Noticias del mercado

-

22:01

New Zealand: NZIER Business Confidence, Quarter IV 15%

-

18:12

WSE: Session Results

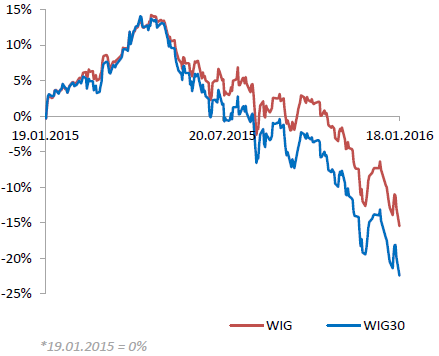

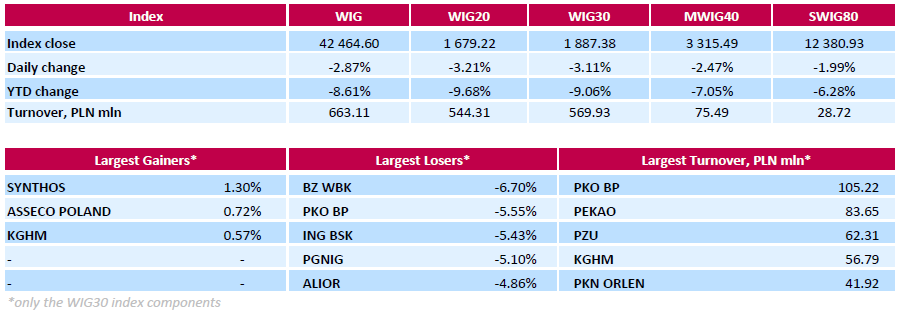

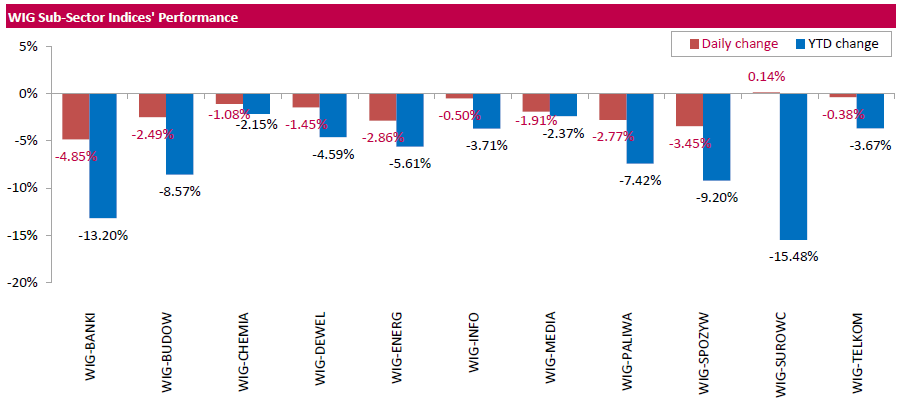

Polish equity market plunged on Monday, with the broad market measure, the WIG Index, declining by 2.87% after an unexpected Poland's foreign currency rating downgrade by Standard & Poor's agency. Materials sector (+0.14%) was the sole gainer among the WIG's 11 industry groups. At the same time, banking sector (-4.85%) was hit the hardest, following the president's Swiss franc mortgage conversion bill presented on Friday.

The large-cap companies' measure, the WIG30 Index, fell by 3.11%. Only three index constituents managed to generate positive returns: chemical producer SYNTHOS (WSE: SNS) gained 1.3%, IT-company ASSECO POLAND (WSE: ACP) added 0.72% and copper mainer KGHM (WSE: KGH) advanced 0.57%. At the same time, the session's most prominent losers were banking names BZ WBK (WSE: BZW), PKO BP (WSE: PKO), ING BSK (WSE: ING) and ALIOR (WSE: ALR), oil and gas producer PGNIG (WSE: PGN), railway freight transport operator PKP CARGO (WSE: PKP) and footwear retailer CCC (WSE: CCC), tumbling between 4.67% and 6.7%.

-

18:00

European stocks close: stocks closed lower on a drop in oil prices

Stock indices traded lower on a drop in oil prices. Concerns over the global oil oversupply weigh on oil prices.

International sanctions on Iran were lifted over the weekend after the International Atomic Energy Agency announced that Tehran had fulfilled its commitment.

Iran said on Sunday that it plans to raise its exports by 500,000 barrels per day.

Iran is a member of the Organization of the Petroleum Exporting Countries (OPEC), and is the fifth biggest OPEC oil producer.

