholesale inventories rose more than expected in November

Total inventories of merchant wholesalers, except manufacturers' sales branches and offices, after adjustment for seasonal variations but not for price changes, were $595.3 billion at the end of November, up 1.0 percent (±0.2 percent) from the revised October level. Total inventories are up 1.4 percent (±1.1 percent) from the revised November 2015 level. The October 2016 to November 2016 percent change was revised from the advance estimate of up 0.9 percent (±0.2 percent) to up 1.0 percent (±0.2 percent).

-

15:15

The number of US job openings was little changed

The number of job openings was little changed at 5.5 million on the last business day of November, the U.S. Bureau of Labor Statistics reported today. Over the month, hires and separations were also little changed at 5.2 million and 5.0 million, respectively. Within separations, the quits rate was unchanged at 2.1 percent and the layoffs and discharges rate was unchanged at 1.1 percent. This release includes estimates of the number and rate of job openings, hires, and separations for the nonfarm sector by industry and by four geographic regions.

-

15:00

U.S.: Wholesale Inventories, November 1% (forecast 0.9%)

-

15:00

U.S.: JOLTs Job Openings, November 5.522 (forecast 5.555)

-

14:53

WSE: After start on Wall Street

After yesterday's withdrawal the US market today began trading at a neutral level. For the Warsaw market it does not matter, we are relatively stronger and the WIG20 index remains at a safe height above the level of 2,000 points. An hour before the close of trading it was 2,030 points (+ 1.04%).

-

14:36

Yahoo! (YHOO) will change its name and will reduce the composition of the Board of Directors after the deal with Verizon Communications (VZ)

-

14:34

U.S. Stocks open: Dow -0.20%, Nasdaq +0.13%, S&P -0.04%

-

14:28

Before the bell: S&P futures -0.04%, NASDAQ futures -0.01%

U.S. stock-index futures were flat as investors await U.S. President-elect Donald Trump's news conference (due on Wednesday) and the begining of the earnings season (due this week).

Global Stocks:

Nikkei 19,301.44 -152.89 -0.79%

Hang Seng 22,744.85 +186.16 +0.83%

Shanghai 3,161.89 -9.34 -0.29%

FTSE 7,258.71 +20.94 +0.29%

CAC 4,888.49 +0.92 +0.02%

DAX 11,578.92 +14.93 +0.13%

Crude $52.18 (+0.42%)

Gold $1,182.00 (-0.24%)

-

13:55

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

30

0.52(1.7639%)

17280

Amazon.com Inc., NASDAQ

AMZN

797.03

0.11(0.0138%)

4841

American Express Co

AXP

76.26

0.40(0.5273%)

1521

Apple Inc.

AAPL

118.94

-0.05(-0.042%)

51125

AT&T Inc

T

40.64

-0.16(-0.3922%)

6225

Barrick Gold Corporation, NYSE

ABX

30

0.52(1.7639%)

17280

Caterpillar Inc

CAT

92.99

0.62(0.6712%)

1720

Chevron Corp

CVX

115.66

-0.18(-0.1554%)

3979

Cisco Systems Inc

CSCO

30.15

-0.03(-0.0994%)

871

Citigroup Inc., NYSE

C

60.14

-0.08(-0.1328%)

468

Facebook, Inc.

FB

124.88

-0.02(-0.016%)

46952

Ford Motor Co.

F

12.65

0.02(0.1584%)

26288

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

15.28

0.60(4.0872%)

379016

General Motors Company, NYSE

GM

36.31

0.30(0.8331%)

1400

Google Inc.

