Market news

-

23:29

Stocks. Daily history for Nov 24’2016:

(index / closing price / change items /% change)

Nikkei 225 18,333.41 +170.47 +0.94%

Shanghai Composite 3,241.49 +0.3516 +0.01%

S&P/ASX 200 5,485.08 0.00 0.00%

FTSE 100 6,829.20 +11.49 +0.17%

CAC 40 4,542.56 +13.35 +0.29%

Xetra DAX 10,689.26 +26.82 +0.25%

S&P 500 2,204.72 +1.78 +0.08%

Dow Jones Industrial Average 19,083.18 +59.31 +0.31%

S&P/TSX Composite 15,075.20 -5.71 -0.04%

-

17:00

European stocks closed: FTSE 100 +11.49 6829.20 +0.17% DAX +26.82 10689.26 +0.25% CAC 40 +13.35 4542.56 +0.29%

-

16:39

WSE: Session Results

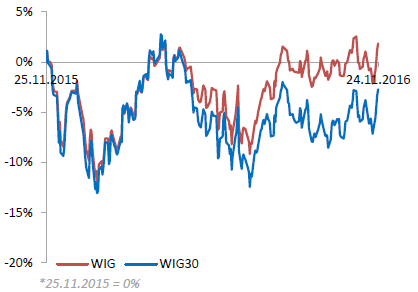

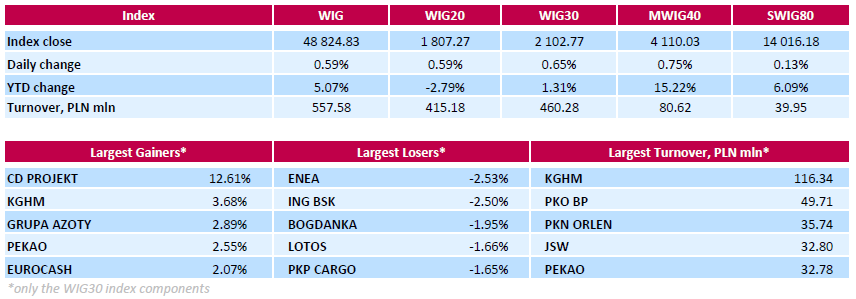

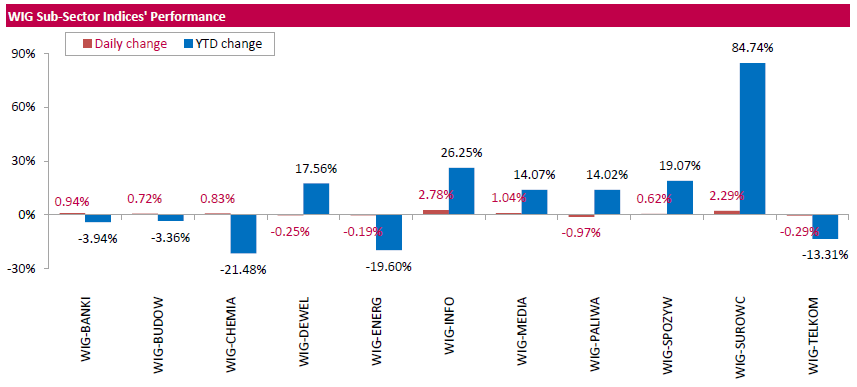

Polish equity market continued its upward trend on Thursday. The broad market measure, the WIG Index, advanced by 0.59%. The WIG sub-sector indices were mainly higher with information technology (+2.78%) outperforming.

The large-cap stocks' measure, the WIG30 Index, rose by 0.65%. Within the index components, videogame developer CD PROJEKT (WSE: CDR) became the session's best performer, as it stocks skyrocketed by 12.61%, helped by the announcement the analysts of one of the market participants re-initiated the stock with a 'Buy' recommendation and a target price of PLN 61 (compared to yesterday's closing price of PLN 43.22). Other major gainers were copper producer KGHM (WSE: KGH), chemical producer GRUPA AZOTY (WSE: ATT) and bank PEKAO (WSE: PEO), which gained 3.68%, 2.89% and 2.55% respectively. On the other side of the ledger, genco ENEA (WSE: ENA) and bank ING BSK (WSE: ING) recorded the sharpest declines, as the stocks corrected by 2.53% and 2.5% respectively after recent growth.

-

14:51

WSE: The final hour

Today in the US we have a day off and it's usually a good enough reason for the disappearance of the volatility in the Euroland markets. Except for the very beginning of trading, the indexes fluctuate slightly around their equilibrium levels. For example, the DAX long time fluctuates around 0.1 percent and it is clear that neither party has an idea for start of trading.

Although there is a stoic in the core markets during the absence of the Americans, our parquet in the last part of session behaves somewhat less. As expected, levels above 1,800 points in the case of the WIG20 force already more cautious. Similarly, the WIG and the sWIG80 approached the lows of the session.

An hour before the end of trading the WIG20 index was at the level af 1,803 points (+0.40%).

-

12:11

WSE: Mid session comment

The first half of today's trading shows quite good level of turnover as for the day without the Americans. In the segment of blue chips we have approx. PLN 220 million of turnover and in the whole market approx. PLN 320 million.