U.S. stock markets are closed for a public holiday on Monday.

Indexes on the close:

Name Price Change Change %

FTSE 100 5,779.92 -24.18 -0.42 %

DAX 9,521.85 -23.42 -0.25 %

CAC 40 4,189.57 -20.59 -0.49 %

-

18:00

European stocks closed: FTSE 5779.92 -24.18 -0.42%, DAX 9521.85 -23.42 -0.25%, CAC 40 4189.57 -20.59 -0.49%

-

17:42

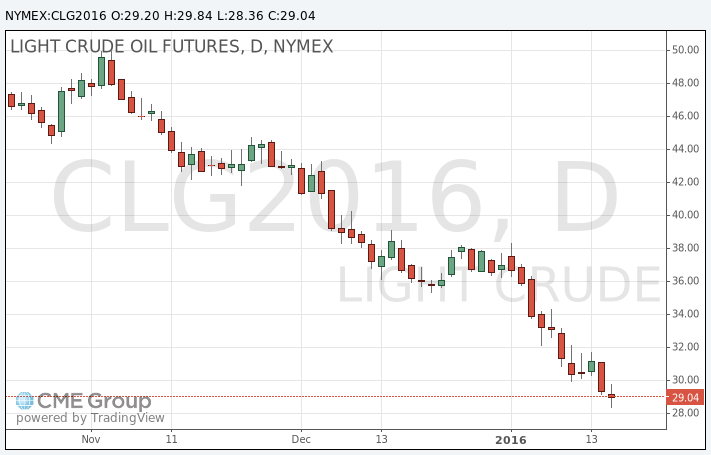

Oil prices slides below $29 a barrel

Oil prices fell below $29 a barrel on concerns over the global oil oversupply. International sanctions on Iran were lifted over the weekend after the International Atomic Energy Agency announced that Tehran had fulfilled its commitment.

Iran said on Sunday that it plans to raise its exports by 500,000 barrels per day.

Iran is a member of the Organization of the Petroleum Exporting Countries (OPEC), and is the fifth biggest OPEC oil producer.

The Organization of the Petroleum Exporting Countries (OPEC) released its monthly report on Monday. OPEC said that oil prices will start to recover this year, adding that supply from non-OPEC members will decline due to low oil prices.

"The analysis indicates that 2016 will be a supply-driven market. It will also be the year when the rebalancing process starts," OPEC said in its report.

Supply from non-OPEC members is expected to fall by 660,000 barrels per day (bpd) in 2016.

OPEC's output declined by 210,000 bpd to 32.18 million bpd in December, according to the report.

Global oil demand is expected to climb by 1.26 million bpd in 2016, OPEC noted.

WTI crude oil for March delivery dropped to $28.36 a barrel on the New York Mercantile Exchange.

Brent crude oil for March slid to $27.67 a barrel on ICE Futures Europe.

-

17:30

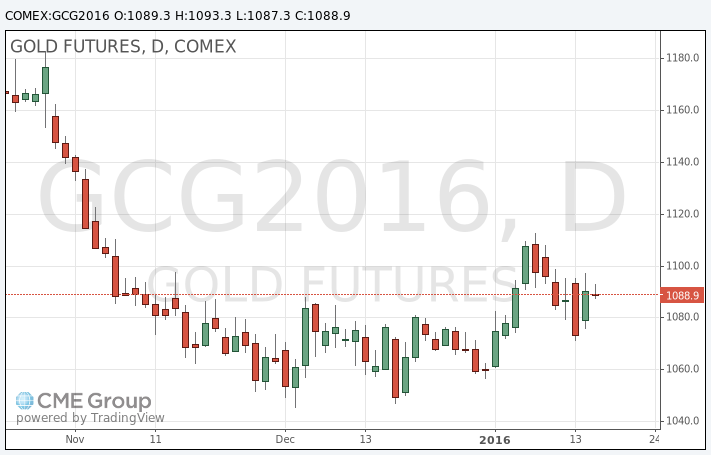

Gold trades little changed

Gold traded little changed in the absence of any major market driver. U.S. stock markets are closed for a public holiday on Monday.

Geopolitical tensions and the slowdown in the Chinese economy support gold. Official economic growth data from China will be released tomorrow. Analysts expect the Chinese economy to expand 6.8% in the fourth quarter, after a 6.9% in the third quarter.

February futures for gold on the COMEX today traded at 1088.90 dollars per ounce.

