Noticias del mercado

-

16:30

U.S.: Crude Oil Inventories, June -4.053

-

16:04

Pending home sales in US down 3.7%

The Pending Home Sales Index, a forward-looking indicator based on contract signings, slid 3.7 percent to 110.8 in May from a downwardly revised 115.0 in April and is now slightly lower (0.2 percent) than May 2015 (111.0). With last month's decline, the index reading is still the third highest in the past year, but declined year-over-year for the first time since August 2014.

Lawrence Yun, NAR chief economist, says pending sales slumped in May across most of the country. "With demand holding firm this spring and homes selling even faster than a year ago1, the notable increase in closings in recent months took a dent out of what was available for sale in May and ultimately dragged down contract activity," he said. "Realtors are acknowledging with increasing frequency lately that buyers continue to -

16:00

U.S.: Pending Home Sales (MoM) , May -3.7% (forecast -1%)

-

15:49

Option expiries for today's 10:00 ET NY cut

EURUSD 1.1050 (636m)

GBPUSD 1.3500 ( GBP 382m)

AUDUSD 0.7290-7300 (AUD 800m) 0.7350 (254m) 0.7500 (670m)

USDCAD 1.3150 (USD 284m)

-

15:47

German Finance Minister Schäuble: We can not exclude a "domino effect" after Brexit

- It would be correct if the UK would have notified the EU of its plans to exit from the block in the foreseeable future.

- We manage to prevent chaos in the financial markets after Brexit.

- Uncertainty in the financial markets will persist.

-

15:18

-

14:34

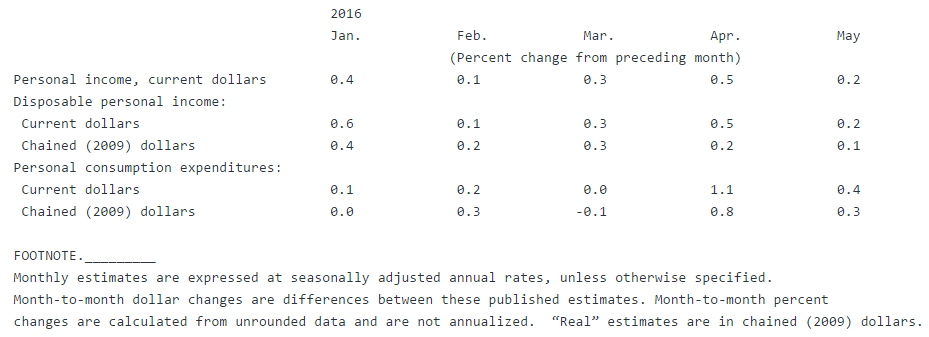

Personal income in US increased slightly lower than forecasts

Personal income increased $37.1 billion, or 0.2 percent, and disposable personal income (DPI) increased $33.9 billion, or 0.2 percent, in May, according to the Bureau of Economic Analysis. Personal consumption expenditures (PCE) increased $53.5 billion, or 0.4 percent. In April, personal income increased $75.4 billion, or 0.5 percent, DPI increased $68.6 billion, or 0.5 percent, and PCE increased $141.2 billion, or 1.1 percent, based on revised estimates.

Real DPI increased 0.1 percent in May, compared with an increase of 0.2 percent in April.

Real PCE increased 0.3 percent, compared with an increase of 0.8 percent.

-

14:31

U.S.: PCE price index ex food, energy, m/m, May 0.2% (forecast 0.1%)

-

14:31

U.S.: PCE price index ex food, energy, Y/Y, May 1.6%

-

14:30

U.S.: Personal Income, m/m, May 0.2% (forecast 0.3%)

-

14:30

U.S.: Personal spending , May 0.4% (forecast 0.4%)

-

14:30

European session review: the pound continues to recover after the collapse

The following data was published:

(Time / country / index / period / previous value / forecast)

