Noticias del mercado

-

21:00

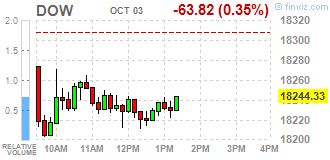

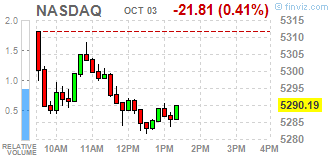

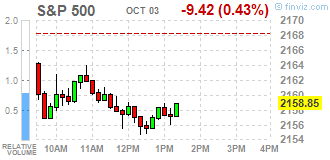

DJIA 18237.68 -70.47 -0.38%, NASDAQ 5289.79 -22.21 -0.42%, S&P 500 2158.13 -10.14 -0.47%

-

19:27

Wall Street. Major U.S. stock-indexes fell

Major U.S. stock-indexes started the fourth quarter on a weak note as healthcare stocks fell and Deutsche Bank's (DB) travails weighed on financials. The German lender is working to reach a settlement with U.S. authorities who have demanded a fine of up to $14 billion for mis-selling mortgage-baked securities.

Most of Dow stocks in negative area (24 of 30). Top gainer - E. I. du Pont de Nemours and Company (DD, +2.36%). Top loser - The Travelers Companies, Inc. (TRV, -1.53%).

All S&P sectors also in negative area. Top loser - Utilities (-1.0%).

At the moment:

Dow 18145.00 -74.00 -0.41%

S&P 500 2150.75 -9.75 -0.45%

Nasdaq 100 4849.50 -20.75 -0.43%

Oil 48.56 +0.32 +0.66%

Gold 1313.20 -3.90 -0.30%

U.S. 10yr 1.62 +0.01

-

18:00

European stocks closed: FTSE 6984.38 85.05 1.23%, DAX 10511.02 UNCH 0%, CAC 4452.99 4.73 0.11%

-

17:54

Oil little changed for the day

In today's trading, oil prices fluctuated, while investors assessed the OPEC agreement, which can interrupt the period of low oil prices.

Purchases from traders and investment managers received support due to hopes for a coordinated reduction in OPEC output to 32.5 - 33 million barrels per day. Such agreements reached by representatives of the cartel within the framework of an informal meeting in Algeria. Meanwhile, a number of market participants expect that the transaction should not be considered until the OPEC concluded.

The risk of disappointment in the OPEC agreement is great, believe Morgan Stanley, and it is unclear whether the cartel agreements aimed only at maintaining the trust of investors for an additional couple of months. The bank says that OPEC to conduct negotiations with Russia and other major oil producers outside the cartel.

Many analysts and traders expect OPEC transaction results, while the market is back under the control of one-day technical traders, said the broker.

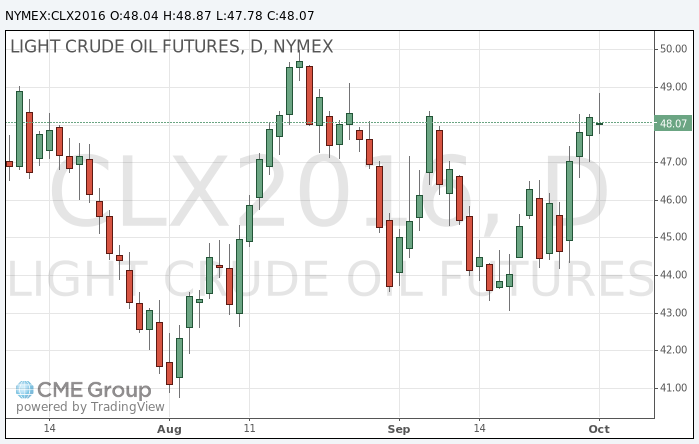

The cost of the November futures for US light crude oil WTI (Light Sweet Crude Oil) rose to 48.87 dollars per barrel on the New York Mercantile Exchange.

November futures price for North Sea petroleum mix of Brent crude rose to 50.90 dollars a barrel on the London Stock Exchange ICE Futures Europe.

-

17:37

WSE: Session Results

Polish equity market closed higher on Monday. The broad market measure, the WIG index, added 0.67%. Sector-wise, media (+1.40%) fared the best, while telecoms (-0.77%) fell the most.

The large-cap benchmark, the WIG30 Index, surged by 0.92%. Within the index components, clothing retailer LPP (WSE: LPP) led the gainers, skyrocketing by 14.12%, supported by the announcement the company's revenues boosted by 20% y/y to appr. PLN 457 mln in September, while its gross margin in the period edged up by 1 ppt y/y to 59%. YTD, LPP's sales increased by 17% y/y to PLN 4.16 bln. Other major advancers were railway freight transport operator PKP CARGO (WSE: PKP), footwear retailer CCC (WSE: CCC) and two banks PEKAO (WSE: PEO) and BZ WBK (WSE: BZW), climbing 9.21%, 3.47%, 2.83% and 2.59% respectively. On the other side of the ledger, IT-company ASSECO POLAND (WSE: ACP) topped the list of the decliners with a 2.17% drop, followed by two gencos TAURON PE (WSE: TPE) and ENERGA (WSE: ENG), falling by 1.92% and 1.33% respectively.

-

17:30

Gold trading lower

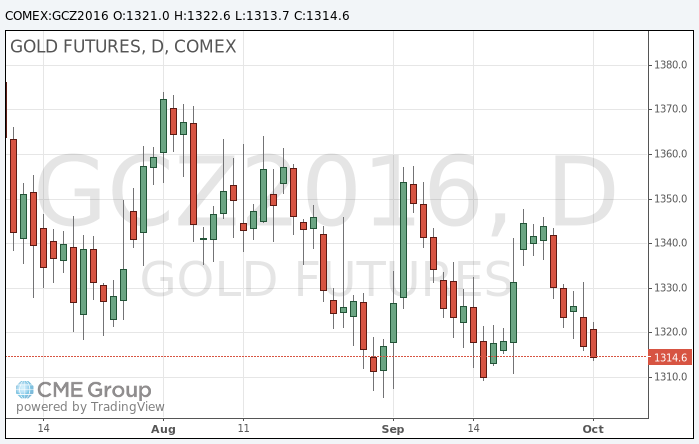

Gold fall today after stronger US data on business activity.

