Market news

-

23:30

Commodities. Daily history for Nov 21’2016:

(raw materials / closing price /% change)

Oil 47.48 -0.02%

Gold 1,214.00 +0.35%

-

23:29

Stocks. Daily history for Nov 21’2016:

(index / closing price / change items /% change)

Nikkei 225 18,106.02 0.00 0.00%

Shanghai Composite 3,218.21 +25.35 +0.79%

S&P/ASX 200 5,364.00 +12.66 +0.24%

FTSE 100 6,777.96 +2.19 +0.03%

CAC 40 4,529.58 +25.23 +0.56%

Xetra DAX 10,685.13 +20.57 +0.19%

S&P 500 2,198.18 +16.28 +0.75%

Dow Jones Industrial Average 18,956.69 +88.76 +0.47%

S&P/TSX Composite 15,039.87 +175.84 +1.18%

-

23:28

Currencies. Daily history for Nov 21’2016:

(pare/closed(GMT +3)/change, %)

EUR/USD $1,0629 +0,38%

GBP/USD $1,2488 +1,08%

USD/CHF Chf1,0086 -0,13%

USD/JPY Y110,81 0,00%

EUR/JPY Y117,78 +0,37%

GBP/JPY Y138,42 +1,11%

AUD/USD $0,7336 +0,01%

NZD/USD $0,7065 +0,72%

USD/CAD C$1,3416 -0,68%

-

23:00

Schedule for today,Tuesday, Nov 22’2016

07:00 Switzerland Trade Balance October 4.37

09:30 United Kingdom PSNB, bln October -10.12

11:00 United Kingdom CBI industrial order books balance November -17 -8

13:30 Canada Retail Sales, m/m September -0.1% 0.6%

13:30 Canada Retail Sales YoY September 1.6%

13:30 Canada Retail Sales ex Autos, m/m September 0.0%

15:00 Eurozone Consumer Confidence (Preliminary) November -8 -7.8

15:00 U.S. Richmond Fed Manufacturing Index November -4

15:00 U.S. Existing Home Sales October 5.47 5.42

21:45 New Zealand Retail Sales, q/q Quarter III 2.3%

21:45 New Zealand Retail Sales YoY Quarter III 6%

21:45 New Zealand PPI Input (QoQ) Quarter III 0.9%

21:45 New Zealand PPI Output (QoQ) Quarter III 0.2%

-

21:06

Major US stock indexes finished trading growth

Major US stock indexes showed a moderate increase, as investors bet on Trump's policy, and expect that the market will be friendly. The dynamics of trading was also influenced by comments the vice-chairman of the US Federal Reserve Stanley Fischer and rising oil prices.

Mr. Fisher in his speech on Monday, said that some of the fiscal measures proposed by Trump, in particular those that improve productivity, can improve the capacity of the economy and help counter some of the long-term economic problems. However, as noted by the deputy chairman of the Fisher, there is not much room to increase the deficit without negative consequences in the future.

Oil prices rose by about 4 per cent, its highest level in three weeks, the reason for that was the weakening of the US dollar and investors' hopes to reach agreement by OPEC to reduce oil output in late November. In late September, at an informal meeting of OPEC in Algeria agreed production limit in the range of 32,5-33 mln. Barrels of oil per day, but on specific limits for each of the countries is no agreement.

Among the corporate nature of the message it is worth noting the news that on Friday, Facebook board (FB) approved the buyback of own shares of class A in the amount of up to $ 6 billion. According to the company, the repurchase program will enter into force in the first quarter of 2017 and will not be have a fixed expiration date. At the same time the company Citigroup (C) announced an increase in share repurchase program by $ 1.75 billion.

DOW index components closed mostly in positive territory (23 of 30). Most remaining shares grew E. I. du Pont de Nemours and Company (DD, + 1.74%). Outsider were shares of 3M Company (MMM, -0.93%).

All business sectors S & P index ended the day higher. The leader turned out to be the basic materials sector (+ 2.2%).

At the close:

Dow + 0.47% 18,956.62 +88.69

Nasdaq + 0.89% 5,368.86 +47.35

S & P + 0.75% 2,198.18 +16.28

-

20:00

DJIA +0.39% 18,942.24 +74.31 Nasdaq +0.77% 5,362.62 +41.11 S&P +0.63% 2,195.74 +13.84

-

17:00

European stocks closed: FTSE 100 +2.19 6777.96 +0.03% DAX +16.56 10681.12 +0.16% CAC 40 +23.61 4527.96 +0.52%

-

16:55

Wall Street. Major U.S. stock-indexes rose

Major U.S. stock-indexes slightly rose as investors bet Donald Trump's policies would be market friendly. The Nasdaq hit a record intraday high on Monday, while the S&P and the Dow were within a hair's breadth of their all-time highs, helped by a jump in technology shares and as a surge in oil prices boosted energy stocks.

