Market news

-

23:29

Stocks. Daily history for Dec 05’2016:

(index / closing price / change items /% change)

Nikkei 225 18,274.99 0.00 0.00%

Shanghai Composite 3,204.95 -38.90 -1.20%

S&P/ASX 200 5,400.44 0.00 0.00%

FTSE 100 6,746.83 +16.11 +0.24%

CAC 40 4,574.32 +45.50 +1.00%

Xetra DAX 10,684.83 +171.48 +1.63%

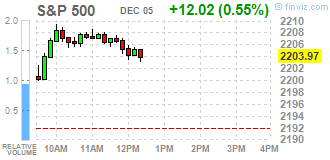

S&P 500 2,204.71 +12.76 +0.58%

Dow Jones Industrial Average 19,216.24 +45.82 +0.24%

S&P/TSX Composite 15,095.17 +42.65 +0.28%

-

21:07

Major US stock indices closed in the green zone

Major stock indexes in Wall Street rose on Monday amid a rise in price of shares of conglomerates sector and technology segment. Dow newly updated records, which was largely due to the growth of the banking and industrial sectors, which are expected to benefit from increased spending on infrastructure and simpler rules for the administration of Donald Trump.

As it became known today, suppliers of services in the US have experienced robust expansion of business activity in November, helped by the fastest growth of new orders in the period of one year. Large workloads and strong business confidence led to a further rise in the rate of job creation to three and a half year low, noted in September. At the same time, input price inflation fell slightly in November, which contributed to slow growth in average prices charged by the services sector, since April. The seasonally adjusted final index of business activity in the US services sector from Markit was 54.6 in November, and remained above the neutral 50.0 value of the ninth month in a row.

At the same time, the index of business activity in the US service sector, which is calculated by the Institute of Supply Management (ISM), improved significantly in November, reaching a level of 57.2 compared with 54.8 in the previous month. According to the forecast, the rate had to rise only to 55.4. Recall, the indicator is the result of a survey of about 400 companies from 60 sectors across the United States. ISM index value greater than 50 is usually considered as an indicator of the growth of industrial activity, but less than 50, respectively, falls.

DOW index closed mixed components (15 black, 15 red). Most remaining shares rose NIKE, Inc. (NKE, + 2.98%). Outsider were shares of UnitedHealth Group Incorporated (UNH, -2.13%).

All business sectors S & P index recorded an increase. The leader turned conglomerates sector (+ 1.3%).

At the close:

Dow + 0.24% 19,216.48 +46.06

Nasdaq + 1.01% 5,308.89 +53.24

S & P + 0.58% 2,204.70 +12.75

-

20:00

DJIA +0.18% 19,205.06 +34.64 Nasdaq +0.89% 5,302.65 +47.00 S&P +0.50% 2,202.85 +10.90

-

17:30

Wall Street. Major U.S. stock-indexes rose

Major U.S. stock-indexes rose on Monday, with financials and technology stocks powering Dow to a new intraday high and boosting the S&P and the Nasdaq. The Dow has been enjoying a record-setting rally, largely driven by bank and industrial stocks, which are expected to benefit the most from higher spending on infrastructure and simpler regulations under a Donald Trump administration.

Most of Dow stocks in positive area (18 of 30). Top gainer - NIKE, Inc. (NKE, +3.27%). Top loser - UnitedHealth Group Incorporated (UNH, -1.86%).

Most S&P sectors also in positive area. Top gainer - Basic Materials (+1.0%). Top loser - Utilities (-0.7%).

At the moment:

Dow 19230.00 +72.00 +0.38%

S&P 500 2203.75 +11.75 +0.54%

Nasdaq 100 4777.25 +38.75 +0.82%

Oil 51.95 +0.27 +0.52%

Gold 1168.40 -9.40 -0.80%

U.S. 10yr 2.40 +0.01

-

17:00

European stocks closed: FTSE 100 +16.11 6746.83 +0.24% DAX +171.48 10684.83 +1.63% CAC 40 +45.50 4574.32 +1.00%