-

17:07

EY Item Club expects the U.K. economy to expand 2.6% in 2016

EY Item Club released its economic forecasts for the U.K. on Monday. The U.K. economy is expected to expand 2.6% in 2016, after a 2.2% in 2015. According to EY Item Club, the economy will be driven by consumer spending, which is expected to rise 2.8% this year.

Inflation is expected to 0.7% in 2016, 1.6% in 2017 and 1.8% in 2018.

The thin-tank expects that the Bank of England (BoE) will not raise its interest rate until November due to low inflation.

EY Item Club said that it forecasts the BoE's interest rate to be 1% by the middle of 2017 and 1.5% by the end of 2017.

-

16:40

Standard & Poor's affirms Belgium's credit rating

Standard & Poor's affirmed Belgium's credit rating at 'AA/A1+' on Friday. The outlook is stable.

The agency noted that economic recovery and reforms support the fiscal and external positions.

"We expect Belgium to reduce its public deficit and maintain a strong external position on the back of gradual economic recovery, supply side reforms, and fiscal consolidation," S&P said.

-

16:21

European Central Bank purchases €15.27 billion of government and agency bonds last week

The European Central Bank (ECB) purchased €15.27 billion of government and agency bonds under its quantitative-easing program last week.

The ECB bought €2.08 billion of covered bonds, and €55 million of asset-backed securities.

The ECB will release its interest rate decision on Thursday. Analysts expect the central bank to keep its monetary policy unchanged.

-

15:57

French President Francois Hollande: the government will spend €2.00 billion to create more jobs in France

French President Francois Hollande said in a speech on Monday that the government will spend €2.00 billion to create more jobs in France.

"These two billion euros will be financed without any new taxes of any kind, in other words, they will be financed by savings," he said.

-

15:51

Saudi oil minister Ali al-Naimi calls for cooperation among oil producing countries

Saudi oil minister Ali al-Naimi on Monday called for cooperation among oil producing countries, which should lead to stability in the global oil market.

"Market forces, as well as the cooperation among the producing nations, always lead to the restoration of stability. This, however, takes some time," he said.

"I'm optimistic about the future, the return of stability to the global oil markets, the improvement of prices and the cooperation among the major producing countries," al-Naimi added.

-

15:43

Oman is ready to cut its oil output

News reported on Monday that Oman, the largest non-OPEC oil producer, is ready to cooperate and to lower oil production, if the other oil producer will do the same.

"Oman is ready to do anything that would stabilize the oil market. 5% or 10% is what I think we need to cut and everyone has to do the same," Oman's oil minister, Mohammad bin Hamad al-Rumhy, said on Monday.

-

15:36

OPEC’s monthly report: oil prices will start to recover this year

The Organization of the Petroleum Exporting Countries (OPEC) released its monthly report on Monday. OPEC said that oil prices will start to recover this year, adding that supply from non-OPEC members will decline due to low oil prices.

"The analysis indicates that 2016 will be a supply-driven market. It will also be the year when the rebalancing process starts," OPEC said in its report.

Supply from non-OPEC members is expected to fall by 660,000 barrels per day (bpd) in 2016.

OPEC's output declined by 210,000 bpd to 32.18 million bpd in December, according to the report.

Global oil demand is expected to climb by 1.26 million bpd in 2016, OPEC noted.

-

15:05

Australia’s inflation gauge rises 0.2% in December

The TD Securities and Melbourne Institute (MI) released their monthly inflation gauge data on Monday. Australia's inflation gauge was up 0.2% in December, after a 0.1% gain in November.

On a yearly basis, inflation gauge rose 2.0% in December from 1.8% in November.

The rise was mainly driven by rises in prices for fruit and vegetables, holiday travel and accommodation, and meat and seafood.

The trimmed mean of the inflation gauge declined to 1.7% year-on-year in December from 1.8% in November.

"We expect headline inflation to increase by 0.3 per cent in the quarter, to be 1.7 per cent higher than a year ago, while we forecast underlying inflation to increase by 0.5 per cent in the quarter, for an annual rate of 2.0 per cent. These forecasts are entirely consistent with the RBA's November projections," Chief Asia-Pac Macro Strategist at TD Securities, Annette Beacher, said.

-

14:40

Option expiries for today's 10:00 ET NY cut

USD/JPY 115.40 (USD 400m) 116.40-50 (484m)

EUR/USD 1.0875 (EUR 297m) 1.0935 (566m) 1.0950 (230m) 1.1000 (407m)

-

14:35

New motor vehicle sales in Australia decline 0.5% in December

The Australian Bureau of Statistics released its new motor vehicle sales on Monday. New motor vehicle sales in Australia fell 0.5% in December, after a 1.3% rise in November. November's figure was revised up from a 1.0% gain.

