Noticias del mercado

-

23:59

Schedule for today, Tuesday, Sep 15’2015:

(time / country / index / period / previous value / forecast)

01:30 Australia New Motor Vehicle Sales (MoM) August -1.3%

01:30 Australia New Motor Vehicle Sales (YoY) August 3.7%

01:30 Australia RBA Meeting's Minutes

03:00 Japan BoJ Interest Rate Decision 0%

03:00 Japan Bank of Japan Monetary Base Target 275

03:00 Japan BoJ Monetary Policy Statement

06:30 Japan BOJ Press Conference

06:45 France CPI, m/m August -0.4%

06:45 France CPI, y/y August 0.2%

08:30 United Kingdom Producer Price Index - Input (MoM) August -0.9% -2.4%

08:30 United Kingdom Producer Price Index - Input (YoY) August -12.4% -13.7%

08:30 United Kingdom Producer Price Index - Output (MoM) August -0.1% -0.2%

08:30 United Kingdom Producer Price Index - Output (YoY) August -1.6% -1.7%

08:30 United Kingdom Retail Price Index, m/m August -0.1% 0.3%

08:30 United Kingdom Retail prices, Y/Y August 1% 0.9%

08:30 United Kingdom HICP, m/m August -0.2% 0.2%

08:30 United Kingdom HICP, Y/Y August 0.1% 0.0%

08:30 United Kingdom HICP ex EFAT, Y/Y August 1.2%

09:00 Eurozone Employment Change Quarter II 0.1%

09:00 Eurozone Trade balance unadjusted July 26.4

09:00 Eurozone ZEW Economic Sentiment September 47.6

09:00 Germany ZEW Survey - Economic Sentiment September 25 18.5

12:30 U.S. NY Fed Empire State manufacturing index September -14.92 -2

12:30 U.S. Retail sales August 0.6% 0.4%

12:30 U.S. Retail sales excluding auto September 0.4% 0.2%

13:15 U.S. Capacity Utilization August 78% 77.8%

13:15 U.S. Industrial Production (MoM) August 0.6% -0.1%

13:15 U.S. Industrial Production YoY August 1.3%

14:00 U.S. Business inventories July 0.8% 0.1%

20:30 U.S. API Crude Oil Inventories September 2.1

22:45 New Zealand Current Account Quarter II 660 -1500

23:30 Australia RBA Assist Gov Debelle Speaks

-

22:15

U.S. stocks declined

U.S. stocks declined, following equities' best week since July, before the Federal Reserve decides on Thursday whether the economy and turbulent financial markets can handle higher interest rates.

The Standard & Poor's 500 Index slipped 0.4 percent to 1,953.02 at 4 p.m. in New York, after the gauge rose 2.1 percent last week. Trading in S&P 500 companies was about 26 percent below the 30-day average for this time of day amid the Jewish new-year holiday.

"I think today we're seeing that tug-of-war in the market again, and nothing is going to matter until we know what the Fed's going to do," said Michael Gayed, the chief investment strategist who helps to manage $200 million at Pension Partners LLC in New York. "I think it's going to be a fun week."

Investors remain confident the Fed will raise borrowing costs this year, even as most bet the central bank will not increase rates at its Sept. 16-17 meeting. Traders are pricing in a 26 percent chance of action on Thursday, down from 48 percent before China's currency devaluation last month. Odds of a move at the December gathering are about 59 percent, according to data compiled by Bloomberg.

Words from Fed Vice Chairman Stanley Fischer in 2014 offer some support for those expecting a move on rates this week. Just months before taking over as the Fed's No.2 official last year, he said that delaying increases carried its own difficulties and the situation is always unclear and monetary policy takes time to affect the economy. "Don't overestimate the benefits of waiting for the situation to clarify," he said.

Chinese stocks slumped the most in three weeks after data added to concern that the country's economic slowdown is deepening. Industrial output missed economists' forecasts, while investment in the first eight months increased at the slowest pace since 2000.

Market swings and rapid shifts in investor sentiment have become more prevalent as uncertainty on the impact of China's slowdown coupled with the Fed's looming rate decision to whipsaw equities. For the ninth time in a row, the S&P 500 posted a weekly return that amounted to a reversal of the prior week's performance. Such a streak of alternating gains and losses has happened only three times in 20 years, according to data.

-

21:00

DJIA 16372.66 -60.43 -0.37%, NASDAQ 4807.06 -15.28 -0.32%, S&P 500 1953.10 -7.95 -0.41%

-

20:16

American focus: the US dollar rose

The US dollar showed gains against major currencies in thin trade as investors have focused on the upcoming Thursday statement, the Federal Reserve's monetary policy. Sentiment on the dollar remained fragile amid fears that the US mixed economic reports and instability in global financial markets will force the US central bank to revise the terms of rise in interest rates this Thursday.

On Friday, data showed that the consumer confidence index from the University of Michigan fell to 85.7 from 91.9 in July, compared with forecasts of a decline to 91.2. Also, the US Labor Department reported that producer price index was unchanged last month after rising in July by 0.2%.

The Fed chief Yellen stated that increasing interest rates depends on the economic indicators, however, it also pointed out that the bank plans to raise interest rates before the end of this year.

Little support for the euro earlier had data on industrial production in the eurozone. Statistical Office Eurostat said that the seasonally adjusted volume of industrial production in the eurozone rose in July by 0.6%, offsetting a decline of 0.3% in June (revised from -0.4%). Experts expect that figure to grow by 0.3%. Meanwhile, industrial production in the EU rose by 0.3% after falling 0.1% the previous month. In annual terms, industrial production increased by 1.9% in euro area and by 1.8% among the 28 EU countries. The Eurostat also reported that the monthly change in the euro area was due to the increase in electricity production (3.0%), capital goods (1.4%) and consumer durables (1.3%). Meanwhile, production of intermediate goods and consumer non-durable goods fell by 0.6%.

The Swiss franc depreciated slightly against the US dollar, breaking the mark of CHF0.9700, which was caused by the publication of weak data on Switzerland. Report submitted by the Federal Statistical Office showed that producer prices and import prices declined substantially at the end of August, when fixing the maximum rate of more than six decades. According to the data, the index of producer prices and imports fell in August by 6.8 percent per annum, after falling 6.4 percent in July. It was the largest drop since April 1950, when this figure fell to 7.1 per cent. It should also be noted, the index shows a continuous drop since October 2013. In monthly terms, the producer price index and import recorded its fifth consecutive monthly decline. At the end of August the index dropped by 0.7 percent (the maximum rate for the three months). Recall that in July, a decline of 0.3 percent.

