Noticias del mercado

-

22:07

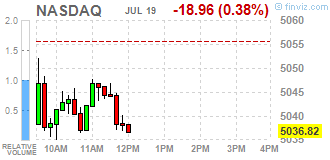

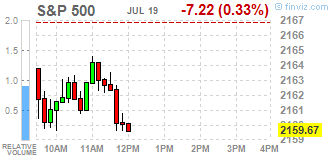

Major US stock indexes finished trading in different directions

Major US stock indexes closed with no unified dynamics on the background of deterioration in the global growth forecast from the International Monetary Fund because of the uncertainty about the impending release of Great Britain from the European Union.

In addition, as it became known today, bookmarks of new homes and building permits rose more than expected in June, partly reflecting a rebound in housing starts in the northeast. Bookmarks new homes in the US rose more than expected in June. The Commerce Department reported that the establishment of new homes jumped 4.8% to an annual rate of 1.189 million in June compared with the revised estimate for May at the level of 1.135 million. Economists had expected the establishment of new homes will rise slightly by 0.5% to 1,170 million to 1.164 million, which was originally reported in the previous month.

Oil prices dropped slightly today, as the market has concerns about the global oversupply of oil. A further fall in prices hinder the news of disruptions to oil supply from Libya. Protest over wages led to the closure of the eastern Libyan oil terminal Harigo, forcing to stop production at the field Safir. As a result, the supply of Libyan oil decreased by about 100 thousand. Barrels per day.

DOW index components closed mostly in the red (18 of 30). Outsider were shares of Microsoft Corporation (MSFT, -1,86%). Most remaining shares rose McDonald's Corp. (MCD, + 2,15%).

All business sectors S & P index showed a decline. Most of the basic materials sector fell (-1.2%).

At the close:

Dow + 0.14% 18,559.08 +26.03

Nasdaq -0.38% 5,036.37 -19.41

S & P -0.14% 2,163.78 -3.11

-

21:00

Dow +0.04% 18,541.03 +7.98 Nasdaq -0.42% 5,034.58 -21.20 S&P -0.24% 2,161.70 -5.19

-

18:06

Wall Street. Major U.S. stock-indexes slightly fell

Major U.S. stock-indexes slightly fell on Tuesday morning, led by a drop in technology and consumer discretionary stocks after Netflix's weak results. Also weighing on sentiment was the International Monetary Fund's move to cut its global growth forecasts for the next two years due to uncertainty over Britain's looming exit from the European Union.

Most of Dow stocks in negative area (22 of 30). Top looser - The Goldman Sachs Group, Inc. (GS, -1,21%). Top gainer - McDonald's Corp. (MCD, +1,68%).

All S&P sectors in negative area. Top looser - Conglomerates (-0,8%).

At the moment:

Dow 18430.00 -21.00 -0.11%

S&P 500 2153.25 -6.75 -0.31%

Nasdaq 100 4594.00 -14.25 -0.31%

Crude Oil 45.69 -0.25 -0.54%

Gold 1333.00 +3.70 +0.28%

U.S. 10yr 1.55 -0.04

-

18:00

European stocks closed: FTSE 100 6,697.37 +1.95 +0.03% CAC 40 4,330.13 -27.61 -0.63% DAX 9,981.24 -81.89 -0.81%

-

17:52

Oil fell slightly

Oil futures are trading slightly lower, since the market has concerns about the global oversupply.

A further fall in prices hinder the news of disruptions to oil supply from Libya. Protest over wages led to the closure of the eastern Libyan oil terminal Harigo, forcing production stop at the Safir field. As a result, the supply of Libyan oil decreased by about 100 thousand barrels per day.

Many analysts say, despite the relative stability of oil market fundamentals still look bearish. "We are entering a period when oil markets may feel the more intense pressure as a result of the return of Iran, - said Olivier Jakob, analyst at Petromatrix. - Saudi Arabia comes from the period of maximum demand amid falling margins from refining. And it's not a very good combination for the market. "

Gradually, investors' attention will switch to the weekly data on US petroleum inventories. The American Petroleum Institute will publish its report today, and the official statistics from the US Department of Energy will be released tomorrow. Experts predict that the Ministry of Energy reported a drop of oil to 2.2 million barrels. "Obviously, the production of shale oil in the US has reached a peak and will continue to fall", - said Phil Flynn of Price Futures Group. However, some analysts warn that the decline in US production may be offset by its increase in other regions of the world.

The cost of the September futures on US light crude oil WTI fell to 45.74 dollars per barrel.

September futures price for North Sea petroleum Brent fell to 46.93 dollars a barrel on the London Stock Exchange ICE Futures Europe.

-

17:39

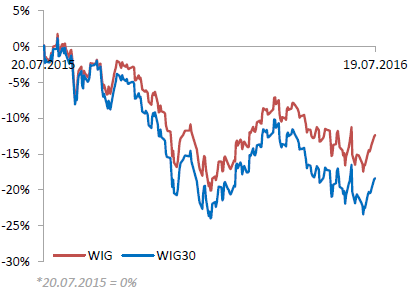

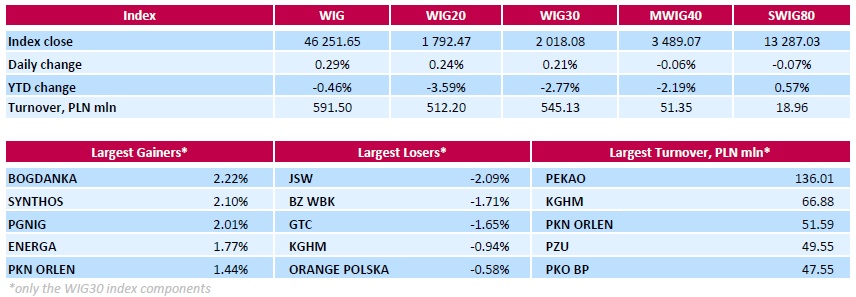

WSE: Session Results

Polish equity market closed higher on Tuesday. The broad market measure, the WIG Index, rose by 0.29%. Sector performance within the WIG Index was mixed. Oil and gas sector (+1.42%) was the strongest group, while materials (-0.90%) lagged behind.

The large-cap stocks' measure, the WIG30 Index, added 0.21%. In the index basket, thermal coal miner BOGDANKA (WSE: LWB) led the way up, climbing by 2.22%. The company announced it could boost coal reserves by 200-350 mln tonnes if it obtains a mining license for Ostrow deposit. Other major gainers were chemical producer SYNTHOS (WSE: SNS), oil and gas producer PGNIG (WSE: PGN) and genco ENERGA (WSE: ENG), which advanced 2.1%, 2.01% and 1.77% respectively. On the other side of the ledger, coking coal producer JSW (WSE: JSW) recorded the largest decline of 2.09%. It was followed by bank BZ WBK (WSE: BZW) and property developer GTC (WSE: GTC), dropping by 1.71% and 1.65% respectively.