Sales of passenger vehicles increased by 0.4% in December, sales of sports utility vehicles were up 0.1%, while sales for other vehicles rose by 0.8%.

On a yearly basis, new motor vehicle sales rose 2.2% in December, after a 6.0% increase in November.

-

14:18

Foreign exchange market. European session: the U.S. dollar traded mixed against the most major currencies in the absence of any major economic reports from the U.S.

Economic calendar (GMT0):

(Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual)

00:30 Australia New Motor Vehicle Sales (MoM) December 1.3% Revised From 1.0% -0.5%

00:30 Australia New Motor Vehicle Sales (YoY) December 6.0% 2.2%

04:30 Japan Tertiary Industry Index November 0.9% -0.8%

04:30 Japan Industrial Production (MoM) (Finally) November 1.4% -1.0% -0.9%

04:30 Japan Industrial Production (YoY) (Finally) -1.4% 1.6% 1.7%

The U.S. dollar traded mixed against the most major currencies in the absence of any major economic reports from the U.S. U.S. are closed for a public holiday today.

The euro traded mixed against the U.S. dollar in the absence of any major economic reports from the Eurozone.

The Italian statistical office Istat released its trade data for Italy on Monday. Italy' trade surplus narrowed to €4.41 billion in November from €4.82 billion in October. October's figure was revised up €4.81 billion.

Exports climbed 6.4% year-on-year in November, while imports increased 3.8%.

The British pound traded higher against the U.S. dollar in the absence of any major economic reports from the U.K.

According to property tracking website Rightmove, U.K. house prices rose 0.5% in January, after a 1.1% drop in December.

"Encouragingly for first-time buyers there's more fresh choice with more property coming to market in their target sector. With their asking prices pretty much the same as a month ago, perhaps the knock-on effects of the more punitive landlord tax regime have arrived early and they now face a dilemma over whether to buy now or wait to see if prices drop in this sector over the next few months," Rightmove director and housing market analyst, Miles Shipside, said.

