Market news

-

23:29

Stocks. Daily history for Jan 03’2017:

(index / closing price / change items /% change)

Hang Seng +149.84 22150.40 +0.68%

CSI 300 +32.15 3342.23 +0.97%

Euro Stoxx 50 +6.35 3315.02 +0.19%

FTSE 100 +35.06 7177.89 +0.49%

DAX -14.09 11584.24 -0.12%

CAC 40 +16.95 4899.33 +0.35%

DJIA +119.16 19881.76 +0.60%

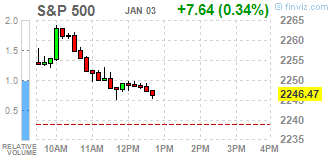

S&P 500 +19.00 2257.83 +0.85%

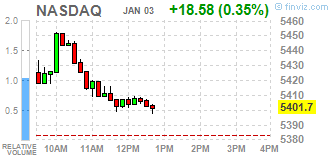

NASDAQ +45.97 5429.09 +0.85%

S&P/TSX +115.44 15403.03 +0.76%

-

21:05

Major US stock indexes finished trading in the "green zone"

Major US stock indexes Wall Street closed with moderate plus, down from the morning marks on the background of falling oil prices.

Data for December signaled the strong end of the year for the US manufacturing sector, and the overall business environment improved at the fastest pace since March 2015. Strong rise in new orders and production volume led to the fastest pace of job creation and a half years. At the same time, the increased costs of customers and optimistic business confidence have led to the largest accumulation of inventories in August, 2014. Seasonally adjusted, the US manufacturing purchasing managers index (PMI) released by the Markit slightly rose to 54.3 in December from 54.1 in November, and signaled a strong improvement in the business environment a little less than two years. Last index growth was largely driven by stronger employment growth and stocks in December, which more than offset slightly weaker increase in output and new orders.

Furthermore, a report published by the Institute for Supply Management (ISM), showed that in December, activity in the US manufacturing sector grew moderately, while exceeding the average forecast. The PMI for the manufacturing was 54.7 points versus 53.2 points in November. Analysts had expected that this figure will rise to only 53.5 points.

At the same time, construction spending in the US rose more than expected in November, reaching its highest level of 10.5 years, which may provide a revision of the economic growth for the fourth quarter estimates. The Commerce Department reported that construction spending increased by 0.9%, to $ 1.18 trillion. This is the highest level since April 2006. The main reason for this change was to increase the expenditure in the private and public sectors.

Oil prices reached 18-month highs, lost all earned position. The increase contributed to hopes that a deal between OPEC and other major oil exporters to cut production reduce the global surplus of supply. Meanwhile, the pressure on the quotation provided the growth of the US dollar and partial profit-taking.

DOW index components closed mostly in positive territory (23 of 30). Most remaining shares rose NIKE, Inc. (NKE, + 2.29%). Outsider were shares of McDonald's Corporation (MCD, -1.75%).

Almost all sectors of the S & P ended the session in positive territory. The leader turned conglomerates sector (+ 1.8%). Reducing only showed utilities sector (-0.3%).

At the close:

Dow + 0.60% 19,880.77 +118.17

Nasdaq + 0.85% 5,429.08 +45.96

S & P + 0.84% 2,257.70 +18.87

-

20:00

DJIA +0.24% 19,809.05 +46.45 Nasdaq +0.41% 5,405.07 +21.95 S&P +0.48% 2,249.56 +10.73

-

17:51

Wall Street. Major U.S. stock-indexes slightly rose

Major U.S. stock-indexes slightly higher on Tuesday as a post-election rally extended into the new year, but stocks pared some of their early gains after oil prices eased from an 18-month high. Oil prices fell 2,44% after touching a high levels as investors keep a close watch on whether major producers keep their promise of limiting output.

Most of Dow stocks in positive area (21 of 30). Top gainer - Verizon Communications Inc. (VZ, +2.20%). Top loser - McDonald's Corporation (MCD, -2.04%).

Most of S&P sectors also in positive area. Top gainer - Conglomerates (+1.2%). Top loser - Utilities (-0.2%).