-

16:50

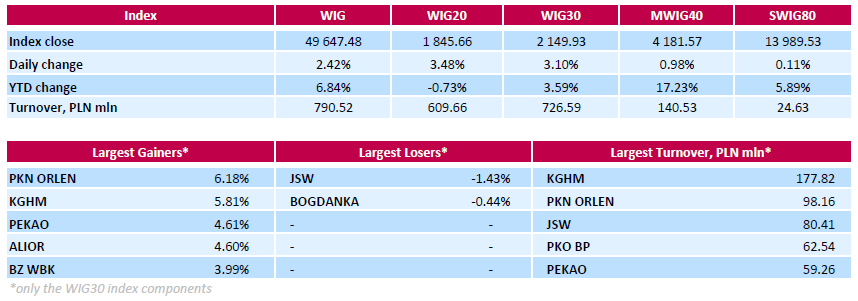

WSE: Session Results

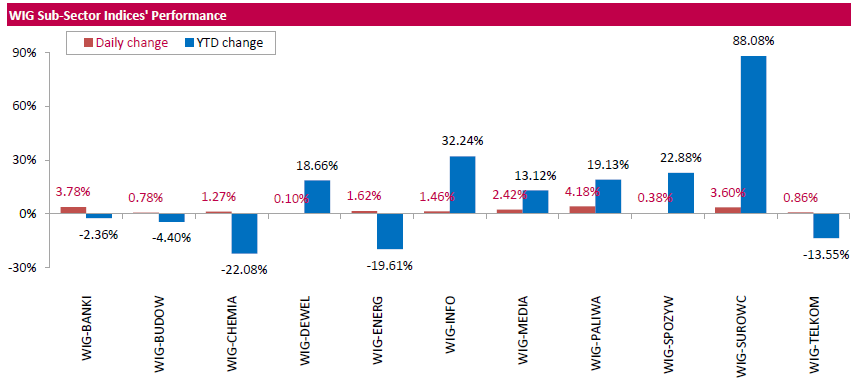

Polish equity closed higher on Monday. The broad market measure, the WIG Index, surged by 2.42%. All sectors in the WIG generated positive returns, with oil and gas (+4.18%), banking sector (+3.78%) and materials (+3.6%) outperforming.

The large-cap stocks' benchmark, the WIG30 Index, grew by 3.1%. There were only two decliners among the index components. Coking coal producer JSW (WSE: JSW) posted the sharpest decline, sliding down 1.43%. It was followed by thermal coal miner BOGDANKA (WSE: LWB), falling by 0.44%. On the plus side, oil refiner PKN ORLEN (WSE: PKN) and copper producer KGHM (WSE: KGH) topped the list of outperformers, climbing by 6.18% and 5.81% respectively, supported by growing prices for oil and copper. Among other major gainers were six constituents, belonging to the banking sector, namely PEKAO (WSE: PEO), ALIOR (WSE: ALR), BZ WBK (WSE: BZW), PKO BP (WSE: PKO), ING BSK (WSE: ING) and MBANK (WSE: MBK), which added between 3.22% and 4.61% percent.

-

14:51

WSE: After start on Wall Street

European markets almost did not notice an increase in uncertainty. Slightly cheaper are mainly Italian banks but other sectors are gaining in value and the best presents sector of the automotive companies. As a result, the German market today gained greater vigor, although in the southern phase of trade gains slightly less than it was before. Increases of 2% on the WSE put us in first place among the most important parquets. The common currency also made up for earlier losses. This is somewhat surprising change, because after today's events, the ECB may be less inclined to reduce their support.

Wall Street opens with an increase of 0.4%, which may not be a significant change, but ranks the index over the broken last week support. This situation indirectly led to another wave of optimism on the Warsaw Stock Exchange.

An hour before the close of trading the WIG20 index was at the level of 1,831 points (+2,67%).

-

14:31

U.S. Stocks open: Dow +0.44%, Nasdaq +0.52%, S&P +0.45%

-

14:17

Before the bell: S&P futures +0.30%, NASDAQ futures +0.37%

U.S. stock-index futures advanced amid rising oil prices and as investors shrug off the Italian referendum defeat and Italy's prime-minister Matteo Renzi's resignation.

Global Stocks:

Nikkei 18,274.99 -151.09 -0.82%

Hang Seng 22,505.55 -59.27 -0.26%

Shanghai 3,204.95 -38.90 -1.20%

FTSE 6,738.88 +8.16 +0.12%

CAC 4,559.10 +30.28 +0.67%

DAX 10,643.98 +130.63 +1.24%

Crude $52.16 (+0.93%)

Gold $1,169.90 (-0.67%)

-

13:46

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

28.86

-0.18(-0.6198%)

8375

Amazon.com Inc., NASDAQ

AMZN

745.25

4.91(0.6632%)

18941

Apple Inc.