The US dollar rose after the manufacturing sector rebounded in September.

According to the report of the Institute for Supply Management (ISM), manufacturing PMI sector rose to 51.5 in September from 49.4 in August. Readings above 50 indicate expanding activity.

The manufacturing sector in recent years harmed the sluggish global economic growth and a strong US dollar.

"Positive news that the production index jumped after the fall, - says Brian Deyndzherfild, an analyst at RBS Securities -. Since September, the Fed signaled its intention to raise interest rates and the market, of course, will follow the economic data."

Earlier, gold prices were largely stable after the decision of the UK to triger article 50.

China's markets are closed from 1 to 9 October.

British Prime Minister Theresa May said on Sunday that the United Kingdom will start the process of exit from the EU no later than March next year, but it did not have any significant impact on the demand for gold.

Brexit calendar unlikely to have a direct impact on the gold price, says Julius Baer analyst, Carsten Menke.

Messages that Deutsche Bank is in talks with the US Justice Department to reduce the compensation designated for settlement of the dispute, also increased investors' appetite for risk.

Gold imports to India fell for the ninth straight month as weak retail demand and high prices have prompted banks and refining company to reduce foreign buying.

The cost of December futures for gold on the COMEX fell to $ 1313.7 per ounce.

-

16:27

-

16:02

US manufacturing ISM beats expectations

Economic activity in the manufacturing sector expanded in September following one month of contraction in August, and the overall economy grew for the 88th consecutive month, say the nation's supply executives in the latest Manufacturing ISM® Report On Business®.

The report was issued today by Bradley J. Holcomb, CPSM, CPSD, chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee. "The September PMI® registered 51.5 percent, an increase of 2.1 percentage points from the August reading of 49.4 percent. The New Orders Index registered 55.1 percent, an increase of 6 percentage points from the August reading of 49.1 percent. The Production Index registered 52.8 percent, 3.2 percentage points higher than the August reading of 49.6 percent. The Employment Index registered 49.7 percent, an increase of 1.4 percentage points from the August reading of 48.3 percent. Inventories of raw materials registered 49.5 percent, an increase of 0.5 percentage point from the August reading of 49 percent. The Prices Index registered 53 percent in September, the same reading as in August, indicating higher raw materials prices for the seventh consecutive month. Manufacturing expanded in September following one month of contraction in August, with nine of the 18 industries reporting an increase in new orders in September (up from six in August), and 10 of the 18 industries reporting an increase in production in September (up from eight in August)."

-

16:00

U.S.: Construction Spending, m/m, August -0.7% (forecast 0.2%)

-

16:00

U.S.: ISM Manufacturing, September 51.5 (forecast 50.3)

-

15:54

Canadian manufacturing PMI lower than forecast

Canadian manufacturers signalled another slowdown in growth momentum during September, with production volumes expanding at the weakest pace for seven months. The latest survey also pointed to a renewed decline in overall new business volumes, partly driven by a sharper drop in export sales. Subdued demand conditions contributed a slight fall in employment numbers and a greater degree of inventory drawdown in September.

At 50.3 in September, down from 51.1 in August, the Markit Canada Manufacturing Purchasing Managers' Index™ (PMI™) pointed to only a marginal improvement in overall business conditions and the slowest pace of recovery since the upturn began in March. Lower new order volumes and reduced payroll numbers were the main negative influences on the headline index, alongside the sharpest drop in pre-production inventories since the start of 2016.

-

15:53

WSE: After start on Wall Street

On the Warsaw market it is worth to note today's pretty good behavior of the banks sector led by Pekao and BZ WBK, which supports a market that is slowly climbing up the next levels. Nevertheless we have take an amendment to the level of the turnover, which is very far from ideal. On the plus side, however, need to be considered full use of the situation in the environment of emerging markets in our region. We managed to return slightly above the level of the Friday's opening and support for both the WIG20 and the WIG was defended.

The market in the United States opens from decrease of approx. 0.2%, which in the first few bars slightly growing. The red color on Wall Street is part of a slightly worse afternoon mood in Europe, where cosmetic discounts were implemented.

An hour before the end of the session the WIG20 index was at the level of 1,727 points (+1,04%).

-

15:52

U.S. manufacturers signalled another moderate upturn - Markit

U.S. manufacturers signalled another moderate upturn in both production volumes and incoming new work during September, but the latest survey indicated a further loss of growth momentum from July's recent peak. Softer overall growth was attributed to generally subdued client demand, alongside a drop in new export sales for the first time in four months.

At the same time, manufacturers sought to streamline their inventories of finished goods, with the pace of stock depletion the fastest since November 2015. The latest survey also pointed to cautious staff hiring strategies, although the rate of job creation picked up from August's recent low.

The seasonally adjusted final Markit U.S. Manufacturing Purchasing Managers' Index™ (PMI™) registered 51.5 in September (flash: 51.4), down slightly from 52.0 in August, to signal the weakest improvement in overall business conditions since June. Slower rates of output and new order growth were the main factors weighing on the headline index, which more than offset a stronger contribution from the staff hiring component.