GOOG

807.75

1.10(0.1364%)

1481

JPMorgan Chase and Co

JPM

86.1

-0.08(-0.0928%)

935

Microsoft Corp

MSFT

62.65

0.01(0.016%)

18227

Nike

NKE

53.42

0.04(0.0749%)

14522

Procter & Gamble Co

PG

84.39

-0.01(-0.0118%)

200

Tesla Motors, Inc., NASDAQ

TSLA

230.78

-0.50(-0.2162%)

5991

The Coca-Cola Co

KO

41.3

-0.02(-0.0484%)

25501

Travelers Companies Inc

TRV

115.53

-1.79(-1.5257%)

521

Verizon Communications Inc

VZ

52.66

-0.02(-0.038%)

3067

Visa

V

81.8

0.05(0.0612%)

14088

Walt Disney Co

DIS

108.09

-0.27(-0.2492%)

11063

Yahoo! Inc., NASDAQ

YHOO

41.8

0.46(1.1127%)

8001

-

13:49

Upgrades and downgrades before the market open

Upgrades:

American Express (AXP) upgraded to Outperform from Perform at Oppenheimer

Downgrades:

Chevron (CVX) downgraded to Hold from Buy at HSBC Securities

Travelers (TRV) downgraded to Sell from Neutral at Goldman

Goldman Sachs (GS) downgraded to Sell from Neutral at Citigroup

Other:

-

13:44

Option expiries for today's 10:00 ET NY cut

EUR/USD 1.0390-1.0405 (EUR 695 M) 1.0500-1.0510 (EUR 448 M) 1.0515-1.0525 (EUR 415 M) 1.0570-1.0575 (EUR 1,065 M) 1.0600-1.0610 (EUR 191 M) 1.0650-1.0660 (EUR 497 M) 1.0685-1.0700 (EUR 417 M) 1.0750 (EUR 534 M)

GBP/USD 1.2190 (GBP 288 M)

USD/JPY 113.95-114.00 (USD 324 M) 114.20 (USD 200 M) 115.50-115.60 (USD 350 M) 115.95-116.00 (USD 998 M) 117.40-117.50 (USD 658 M) 118.00 (USD 200 M)

AUD/USD 0.7200 (AUD 1,897 M) 0.7290-0.7300 (AUD 449 M) 0.7400 (AUD 595 M)

USD/CAD 1.3280-1.3285 (USD 295 M) 1.3395-1.3400 (USD 290 M)

NZD/USD 0.6900 (NZD 200 M)

-

13:41

Canadian housing starts kept a steady pace in December

The trend measure of housing starts in Canada was 198,053 units in December compared to 200,105 in November, according to Canada Mortgage and Housing Corporation (CMHC). The trend is a six-month moving average of the monthly seasonally adjusted annual rates (SAAR) of housing starts.

"December saw multi-unit construction slow for the third consecutive month in Canada, leading housing starts to trend down," said Bob Dugan, CMHC Chief Economist. "However, 2016 still counted more home starts than 2015. Increased demand for single-detached homes more than offset the decline we're seeing in multi-unit construction - a decline that's in response to efforts to manage current inventories."

-

13:30

Canada: Building Permits (MoM) , November -0.1% (forecast 2.4%)

-

13:14

Canada: Housing Starts, December 207 (forecast 187)