Meanwhile, another report showed that retail sales (seasonally adjusted) fell in July by 0.6 percent compared with 1.4 percent the previous month. In annual terms, sales decreased by 0.1 percent after falling 0.9 percent in June. Retail sales of food, beverages and tobacco increased by 0.7 percent, while sales in the non-food sector rose by 0.3 percent. Excluding fuel, sales (seasonally adjusted) fell by 0.4 percent compared to June.

The pound fell against the dollar and reached $ 1.5370. Investors turn their attention to tomorrow's report on inflation in Britain, which may affect the prospects for changes in interest rates of the Central Bank. Little influenced by the statement made by the Bank of England Martin Huila. He noted that interest rates in the UK should be raised "relatively soon" in order to achieve the inflation target over the medium term. "Solid growth in wages and improvement in the labor market is likely to help boost inflation to the target level in the next two or three years - said Wil. - Monetary policy should be adapted to such conditions. As a result, it seems likely that the banking the rate will need to raise in a relatively short time. " He will also noted that cheap oil has become one of the driving factors of reducing inflation in recent months, and added that such shocks could last for some time. However, he said that, in future, there is good reason to expect a return of inflation to the target value on the background of strong wage growth and the introduction of new national subsistence minimum.

-

18:48

Wall Street. Major U.S. stock-indexes fell

Major U.S. stock-indexes fell in morning trading on Monday as investors awaited Federal Reserve's interest rate meeting this week even as fears of slowing growth in China continue to rattle global markets. Stocks are expected to remain volatile in the run-up to the policy meeting on Wednesday and Thursday, when the Fed is expected to decide on its first interest rate increase since 2006. Data on Monday showed that growth in China's investment and factory output in August missed forecasts, raising the chances that China's third-quarter economic growth may dip below 7% for the first time since the global crisis.

Most of Dow stocks in negative area (26 of 30). Top looser - Visa Inc. (V, -1.45%). Top gainer - Apple Inc. (AAPL, +0.78).

Almost all S&P index sectors in negative area. Top looser - Conglomerates (-0.9%). Top gainer - Utilities (+0,1%).

At the moment:

Dow 16262.00 -75.00 -0.46%

S&P 500 1941.25 -9.00 -0.46%

Nasdaq 100 4293.50 -21.75 -0.50%

10 Year yield 2,18% -0,01

Oil 43.87 -0.76 -1.70%

Gold 1108.30 +5.00 +0.45%

-

18:38

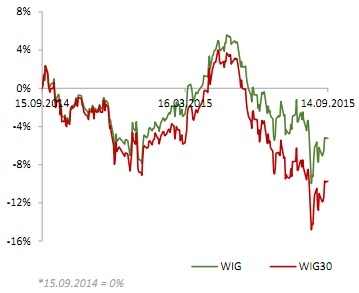

WSE: Session Results

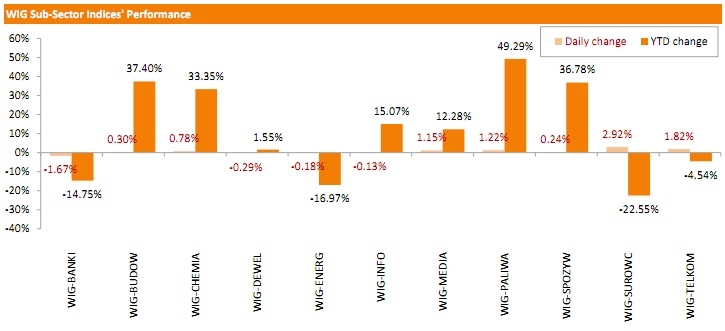

Polish equity market closed flat on Monday. The broad market measure, the WIG Index, slid down 0.07%. Sector-wise, materials (+2.92%) outperformed, while banking sector (-1.67%) lagged behind.

The large-cap stocks' measure, the WIG30 Index, edged up 0.08%. BOGDANKA (WSE: LWB) was the standout performer in the WIG30 Index basket, skyrocketing by 24.12% on media report that ENEA (WSE: ENA; +1.21%) offered PLN 1.48 bln (USD 398mln) for a 64.6-stake in the company. This implied a share price of PLN 67.39, or nearly 29% above LWB's Friday close. Other notable gainers were JSW (WSE: JSW), KERNEL (WSE: KER) and HANDLOWY (WSE: BHW), returning 6.45%, 2.03% and 2.02% respectively. On the other side of the ledger, banking names PEKAO (WSE: PEO), PKO BP (WSE: PKO), ING BSK (WSE: ING) and BZ WBK (WSE: BZW) were hit the hardest, tumbling 1.28-3.28% on speculations regarding the conversion of CHF-denominated loans. They were followed by PGE (WSE: PGE) and GTC (WSE: GTC), losing 1.17% and 1.04% respectively.

-

18:00

European stocks close: stocks closed mixed as market participants were cautious ahead of the Fed’s interest rate decision this week

Stock indices closed mixed as market participants were cautious ahead of the Fed's interest rate decision this week.

Meanwhile, the economic data from the Eurozone was better than expected. Eurostat released its industrial production data for the Eurozone on Monday. Industrial production in the Eurozone rose 0.6% in July, exceeding expectations for a 0.3% increase, after a 0.3% drop in June. June's figure was revised up from a 0.4%.

The increase was driven by a rise in energy, durable consumer goods and capital output. Energy output climbed 3.0% in July, durable consumer goods were up 1.3%, while capital goods output rose by 1.4%.

Intermediate goods declined by 0.6% in July, while non-durable consumer goods output fell 0.6%.

On a yearly basis, Eurozone's industrial production gained 1.9% in July, exceeding expectations for a 0.6% rise, after a 1.5% increase in June.

The increase was driven by a rise in durable consumer goods, capital goods and energy output. Durable consumer goods climbed by 2.6% in July from a year ago, capital goods rose by 2.2%, while energy output gained by 5.1%.

Non-durable consumer goods were up by 1.7%, while intermediate output was up by 0.5%.