1:00 Australia Sales of new buildings, m / m in May -4.7% -4.4%

6:00 UK House Price Index from Nationwide, m / m in June 0.2% 0% 0.2%

6:00 UK House Price Index from Nationwide, y / y in June 4.7% 4.9% 5.1%

6:00 Germany consumer confidence index from the GfK July 9.8 9.8 10.1

6:00 Switzerland indicator of consumer activity from May 1.24 1.35 UBS

8:30 Volume UK net lending to individuals, 1.6 billion in May 4.3

8:30 UK Changing the volume of consumer lending, million 1400 1503 May 1294

8:30 UK approved applications for mortgage loans, th. May 66.21 65.25 67.04

9:00 Eurozone index of sentiment in the economy in June 104.6 104.7 104.4

9:00 Eurozone consumer confidence index (final data) June -7 -7 -7.3

9:00 Eurozone Sentiment Index in the business community June 0.26 0.26 0.22

9:00 Eurozone business confidence index in industry in June -3.7 -3 -2.8

12:00 Germany Consumer Price Index m / m (preliminary data) June 0.3% 0.2% 0.1%

12:00 Germany Consumer Price Index y / y (preliminary data) June 0.1% 0.3% 0.3%

The euro rose slightly against the dollar, returning to yesterday's high, which was associated with the expectations of US reports, including personal income and expenses, and home sales. Investors also continue to follow the news from the EU summit, during which politicians discuss Britain's decision to leave the EU. Market analysts believe that European leaders will expect to see negative economic data, before taking measures against the consequences of the referendum.

he results of the research, published by the European Commission showed that economic confidence in the euro area fell in June, contrary to expectations of a slight increase. According to the data, the index of economic sentiment, which is a gauge of consumer and business confidence fell in June to 104.4 points from 104.6 points in May (revised from 104.7 points). In addition, it was announced that the final index of sentiment among consumers dropped in June from -7.0 points to -7.3 points, confirming the initial assessment, but exceeded the experts' forecasts (-7.0 points).

Sentiment in the services sector fell to 10.8 from 11.3 in May, but the index of business optimism in industry rose to -2.8 from -3.7. It was expected that the confidence in industry improved to -3.0. The index of sentiment in the business circles dropped to 0.22 from 0.26 in May. Analysts predicted that the rate will remain unchanged.

The pound rose moderately against the dollar, helped by renewed risk appetite, as well as statistics on Britain. The Bank of England said that the volume of consumer credit has increased significantly in May, recording the fastest pace since 2005. According to the data, in May, the number of approved applications for mortgage loans rose to 67 042 compared to 66 205 in April (revised from 66,250).

Analysts had forecast a contraction of approved applications to 65 250. In the meantime, consumer loans increased in May by 9.9 percent in annual terms (up to 1.503 billion gbp), showing the biggest gain since November 2005. Economists had expected a rise to 1.4 billion gbp.

Net mortgage lending rose in May to 2.824 billion pounds, which was more than forecast (2.2 billion). Consumer credit rose by 1.503 billion gbp. Lending to non-financial enterprises increased by 2.814 bn. pounds after falling 176 million n April.

Also today, Fitch revised the outlook on the reduction of Britain's GDP, adding that it may encourage the Central Bank to lower the rate to 0.25% by the end of the year.