Oil prices jumped more 3,5% to a near three-week high on hopes that the OPEC would agree to an output cut next week and the dollar index first drop in 11 days.

Most of Dow stocks in positive area (22 of 30). Top gainer - Apple Inc. (AAPL, +1.62%). Top loser - 3M Company (MMM, -0.99%).

All S&P sectors in positive area. Top gainer - Basic Materials (+2.0%).

At the moment:

Dow 18886.00 +33.00 +0.18%

S&P 500 2190.50 +9.75 +0.45%

Nasdaq 100 4846.75 +38.25 +0.80%

Oil 48.04 +1.68 +3.62%

Gold 1210.90 +2.20 +0.18%

U.S. 10yr 2.33 +0.00

-

16:43

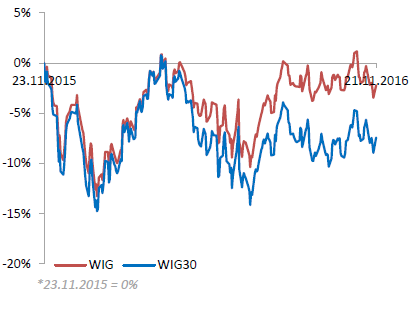

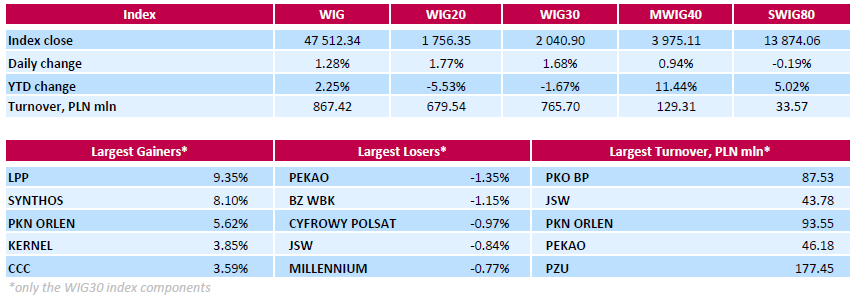

WSE: Session Results

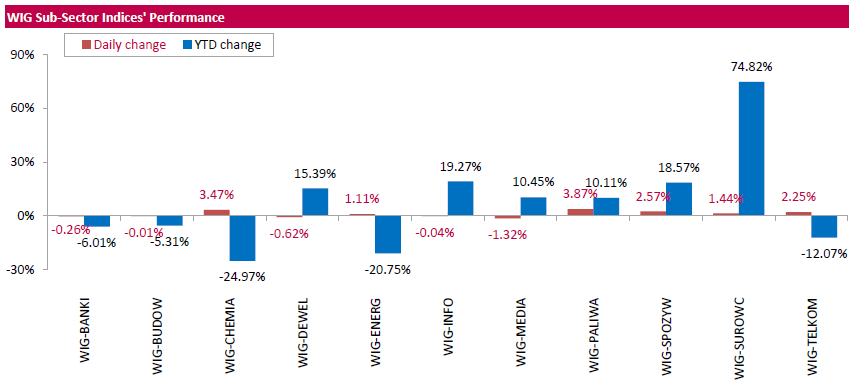

Polish equity market surged on Monday. The broad market measure, the WIG index, rose by 1.28%. Sector performance within the WIG Index was mixed. Oil and gas (+3.87%) fared the best, while media (-1.32%).fell the most.

The large-cap stocks' measure, the WIG30 Index, gained 1.68%. In the index basket, clothing retailer LPP (WSE: LPP) and chemical producer SYNTHOS (WSE: SNS) were the biggest advancers, climbing by 9.35% and 8.1% respectively. The latter was helped by the announcement the company's management decided to offer PLN 701.3 mln advance dividend from 2016 profit (or PLN 0.53 per share). Other noticeable risers were agricultural producer KERNEL (WSE: KER), footwear retailer CCC (WSE: CCC) and two oil refiners LOTOS (WSE: LTS) and PKN ORLEN (WSE: PKN), which added between 3.44% and 5.62%. On the other side of the ledger, banking names PEKAO (WSE: PEO) and BZ WBK (WSE: BZW) led the decliners, dropping by 1.35% and 1.15% respectively. They were followed by media group CYFROWY POLSAT (WSE: CPS), coking coal miner JSW (WSE: JSW) and bank MILLENNIUM (WSE: MIL), which dropped by 0.97%, 0.84% and 0.77% respectively.