-

17:29

Gold continue to accumulate

Gold moderately increased in price in the first half of the session, but later lost almost all positions on the background of a significant strengthening of the dollar after the release of strong US housing data.

The dollar index rose to its highest level since mid-March making dollar-denominated gold more expensive for holders of foreign currency.

The US Commerce Department reported that housing starts rebounded in June by 4.8 percent to an annual rate of 1.189 million compared with the revised estimate for May at the level of 1.135 million. Building permits, an indicator of future housing demand, also rose by 1.5 percent to an annual rate of 1.153 million in June compared with the revised 1.136 million in May. Economists assumed that the building permit will increase to 1.150 million from 1.138 million, which was originally reported in May.

"Lately we see more positive economic data from the US. Against this background, the likelihood that the Federal Reserve will return to the question of raising rates inceased.", - Said Nitessh Shah. Recall, higher rates have a downward pressure on the price of gold.

The course of trading was also affected by expectations of the European Central Bank meeting outcome. Economists say that the ECB is likely to refrain from further easing, but it can make changes to the bond buying program by expanding the list of assets available for acquisition.

Gold reserves in the largest investment fund SPDR Gold Trust rose yesterday by 0.25 percent and amounted to 965.22 tons.

The cost of the August gold futures on the COMEX rose to $ 1329.90 per ounce.

-

16:48

Sell Gbp/Usd - Morgan Stanley trade of the week

Currency investors should consider selling GBP/USD this week, advises Morgan Stanley in its weekly FX pick to clients.

"The BoE have made it clear that they will ease further this summer, most likely at the August meeting when they have run through new forecasts on the economy. More important for GBP is the environment that economic data will come in weaker as business activity slows down. Sure, the political risks have reduced as a Prime Minister and cabinet have been appointed. The GBP reaction going forward will be in response to monetary policy expectations as a result of weakness in data. The markets will pay particular attention to survey data between now and August 4.

From the GBP side, our view goes beyond immediate trade and growth shocks, and is focused on reduced prospects for investment, and what we see as an unsustainable current account deficit. The risk to this trade is that the broader USD weakness limits any downside in GBPUSD for now," MS argues.

We like to sell GBPUSD at 1.3500 with a target of 1.2500 and stop at 1.3800.

*MS maintains a limit order to sell GBP/USD in its portfolio with the same trade levels. Via efxnews.

-

16:28

ECB Seen in Search for "Comparatively Uncontroversial" Option - Dow Jones

According to Dow Jones Newswires, since the European Central Bank's inflation target is likely to remain unattainable for some considerable time, the bank will have to leave open the option to extend the duration of its asset purchase program, says Christian Reicherter, analyst at DZ Bank. It doesn't expect any adjustments to be made to key interest rates or to the purchase program at the upcoming meeting Thursday, but looks for changes in September. According to DZ Bank, one of the "comparatively uncontroversial" options which the ECB could take to further broaden the available universe of German government securities would be to raise the issue limit for bonds without a CAC-clause, Mr. Reicherter says.

-

15:50

Option expiries for today's 10:00 ET NY cut

EUR/USD: 1.0990-1.1000 (EUR 544m) 1.1100 (1.1bln) 1.1145 (356m)

USD/JPY: 105.35-50 (USD 441m)

GBP/USD 1.3200 (GBP 821m) 1.3500 (824m)

EUR/GBP 0.8300 (EUR 596m)

AUD/USD 0.7600 (AUD 380m) 0.7625 (290m)

USD/CAD 1.2960-65 (USD 400m)

NZD/USD 0.7200 (NZD 200m)

-

15:47

WSE: After start on Wall Street

The quotations on Wall Street started on the red side of the market. It seems that after many successful sessions where demand calmly controlled the situation, keeping the S&P500 at new levels, the market today prepares us to test the possibility of demand. It is very important that for the last more than two years, each attempt to go to new levels ended in failure. Therefore, the market may now be very sensitive to any sign of indisposition of buyers. Condition of Wall Street also will affect the global risk aversion, thereby preserving of emerging markets, which for us is more direct guideline.

-

15:42

IMF cuts global growt forecasts

- 2016 UK growth forecast reduced to 1.7% from 1.9% in April. 2017 growth at 1.3% from 2.2% in April

- IMF would've revised 2017 global growth forecast slightly upward if not for Brexit

- Japan growth forecast cut to 0.3% from 0.5%. Improves 2017 to 0.1% from a -0.1% contraction

- raises China 2016 growth forecasts to 6.6% from 6.5%. Sees 2017 growth slowing to 6.2%

- Global growth could fall to 2.8% in 2016 and 2017 under its severe alternative scenario of UK - EU divorce negotiations going badly, financial stress intensifying

-

15:32

U.S. Stocks open: Dow -0.06%, Nasdaq -0.25%, S&P -0.24%

-

15:11

Before the bell: S&P futures -0.19%, NASDAQ futures -0.20%

U.S. stock-index futures slipped following a mix of earnings reports, as investors weighed the prospects for further gains after equities closed Monday at fresh records.

Global Stocks:

Nikkei 16,723.31 +225.46 +1.37%

Hang Seng 21,673.2 -129.98 -0.60%

Shanghai Composite 3,036.2 -7.37 -0.24%

FTSE 6,692.18 -3.24 -0.05%

CAC 4,325.57 -32.17 -0.74%

DAX 9,963.83 -99.30 -0.99%

Crude $45.09 (-0.33%)

Gold $1331.90 (+0.20%)

-

14:52

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

10.8

-0.12(-1.0989%)

91255

ALTRIA GROUP INC.

MO

68.93

-0.24(-0.347%)

4109

Amazon.com Inc., NASDAQ

AMZN

734.67

-1.40(-0.1902%)

5297

American Express Co

AXP

63.56

-0.43(-0.672%)

2665

Apple Inc.

AAPL

99.53

-0.30(-0.3005%)

52539

AT&T Inc

T

42.81

-0.04(-0.0933%)

539

Barrick Gold Corporation, NYSE

ABX

21.55

-0.06(-0.2777%)

36555

Chevron Corp

CVX

106.05

-0.04(-0.0377%)

695

Cisco Systems Inc

CSCO

29.9

-0.01(-0.0334%)

8839

Citigroup Inc., NYSE

C

44.32

-0.25(-0.5609%)

10971

Exxon Mobil Corp

XOM

95

0.18(0.1898%)

1820

Facebook, Inc.

FB

119.07

-0.30(-0.2513%)

90293

Ford Motor Co.

F

13.6

-0.05(-0.3663%)

6690

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

12.95

-0.19(-1.446%)

134719

General Electric Co

GE

32.8

-0.11(-0.3342%)

9654

General Motors Company, NYSE

GM

30.72

-0.15(-0.4859%)

13724

Goldman Sachs

GS

162

-1.33(-0.8143%)

127320

Google Inc.

GOOG

731.9

-1.88(-0.2562%)

2321

Home Depot Inc

HD

136.3

-0.04(-0.0293%)

1397

Intel Corp

INTC

34.95

-0.10(-0.2853%)

14421

International Business Machines Co...