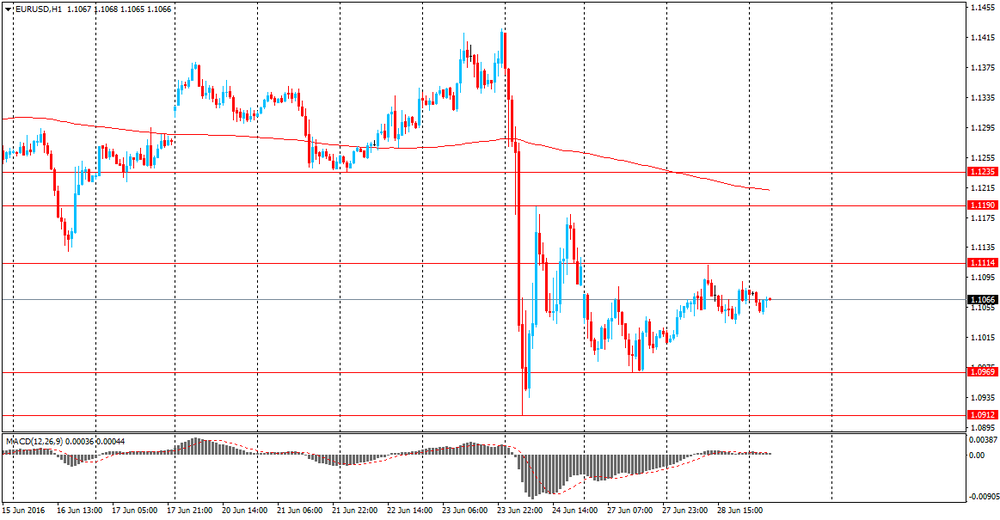

EUR / USD: during the European session rose to $ 1.1102

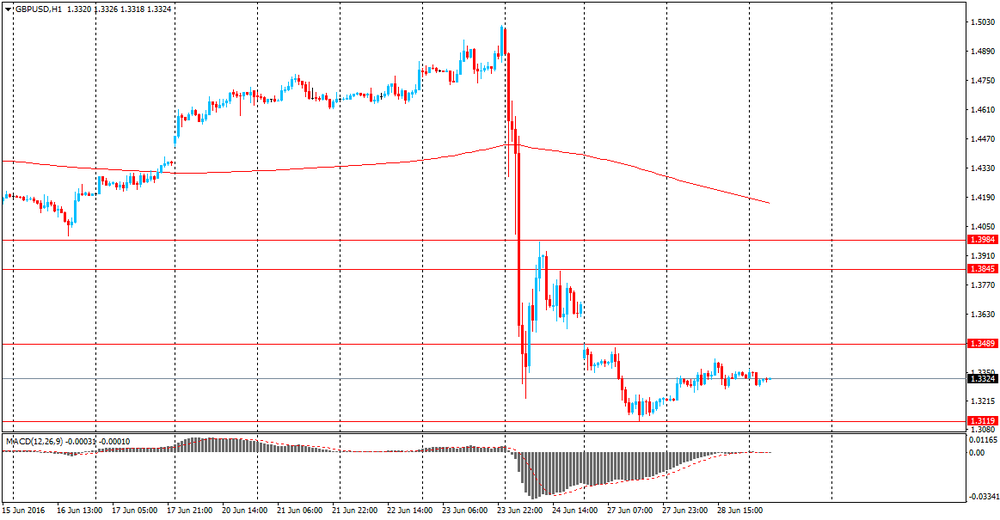

GBP / USD: rose to $ 1.3453

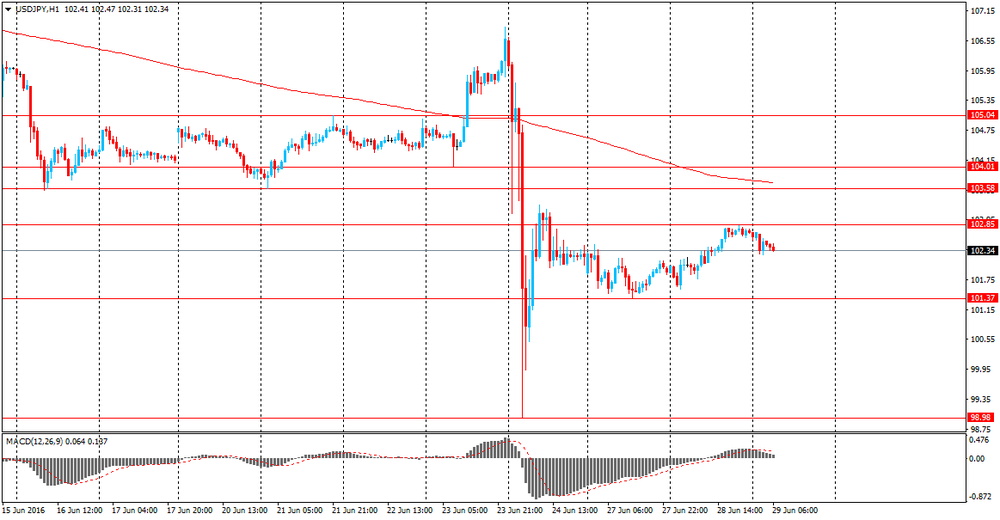

USD / JPY: rose from Y102.14 to Y102.75

-

14:10

Germany’s inflation lower in June

Flash CPI index in Germany fell monthly to 0.1% from a previous value of 0.3%. Bloomberg forecasts indicated the rise of inflation with 0.2%. CPI measures the changes in the price of goods and services purchased by consumers.

