Market news

-

23:28

Commodities. Daily history for Feb 13’2017:

(raw materials / closing price /% change)

Oil 52.87 -0.11%

Gold 1,226.10 +0.02%

-

23:27

Stocks. Daily history for Feb 13’2017:

(index / closing price / change items /% change)

Nikkei +80.22 19459.15 +0.41%

TOPIX +7.64 1554.20 +0.49%

Hang Seng +136.00 23710.98 +0.58%

CSI 300 +22.78 3436.27 +0.67%

Euro Stoxx 50 +34.40 3305.23 +1.05%

FTSE 100 +20.17 7278.92 +0.28%

DAX +107.46 11774.43 +0.92%

CAC 40 +59.87 4888.19 +1.24%

DJIA +0.00 20412.16 +0.00%

S&P 500 +12.15 2328.25 +0.52%

NASDAQ +29.83 5763.96 +0.52%

S&P/TSX +27.46 15756.58 +0.17%

-

23:26

Currencies. Daily history for Feb 13’2017:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,0597 -0,38%

GBP/USD $1,2524 +0,32%

USD/CHF Chf1,0056 +0,29%

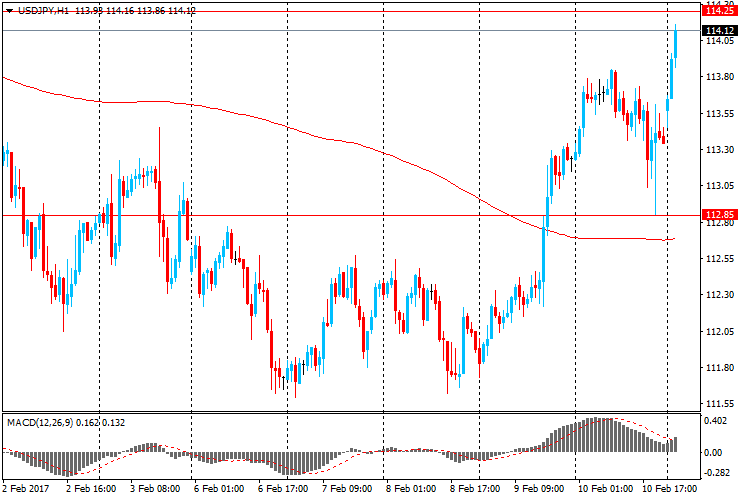

USD/JPY Y113,72 +0,33%

EUR/JPY Y120,53 -0,03%

GBP/JPY Y142,42 +0,65%

AUD/USD $0,7639 -0,45%

NZD/USD $0,7174 -0,28%

USD/CAD C$1,307 -0,11%

-

23:03

Schedule for today, Tuesday, Feb 14’2017 (GMT0)

