Market news

-

23:37

Stocks. Daily history for Nov 23’2016:

(index / closing price / change items /% change)

Shanghai Composite 3,241.47 -6.88 -0.21%

S&P/ASX 200 5,484.36 0.00 0.00%

FTSE 100 6,817.71 -2.01 -0.03%

CAC 40 4,529.21 -19.14 -0.42%

Xetra DAX 10,662.44 -51.41 -0.48%

S&P 500 2,204.72 +1.78 +0.08%

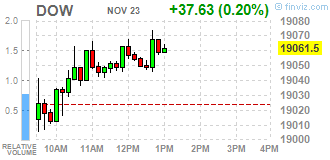

Dow Jones Industrial Average 19,083.18 +59.31 +0.31%

S&P/TSX Composite 15,080.91 -19.47 -0.13%

-

21:07

Major US stock indices showed mixed trends

Major US stock indexes finished trading mixed, but only with a slight change. The Dow Jones newly updated records, while the drop in shares of technology giants kept the Nasdaq in negative territory.

As it became known today, new orders for capital goods produced in the United States rebounded in October, due to the growth in demand for machinery and a number of other equipment, is the latest sign of the acceleration in economic growth at the beginning of the 4th quarter. The Commerce Department reported that non-defense capital goods orders excluding aircraft, planned indicator of business spending, rose 0.4% after it decreased by 1.4% in September.

In addition, the number of Americans who applied for unemployment benefits rose to a 43-year low last week, but remain below the level that is consistent with the tightening of the labor market. Primary applications for state unemployment benefits increased by 18,000 and reached a seasonally adjusted 251,000 for the week ending November 19, the Labor Department reported Wednesday.

However, the final results of the studies submitted by Thomson-Reuters and Institute of Michigan, showed that in November US consumers felt more optimistic about the economy than last month. According to the data, in November consumer sentiment index rose to 93.8 points compared with a final reading of 87.2 points in October and November preliminary value of 91.6 points. It was predicted that the index was 91.6.

It should also be noted that sales of new single-family homes unexpectedly fell up to October. However, experts believe that this is a temporary phenomenon for the new housing market, taking into account the ongoing improvement in the labor market. The US Commerce Department said, the seasonally adjusted new home sales fell in October by 1.9%, reaching 563.000 units (in terms of annual growth). The pace of sales for September were revised to 574,000 units from 593,000 units. It was expected that sales of single-family homes, which accounted for about 9.1% of total sales of property, amount to 593,000 units.

Oil recovered earlier lost ground, and went back to the opening level, helped by data from the US Department of Energy and the statements of the Minister of Oil of Iraq. US Department of Energy reported that crude oil inventories declined moderately by the end of last week, despite the expected increase. According to the data, during the week from 12 to 18 November crude oil inventories fell to 1.255 million. Barrels to 489.029 million. Barrels. Analysts on average had forecast growth stocks at 0.671 million. Barrels.

DOW index components closed mostly in positive territory (19 of 30). Most remaining shares rose Caterpillar Inc. (CAT, + 2.77%). Outsider were shares of Microsoft Corporation (MSFT, -1.28%).

Sector S & P index closed trading mixed. The leader turned out to be the industrial goods sector (+ 0.8%). Most utilities sector fell (-0.9%).

At the close:

Dow + 0.31% 19,082.36 +58.49

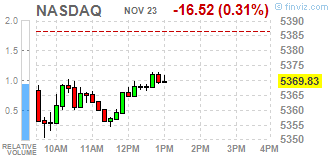

Nasdaq -0.11% 5,380.68 -5.67

S & P + 0.08% 2,204.63 +1.69

-

20:01

DJIA +0.19% 19,060.37 +36.50 Nasdaq -0.37% 5,366.48 -19.87 S&P -0.07% 2,201.31 -1.63

-

18:11

Wall Street. Major U.S. stock-indexes mixed

Major U.S. stock-indexes mixed. The Dow hit an all-time high for the third straight day on Wednesday, helped by a record-setting surge in industrial stocks, but a drop in technology heavyweights kept the S&P 500 and the Nasdaq in negative territory.

Most of Dow stocks in positive area (18 of 30). Top gainer - Caterpillar Inc. (CAT, +2.48%). Top loser - Microsoft Corporation (MSFT, -1.24%).

Most S&P sectors in negative area. Top gainer - Industrial goods (+0.6%). Top loser - Utilities (-0.6%).

