Noticias del mercado

-

21:00

DJIA 18507.75 -39.55 -0.21%, NASDAQ 5232.23 -27.85 -0.53%, S&P 500 2179.54 -7.36 -0.34%

-

18:00

European stocks closed: FTSE 6835.78 -32.73 -0.48%, DAX 10622.97 30.09 0.28%, CAC 4435.47 14.02 0.32%

-

17:52

Oil fell on US stocks data

Oil prices continued to fall after the US Department's of Energy weekly data showed an increase in total reserves of oil and petroleum products to a new record high.

Inventory data for the week of 13-19 August grew by 6.6 million barrels to 1.4 billion barrels, and it signals the preservation of oversupply in the market.

In the reporting week, US crude oil inventories rose by 2.5 million barrels, while analysts had expected a small decrease in stocks.

Inventories of gasoline, distillates (including diesel) propane and ethanol also rose.

Total stocks of oil and oil products "all continue to grow," stated Jim Ritterbusch of Ritterbusch & Associates. Usually at this time of the year crude oil stocks are reduced, since refineries are actively processed oil into gasoline to meet demand. "This growth is unusual," - added the analyst.

US domestic oil production fell to 49,000 barrels a day to 8.5 million barrels a day. Last week production unexpectedly rose, but the Energy Information Administration Energy explained this by a "change in algorithm".

On Tuesday, oil prices rose amid reports that Iran intends to participate in the OPEC meeting scheduled for September, to discuss coordinated production constraints. Similar negotiations that took place in April, ended without result, because Iran refused to limit production.

Many analysts still showing skepticism about Iran's participation in the agreement.

The cost of the October futures for US light crude oil WTI fell to 46.45 dollars per barrel.

October futures price for North Sea petroleum mix of Brent crude rose to 48.68 dollars a barrel on the London Stock Exchange ICE Futures Europe.

-

17:39

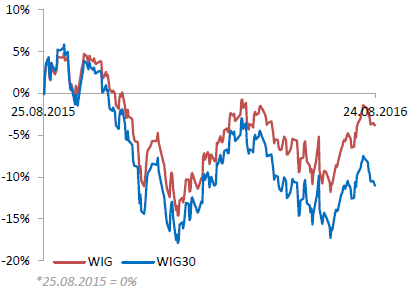

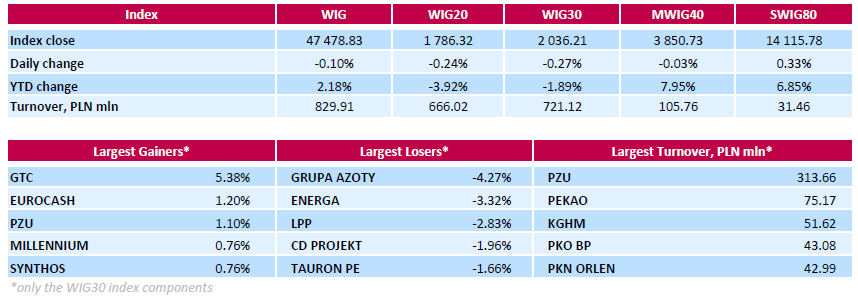

WSE: Session Results

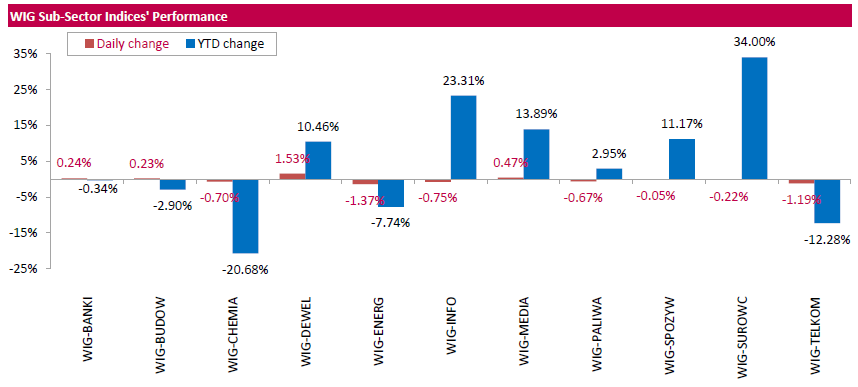

Polish equity market closed lower on Wednesday. The broad market benchmark, the WIG Index, fell by 0.1%. Sector performance in the WIG Index was mixed. Utilities (-1.37%) recorded the biggest decline, while developing sector (+1.53%) outpaced.