00:30 Australia National Australia Bank's Business Confidence January 6

01:30 China PPI y/y January 5.5% 6.3%

01:30 China CPI y/y January 2.1% 2.4%

04:30 Japan Industrial Production (MoM) (Finally) December 1.5% 0.5%

04:30 Japan Industrial Production (YoY) (Finally) December 4.6% 3%

07:00 Germany CPI, m/m (Finally) January 0.7% -0.6%

07:00 Germany CPI, y/y (Finally) January 1.7% 1.9%

07:00 Germany GDP (QoQ) (Preliminary) Quarter IV 0.2% 0.5%

07:00 Germany GDP (YoY) (Preliminary) Quarter IV 1.5% 1.7%

08:15 Switzerland Producer & Import Prices, m/m January 0.2%

08:15 Switzerland Producer & Import Prices, y/y January 0.0%

08:15 Switzerland Consumer Price Index (MoM) January -0.1%

08:15 Switzerland Consumer Price Index (YoY) January 0.0% 0.3%

09:30 United Kingdom Producer Price Index - Output (MoM) January 0.1% 0.4%

09:30 United Kingdom Producer Price Index - Output (YoY) January 2.7% 3.2%

09:30 United Kingdom Producer Price Index - Input (MoM) January 1.8% 0.6%

09:30 United Kingdom Producer Price Index - Input (YoY) January 15.8% 18%

09:30 United Kingdom Retail Price Index, m/m January 0.6% -0.4%

09:30 United Kingdom Retail prices, Y/Y January 2.5% 2.8%

09:30 United Kingdom HICP, m/m January 0.5% -0.5%

09:30 United Kingdom HICP, Y/Y January 1.6% 1.9%

09:30 United Kingdom HICP ex EFAT, Y/Y January 1.6% 1.8%

10:00 Eurozone Industrial production, (MoM) December 1.5% -1.5%

10:00 Eurozone Industrial Production (YoY) December 3.2% 1.7%

10:00 Eurozone ZEW Economic Sentiment February 23.2

10:00 Eurozone GDP (QoQ) (Revised) Quarter IV 0.3% 0.5%

10:00 Eurozone GDP (YoY) (Revised) Quarter IV 1.7% 1.8%

10:00 Germany ZEW Survey - Economic Sentiment February 16.6 15

13:30 U.S. PPI, m/m January 0.3% 0.3%

13:30 U.S. PPI excluding food and energy, m/m January 0.2% 0.2%

13:30 U.S. PPI, y/y January 1.6% 1.6%

13:30 U.S. PPI excluding food and energy, Y/Y January 1.6% 1.1%

15:00 U.S. Federal Reserve Chair Janet Yellen Testifies

23:30 Australia Westpac Consumer Confidence February 97.4

-

21:46

New Zealand: Food Prices Index, y/y, January 1.4%

-

21:06

Major US stock indexes finished trading in the "green zone"

Major US stock indexes again renewed record highs, and the total capitalization of the S & P 500 index companies reached $ 20 trillion for the first time in history against the backdrop of Trump comments on tax reform. The US president vowed on Thursday that will make an important statement about the tax reform in the next few weeks, sparking a rally that stalled amid concerns about protectionist attitudes and the lack of clarity with regard to political reforms.

Later, important data, including the producer price index (Tuesday), retail sales, consumer price index and industrial production (Wednesday), as well as the laying of new homes (Thursday) will be released this week. In addition, the focus of attention of market participants gradually shifted to the semi-annual report of the Federal Reserve Chairman Janet Yellen. The head of the Federal Reserve will act to Congress on Tuesday and Wednesday.

Oil prices fell nearly 2 percent, as positive from the OPEC report was offset by signs of increasing production of oil in the United States and a stronger dollar. The pressure on oil futures continued to Baker Hughes' report on the number in the US rig. Recall, on Friday in Baker Hughes reported that according to the results ended February 10 working weeks, the number of drilling rigs in the country has increased by 12 units, or 1.6%, to 741 units, including oil - 8 units, or 1 , 4%, to 591 pieces (up to October 2015), the number of gas-producing plants has increased by 4 points, or 2.8%, to 149 units.

DOW index components closed mostly in positive territory (25 of 30). leaders of growth were shares of Caterpillar Inc. (CAT, + 2.32%). Most remaining shares fell Verizon Communications Inc. (VZ, -0.82%).

All business sectors S & P index ended the session in positive territory. The leader turned out to be the financial sector (+ 0.9%).

At the close:

Dow + 0.70% 20,412.13 +142.76

Nasdaq + 0.52% 5,763.96 +29.83

S & P + 0.52% 2,328.24 +12.14

-

20:00

DJIA +0.75% 20,420.56 +151.19 Nasdaq +0.54% 5,765.35 +31.22 S&P +0.54% 2,328.69 +12.59

-

18:26

Wall Street. Major U.S. stock-indexes rose

Major U.S. stock-indexes hit record intraday highs on Monday, with the S&P 500's market capitalization topping $20 trillion for the first time ever, as the "Trump trade" was jump-started on renewed optimism about the economy. President Donald Trump vowed last Thursday to make a major tax announcement in the next few weeks, rekindling a rally that has stalled amid concerns over his protectionist stance and lack of clarity on policy reforms.

Most of Dow stocks in positive area (23 of 30). Top loser - Verizon Communications Inc. (VZ, -1.01%). Top gainer - Caterpillar Inc. (CAT, +2.56%).

Most of S&P sectors in positive area. Top gainer - Financials (+0.9%). Top loser - Conglomerates (-0.6%).

At the moment:

Dow 20365.00 +142.00 +0.70%

S&P 500 2325.75 +13.00 +0.56%

Nasdaq 100 5254.50 +27.75 +0.53%

Oil 52.87 -0.99 -1.84%

Gold 1225.30 -10.60 -0.86%

U.S. 10yr 2.44 +0.03

-

17:00

European stocks closed: FTSE 100 +20.17 7278.92 +0.28% DAX +107.46 11774.43 +0.92% CAC 40 +59.87 4888.19 +1.24%