At the moment:

Dow 19031.00 +36.00 +0.19%

S&P 500 2199.25 -1.00 -0.05%

Nasdaq 100 4844.25 -30.50 -0.63%

Oil 48.14 +0.11 +0.23%

Gold 1190.50 -20.70 -1.71%

U.S. 10yr 2.36 +0.04

-

17:00

European stocks closed: FTSE 100 -2.01 6817.71 -0.03% DAX -51.41 10662.44 -0.48% CAC 40 -19.14 4529.21 -0.42%

-

16:47

WSE: Session Results

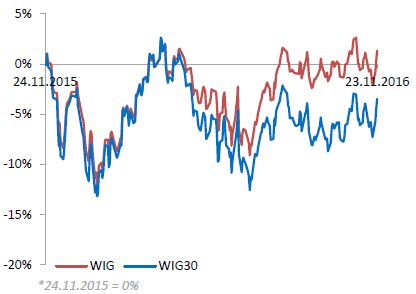

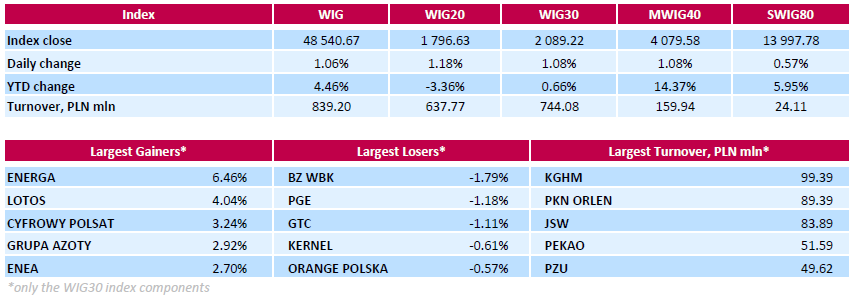

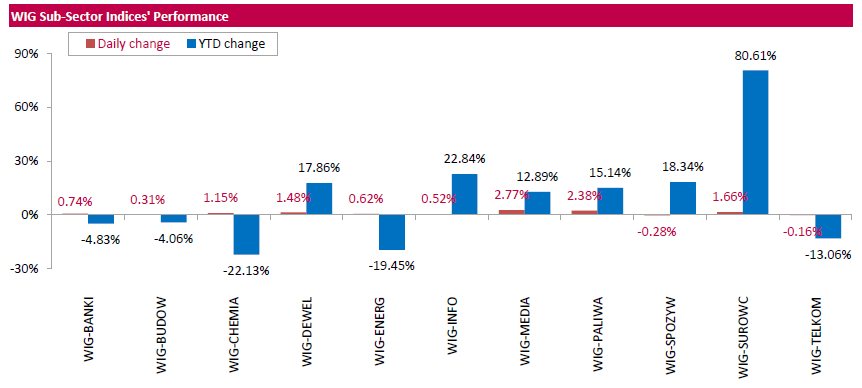

Polish equity market closed higher on Wednesday. The broad market measure, the WIG index, surged by 1.06%. Sector performance within the WIG was mainly positive as nine sectors recorded advances, with media (+2.77%) outpacing.

The large-cap stocks' measure, the WIG30 Index, rose by 1.08%. In the index basket, genco ENERGA (WSE: ENG) posted the strongest advance, up 6.46%. The company stated it is in talks with the European Investment Bank (EIC) on a EUR 250 mln issue of hybrid bonds in order to finance distribution and generation investments. The deal with EIB is expected to be struck near the end of first quarter of 2017. Other major outperformers were media group CYFROWY POLSAT (WSE: CPS), chemical producer GRUPA AZOTY (WSE: ATT), genco ENEA (WS: ENA) and two oil refiners LOTOS (WSE: LTS) and PKN ORLEN (WSE: PKN), which added between 2.69% and 4.04%. On the other side of the ledger, bank BZ WBK (WSE: BZW) and genco PGE (WSE: PGE) led a handful of losers, dropping by 1.79% and 1.18% respectively.

-

14:53

WSE: After start on Wall Street

The afternoon reading of data from the US economy surprised positively. The preliminary reading of durable goods orders - an increase of 1 percent - without transportation - can be considered as the good result.

The data on the number of new unemployed surprise at minus, but is mitigated by the fact that the report appears after strong data from the previous week. Data improve the situation of the dollar and the same spoil the situations of our national currency.

The EURUSD pair drops of 0.7 percent, which responses with increase of USDPLN pair by 1.1 percent. The zloty also weakened against the euro - the EURPLN pair is rising by 0.3 percent.