-

15:54

Gold price rose helped by a weaker dollar

Gold price rose Monday, as a weaker dollar lifted the metal from recent lows.

Gold for December delivery was up 0.4% at $1,213.40 a troy ounce on the Comex division of the New York Mercantile Exchange.

The Wall Street Journal Dollar Index, which weighs the U.S. currency against a basket of 16 others, was recently down 0.5% at 91.18. Gold is priced in dollars and becomes more affordable to foreign buyers when the currency declines.

Monday's move came on the heels of a 4.7% decline in gold prices this month, as fading political uncertainty and increasing expectations that the Federal Reserve will soon raise interest rates dragged the metal to its lowest level since February, according to Dow Jones.

Gold pays nothing to its holders and struggles to compete with yield-bearing investments when rates rise.

-

15:49

Aussie leading index up 0.5% in September

The Conference Board Leading Economic Index®(LEI) for Australia increased 0.5 percent in September 2016 to 104.5 (2010=100) and the Conference Board Coincident Economic Index®(CEI) increased 0.1 percent in September 2016 to 110.9 (2010=100). This index is designed to predict the direction of the economy, but it tends to have a muted impact because most of the indicators used in the calculation are released previously.

-

15:30

Australia: Conference Board Australia Leading Index, September 0.5%

-

15:21

OECD GDP doubled in the 3rd quarter

Real gross domestic product of the Member States of the Organization for Economic Cooperation and Development has grown significantly in the third quarter, data showed today.

GDP growth accelerated to to 0.6 percent from 0.3 percent in the second quarter. Growth accelerated in most major economies of the group of seven, with the exception of the UK and Germany, where growth slowed in the third quarter.

In the United States the growth improved to 0.7 percent compared with 0.4 percent in the previous quarter.

The growth also improved in Japan to 0.5 percent from 0.2 percent, and in France and Italy 0.3 percent and 0.2 percent, respectively. In the eurozone, growth was steady at 0.3 percent.

In annual terms, GDP growth of OECD countries was 1.7 percent, little changed compared with the previous quarter at 1.6 per cent.

-

14:52

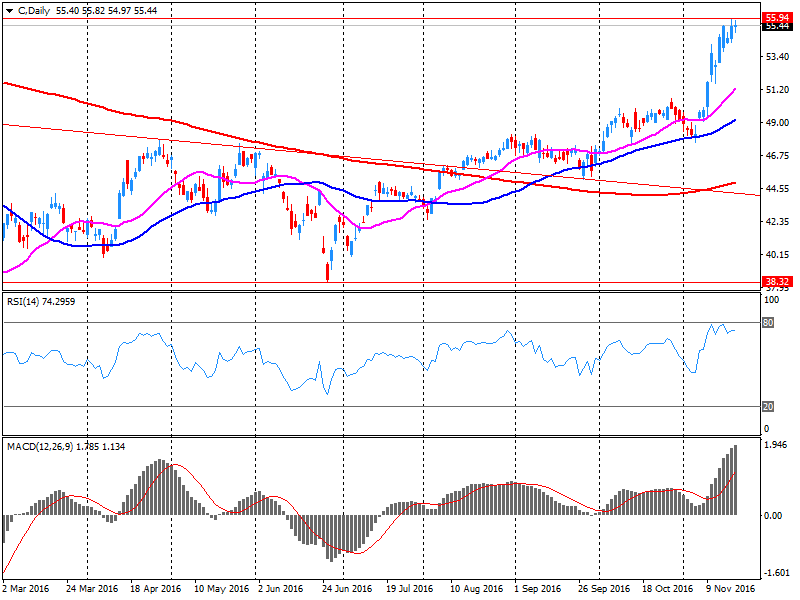

Company news: Citigroup (C) announced an increase of buyback program of $ 1.75 billion

Thus, the total amount of buybacks, taking into account those which the company announced earlier this year (including an increase in the quarterly dividend on Citi common stock to $ 0.16 / share and total share buyback program of up to $ 8.6 billion.) will total $ 10.4 bln to $ 12.2 billion.

Citi shares rose to a high of $ 55.90 (+ 0.79%).