IBM

162

2.14(1.3387%)

22038

Johnson & Johnson

JNJ

125.76

2.62(2.1277%)

166431

JPMorgan Chase and Co

JPM

63.69

-0.27(-0.4221%)

7447

McDonald's Corp

MCD

124.23

0.43(0.3473%)

939

Merck & Co Inc

MRK

59.11

0.09(0.1525%)

262

Microsoft Corp

MSFT

54

0.04(0.0741%)

29006

Pfizer Inc

PFE

36.64

-0.00(-0.00%)

5417

Tesla Motors, Inc., NASDAQ

TSLA

225

-1.25(-0.5525%)

15054

The Coca-Cola Co

KO

45.57

-0.06(-0.1315%)

1550

Travelers Companies Inc

TRV

117.38

-0.00(-0.00%)

950

Twitter, Inc., NYSE

TWTR

18.52

-0.13(-0.697%)

35888

UnitedHealth Group Inc

UNH

140.55

-0.20(-0.1421%)

3161

Visa

V

78.31

-0.00(-0.00%)

2606

Wal-Mart Stores Inc

WMT

73.85

0.01(0.0135%)

200

Yahoo! Inc., NASDAQ

YHOO

37.79

-0.16(-0.4216%)

8212

Yandex N.V., NASDAQ

YNDX

21.61

0.11(0.5116%)

43461

-

14:46

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Other:

Microsoft (MSFT) initiated with a Market Perform at William Blair

Yahoo! (YHOO) target raised to $39 from $38 at RBC Capital Mkt

Yahoo! (YHOO) target raised to $43 from $42 at UBS

Yahoo! (YHOO) maintained with a Neutral at Mizuho

IBM (IBM) target raised to $186 from $166 at Drexel Hamilton

-

14:44

US: housing starts and building permits rose significantly

Building Permits

Privately-owned housing units authorized by building permits in June were at a seasonally adjusted annual rate of 1,153,000. This is 1.5 percent (±1.3%) above the revised May rate of 1,136,000, but is 13.6 percent (±0.6%) below the June 2015 estimate of 1,334,000. Single-family authorizations in June were at a rate of 738,000; this is 1.0 percent (±1.5%)* above the revised May figure of 731,000. Authorizations of units in buildings with five units or more were at a rate of 384,000 in June.

Housing Starts

Privately-owned housing starts in June were at a seasonally adjusted annual rate of 1,189,000. This is 4.8 percent (±13.5%)* above the revised May estimate of 1,135,000, but is 2.0 percent (±12.9%)* below the June 2015 rate of 1,213,000. Single-family housing starts in June were at a rate of 778,000; this is 4.4 percent (±15.8%)* above the revised May figure of 745,000. The June rate for units in buildings with five units or more was 392,000.

-

14:38

European session review: the pound fell despite higher inflation

The following data was published:

(Time / country / index / period / previous value / forecast)

8:30 UK Producer Price Index (m / m) June 0.2% 0.1% Revised to 0.2% 0.2%

8:30 UK producers selling prices index, y / y in June -0.6% -0.7% Revised to -0.5% -0.4%

8:30 UK producers purchase prices index m / m 2.2% Revised June from 2.6% 1.1% 1.8%

8:30 UK purchasing producer prices index, y / y in June -4.4% -3.9% Revised to -0.8% -0.5%

8:30 UK Retail Price Index m / m in June 0.3% 0.2% 0.4%

8:30 UK Retail Price Index y / y in June 1.4% 1.5% 1.6%

8:30 UK Consumer Price Index m / m in June 0.2% 0.1% 0.2%

8:30 UK consumer price index base value, y / y in June 1.2% 1.3% 1.4%

8:30 UK Consumer Price Index y / y in June 0.3% 0.4% 0.5%

9:00 Eurozone index of sentiment in the business environment from the ZEW Institute in July 20.2 -14.7

9:00 Germany Sentiment Index in the business environment of the institute ZEW July 19.2 9.1 -6.8

The British pound fell, although inflation data in the UK was higher than forecast. According to analysts, it signals the market belief that the Bank of England at its meeting scheduled for August 4, will resort to change the monetary policy.

Initially, the pound being able to overcome the barrier of $ 1.32, however, turned out to be a temporary increase.

The weakness of the pound, which is observed after Brexit, obviously, put upward pressure on inflation, but the economic stimululus by the Bank of England is still expected.

Markets are preparing for the possibility that the International Monetary Fund (IMF) will cut its economic forecast.

In the UK, inflation accelerated more than expected in June, showed the data of the Office for National Statistics on Tuesday.

Consumer prices rose 0.5 percent year on year in June, faster than the growth of 0.3 percent recorded in May. Inflation was expected to rise to 0.4 percent.

Core inflation, which excludes energy, food, alcoholic beverages and tobacco, rose to 1.4 percent from 1.2 percent in May.On a monthly basis, consumer prices rose 0.2 percent in June as in May, above expectations of a growth by 0.1 percent.

In another report ONS showed that the index of producer prices has decreased by 0.4 percent compared to the previous year.

On a monthly basis, the index for Producer Price rose by 0.2 percent for the second month in a row.

Purchase prices of manufacturers registered a slower annual decline of 0.5 percent after easing 4.4 percent in May. Economists had forecast a 0.8 percent drop in June.

On a monthly basis the index of purchase prices of manufacturers advanced 1.8 percent, compared with the growth of 2.2 percent in the previous month and an increase of 1.1 percent forecast.

On Monday, the pound jumped to session highs after a Bank of England official said he was not sure that he would support lowering the interest rate at the August meeting of the central bank.

Minutes published last Thursday clearly demonstrated the intention of the bank to ease monetary policy next month to counter the adverse economic impact of Brexit.

The Bank of England kept interest rates at 0.5%, which was a surprise to the markets.

At the same time, Moody's warned that the creditworthiness of the United Kingdom is under pressure after the decision to leave the EU.

Moody's reported that the medium-term prospects for the British economy may be reduced if it fails to reach a new trade agreement with Europe, but also noted that economic growth will slow down significantly in the near future.

The rating agency forecast UK growth in 2016 at 1.5% and nearly 1% in 2017.

The euro fell against the US dollar after weak data from the ZEW institute. The indicator of economic sentiment in Germany fell in July to its lowest level in more than three years from Brexit fears and, consequently, uncertainty for the economy.

The index of sentiment in the business environment fell to -6.8 from 19.2 in June. The last reading was the lowest since November 2012 and well below the long-term average of 24.3 points.

"Brexit surprised the majority of financial market experts. The uncertainty about the consequences of the vote for the German economy is largely responsible for the significant decline in economic sentiment," said ZEW President Achim Wambach.

"In particular, concerns about export prospects and stability of the European banking and financial system, probably will fall heavily on the economic outlook."

The index of current conditions fell to 49.8 from 54.5. Economists expected the index to be 51.8.

The indicator of the current economic situation declined by 2.4 points to minus 12.4 points.