Indexes on the close:

Name Price Change Change %

FTSE 100 6,084.59 -33.17 -0.54 %

DAX 10,131.74 +8.18 +0.08 %

CAC 40 4,518.15 -30.57 -0.67 %

-

18:00

European stocks closed: FTSE 6084.59 -33.17 -0.54%, DAX 10131.74 8.18 0.08%, CAC 40 4518.15 -30.57 -0.67%

-

17:40

Oil prices decline on concerns over the global oil oversupply

Oil prices declined on concerns over the global oil oversupply. The Organization of the Petroleum Exporting Countries (OPEC) released its monthly report on Monday. OPEC said that its oil production was 31.54 million barrels a day of crude in August, higher than in July. The target is 30 million barrels a day.

OPEC expects the oil demand for its crude to be average 30.31 million barrels per day (bpd) next year, up 190,000 bpd from last month.

OPEC expects that non-OPEC members will rise their output by 160,000 bpd next year, down 110,000 bpd from last month, while U.S. shale oil production was downgraded by 100,000 bpd.

Global oil demand growth is expected to be 1.29 million bpd in 2016, down 50,000 bpd from last month.

The oil driller Baker Hughes reported on Friday that the number of active U.S. rigs declined by 10 rigs to 652 last week. It was the second consecutive decrease.

Combined oil and gas rigs fell by 16 to 848.

Earlier last week, Baker Hughes said that the average total rig count declined by 17 to 883 in August from July.

WTI crude oil for October delivery fell to $43.81 a barrel on the New York Mercantile Exchange.

Brent crude oil for October declined to $47.13 a barrel on ICE Futures Europe.

-

17:22

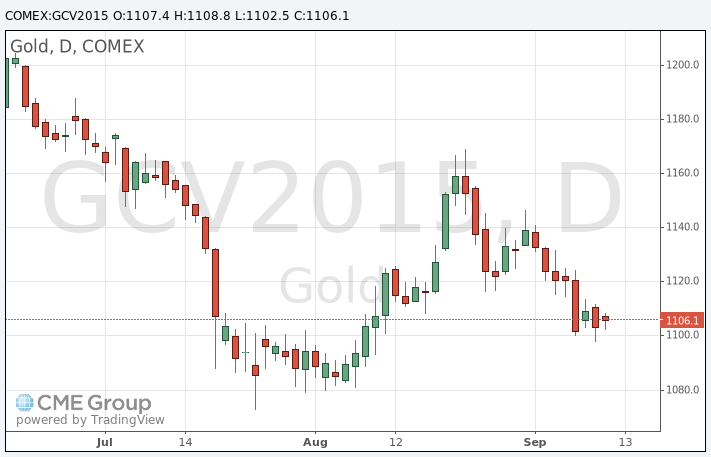

Gold price declines slightly

Gold price fell on the uncertainty over the Fed's interest rate hike continue to weigh on gold. It remains unclear if the Fed will start raising its interest rate in September or not.

The U.S. economic data was mixed in the recent weeks. The labour market continued to strengthen, while the inflation and wage growth remained low.

Gold is traded in U.S. dollars. It suffers when the U.S. dollar strengthens, becoming more expensive for holders of other currencies.

October futures for gold on the COMEX today fell to 1102.50 dollars per ounce.

-

17:03

European Central Bank Governing Council member Josef Bonnici: it will take time to see a full impact of the central bank’s asset buying programme

The European Central Bank Governing Council member Josef Bonnici said on Monday that it will take time to see a full impact of the central bank's asset buying programme. He added that it too early to decide on further stimulus measures.

-

16:58

Final industrial production in Japan declines 0.8% in July

Japan's Ministry of Economy, Trade and Industry released its final industrial production data on Monday. Industrial production in Japan declined at a seasonally adjusted rate of 0.8% in July, down from the preliminary reading of 0.6% fall, after 1.1% rise in June.

Shipments were down 0.4% in July, down from the preliminary reading of a 0.3, while inventories declined 0.8%, in line with the preliminary reading.

On a yearly basis, industrial production in Japan was flat in July, down from the preliminary reading of 0.2% increase, after a 2.3% rise in June.

-

16:36

European Central Bank purchases €13.02 billion of government and agency bonds last week

The European Central Bank (ECB) purchased €13.02 billion of government and agency bonds under its quantitative-easing program last week.

ECB'S asset buying programme is intended to run to September 2016.

The ECB bought €3.89 billion of covered bonds, and €366 million of asset-backed securities.

-

16:15

OPEC expects higher demand for its oil in 2016

The Organization of the Petroleum Exporting Countries (OPEC) released its monthly report on Monday. OPEC expects the oil demand for its crude to be average 30.31 million barrels per day (bpd) next year, up 190,000 bpd from last month.

"Despite moderate economic growth, recent data shows better-than-expected oil-demand in the main consuming countries. At the same time, U.S. oil production has shown signs of slowing. This could contribute to a reduction in the imbalance of oil market fundamentals, however, it remains to be seen to what extent this can be achieved in the months to come," OPEC said.

OPEC expects that non-OPEC members will rise their output by 160,000 bpd next year, down 110,000 bpd from last month, while U.S. shale oil production was downgraded by 100,000 bpd.

Global oil demand growth is expected to be 1.29 million bpd in 2016, down 50,000 bpd from last month.

-

15:45

Option expiries for today's 10:00 ET NY cut

USDJPY 120.00 (USD 848m)

EURUSD 1.1150 (EUR 1bln) 1.1450 (1.1bln)

GBPUSD 1.5200 (GBP 268m) 1.5370 (255m)

EURJPY 136.00 (EUR 250m)

-

15:35

U.S. Stocks open: Dow -0.03%, Nasdaq +0.13%, S&P -0.03%

-

15:22

Before the bell: S&P futures +0.05%, NASDAQ futures +0.21%

U.S. stock-index futures were little changed as investors speculated on whether the Federal Reserve will raise interest rates at Thursday's meeting.

Global Stocks:

Nikkei 17,965.7 -298.52 -1.63%

Hang Seng 21,561.9 +57.53 +0.27%

Shanghai Composite 3,114.87 -85.37 -2.67%

FTSE 6,093.78 -23.98 -0.39%

CAC 4,530.19 -18.53 -0.41%

DAX 10,119.02 -4.54 -0.04%

Crude oil $44.30 (-0.74%)

Gold $1104.50 (+0.11%)

-

15:21

Preliminary real GDP in the OECD area climbs 0.7% in the second quarter

The Organization for Economic Cooperation and Development (OECD) released its preliminary real gross domestic product (GDP) growth figures on Monday. Real GDP of 34 OECD member countries rose 0.7% in the second quarter, after a 0.5% gain in the first quarter.