-

16:33

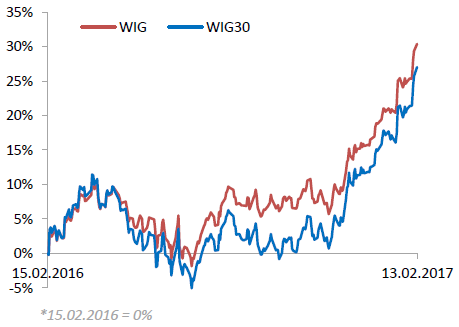

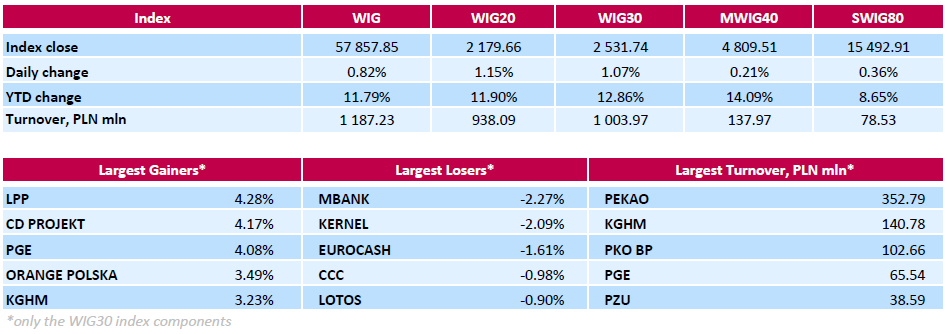

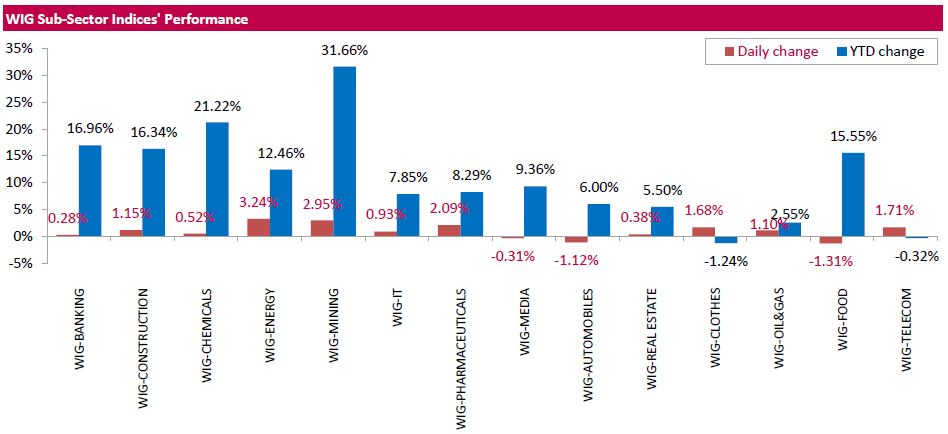

WSE: Session Results

Polish equity market closed higher on Monday. The broad market measure, the WIG Index, surged by 0.82%. The WIG sub-sector indices were mainly higher with energy stocks (+3.24%) outperforming.

The large-cap stocks' measure, the WIG30 Index, advanced 1.07%. Over 2/3 of all index components returned gains, with the way up led by clothing retailer LPP (WSE: LPP), videogame developer CD PROJEKT (WSE: CDR) and genco PGE (WSE: PGE), jumping by 4.28%, 4.17% and 4.08% respectively. PGE released it estimated its 2016 net profit to amount to PLN 2.45 bln ($604.95 mln) compared to a PLN 3-billion loss in 2015. Other major gainers were telecommunication services provider ORANGE POLSKA (WSE: OPL), copper producer KGHM (WSE: KGH) and three utilities names ENEA (WSE: ENA), ENERGA (WSE: ENG) and TAURON PE (WSE: TPE), surging by 2.38%-3.49%. On the other side of the ledger, bank MBANK (WSE: MBK) and agricultural producer KERNEL (WSE: KER) topped decliners' list, falling by 2.27% and 2.09% respectively.

-

15:46

Gold traded at 1 week lows

Gold prices fell to a more than one-week low on Monday, as a stronger dollar weighed on the metal and investors awaited a meeting from the Federal Reserve later this week, says Dow Jones.

Spot gold fell by 0.43% to $1,230.60 a troy ounce in midmorning trade in Europe, the lowest price since Feb. 3.

On Monday, the WSJ Dollar Index, which weighs the dollar against a basket of other currencies, was up 0.08%. A stronger dollar is often bearish for gold and other dollar-denominated commodities, because it makes the metal more expensive for investors who hold other currencies.

Investors were waiting for comments from Federal Reserve Chairwoman Janet Yellen on Tuesday and Wednesday. However, a rate increase isn't expected until June, according to Fed fund futures tracked by CME.

-

14:51

WSE: After start on Wall Street

The Americans started the new week on continued upward movement, encouraged by, among others, today's optimism in Europe. All three major indexes begin trading from new historical records.