The large-cap stocks' measure, the WIG30 Index, lost 0.27%. In the index basket, chemical producer GRUPA AZOTY (WSE: ATT) tumbled the most, down 4.27%, as the company posted lower-than-expected Q2 earnings. Its net income amounted to PLN 44.4 mln in Q2, down 62.6% y/y and well below analysts' consensus estimate of PLN 118.8 mln. Meanwhile, the company's revenues fell by 5.2% y/y to PLN 2.16 bln in Q2, but beat analysts' consensus estimate of PLN 2.04 bln. Given weak Q2 earnings, GRUPA AZOTY cut its FY16 capital expenditure target by 20% to PLN 1.6 bln. Other major decliners were genco ENERGA (WSE: ENG), clothing retailer LPP (WSE: LPP) and videogame developer CD PROJEKT (WSE: CDR), plunging by 3.32%, 2.83% and 1.96% respectively. On the other side of the ledger, property developer GTC (WSE: GTC) led the gainers, climbing by 5.38%, as the company's quarterly financial report revealed it returned to profit in the Q2, helped by lower financial costs and revaluation of assets and real estate development projects. GTC posted net income for Q2 of EUR 18.8 mln, a turnaround from a loss of EUR 1.9 mln for the same three-month period last year. The bottom-line result was generally in-line with analysts' consensus estimate of EUR 18.3 mln.

-

17:29

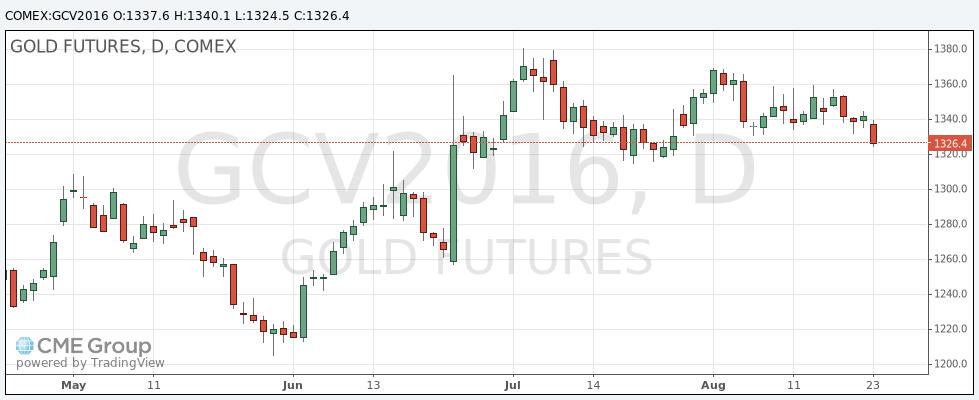

Gold price decrease today

Gold prices fell to 4 weeks low as investors closed their positions on the background of the Jackson Hole meeting on friday.

Traders are waiting for the symposium during which will Fed Chairwoman Janet Yellen will deliver a speech. It is expected that signals about the possible timing of the Fed's interest rate increase can be served at the event. The market does not expect an immediate increase in interest rates, but any surprises in the speech may catch investors off guard and put pressure on the gold market.

A stronger dollar also makes gold prices which are set in US currency less attractive for holders of other currencies.

The dollar index, which tracks the US currency against a basket of other currencies, rose 0.1% to 85.79.

In preparation for the Fed symposium investors reduce the number of positions said Peter Hug from Kitco Metals.

"Traders may be too carried away with long positions now and not want to be caught off guard and thus closed some bets." - adds Hag.

Since the beginning of the year the price of gold rose more than 25%, as the comments from the central bank contributed to the reduction of expectations of rising interest rates, and investors preferred to invest money in safe-haven assets.

The cost of the October futures on COMEX rose to $ 1,324.50 an ounce.

-

17:24

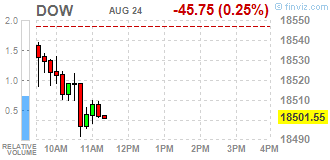

Wall Street. Major U.S. stock-indexes little changed

Major U.S. stock-indexes little changed on Wednesday as investors kept up their wait for Federal Reserve Chair Janet Yellen's speech on Friday for clues on the timing of an interest rate hike.

Most of Dow stocks in negative area (21 of 30). Top gainer - NIKE, Inc. (NKE, +0.92%). Top loser - Verizon Communications Inc. (VZ, -0.80%).