-

12:59

Orders

EUR/USD

Offers 1.0630 1.0650 1.0680 1.0700 1.0725-30 1.0750

Bids 1.0580 1.0560 1.0520 1.0500 1.0480 1.0450 1.0420 1.0400

GBP/USD

Offers 1.2160 1.2180 1.2200 1.2220 1.2250 1.2280 1.2300

Bids 1.2100 1.2080-85 1.2050 1.2030 1.2000 1.1980 1.1950

EUR/GBP

Offers 0.8780 0.8800 0.8830 0.8850 0.8875 0.8900

Bids 0.8700 0.8680-85 0.8660 0.8640 0.8620 0.8600

EUR/JPY

Offers 123.00 123.30 123.60 123.85 124.00-10 124.30 124.50

Bids 122.50 122.30 122.00 121.75 121.50 121.00

USD/JPY

Offers 116.00 116.20 116.50 116.80 117.00 117.20 117.50-55 117.80 118.00

Bids 115.50 115.20 115.00 114.80 114.50 114.30 114.00

AUD/USD

Offers 0.7380-85 0.7400 0.7420-25 0.7450 0.7475 0.7500

Bids 0.7330 0.7300 0.7280 0.7250 0.7230 0.7200

-

12:01

WSE: Mid session comment

In the forenoon phase of today's session, the Warsaw market has consistently realized the growth plan. At the halfway point of trading the level of turnover in the blue chips segment was amounted to PLN 350 million, what is a quite good result. The market is strong and the WIG20 index remains more than 20 points above the level of 2,000 points. Among the largest companies the leader of growth is KGH with approx. 3% rate of increase To favor returned JSW (component of the WIG40 index), which shares gaining over 6%.

In the middle of trading the WIG20 index was at the level of 2.027 points (+0,89%).

-

11:46

Major European stock indices trading in the green zone

European stock indices show a slight increase, fueled by the financial results of companies, as well as higher prices of commodities. At the same time, the British FTSE 100 continues to update the historical highs against the backdrop of sterling's fall.

Some influence on the course of trading provided statistics from Britain and France. According to the British Retail Consortium (BRC) comparable retail sales in the UK in December increased by 1% compared to the same month a year ago. Head of retail department, Paul Martin said that retailers were lucky with the timing. The fact that Christmas fell on Sunday, giving customers the chance to use the weekend for final purchases in shops, which increased sales.

Meanwhile, the statistical office Insee said that the volume of industrial production in France rose in November by 2.2% compared with a decrease of 0.1% in October. Economists had forecast growth of only 0.6%. Thus the data significantly exceeded the expectations of most experts and were the most positive in the last three months. Production of coking coal and refined petroleum products increased by 6.3%, transport equipment by 3.4%. The volume of mineral production grew by 1.5%. Meanwhile, construction fell in November by 0.3%, after rising 2% in the previous month.

The composite index of the largest companies in the region Stoxx Europe 600 rose 0.03 percent, to 363.79. Shares of automobile companies also rose 0.4 percent after the German automaker Volkswagen said that the steady growth of sales in China and Eastern Europe helped offset losses from environmental scandal in major markets. Shares of Volkswagen rose about 1 percent.

Banking stocks show a negative dynamics, as in the Italian banking shows new problems. Popolare di Vicenza and Veneto Banca, which were saved in the past year, have to offer a deal to shareholders, which could cost the banks more than 600 million euros.

Capitalization of WM Morrison rose 4.2 percent after the British retailer has improved its forecast for profit in response to the very high volume of Christmas sales for the past seven years.

Tesco value increased by 4.4 percent, as the retailer recorded the bigest sales among the four largest supermarkets during the 4th quarter of 2016.

At the moment:

FTSE 100 +25.99 7263.76 + 0.36%

DAX +24.74 11588.73 + 0.21%

CAC 40 +4.78 4892.35 + 0.10%

-

10:43

EUR / USD fell moderately, reaching a session low, which was due to recovery of the US dollar, as well as partial profit-taking. Now the pair is trading at $ 1.0583. Important support at $ 1.0510 (January 9 low)

The US Dollar Index, showing the US dollar against a basket of six major currencies, traded down 0.07 percent at 101.85.

-

09:30

Turkish Lira hit record low around 3.7790 per USD in early trade

-

09:17

Goldman: China's Been Trying To Make Yuan Look Good Since Trump's Victory

-

08:39

Major stock markets in Europe trading mixed: FTSE + 0.2%, new record high of 7,256.94, DAX + 0.2%, CAC40 + 0.2%, FTMIB + 0.3%, IBEX -0.2%

-

08:17

WSE: Before opening

WIG20 index opened at 2007.40 points (-0.09%)*

WIG 53095.46 0.17%

WIG30 2312.97 0.20%

mWIG40 4264.40 0.16%

*/ - change to previous close

The cash market started the day from a small discount at modest turnover traditionally focused on KGHM shares. After the first transaction we go up and course of the WIG20 index rises clearly above the level of 2,000 points. In Europe the German DAX gaining approx. 0.2%.