In Warsaw market, an hour before the close of trading the WIG20 index was at the level of 2,175 points (+0,98%) and the turnover in the segment of blue chips was amounted to PLN 750 million.

-

14:48

Forces likely to keep euro subdued near term - CIBC

"Although Eurozone growth has accelerated recently, there's reason to remain cautious on the currency in the near-term.

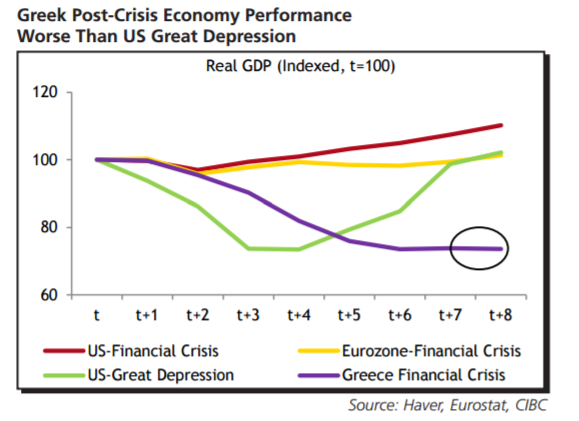

With the economy only recently eclipsing its pre-crisis high-water mark, the material output gap will keep monetary policy stimulative for some time. The rise of populism will also weigh on the euro ahead of a number of key elections in the region this year, and Greek debt negotiations are making headlines again.

Relative to its pre-crisis level, the Greek economy is now down by a magnitude similar to the US during the worst of the Great Depression. Greece's plight has been more protracted, in part because Eurozone monetary policy remains too restrictive for the hardest hit countries. If debt negotiations heat up further, expect renewed speculation as to whether Greece would be better off leaving the union".

CIBC targets EUR/USD at 1.04 by the end of Q1.

Copyright © 2017 CIBC, eFXnews™

-

14:34

U.S. Stocks open: Dow +0.37%, Nasdaq +0.38%, S&P +0.31%

-

14:29

Before the bell: S&P futures +0.22%, NASDAQ futures +0.17%

U.S. stock-index futures advanced, as stocks continued to be supported by President Donald Trump's promise to unveil a "phenomenal" tax reform plan in the coming weeks.

Global Stocks:

Nikkei 19,459.15 +80.22 +0.41%

Hang Seng 23,710.98 +136.00 +0.58%

Shanghai 3,217.22 +20.52 +0.64%

FTSE 7,271.98 +13.23 +0.18%

CAC 4,892.47 +64.15 +1.33%

DAX 11,787.62 +120.65 +1.03%

Crude $53.45 (-0.76%)

Gold $1,228.00 (-0.64%)

-

13:58

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

3M Co

MMM

179.72

0.72(0.4022%)

833

ALTRIA GROUP INC.

MO

29.84

0.12(0.4038%)

20870

Amazon.com Inc., NASDAQ

AMZN

832.51

5.05(0.6103%)

27010

American Express Co

AXP

78.68

0.20(0.2548%)

401

AMERICAN INTERNATIONAL GROUP

AIG

65.81

0.20(0.3048%)

738

Apple Inc.

AAPL

29.84

0.12(0.4038%)

20870

AT&T Inc

T

244.21

1.49(0.6139%)

9445

Barrick Gold Corporation, NYSE

ABX

19.18

-0.31(-1.5906%)

48403

Boeing Co

BA

165

-1.23(-0.7399%)

9011

Chevron Corp

CVX

113.41

0.36(0.3184%)

3206

E. I. du Pont de Nemours and Co

DD

77.14

0.31(0.4035%)

1482

Facebook, Inc.

FB

244.21

1.49(0.6139%)

9445

Ford Motor Co.

F

12.54

0.03(0.2398%)

30737

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

29.84

0.12(0.4038%)

20870

General Electric Co

GE

29.84

0.12(0.4038%)

20870

General Motors Company, NYSE

GM

29.84

0.12(0.4038%)

20870

Goldman Sachs

GS

244.21

1.49(0.6139%)

9445

Google Inc.

GOOG

117.64

-2.09(-1.7456%)

5526

Home Depot Inc

HD

140.5

0.65(0.4648%)

1379

Intel Corp

INTC

35.41

0.07(0.1981%)

5557

International Business Machines Co...