Harmonised Index of Consumer Prices (HICP) unchanged at +0.2%. No impact or Eur/Usd in a quiet trading so far.

-

14:00

Germany: CPI, y/y , June 0.3% (forecast 0.3%)

-

14:00

Germany: CPI, m/m, June 0.1% (forecast 0.2%)

-

13:46

Orders

EUR/USD

Offers 1.1120-25 1.1150 1.1170 1.1200 1.1200 1.1230-40 1.1280 1.1300

Bids 1.1050-55 1.1025-30 1.1000 1.0975-80 1.0930 1.0900 1.0885 1.0850

GBP/USD

Offers 1.3425-30 1.3450 1.3475-80 1.3500 1.3550 1.3580 1.3600

Bids 1.3345-50 1.3330 1.3280 1.3255-60 1.3230 1.3200 1.3170 1.3150 1.3100

EUR/GBP

Offers 0.8320 0.8330-35 0.8350 0.8370-75 0.8400 0.8465 0.8500

Bids 0.8275-80 0.8250 0.8200-0.8195 0.8165 0.81500 0.8130 0.8100

EUR/JPY

Offers 113.30 113.55-60 113.80 114.00 114.30 114.50 115.00

Bids 112.55-60 112.30-35 112.00 111.70 111.50 111.00 110.60 110.00 109.50 109.00

USD/JPY

Offers 102.50 102.75-80 103.00 103.25 103.50 103.85 104.00

Bids 102.00 101.80 101.65 101.50 101.20-25 100.65 100.00

AUD/USD

Offers 0.7420-25 0.7450-55 0.7485 0.7500 0.7520 0.7550

Bids 0.7375-80 0.7350-55 0.7320 0.7300 0.7285 0.7265 0.7230 0.7200

-

13:14

Fitch forecast: Bank of England will lower rates by 0.25% by year-end

US ratings agency out with a client note 29 June 2016

- UK to face large investment shock post-Brexit.

- 2017 & 2018 GDP to fall to around 1%.

- uncertainty to prompt firms to delay investment, hiring decisions.

-

11:41

BofA Merill Lynch: Gbp/Usd to 1.30 at the end of 2016

eFXnews quoting a Bank of America Merill Lynch forecast:

Sailing into the unknown:

FX markets were surprised by the Brexit vote. The implications of the referendum result are hard to nail down, but we expect them to be negative in most scenarios. We would also expect markets to start pricing some tail risks that other countries may decide to leave the EU as well. More broadly, we would expect Brexit to trigger a chain of non-linear events well into the long-term that are hard to predict and may seem unrelated today, a butterfly effect on steroids. Brexit could prove to be just the end of the beginning.

Negative for European currencies:

We believe that the result of the UK referendum for exit from the EU is negative for the major European currencies, most for GBP, then for EUR. We expect it to be positive for JPY, followed by the USD. High beta currencies could find support in further easing by major central banks in the short term.

New projections:

In this context, we are revising our G10 projections. Our baseline was assuming that the UK would stay in the EU, although this was a very close call. However, we avoid bold changes in projections beyond GBP, as no G10 economy is strong enough to afford a strong currency.

We expect EUR/USD to end 2016 at 1.05, from 1.08 before, appreciating to 1.10 by the end of 2017, from 1.15 before.

We expect JPY to remain strong and now forecast USD/JPY to end 2016 at 105. Our previous projection was 110, but with substantial downside risks. Moreover, USDJPY can overshoot below 100 in the short term.

We now expect GBP/USD to end 2016 at 1.30, from 1.59 in the Remain scenario. We expect further GBP weakness in 2017.