Real GDP of the United States was up to 0.9% from 0.2%, real GDP of Germany rose to 0.4% from 0.3%, while Britain's economy increased to 0.7% from 0.4%.

GDP of China rose 1.7% in the second quarter, up from 1.4% in the first quarter.

GDP of France dropped to 0.0% from 0.7%, Italy's economy decreased to 0.3% from 0.4%, while Japan's GDP plunged to -0.3% from 1.1%.

Eurozone's economy expanded at 0.4% in the second quarter, after a 0.5% rise in the first quarter.

On a yearly basis, GDP of 34 OECD member countries was up 3.2% in the second quarter, after a 3.2% gain in the previous quarter.

-

15:06

Wall Street. Stocks before the bell

(company / ticker / price / change, % / volume)(company / ticker / price / change, % / volume)

Apple Inc.

AAPL

116.75

2.22%

1.2M

Yandex N.V., NASDAQ

YNDX

11.34

0.62%

1.3K

General Motors Company, NYSE

GM

30.30

0.50%

2.0K

Cisco Systems Inc

CSCO

26.10

0.31%

21.6K

Procter & Gamble Co

PG

68.60

0.26%

1K

Boeing Co

BA

135.00

0.25%

0.1K

JPMorgan Chase and Co

JPM

62.71

0.24%

0.1K

Facebook, Inc.

FB

92.25

0.22%

21.3M

Hewlett-Packard Co.

HPQ

27.20

0.18%

3.0K

Walt Disney Co

DIS

104.62

0.13%

4.3K

Citigroup Inc., NYSE

C

51.15

0.10%

0.7K

Ford Motor Co.

F

13.72

0.07%

12.0K

Microsoft Corp

MSFT

43.50

0.05%

7.6K

The Coca-Cola Co

KO

38.15

0.05%

9.6K

Twitter, Inc., NYSE

TWTR

27.40

0.04%

9.8K

E. I. du Pont de Nemours and Co

DD

48.45

0.02%

2.6K

Johnson & Johnson

JNJ

92.93

0.00%

0.3K

Starbucks Corporation, NASDAQ

SBUX

56.53

0.00%

8.4M

AT&T Inc

T

32.70

-0.06%

10.7K

McDonald's Corp

MCD

97.35

-0.06%

3.6K

Intel Corp

INTC

29.45

-0.07%

2.2K

Amazon.com Inc., NASDAQ

AMZN

529.00

-0.08%

6.5K

Google Inc.

GOOG

625.00

-0.12%

0.8K

Tesla Motors, Inc., NASDAQ

TSLA

249.90

-0.14%

2.4M

Goldman Sachs

GS

185.00

-0.15%

0.2K

General Electric Co

GE

24.91

-0.16%

0.5K

Travelers Companies Inc

TRV

99.30

-0.19%

1.4K

Chevron Corp

CVX

75.64

-0.20%

0.1K

Pfizer Inc

PFE

32.90

-0.21%

0.4K

Home Depot Inc

HD

115.17

-0.23%

0.7K

International Business Machines Co...

IBM

147.00

-0.25%

1.7K

Wal-Mart Stores Inc

WMT

64.49

-0.25%

6.8K

Visa

V

70.52

-0.34%

2.5K

Caterpillar Inc

CAT

72.38

-0.34%

0.4K

ALCOA INC.

AA

9.60

-0.52%

3.1K

Exxon Mobil Corp

XOM

72.30

-0.54%

1.7K

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

11.32

-0.70%

9.5K

ALTRIA GROUP INC.

MO

52.20

-0.74%

0.3K

Barrick Gold Corporation, NYSE

ABX

6.30

-0.79%

63.3K

Yahoo! Inc., NASDAQ

YHOO

30.90

-1.69%

20.2K

-

15:04

Greek import prices drop 2.4% in July

The Hellenic Statistical Authority released its import prices data for Greece on Monday. Greek import prices fell 2.4% in July, after a 1.0% decline in June.

On a yearly basis, import prices dropped 11.5% in July, after a 10.5% decrease in June.

Import prices for energy plunged by 36.3% in July, while price for non-durable consumer goods declined by 0.6%.

Prices of capital goods rose 0.2% in July, while intermediate goods prices increased 0.7%.

-

14:46

Final consumer prices in Italy increase 0.2% in August

The Italian statistical office Istat released its final consumer price inflation data for Italy on Monday. Final consumer prices in Italy increased 0.2% in August, in line with the preliminary reading, after a 0.1% decline in July.

The rise was mainly driven by a lower fall in energy (-1.3%) and higher services costs (+0.6%).

On a yearly basis, consumer prices climbed 0.2% in August, in line with the preliminary reading, after a 0.2% increase in July.

The annual inflation was driven by an increase in prices of some services.

-

14:16

Foreign exchange market. European session: the euro traded lower against the U.S. dollar despite the better-than-expected economic data from the Eurozone

Economic calendar (GMT0):

(Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual)

04:30 Japan Tertiary Industry Index July 0.3% 0.2%

04:30 Japan Industrial Production (YoY) (Finally) July 2.3% 0.2% 0.0%

04:30 Japan Industrial Production (MoM) (Finally) July 1.1% -0.6% -0.8%

07:15 Switzerland Producer & Import Prices, m/m August -0.3% -0.7%

07:15 Switzerland Producer & Import Prices, y/y August -6.4% -6.8%

07:15 Switzerland Retail Sales (MoM) July 1.4% -0.6%

07:15 Switzerland Retail Sales Y/Y July -0.9% -0.1%

09:00 Eurozone Industrial production, (MoM) July -0.3% Revised From -0.4% 0.3% 0.6%

09:00 Eurozone Industrial Production (YoY) July 1.5% Revised From 1.2% 0.6% 1.9%

The U.S. dollar traded higher against the most major currencies in the absence of of any U.S. economic data today.

The euro traded lower against the U.S. dollar despite the better-than-expected economic data from the Eurozone. Eurostat released its industrial production data for the Eurozone on Monday. Industrial production in the Eurozone rose 0.6% in July, exceeding expectations for a 0.3% increase, after a 0.3% drop in June. June's figure was revised up from a 0.4%.