IBM

178.92

0.24(0.1343%)

2501

International Paper Company

IP

117.64

-2.09(-1.7456%)

5526

Johnson & Johnson

JNJ

244.21

1.49(0.6139%)

9445

JPMorgan Chase and Co

JPM

87.34

0.34(0.3908%)

17616

Microsoft Corp

MSFT

64.11

0.11(0.1719%)

12664

Nike

NKE

29.84

0.12(0.4038%)

20870

Pfizer Inc

PFE

32.39

0.04(0.1236%)

5315

Procter & Gamble Co

PG

88.35

0.38(0.432%)

1543

Tesla Motors, Inc., NASDAQ

TSLA

117.64

-2.09(-1.7456%)

5526

The Coca-Cola Co

KO

40.72

0.14(0.345%)

18129

Travelers Companies Inc

TRV

117.64

-2.09(-1.7456%)

5526

Twitter, Inc., NYSE

TWTR

15.62

0.04(0.2567%)

209770

United Technologies Corp

UTX

117.64

-2.09(-1.7456%)

5526

UnitedHealth Group Inc

UNH

160.69

-0.06(-0.0373%)

2854

Verizon Communications Inc

VZ

29.84

0.12(0.4038%)

20870

Visa

V

86.22

0.32(0.3725%)

2043

Wal-Mart Stores Inc

WMT

29.84

0.12(0.4038%)

20870

Walt Disney Co

DIS

109.22

-0.04(-0.0366%)

5752

Yandex N.V., NASDAQ

YNDX

29.84

0.12(0.4038%)

20870

-

13:55

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Travelers (TRV) downgraded to Mkt Perform from Outperform at FBR & Co.; target $119

Boeing (BA) downgraded to Underperform from Neutral at Buckingham Research

Other:

Apple (AAPL) target raised to $150 from $133 at Goldman

-

13:49

Option expiries for today's 10:00 ET NY cut

EUR/USD: 1.0600-05 (EUR 693m) 1.0650 (955m) 1.0700 (887m) 1.0780 (1.33bln) 1.0950 (880m)

USD/JPY: 112.00 (USD 607m) 112.50 (350m) 114.00 (670m) 115.00 (465m)

GBP/USD: 1.2565-70 (GBP 437m) 1.2600 (469m)

AUD/USD: 0.7400 (AUD 571m)

USD/CAD 1.2975 (USD 485m)

-

13:42

ING Sees EUR/USD Fall to $1.05 This Week, USD/JPY at 115

-

13:12

OPEC Monthly Oil Market Report

The OPEC Reference Basket averaged $52.40/b in January, representing a gain of 73¢ over the previous month. NYMEX WTI and ICE Brent also saw gains, increasing by 44¢ and 53¢ to average $52.61/b and $55.45/b, respectively. Production adjustments by OPEC and some non-OPEC producers supported the market, although gains were capped by increased drilling activity in the US. The Brent-WTI spread widened slightly to average $2.84/b in January.

Global economic growth expectations remain at 3.0% in 2016 and 3.2% in 2017. OECD growth in 2017 was revised up to 1.9%, following upward adjustments in the Euro-zone and UK. US economic growth remains unchanged at 2.2%. Forecasts for China and India in 2017 also remain unchanged at 6.2% and 7.1%, respectively. Russia's 2017 growth was revised up to 1.0%, while Brazil's growth forecast remains unchanged at 0.4%.

World oil demand growth in 2016 is expected to increase by 1.32 mb/d, following an upward adjustment of 70 tb/d to reflect continued better-than-expected consumption in OECD Europe and Asia Pacific. Total oil demand is now estimated to average 94.62 mb/d, taking into account base line adjustments to China of around 0.12 mb/d. In 2017, world oil demand growth is seen to reach 1.19 mb/d, representing an upward revision of 35 tb/d to now average 95.81 mb/d.

-

13:00

Orders

EUR/USD

Offers: 1.0680 1.0700-05 1.0730 1.0750

Bids: 1.0620 1.0600 1.0580 1.0550 1.0520 1.0500

GBP/USD

Offers: 1.2550 1.2580 1.2600 1.2630 1.2650 1.2685 1.2700

Bids: 1.2500 1.2480 1.2450 1.2430 1.2400 1.2380 1.2345-50

EUR/GBP

Offers: 0.8520 0.8535 0.8550 0.8585 0.8600 0.8630-35 0.8650

Bids: 0.8480-85 0.8465 0.8450 0.8430 0.8400

EUR/JPY

Offers: 121.35 121.50 121.80 122.00 122.50

Bids: 121.00 120.80 120.50 102.30 120.00 119.75 119.50

USD/JPY

Offers: 113.80 114.00 114.20 114.50 114.75 115.00

Bids: 113.20 113.00 112.80 112.50 112.00

AUD/USD

Offers: 0.7685-90 0.7700 0.7730 0.7750 0.7780 0.7800

Bids: 0.7660 0.7620 0.7600 0.7580 0.7550 0.7520 0.7500

Информационно-аналитический отдел TeleTrade

-

12:03

WSE: Mid session comment

The light consolidation on the Warsaw market in the first hour of trading was a base for further expansion of the upward move, which ultimately resulted in increases above 1% for the WIG20 index. The driving force behind growth is today the energy sector, where an actuating impulse proved to be the results of PGE.