-

15:45

U.S.: Manufacturing PMI, September 51.5 (forecast 51.4)

-

15:40

Option expiries for today's 10:00 ET NY cut

EURUSD: 1.1175 (EUR 251m) 1.1200 611m) 1.1280 (334m) 1.1325 (368m)

USDJPY: 100.00 (USD 486m) 100.90 (891m) 102.05-06 (1.34bln) 102.21 (540m) 102.30-35 (800m)

GBPUSD: 1.2975 (GBP 304m) 1.3100 (246m)

AUDUSD: 0.7600 (AUD 205m) 0.7640 (815m)

USDCAD: 1.3000 (USD 301m) 1.3075 (260m) 1.3095 (416m) 1.3100 (792m) 1.3200 (440m)

NZD/USD: 0.7332 (NZD 225m)

AUD/JPY: 78.00 (AUD 460m)

-

15:31

U.S. Stocks open: Dow -0.24%, Nasdaq -0.21%, S&P -0.22%

-

15:21

Before the bell: S&P futures -0.23%, NASDAQ futures -0.16%

U.S. stock-index futures slipped, following a rally Friday spurred by diminished concerns over the health of Deutsche Bank (DB), while investors awaited a reading on American manufacturing activity.

Global Stocks:

Nikkei 16,598.67 +148.83 +0.90%

Hang Seng 23,584.43 +287.28 +1.23%

Shanghai Closed

FTSE 6,978.50 +79.17 +1.15%

CAC 4,446.97 -1.29 -0.03%

DAX Closed

Crude $48.61 (+0.77%)

Gold $1319.60 (+0.19%)

-

14:53

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

10.15

0.01(0.0986%)

26466

Amazon.com Inc., NASDAQ

AMZN

836.45

-0.86(-0.1027%)

12513

Apple Inc.

AAPL

112.89

-0.16(-0.1415%)

85147

Barrick Gold Corporation, NYSE

ABX

17.77

0.05(0.2822%)

32187

Chevron Corp

CVX

102.93

0.01(0.0097%)

4418

Cisco Systems Inc

CSCO

31.56

0.10(0.3179%)

14821

Citigroup Inc., NYSE

C

47.19

-0.04(-0.0847%)

8719

E. I. du Pont de Nemours and Co

DD

67.9

0.93(1.3887%)

18470

Exxon Mobil Corp

XOM

87.55

0.27(0.3094%)

1129

Facebook, Inc.

FB

128.35

0.08(0.0624%)

41359

Ford Motor Co.

F

12.09

0.02(0.1657%)

36893

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

11.07

0.21(1.9337%)

62091

General Electric Co

GE

29.59

-0.03(-0.1013%)

54794

General Motors Company, NYSE

GM

31.75

-0.02(-0.063%)

354

Goldman Sachs

GS

161.05

-0.22(-0.1364%)

3222

Google Inc.

GOOG

776.95

-0.34(-0.0437%)

1143

Intel Corp

INTC

37.76

0.01(0.0265%)

14713

JPMorgan Chase and Co

JPM

66.51

-0.08(-0.1201%)

4600

McDonald's Corp

MCD

115.25

-0.11(-0.0954%)

17553

Nike

NKE

52.8

0.15(0.2849%)

7541

Procter & Gamble Co

PG

89.7

-0.05(-0.0557%)

4747

Tesla Motors, Inc., NASDAQ

TSLA

212.25

8.22(4.0288%)

102761

The Coca-Cola Co

KO

42.36

0.04(0.0945%)

641

Twitter, Inc., NYSE

TWTR

23.8

0.75(3.2538%)

598772

United Technologies Corp

UTX

101.75

0.15(0.1476%)

8629

Verizon Communications Inc

VZ

52.05

0.07(0.1347%)

20840

Walt Disney Co

DIS

92.81

-0.05(-0.0538%)

15368

Yahoo! Inc., NASDAQ

YHOO

43.18

0.08(0.1856%)

2295

Yandex N.V., NASDAQ

YNDX

21.44

0.39(1.8527%)

8687

-

14:51

Upgrades and downgrades before the market open

Upgrades:

Freeport-McMoRan (FCX) upgraded to Buy from Hold at Deutsche Bank

Barrick Gold (ABX) upgraded to Buy from Hold at Deutsche Bank

DuPont (DD) upgraded to Buy from Neutral at Citigroup

Downgrades:

Other:

Chevron (CVX) added to US Large Cap Fundamental List at BMO Capital

Apple (AAPL) maintained with an Overweight at Piper Jaffray; target $151

-

14:35

UK corporate taxes to be cut to 17% by end of parliament - Hammond

-

14:20

European session review: the British pound dropped significantly against the US dollar

The following data was published:

(Time / country / index / period / previous value / forecast)

6:00 Germany official holiday

7:15 Switzerland Retail Sales m / m in August 0.2%

07:15 Switzerland Retail sales, y / y in August -2.2%

Switzerland 7:30 PMI in the manufacturing sector in September 51 53.2

France 7:50 PMI in the manufacturing sector (the final data) September 48.3 49.5 49.7

Germany 7:55 PMI in the manufacturing sector (the final data) September 53.6 54.3 54.3

08:00 Eurozone PMI in the manufacturing sector (the final data) September 51.7 52.6 52.6

8:30 UK PMI Manufacturing Index September 53.3 52.1 55.4

The pound depreciated significantly against the US dollar, approaching July 6 low on comments by British Prime Minister on the Brexit process. However, a further currency collapse halted by extremely strong data on business activity in the manufacturing sector of the United Kingdom. Recall, in the weekend Theresa May said that the authorities intend to triger Article 50 of the Lisbon Treaty, providing for the country's right to withdraw from the EU until the end of March 2017. She stressed that Brexit is an "extremely difficult" process and the British authorities have to carry out lengthy negotiations with Brussels regarding the details of the country's exit from the union. The authorities plan to continue an active trade policy with the EU Member States.

Also today, financial minister Hammond warned that the UK economy will face turbulence, when the government will negotiate the exit from the EU. Hammond said he would like to see a deal with the EU, which included the full access of British companies to the EU's single market, while at the same time, the government listens to the call of the voters who need to regain control over the country's borders.