At the opening of trading on Wall Street, the S&P500 index has returned above the level of 2,200 points, although currently we can see slight declines in the US stock indices.

In the Warsaw market the withdrawal of the WIG20 has stopped at the level from the session opening and in Europe is visible attempt to rebuild after finding a local bottom. Our market still underlines visible from the beginning of the week relative strength against the major European parquet.

An hour before the close of trading in Warsaw the WIG20 index was at the level of 1,781 points (+0,35%).

-

14:35

U.S. Stocks open: Dow +0.04%, Nasdaq -0.48%, S&P -0.26%

-

14:30

Before the bell: S&P futures -0.17%, NASDAQ futures -0.27%

U.S. stock-index futures fell, as expectations the Fed would rise rates grew following some upbeat data on durable goods orders.

Global Stocks:

Nikkei Closed

Hang Seng 22,676.69 -1.38 -0.01%

Shanghai 3,241.47 -6.88 -0.21%

FTSE 6,801.91 -17.81 -0.26%

CAC 4,523.88 -24.47 -0.54%

DAX 10,643.10 -70.75 -0.66%

Crude $47.57 (-0.96%)

Gold $1,193.90(-1.43%)

-

14:08

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

3M Co

MMM

172.31

0.40(0.2327%)

1000

ALCOA INC.

AA

31

-0.34(-1.0849%)

3493

Amazon.com Inc., NASDAQ

AMZN

781.75

-3.58(-0.4559%)

15651

Apple Inc.

AAPL

111.5

-0.30(-0.2683%)

45963

Barrick Gold Corporation, NYSE

ABX

14.69

-0.66(-4.2997%)

157527

Boeing Co

BA

149.14

-0.38(-0.2541%)

1507

Caterpillar Inc

CAT

94.9

1.28(1.3672%)

28687

Citigroup Inc., NYSE

C

56.33

0.23(0.41%)

28410

Deere & Company, NYSE

DE

101.25

9.24(10.0424%)

744598

Exxon Mobil Corp

XOM

86.31

-0.37(-0.4269%)

3940

Facebook, Inc.

FB

121.27

-0.20(-0.1647%)

58742

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

14.82

-0.30(-1.9841%)

220077

General Electric Co

GE

31.17

-0.01(-0.0321%)

21407

General Motors Company, NYSE

GM

33.75

-0.06(-0.1775%)

472

Goldman Sachs

GS

211.4

0.29(0.1374%)

5561

Google Inc.

GOOG

765

-3.27(-0.4256%)

1876

Hewlett-Packard Co.

HPQ

15.24

-0.71(-4.4514%)

19855

Intel Corp

INTC

35.46

-0.02(-0.0564%)

2936

International Business Machines Co...

IBM

162.3

-0.37(-0.2275%)

1389

Johnson & Johnson

JNJ

112.2

-0.54(-0.479%)

7381

JPMorgan Chase and Co

JPM

78.63

0.10(0.1273%)

5710

McDonald's Corp

MCD

119.68

-0.01(-0.0084%)

135

Merck & Co Inc

MRK

60

-1.70(-2.7553%)

100944

Microsoft Corp

MSFT

61.05

-0.07(-0.1145%)

7920

Pfizer Inc

PFE

31.13

-0.20(-0.6384%)

10610

Procter & Gamble Co

PG

82.77

0.01(0.0121%)

1041

Starbucks Corporation, NASDAQ

SBUX

56.7

-0.42(-0.7353%)

1742

Tesla Motors, Inc., NASDAQ

TSLA

190.8

-0.37(-0.1935%)

17882

The Coca-Cola Co

KO

41.25

-0.12(-0.2901%)

7300

Twitter, Inc., NYSE

TWTR

18.49

-0.14(-0.7515%)

150673

Wal-Mart Stores Inc

WMT

70.38

0.26(0.3708%)

600

Walt Disney Co

DIS

97.75

0.04(0.0409%)

1967

Yahoo! Inc., NASDAQ

YHOO

40.99

-0.02(-0.0488%)

508

Yandex N.V., NASDAQ

YNDX

18.63

-0.32(-1.6887%)

4100

-

13:44

Upgrades and downgrades before the market open

Upgrades:

Volkswagen AG (VOW3) upgraded to Buy from Sell at Goldman

Downgrades:

Twitter (TWTR) downgraded to Negative from Mixed at OTR Global

Other:

-

13:35

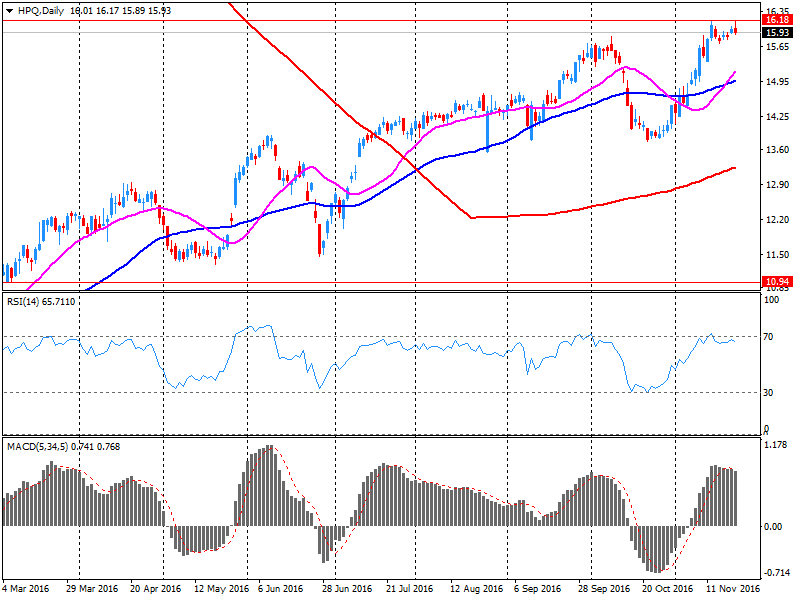

Company News: HP (HPQ) posts Q4 earnings in line with analysts' estimate

HP Inc. reported Q4 FY 2016 earnings of $0.36 per share (versus $0.93 in Q4 FY 2015), in-line with analysts' consensus estimate of $0.36.

The company's quarterly revenues amounted to $12.512 bln (+5.2% y/y), beating analysts' consensus estimate of $11.880 bln.

The company issued downside guidance for Q1 FY 2017, projecting EPS of $0.35-0.38 versus analysts' consensus estimate of $0.38.

HP reaffirmed guidance for FY 2017, forecasting EPS of $1.55-1.65 versus analysts' consensus estimate of $1.60.

HPQ fell to $15.69 (-1.63%) in pre-market trading.

-

13:18

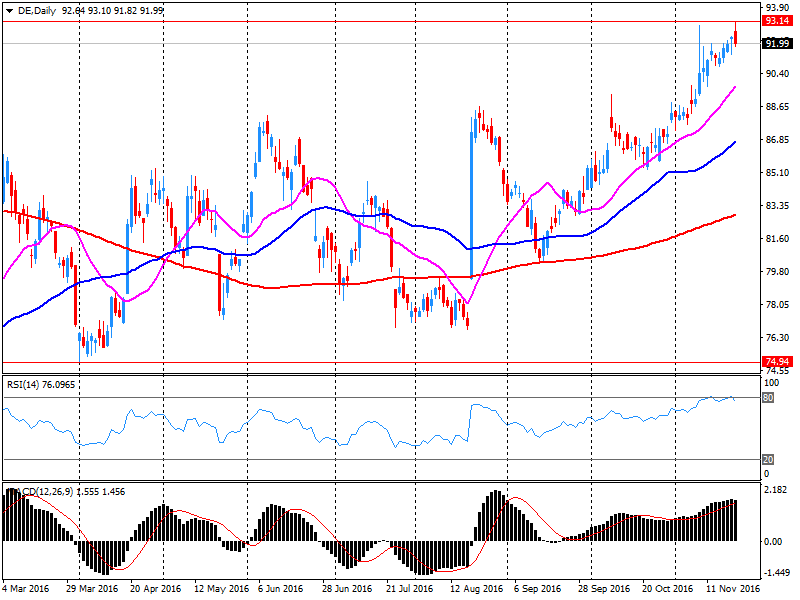

Company News: Deere (DE) quarterly results beat analysts’ expectations

Deere reported Q4 FY 2016 earnings of $0.90 per share (versus $1.08 in Q4 FY 2015), beating analysts' consensus estimate of $0.39.

The company's quarterly revenues amounted to $5.650 bln (-4.8% y/y), beating analysts' consensus estimate of $5.363 bln.

DE rose to $102.55 (+11.46%) in pre-market trading.

-

12:05

WSE: Mid session comment

Morning, preliminary readings of PMI indices did not arouse strong emotions. Industry data from Germany and France were slightly worse than expected, but the service sector showed better-than-expected level. The reading for the whole euro zone was better than expected in the case of industry and services. The data are calm in pronunciation and will quickly be forgotten.