At the halfway point of quotations the WIG20 index stood at the level of 2,181 points (+1,26%). The turnover is satisfactory and in the segment of the largest companies was amounted to more than PLN 350 million.

-

11:51

Major European stock indices trading in positive territory

The stock indexes in Western Europe are rising for a fifth straight session, while the British FTSE 100 rose to 4 weeks high due to the rise in quotations of mining companies.

The composite index of the largest companies in the region Stoxx Europe 600 rose by 0.3% - to 368.50 points.

Mining stocks rise in price on Monday due to the rise in copper and iron ore prices.

Mining sector index gained 1.3%, before reaching August 2014 highs, after the price of copper rose to 20 months high because of concerns about supplies.

Price of Rio Tinto shares rose by 12%, BHP Billiton +2,1%, Anglo American rose 1,9%, Fresnillo +1.5%.

Investors also reacted to the results of the meeting between Donald Trump and Japanese Prime Minister Shinzo Abe. "The United States supports its ally", - said D.Tramp, which reduced fears about the complications of trade relations between the two countries.

Today will be held a meeting between D.Trump with the Prime Minister of Canada Justin Trudeau.

"Investors have calmed down since Trump previous position caused some concern, not to mention the prospects of the deterioration of trade relations with the region and the overall protection of foreign policy", - says Ekrlem Craig, senior analyst at Oanda.

The market value of pharmaceutical company Stada Arzneimittel AG jumped 13% after the company announced the 2 proposals to purchase one of which - from a private investment company Cinven Partners LLP.

Share of Royal Bank of Scotland rose 1.3%. The Bank has announced plans to cut $ 1 billion in costs annually.

Saab shares fell by 5.5%, as the company's financial performance for the fourth quarter of last year fell short of market expectations.

At the moment:

FTSE 7262.45 3.70 0.05%

DAX 11734.46 67.49 0.58%

CAC 4864.25 35.93 0.74%

-

11:09

Oil is trading lower

This morning, the New York futures for Brent fell 0.78% to $ 56.26 and WTI fell 0.84% to $ 53.42. Recall OPEC members and Russia agreed to reduce production by about 1.8 million barrels per day in order to restore balance in the global supply. Russia in January has reduced production to 11.11 million bpd from 11.21 million bpd in December 2016.

At the same time, drilling rigs in the US rose by 8 to 591 units, Baker Hughes data. This is the highest since October 2015.

-

10:07

EU Sees GDP Growth Throughout Bloc in 2016-2018 For The First Time Since 2008 - Dow Jones. Economic forecasts

-

EU Deficit at 1.6% in 2018, In Line With Previous Forecast

-

EU Deficit at 1.7% in 2017, In Line With Previous Forecast

-

EU Unemployment at 7.8% in 2018, Down From 7.9% Previously Forecast

-

EU Unemployment at 8.1% in 2017, Down From 8.3% Previously Forecast

-

EU Inflation at 1.7% in 2018, In Line With Previous Forecast

-

EU Inflation at 1.8% in 2017, Up From 1.6% Previously Forecast

-

Eurozone Inflation at 1.7% in 2017, Up From 1.4% Previously Forecast

-

Eurozone Growth at 1.8% in 2018, Up From 1.7% Previously Forecast

-

European Commission Sees Uncertainty Slowing Business Investment

-

European Commission: Impact in Economy of Brexit Vote Yet to be Felt

-

EU Sees German 2017 GDP +1.6% on Year

-

-

09:53

Option expiries for today's 10:00 ET NY cut

EUR/USD: 1.0600-05 (EUR 693m) 1.0650 (955m) 1.0700 (887m) 1.0780 (1.33bln) 1.0950 (880m)

USD/JPY: 112.00 (USD 607m) 112.50 (350m) 114.00 (670m) 115.00 (465m)

GBP/USD: 1.2565-70 (GBP 437m) 1.2600 (469m)

AUD/USD: 0.7400 (AUD 571m)

USD/CAD 1.2975 (USD 485m)

Информационно-аналитический отдел TeleTrade

-

09:38

India’s prospects of still-higher oil prices and core inflation being sticky should prevent the central bank from lowering interest rates any further - DBS