EUR / USD: during the European session, the pair fell to $ 1.1023

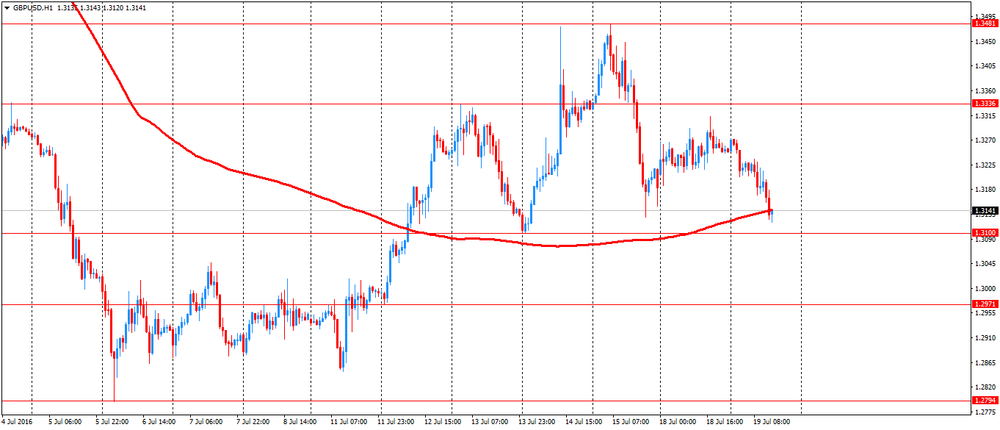

GBP / USD: during the European session, the pair fell to $ 1.3120

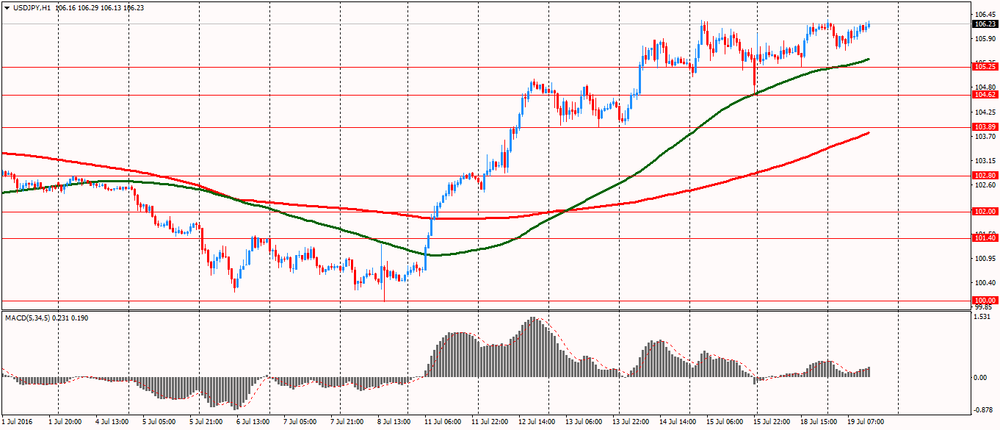

USD / JPY: during the European session, the pair rose to Y106.29

-

14:30

U.S.: Building Permits, June 1153 (forecast 1150)

-

14:30

U.S.: Housing Starts, June 1189 (forecast 1170)

-

13:51

Reuters: UK will not invoke EU Article 50 this year, government lawyer says

According to Reuters, Britain will not begin its formal divorce from the European Union by invoking Article 50 of the Lisbon Treaty this year, a government lawyer told the High Court on Tuesday.

Lawyer Jason Coppell indicated however that the government's current position could change.

"The current position is that notification will not occur before the end of 2016," Coppell said.

Prime Minister Theresa May has said article 50, which starts a two-year countdown to exit, should not be triggered this year.

Coppell was speaking at the start of the first of a series of lawsuits brought by individuals to demand that the British government win legislative approval from parliament before triggering Article 50.

-

13:50

Company News: Goldman Sachs (GS) Q2 results beat analysts’ expectations

Goldman Sachs reported Q2 FY 2016 earnings of $3.72 per share (versus $4.75 in Q2 FY 2015), beating analysts' consensus estimate of $3.05.

The company's quarterly revenues amounted to $7.932 bln (-12.5% y/y), beating analysts' consensus estimate of $7.485 bln.

GS rose to $164.25 (+0.56%) in pre-market trading.

-

13:48

Orders

EUR/USD

Offers : 1.1080 1.1100 1.1125-30 1.1150 1.1170 1.1185 1.1200

Bids: 1.1050 1.1030 1.1000 1.0975-80 1.0950 1.0930 1.0900

GBP/USD

Offers : 1.3225-30 1.3250 1.3270-75 1.3290-1.3300 1.3320 1.3350 1.3380 1.3400

Bids: 1.3180 1.3150 1.3130-35 1.3100 1.3060 1.3020 1.3000

EUR/GBP

Offers : 0.8400-05 0.8420-25 0.8450 0.8470 0.8485 0.8500

Bids: 0.8380 0.8360 0.8350 0.8325-30 0.8300 0.8285 0.8255-60 0.8230 0.8200

EUR/JPY

Offers : 117.50 117.70 118.00 118.25 118.50 119.00

Bids: 116.85 116.50 116.25 116.00 115.50 115.00 114.60 114.00

USD/JPY

Offers : 106.20 106.30-35 106.50 106.70 107.00 107.50

Bids: 105.80 105.60 105.30-35 105.00 104.80 104.50-60 104.20 104.00 103.80 103.50

AUD/USD

Offers : 0.7550 0.7580 0.7600 0.7620 O.7635 0.7650-55 0.7680 0.7700

Bids: 0.7500 0.7485 0.7470 0.7450 0.7420 0.7400

-

13:08

WSE: Mid session comment

The reading of the ZEW index (-6.8; forecast 9.1), which fell to negative values clearly disappointed. The data for the first time take into account the outcome of the referendum in the UK. Anxiety respondents focuses on exports, the stability of the banking and financial system in Europe. The market reaction to the data was minimal, because it does not contribute many of the new, to the situation.

Our market catches a shortness of breath today, although only consolation is the fact that is a smaller scale than in Euroland. In the mid-session the WIG20 index was at 1,783 points (-0,24%) and with the turnover of PLN 231 mln.