-

11:12

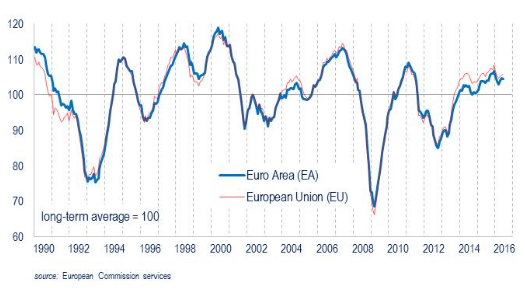

Economic sentiment in Euro Zone unchanged

In June, after two consecutive months of improved readings, the Economic Sentiment Indicator (ESI) remained broadly unchanged in both the euro area (-0.2 points to 104.4) and the EU (+0.1 points to 105.7).

Inflation expectations increased to 5.1 from 3.4 prior. Eur/Usd little changed so far.

-

11:05

Shibayama: Bank of Japan won't hesitate to respond to excessive FX speculation

-

Should not rule out solo fx intervention in the case of excessive yen rises.

-

BOJ should stand ready to hold emergency policy meeting if market moves become excessive.

-

Further easing should take into account the fact that negative rates caused a bigger than expected impact.

-

-

11:01

Eurozone: Consumer Confidence, June -7.3 (forecast -7)

-

11:00

Eurozone: Economic sentiment index , June 104.4 (forecast 104.7)

-

11:00

Eurozone: Business climate indicator , June 0.22 (forecast 0.26)

-

11:00

Eurozone: Industrial confidence, June -2.8 (forecast -3)

-

10:38

United Kingdom: lending to individuals increased $4.3 bln

Total lending to individuals increased by £4.3 billion in May, compared to the average of £5.1 billion over the previous six months. The three-month annualised and twelve-month growth rates were 4.1% and 4.0% respectively.

-

10:36

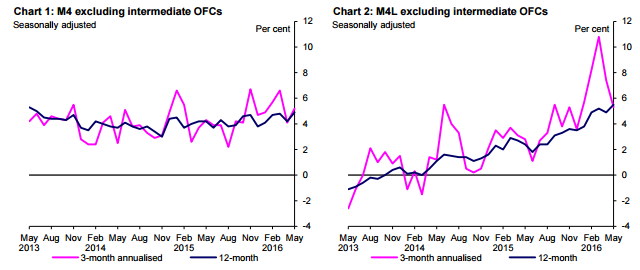

Money supply in UK increased in May

UK broad money, M4ex, is defined as M4 excluding intermediate other financial corporations (OFCs). M4ex increased by £16.7 billion in May, compared to the average monthly increase of £6.9 billion over the previous six months. The three-month annualised and twelve-month growth rates were 5.2% and 4.9% respectively. M4Lex is defined as M4 lending excluding intermediate OFCs. M4Lex increased by £11.8 billion in May, compared to the average monthly increase of £9.6 billion over the previous six months. The three-month annualised and twelve-month growth rates were 5.3% and 5.5% respectively.

Economic data calculated before Brexit so next month's data will have a bigger impact on the pound.

-

10:31

Oil is rising in today’s trading

This morning, New York crude oil futures WTI rose by 1.09% to $ 48.37 per barrel and Brent oil futures climbed 0.89% to $ 49.69 per barrel. Thus, the black gold is gaining around 1%, as investors began to invest in commodity assets, after risks associated with the exit of Britain from the European Union fades. The second reason for the oil price growth - a strike in Norway and the crisis in Venezuela. In addition, data from the American Petroleum Institute (API) showed a reduction in reserves to 3.86 million barrels per week.

-

10:31

United Kingdom: Net Lending to Individuals, bln, May 4.3

-

10:30

United Kingdom: Consumer credit, mln, May 1503 (forecast 1400)

-

10:30

United Kingdom: Mortgage Approvals, May 67.04 (forecast 65.25)

-

10:01

Option expiries for today's 10:00 ET NY cut

EUR/USD 1.1050 (636m)

GBP/USD 1.3500 ( GBP 382m)

AUD/USD 0.7290-7300 (AUD 800m) 0.7350 (254m) 0.7500 (670m)

USD/CAD 1.3150 (USD 284m)

-

09:51

Review of financial and economic press: the Parliament of Netherlands rejected the Nexit idea

D / W

German Chancellor Angela Merkel believes that Brexit is a foregone conclusion and irreversible. In her opinion, as expressed on Tuesday, June 28 during a summit in Brussels, "everything can not be deployed again." Now is not the time for wishful thinking, the Chancellor said. It also welcomed the plan, according to which the new summit of EU heads of states will be held in September without the participation of London.