At the moment:

Dow 19727.00 +7.00 +0.04%

S&P 500 2243.00 +6.75 +0.30%

Nasdaq 100 4889.50 +25.50 +0.52%

Oil 52.41 -1.31 -2.44%

Gold 1162.00 +10.30 +0.89%

U.S. 10yr 2.46 +0.02

-

17:41

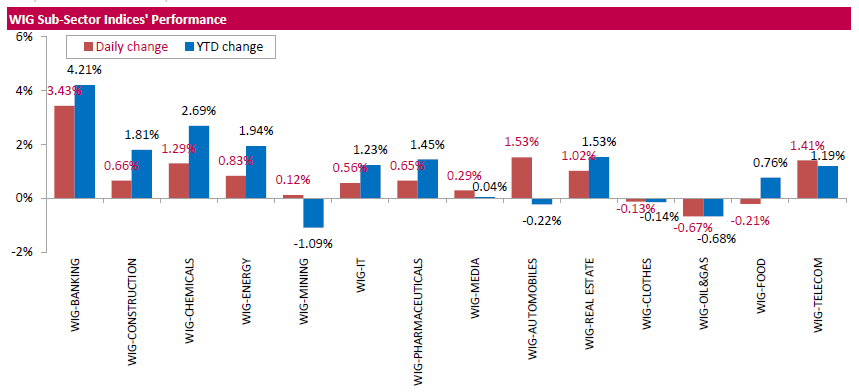

WSE: Session Results

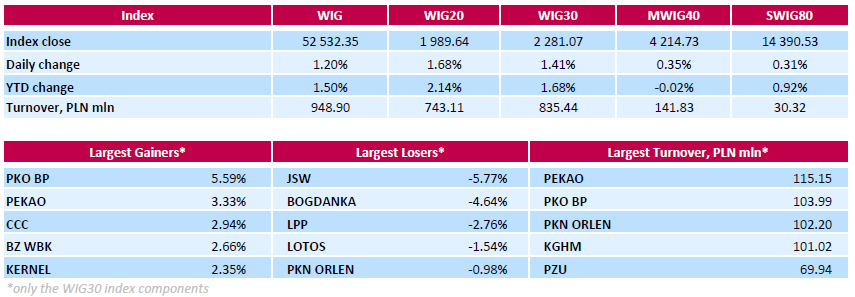

Polish equity market closed higher on Tuesday. The broad market measure, the WIG Index, rose by 1.2%. The WIG sub-sector indices were mainly higher with banking stocks (+3.43%) outperforming.

The large-cap stocks' measure, the WIG30 Index, surged by 1.41%. A majority of the index components returned gains, with the way up led by banking sector names BKO BP (WSE: PKO) and PEKAO (WSE: PEO), which soared by 5.59% and 3.33% respectively. Other major advancers were footwear retailer CCC (WSE: CCC), agricultural producer KERNEL (WSE: KER) and chemical producer SYNTHOS (WSE: SNS), which added between 2.35% and 2.94%. Among few decliners, coal miners JSW (WSE: JSW) and BOGDANKA (WSE: LWB) were the weakest performers, tumbling by 5.77% and 4.64% respectively. They were followed by clothing retailer LPP (WSE: LPP), dropping by 2.76%. The company reported yesterday its consolidated revenues totaled about PLN 737 mln in December 216, up 13% y/y. At the same time, the company announced that the results for December 2016 were influenced by a one-off operation involving the wholesale of old collections on stock both in Poland and at twelve foreign units. The value of these inventories was PLN 120 mln. As a result, its gross margin on the December sales decreased to approx. 36% from 51% before that operation.

-

17:00

European stocks closed: FTSE 100 +35.06 7177.89 +0.49% DAX -14.09 11584.24 -0.12% CAC 40 +16.95 4899.33 +0.35%

-

14:52

WSE: After start on Wall Street

The Americans started the new year with considerable optimism and their yesterday's absence means that Wall Street has to work off arrears to the markets in Europe. In Warsaw Stock Exchange consistently grow large companies, indicating the influx of foreign purchase orders. The leader of growth is PKO BP (WSE: PKO), stands out also Tauron (WSE: TPE), Orange (WSE: OPL) and Pekao (WSE: PEO).

An hour before the close of trading the WIG20 index was at the level of 1,978 points (+1.07%) and turnover in the segment of the largest companies was amounted to PLN 535 million.

-

14:35

U.S. Stocks open: Dow +0.83%, Nasdaq +0.80%, S&P +0.79%

-

14:25

Before the bell: S&P futures +0.83%, NASDAQ futures +0.83%

U.S. stock-index futures rose amid strength in major foreign equity bourses and in commodities markets, supported by upbeat Chinese economic data. The Caixin Purchasing Managers' Index (PMI), which tracks manufacturing activity in China, recorded the fastest rate of improvement since January, 2013.