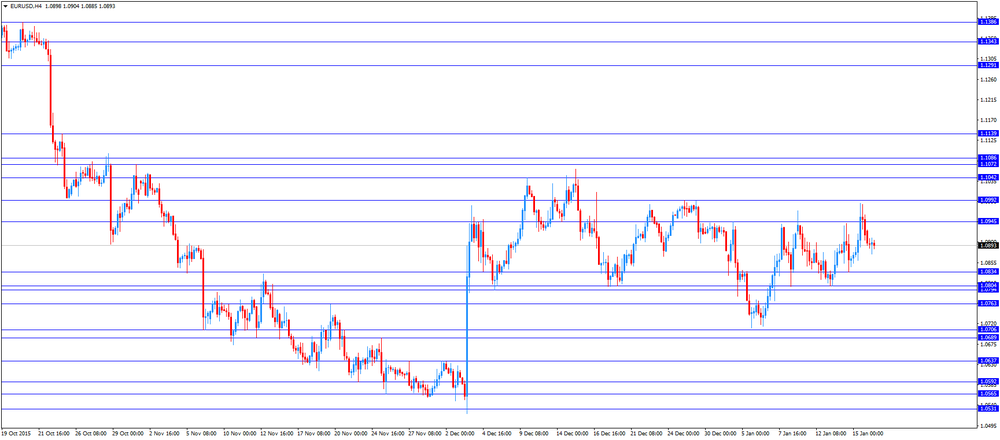

EUR/USD: the currency pair mixed

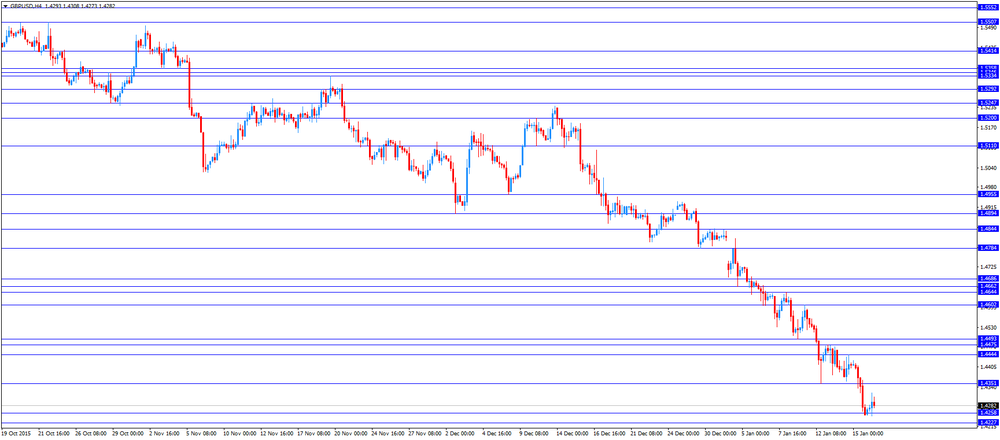

GBP/USD: the currency pair rose to $1.4322

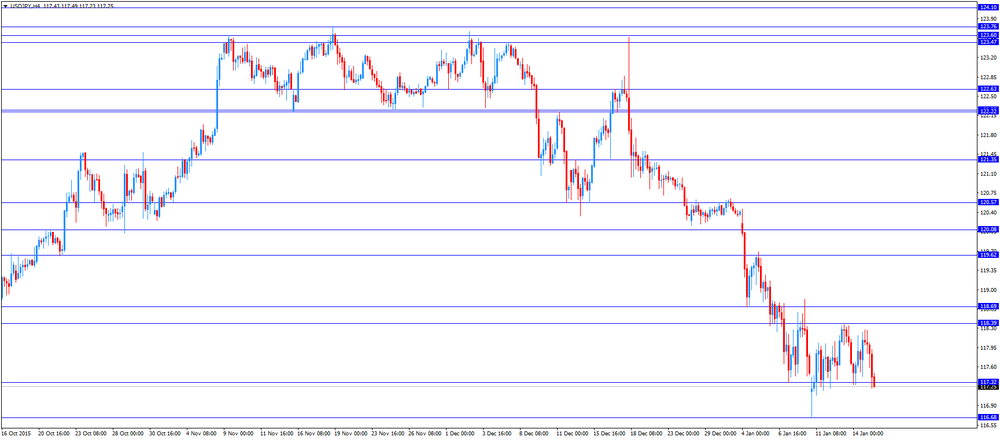

USD/JPY: the currency pair increased to Y117.43

The most important news that are expected (GMT0):

21:00 New Zealand NZIER Business Confidence Quarter IV -14%

-

14:00

Orders

EUR/USD

Offers 1.0900 1.0920 1.0935 1.0950 1.0965 1.0985 1.1000 1.1025 1.1050 1.1080 1.1100

Bids1.0855-60 1.0840 1.0825 1.0800-10 1.0780-85 1.0750 1.0720 1.0700 1.0675 1.0650

GBP/USD

Offers 1.4325-30 1.4350 1.4380 1.4400 1.4425 1.4450 1.4480 1.4500

Bids1.4280-85 1.4265 1.4260 1.4230 1.4200 1.4175 1.4150

EUR/GBP

Offers 0.7620 0.7640-45 0.7665 0.7680 0.7700 0.7730 0.7750

Bids0.7580-85 0.7550 0.7525 0.7500 0.7475-80 0.7450 0.7420 0.7400

EUR/JPY

Offers 128.00 128.30 128.50 128.80 129.00 129.30 129.50

Bids127.50 127.30 127.00 126.80 126.50 126.30 126.00

USD/JPY

Offers 117.50 117.65 117.85 118.00.118.25 118.40 118.60 118.80-85 119.00

Bids117.20 117.00 116.85 116.65 116.50 116.30 116.00

AUD/USD

Offers 0.6920 0.6950 0.6980 0.7000 0.7025-30 0.7050-55 0.7080 0.7100

Bids0.6880 0.6865 0.6850 0.6830 0.6800 0.6785 0.6750

-

12:00

European stock markets mid session: stocks traded lower on a drop in oil prices

Stock indices traded lower on a drop in oil prices. Concerns over the global oil oversupply weigh on oil prices.

International sanctions on Iran were lifted over the weekend after the International Atomic Energy Agency announced that Tehran had fulfilled its commitment.

Iran said on Sunday that it plans to raise its exports by 500,000 barrels per day.

Iran is a member of the Organization of the Petroleum Exporting Countries (OPEC), and is the fifth biggest OPEC oil producer.

U.S. stock markets will be closed for a public holiday on Monday.