In London Brexit opponents rally

More than a thousand people (according to other sources - a few thousand) gathered on Tuesday, June 28 at London's Trafalgar Square for a rally aimed against Brexit. The action took place despite the fact that earlier the organizers said that it will be canceled because of the inability to guarantee the security of its members. The rally was held under the motto "Stay together" (Stand together). Leader of "Liberal Democrats" Tim Farron, also came to Trafalgar Square, said the gathering in question.

Brussels after Brexit: The EU recognizes its share of the blame for the results of the referendum

In Brussels on Tuesday, began the summit of heads of states and governments of EU member states - the first since the referendum on UK. The main working of the EU summit meeting will be held on Wednesday, 29 June. David Cameron will not take part in them.

The Parliament of the Netherlands rejected the Nexit idea

The Parliament of the Netherlands did not support the right Freedom Party leader Geert Wilders' proposal to hold a referendum on the country's membership in the European Union. At a meeting on Tuesday, the referendum idea was supported by only 14 deputies out of 75. Wilders proposed that the authorities do as much as possible to carry out "Nexit". However, under the current laws of the Netherlands a popular vote on EU membership is impossible.

Newspaper. ru

FT: Brexit day was the most unstable in the foreign exchange market history

The British Treasury has warned about the growth of tax due to Brexit.

UK Finance Minister George Osborne announced a tax increase and reduction of budget expenditures in connection with the referendum on withdrawal from the EU, according to Reuters.

FT: Brexit could cost the world economy more than $ 3 trillion

Stock markets around the world lost a record $ 3 trillion over two trading days after the results of the referendum. Provoked panic selling on the leading trading floors of the world, writes the Financial Times with reference to the market participants.

Total will develop the largest oil field in Qatar

The French oil company Total has been selected to develop the largest oil field in Qatar, Bloomberg writes. It is noted that Total has won a 30% stake in partnership with Qatar Petroleum. The two companies will create a new company North Oil Co. for Shaheen field development in the next 25 years.

RBC

Toyota announced a withdrawal of 1.43 million vehicles worldwide

Toyota announced a recall of 1.43 million hybrids Prius and Lexus CT200h due to a possible defect at the airbags. This will affect cars from 2010-2012.

-

09:17

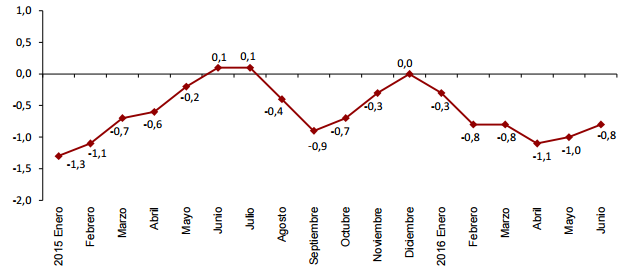

Spanish inflation better than forecasts

The estimated CPI annual inflation in June 2016 was -0.8%, according to the leading indicator compiled by the INE.

This indicator provides a preview of CPI, if confirmed, would be a increase of two tenths in the annual rate, since in May the change was -1.0%.

This behavior influences the rise in fuel prices (diesel and gas) and electricity.

-

09:05

Today’s events:

At 08:00 GMT the ECB board member Benoit Coeure will deliver a speech.

At 10:30 GMT the ECB Vice-President Vitor Constancio will give a speech.

At 16:00 GMT the ECB member Yves Mersch owill make a speech.

Day 2 of the EU economic summit.

-

08:49

Asian session review: we know what happens after tight ranges

The yen has stabilized, halting its recent strong gains. Today, Japanese Prime Minister Shinzo Abe urged the Bank of Japan to provide sufficient funds to satisfy market liquidity. He also instructed the Minister of Finance Aso to pay the utmost attention to movements in the currency and the financial markets.

Abe said that the uncertainty and risks in the financial markets persist and the government is ready to mobilize all available means of policies to support the Japanese economy.