Markit Economics and CIBS showed that UK's manufacturing sector expanded in September at the fastest pace since mid-2014, helped by faster growth in output and new orders. As it became known, the index of manufacturing activity improved in September to 55.4 points compared to 53.4 points in August. The last reading was the highest since June 2014. Economists had expected the index to decline moderately to 52.1 points. "The rebound in the last two months has been encouragingly strong, and puts the sector on course, which will provide an additional positive contribution to GDP in the 3rd quarter," - said Rob Dobson, senior economist at Markit.

The euro traded in a range against the US dollar, while remaining near the opening level. However, little support has provided statistics for the euro area. The final data published byMarkit Economics showed that business activity in the euro zone's manufacturing sector accelerated last month, confirming preliminary estimates. The PMI for the manufacturing sector rose to 52.6 points compared with 51.7 points in the previous month. In addition, the report stated that the growth of production, new orders, new export orders and employment accelerated in September compared to August. "Today's PMI data indicate that the production, which grew at a steady pace in the second quarter (by about 2 per cent per annum), gained further momentum in September," - said Chris Williamson, chief economist at the business IHS Markit.

Among Member States, Germany and Austria recorded the fastest growth in September. Italy has returned to expansion, while France came close to stabilizing. German Manufacturing PMI rose to a three-month high, and amounted to 54.3 points compared to 53.6 points in August. The final readings correspond to the preliminary assessment. It is worth emphasizing the expansion of activity in the sector observed during the last 22 months. Meanwhile, the French manufacturing PMI improved to 49.7 from 48.3 in August. This is the highest score in the last seven months, and only slightly below the neutral mark of 50.0. The value was also higher than the preliminary assessment of 49.5.

EUR / USD: during the European session, the pair traded in a narrow range

GBP / USD: during the European session, the pair fell to $ 1.2844

USD / JPY: during the European session, the pair traded in a narrow range

-

13:50

Orders

EUR/USD

Offers 1.1250 1.1280 1.1300 1.1320 1.1350

Bids 1.1220 1.1200 1.1185 1.1150-60 1.1125-301.1100 1.1080 1.1050

GBP/USD

Offers 1.2875-80 1.2900 1.2930 1.2950 1.2980 1.3000

Bids 1.2820-1.2800 1.2785 1.2750 1.2730 1.2700

EUR/GBP

Offers 0.8750 0.8765 0.8780 0.8800

Bids 0.8720 0.8700 0.8685 0.8650 0.8620 0.8600

EUR/JPY

Offers 114.20 114.50 114.75-80 115.00 115.35 115.50 116.00

Bids 113.50 113.35 113.00 112.50 112.25 112.00 111.85 111.50 111.00

USD/JPY

Offers 101.80 102.00 102.20 102.50 102.80 103.00

Bids 101.00 101.85 100.70 100.50 100.25 100.00-05

AUD/USD

Offers 0.7680 0.7700 0.7720 0.7750 0.7800

Bids 0.7635-40 0.7600 0.7585 0.7565 0.7550 0.7530 0.7500

-

13:11

Major stock indices in Europe show a positive trend

European stocks traded in the green zone on the rise of energy companies and financial firms. Support for indices also provides statistics for the euro area and the United Kingdom.

The final data published by Markit Economics showed that business activity in the euro zone's manufacturing sector accelerated last month, confirming preliminary estimates. The PMI for the manufacturing sector rose to 52.6 points compared with 51.7 points in the previous month. In addition, the report stated that the growth of production, new orders, new export orders and employment accelerated in September compared to August. "Today's PMI data indicate that the production, which grew at a steady pace in the second quarter (by about 2 per cent per annum), gained further momentum in September," - said Chris Williamson, chief economist at the business IHS Markit.

A separate report from Markit Economics and CIBS showed that UK's manufacturing sector expanded in September at the fastest pace since mid-2014, helped by faster growth in output and new orders. As it became known, the index of manufacturing activity improved in September to 55.4 points compared to 53.4 points in August. The last reading was the highest since June 2014. Economists had expected the index to decline moderately to 52.1 points. "The rebound in the last two months has been encouragingly strong, and puts the sector on course, which will provide an additional positive contribution to GDP in the 3rd quarter," - said Rob Dobson, senior economist at Markit.

The composite index of the largest companies in the region Stoxx Europe 600 up 0.2 percent. The trading volume today is about 15 percent lower than the average for the last 30 days, as the German stock exchange is closed for a national holiday.

FTSE 100 index in Britain rose by more than 1.1 per cent, the best result among the Western European markets. Exporting companies benefited from a significant drop in the pound after UK Prime Minister Theresa May said it will triger article 50 at the end of March 2017.

Capitalization of Royal Dutch Shell Plc rose by 3 percent, supported by rising oil prices.

Shares of Henderson Group Plc rose 12 percent after the company announced a merger with the American Janus Capital Group Inc. As a result of this transaction, the Group will be established with assets of more than $ 320 billion and a total market capitalization of more than $ 6 billion.

At the moment:

FTSE 100 +80.78 6980.11 + 1.17%

DAX Closed

CAC 40 +13.62 4461.88 + 0.31%

-

13:03

WSE: Mid session comment

The first half of today's trading brought make up for an artificial auction in the segment of blue chips from Friday's closing. In the segment of small and medium-sized companies market behaves neutrally. There is not much better In the markets in Europe.

In the middle of today's trading the WIG20 index was at the level of 1,720 points (+ 0.64%). The turnover in the segment of the largest companies was amounted to PLN 150 million.