The increase was driven by a rise in energy, durable consumer goods and capital output. Energy output climbed 3.0% in July, durable consumer goods were up 1.3%, while capital goods output rose by 1.4%.

Intermediate goods declined by 0.6% in July, while non-durable consumer goods output fell 0.6%.

On a yearly basis, Eurozone's industrial production gained 1.9% in July, exceeding expectations for a 0.6% rise, after a 1.5% increase in June.

The increase was driven by a rise in durable consumer goods, capital goods and energy output. Durable consumer goods climbed by 2.6% in July from a year ago, capital goods rose by 2.2%, while energy output gained by 5.1%.

Non-durable consumer goods were up by 1.7%, while intermediate output was up by 0.5%.

The British pound traded lower against the U.S. dollar in the absence of any major economic reports from the U.K.

The Swiss franc traded lower against the U.S. dollar after the weak economic data from Switzerland. Retail sales in Switzerland declined at an annual rate of 0.1% in July, after a 0.9% drop in June.

Sales of food, beverages and tobacco fell at an annual rate of 0.6% in July, while non-food sales dropped 2.7%.

On a monthly basis, retail sales fell by 0.6% in July, after a 1.4% increase in June.

Sales of food, beverages and tobacco were down 0.4% in July, while non-food sales decreased 1.0%.

Switzerland's producer and import prices fell 0.7% in August, after a 0.3% drop in July.

The decline was mainly driven by lower prices for chemical and pharmaceutical products.

On a yearly basis, producer and import prices plunged 6.8% in August, after a 6.4% drop in July. It was the biggest drop since April 1950.

