Market news

-

23:28

Stocks. Daily history for Jan 09’2017:

(index / closing price / change items /% change)

Hang Seng +55.68 22558.69 +0.25%

CSI 300 +16.23 3363.90 +0.48%

Euro Stoxx 50 -12.20 3308.97 -0.37%

FTSE 100 +27.72 7237.77 +0.38%

DAX -35.02 11563.99 -0.30%

CAC 40 -22.27 4887.57 -0.45%

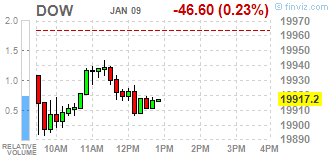

DJIA -76.42 19887.38 -0.38%

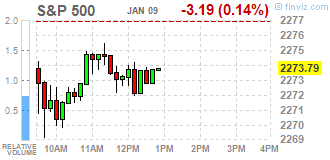

S&P 500 -8.08 2268.90 -0.35%

NASDAQ +10.76 5531.82 +0.19%

S&P/TSX -107.10 15388.95 -0.69%

-

20:00

DJIA 19903.43 -60.37 -0.30%, NASDAQ 5532.90 11.84 0.21%, S&P 500 2270.53 -6.45 -0.28%

-

17:52

Wall Street. Major U.S. stock-indexes mixed

Major U.S. stock-indexes mixed on Monday. Declines in bank and energy companies distancing the Dow from the 20,000 mark, while gains in technology stocks pushed the Nasdaq to a record intraday high.

Most of Dow stocks in negative area (20 of 30). Top gainer - E. I. du Pont de Nemours and Company (DD, +1.83%). Top loser - Exxon Mobil Corporation (XOM, -2.01%).

Most of S&P sectors also in negative area. Top gainer - Healthcare (+0.4%). Top loser - Conglomerates (-1.0%).

At the moment:

Dow 19836.00 -61.00 -0.31%

S&P 500 2267.50 -4.00 -0.18%

Nasdaq 100 5020.00 +16.00 +0.32%

Oil 52.40 -1.59 -2.94%

Gold 1183.00 +9.60 +0.82%

U.S. 10yr 2.32 -0.04

-

17:01

European stocks closed: FTSE 7237.77 27.72 0.38%, DAX 11563.99 -35.02 -0.30%, CAC 4887.57 -22.27 -0.45%

-

16:27

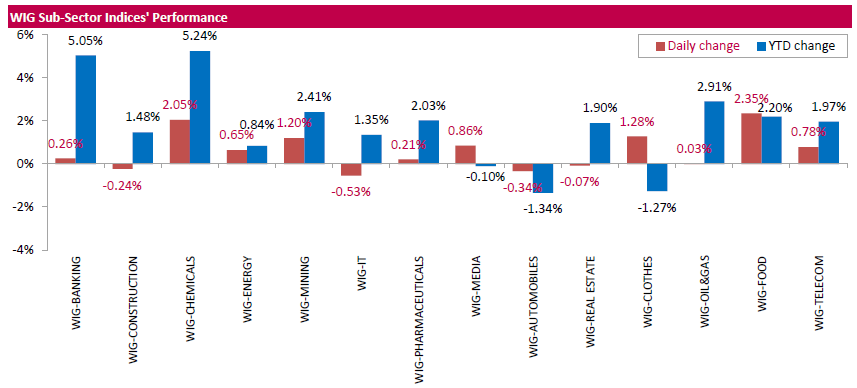

WSE: Session Results

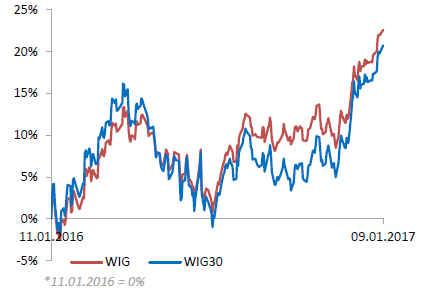

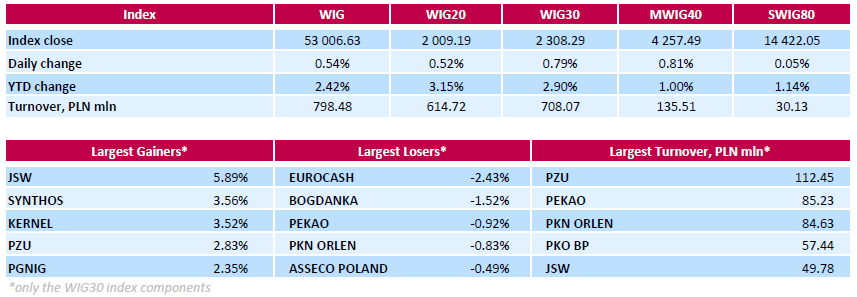

Polish equity market closed higher on Monday. The broad market measure, the WIG Index, rose by 0.54%. The WIG sub-sector indices were mainly higher with food stock gauge (+2.35%) outperforming.