S&P sectors also in negative area. Top loser - Basic Materials (-0.7%).

At the moment:

Dow 18484.00 -44.00 -0.24%

S&P 500 2180.75 -4.50 -0.21%

Nasdaq 100 4809.50 -7.50 -0.16%

Oil 46.80 -1.30 -2.70%

Gold 1329.90 -16.20 -1.20%

U.S. 10yr 1.56 +0.01

-

17:23

Gunmen Storm American University In Afghanistan In Kabul: Explosions, Gunfire Ongoing - Zerohedge

-

16:38

US crude oil inventories way above forecasts. Oil trading lower

U.S. crude oil refinery inputs averaged 16.7 million barrels per day during the week ending August 19, 2016, 186,000 barrels per day less than the previous week's average. Refineries operated at 92.5% of their operable capacity last week. Gasoline production decreased last week, averaging over 10.0 million barrels per day. Distillate fuel production decreased last week, averaging over 4.8 million barrels per day.

U.S. crude oil imports averaged over 8.6 million barrels per day last week, up by 449,000 barrels per day from the previous week. Over the last four weeks, crude oil imports averaged 8.5 million barrels per day, 13.3% above the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) last week averaged 801,000 barrels per day. Distillate fuel imports averaged 224,000 barrels per day last week. U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 2.5 million barrels from the previous week. At 523.6 million barrels,

U.S. crude oil inventories are at historically high levels for this time of year. Total motor gasoline inventories remained unchanged last week, and are well above the upper limit of the average range. Finished gasoline inventories increased while blending components inventories decreased last week. Distillate fuel inventories increased by 0.1 million barrels last week and are near the upper limit of the average range for this time of year. Propane/propylene inventories rose 2.4 million barrels last week and are above the upper limit of the average range. Total commercial petroleum inventories increased by 6.6 million barrels last week.

-

16:30

U.S.: Crude Oil Inventories, August 2.501 (forecast -0.85)

-

16:05

US existing home sales declined hard

According to the National Association of Realtors, slowed by frustratingly low inventory levels in many parts of the country, existing-home sales lost momentum in July and decreased year-over-year for the first time since November 2015. Only the West region saw a monthly increase in closings in July.

Total existing-home sales, which are completed transactions that include single-family homes, townhomes, condominiums and co-ops, fell 3.2 percent to a seasonally adjusted annual rate of 5.39 million in July from 5.57 million in June. For only the second time in the last 21 months, sales are now below (1.6 percent) a year ago (5.48 million).

-

16:00

U.S.: Existing Home Sales , July 5.39 (forecast 5.51)

-

15:47

Option expiries for today's 10:00 ET NY cut

EURUSD 1.1100, 1.1160/65/70 (650m), 1.1190 1.1200/05, 1.1270 1.1375 1.1450

USDJPY 98.20 99.95 100.75 101.00 102.25/30

GBPUSD 1.2880 1.3400

AUDUSD 0.7435/40, 0.7450, 0.7460/65

NZDUSD 0.7325 (318m)

USDCHF 0.9715/20 0.9875/80

EURCHF 1.0700 1.0825

-

15:47

WSE: After start on Wall Street

Behind us quiet neutral opening on Wall Street. No major shift seems to be a good strategy when the markets are waiting for Janet Yellen speech in Jackson Hole. The S&P500 index consolidates in the area of records in the trend and a week before the end of the month has not sinned with force and rather looking for tranquility. The opening in America did not affect in any way the quotation on the Warsaw market. For about an hour before the end of the session the WIG20 index was at the level of 1,782 points (-0.48%).

-

15:32

U.S. Stocks open: Dow -0.15%, Nasdaq -0.12%, S&P -0.11%

-

15:27

Before the bell: S&P futures +0.02%, NASDAQ futures +0.07%

U.S. stock-index futures were little changed as investors awaited Friday's speech from Federal Reserve Chair Janet Yellen for clues on when to expect higher borrowing costs.

Global Stocks:

Nikkei 16,597.30 +99.94 +0.61%

Hang Seng 22,820.78 -178.15 -0.77%

Shanghai 3,085.82 -3.88 -0.13%

FTSE 6,852.33 -16.18 -0.24%

CAC 4,449.92 +28.47 +0.64%

DAX 10,647.13 +54.25 +0.51%

Crude $47.29 (-1.68%)

Gold $1336.60 (-0.71%)

-

15:13

US house price index up 0.2% in June

U.S. house prices rose 1.2 percent in the second quarter of 2016 according to the Federal Housing Finance Agency (FHFA) House Price Index (HPI). House prices rose 5.6 percent from the second quarter of 2015 to the second quarter of 2016. FHFA's seasonally adjusted monthly index for June was up 0.2 percent from May.