Bank of Japan governor, Kuroda, in turn, said that Japanese banks do not have problems with funding in foreign currency and the Bank of Japan will be able to add funds to the market if necessary.

The volume of retail sales in Japan remained unchanged at the level of 0.0% in May. In annual terms, this figure fell to -1.9% from the previous value of -0.9%. Analysts expected a decline to -1.6%.

Retail sales in large stores in Japan also declined, reaching 2.2% in May after falling 0.7% in April

Pound traded near the low of June 24 as the market is concerned about the possible consequences of Brexit. Recall, the pound touched its lowest level since mid-1985 - $ 1.3119, having fallen by 11.5% compared to the closing level on June 23.

The euro has stabilized in a tight range, preparing the next sharp move. Yesterday ECB President Draghi in an interview with Bloomberg said that the UK decision to leave the EU could lead to a reduction in euro zone GDP growth of 0.5%. GDP growth will decline, at least for three years. Draghi also said that it is time to pay attention to the potential Brexit impact on the banking and could have a negative impact on the currency markets.

The Australian dollar generally traded around yesterday's high. Since the beginning of the session, the AUD/USD fell slightly against the background of negative data on new home sales in Australia. As it became known, new home sales in Australia declined in May to -4.4%, after declining in April at -4.7%.

Despite a slight improvement, sales of new homes continued to decline since the beginning of this year. Sales of detached houses fell by -6.7% and sales of apartment buildings rose by + 4.9%.

EUR / USD: during the Asian session, the pair traded in the $ 1.1045-60 range.

GBP / USD: traded in of $ 1.3285-1.3305 range.

USD / JPY: traded in Y101.15-25 range.

-

08:30

Options levels on wednesday, June 29, 2016:

EUR/USD

Resistance levels (open interest**, contracts)

$1.1315 (1979)

$1.1234 (3074)

$1.1172 (1100)

Price at time of writing this review: $1.1059

Support levels (open interest**, contracts):

$1.1008 (9785)

$1.0949 (9021)

$1.0874 (15168)

Comments:

- Overall open interest on the CALL options with the expiration date July, 8 is 41778 contracts, with the maximum number of contracts with strike price $1,1500 (5265);

- Overall open interest on the PUT options with the expiration date July, 8 is 90102 contracts, with the maximum number of contracts with strike price $1,0900 (15168);

- The ratio of PUT/CALL was 2.16 versus 2.29 from the previous trading day according to data from June, 28

GBP/USD

Resistance levels (open interest**, contracts)

$1.3607 (455)

$1.3510 (679)

$1.3414 (95)

Price at time of writing this review: $1.3320

Support levels (open interest**, contracts):

$1.3190 (3034)

$1.3093 (419)

$1.2995 (2409)

Comments:

- Overall open interest on the CALL options with the expiration date July, 8 is 31281 contracts, with the maximum number of contracts with strike price $1,5000 (4020);

- Overall open interest on the PUT options with the expiration date July, 8 is 44370 contracts, with the maximum number of contracts with strike price $1,3500 (4293);

- The ratio of PUT/CALL was 1.42 versus 1.61 from the previous trading day according to data from June, 28

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

08:19

Danske Bank about post-Brexit setup

EUR/USD. We are adjusting our EUR/USD forecasts in line with what we communicated before and immediately after Brexit. We now forecast EUR/USD at 1.09 in 1M (1.11 previously), 1.07 (1.10) in 3M, 1.10 (1.14) in 6M and 1.14 (1.18) in 12M. Short-term, we expect increased political uncertainty in the eurozone and the prospects of further monetary easing to weigh on EUR/USD. However, medium-term we continue to expect that the undervaluation of the EUR and the large eurozone-US current account differential will support the EUR.

USD/JPY. We are lowering our USD/JPY forecasts to 105 in 1M (108 previously), 107 in 3M (112), 108 in 6M (112) and 108 in 12M (112). Brexit and our call that the Fed will now be on hold for the rest of 2016 imply that there is less room for USD/JPY to move higher. We continue to expect that BoJ will ease aggressively in July by cutting interest rates by 20bp and to announce additional quantitative easing. In addition, the risks of FX intervention are increasing. Hence, we expect USD/JPY to edge higher on 0-3M and stabilise medium-term.