After fifteen minutes of trading the WIG 20 index reached the level of 2,014 points (+ 0.25%).

-

07:48

Fench output bounced back markedly in the manufacturing industry - INSEE

In November 2016, output bounced back markedly in the manufacturing industry (+2.3% after −0.6%). It also grew sharply in the whole industry (+2.2% after −0.1%).

Over the past three months, output grew in the manufacturing industry (+0.6% q-o-q), as well as in the overall industry (+0.7% q-o-q).

Output increased in all branches. It rose sharply in mining and quarrying; energy; water supply (+1.9%), in the manufacture of transport equipment (+1.1%) and in the manufacture of food products and beverages (+0.9%). It soared in the manufacture of coke and refined petroleum products (+16.6%). Finally, it went up slightly in "other manufacturing" (+0.2%) and in the manufacture of machinery and equipment goods (+0.5%).

-

07:45

France: Industrial Production, m/m, November 2.2% (forecast 0.6%)

-

07:22

Positive start of trading expected on the major stock exchanges in Europe: DAX + 0.3%, CAC40 + 0.2%, FTSE + 0.2%

-

07:19

Options levels on tuesday, January 10, 2017

EUR/USD

Resistance levels (open interest**, contracts)

$1.0757 (2312)

$1.0715 (2281)

$1.0683 (356)

Price at time of writing this review: $1.0598

Support levels (open interest**, contracts):

$1.0532 (1104)

$1.0496 (1115)

$1.0450 (2414)

Comments:

- Overall open interest on the CALL options with the expiration date March, 13 is 52302 contracts, with the maximum number of contracts with strike price $1,1500 (3223);

- Overall open interest on the PUT options with the expiration date March, 13 is 59971 contracts, with the maximum number of contracts with strike price $1,0000 (5322);

- The ratio of PUT/CALL was 1.15 versus 1.15 from the previous trading day according to data from January, 9

GBP/USD

Resistance levels (open interest**, contracts)

$1.2411 (252)

$1.2314 (130)

$1.2219 (107)

Price at time of writing this review: $1.2142

Support levels (open interest**, contracts):

$1.2083 (447)

$1.1987 (1666)

$1.1890 (2874)

Comments:

- Overall open interest on the CALL options with the expiration date March, 13 is 15493 contracts, with the maximum number of contracts with strike price $1,2800 (3002);

- Overall open interest on the PUT options with the expiration date March, 13 is 19667 contracts, with the maximum number of contracts with strike price $1,1500 (3214);

- The ratio of PUT/CALL was 1.27 versus 1.20 from the previous trading day according to data from January, 9

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

07:14

WSE: Before opening

Monday's session on the New York stock exchange has brought a historical record of the Nasdaq Comp., which was driven by increases of biotech companies, but also declines in the Dow Jones and S&P 500. The dollar weakened against the yen and euro. Heavily dropped the price of crude oil. The Nasdaq Comp. went up at the close of 0.19 percent, the Dow Jones Industrial fell 0.38 percent. while the S&P 500 lost 0.35 percent.

Yesterday the Warsaw Stock Exchange managed to breach the 2,000 point barrier for the WIG20 index, even under the adverse conditions. Now this movement requires confirmation, and the environment for doing it has not changed and remains unfavorable.

At the beginning of today's session there is no positive information. The British pound remains weak, oil become cheaper and gold was strengthened by uncertainty. In the morning, contracts in the US are slightly weaker. In Asia, the Nikkei lost 0.8% and the only consolation is better behavior of the remaining Asian parquets.

Today's macro calendar does not bring readings valuable for investors. In addition, publication of the results of the Alcoa company has been postponed to January 24. The only plus in the morning is the increase in copper prices.

Polish Finance Ministry confirmed earlier information that is prepared a plan to increase the taxation of foreign currencies assets of the banks to encourage them to voluntary conversion of loans denominated in foreign currencies to the zloty. It is a reminder about the ongoing problem of the domestic banking sector.

