Market news

-

18:00

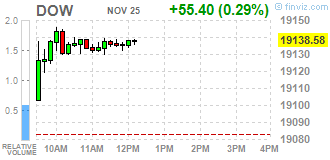

DJIA +0.25% 19,131.49 +48.31 Nasdaq +0.26% 5,394.52 +13.84 S&P +0.33% 2,211.93 +7.21

-

17:15

Wall Street. Major U.S. stock-indexes rose

Major U.S. stock-indexes hit record highs on Black Friday, helped by gains in consumer stocks at the start of the crucial holiday shopping season. Since the U.S. election, the three main U.S. indexes have hit all-time highs and closed at record levels multiple times in the past few days, most recently on Wednesday, when industrials boosted the Dow and S&P to record-high closes.

Most of Dow stocks in positive area (22 of 30). Top gainer - Cisco Systems, Inc. (CSCO, +1.40%). Top loser - Caterpillar Inc. (CAT, -0.63%).

Most S&P sectors in positive area. Top gainer - Conglomerates (+1.3%). Top loser - Basic Materials (-0.7%).

At the moment:

Dow 19106.00 +52.00 +0.27%

S&P 500 2207.50 +6.75 +0.31%

Nasdaq 100 4866.50 +17.00 +0.35%

Oil 46.34 -1.62 -3.38%

Gold 1180.40 -8.90 -0.75%

U.S. 10yr 2.38 +0.02

-

17:01

European stocks closed: FTSE 100 +11.55 6840.75 +0.17% DAX +10.01 10699.27 +0.09% CAC 40 +7.71 4550.27 +0.17%

-

16:53

WSE: Session Results

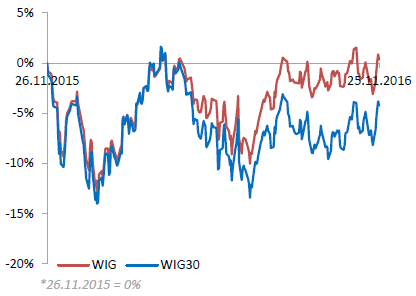

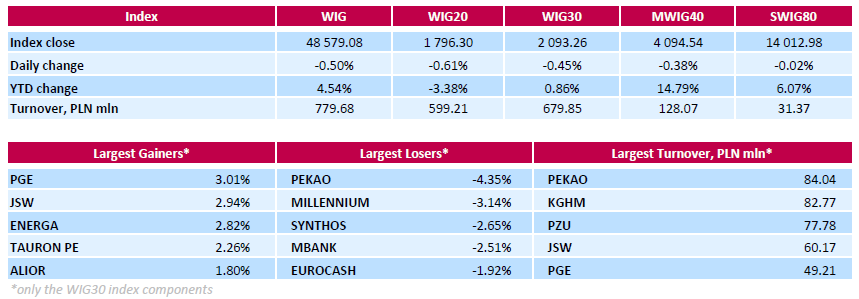

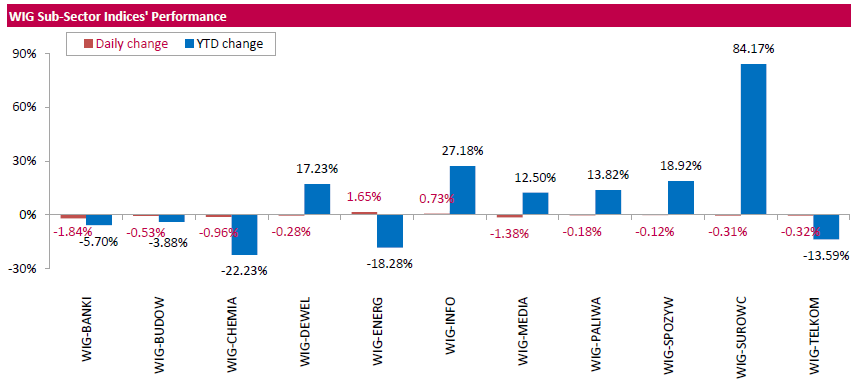

Polish equity market retreated on Friday. The broad market benchmark, the WIG index, fell by 0.5%. The WIG sub-sector indices were mainly lower with banking sector (-1.84%) underperforming.

The large-cap stocks' measure, the WIG30 Index, dropped by0.45%. In the WIG30 index basket, banking name PEKAO (WSE: PEO) was hit the hardest, down 4.35%. Poland's deputy prime minister Mateusz Morawiecki stated that the Polish state-run insurer PZU (WSE: PZU; +1.46%) and Polish Development Fund (PFR) are in the final stage of talks with Italy's UniCredit over buying its stake in PEKAO. Other largest decliners were chemical producer SYNTHOS (WSE: SNS) and two banks MILLENNIUM (WSE: MIL) and MBANK (WSE: MBK), which lost between 2.51% and 3.14%. On the other side of the ledger, gencos PGE (WSE: PGE) and ENERGA (WSE: ENG) were among the biggest advancers, climbing by a respective 3.01% and 2.82%, as Poland's energy minister Krzysztof Tchorzewski stated the country's state-run utilities will not be expected to invest more money to support the country's troubled coal mining firms.