Current figures:

Name Price Change Change %

FTSE 100 5,800.18 -3.92 -0.07 %

DAX 9,521.36 -23.91 -0.25 %

CAC 40 4,195.24 -14.92 -0.35 %

-

11:47

People’s Bank of China injected 55 billion yuan into market

The People's Bank of China (PBoC) injected 55 billion yuan ($8.36 billion) into market through its short-term liquidity operations (SLO) on Monday.

The reason for this injection could be the decision to boost liquidity.

-

11:41

Italy’ trade surplus falls to €4.41 billion in November

The Italian statistical office Istat released its trade data for Italy on Monday. Italy' trade surplus narrowed to €4.41 billion in November from €4.82 billion in October. October's figure was revised up €4.81 billion.

Exports climbed 6.4% year-on-year in November, while imports increased 3.8%.

On a monthly basis, exports rose a seasonally-adjusted 3.5% in November, while imports were up 1.4%.

The seasonally-adjusted trade surplus with the EU was €1.48 billion in November, while the trade surplus with non-EU countries was €2.80 billion.

-

11:32

The People's Bank of China will raise the reserve requirement ratio on yuan deposits of offshore bank

The People's Bank of China (PBoC) said on Monday that it raised the reserve requirement ratio on yuan deposits of offshore banks.

The central bank noted that the ratio will be raised to "normal levels" from zero.

Changes will be effective on January 25.

-

11:17

Home prices in China rise in December

China's National Bureau of Statistics (NBS) said on Monday that average new home prices in 70 major cities climbed at an annual rate of 7.7% in December, after a 6.5% gain in November.

The main contributor was Shenzhen, where home prices jumped by 46.8% year-on-year in December.

On a monthly base, house prices increased in 39 of 70 cities, prices slid in 27 cities, while prices remained unchanged in 4 cities.

-

10:41

International sanctions on Iran are lifted

International sanctions on Iran were lifted over the weekend after the International Atomic Energy Agency announced that Tehran had fulfilled its commitment.

Iran said on Sunday that it plans to raise its exports by 500,000 barrels per day.

Iran is a member of the Organization of the Petroleum Exporting Countries (OPEC), and is the fifth biggest OPEC oil producer.

-

10:31

Rightmove: U.K. house prices rise 0.5% in January

According to property tracking website Rightmove, U.K. house prices rose 0.5% in January, after a 1.1% drop in December.

"Encouragingly for first-time buyers there's more fresh choice with more property coming to market in their target sector. With their asking prices pretty much the same as a month ago, perhaps the knock-on effects of the more punitive landlord tax regime have arrived early and they now face a dilemma over whether to buy now or wait to see if prices drop in this sector over the next few months," Rightmove director and housing market analyst, Miles Shipside, said.

On a yearly basis, house prices in the U.K. climbed 6.5% in January, after a 7.4% increase in December.

-

10:19

The number of active U.S. rigs falls by 1 rigs to 515 last week

The oil driller Baker Hughes reported on Friday that the number of active U.S. rigs declined by 1 rigs to 515 last week. It was the lowest level since April 2010.

The gas rig count decreased by 13 to 135.

Combined oil and gas rigs declined by 14 to 650.

-

10:00

Earnings Season in U.S.: Major Reports of the Week

January 19

Before the Open:

Bank of America (BAC). Consensus EPS $0.27, Consensus Revenue $19891.85 mln

Morgan Stanley (MS). Consensus EPS $0.34, Consensus Revenue $7473.32 mln

UnitedHealth (UNH). Consensus EPS $1.38, Consensus Revenue $43109.79 mln

After the Close:

IBM (IBM). Consensus EPS $4.82, Consensus Revenue $22123.53 mln

January 20

Before the Open:

Goldman Sachs (GS). Consensus EPS $3.62, Consensus Revenue $7044.11 mln

January 21

Before the Open:

Travelers (TRV). Consensus EPS $2.66, Consensus Revenue $6068.00 mln

Verizon (VZ). Consensus EPS $0.88, Consensus Revenue $34151.73 mln

After the Close:

American Express (AXP). Consensus EPS $1.13, Consensus Revenue $8399.38 mln

Starbucks (SBUX). Consensus EPS $0.45, Consensus Revenue $5397.07 mln

January 22

Before the Open:

General Electric (GE). Consensus EPS $0.49, Consensus Revenue $36008.63 mln

-

09:41

Japan's tertiary industry activity index drops 0.8% in November

Japan's Ministry of Economy, Trade and Industry released its tertiary industry activity index on Monday. The index dropped 0.8% in November, after a 0.9% increase in October.