-

06:54

Swiss unemplyment rate rose 0.2% in December

Registered unemployment in December 2016 - According to the SECO surveys, at the end of December 2016 159'372 unemployed persons were registered with the Regional Employment Centers (RAV), 10,144 more than in the previous month. The unemployment rate thus rose from 3.3% in November 2016 to 3.5% in the reporting month. Compared to the previous month, unemployment increased by 743 persons (+ 0.5%). Note Media conversation At 10 o'clock in the SECO building at the Holzikofenweg 36 (room 2.U06) in Berne a media discussion takes place. The speakers will then be available for questions and interviews.

-

06:45

Switzerland: Unemployment Rate (non s.a.), December 3.5% (forecast 3.3%)

-

06:36

The growth of China's GDP in 2016 is likely to be about 6.7%

During today's press conference the head of the State Committee for National Development and Reform Commission Xu Shaoshi said that China's GDP growth in 2016 is likely to be about 6.7%. "The growth rate of China's economy in the current year will be from 6.7% up", - said Xu Shaoshi. He added that in the last year there was a difficult situation in the global economy as well as in China's, but in general, the Chinese economy continues to grow steadily due to the processes of structural change in industrial production.

-

06:31

US Dollar lower as investors cautious ahead of Trump news conference

-

06:29

Chinese CPI inflation fell slightly

The consumer price index, published by the State Statistical Office (GUS), China, in December, on an annualized basis, was 2.1%, lower than the previous value, and economists forecast of 2.3%. The calculation of this indicator includes the price of food, clothing, education, health care, transportation, utilities, leisure. The indicator is calculated monthly and is the main indicator of inflation.

Also, China's State Statistical Department reported that the growth of the producer price index that reflects changes in wholesale prices for goods and services in China, in December compared with the same period last year, touched the high for the last five years. PPI rose 5.5%, well above economists' forecast of 4.5% and the previous value of 3.3%.

-

06:25

Australian retail turnover rose 0.2 per cent in November

Australian retail turnover rose 0.2 per cent in November 2016, seasonally adjusted, according to the latest Australian Bureau of Statistics (ABS) Retail Trade figures.

This follows a rise of 0.5 per cent in October 2016.

In seasonally adjusted terms, there were rises in food retailing (0.4 per cent), clothing, footwear and personal accessory retailing (1.7 per cent) and household goods retailing (0.2 per cent). There were falls in cafes, restaurants and takeaway food services (-0.8 per cent), department stores (-0.3 per cent) and other retailing (-0.1 per cent).

-

06:14

Global Stocks

European stocks lost altitude Monday, with Lufthansa, Fresenius and William Hill among the biggest losers after they gave discouraging updates on their businesses.

U.S. stocks retreated Monday as the Dow Jones Industrial Average pulled back further from the psychologically significant 20,000 milestone, although the Nasdaq bucked the weak trend to finish at an all-time closing high for a second session in a row. Equities have been strong performers recently, highlighted by a nearly 10% climb over the past three months. Most of the gains in stocks have been the result of the presidential election in the U.S. Investors have bet that the policies president-elect Donald Trump is expected to support will accelerate economic growth - a bullish scenario for stocks.

China's consumer inflation slowed in December, losing speed for the first time in four months, but producer inflation quickened at a pace much faster than economists expected, official data showed Tuesday. China's consumer price index increased 2.1% in December from a year earlier, rising at slower pace than a 2.3% year-over-year gain in November, the National Bureau of Statistics said, adding that a higher base for comparison from the year-earlier period was the main factor weighing on the headline figure.

-

05:02

Japan: Consumer Confidence, December 43.1 (forecast 41.3)

-

01:30

China: PPI y/y, December 5.5% (forecast 4.5%)

-

01:30

China: CPI y/y, December 2.1% (forecast 2.3%)

-

00:30

Australia: Retail Sales, M/M, November 0.2%

-