-

12:57

UK financial minister Hammond: No ifs, no buts, no second referendum, we are leaving the EU

-

Brexit process will be complex

-

We have the skills and ingenuity to make an exit a success

-

Brexit will need meticulous planning and steely determination

-

We are entering EU negotiations with the economy fundamentally robust

*via forexlive

-

-

11:37

Bank of England Sees Risks of 'Sharp Adjustment' in U.K.Commercial Real Estate

-

11:15

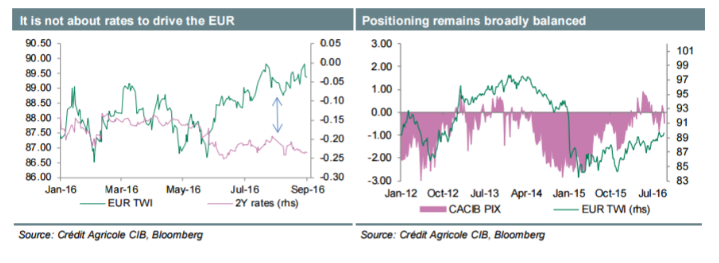

EUR: Stable This Week On Empty Calendar & Balanced Positioning - Credit Agricole

"Stabilising ECB rate expectations have been keeping the single currency broadly stable of late. Given an empty calendar when it comes to market moving data releases this is unlikely to change this week.

If anything there may be some focus on September PMI readings, which are likely to confirm moderately expanding business activity. However, considering it will be final readings, there is only limited surprise potential. In terms of speeches, ECB Governing Council Knot will be in focus. He is unlikely to make a case of changing monetary policy expectations. This in turn should leave the single currency driven by external factors such as global risk sentiment and Fed rate expectations.

Still, the main domestic risk may be related to the ongoing woes in the banking sector, including woes related to Deutsche Bank".

Copyright © 2016 Credit Agricole CIB, eFXnews™

-

11:01

Option expiries for today's 10:00 ET NY cut

EUR/USD: 1.1175 (EUR 251m) 1.1200 611m) 1.1280 (334m) 1.1325 (368m)

USD/JPY: 100.00 (USD 486m) 100.90 (891m) 102.05-06 (1.34bln) 102.21 (540m) 102.30-35 (800m)

GBP/USD: 1.2975 (GBP 304m) 1.3100 (246m)

AUD/USD: 0.7600 (AUD 205m) 0.7640 (815m)

USD/CAD: 1.3000 (USD 301m) 1.3075 (260m) 1.3095 (416m) 1.3100 (792m) 1.3200 (440m)

NZD/USD: 0.7332 (NZD 225m)

AUD/JPY: 78.00 (AUD 460m)

-

10:53

Oil trading lower at the start of the week

This morning, the New York futures for Brent have fallen by 0.35% to $ 48.08 and WTI down 0.14% to $ 50.12 per barrel. Thus, the black gold is traded in the red zone on a potential correction as OPEC agreement on joint action to stabilize the oil market still supports the prices. The cartel at an informal meeting in Algeria on Wednesday agreed on a production limit in the range of 32,5-33 million barrels of oil per day. The final decision will be taken at a meeting on November 30 in Vienna. Also, traders note statistics from the US oil service company Baker Hughes. At the end of last week the number of drilling rigs increased by 11 units, or 2.15%, to 522 units. The annualized rate decreased to 287 units or 35.4%. The amount of oil rigs increased by 7 units, or 1.67%, up to 425 pieces.

-

10:37

UK manufacturing PMI better than forecast. Can it support the pound?

Conditions in the UK manufacturing sector continued to improve at the end of the third quarter. Rates of expansion in output and new orders accelerated further, rising at rates rarely achieved since the middle of 2014. The domestic market remained a prime driver of new business wins, while the weaker sterling exchange rate drove up new orders from abroad.

At 55.4 in September, up from 53.4 in August, the seasonally adjusted Markit/CIPS Purchasing Managers' Index® (PMI® ) rose to its highest level since June 2014. Furthermore, the rebound in the PMI level since its EU-referendum related low in July has been sufficient to make the third quarter average (52.3) the best during the year-to-date.

September saw manufacturing production expand at the quickest pace since May 2014. Growth was led by the consumer goods sector, where output rose at the quickest pace in one-and-a-half years. There were also substantial and accelerated increases at intermediate (11-month high) and investment (eight-month high) goods producers.

-

10:30

United Kingdom: Purchasing Manager Index Manufacturing , September 55.4 (forecast 52.1)

-

10:00

Eurozone: Manufacturing PMI, September 52.6 (forecast 52.6)

-

09:57

German mafacturing activity stable compared to last month

September data signalled ongoing growth of German manufacturing, with the rate of improvement in the sector reaching a three-month high. This was highlighted by the final seasonally adjusted Markit/BME Germany Manufacturing Purchasing Managers' Index® (PMI® ) - a singlefigure snapshot of the performance of the manufacturing economy - rising from August's 53.6 to 54.3. The PMI has signalled growth in each of the past 22 months.

In response to rising demand, manufacturers scaled up their production volumes in September. The rate of increase was unchanged from August and solid overall. Survey data signalled that output expanded at consumer, intermediate and investment goods producers.

Some companies used existing stock in order to satisfy higher demand. This was signalled by a reduction in post-production inventories. Moreover, the rate at which stocks of finished goods fell was the most marked in over six-and-a-half years.

-

09:55

Germany: Manufacturing PMI, September 54.3 (forecast 54.3)

-

09:50

September saw an improved performance among Italy’s manufacturers - Markit

September saw an improved performance among Italy's manufacturers, although the overall picture remained one of only modest growth. Output rose at a slightly quicker rate than in August as new orders returned to expansion, led by a stronger increase in new business from abroad. The pace of job creation also quickened, though remained only moderate overall. Elsewhere, input price inflation was at a 14-month high but still muted by historical standards.

The headline Markit Italy Manufacturing Purchasing Managers' Index® (PMI® ) - a single-figure measure of developments in overall business conditions - moved to 51.0 September, improving on August's 49.8, which was the first sub-50 reading in over one-and-a-half years.