AAPL

110.16

0.26(0.2366%)

44739

AT&T Inc

T

38.62

0.01(0.0259%)

3899

Barrick Gold Corporation, NYSE

ABX

15.32

-0.34(-2.1711%)

33450

Boeing Co

BA

152

-0.25(-0.1642%)

421

Caterpillar Inc

CAT

95.41

0.27(0.2838%)

2881

Chevron Corp

CVX

113.78

0.78(0.6903%)

391

Cisco Systems Inc

CSCO

29.36

0.11(0.3761%)

2672

Citigroup Inc., NYSE

C

56.35

0.33(0.5891%)

21494

Exxon Mobil Corp

XOM

87.58

0.54(0.6204%)

2471

Facebook, Inc.

FB

115.95

0.55(0.4766%)

53906

Ford Motor Co.

F

12.35

0.11(0.8987%)

25832

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

15.7

0.28(1.8158%)

195468

General Electric Co

GE

31.42

0.08(0.2553%)

7294

General Motors Company, NYSE

GM

35.21

0.18(0.5138%)

8560

Goldman Sachs

GS

225

1.64(0.7342%)

2640

Google Inc.

GOOG

754.06

3.56(0.4744%)

2436

Home Depot Inc

HD

130

0.13(0.1001%)

1189

Intel Corp

INTC

34.3

0.14(0.4098%)

2069

International Business Machines Co...

IBM

159.99

-0.03(-0.0187%)

500

International Paper Company

IP

50.5

0.04(0.0793%)

500

Johnson & Johnson

JNJ

112.5

0.54(0.4823%)

728

JPMorgan Chase and Co

JPM

81.91

0.31(0.3799%)

8926

McDonald's Corp

MCD

119.61

1.37(1.1587%)

3382

Merck & Co Inc

MRK

61.5

0.37(0.6053%)

350

Microsoft Corp

MSFT

59.36

0.11(0.1857%)

1934

Nike

NKE

51.01

0.55(1.09%)

7111

Pfizer Inc

PFE

31.7

0.07(0.2213%)

1951

Procter & Gamble Co

PG

82.47

0.07(0.085%)

2792

Starbucks Corporation, NASDAQ

SBUX

56.81

-0.40(-0.6992%)

10311

Tesla Motors, Inc., NASDAQ

TSLA

182.8

1.33(0.7329%)

6922

The Coca-Cola Co

KO

40.4

0.04(0.0991%)

3118

Twitter, Inc., NYSE

TWTR

18.02

0.09(0.502%)

23564

United Technologies Corp

UTX

108.68

0.46(0.4251%)

200

Verizon Communications Inc

VZ

49.85

0.04(0.0803%)

5622

Visa

V

76.53

0.81(1.0697%)

7435

Wal-Mart Stores Inc

WMT

70.98

0.10(0.1411%)

4365

Walt Disney Co

DIS

99.2

0.70(0.7107%)

401

Yahoo! Inc., NASDAQ

YHOO

40.28

0.21(0.5241%)

100

Yandex N.V., NASDAQ

YNDX

18.7

0.28(1.5201%)

8980

-

13:42

Upgrades and downgrades before the market open

Upgrades:

Visa (V) upgraded to Buy from Neutral at Guggenheim

McDonald's (MCD) upgraded to Buy from Neutral at Nomura

NIKE (NKE) upgraded to Buy from Hold at HSBC Securities

Downgrades:

Alcoa (AA) downgraded to Neutral from Buy at Citigroup

Other:

Caterpillar (CAT) target raised to $89 from $78 at JP Morgan; Neutral

Hewlett Packard Enterprise (HPE) target raised to $25 from $22 at Maxim Group

-

13:15

Apple (AAPL) have hinted about working on unmanned vehicles

According to WSJ, Apple actually admitted that is working on unmanned vehicles, writing a letter to the public transport US regulator, requesting comments and suggestions on the new technology.