-

13:06

Turkish central bank cuts overnight rate by 0.25 %

-

13:06

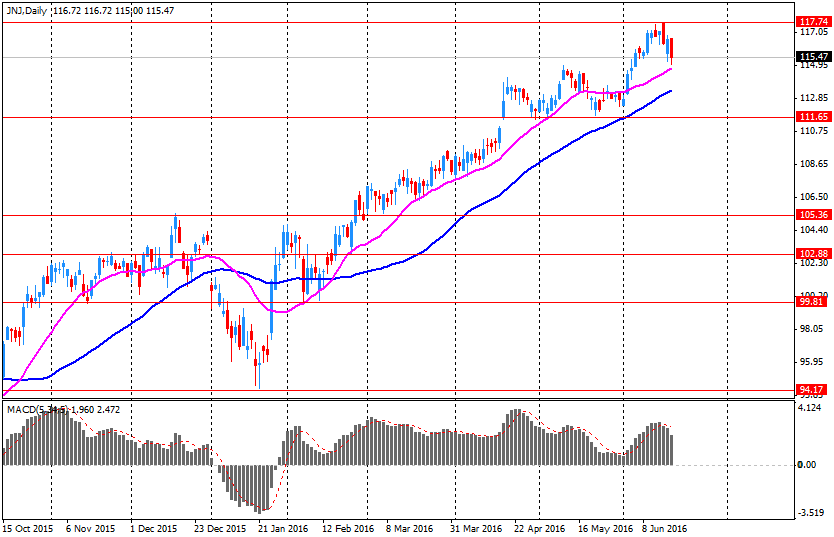

Company News: Johnson & Johnson (JNJ) Q2 results beat analysts’ estiamtes

Johnson & Johnson reported Q2 FY 2016 earnings of $1.74 per share (versus $1.71 in Q2 FY 2015), beating analysts' consensus estimate of $1.68.

The company's quarterly revenues amounted to $18.482 bln (+3.9% y/y), beating analysts' consensus estimate of $17.986 bln.

JNJ rose to $126.01 (+2.33%) in pre-market trading.

-

13:05

Russia and Turkey will resume charter flights until the end of the year

Russia and Turkey will resume charter flights until the end of the year. Such an opinion was expressed by the executive director of the Association of Tour Operators of Russia (ATOR) Maya Lomidze, in an interview.

"The attempt of military coup in Turkey is strongly reflected in the significant decline of demand".

Earlier Lomidze stated that recent developments in Turkey could lead to the delayed restoration of charter flights.

On the night of July 16 a rebel group was attempted o a military coup. The main conflicts were in Ankara and Istanbul. The country's leadership has announced that the coup is suppressed. According to the latest information, 208 Turkish citizens were killed and 100 rebels were killed, about 1.5 thousand people were injured.

-

12:42

Major stock indices in Europe are falling

In today's mid trading, European stock indices down influenced by stock prices of mining and oil companies.

The composite index of the largest companies in the region Stoxx Europe 600 fell by 0.9% - to 335.82 points.

Stock indices on Monday trading mixed, with Britain's FTSE rose 0.4% to its highest level since August 2015.

Economic data also put presurre on stocks as sentiment in the business environment of the ZEW Institute in Germany and the euro zone declined sharply. The indicator of economic sentiment in Germany fell in July to its lowest level in more than three years, amid Brexit and, consequently, uncertainty for the economy.

The index of sentiment in the business environment from the ZEW Institute in Germany fell to -6.8 from 19.2 in June. The last reading was the lowest since November 2012 and well below the long-term average of 24.3 points.

"Brexit Voting surprised the majority of financial market experts. The uncertainty about the consequences of the vote for the German economy is largely responsible for the significant decline in economic sentiment," said ZEW President Achim Wambach.

"In particular, concerns about export prospects for and stability of the European banking and financial system, probably will fall heavily on the economic outlook."

The index of current conditions survey fell to 49.8 from 54.5. Economists expected the index to be 51.8.

The index of sentiment in the business environment of the ZEW institute in the euro zone decreased by 34.9 points to minus 14.7 points.

The indicator of the current economic situation declined by 2.4 points to minus 12.4 points.

Shares of oil companies are getting cheaper in the course of trading: the price of BP shares fell 0.4%.

The value of Rio Tinto fell 3%. One of the world's largest mining companies increased shipments of iron ore in the second quarter of 2016 by 7% compared with the previous quarter - to 82.2 million tons. The indicator, however, was worse than market expectations.

Shares of other mining companies also cheaper: Glencore's stock price has fallen by 3%, BHP Billiton - by 3.2%.

Shares of Dutch chemical company Akzo Nobel fell by 5%. The company's profit in the second quarter grew by 8.6%, exceeding market expectations. However, Akzo Nobel has warned that the market environment remains uncertain with the difficult conditions in some countries and segments.

Shares of the Swedish rubber products manufacturer Trelleborg fell by 5.6%. Earnings coincided with analysts' expectations, but the company reported an increase in economic uncertainty in connection with the decision of the UK to withdraw from the European Union and has given careful forecast for the future.

At the moment:

FTSE 6667.42 -28.00 -0.42%

DAX 9938.17 -124.96 -1.24%

CAC 4318.07 -39.67 -0.91%

-

12:25

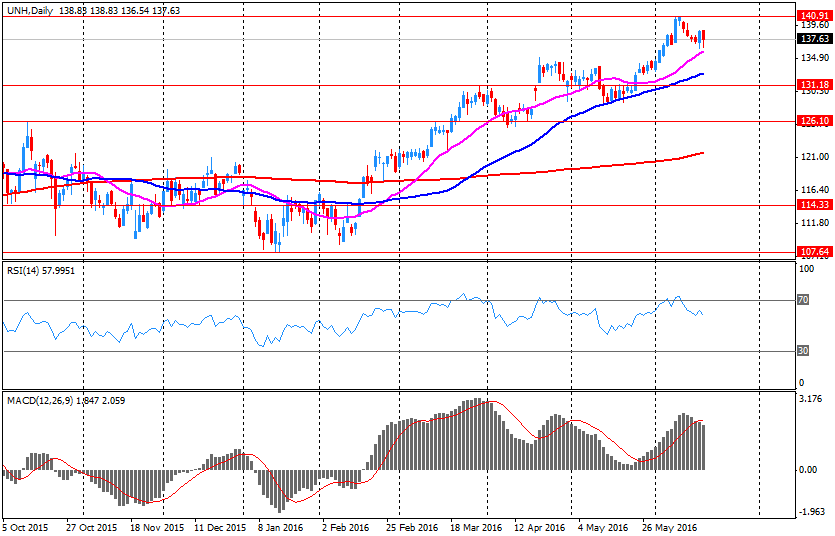

Company News: UnitedHealth (UNH) Q2 results beat analysts’ estimates

UnitedHealth reported Q2 FY 2016 earnings of $1.96 per share (versus $1.64 in Q2 FY 2015), beating analysts' consensus estimate of $1.89.

The company's quarterly revenues amounted to $46.485 bln (+28.2% y/y), beating analysts' consensus estimate of $45.039 bln.

UNH closed Monday's trading session at $140.75 (-0.41%).