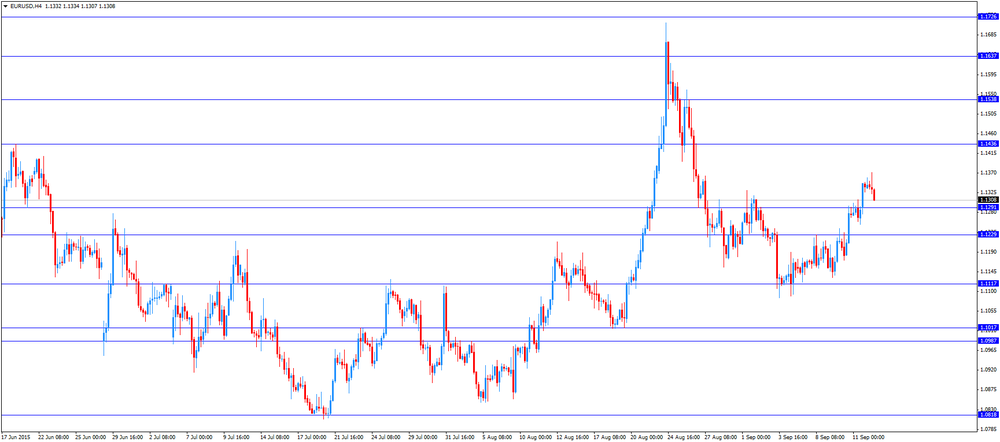

EUR/USD: the currency pair fell to $1.1307

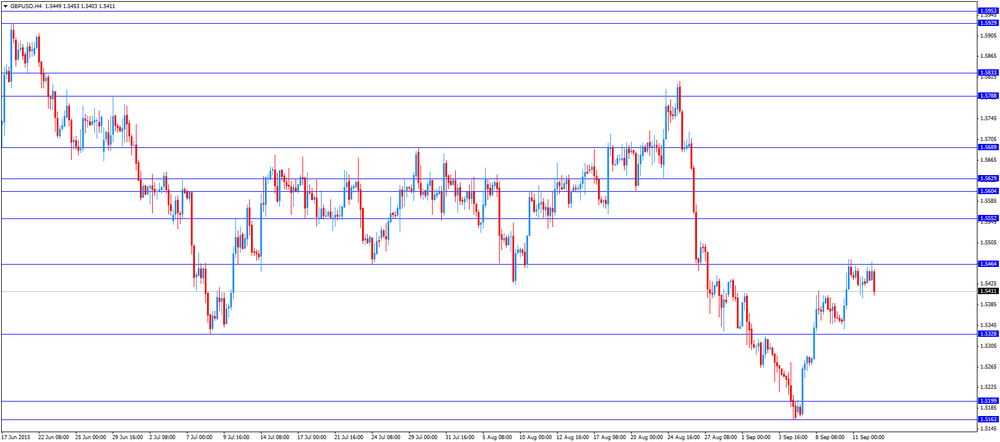

GBP/USD: the currency pair declined to $1.5403

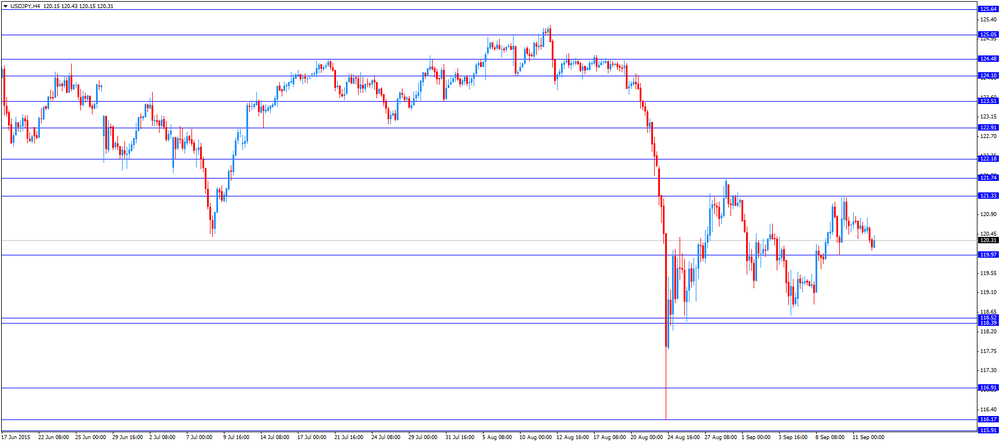

USD/JPY: the currency pair rose to Y120.43

-

14:00

Orders

EUR/USD

Offers 1.1355-60 1.1370-75 1.1390-1.1400 1.1420 1.1450

Bids 1.1320 1.1300 1.1285 1.1265-70 1.1250 1.1225 1.1200

GBP/USD

Offers 1.5480 1.5500-10 1.5530 1.5550 1.5585 1.5600 1.5630 1.5650

Bids 1.5450 1.5425-30 1.5400 1.5380 1.5350 1.5330 1.5320 1.5300

EUR/GBP

Offers 0.7355-60 0.7380-85 0.7400 0.7425 0.7450

Bids 0.7320-25 0.7300 0.7295-0.7300 0.7280 0.7260-65 0.7250

EUR/JPY

Offers 136.60 136.80 137.00 137.50 137.80 138.00

Bids 136.20 136.00 135.80 135.50 135.00 134.80-85 134.65 134.50

USD/JPY

Offers 120.50 120.80 121.00 121.20 121.35 121.50 121.80 122.00

Bids 120.00 119.80-85 119.50 119.30 119.00 118.85 118.50

Offers 0.7120-25 0.7150 0.7180 0.7200

Bids 0.7045-50 0.7020 0.7000 0.6980-85 0.6965 0.6950

-

12:00

European stock markets mid session: stocks traded higher on the better-than-expected economic data from the Eurozone

Stock indices traded higher on the better-than-expected economic data from the Eurozone. Eurostat released its industrial production data for the Eurozone on Monday. Industrial production in the Eurozone rose 0.6% in July, exceeding expectations for a 0.3% increase, after a 0.3% drop in June. June's figure was revised up from a 0.4%.

The increase was driven by a rise in energy, durable consumer goods and capital output. Energy output climbed 3.0% in July, durable consumer goods were up 1.3%, while capital goods output rose by 1.4%.

Intermediate goods declined by 0.6% in July, while non-durable consumer goods output fell 0.6%.

On a yearly basis, Eurozone's industrial production gained 1.9% in July, exceeding expectations for a 0.6% rise, after a 1.5% increase in June.

The increase was driven by a rise in durable consumer goods, capital goods and energy output. Durable consumer goods climbed by 2.6% in July from a year ago, capital goods rose by 2.2%, while energy output gained by 5.1%.

Non-durable consumer goods were up by 1.7%, while intermediate output was up by 0.5%.

Current figures:

Name Price Change Change %

FTSE 100 6,165.79 +48.03 +0.79 %

DAX 10,149.02 +25.46 +0.25 %

CAC 40 4,559.89 +11.17 +0.25 %

-

11:43

Swiss retail sales fall 0.6% in July

The Federal Statistical Office released its retail sales data for Switzerland on Monday. Retail sales in Switzerland declined at an annual rate of 0.1% in July, after a 0.9% drop in June.

Sales of food, beverages and tobacco fell at an annual rate of 0.6% in July, while non-food sales dropped 2.7%.

On a monthly basis, retail sales fell by 0.6% in July, after a 1.4% increase in June.

Sales of food, beverages and tobacco were down 0.4% in July, while non-food sales decreased 1.0%.

-

11:34

Switzerland's producer and import prices fall 0.7% in August

The Federal Statistical Office released its producer and import prices data on Monday. Switzerland's producer and import prices fell 0.7% in August, after a 0.3% drop in July.

The decline was mainly driven by lower prices for chemical and pharmaceutical products.

The Import Price Index decreased by 1.0% in August, while producer prices fell 0.6%.

On a yearly basis, producer and import prices plunged 6.8% in August, after a 6.4% drop in July. It was the biggest drop since April 1950.

The Import Price Index fell by 11.2% year-on year in August, while producer prices dropped 4.8%.

-

11:22

Eurozone’s industrial production rises in July

Eurostat released its industrial production data for the Eurozone on Monday. Industrial production in the Eurozone rose 0.6% in July, exceeding expectations for a 0.3% increase, after a 0.3% drop in June. June's figure was revised up from a 0.4%.

The increase was driven by a rise in energy, durable consumer goods and capital output. Energy output climbed 3.0% in July, durable consumer goods were up 1.3%, while capital goods output rose by 1.4%.

Intermediate goods declined by 0.6% in July, while non-durable consumer goods output fell 0.6%.

On a yearly basis, Eurozone's industrial production gained 1.9% in July, exceeding expectations for a 0.6% rise, after a 1.5% increase in June.

The increase was driven by a rise in durable consumer goods, capital goods and energy output. Durable consumer goods climbed by 2.6% in July from a year ago, capital goods rose by 2.2%, while energy output gained by 5.1%.

Non-durable consumer goods were up by 1.7%, while intermediate output was up by 0.5%.

-

11:00

Eurozone: Industrial production, (MoM), July 0.6% (forecast 0.3%)

-

11:00

Eurozone: Industrial Production (YoY), July 1.9% (forecast 0.6%)

-

10:54

European Central Bank Executive Board member Benoit Coeure: the economy in the Eurozone is too weak to create enough jobs

The European Central Bank (ECB) Executive Board member Benoit Coeure said in an interview on Friday that the economy in the Eurozone is too weak to create enough jobs.

"Growth is still not strong enough to create a sufficient number of jobs. When inflation is weak, the best way to bring it up to the 2 percent objective is to support economic activity," he said.

Coeure pointed out that growth and employment are very important for price stability.

-

10:50

Standard & Poor's affirms Greece's sovereign debt rating at CCC+

The rating agency Standard & Poor's on Friday affirmed Greece's sovereign debt rating at CCC+. The outlook remained stable.

The agency warned that it will downgrades the country's rating if the government does not implement reforms.

"We could lower the ratings on Greece if the new government cannot implement the reforms it has agreed to in the Memorandum of Understanding signed with the European Commission," Standard & Poor's said.

Greece will elect the new parliament on September 20.

The agency expect the Greece's economy to contract 3% this year.

-

10:34

The number of active U.S. rigs declined by 10 rigs to 652 last week

The oil driller Baker Hughes reported on Friday that the number of active U.S. rigs declined by 10 rigs to 652 last week. It was the second consecutive decrease.

Combined oil and gas rigs fell by 16 to 848.

Earlier last week, Baker Hughes said that the average total rig count declined by 17 to 883 in August from July.

-

10:22

U.S. budget deficit falls to $64.4 billion in August

The U.S. Treasury Department released its federal budget data on Friday. The budget deficit decreased to $64.4 billion in August, down from a deficit of $149.2 billion in July.

The budget deficit declined due to shifts in the timing of certain benefit payments.