The large-cap stocks' measure, the WIG30 Index, surged by 0.79%. A majority of the index components returned gains, with the way up led by coking coal miner JSW (WSE: JSW), which advanced 5.89% as the stock continued to recover after significant declines in late December through early January, which pushed its quotation down nearly 20%. Other major advancers were chemical producer SYNTHOS (WSE: SNS), agricultural producer KERNEL (WSE: KER) and insurer PZU (WSE: PZU), which soared 3.56%, 3.52% and 2.83% respectively. At the same time, FMCG-wholesaler EUROCASH (WSE: EUR) led a handful of decliners with a 2.43% drop, followed by thermal coal miner BOGDANKA (WSE: LWB), bank PEKAO (WSE: PEO), oil refiner PKN ORLEN (WSE: PKN) and IT-company ASSECO POLAND (WSE: ACP), tumbling between 0.49% and 1.52%.

-

14:53

WSE: After start on Wall Street

The market in the United States opened quietly, and the S&P500 index began from discount of 0.14%. After the first transaction the bears took advantage and the S&P500 lost 0.3 percent, what turns out to be a weaker than expected scenario. The Warsaw WIG20 index is today one of the strongest indices in Europe and an hour before the close of trading the WIG20 index was at the level of 2,002 points (+0.17%).

-

14:34

U.S. Stocks open: Dow -0.29%, Nasdaq +0.14%, S&P -0.20%

-

14:28

Before the bell: S&P futures -0.15%, NASDAQ futures +0.01%

U.S. stock-index futures were flat amid tumbling oil prices and due to lack of macroeconomic data.

Global Stocks:

Nikkei Closed.

Hang Seng 22,558.69 +55.68 +0.25%

Shanghai 3,171.60 +17.28 +0.55%

FTSE 7,229.73 +19.68 +0.27%

CAC 4,873.75 -36.09 -0.74%

DAX 11,535.19 -63.82 -0.55%

Crude $52.95 (-1.93%)

Gold $1,181.20 (+0.66%)

-

14:06

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

3M Co

MMM

178

-0.23(-0.129%)

200

ALCOA INC.

AA

30.7

0.02(0.0652%)

4033

ALTRIA GROUP INC.

MO

68.28

0.05(0.0733%)

1314

Amazon.com Inc., NASDAQ

AMZN

796.48

0.49(0.0616%)

20147

American Express Co

AXP

76.1

0.63(0.8348%)

26338

AMERICAN INTERNATIONAL GROUP

AIG

66.82

0.01(0.015%)

1594

Apple Inc.

AAPL

118.11

0.20(0.1696%)

130921

AT&T Inc

T

41.34

0.02(0.0484%)

3188

Barrick Gold Corporation, NYSE

ABX

17.24

0.31(1.8311%)

98796

Boeing Co

BA

159.05

-0.05(-0.0314%)

416

Caterpillar Inc

CAT

92.62

-0.42(-0.4514%)

4240

Chevron Corp

CVX

116.36

-0.48(-0.4108%)

1005

Cisco Systems Inc

CSCO

30.29

0.06(0.1985%)

1233

Citigroup Inc., NYSE

C

60.08

-0.47(-0.7762%)

7374

Deere & Company, NYSE

DE

105.8

-0.69(-0.6479%)

690

Exxon Mobil Corp

XOM

88.26

-0.24(-0.2712%)

2814

Facebook, Inc.

FB

123.47

0.06(0.0486%)

74025

Ford Motor Co.

F

12.8

0.04(0.3135%)

26810

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

14.79

-0.11(-0.7383%)

36704

General Electric Co

GE

31.63

0.02(0.0633%)

10804

General Motors Company, NYSE

GM

35.85

-0.14(-0.389%)

31567

Goldman Sachs

GS

243.11

-1.79(-0.7309%)

14812

Google Inc.

GOOG

808

1.85(0.2295%)

4601

Home Depot Inc

HD

134

0.47(0.352%)

1649

Intel Corp

INTC

36.55

0.07(0.1919%)

2054

International Business Machines Co...