-

14:51

WSE: After start on Wall Street

Published data from the national economy were not good. Virtually all surprised negatively, with the worst fall out of investments (the decrease in construction output by 20.1%). It did not help one working day less, but even after taking it into account the total production increased by 1.3% y/y. From the point of view of the Warsaw Stock Exchange, it is essential the poor performance of processing activities (down 0.5%). Better looks consumption but still disappointing. Moreover we may see rising of producer prices, which means the pressure on the profit margins of companies.

In general, the opening of the fourth quarter is weak. In the case of large companies (whose results are not so dependent on the domestic economy) it does not really matter, these data are more likely to affect the valuation of smaller companies. As we may see at the chart of the sWIG80, it stands out today with weakness and is close to the lows from Friday. There was also no correction on the Polish zloty, which may suggest a signal of changes in the quotations of our currency.

The American market began from a quite big increase. An hour before the close of trading in Warsaw, the WIG20 index was at the level of 1,753 points (+1,63%).

-

14:34

U.S. Stocks open: Dow +0.23%, Nasdaq +0.29%, S&P +0.39%

-

14:28

Before the bell: S&P futures +0.26%, NASDAQ futures +0.02%

U.S. stock-index futures gained, supported by higher oil prices and the lingering effects of the post-election rally.

Global Stocks:

Nikkei 18,106.02 +138.61 +0.77%

Hang Seng 22,357.78 +13.57 +0.06%

Shanghai 3,218.21 +25.35 +0.79%

FTSE 6,782.70 +6.93 +0.10%

CAC 4,527.42 +23.07 +0.51%

DAX 10,703.59 +39.03 +0.37%

Crude $46.92 (+2.69%)

Gold $1,213.60 (+0.41%)

-

13:57

Important bids on GBP/USD as the pair recovers friday’s losses. Clear accumulation on H4

-

13:53

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

3M Co

MMM

170.9

-2.06(-1.191%)

4156

ALCOA INC.

AA

30.85

-1.00(-3.1397%)

8351

Amazon.com Inc., NASDAQ

AMZN

768

7.84(1.0314%)

25849

Apple Inc.

AAPL

110.5

0.44(0.3998%)

75154

AT&T Inc

T

37.66

0.25(0.6683%)

4546

Caterpillar Inc

CAT

92.7

0.36(0.3899%)

531

Chevron Corp

CVX

110.2

1.00(0.9157%)

7082

Cisco Systems Inc

CSCO

30.15

-0.03(-0.0994%)

7079

Citigroup Inc., NYSE

C

55.88

0.42(0.7573%)

48525

E. I. du Pont de Nemours and Co

DD

69

-0.17(-0.2458%)

1402

Exxon Mobil Corp

XOM

86.22

0.94(1.1023%)

12897

Facebook, Inc.

FB

118.39

1.37(1.1707%)

147893

Ford Motor Co.

F

11.81

0.05(0.4252%)

13145

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

14.22

0.49(3.5688%)

222797

General Electric Co

GE

30.72

0.05(0.163%)

2458

General Motors Company, NYSE

GM

33.05

0.05(0.1515%)

1047

Goldman Sachs

GS

210.9

0.55(0.2615%)

2167

Google Inc.

GOOG

763.7

3.16(0.4155%)

4673

Home Depot Inc

HD

128.88

0.55(0.4286%)

112

Intel Corp

INTC

35.1

0.15(0.4292%)

2863

International Business Machines Co...

IBM

160.3

-0.09(-0.0561%)

322

International Paper Company

IP

47.7

-0.75(-1.548%)

2910

Johnson & Johnson

JNJ

115.82

0.46(0.3988%)

1408

JPMorgan Chase and Co

JPM

78.08

0.37(0.4761%)

5690

McDonald's Corp

MCD

119.7

0.25(0.2093%)

1692

Microsoft Corp

MSFT

60.52

0.17(0.2817%)

4833

Pfizer Inc

PFE

31.6

0.12(0.3812%)

1235

Tesla Motors, Inc., NASDAQ

TSLA

186

0.98(0.5297%)

7695

The Coca-Cola Co

KO

41

-0.12(-0.2918%)

9585

Twitter, Inc., NYSE

TWTR

18.75

0.02(0.1068%)

21317

Verizon Communications Inc

VZ

48.01

-0.06(-0.1248%)

1565

Wal-Mart Stores Inc

WMT

68.7

0.16(0.2334%)

4133

Walt Disney Co

DIS

98.4

0.16(0.1629%)

4643

Yandex N.V., NASDAQ

YNDX

18.72

0.25(1.3535%)