-

14:53

WSE: After start on Wall Street

In the afternoon phase of today's session, the descent of the WIG20 index under 1,800 points was deepened by a dozen points and the level of today's decline is proportional to market optimism on the previous sessions of the week. Than for a new impetus to the fight against resistance we may count only in the new week, but after today's hesitance the market probably will hide again in the middle of a few weeks consolidation. One of the biggest outsiders in the first line of companies today is Bank Pekao (WSE: PEO) the valuation of which losing more than 4 per cent.

The opening on Wall Street maintains the S&P500 index above the level of 2,200 points, although we get the feeling that above this level bulls running out of arguments to continue trading.

On the threshold of the last trading hours this week the WIG20 index was at 1,793 points (-0.75%).

-

14:34

U.S. Stocks open: Dow +0.28%, Nasdaq +0.08%, S&P +0.17%

-

14:27

Before the bell: S&P futures +0.22%, NASDAQ futures +0.14%

U.S. stock-index futures advanced. The S&P 500 and the Dow were poised to hit record highs on Black Friday, with the focus on retailers at the start of the crucial holiday shopping season.

Global Stocks:

Nikkei 18,381.22 +47.81 +0.26%

Hang Seng 22,723.45 +114.96 +0.51%

Shanghai 3,261.49 +19.76 +0.61%

FTSE 6,837.87 +8.67 +0.13%

CAC 4,536.90 -5.66 -0.12%

DAX 10,676.28 -12.98 -0.12%

Crude $47.54 (-0.88%)

Gold $1,186.50 (-0.24%)

-

13:58

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

31.5

-0.01(-0.0317%)

3582

ALTRIA GROUP INC.

MO

64.21

0.19(0.2968%)

177200

Amazon.com Inc., NASDAQ

AMZN

785.4

5.28(0.6768%)

25400

Apple Inc.

AAPL

111.12

-0.11(-0.0989%)

20877

AT&T Inc

T

38.97

0.24(0.6197%)

11893

Boeing Co

BA

150

0.26(0.1736%)

702

Caterpillar Inc

CAT

96.49

0.31(0.3223%)

16910

Chevron Corp

CVX

110.6

-0.40(-0.3604%)

3210

Cisco Systems Inc

CSCO

29.65

-0.06(-0.202%)

1340

Citigroup Inc., NYSE

C

56.9

0.21(0.3704%)

10656

Deere & Company, NYSE

DE

101.62

-0.55(-0.5383%)

16308

Exxon Mobil Corp

XOM

86.31

-0.61(-0.7018%)

278

Facebook, Inc.

FB

121.06

0.22(0.1821%)

76920

Ford Motor Co.

F

86.31

-0.61(-0.7018%)

278

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

16.34

0.13(0.802%)

1175264

General Electric Co

GE

31.39

0.05(0.1595%)

2300

General Motors Company, NYSE

GM

33.83

-0.03(-0.0886%)

1130

Goldman Sachs

GS

212.26

-0.05(-0.0236%)

3042

Google Inc.

GOOG

764.9

3.91(0.5138%)

2715

HONEYWELL INTERNATIONAL INC.

HON

86.31

-0.61(-0.7018%)

278

Intel Corp

INTC

35.25

0.05(0.142%)

3428

International Business Machines Co...

IBM

161.84

-0.14(-0.0864%)

240

Johnson & Johnson

JNJ

113.5

0.43(0.3803%)

863

JPMorgan Chase and Co

JPM

79

0.14(0.1775%)

3029

Merck & Co Inc

MRK

61.8

0.16(0.2596%)

1711

Microsoft Corp

MSFT

60.42

0.02(0.0331%)

4998

Nike

NKE

51.5

0.16(0.3116%)

3346

Pfizer Inc

PFE

31.6

0.18(0.5729%)

20055

Procter & Gamble Co

PG

82.86

0.18(0.2177%)

269216

Starbucks Corporation, NASDAQ

SBUX

57.63

0.04(0.0695%)

283

Tesla Motors, Inc., NASDAQ

TSLA

193.75

0.61(0.3158%)

4449

The Coca-Cola Co

KO

41.15

0.03(0.073%)

396076

Twitter, Inc., NYSE

TWTR

18.28

0.06(0.3293%)

5460

Verizon Communications Inc

VZ

50.36

0.13(0.2588%)

925

Visa

V

79.8

0.23(0.2891%)

1200

Wal-Mart Stores Inc

WMT

71.35

0.52(0.7342%)

157158

Walt Disney Co

DIS

98.59

0.33(0.3358%)

8858

Yahoo! Inc., NASDAQ

YHOO

41.1

0.14(0.3418%)

3430

-

13:55

Upgrades and downgrades before the market open

Upgrades:

Deere (DE) upgraded to Neutral from Underperform at Longbow

Downgrades:

Other:

Deere (DE) target raised to $98 from $80 at RBC Capital Mkts

-

12:04

Major stock indices in Europe almost flat

The decline of oil prices had a negative impact on the securities of the energy sector, while shares of Italian lenders put pressure on the index of the banking sector in Europe.