-

08:59

Major stock markets in Europe trading in the green zone: FTSE 100 7,270.18 11.43 0.16%, DAX 11,696.73 29.76 0.26%, CAC 40 4,845.27 16.95 0.35%, IBEX 35 9,407.80 29.70 0.32%, Stoxx 600 368.23 0.84 0.23%

-

08:39

Moody's Investors Service says that liquidity conditions in China's financial system appear to be tightening

"We expect that a combination of tighter liquidity conditions and stricter regulatory scrutiny on the banks' off-balance-sheet activities will curb the banks' incentives to engage in regulatory arbitrage and gradually dampen the fast-growing component of shadow banking activities," says Michael Taylor, a Moody's Managing Director and Chief Credit Officer for Asia Pacific.

On the other hand, demand from shadow bank borrowers will be relatively inelastic to higher interest rates, given the continuing financing needs in sectors such as property, local government financing vehicles and overcapacity industries.

Moody's also says that the composition of credit flows are undergoing important shifts, even while economy-wide leverage continues to increase.

In recent months, credit flows have been sustained by bank lending and "core" shadow banking. Mortgage loans have continued to contribute a rising share of headline bank lending, while in Q4 2016, the growth rate of trust loans registered its first significant increase since mid-2014.

-

08:17

WSE: After opening

WIG20 index opened at 2161.17 points (+0.30%)*

WIG 57658.42 0.48%

WIG30 2518.87 0.55%

mWIG40 4809.77 0.22%

*/ - change to previous close

The cash market (the WIG20 index) opened with increase of 0.3% at a high turnover focused on gaining KGHM shares. It also stands out the PGE, which published better than expected results. This situation supports other energy companies. As a result, we are dealing with another positive opening and enlargement of growth after the first transaction.

After fifteen minutes of trading the WIG20 index was at the level of 2,163 points (+0,39%).

-

08:10

US, South Korea and Japan request UN meeting on North Korea missile launch @Livesquawk

-

08:09

Today’s events

-

At 10:00 GMT Italy will hold an auction of 30-year bonds

-

At 10:00 GMT The European Commission will publish the EU economic forecast

-

At 11:00 GMT the Bundesbank Monthly Report

-

-

07:31

Positive start of trading expected on the major stock exchanges in Europe: DAX + 0.6%, CAC40 + 0.5%, FTSE + 0.2%

-

07:30

RBS gives 4 reasons for structurally bullish USD against EUR & JPY

"We remain bullish on the dollar expecting the euro and yen to trade in weaker ranges of 1.00-1.10 and 115-125 this year.

First, US data flow remains consistent with the Federal Open Market Committee hiking interest rates three times in 2017. January's employment report showed payrolls rising by 227k. Though revisions shaved 39k off the prior two months' payrolls, current job gains are 'well above the pace of 75,000 to 125,000 per month that is probably consistent with keeping the unemployment rate stable over the longer run' as Fed Chair Yellen observed in her January 19 economic outlook speech.

Second, Fed officials continue to see further rate rises this year. The January 31-February 1 FOMC statement was little changed from December's. But policymakers acknowledged the improvement in 'animal spirits' seen since November's elections by adding the line 'measures of consumer and business sentiment have improved of late.' Short term rates markets have little priced for the next FOMC meeting on March 14-15.

Third, market expectations for near term fiscal loosening may have ebbed as the White House and Congress negotiate on border adjustment and corporate and income tax policies. But if the Trump administration finds agreement with the Republican leadership in the next few weeks, the dollar, stocks and Treasury yields will rally sharply again. The new president is due to give a state of the union address on February 28.

Last, the Trump administration's latest immigration policies are unlikely to lead to a sharp re-allocation of Middle East funds away from the US as occurred in 2002 after the Bush administration's response to the September 11 2001 terror attacks. The new restrictions on arrivals from seven Middle East and North African countries did not include citizens from the largest holders of capital in the region - Saudi Arabia, Kuwait, Qatar and the United Arab Emirates.

The main risk in the near term for dollar bulls remains the lack of a clear, near term catalyst from either the Fed or the new US administration to spark a new round of greenback buying.

The next key events will be Yellen's 'Humphrey-Hawkins' testimony on February 14-15 and the FOMC minutes on February 22".

Copyright © 2017 RBS, eFXnews™

-

07:27

ECB's Villeroy: French Don't Wish to Exit from Eurozone

-

French Economic Growth Seen at 1.3% in 2017

-

Exit from Eurozone Would Cost France EUR30B Per Year

-

-

07:25

The yen fell after the publication of weaker-than-expected Japanese GDP data

USD / JPY has risen more than 50 points, breaking the level of Y114.00, after Japan's GDP for the fourth quarter, which turned out to be weaker than expected.