-

12:02

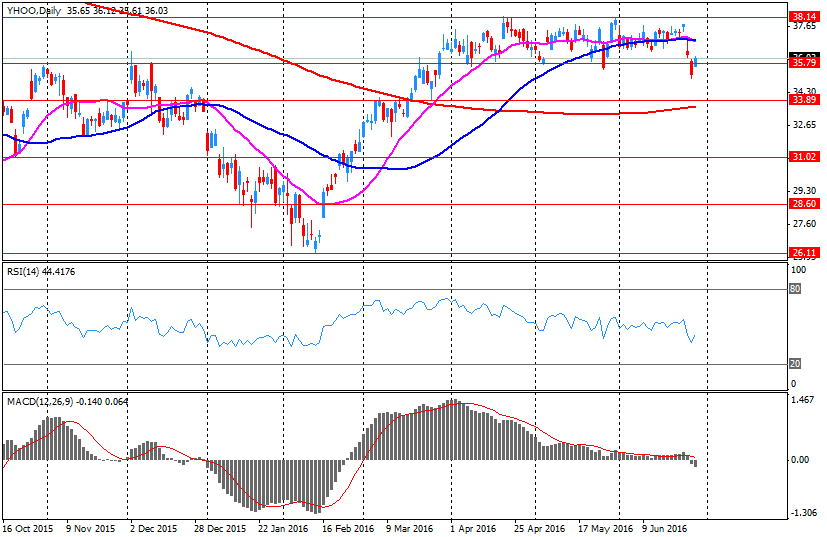

Company News: Yahoo! (YHOO) Q2 earnings miss analysts’ estimates

Yahoo! reported Q2 FY 2016 earnings of $0.09 per share (versus $0.16 in Q2 FY 2015), missing analysts' consensus estimate of $0.10.

The company's quarterly revenues amounted to $0.842 bln (-19.3% y/y), generally in-line with analysts' consensus estimate of $0.837 bln.

YHOO closed Monday's trading session at $37.95 (+0.61%).

-

11:52

UK house price index up 8.1%

-

the average price of a property in the UK was £211,230

-

the annual price change for a property in the UK was 8.1%

-

the monthly price change for a property in the UK was 1.1%

-

the monthly index figure for the UK was 110.8 (January 2015 = 100)

The timing of the stamp duty tax seems to have cooled demand in recent months, but this follows an extended period of increases in activity. Following a 6.2% fall on the month in April 2016, the volume of lending approvals for house purchases recovered slightly, by 1.3% in May. However, approvals on a monthly basis are still below the levels seen in the 10 months before the stamp duty changes. Following a strong increase in sales in the month prior to the stamp duty changes (March 2016), UK home sales fell by 42.3% in April 2016 to their lowest level since May 2013.

-

-

11:50

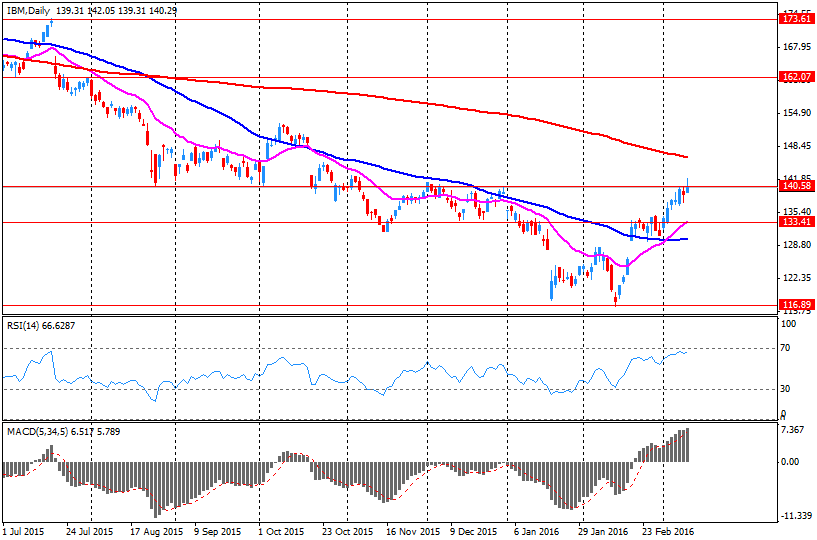

Company News: IBM (IBM) Q2 results beat analysts’ expectations

IBM reported Q2 FY 2016 earnings of $2.95 per share (versus $3.84 in Q2 FY 2015), beating analysts' consensus estimate of $2.89.

The company's quarterly revenues amounted to $20.238 bln (-2.8% y/y), beating analysts' consensus estimate of $20.063 bln.

IBM rose to $161.83 (+1.23%) in pre-market trading.

-

11:34

Germany and EU Economic Sentiment caught up in Brexit Vote. This is how EU and UK data will look like in the next months?

The ZEW Indicator of Economic Sentiment for Germany decreased sharply in July 2016. The index has decreased by 26.0 points compared to the previous month, now standing at minus 6.8 points (long-term average: 243 points). This is the indicator's lowest reading since November 2012. "The Brexit vote has surprised the majority of financial market experts. Uncertainty about the vote's consequences for the German economy is largely responsible for the substantial decline in economic sentiment. In particular, concerns about the export prospectus and the stability of the European banking and financial system are likely to be a burden".

-

11:00

Germany: ZEW Survey - Economic Sentiment, July -6.8 (forecast 9.1)

-

11:00

Eurozone: ZEW Economic Sentiment, July -14.7

-

10:35

Better inflation from UK but the pound's reaction is limited so far

The Consumer Prices Index (CPI) rose by 0.5% in the year to June 2016, compared with a 0.3% rise in the year to May.

The June rate is a little above the position seen for most of 2016, though it is still relatively low historically.

Rises in air fares, prices for motor fuels and a variety of recreational and cultural goods and services were the main contributors to the increase in the rate.

These upward pressures were partially offset by falls in the price of furniture and furnishings and accommodation services.

CPIH (not a National Statistic) rose by 0.8% in the year to June 2016, up from 0.7% in May.

-

10:32

Oil fell moderatly in early trading

This morning, New York crude oil futures for WTI fell 0.22% to $ 45.84 per barrel and Brent oil futures were down 0.17% to $ 46.86 per barrel. Thus, the black gold fell slightly, amid fears of an excess supply on the market. After the coup in Turkey and the overlap of the Bosphorus Strait, traders expected disruptions of oil supplies to the world markets, but their hopes were dashed. Therefore, oversupply of oil, which continues to remain on the market, adversely affect the price. Also, investors are waiting for the American Petroleum Institute data on oil reserves. Analysts expect US stocks of crude oil to decrease by 2.2 million barrels.