Today special mention deserve shares of CD Projekt (WSE: CDR), which take up to new highs and support approaching previous highs by the mWIG40 index. The blue chips are not worse, and the WIG20 maintains its positive behavior against the European environment. A day without Americans traditionally should lead to a peaceful trading and so in fact we observe. Thus the session is marked by consolidation in the near distance from yesterday's closing. The same behavior of the main European indices remains unsatisfactory due to the impotence of breakthrough the clear important resistance.

At the halfway point of today's session the WIG20 index was at the level of 1,801 points (+ 0.29%).

-

11:58

Major stock indices in Europe little changed

Stock indices of the major economies of Western Europe noting the increase in the shares of European pharmaceutical companies.

As IFO swoed the index of German business confidence in the economy in November remained at the level of 110.4 points, while analysts expected 110.5 points.

The German economy in the 3rd quarter increased by 0.2% compared with the previous three months. The dynamics coincided with the preliminary estimate and market expectations.

Also, Spanish data pointed to the growth of the economy in the third quarter by 0.7% compared with the previous quarter. The indicator has coincided with the market forecast. It is noted that for the past six quarters Spain's GDP grew by 0.8%.

As follows from the FOMC minutes, Fed officials actively discussed the rise in interest rates and came to the conclusion that this increase "may be appropriate soon enough."

According to the markets the chances of such a development in December is estimated at 100%.

The composite index of the largest companies in the region Stoxx Europe 600 rose 0,1% - to 341.09 points.

The value of securities of pharmaceutical companies Shire PLC and Novartis AG rose more than 0.4%.

Quotes of Banco Popolare climbed 1.8% after Goldman Sachs analysts worsened earnings for the period to 2020, but kept the rating of "buy".

Shares of Remy Cointreau, the second largest producer of alcohol in France rose by 1.8%. The company increased its net profit in the first half by 15% - up to 76 million euros.

Shares of Volkswagen rose 0.96% after CEO Herbert Diss said the company will no longer sell diesel models in the US.

At the moment:

FTSE 6799.57 -18.14 -0.27%

DAX 10669.90 7.46 0.07%

CAC 4533.95 4.74 0.10%

-

08:25

Major stock exchanges trading in the green zone: FTSE + 0.1%, DAX + 0.3%, CAC40 + 0.2%, FTMIB + 0,4%, IBEX + 0.3%

-

08:17

WSE: After opening

WIG20 index opened at 1798.00 points (+0.08%)*

WIG 48656.65 0.24%

WIG30 2094.92 0.27%

mWIG40 4085.85 0.15%

*/ - change to previous close

The futures market (contracts FW20Z1620) opened with a new dose of optimism, 8 points above yesterday's close. It was quite high opening, especially in relations with the peaceful environment, where the contract for the DAX was neutral with respect to yesterday's close.

The cash market starts today with no surprises. After what we have seen in the first minutes of contracts trading, the WIG20 increase in the first stage of today's session over 1,800 points. For now, the main driving force among the blue chips remains, of course, KGHM, which grows more than 2 percent. in response to a further strong increase in raw material prices.

After fifteen minutes of trading the WIG20 index was at the level of 1,797 points (+0,07%).

-

07:29

WSE: Before opening

Wednesday's session on the New York stock exchanges has brought little changes, but the Dow Jones, which at the end of the day increased by 0.31 percent to 19 083.76 points, reached the highest level in history.

Today's session due to the Thanksgiving holiday in the US should be reasonably calm. There is also no important reports in the macro calendar today.

The behavior of the Asian parquets in the morning is slightly downward. It stands out only the Japanese Nikkei, but this is due to the need to make up for the lack of yesterday's trading. Most parquets in Asia are slightly losing value. We may see continuing rise of metals prices, despite the persistent strength of the dollar. The same this morning copper gained another 2% and should support the behavior of such companies as KGHM.

In the case of the Warsaw Stock Exchange the yesterday's good behavior, in contrast to the weakness of Western Europe, was a big plus. The WIG20 index reached the area of 1,800 pts., which might have to tone down the appetite for growth. We approached the levels where previous waves of growth turned away, and the session without Wall Street does not serve growth solutions.

-

07:18

Positive start of trading expected on the major stock exchanges in Europe: DAX + 0.3%, CAC40 + 0.2%, FTSE + 0.3%

-

06:01

Global Stocks

European stocks ended with a small loss Wednesday, the first pullback in three sessions, as bank shares declined. "Markets in Europe have again struggled to keep track of record breaking U.S. markets, rolling over into the afternoon session on the back of a selloff in bond markets and a sharp rise in the U.S. dollar," said Michael Hewson, chief market analyst at CMC Markets UK, in a note.

Dow industrials and the S&P 500 notched a third straight record close on Wednesday, boosted in part by industrials, while the Nasdaq lagged behind in trading ahead of the Thanksgiving Day holiday. It's the third session in a row both the Dow and the S&P 500 have turned in record closes.

Asian markets were broadly down Thursday, in response to strong overnight U.S. economic data Thursday that pointed to rate rises, more dollar strength and the possibility of more capital flight from Asia. Durable goods orders in the U.S. rose 4.8% in October from a month earlier, well above the 2.7% gain predicted by economists surveyed by The Wall Street Journal. A gauge of U.S. consumer sentiment rose in November, signaling rising confidence in the economy.

-