-

09:50

France: Manufacturing PMI, September 49.7 (forecast 49.5)

-

09:47

Major stock exchanges trading in the green zone: FTSE 100 6,930.88 +31.55 + 0.46%, Xetra DAX 10,511.02 +105.48 + 1.01%

-

09:34

September saw growth momentum in the Spanish manufacturing sector - Markit

September saw growth momentum in the Spanish manufacturing sector recover somewhat as output, new orders and employment all rose at sharper rates than in August. Firms continued to display a preference for stock reduction, however. On the price front, the rate of cost inflation picked up but competitive pressures meant that output prices were reduced marginally.

The PMI rose to 52.3 in September, up from 51.0 in August and the highest since April. The reading signalled a solid monthly improvement in the health of the sector. Business conditions have now strengthened in each of the past 34 months.

-

09:30

Switzerland: Manufacturing PMI, September 53.2

-

09:14

Sterling Falls to 7-Week Low of 0.8720 Per Euro

-

09:13

WSE: After opening

WIG20 index opened at 1713.16 points (+0.21%)*

WIG 47169.38 0.18%

WIG30 1982.01 0.28%

mWIG40 4029.85 -0.01%

*/ - change to previous close

The cash market started a new month with increase of 0.22% to 1,713 points, at usual Monday's modest turnover. The PMI index for the domestic industry was slightly better than forecasts and increased to 52.2 points from 51.5 points previously. The environment is quiet and the CAC40 lost 0.1%, so this behavior is slightly worse than might have been expected early in the morning.

-

08:45

Get Ready For Another Big Slide In Cable: Where To Target - CIBC

"Despite the fact that economic indicators have shown less of a slowdown than had been expected, the post-Brexit vote environment hasn't been particularly positive for sterling. The recent short-covering rally in sterling ran out of steam just shy of 1.35, with the currency retreating thereafter. With some of the more pessimistic forecasts calling for an outright recession in 2017, investors are still wary of the spectre of additional policy stimulus from the Bank of England. Despite criticism from a number of politicians, Governor Carney could still ease policy further should data disappoint.

As time has progressed, the likelihood of a so-called 'hard-Brexit' has increased. That situation would involve giving up single market access for control over immigration. While the Bank of England can't offset the long-term growth implications of such a scenario, it is increasing the chances that the MPC decides to take rates down to its effective lower bound of 0.10% in the coming months.

Markets are currently pricing in only a 25% chance of rate cut by year-end, leaving room for another cut to depress the currency. With the Chancellor giving a fiscal update on November 23rd, the precise timing of an interest rate cut is difficult to pin down. But whether the central bank eases ahead of that November fiscal update or waits until December, either outcome would see sterling weakening in the coming months".

CIBC targets GBP/USD at 1.25 by year-end.

Copyright © 2016 CIBC, eFXnews™

-

08:43

Positive start of trading expected on the major stock exchanges in Europe: CAC40 futures flat, FTSE + 0.2%

-

08:42

Asian session review: the yen little changed

The yen was trading subdued amid statistics published today. As it became known, the Tankan large manufacturers index, published by the Bank of Japan, and reflecting general business conditions for large Japanese manufacturing companies amounted to 6, which coincided with the value in the first quarter, but was lower than economists' forecast of 7. Tankan services sector fell to 18 from the previous value of 19. This index is an indicator of the growth of domestic demand and the health of non-tradable sector. Also,the all industries index grew by 6.3%, which is higher than the previous value of 6.2%, but below economists' forecast of 6.8%.

The pound has dropped significantly since the beginning of the session, after the British prime minister Theresa May said that Britain will begin the process of exit from the European Union no later than March 2017. The Prime Minister said that the exit from the EU is quite complex, and expressed the need to begin preparatory work with the remaining countries in the EU, so that when the time comes, the negotiation process will be smoother. "This is important not only for the UK, it is important for the whole of Europe, so we made the best of it, with the least problems for business", - she said.

In addition, this week, traders will be waiting for official data on the UK's service sector, industrial production and production in the manufacturing industry, which will be released on Friday. Economists polled by Wall Street Journal, expected that production in the manufacturing industry of Great Britain grew by 0.5% in August, after unchanged in July.

EUR / USD: during the Asian session, the pair was trading in the $ 1.1225-40 range

GBP / USD: during the Asian session the pair fell to $ 1.2920

USD / JPY: during the Asian session, the pair was trading in the Y101.20-65 range

-

08:34

Moody's: Japan policy stimulus will support growth, medium-term challenges remain

Moody's Japan K.K. has released its latest issue of Inside Japan, which says that persistent low economic growth and inflation in Japan (A1 stable) has prompted a shift toward greater monetary and fiscal accommodation, and led the rating agency to raise its forecasts for real GDP growth to 0.7% this year and 0.9% in 2017, following a 0.5% increase in 2015.

Moody's says the delay in the consumption tax hike and the implementation of additional fiscal stimulus, alongside the Bank of Japan's new monetary framework unveiled on 21 September, are the latest policy measures aimed at reviving economic growth and inflation, while providing room for structural reforms, such as increasing labor force participation.

But the positive impact of these structural reforms will be set against intensifying pressures on growth and fiscal expenditure from an aging population.

In the absence of a marked boost to growth from structural reform, we estimate that Japan's already high debt burden will further edge up over the next decade.

Moody's conclusions are contained in the latest edition of its "Inside Japan" publication. Moody's bi-annual compendium includes recent key research and commentaries published, as well as a list of recent rating actions across all sectors in Japan.

Moody's report also includes the press release on its affirmation of Japan's A1 sovereign rating on 30 August, which reflected (1) the slow but continuing progress in developing a policy and reform framework which could ultimately reflate the Japanese economy and reverse the rise in government debt and (2) its expectation that funding costs for the government will remain low and stable.

In addition to the sovereign update, Moody's compendium aggregates a selection of recently published sovereign, corporate finance, financial institution and structured finance key research pieces.