The fall was driven by declines in living and amusement-related services, wholesale trade, retail trade, transport and Postal activities, finance and insurance, goods rental and leasing(include automobile rental and leasing), and electricity, gas, heat supply and water industries.

-

09:27

Final industrial production in Japan drops 0.9% in November

Japan's Ministry of Economy, Trade and Industry released its final industrial production data on Monday. Final industrial production in Japan declined 0.9% in November, up from the preliminary estimate of a 1.0% drop, after a 1.4% increase in October.

Industrial shipments slid 2.4% in November, up from the preliminary estimate of a 2.5% fall, while inventories rose 0.4%, in line with the preliminary estimate.

On a yearly basis, Japan's industrial production was up 1.7% in November, up from the preliminary estimate of a 1.6% rise, after a 1.4% decline in October.

-

09:22

Option expiries for today's 10:00 ET NY cut

USD/JPY 115.40 (USD 400m) 116.40-50 (484m)

EUR/USD 1.0875 (EUR 297m) 1.0935 (566m) 1.0950 (230m) 1.1000 (407m)

-

08:08

Foreign exchange market. Asian session: the U.S. dollar advanced

Economic calendar (GMT0):

Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual

00:30 Australia New Motor Vehicle Sales (MoM) December 1.3% Revised From 1.0% -0.5%

00:30 Australia New Motor Vehicle Sales (YoY) December 6.0% 2.2%

04:30 Japan Tertiary Industry Index November 0.9% -0.8%

04:30 Japan Industrial Production (MoM) (Finally) November 1.4% -1.0% -0.9%

04:30 Japan Industrial Production (YoY) (Finally) -1.4% 1.6% 1.7%

The U.S. dollar rose against the euro and the yen after having declined on Friday. At the end of the previous week the euro gained on weak U.S. data and negative start to the trading session on stock markets. The U.S. commerce department reported on Friday that retail sales unexpectedly declined in December suggesting the country's economy had slowed in the fourth quarter. Retail sales fell by 0.1% in December after a revised 0.4% growth in November. Meanwhile the Federal Reserve reported on Friday that industrial production contracted more than expected in the U.S. in December. The corresponding index fell by 0.4% m/m, while economists had expected a more modest decline of 0.2%. Industrial production fell by 1.8% on an annualized basis.

Market participants also paid attention to comments by Federal Reserve's William Dudley. He admitted that inflation expectations weakened and he would not wish to see the situation worsen.

The Australian dollar rose on domestic inflation data. The TD Securities reported that consumer prices rose by 0.2% in December after the 0.1% rise in November. Inflation rose by 2.0% on a y/y basis. The Reserve Bank of Australia's target range is 2-3%.

EUR/USD: the pair fell to $1.0881 in Asian trade

USD/JPY: the pair rose to Y117.23

GBP/USD: the pair climbed to $1.4276

The most important news that are expected (GMT0):

(time / country / index / period / previous value / forecast)

21:00 New Zealand NZIER Business Confidence Quarter IV -14%

-

07:49

Oil prices extended declines

West Texas Intermediate futures for February delivery plunged to $29.75 (-2.11%), while Brent crude dropped to $28.05 (-3.08%) amid concerns that the global supply glut could worsen once Iran boosts exports. On Sunday the UN confirmed that Tehran fulfilled its obligations under a landmark deal to curb its nuclear programme. Iranian deputy oil minister said his country was ready to increase its crude oil exports by 500,000 barrels per day. Many analysts expect prices to remain under pressure.

U.S. crude oil inventories are ample and China's slowing economy is unable to absorb additional supplies.

-

07:15

Gold edged up

Gold slightly climbed to $1,091.30 (+0.06%) amid falling stocks and as weaker-than-expected data on the U.S. economy raised concerns over the chances that the Federal Reserve will conduct another rate hike in March. Retail sales and industrial production missed estimates in December.

Physical demand was sluggish as buyers from one of the major consumers China cut spending amid slowing economy.

Nevertheless a research by Thomson Reuters, quoted in the Financial Times magazine on Sunday, suggested that gold prices could experience upward pressure. The research showed that global production of gold is likely to decline by 3% in 2016 after seven straight years of rising output. Production reached its peak in 2015.