1055

-

13:52

Option expiries for today's 10:00 ET NY cut

EUR/USD 1.0625-30 (EUR 426m) 1.0675 (388m) 1.0700 (1.08bln) 1.0775 (201m)

USD/JPY 109.00 (USD 1.0bln) 109.10 (550m) 110.00 (795m)

GBP/USD 1.2500 (286m)

EUR/GBP 0.8800 (EUR 200m)

USD/CAD 1.3500 (USD 277m) 1.3580 (200m)

NZD/USD 0.6900 (301m) 0.7120 (202m)

EUR/SEK 9.8500 (EUR 469m)

-

13:49

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

3M (MMM) downgraded to Sell from Neutral at Goldman

Other:

Starbucks (SBUX) initiated with a Neutral at Buckingham Research

McDonald's (MCD) removed from Analyst Focus List at JP Morgan

Freeport-McMoRan (FCX) target raised to $20 from $15 at Cowen

-

13:47

Fischer: FOMC Will Stay Focused on Inflation Issue

-

Will Take Expected Inflation Into Account Partly Because It Has Impact on Actual Inflation

-

No Central Banker Would Ever Say They Don't Worry About Risks Like Inflation

-

Haven't Heard Anything That Suggests We Ought to Change Fed's Balance Sheet

-

Fed Has Well-Defined Task, Continues to Operate Independent of Political Cycle

-

Fed's Independence Extremely Important When Politics Is Disturbed

-

If We Don't Fix Wall Street, Unclear if We Will Have Solved 'Too Big to Fail' Problem

-

Crisis Caused by 'Bad Behavior, Bad Strategy' in Financial Sector

-

Without Fed, 2008 Crisis 'Could Have Been Very Much Worse'

-

-

13:45

Canadian Wholesale Sales decreased in September

Wholesale sales decreased 1.2% to $56.0 billion in September, following increases in four of the previous five months. Declines were recorded in five subsectors, led by lower sales in the machinery, equipment and supplies and the miscellaneous subsectors.

In volume terms, wholesale sales decreased 1.5% in September.

Sales decreased in five of seven subsectors in September, accounting for 65% of total wholesale sales.

The machinery, equipment and supplies subsector recorded the largest decline in dollar terms in September, down 4.0% to $10.9 billion, its lowest level since April 2016. In September, three out of four industries posted declines, led by the other machinery, equipment and supplies (-7.8%) and the computer and communications equipment and supplies (-4.6%) industries.

Sales in the miscellaneous subsector declined 3.1% to $7.0 billion, following a 4.6% increase in August. While four of five industries reported declines, a 8.0% decrease in the agricultural supplies industry contributed the most to the downturn in September.

-

13:30

Canada: Wholesale Sales, m/m, September -1.2% (forecast 0.4%)

-

12:49

Orders

EUR/USD

Offers : 1.0645-50 1.0665 1.0685 1.0700 1.0730 1.0750-60 1.0780 1.0800 1.0825-30 1.0850

Bids : 1.0620 1.0600 1.0575-80 1.0550 1.0535 1.0520 1.0500 1.0480 1.0450

GBP/USD

Offers : 1.2365 1.2385 1.2400 1.2425-30 1.2445-50 1.2485 1.2500-05

Bids : 1.2315-20 1.2300 1.2285 1.2270 1.2250-55 1.2220 1.2200

EUR/GBP

Offers : 0.8625-30 0.8660 0.8680-85 0.8700

Bids : 0.8575-80 0.8550 0.8525-30 0.8500 0.8480 0.8455-60

EUR/JPY

Offers : 118.00 118.45-50 119.00 119.50 120.00

Bids : 117.60 117.30 117.00 116.80 116.50 116.25-30 116.00

USD/JPY

Offers : 111.20 111.35 111.50 111.85 112.00 112.20 112.50

Bids : 110.80-85 110.60 110.50 110.20 110.00 109.80 109.50 109.30 109.00

AUD/USD

Offers : 0.7350 0.7380 0.7400 0.7420 0.7445-50 0.7480 0.7500-05

Bids : 0.7300 0.7285 0.7250 0.7220 0.7200

-

12:47

Putin believes that OPEC will agree on a production cut

Russian President Vladimir Putin believes that OPEC may agree to freeze the oil output.

"I can not say 100% if there will be an agreement, but it is a strong likelihood that it will be achieved", - the Russian leader said at a press conference after the APEC summit.