The composite index of the largest companies in the region Stoxx Europe 600 fell by 0.08% to 341.57 points. The indicator increased by 0.7% since the beginning of this week.

European oil and gas companies index sank 0.71% as oil prices dropped more than 1% on the back of a strong dollar.

Mining shares are mixed amid falling prices for oil and copper, as well as the rise of the value of gold.

Shares of Royal Dutch Shell and BP fell 0.5%.

Shares of Rio Tinto rose 1%, Randgold Resources +1,2%, Glencore - have fallen in price 0,2%, Boliden -0.5%.

Shares of Italian banks fell by 0.45% due to concerns about the outcome of the referendum on the reform of the Constitution, which may collapse the government of the reformist Prime Minister Matteo Renzi. European banking index fell by 0.55%. the referendum will be held Dec 4

At the same time, the health sector index rose 0.61%.

Support to the sector had a sharp rally of Swiss biotech company Actelion after news that Johnson & Johnson made its takeover attempt. Actelion shares rose nearly 9% and ready to show the maximum one-day rise since mid-2014.

Daily Mail shares fell 3,7% after Barclays lowered to "underperform".

At the moment:

FTSE 6827.59 -1.61 -0.02%

DAX 10681.69 -7.57 -0.07%

CAC 4536.98 -5.58 -0.12%

-

12:03

WSE: Mid session comment

The session in Warsaw due to limited activity of the global players have to be calm, but slowly this baseline scenario faces a growing risk. We descend on minima session with a fall of the WIG20 by about 1 percent. The combination of meeting the WIG20 index with the levels of resistance and the upper limit of consolidation together with neutral attitude of core markets have given mix, which turned out to be stronger on the side of local factors. The market clearly hesitated at the height of 1,800 points and at this stage ignores even the strengthening of the zloty against the dollar and the euro.

After a few better sessions the WSE returns today to the relative weakness of that we have had in many months.

At the halfway point of today's quotations, the WIG20 index was st the level of 1,788 points (-1,03%).

-

08:23

Major stock exchanges trading in the green zone: FTSE 100 6,840.99 11.79 + 0.17%, DAX 10,699.15 9.89 + 0.09%, CAC 40 4,551.17 8.61 + 0.19%

-

07:21

Positive start of trading expected on the major stock exchanges in Europe: DAX + 0.2%, CAC40 + 0.1%, FTSE + 0.3%

-

06:30

WSE: before opening

Yesterday's holiday in the US and the lack of quotations on Wall Street causes that this morning in Europe is not going to be particularly exciting. Quiet trading is also seen in Asia.

The contracts on the S&P500 recorded now cosmetic loss. Minimally shifts appear on the currency market, where Eurodollar gaining 0.1 percent. Today's macro calendar does not contain critical data, so we may assume that in the environment there will be little change until the game will join players from the USA.

On the Warsaw market last four sessions were successful for the WIG20 index. Yesterday's rise in the absence of Wall Street indicates that the market is optimistic. However, from the point of view of technical analysis, resistance zone located above the level of 1810 points may encouraged to take profits.

Warsaw index since almost half of a year is moving in a trend channel with a horizontal limits set roughly at about 1,700 points from the bottom and 1,800 points from the top. So a really strong impulse is necessary to break the index out this template behavior. Such negative impulse could be unfavorable for the Prime Minister Renzi decision of the Italian referendum on December 4. In turn, the positive would be a classic rally of St. Claus on global stock markets, which, in fact we have not seen in three years.

-

06:01

Global Stocks

European stocks scored modest gains Thursday, with mining shares battling against dollar strength during a quieter-than-usual session with U.S. markets closed for the Thanksgiving holiday. "The usual Thanksgiving calm has descended across markets, as European investors reconcile themselves to a day of low volumes and quiet trading," said Chris Beauchamp, chief market analyst at IG, in an note.

U.S. stock futures edged up on Thursday, as traders focused on their Thanksgiving Day celebrations rather than making big bets. U.S. stock markets and the bond market are closed Thursday for the holiday, and equity trading hours will be shortened on Friday.

Asian share markets were broadly higher early Friday, with Japan's Nikkei leading after the yen hit a fresh eight-month low against the dollar, helping boost the competitiveness of the country's exports.

-