-

08:32

Former Bank of Japan board member, Nobiyuki Nakahara: the control of bond yields is a mistake

Today, a former BoJ's board member and part-time assistant to Prime Minister Abe, Mr. Nakahara Nobiyuki stated his disagreement with the changes made at the last meeting of the Bank of Japan. The official spoke out against the fact that the central element of the easing policy was to control bond yields.

-

08:28

German minister accuses Deutsche Bank of making speculation its business - Reuters

-

08:27

WSE: Before opening

Today we begin another month and quarter in the markets. The beginning of the month means the readings of PMI and ISM in the United States, which is the most important macroeconomic publication of the day.

The markets attention, however, will focus on information relating to Deutsche Bank. On Friday, late in the evening, there were reports that the US Justice Department is negotiating with the bank decrease previously proposed penalty of up to US $ 5.4 billion from the original $ 14 billion. In response the DB shares gained 14% in United States. This information also influenced the positive sentiment on Wall Street, where major indexes rose after approx. 0.8%.

Today, because of the holidays the Frankfurt Stock Exchange will be closed, so we have to wait until tomorrow to find out the sentiment to the DB in home country.

In turn, in Asia the whole week will celebrate the Chinese, but on the weekend there were official PMI data for both the service and industry sectors, which have been well received by investors. Asian markets are dominated by noticeable increases. Also grow contracts in the United States, so in Europe, at the beginning we may expect the dominance of the green color.

On the Warsaw market another "miracle fixing" on Friday this time understated quoting, so some decline on Friday was somewhat artificial and may be made up for today.

-

08:23

Australian manufacturing stabilises in September

-

After a sharp drop in August, the Australian Industry Group Australian Performance of Manufacturing Index (Australian PMI® ) increased by 2.9 points to a broadly stable 49.8 points in September (results below 50 indicate contraction, the distance from 50 points indicates the strength of contraction).

-

The stabilisation in the Australian PMI® in September was heavily influenced by activity in the food & beverages sub-sector which recovered after contracting in August. This key sector (now contributing around 28% of all manufacturing output) appears to have addressed the factors that drove a contraction in production and sales in August.

-

Three of the seven activity sub-indexes in the Australian PMI® expanded in September after contracting in August. Production (52.6 points), deliveries (56.4 points) and sales (51.4 points) expanded and exports stabilised (50.0 points). Employment (46.7 points) and stocks (44.3 points) contracted again. New orders slipped into contraction (48.3 points).

-

-

08:20

UK to trigger Article 50 by end-March 2017. GBP/USD gaps down after opening. Sell the rumors, buy the facts?

-

08:16

Japan's manufacturing activity expanded for the first time in seven months

According to rttnews, Japan's factory activity expanded for the first time in seven months in September, though marginally, survey figures from Markit Economics showed Monday.

The Nikkei Manufacturing Purchasing Managers' Index rose to 50.4 in September from 49.5 in August. Any reading above 50 indicates expansion in the sector, while a score below 50 suggests contraction.

Output grew for the second consecutive month in September, while new orders declined at a slower pace. As a result, firms raised their staffing levels during the month, with the rate of job creation picking up slightly.

On the price front, both input and output prices decreased further in September.

-

07:09

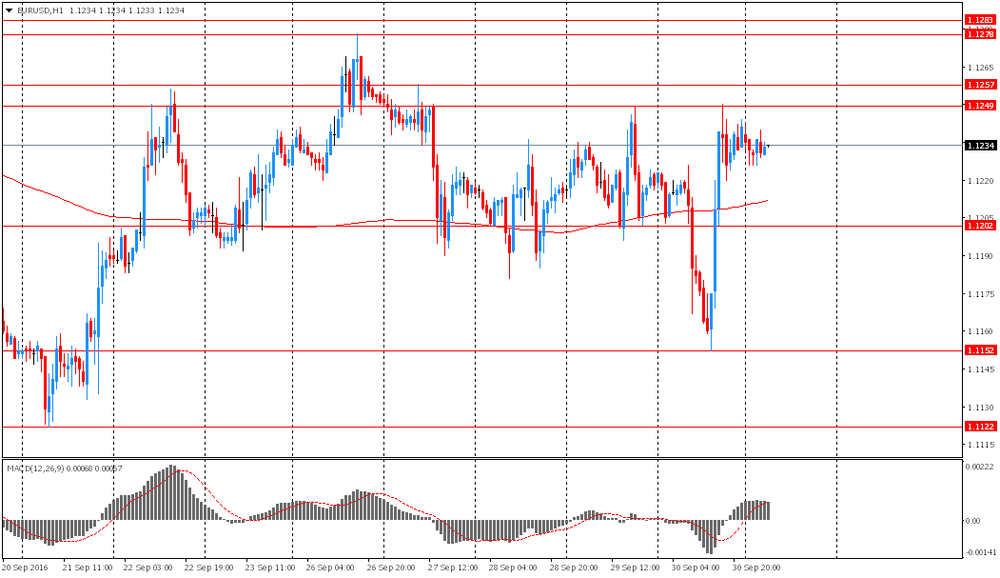

Options levels on monday, October 3, 2016:

EUR/USD

Resistance levels (open interest**, contracts)

$1.1367 (4464)

$1.1334 (3055)

$1.1287 (1020)

Price at time of writing this review: $1.1234

Support levels (open interest**, contracts):

$1.1181 (3907)

$1.1140 (4461)

$1.1094 (5082)

Comments:

- Overall open interest on the CALL options with the expiration date October, 7 is 38847 contracts, with the maximum number of contracts with strike price $1,1500 (6175);

- Overall open interest on the PUT options with the expiration date October, 7 is 39189 contracts, with the maximum number of contracts with strike price $1,1100 (5082);

- The ratio of PUT/CALL was 1.01 versus 1.03 from the previous trading day according to data from September, 30