-

12:05

WSE: Mid session comment

The first half of today's trading brought significantly higher level of turnover as at the beginning of the week. Positively stand out today shares of KGHM and PZU. Generally, the Warsaw Stock Exchange presents a better attitude than the surroundings. In Western European markets declines from the second hour of trading have made up and the indices returned to light increases.

A big help for our market is some warming around emerging markets, a weaker dollar and stronger commodity prices. The WIG20 index has reached the new session highs and defeats peaks from Friday.

At the halfway point of today's trading, the WIG20 index was at the level of 1,746 points (+ 1.21%), the turnover in the segment of the largest companies was amounted to PLN 293 million.

-

11:38

Major stock indices in Europe trading in the green zone

Stock indices in Europe have showed gains on the background of mixed financial statements of some companies, and fears that the expectations after the US elections have been overly optimistic. At the same time the shares of mining companies continue to rise due to higher prices for oil and metals.

Today, investors expect comments from European Central Bank President Mario Draghi, after he confirmed last week that the bank is ready to implement new stimulus measures if necessary.

European stocks strengthened after ECB President Mario Draghi said on Friday that the central bank will continue to use all available tools.

Speaking at the 26th European Banking Congress in Frankfurt, Draghi added that the recovery of the eurozone economy is still largely based on the accommodative monetary policy.

The composite index of the largest companies in the region Stoxx Europe 600 rose 0.03% to 339.49 points.

Essentra shares tumbled 19% after the deterioration of the annual profit and revenue.

The market value of Mitie Group Plc, providing cleaning services for offices, decreased by 14%, as the company forecast earnings below previous estimates and market expectations.

Meanwhile, the stock prices of mining corporations BHP Billiton, Rio Tinto and Glencore rose at least 1%. Randgold added 2.1%, Fresnillo +1,9%.

BP shares increased by 1%, Royal Dutch Shell 1,5%. Brent crude oil increased by 1.3%, to $ 45.91 per barrel.

At the moment:

FTSE 6802.06 26.29 0.39%

DAX 10689.52 24.96 0.23%

CAC 4523.99 19.64 0.44%

-

10:21

UK PM, May determined to deliver change demanded in EU referendum

-

EU negotiations cannot be done quickly

-

Business must commit to investing in Britain for the long term

-

Autumn statement will be ambitious for business and ambitious for Britain

-

Chancellor will commit to providing a strong and stable foundation for our economy

-

Brexit offers an opportunity to get dynamic trading agreements

-

Needs to take the time to get our Brexit negotiating position clear

*forexlive

-

-

10:21

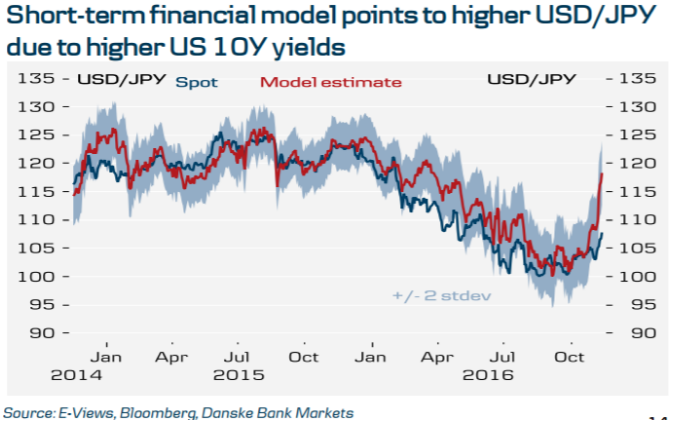

USD/JPY fair value at 115.50 due to US 10’s - Danske

"The election of Donald Trump as the next US President has prompted a significant increase in US inflation expectations and base metal prices driven by expectations of a significant boost to public spending, including a large infrastructure spending programme.

The US yield curve has steepened significantly as higher inflation expectations have driven an increase in yields on longer dated US government bonds. USD/JPY has historically been highly correlated with yields on 10Y US Treasuries as a widening of the rate spread tends to support portfolio investments flows out of Japan and into the US.

Our short-term financial model currently implies a fair value estimate of USD/JPY at 115.50 based primarily on the recent increase in the 10Y US interest rate.

Moreover, USD/JPY carry has become increasingly negative with 3M FX forwards trading at the lowest level since 2008. This has made it more expensive for Japanese investors to hedge USD assets, which might eventually start to weigh on the JPY if Japanese investors lower USD hedge ratios as long USD/JPY becomes more attractive from a carry perspective.