Global Stocks:

Nikkei Closed

Hang Seng 22,150.40 +149.84 +0.68%

Shanghai 3,136.28 +32.65 +1.05%

FTSE 7,180.16 +37.33 +0.52%

CAC 4,903.51 +21.13 +0.43%

DAX 11,594.13 -4.20 -0.04%

Crude $54.89 (+1.86%)

Gold $1,151.10 (-0.08%)

-

13:54

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

Amazon.com Inc., NASDAQ

AMZN

757.2

7.33(0.9775%)

50760

AMERICAN INTERNATIONAL GROUP

AIG

65.7

0.39(0.5971%)

1358

Apple Inc.

AAPL

116.1

0.28(0.2418%)

114981

Barrick Gold Corporation, NYSE

ABX

16.15

0.17(1.0638%)

72563

Chevron Corp

CVX

118.69

0.99(0.8411%)

7390

Citigroup Inc., NYSE

C

60.25

0.82(1.3798%)

32308

E. I. du Pont de Nemours and Co

DD

73.5

0.10(0.1362%)

680

Exxon Mobil Corp

XOM

91.18

0.92(1.0193%)

5671

Facebook, Inc.

FB

116.01

0.96(0.8344%)

107183

FedEx Corporation, NYSE

FDX

187.17

0.97(0.5209%)

861

Ford Motor Co.

F

12.18

0.05(0.4122%)

87443

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

13.44

0.25(1.8954%)

81026

General Electric Co

GE

31.69

0.09(0.2848%)

21594

General Motors Company, NYSE

GM

34.71

-0.13(-0.3731%)

110979

Goldman Sachs

GS

242.11

2.66(1.1109%)

12095

Hewlett-Packard Co.

HPQ

15.1

0.26(1.752%)

107258

Home Depot Inc

HD

134.91

0.83(0.619%)

8261

Intel Corp

INTC

36.48

0.21(0.579%)

633351

International Business Machines Co...

IBM

166.8

0.81(0.488%)

5155

Johnson & Johnson

JNJ

115.65

0.44(0.3819%)

5714

JPMorgan Chase and Co

JPM

87.22

0.93(1.0778%)

17985

Microsoft Corp

MSFT

62.52

0.38(0.6115%)

37222

Nike

NKE

51.65

0.82(1.6132%)

51850

Pfizer Inc

PFE

32.69

0.21(0.6465%)

20570

Procter & Gamble Co

PG

84.48

0.40(0.4757%)

7221

Starbucks Corporation, NASDAQ

SBUX

55.98

0.46(0.8285%)

6583

Tesla Motors, Inc., NASDAQ

TSLA

216.3

2.61(1.2214%)

34397

The Coca-Cola Co

KO

41.65

0.19(0.4583%)

6006

Twitter, Inc., NYSE

TWTR

16.28

-0.02(-0.1227%)

118616

UnitedHealth Group Inc

UNH

161.06

1.02(0.6373%)

852

Verizon Communications Inc

VZ

53.81

0.43(0.8055%)

19933

Wal-Mart Stores Inc

WMT

69.3

0.18(0.2604%)

2629

Walt Disney Co

DIS

105.5

1.28(1.2282%)

22462

Yahoo! Inc., NASDAQ

YHOO

39.06

0.39(1.0085%)

3288

Yandex N.V., NASDAQ

YNDX

20.77

0.64(3.1793%)

13784

-

13:47

Upgrades and downgrades before the market open

Upgrades:

Walt Disney (DIS) upgraded to Buy at Evercore ISI

Verizon (VZ) upgraded to Buy from Neutral at Citigroup

Downgrades:

Other:

Facebook (FB) initiated with a Buy at Aegis

Twitter (TWTR) initiated with a Sell at Aegis; target $14

Amazon (AMZN) resumed with a Overweight at Piper Jaffray; target $900

-

12:01

WSE: Mid session comment

The first half of today's trading was under the sign of robust growth of the Warsaw WIG20 index. Thus, the return of foreign investors nothing broke but actually helps, because yesterday's positive trend was captured, even with a slightly disappointing attitude of the environment, especially at the level of the DAX. However, Europe's mood is positive and the Warsaw market entered into this trend.

At the halfway point of quotations the WIG20 index was at the level of 1,978 points (+ 1.13%); the turnover in the segment of the largest companies was amounted to PLN 285 million.