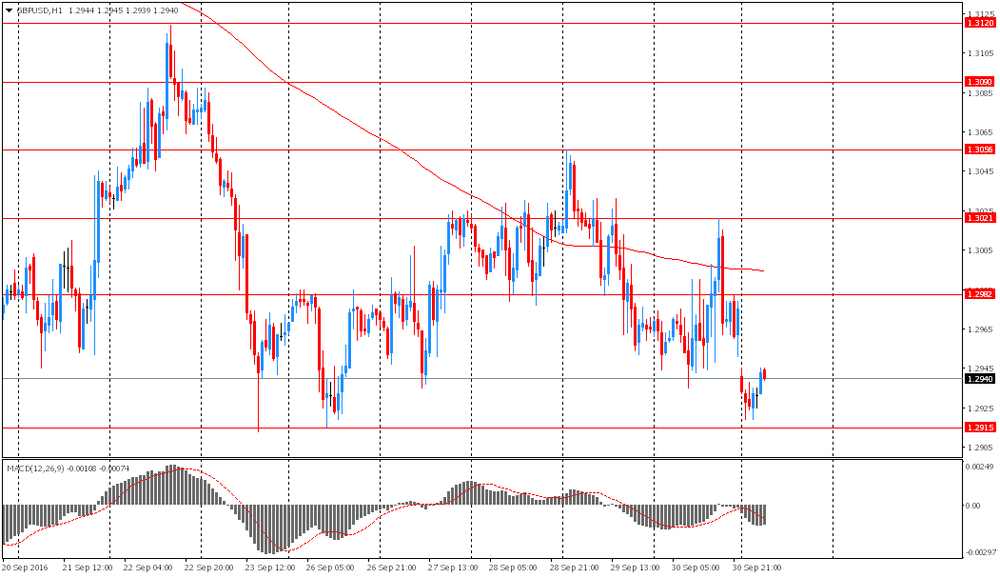

GBP/USD

Resistance levels (open interest**, contracts)

$1.3201 (1441)

$1.3103 (1458)

$1.3006 (801)

Price at time of writing this review: $1.2939

Support levels (open interest**, contracts):

$1.2897 (1410)

$1.2799 (1731)

$1.2700 (1425)

Comments:

- Overall open interest on the CALL options with the expiration date October, 7 is 27990 contracts, with the maximum number of contracts with strike price $1,3500 (3374);

- Overall open interest on the PUT options with the expiration date October, 7 is 22994 contracts, with the maximum number of contracts with strike price $1,3000 (3363);

- The ratio of PUT/CALL was 0.82 versus 0.84 from the previous trading day according to data from September, 30

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

07:07

Global Stocks

European stock markets on Friday erased earlier sharp losses and closed slightly higher as concerns over Deutsche Bank's financial health subsided on hopes the lender will pay a lower-than-feared fine to U.S. regulators.

U.S. stocks closed higher Friday, but off their session highs, boosted by a double-digit rally in Deutsche Bank AG shares, which were recovering from brutal losses in the previous session amid heightened concerns about the health of the German lender's balance sheet.

Asian shares got the new quarter off to a firm start on Monday, while sterling tumbled as Britain set a March deadline to start divorce proceedings from the European Union. Risk sentiment had benefited on Friday from reports Deutsche Bank was negotiating a much smaller fine with the U.S. Department of Justice, though the Wall Street Journal reported on Sunday that the talks were still in flux.

-

02:30

Japan: Manufacturing PMI, September 50.4 (forecast 50.3)

-

01:50

Japan: BoJ Tankan. Non-Manufacturing Index, Quarter III 18 (forecast 18)

-

01:50

Japan: BoJ Tankan. Manufacturing Index, Quarter III 6 (forecast 7)

-

01:02

Commodities. Daily history for Sep 30’2016:

(raw materials / closing price /% change)

Oil 48.05 -0.39%

Gold 1,318.80 +0.13%

-

01:01

Stocks. Daily history for Sep 30’2016:

(index / closing price / change items /% change)

Nikkei 225 16,449.84 -243.87 -1.46%

Shanghai Composite 3,005.51 +7.03 +0.23%

S&P/ASX 200 5,435.92 -35.34 -0.65%

FTSE 100 6,899.33 -20.09 -0.29%

CAC 40 4,448.26 +4.42 +0.10%

Xetra DAX 10,511.02 +105.48 +1.01%

S&P 500 2,168.27 +17.14 +0.80%

Dow Jones Industrial Average 18,308.15 +164.70 +0.91%

S&P/TSX Composite 14,725.86 -28.69 -0.19%

-

00:59

Currencies. Daily history for Sep 30’2016:

(pare/closed(GMT +3)/change, %)

EUR/USD $1,1210 -0,28%

GBP/USD $1,2842 -1,04%

USD/CHF Chf0,9734 +0,22%

USD/JPY Y101,63 +0,30%

EUR/JPY Y113,94 +0,03%

GBP/JPY Y130,5 -0,75%

AUD/USD $0,7676 +0,23%

NZD/USD $0,7274 -0,12%

USD/CAD C$1,3115 -0,09%

-

00:30

Australia: AIG Manufacturing Index, September 49.8

-

00:04

Schedule for today,Monday, Oct 03’2016

00:30 Japan Manufacturing PMI (Finally) September 49.5 50.3

07:15 Switzerland Retail Sales (MoM) August 0.2%

07:15 Switzerland Retail Sales Y/Y August -2.2%

07:30 Switzerland Manufacturing PMI September 51

07:50 France Manufacturing PMI (Finally) September 48.3 49.5

07:55 Germany Manufacturing PMI (Finally) September 53.6 54.3

08:00 Eurozone Manufacturing PMI (Finally) September 51.7 52.6

08:30 United Kingdom Purchasing Manager Index Manufacturing September 53.3 52.1

13:45 U.S. Manufacturing PMI (Finally) September 52 51.4

14:00 U.S. Construction Spending, m/m August 0% 0.2%

14:00 U.S. ISM Manufacturing September 49.4 50.3

20:00 U.S. Total Vehicle Sales, mln September 16.98 17.3

-