Hence, if the US reflation theme continues to build a case for higher US interest rates, we see a case for further portfolio investment outflows out of Japan, which in a combination with higher FX hedging costs on USD assets is likely to weigh on JPY over the medium term.

Finally, we note that higher commodity prices, in particular higher oil prices, will be a negative for the Japanese current account, which has improved substantially over the past couple of years due to the combination of previous weakening of the JPY and the oil price decline. A weakening of Japan's external balances implies less JPY appreciation pressure in the medium to long term".

Copyright © 2016 Danske, eFXnews™

-

10:09

Goldman Sachs increases 2017 forecast for WTI to $ 55

Goldman Sachs analysts have revised the forecast for oil prices in 2017. The bank's experts have raised expectations for WTI to $ 55. Goldman Sachs simulate the situation of a production cut from OPEC and the partial freeze of production in Russia.

-

10:04

The number of Eurozone banks directly supervised by ECB falls to 127

-

09:24

Oil is trading higher

This morning, the New York futures for Brent increased by 1.56% to $ 47.59 and WTI rose by + 1.57% to $ 47.09 per barrel. OPEC slightly worsened the outlook for global oil demand next year by -0.01 million barrels per day, compared with the October forecast, to 95.55 million barrels. The forecast worsened as a result of a decrease in supply from the United States, Mexico, Norway, the UK, Malaysia, Kazakhstan and China.

-

08:49

EUR/USD off Lows, Fed Speaker Comments Eyed

-

08:35

Major stock exchanges trading in the green zone: FTSE 100 6,798.56 22.79 0.34%, DAX 10,695.73 31.17 0.29%, CAC 40 4,524.04 19.69 0.44%

-

08:35

Option expiries for today's 10:00 ET NY cut

EUR/USD 1.0625-30 (EUR 426m) 1.0675 (388m) 1.0700 (1.08bln) 1.0775 (201m)

USD/JPY 109.00 (USD 1.0bln) 109.10 (550m) 110.00 (795m)

GBP/USD 1.2500 (286m)

EUR/GBP 0.8800 (EUR 200m)

USD/CAD 1.3500 (USD 277m) 1.3580 (200m)

NZD/USD 0.6900 (301m) 0.7120 (202m)

EUR/SEK 9.8500 (EUR 469m)

-

08:19

WSE: After opening

WIG20 index opened at 1731.39 points (+0.33%)*

WIG 47147.41 0.50%

WIG30 2019.12 0.60%

mWIG40 3955.02 0.43%

*/ - change to previous close

The futures market started the new week from increase of 0.7% (1,738 points). It's better preservation than in the environment, where the contract for the DAX grew by 0.3% at the opening.

In the cash market gain in the main part the shares of commodity companies or companies relying on rising prices of raw materials such as KGHM (which the rate increases by 3.5%, focusing on a main activity), JSW and Lotos. This good opening of today's trading moved away the vision of breaking the support, however does not mean a return to growth.

After fifteen minutes of trading the WIG20 index was at the level of 1,733 points (+0,44%).

-

08:06

Today’s events

-

At 13:00 GMT the Federal Reserve Vice Chairman Stanley Fischer will deliver a speech

-

At 16:00 GMT the ECB board member Benoit Coeure will deliver a speech

-

At 16:30 GMT the ECB president Mario Draghi will deliver a speech

-

At 19:25 GMT Andy Haldane of the Bank of England will make a speech

-

-

07:32

Deutsche Bank says that everything align perfectly for EUR/USD short

"In the short-term there are some factors that should at least contain the rise in Treasury yields, including: i) limits to how steep the US yield curve will get before carry constrains the long-end backup in yields. Example: US T.Note 10s minus 2s rarely trade above 250bps for any length of time.

ii) care of a global negative output gap, the world likely still has a disinflationary bias, although protectionism is bound to challenge this; and, here is the big wildcard,

iii) Trump's election and Brexit have underscored the rise in global political risk. Most immediately pressing is the French Presidential election that has enormous ramifications for the EUR's future, and global risk. Ironically, this could still lead to a desperate flight to US (and Japan) quality.

One broad point about Trump's election, is there is scope for an over-reaction, but there is even more potential for a failure of the collective imagination to understand the forces unleashed.

In some markets the impact of a probable change in fiscal policy (bond bearish, risk appetite positive) and a shift in political risk (T.bond bullish, but risk negative) will be in conflict. One trade where the economic and political risks align perfectly, in our view, is the short EUR/USD currency trade.