-

07:11

Options levels on monday, January 18, 2016:

EUR / USD

Resistance levels (open interest**, contracts)

$1.1024 (2914)

$1.0984 (1866)

$1.0957 (1528)

Price at time of writing this review: $1.0896

Support levels (open interest**, contracts):

$1.0863 (517)

$1.0825 (1254)

$1.0772 (3877)

Comments:

- Overall open interest on the CALL options with the expiration date February, 5 is 37216 contracts, with the maximum number of contracts with strike price $1,1050 (3502);

- Overall open interest on the PUT options with the expiration date February, 5 is 52873 contracts, with the maximum number of contracts with strike price $1,0700 (7953);

- The ratio of PUT/CALL was 1.42 versus 1.38 from the previous trading day according to data from January, 15

GBP/USD

Resistance levels (open interest**, contracts)

$1.4504 (1056)

$1.4406 (169)

$1.4310 (25)

Price at time of writing this review: $1.4273

Support levels (open interest**, contracts):

$1.4190 (1020)

$1.4094 (627)

$1.3996 (240)

Comments:

- Overall open interest on the CALL options with the expiration date February, 5 is 20561 contracts, with the maximum number of contracts with strike price $1,4700 (3091);

- Overall open interest on the PUT options with the expiration date February, 5 is 19739 contracts, with the maximum number of contracts with strike price $1,4550 (2011);

- The ratio of PUT/CALL was 0.96 versus 0.93 from the previous trading day according to data from January, 15

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

06:59

Global Stocks: U.S. stock indices posted sharp declines

U.S. stock indices fell on Friday with plunging oil prices being the biggest contributors to declines as market participants prepared for a rise in supplies from Iran.

The Dow Jones Industrial Average plunged 390.97 points, or 2.4%, to 15,988.08. The S&P 500 declined 44.85 point, or 2.3%, to 1,876.99 (all of its 10 sectors fell). The Nasdaq Composite lost 126.59 points, or 2.7%, to 4,488.42.

A renewed selloff in Chinese stocks weighed on U.S. markets. Meanwhile both S&P 500 and the Dow lost more than 2% over the week. However the Nasdaq outpaced their declines and lost more than 3% over the week.

The Federal Reserve reported on Friday that industrial production contracted more than expected in the U.S. in December. The corresponding index fell by 0.4% m/m, while economists had expected a more modest decline of 0.2%. Industrial production fell by 1.8% on an annualized basis.

This morning in Asia Hong Kong Hang Seng fell 0.50%, or 97.13, to 19,423.64. China Shanghai Composite Index gained 1.10%, or 31.79, to 2,932.76. The Nikkei lost 1.03%, or 177.44, to 16,969.67.

Asian stocks traded mixed as declines in Wall Street encouraged investors to sell. Market participants are waiting for China GDP data due on Tuesday. This report might have significant influence on global stock markets as concerns over the Chinese economy have been key negative factors for stocks.

-

05:34

Japan: Industrial Production (MoM) , November -0.9% (forecast -1.0%)

-

05:34

Japan: Industrial Production (YoY), 1.7% (forecast 1.6%)

-

05:32

Japan: Tertiary Industry Index , November -0.8%

-

03:03

Nikkei 225 16,900.44 -246.67 -1.44%, Hang Seng 19,330.66 -190.11 -0.97%, Shanghai Composite 2,866.74 -34.23 -1.18%

-

01:32

Australia: New Motor Vehicle Sales (MoM) , December -0.5%

-

01:32

Australia: New Motor Vehicle Sales (YoY) , December 2.2%

-

01:04

Commodities. Daily history for Jan 15’2016:

(raw materials / closing price /% change)

Oil 29.70 -4.84

Gold 1,088.60 +0.96

-

01:03

Stocks. Daily history for Sep Jan 15’2016:

(index / closing price / change items /% change)

Nikkei 225 17,147.11 -93.84 -0.54 %

Hang Seng 19,520.77 -296.64 -1.50 %

Shanghai Composite 2,902.22 -105.43 -3.51 %

FTSE 100 5,804.1 -114.13 -1.93 %

CAC 40 4,210.16 -102.73 -2.38 %

Xetra DAX 9,545.27 -248.93 -2.54 %

S&P 500 1,880.33 -41.51 -2.16 %

NASDAQ Composite 4,488.42 -126.59 -2.74 %

Dow Jones 15,988.08 -390.97 -2.39 %

-

01:02

Currencies. Daily history for Jan 15’2016:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,0917 +0,49%

GBP/USD $1,4251 -1,12%

USD/CHF Chf1,0019 -0,29%

USD/JPY Y116,95 -0,94%

EUR/JPY Y127,67 -0,45%

GBP/JPY Y166,66 -2,07%

AUD/USD $0,6859 -1,79%

NZD/USD $0,6457 -0,23%

USD/CAD C$1,4528 +1,12%

-