According to the Cabinet of Ministers of Japan, Japan's GDP in the fourth quarter, seasonally adjusted, increased by 0.2%, lower than economists forecast and the previous value of 0.3%. On an annualized basis, Japan's economy grew by 1.0%, which is below the forecast of 1.1%. However, the value of the third quarter was revised from 1.3% to 1.4% GDP report expresses the total value of all final goods and services in monetary terms, made by Japan for a certain period of time. This is the main macroeconomic indicators of market activity because it assesses the growth or decline of the economy.

Nominal GDP increased by 0.3% after +0.2% prior. This was an increase for the fourth quarter in a row. The GDP deflator, indicating the rate of inflation, dropped by 0.1%, while analysts expected a decline of -0.2%.

Consumer spending in the fourth quarter remained flat after rising 0.3% in the third quarter, but business spending increased by 0.9% after declining 0.3% previously.

Exports expanded rapidly since the fourth quarter of 2014. The contribution of external demand to GDP was + 0.2%, domestic demand flat.

-

07:20

WSE: Before opening

Friday's session on the New York stock exchange ended with increases in the major indexes. Dow Jones, S & P 500 and Nasdaq once again reached historical peaks. The market received a positive announcement rapid presentation by Donald Trump's plan for tax cuts, which are to stimulate the economy to faster growth.

This morning brings a slight growth in Asian markets, which results in a slight increase of contracts in the US and promises an optimistic start in Europe. In addition, the price of copper is rising an is the highest since May 2015.

-

07:16

German selling prices in wholesale trade increased by 4.0% in January

As reported by the Federal Statistical Office (Destatis), the selling prices in wholesale trade increased by 4.0% in January 2017 from the corresponding month of the preceding year. In December 2016 and in November 2016 the annual rates of change were +2.8% and +0.8%, respectively. From December 2016 to January 2017 the index rose by 0.8%.

-

06:31

Global Stocks

European stocks advanced for a fourth straight day on Friday, boosted by optimism over strong export data from China and a round of upbeat corporate results. Mining companies helped propel the index higher on Friday, after China said its exports jumped 7.9% in January, up from a 6.1% drop in December. As China is a major user of natural resources, any hint of strong economic growth in the country tends to buoy the commodity sector.

U.S. stock-market indexes registered fresh records Friday and posted a third straight weekly gain, as investors focused on President Donald Trump's pledge to move quickly on changes to the tax code-which has the potential to deliver a jolt to corporate earnings. Friday's record closes come a day after all three main indexes closed at all-time highs, after Trump promised to announce a "phenomenal" tax policy in a few weeks.

Global stocks kicked off the week on a positive note, with markets in Asia extending gains, as recent actions by President Donald Trump helped soothe investor worries about ties between the U.S. and its key Asian trading partners. At a joint appearance over the weekend with Japanese Prime Minister Shinzo Abe, Trump said that the "United States of America stands behind Japan, its great ally, 100%," following the launch of a ballistic missile by North Korea that landed in the Sea of Japan.

-

06:02

Options levels on monday, February 13, 2017

EUR/USD

Resistance levels (open interest**, contracts)

$1.0751 (2697)

$1.0702 (2711)

$1.0672 (1349)

Price at time of writing this review: $1.0627

Support levels (open interest**, contracts):

$1.0592 (3471)

$1.0569 (3657)

$1.0541 (4868)

Comments:

- Overall open interest on the CALL options with the expiration date March, 13 is 67892 contracts, with the maximum number of contracts with strike price $1,0800 (4937);

- Overall open interest on the PUT options with the expiration date March, 13 is 79417 contracts, with the maximum number of contracts with strike price $1,0000 (5089);

- The ratio of PUT/CALL was 1.17 versus 1.17 from the previous trading day according to data from February, 10

GBP/USD

Resistance levels (open interest**, contracts)

$1.2702 (2986)

$1.2704 (2184)

$1.2607 (2146)

Price at time of writing this review: $1.2499

Support levels (open interest**, contracts):

$1.2392 (1894)

$1.2295 (3568)

$1.2197 (1482)

Comments:

- Overall open interest on the CALL options with the expiration date March, 13 is 33369 contracts, with the maximum number of contracts with strike price $1,2500 (3518);

- Overall open interest on the PUT options with the expiration date March, 13 is 37066 contracts, with the maximum number of contracts with strike price $1,2300 (3568);

- The ratio of PUT/CALL was 1.11 versus 1.13 from the previous trading day according to data from February, 10

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-