-

11:55

Major stock indices in Europe trading in the green zone

European stocks rose for a third day continuing the bull market, as data showed that the Purchasing Managers' Index in the manufacturing sector and services in China were relatively strong in 2016.

The activity index of the manufacturing sector of China's economy by Caixin, also published by Markit Economics, in December was 51.9, higher than the previous value of 50.9 and economists' forecast of 50.7. As can be seen from the data, the index increased by 0.1 points and reached the highest level since January 2013. Chief Economist at Caixin Shenchzhun Zheng said that in December there was the development of positive trends in the Chinese economy, the majority of sub-indices show positive trends. However, he noted that despite the improvement of the situation, the Government of China need to remain vigilant to ensure the stability of the economy.

UK manufacturing sector expanded at the fastest pace in 30 months in December, showed on Tuesday the results of the survey by IHS Markit. PMI rose to 56.1 in December from 53.6 in November. The score was significantly higher than its long-term average of 51.5 and the expected level of 53.3.

PMI indicates expansion in each of the past five months. The study showed that in December, growth in production and new orders were among the best that have seen over the past two and a half years. Manufacturers benefited from a strong influx of new orders from domestic and overseas customers. Employment increased for the fifth consecutive month in December, while the job creation has accelerated the most in 14 months. On the price front, selling prices remained among the fastest throughout the survey history.

"Based on its historical connection with official data on industrial production, the survey indicates that the quarterly growth rate of close to 1.5 per cent, showing a surprisingly robust pace, given the weak start of the year and the uncertainty surrounding the referendum on EU membership," said Rob Dobson, senior economist at IHS Markit.

Banking stocks were the best performers, having jumped more than 1.3 percent. Shares of the new merged bank BPM in Italy have been at the top of the European index of the second day in a row, rising by more than 6 per cent in mid-morning trading. Italian banking index moves up, despite news that the sale of three small banks could be in jeopardy after the European Commission asked to postpone the process, at least for a week.

At the moment:

FTSE 7173.75 30.92 0.43%

DAX 11596.41 -1.92 -0.02%

CAC 4905.36 22.98 0.47%

-

08:44

Major European stock markets trading in the green zone: FTSE + 0.3%, DAX + 0.3%, CAC40 + 0.5%, FTMIB + 0.5%, IBEX + 0.3%

-

08:18

WSE: After opening

WIG20 index opened at 1961.73 points (+0.26%)*

WIG 52040.34 0.26%

WIG30 2256.64 0.32%

mWIG40 4197.83 -0.06%

*/ - change to previous close

The futures market (FW20H1720) began trading with an increase of eight points over yesterday's closing and subsequent transactions brought further upward movement.

The cash market just started in positive territory. After the message about the possible loss of a contract with Biedronka retail chain negatively stands out Wawel (WSE:WWL). After the first transactions the WIG20 index clearly went over the level of 1,950 points, what causes a slow directing of attention to the important psychological barrier of 2,000 points.

After fifteen minutes of trading the index of the largest companies was at 1,969 points (+ 0.63%)

-

07:21

WSE: Before opening

Today are back to the game the main financial markets. Not working yet Japan and New Zealand, but on other continents we will have already full set of investors. From the point of view of the Warsaw Stock Exchange the most important is that back comes London and New York, which means a return to normality and orders from abroad. Tested will also be yesterday's New Year optimism, which is sustained so far. In Asia dominate the rise, contracts in the US are also gaining in value, quite a lot, as 0.6%. Thus, the mood in the morning is good, what forecasts positive opening of European markets.

Today's macro calendar is marked by the publication of PMI's. Tonight we met this kind of publication from China, a score of 51.9 points vs. the forecast of 50.7 points. At 10:30 (Warsaw time) we will know the PMI for the UK industry, while in the US the rate will be released at 15:45 and it is assumed its delicate growth from 54.1 points to 54.2 points. At 16:00 we will know different, but similar reading, namely the ISM index for the industry sector.

-

07:03

Positive start of trading expected on the major stock exchanges in Europe: DAX + 0.2%, CAC40 + 0.1%, FTSE + 0.1%

-

00:00

Open of the Market

Positive start for European stocks. After the first exchanges on the Frankfurt Dax of 0.28% to 11,630 points, + 0.46% for the CAC 40 and + 0.38% for the Eurostoxx 50. Somewhat sparse European economic agenda with the data on the German employment market and the British manufacturing PMI.

Today, to be reported the re-opening of Wall Street after being closed for the New Year festivities. -