-

10:30

United Kingdom: Producer Price Index - Output (YoY) , June -0.4% (forecast -0.5%)

-

10:30

United Kingdom: HICP, Y/Y, June 0.5% (forecast 0.4%)

-

10:30

United Kingdom: Retail prices, Y/Y, June 1.6% (forecast 1.5%)

-

10:30

United Kingdom: HICP, m/m, June 0.2% (forecast 0.1%)

-

10:30

United Kingdom: Producer Price Index - Input (YoY) , June -0.5% (forecast -0.8%)

-

10:30

United Kingdom: Retail Price Index, m/m, June 0.4% (forecast 0.2%)

-

10:30

United Kingdom: Producer Price Index - Input (MoM), June 1.8% (forecast 1.1%)

-

10:30

United Kingdom: HICP ex EFAT, Y/Y, June 1.4% (forecast 1.3%)

-

10:30

United Kingdom: Producer Price Index - Output (MoM), June 0.2% (forecast 0.2%)

-

10:00

Review of financial and economic press: Moody's put Turkey’s rating on review for downgrade

D / W

FAZ: The EU at a crossroads

Kerry: US-EU free trade area can compensate for the damage caused by Brexit

After the decision of the UK to withdraw from the EU Secretary of State John Kerry said the European Union has increased importance of the transatlantic trade and investment partnership agreements (TTIP). Speaking on Monday, July 18 at a meeting of EU foreign ministers in Brussels, Kerry said that the free trade agreement between the US and the European Union could serve as a counterweight to the negative economic consequences of Brexit. According to him, the US administration intends to reach an agreement with the European partners on this issue this year.

newspaper. ru

Bloomberg: Moody's put the rating of Turkey on review for downgrade

International rating agency Moody`s Investors Service placed the long-term credit rating of Turkey to the list of downward revision after the country was in an attempted military coup, Bloomberg writes.

IMF: Inflation in Venezuela in 2017 could exceed 1600%

The rise in prices in Venezuela at the end of this year may reach 480%, and exceeded 1640% next year, writes the Wall Street Journal, referring to the International Monetary Fund (IMF).

Stabilization of the Greek economy

The Greek authorities intend to hold a series of major reforms in the autumn, according to the Ministry of Finance Euclid Tsakalotosa. "The Greek government will conduct major reforms in the autumn. six or seven bills will be introduced, which will help the development of the economy ", - he said after talks with European Commissioner for Economy and Finance Pierre Moscovici.

Bank of America's profit for the second quarter fell by almost 20%

The second-largest US bank, Bank of America (BofA), reported a drop in quarterly profit by 19.4%, Reuters reported with reference to the report of the bank.

-

10:00

Option expiries for today's 10:00 ET NY cut

EUR/USD: 1.0990-1.1000 (EUR 544m) 1.1100 (1.1bln) 1.1145 (356m)

USD/JPY: 105.35-50 (USD 441m)

GBP/USD 1.3200 (GBP 821m) 1.3500 (824m)

EUR/GBP 0.8300 (EUR 596m)

AUD/USD 0.7600 (AUD 380m) 0.7625 (290m)

USD/CAD 1.2960-65 (USD 400m)

NZD/USD 0.7200 (NZD 200m)

-

09:25

Major stock exchanges trading mixed after opening: DAX 10,030.61-32.52-0.32%, FTSE 100 6,681.84 + 12.60 + 0.19%, CAC 40 4,344.65-13.09-0.30%

-

09:14

WSE: After opening

WIG20 index opened at 1787.40 points (-0.04%)*

WIG 46226.05 0.23%

WIG30 2014.84 0.05%

mWIG40 3488.05 -0.09%

*/ - change to previous close

Changes in our environment from yesterday's closing are not too large, therefore, there is also reason for no major shift in the market within the opening. Today, one of the most interesting topics will be whether the relative strength of Polish assets will be shown on, or was it just a one-day stress, perhaps associated with changes in allocation in the basket of Emerging Markets assets at the expense of Turkey.

-

09:14

Citi: Core inflation in Australia in the second quarter will be 0.3%

Citi analysts said that core inflation in Australia in the second quarter will be 0.3%, and this will be enough to convince the Reserve Bank of Australia to cut its key interest rate by 25 basis points at the August meeting.

If inflation goes above this level, the lowering of the rates in August will be less likely, especially given the recent data that pointed to improvement in business sentiment and an increase in the number of jobs to full-time employment.

The ANZ also believe that the RBA will lower the key interest rate in August. "Core inflation in the second quarter is likely to remain low and the labor market has lost momentum in the current year, which could lead to a decrease in the key rate".

-

08:53

Expected negative start of trading on the major stock exchanges in Europe: DAX -0,4%, FTSE 100 -0,3%, CAC 40 -0.2%

-

08:32

Options levels on tuesday, July 19, 2016:

EUR/USD

Resistance levels (open interest**, contracts)

$1.1243 (3761)

$1.1211 (2190)

$1.1163 (1497)

Price at time of writing this review: $1.1072

Support levels (open interest**, contracts):

$1.0983 (3117)

$1.0914 (3749)

$1.0874 (6872)

Comments:

- Overall open interest on the CALL options with the expiration date August, 5 is 36244 contracts, with the maximum number of contracts with strike price $1,1200 (3761);

- Overall open interest on the PUT options with the expiration date August, 5 is 47534 contracts, with the maximum number of contracts with strike price $1,0900 (6872);

- The ratio of PUT/CALL was 1.31 versus 1.36 from the previous trading day according to data from July, 18

GBP/USD

Resistance levels (open interest**, contracts)

$1.3509 (1395)

$1.3412 (1910)

$1.3317 (710)

Price at time of writing this review: $1.3216

Support levels (open interest**, contracts):

$1.3088 (973)

$1.2991 (1390)

$1.2894 (752)

Comments:

- Overall open interest on the CALL options with the expiration date August, 5 is 22759 contracts, with the maximum number of contracts with strike price $1,3400 (1910);

- Overall open interest on the PUT options with the expiration date August, 5 is 20964 contracts, with the maximum number of contracts with strike price $1,2950 (2400);

- The ratio of PUT/CALL was 0.92 versus 0.90 from the previous trading day according to data from July, 18

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

08:22

WSE: Before opening

Yesterday's session in the US ended with minor increases to new records. In Asia, after returning to parquet of Japanese investors, we may see increases on the Tokyo Stock Exchange (the Nikkei index +1,39%). Slightly falling contracts in the US (S&P500 Fut; -0.15%). The morning atmosphere can be assessed as calm, so the session in Warsaw should start at neutral levels.

In today's macro calendar appears the publication of the ZEW index and national data on industrial production and retail sales however investors are waiting for the ECB meeting on Thursday, as central banks are in the center of attention again.

On the Warsaw Stock Exchange today will be cut off rights to dividends from shares of PGNiG (PLN 0.18; dyvidend yield 3.14%), which will have a negative influence on the WIG20 in scale of approx. 0.2%. The WIG20 index yesterday had gone to the psychological level of 1,800 points, which is near a natural resistance. Crossing ot this level will open the way to the peaks of the Brexit referendum.

-

08:19

UK’s CPI is the main event of the day. Although most of the data was compiled before Brexit we will have a clear view about its impacts. Keep an eye on the pound

-

08:16

ECB may keep its dovish policy stance - Citi

The ECB will announce the rate decision this week. Although we expect the ECB may keep the interest rate and monetary policy unchanged, it may keep its dovish policy stance and may announce to extend QE in September, which may undermine EUR.

EUR/USD may find resistance at 1.1199. The pair may range trade between 1.0782-1.1199, with downside bias.

-

08:12

On Thursday, the RBNZ will assess the current economic situation

New Zealand's dollar fell after the Reserve Bank of New Zealand has recently announced its intention to present a new assessment of the economic situation on Thursday.