In the letter to the National Highway Traffic Safety Administration, Director of Product Development Steve Kenner, said the company "will invest heavily in machine learning and automation, and full of enthusiasm for the automated systems capacities in many areas, including transport. " In this case, as the newspaper notes, the letter did not disclose any details about the project.

Recall, for several years now there are rumors that Apple is working on a project code-named Project Titan for electric vehicle production. However, the company never publicly acknowledged it.

Apple also encourages the regulator to quickly adopt new safety rules, which, however, need to be flexible. As noted by Mr. Kenner, "improving the regulatory flexibility", the controller will "contribute to the implementation of innovation and promote" the development of life-saving technologies. "

AAPL shares rose in premarket trading to $ 110.44 (+ 0.49%).

-

12:05

WSE: Mid session comment

The forenoon readings of PMIs from services sector in Europe proved to be very good. It did not cause a greater reaction in the market, as investors traditionally are more focused on reports from the industry.

Today's market behavior is another, surprising reaction to a political event which was the referendum in Italy last weekend. The German DAX rising 1.5%, while the French CAC40 booster exceeds 1.2%. Our market is further supported by the good behavior of raw materials, where drops of oil have been completed and WIG20 in the first hour of trading was elevated above the level of 1,800 points. In the middle of trading the turnover among the largest companies exceeded the level of PLN 250 million, which is not bad for a Monday, although one-third of it is KGHM.

At the halfway point of today's session the WIG20 index was at the level of 1,819 points (+ 2.01%).

-

08:45

Major stock markets trading in the red zone: FTSE -0.4%, DAX -0.1%, CAC40 -0.4%, FTMIB -1.7%, IBEX -0.9%

-

08:17

WSE: After opening

WIG20 index opened at 1788.93 points (+0.30%)*

WIG 48732.15 0.53%

WIG30 2098.93 0.65%

mWIG40 4159.57 0.45%

*/ - change to previous close

The futures market began the new week with a surprising and considerable increase of 0.73% to 1,795 points. In the surrounding derivative on DAX lost approx. 0.2%, and the difference in the behavior may result from a positive reception of Friday's S&P statement.

The cash market also began with modest increases with a modest turnover beyond excluding the traditional distinctive behavior of KGHM shares. The copper conglomerate stands out positively, and indeed highly opens. The German DAX also gained at the opening, the same market shows that the Italian referendum does not work unfavorably.

After fifteen minutes of trading in Warsaw, the WIG20 index was at 1,796 points (+ 0.73%)

-

07:28

WSE: Before opening

Over the weekend Italy held a constitutional referendum. According to preliminary data, the Italians are against changes in the constitution, which will probably lead to the resignation of the government.

Markets reacted negatively with the weakening of the euro and pressure on risky assets. This reaction, however, proved to be short-lived. The euro stabilizes after night considerable discounts. On the other hand contracts in the United States opened with the gap, but did not fall further. The Asian markets are dominated by the red color, but the price of copper is gaining in value.

On Friday, Standard & Poor's upgraded the rating outlook for Poland to "stable" from "negative", supporting the assessment of the country at "BBB plus". In explanation they said that concerns about the independence of the central bank were dropped. An overall statement of the S&P was a big surprise and it seems that domestic investors will not pay greater attention to the message considering it to be unreliable. On the other hand, from the point of view of foreign investors, it is a plus, but is offset by the unfavorable outcome of the referendum in Italy.

Hence morning mix of information for the Warsaw market is different. We have positive news, we also have negative ones, although based on the model of similar situation this year we should not expect any disaster. In theory, this should mean a negative initial impulse, which, however, does not necessarily continue until the end of the session. In the meantime, there will be PMI / ISM readings for services sector, where traditionally reports from the US will be the most important.

-

07:24

Negative start of trading expected on the major stock exchanges in Europe: DAX -0.8%, CAC40 -0.5%, FTSE -0.4%

-

06:14

Global Stocks

U.S. stocks struggled for direction Friday with the Dow industrials finishing lower and the S&P 500 and the Nasdaq closing slightly higher as investors digested a weaker-than-expected payroll report, favoring sectors viewed as safe in economically uncertain times.

Asian shares fell on Monday Italian Prime Minister Matteo Renzi after he suffered a humiliating defeat in a referendum over constitutional reforms and investors eyed a growing spat between the incoming U.S. administration China.

-