IBM

169.37

-0.16(-0.0944%)

361

Johnson & Johnson

JNJ

116.8

0.50(0.4299%)

570

JPMorgan Chase and Co

JPM

85.68

-0.44(-0.5109%)

28451

McDonald's Corp

MCD

121.09

0.33(0.2733%)

211

Microsoft Corp

MSFT

62.95

0.11(0.175%)

3971

Nike

NKE

53.89

-0.02(-0.0371%)

9005

Pfizer Inc

PFE

33.5

0.02(0.0597%)

8029

Procter & Gamble Co

PG

84.19

-0.84(-0.9879%)

34478

Starbucks Corporation, NASDAQ

SBUX

57.39

0.26(0.4551%)

17699

Tesla Motors, Inc., NASDAQ

TSLA

228.95

-0.06(-0.0262%)

6671

The Coca-Cola Co

KO

41.25

-0.49(-1.1739%)

81072

UnitedHealth Group Inc

UNH

161.58

-0.83(-0.5111%)

1720

Visa

V

82.2

-0.01(-0.0122%)

697

Wal-Mart Stores Inc

WMT

68.5

0.24(0.3516%)

2310

-

13:43

Upgrades and downgrades before the market open

Upgrades:

American Express (AXP) upgraded to Buy from Neutral at BofA/Merrill

Downgrades:Procter & Gamble (PG) downgraded to Sell from Neutral at Goldman

Coca-Cola (KO) downgraded to Sell from Neutral at Goldman

Other:Coca-Cola (KO) initiated with an Equal Weight at Barclays

-

12:01

WSE: Mid session comment

During the first half of today's session the volatility was low and the graph of the WIG20 repeatedly pushed the level of 2,000 points. The Warsaw market today is more powerful than the environment where the German DAX lost approx. 0.6 percent.

At the halfway point of today's quotations the WIG20 index was at the level of 2,001 points (+0,13%) and the turnover in the segment of largest companies was amounted to PLN 273 million.

-

09:20

Major stock markets in Europe trading mixed: FTSE + 0.33%, DAX -0.23%, CAC40 -0.2%, FTMIB + 0.02%, IBEX - 0.2%

-

08:17

WSE: After opening

WIG20 index opened at 1999.15 points (+0.02%)*

WIG 52783.13 0.12%

WIG30 2292.94 0.12%

mWIG40 4233.58 0.24%

*/ - change to previous close

The cash market started the new week from the neutral level, similar like the German DAX. The first transactions brought a slight weakening, however, we still look at the round level of 2,000 points. The turnover in the segment of the largest companies are not large, which may mean that investors have not returned yet after the three-day break.

After fifteen minutes of trading the WIG20 index was at the level of 1,996 points (-0,13%).

-

07:46

Negative start of trading expected on the major stock exchanges in Europe: DAX -0.2%, CAC40 -0.1%, FTSE -0.1%

-

07:20

WSE: Before opening

Today's session for the Warsaw market will mean the need to adapt to the changes that took place on Friday, when the Warsaw Stock Exchange was not working. On Friday were published data from the US labor market, which were slightly worse than expected, although the positive revisions for November improved sentiment. After the publication slightly strengthened the dollar and increased interest rates on bonds. Slightly cheaper was gold, while oil and copper have reacted rather stable. Stock markets around the world rose a little bit. In the US on Friday, the indices S&P500 and Nasdaq set new highs, but with the rather small increases of 0.35% and 0.6% respectively. The DJIA index rose by 0.3%, but the psychological level of 20,000 points has not been defeated. Today in the morning changes in Asia are rather small and peaceful and quotations of futures on the US indices rise slightly.

From the point of view of the Warsaw Stock Exchange it means rather quiet entry into the new week with a continuous looking at the level of 2,000 points.

In the macro calendar today there is no publication which could have a significant impact on the markets. Today begins the resulting season in the US, after the session Alcoa will give their results.

-

06:45

Global Stocks

Modest gains on Wall Street pushed the S&P 500 and Nasdaq Composite to record levels, while the Dow closed a fraction below the closely watched 20,000 level, following a December U.S. jobs report that investors interpreted as generally positive. All three benchmarks posted solid weekly gains, continuing the postelection rally on Wall Street. The U.S. economy created 156,000 jobs last month, below the consensus of 180,000 forecast by the economists polled by MarketWatch. However, sharp upward revisions for November jobs number and a slight trimming of October number means the latest payrolls were more or less in line, according to analysts.

Shares in Asia were broadly higher Monday, catching a further uplift from end-of-week gains in the U.S. The advance also follows strength last week in the region, where the Hang Seng saw its biggest weekly gain in three months and the Shanghai Composite SHCOMP, +0.47% snapped a five-week losing streak.

-