In the first half of the trading, wave of supply in the major European markets brought the indices DAX and CAC40 to new session lows and declines exceeded 0.7 percent. Poorly behaves also contract on the S&P500, what may warn of a potential correction that may occur on Wall Street after the recent successes of the bulls.

Our market is still relatively stronger and remains over the line with a turnover approaching the level of PLN 400 million (the WIG index). This is a clear plus for the bulls, which may have a positive effect when European parquets will reach the bottom of the session and will start the process of rebuilding.

At the halfway point of today's trading the WIG20 index stood at the level of 1,779 points (+ 0,20%).

-

11:39

Major stock indices in Europe trading mixed

Stock indices in Western Europe show a mixed trend as investors assess the statistical data from the euro zone and are waiting for US economic data.

Euro zone services PMI rose from 53.2 points to 54.1 points - the highest since December 2015, according to preliminary data of Markit Economics.

"Preliminary estimates indicate that November will see the best monthly growth of business activity in the current year, - said a Chris Williamson - IHS Markit.

The composite index of the largest companies in the region Stoxx Europe 600 fell 0.39% - to 339.69 points.

The value of mining companies continued following raw material prices; capitalization of BHP Billiton and Fresnillo rose more than 2.5%.

However, the share prices of European banks fall on Wednesday, while Barclays lost 0.4% of market value, Credit Suisse - 0,9%, BNP Paribas - 0,5%.

Shares of Italian banks were among the outsiders in the run-up to the constitutional referendum. UniCredit Securities lost more than 3%, while shares of Banco Popolare di Milano fell by 5%.

Daimler shares fell 0.8% after reports that one of the leaders of the automaker was fired after being accused of insulting the Chinese people.

At the moment:

FTSE 6848.11 28.39 0.42%

DAX 10648.38 -65.47 -0.61%

CAC 4521.76 -26.59 -0.58%

-

08:19

WSE: After opening

WIG20 index opened at 1772.69 points (-0.17%)*

WIG 48117.17 0.18%

WIG30 2070.44 0.17%

mWIG40 4044.82 0.22%

*/ - change to previous close

The WIG20 futures today's trading began with 4 points above yesterday's close, but this advantage was given fairly quickly. Contracts for major European parquets suggested a slight withdrawal indexes.

The cash market began trading neutrally among the blue chips. Rapid improvement in the first minutes coincides with a positive surprise of the PMI reading from France, although it is rather the case given the absence of a similar reaction in Euroland. Among blue chips positively stands out Energa (WSE: ENG) with an increase of nearly 5 per cent and again KGH. Withdrawal we may see in PGE, which is under pressure of "sell" recommendation from Deutsche Bank.

After fifteen minutes of trading, the WIG20 index was at the level of 1,778 points (+0,15%).

-

07:52

Positive start of trading expected on the major stock exchanges in Europe: DAX + 0.3%, CAC40 + 0.3%, FTSE + 0.5%

-

07:32

WSE: Before opening

Wall Street has had another upward session, but it should be noted nightly withdrawal of the contract on the S&P500, which although losing only cosmetic value, but recalls that the meeting with 2,200 points it is not completed.

Wednesday is actually the last day of regular trading this week in the US - on Thursday, there are no sessions, and Friday sessions are shortened.

For this reason, it has been accelerated publication of macro data - including important reading of the number of new unemployed. Previously we will see a preliminary readings of PMI indices in Europe. Economic indicators and labor market data in the US remind that after the holiday weekend markets will come in the new month, the beginning of which brings the monthly data from the US labor market and readings of PMI and ISM indices from the US economy.

In the Warsaw market the last two sessions were successful, although part of the strength of the Warsaw Stock Exchange, with the accent on the WIG20, comes from adjustments of the dollar to emerging market currencies, including the zloty. Thus, the market performance largely depends on the condition of the zloty and the behavior of the dollar.

-

05:55

Global Stocks

Europe's main equity benchmark marched higher Tuesday, helped by advances for miners and U.K. manufacturer Rotork PLC, while a fake news release rocked French builder Vinci SA.

Major U.S. stock indexes closed at record highs for a second straight session Tuesday, with the Dow industrials and the S&P 500 also clearing noteworthy psychological barriers. U.S. stocks closed higher Tuesday as the Dow industrials and S&P 500 cleared psychological milestones but major indexes simultaneously reached record highs for a second straight day.

Asian shares traded in positive territory Wednesday, taking a lead from record gains in the U.S. overnight that were driven by continuing post-election exuberance.

-