In the first 11 months of the fiscal year 2015, which ends at September this year, the budget deficit totalled $530 billion, 10% lower than a year ago.

-

10:12

The Wall Street Journal survey: about 46% of economists expect the Fed to start raising its interest rate in September

According to The Wall Street Journal survey, about 46% of economists expect the Fed to start raising its interest rate in September. About 9.5% expect that the Fed would raise its interest in October, 35% said the Fed would wait until December, while 9.5% expect that the Fed will start raising its interest rate in 2016.

82% of economists expected last month that the Fed to start raising its interest rate in September, while 13% expected the first interest rate hike in December.

-

09:31

Switzerland: Retail Sales Y/Y, July -0.1%

-

09:17

Switzerland: Retail Sales (MoM), July -0.6%

-

09:15

Switzerland: Producer & Import Prices, y/y, August -6.8%

-

09:15

Switzerland: Producer & Import Prices, m/m, August -0.7%

-

08:53

Oil prices declined

West Texas Intermediate futures for October delivery slid to $44.51 (-0.27%), while Brent crude fell to $47.74 (-0.83%) amid weak demand.

The International Energy Agency said on Friday that the number of drilling rigs in the U.S. fell by 10 to 652 last week. The agency noted that persistent production cuts could rebalance the market in 2016. Nevertheless now oil oversupply and declines in global car sales (-1.0% y/y in August) continue to weigh on prices.

Kuwait set its October Official Selling Price for crude to Asia 60 cents below its September level. OPEC's monthly market report will be published later today.

Traders are also waiting for a Federal Reserve's policymaking meeting this week.

-

08:38

Gold steady ahead of Federal Reserve meeting

Gold is currently at $1,107.40 (+0.37%) near a one-month low as investors await a Federal Reserve meeting later this week. The central bank will announce its interest rate decision on Thursday. Uncertainty regarding forecasts for the result of the meeting persists and may weigh on prices, although bullion is unlikely to choose a direction before the decision is known.

Concerns over China's economy, mixed economic data and turmoil in stock markets have intensified doubts about the probability of a rate hike in the U.S. this month. Preliminary Reuters/Michigan Consumer Sentiment Index, which reflects consumer confidence in the U.S., fell to 85.7 in September from 91.9 reported previously, while economists had expected a moderate decline to 91.2.

-

08:35

Global Stocks: U.S. indices advanced

U.S. stock indices advanced on Friday in a relatively calm session as investors prepared for a Fed policymaking meeting scheduled for September 16-17.

Technology and health-care stocks led the gains last week, while stocks of energy companies declined amid low oil prices.

The Dow Jones Industrial Average rose 102.49 points, or 0.6%, to 16,432.89 (+2% over the week). The S&P 500 gained 8.72 points, or 0.5%, to 1,961.01 (+2.1% over the week). The Nasdaq Composite Index climbed 26.09 points, or 0.5%, to 4,822.34 (+3% over the week).

This morning in Asia Hong Kong Hang Seng slid 0.10%, or 22.15 points, to 21,482.22. China Shanghai Composite Index fell 3.20%, or 102.53 point, to 3,097.71. The Nikkei lost 1.35%, or 246.99 points, to 18,017.23.

Asian stock indices declined as investors assessed the latest data from China. The National Bureau of Statistics of China reported on Sunday that the country's industrial production rose by 6.1% y/y in August vs 6.4% expected and 6.0% previous. Meanwhile retail sales exceeded expectations and rose by 10.5% y/y in the same month. Fixed asset investment rose by 10.9% y/y in the first eight months of the current year, which is below expectations for an 11.1% growth and the previous reading of 11.2%. Slower investment growth points to a weaker economic growth in China.

Japanese stocks were weighed by data from China and the looming Fed meeting.

-

08:31

Foreign exchange market. Asian session: the yen gained

Economic calendar (GMT0):

Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual

04:30 Japan Tertiary Industry Index July 0.3% 0.2%

04:30 Japan Industrial Production (YoY) (Finally) July 2.3% 0.2% 0.0%

04:30 Japan Industrial Production (MoM) (Finally) July 1.1% -0.6% -0.8%

The yen advanced against the U.S. dollar after demand for this safe-haven currency had grown amid data on the Chinese economy. The National Bureau of Statistics of China reported on Sunday that the country's industrial production rose by 6.1% y/y in August vs 6.4% expected and 6.0% previous. Meanwhile retail sales exceeded expectations and rose by 10.5% y/y in the same month. Fixed asset investment rose by 10.9% y/y in the first eight months of the current year, which is below expectations for an 11.1% growth and the previous reading of 11.2%.

Federal Open Market Committee meeting will be this week's key event. A survey by the Wall Street Journal showed that approximately 46% of the economists surveyed last week expect the Fed to raise rates in September. 35% of economists said the Fed would raise rates in December and 9.5% said they expect a liftoff in 2016.

The New Zealand dollar managed to recover early losses amid Prime Minister John Key speech. He said that the government is always ready to respond to economic slowdown. Last week John Key sounded very optimistic about the country's economy.