Analysts at Barclays recommended a sell on NZD/USD this week with the target of $ 0.7005. "On Thursday, the RBNZ will assess the current economic situation, and, according to our forecast, in the eve of this event, the kiwi will remain under pressure". The new assessment of the economic situation may create conditions for lowering rates at the next meeting of the RBNZ, which takes place on August 11th.

Commonwealth Bank of Australia said that NZD/USD, may be strong despite the prospect of further rate cut and expect to finds support in $ 0.6900 area.

-

08:07

Reserve Bank of Australia meeting minutes: Inflation will remain low for quite some time

- we watch the economic data and especially data on inflation, housing market, employment, to determine when it is necessary to change rates

- labor costs are very low

- housing market indicators in recent years have been mixed

- employment data more ambiguous

- commodity prices have strengthened, the Australian dollar exchange rate in line with expectations

- revision of the forecasts in August will help to identify the policy rate

-

08:03

Reserve Bank of New Zealand proposed changes to loan-to-value restrictions

The Reserve Bank of New Zealand proposed changes to loan-to-value restrictions to mitigate risks from financial stability stemming from property overheating.

In a consultation paper, released Tuesday, the bank said investors should deposit at least 40 for a home loan.

"No more than 5 percent of bank lending to residential property investors across New Zealand would be permitted with an LVR of greater than 60 percent," the bank said.

The proposed restriction is set to simplify the LVR policy by removing the current distinction between lending in Auckland and the rest of the country.

The banking system is heavily exposed to the property market and investor lending has been increasing rapidly, RBNZ Governor Graeme Wheeler said. The proposed restrictions recognize the higher risks associated with such lending, he added.

Wheeler observed that a sharp correction in house prices is a key risk to the financial system, and there are clear signs that this risk is increasing across the country.

The consultations will conclude on August 10 and new restrictions will take effect on September 1.

-

07:03

Global Stocks

European stocks finished mostly higher Monday, led by ARM Holdings PLC soaring on the chip designer's $32 billion buyout deal.

But Turkish shares closed down in the wake of a failed military coup.

The Stoxx Europe 600 SXXP, +0.23% rose 0.2% to end at 338.70, after the pan-European index on Friday slipped 0.2%.

U.S. stocks eked out small gains Monday, pushing both the Dow Jones Industrial Average and the S&P 500 Index to fresh all-time closing highs and the Nasdaq Composite Index to its highest finish of 2016.

The S&P 500 SPX, +0.24% traded within a narrow 8-point range and closed up 5.15 points, or 0.2%, at 2,166.89, a new closing high, led by gains in tech, materials and financials.

The Dow industrials DJIA, +0.09% closed at a new high for the fifth day in a row while trading within a 66-point range.

The Nasdaq Composite Index COMP, +0.52% rose 26.19 points, or 0.5%, to close at 5,055.78, after trading within a 33-point range. The Nasdaq is up 1% for the year.

Stocks got a boost by a flurry of upbeat earnings reports from financial companies, most notably Bank of America Corp. BAC, +3.29%

Asian shares slipped on Tuesday, as a downturn in crude oil curbed the enthusiasm from fresh record highs on Wall Street.

China stocks were lower, with both the CSI300 index .CSI300 of the largest listed companies in Shanghai and Shenzhen and the Shanghai Composite Index .SSEC down 0.4 percent.

Japan's Nikkei stock index .N225 pared early gains but was still up 0.5 percent, as markets reopened after a public holiday on Monday and responded to a weaker yen.

In the previous week, the benchmark index had gained 9.2 percent to notch its biggest weekly gain since December 2009, helped by Wall Street as well as hopes that the Bank of Japan will deliver further stimulus as early as its next policy meeting later this month.

Japanese policymakers won't go as far as funding government spending through direct debt monetization, but might pursue a mix of aggressive fiscal and monetary expansion to battle deflation, according to sources familiar with the matter.

A failed coup in Turkey had dented risk sentiment and bolstered the perceived safe-haven yen before it ran its course. On Monday, Turkey purged its police force after rounding up thousands of soldiers and called for the United States to hand over a cleric that the Turkish government accuses of being behind the takeover attempt.

-

04:04

Nikkei 225 16,539.67 +41.82 +0.3 %, Hang Seng 21,663.45 -139.73 -0.6 %, Shanghai Composite 3,040.6 -2.96 -0.1 %

-

00:33

Commodities. Daily history for Jul 18’2016:

(raw materials / closing price /% change)

Oil 45.20 -0.09%

Gold 1,329.10 -0.02%

-

00:32

Stocks. Daily history for Jun Jul 18’2016:

(index / closing price / change items /% change)

Hang Seng 21,803.18 +143.93 +0.66 %

S&P/ASX 200 5,458.47 +28.90 +0.53 %

Shanghai Composite 3,043.91 -10.39 -0.34 %

FTSE 100 6,695.42 +26.18 +0.39 %

CAC 40 4,357.74 -14.77 -0.34 %

Xetra DAX 10,063.13 -3.77 -0.04 %

S&P 500 2,166.89 +5.15 +0.24 %

NASDAQ Composite 5,055.78 +26.20 +0.52 %

Dow Jones 18,533.05 +16.50 +0.09 %

-

00:31

Currencies. Daily history for Jul 18’2016:

(pare/closed(GMT +3)/change, %)

EUR/USD $1,1073 +0,34%

GBP/USD $1,3249 +0,50%

USD/CHF Chf0,9822 +0,01%

USD/JPY Y106,13 +1,20%

EUR/JPY Y117,52 +1,56%

GBP/JPY Y140,61 +1,68%

AUD/USD $0,7578 +0,05%

NZD/USD $0,7052 -0,88%

USD/CAD C$1,295 -0,12%

-

00:03

Schedule for today, Tuesday, Jul 19’2016:

(time / country / index / period / previous value / forecast)

01:30 Australia RBA Meeting's Minutes

08:30 United Kingdom Producer Price Index - Output (MoM) June 0.1% 0.2%

08:30 United Kingdom Producer Price Index - Output (YoY) June -0.7% -0.5%

08:30 United Kingdom Producer Price Index - Input (MoM) June 2.6% 1.1%

08:30 United Kingdom Producer Price Index - Input (YoY) June -3.9% -0.8%

08:30 United Kingdom Retail Price Index, m/m June 0.3% 0.2%

08:30 United Kingdom Retail prices, Y/Y June 1.4% 1.5%

08:30 United Kingdom HICP, m/m June 0.2% 0.1%

08:30 United Kingdom HICP ex EFAT, Y/Y June 1.2% 1.3%

08:30 United Kingdom HICP, Y/Y June 0.3% 0.4%

09:00 Eurozone ZEW Economic Sentiment July 20.2

09:00 Germany ZEW Survey - Economic Sentiment July 19.2 9.1

12:30 U.S. Housing Starts June 1164 1170

12:30 U.S. Building Permits June 1138 1150

-