USD/CAD: We still expect the fundamentally undervalued 'loonie' to gradually appreciate over the coming year on the back of valuation, a gradually higher oil price, markets re-pricing BoC monetary policy and a generally improved growth outlook in North America. On the back of the decline in oil prices and with the outlook of more short-term USD strength we lift our forecast profile to 1.33 in 1M (from 1.31), 1.31 in 3M (1.28), 1.28 in 6M (1.26) and 1.25 in 12M (1.24).

-

08:15

FOMC member Jerome Powell: Fed ready to act if the pressure increase

- UK decision to withdraw from the EU has increased the risks with new challenges for the United States and other countries.

- It is too early to judge the effects of Brexit on the United States.

- Global economic and financial conditions are particularly important for the United States.

- The most important task of the Federal Reserve is to assess the implications for monetary policy, as the United States continues to make progress on employment and inflation targets.

- The Fed is closely watching inflation expectations, it is important that they remain fixed for the Fed to achieve the goal of 2%.

- Alarmingly possible loss of momentum in the labor market.

-

08:12

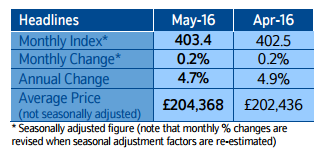

House price index in UK up 0.2%

Commenting on the figures, Robert Gardner, Nationwide's Chief Economist, said:

"UK house prices edged up 0.2% in May and, as a result, the annual rate of house price growth was little changed at 4.7%, compared with 4.9% in April.

The annual pace of house price growth remains in the fairly narrow range between 3% and 5% that has been prevailing for much of the past twelve months.

In the near term, it's going to be difficult to gauge the underlying strength of activity in the housing market due to the volatility generated by the stamp duty changes which took effect from 1 April.

Indeed, the number of residential property transactions surged to an all-time high in March, some c11% higher than the pre-crisis peak as buyers of second homes sought to avoid the additional tax liabilities".

-

08:07

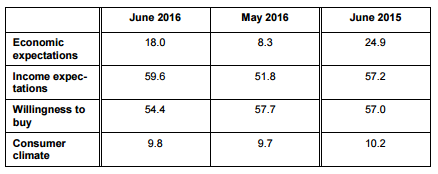

Economic expectations of German citizens have improved considerably

The overall consumer climate indicator is forecasting 10.1 points for July compared with 9.8 points in June. Economic and income expectations are markedly on the up, while willingness to buy fell slightly.

Consumers expect the German economy to be in good shape over the coming months. This has resulted in a considerable increase in economic expectations this month. Given this outlook, income expectations have reached their highest level since German reunification. Only willingness to

buy is slightly down, but is still at a very strong level.

The economic expectations of German citizens have improved considerably in June. The indicator has gained 9.7 points to reach a total of 18 points.

This represents the third increase in a row, and the highest value since June 2015, when the indicator stood at 18.4 points. There is currently a clear upward trend.

-

08:02

Germany: Gfk Consumer Confidence Survey, July 10.1 (forecast 9.8)

-

08:01

United Kingdom: Nationwide house price index , June 0.2% (forecast 0%)

-

08:01

United Kingdom: Nationwide house price index, y/y, June 5.1% (forecast 4.9%)

-

08:00

Switzerland: UBS Consumption Indicator, May 1.35

-

03:16

Australia: HIA New Home Sales, m/m, May -4.4%

-

01:50

Japan: Retail sales, y/y, May -1.9% (forecast -1.6%)

-

00:31

Currencies. Daily history for Jun 28’2016:

(pare/closed(GMT +3)/change, %)

EUR/USD $1,1077 +0,53%

GBP/USD $1,3328 +0,77%

USD/CHF Chf0,98 +0,26%

USD/JPY Y102,70 +0,77%

EUR/JPY Y113,77 +1,31%

GBP/JPY Y136,87 +1,55%

AUD/USD $0,7387 +0,66%

NZD/USD $0,7053 +0,82%

USD/CAD C$1,3025 -0,41%

-