EUR/USD: the pair fluctuated within $1.1335-60 in Asian trade

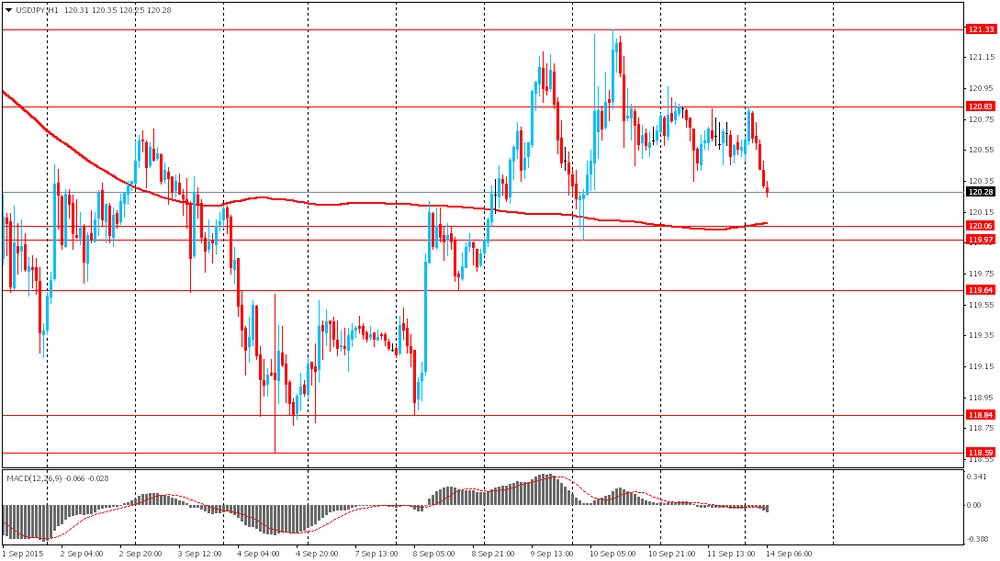

USD/JPY: the pair fell to Y120.25

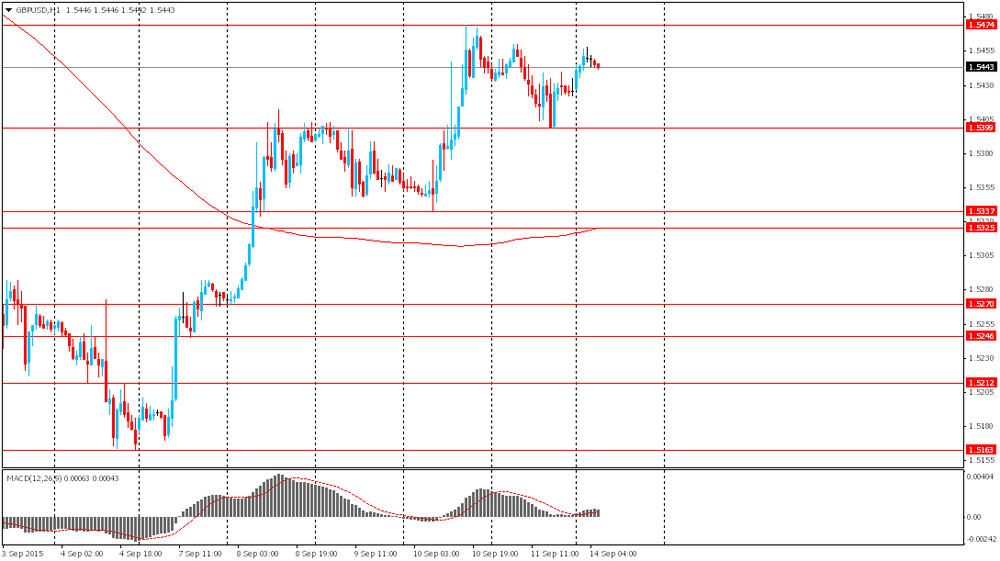

GBP/USD: the pair traded within $1.5425-55

The most important news that are expected (GMT0):

(time / country / index / period / previous value / forecast)

07:15 Switzerland Producer & Import Prices, m/m August -0.3%

07:15 Switzerland Producer & Import Prices, y/y August -6.4%

07:15 Switzerland Retail Sales (MoM) July 1.4%

07:15 Switzerland Retail Sales Y/Y July -0.9%

09:00 Eurozone Industrial production, (MoM) July -0.4% 0.3%

09:00 Eurozone Industrial Production (YoY) July 1.2% 0.6%

-

08:15

Options levels on monday, September 14, 2015:

EUR / USD

Resistance levels (open interest**, contracts)

$1.1475 (1570)

$1.1436 (1266)

$1.1397 (530)

Price at time of writing this review: $1.1348

Support levels (open interest**, contracts):

$1.1249 (429)

$1.1204 (949)

$1.1148 (2253)

Comments:

- Overall open interest on the CALL options with the expiration date October, 9 is 48412 contracts, with the maximum number of contracts with strike price $1,1500 (4293);

- Overall open interest on the PUT options with the expiration date October, 9 is 63303 contracts, with the maximum number of contracts with strike price $1,1000 (5976);

- The ratio of PUT/CALL was 1.31 versus 1.30 from the previous trading day according to data from September, 11

GBP/USD

Resistance levels (open interest**, contracts)

$1.5704 (1257)

$1.5606 (1289)

$1.5510 (1694)

Price at time of writing this review: $1.5448

Support levels (open interest**, contracts):

$1.5387 (882)

$1.5292 (1153)

$1.5194 (2728)

Comments:

- Overall open interest on the CALL options with the expiration date October, 9 is 20188 contracts, with the maximum number of contracts with strike price $1,5500 (1694);

- Overall open interest on the PUT options with the expiration date October, 9 is 19826 contracts, with the maximum number of contracts with strike price $1,5200 (2728);

- The ratio of PUT/CALL was 0.98 versus 0.91 from the previous trading day according to data from September, 11

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

06:32

Japan: Tertiary Industry Index , July 0.2%

-

04:16

Nikkei 22518,213.76 -50.46 -0.28 %, Hang Seng 21,749.9 +245.53 +1.14 %, Shanghai Composite 3,192.98 -7.26 -0.23 %

-

00:31

Commodities. Daily history for Sep 11’2015:

(raw materials / closing price /% change)

Oil 44.7 8+0.34%

Gold 1,107.90 +0.42%

-

00:31

Stocks. Daily history for Sep 11’2015:

(index / closing price / change items /% change)

Nikkei 225 18,264.22 -35.40 -0.19 %

Hang Seng 21,504.37 -58.13 -0.27 %

S&P/ASX 200 5,071.08 -23.93 -0.47 %

Shanghai Composite 3,200.45 +2.56 +0.08 %

FTSE 100 6,117.76 -38.05 -0.62 %

CAC 40 4,548.72 -47.81 -1.04 %

Xetra DAX 10,123.56 -86.88 -0.85 %

S&P 500 1,961.05 +8.76 +0.45 %

NASDAQ Composite 4,822.34 +26.09 +0.54 %

Dow Jones 16,433.09 +102.69 +0.63 %

-

00:28

Currencies. Daily history for Sep 11’2015:

(pare/closed(GMT +3)/change, %)

EUR/USD $1,1338 +0,56%

GBP/USD $1,5426 -0,11%

USD/CHF Chf0,969 -0,42%

USD/JPY Y120,57 -0,09%

EUR/JPY Y136,68 +0,44%

GBP/JPY Y186,02 -0,19%

AUD/USD $0,7089 +0,23%

NZD/USD $0,6314 +0,30%

USD/CAD C$1,3264 +0,20%

-