Deutsche Bank maintains a short EUR/USD position from 1.0750".

Copyright © 2016 DB, eFXnews™

-

07:28

Positive start of trading expected on the major stock exchanges in Europe: DAX + 0.1%, CAC 40 + 0.3%, FTSE + 0.1%

-

07:25

Broadbent Says BoE Can Tolerate High Inflation Than Larger Rise In Unemployment - rttnews

-

07:24

Japan’s Business activity index rose in September by 0.2%

According to data released today by the Ministry of Economy, Trade and Industry of Japan, the index of business activity in all sectors of the economy rose in September by 0.2% vs +0.1% expected. This is the fourth month in a row as the figure increases. Private industry index rose by 0.2% on a monthly basis, while economists had expected the index to remain unchanged in September.

The index which measures the volume of construction activity showed an increase of 2.0%. At the same time, sub-activity index fell by 0.1% in the services sector. On an annual basis, the index of business activity in the industry has grown at a slower pace, only 1.3% after rising 1.7% in the previous month.

-

07:21

WSE: Before opening

We begin a new week, which in the case of the US market will be shortened due to Thursday's Thanksgiving Day. The mood in the morning rather not indicate any significant changes. Contracts in the US gain slightly after a slight decline in the S&P 500 on Friday. Quotations in Asia are mixed, but in China and Japan increases are observed. The dollar remains relatively strong, although we may see another attempt to its slight weakening. It is worth to pay attention to the row material market, where rising prices of copper and oil. Generally, from above mentioned factors comes out a pretty good situation for the Warsaw market.

During today's session we will be announced of important for the local market readings. These will be the data on industrial production and retail sales for October. The market expects a slowdown readings to 0.8% y/y (production) and 4.0% y/y (retail sales). However this will mainly be an impact of seasonal effects (a smaller number of working days). In the case of construction output is expected to remain negative trend (-16.3% y/y). These data will be very important, because the market can see the uncertainty as to the condition of the national economy.

The beginning of the new week in the currency market brings a little stronger PLN, but still on most lists Polish currency is the weakest for several months (except for the USD/PLN pair, where the zloty is the weakest since 2002). PLN is valued by the market as follows: PLN 4.1850 to the US dollar, PLN 4.4324 against the euro. Yields on Polish debt amounts to 3.66% for 10-year securities.

-

07:21

Japan's trade surplus below forecast

The positive balance of Japan's foreign trade in October totaled Y496,2 billion, lower than the forecast of Y610 billion. The total trade balance, published by Japan's Ministry of Finance estimates the balance between imports and exports. A positive value represents a trade surplus while a negative - a trade deficit. Due to the high dependence on exports the Japanese economy is highly dependent on the trade surplus.

Also, Japan's Ministry of Finance reported that exports from Japan to Europe in October fell by -9.5% y / y and to US -11.2% y / y, while to China -9.2% y / y.

-

07:16

Trump to be held to his word on Fed independence: Bullard

-

06:06

Options levels on monday, November 21, 2016:

EUR/USD

Resistance levels (open interest**, contracts)

$1.0851 (2933)

$1.0784 (910)

$1.0731 (522)

Price at time of writing this review: $1.0599

Support levels (open interest**, contracts):

$1.0480 (4182)

$1.0420 (6042)

$1.0386 (1847)

Comments:

- Overall open interest on the CALL options with the expiration date December, 9 is 73608 contracts, with the maximum number of contracts with strike price $1,1200 (6182);

- Overall open interest on the PUT options with the expiration date December, 9 is 66024 contracts, with the maximum number of contracts with strike price $1,0500 (6042);

- The ratio of PUT/CALL was 0.90 versus 0.87 from the previous trading day according to data from November, 18

GBP/USD

Resistance levels (open interest**, contracts)

$1.2604 (1572)

$1.2506 (1732)

$1.2410 (782)

Price at time of writing this review: $1.2337

Support levels (open interest**, contracts):

$1.2291 (3934)

$1.2194 (1277)

$1.2097 (1089)

Comments:

- Overall open interest on the CALL options with the expiration date December, 9 is 34924 contracts, with the maximum number of contracts with strike price $1,3400 (2612);

- Overall open interest on the PUT options with the expiration date December, 9 is 36654 contracts, with the maximum number of contracts with strike price $1,2300 (3934);

- The ratio of PUT/CALL was 1.05 versus 1.06 from the previous trading day according to data from November, 18

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

04:46

Japan: All Industry Activity Index, m/m, September 0.2% (forecast 0.1%)

-