Home prices rose in every state except Vermont between the second quarter of 2015 and the second quarter of 2016. The top five states in annual appreciation were: 1) Oregon 11.7 percent; 2) Washington 10.3 percent; 3) Colorado 10.2 percent; 4) Florida 10.0 percent; and 5) Nevada 9.6 percent.

Among the 100 most populated metropolitan areas in the U.S., annual price increases were greatest in North Port-Sarasota-Bradenton, FL, where prices increased by 15.7 percent. Prices were weakest in Bridgeport-Stamford-Norwalk, CT, where they fell 3.3 percent.

-

15:10

Belgium’s business barometer dropped sharply in August

The National Bank of Belgium's business barometer dropped sharply in August, offsetting the improvement of the business climate recorded in the previous two months.

The business climate declined in all branches of activity.

In the manufacturing industry business pessimism showed in all components, but especially as to the assessment of overall order books.

After three consecutive improvements, business climate deteriorated in the business-related services. The recent development of activity was held to be far more negatively and expectations regarding firms' own activity proved to be less bright as well.

In the building industry the loss of confidence was due to the sharp fall in new orders received and to a far more unfavourable assessment of the overall order books

The further decline of confidence in trade is due mainly to the sharp deterioration in the prospects as to employment. Inaddition, demand expectations continued to worsen

-

15:01

U.S.: Housing Price Index, m/m, June 0.2% (forecast 0.3%)

-

15:00

Belgium: Business Climate, August -3.1 (forecast 1)

-

14:57

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

3M Co

MMM

179.77

0.00(0.00%)

60466

ALCOA INC.

AA

10.43

-0.07(-0.6667%)

1603

ALTRIA GROUP INC.

MO

66.5

0.04(0.0602%)

133526

Amazon.com Inc., NASDAQ

AMZN

762.98

0.53(0.0695%)

2995

American Express Co

AXP

65.65

-0.03(-0.0457%)

300

AMERICAN INTERNATIONAL GROUP

AIG

59.02

0.00(0.00%)

128505

Apple Inc.

AAPL

108.96

0.11(0.1011%)

12685

AT&T Inc

T

40.85

-0.00(-0.00%)

551

Barrick Gold Corporation, NYSE

ABX

19.89

-0.20(-0.9955%)

88662

Boeing Co

BA

134.14

0.00(0.00%)

36686

Caterpillar Inc

CAT

84.01

0.00(0.00%)

519

Chevron Corp

CVX

101.16

-0.52(-0.5114%)

2600

Cisco Systems Inc

CSCO

30.92

-0.06(-0.1937%)

240

Citigroup Inc., NYSE

C

46.68

0.09(0.1932%)

3427

Deere & Company, NYSE

DE

87.9

-0.19(-0.2157%)

1456

E. I. du Pont de Nemours and Co

DD

70.425

-0.015(-0.0213%)

45798

Exxon Mobil Corp

XOM

87.58

-0.14(-0.1596%)

794

Facebook, Inc.

FB

124.52

0.15(0.1206%)

18458

FedEx Corporation, NYSE

FDX

168.59

0.00(0.00%)

11857

Ford Motor Co.

F

12.39

-0.03(-0.2415%)

6105

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

11.85

-0.13(-1.0851%)

110735

General Electric Co

GE

31.29

0.06(0.1921%)

3865

General Motors Company, NYSE

GM

31.85

-0.05(-0.1567%)

296120

Goldman Sachs

GS

166.1

0.02(0.012%)

3257

Google Inc.

GOOG

771.13

-0.95(-0.123%)

59684

Hewlett-Packard Co.

HPQ

14.64

0.07(0.4804%)

2748

Home Depot Inc

HD

135.8

-0.42(-0.3083%)

2663

HONEYWELL INTERNATIONAL INC.

HON

116.81

-0.20(-0.1709%)

200

Intel Corp

INTC

35.31

-0.09(-0.2542%)

219

International Business Machines Co...

IBM

160.26

0.00(0.00%)

71104

International Paper Company

IP

46.96

0.00(0.00%)

49149

Johnson & Johnson

JNJ

119.44

0.00(0.00%)

294876

JPMorgan Chase and Co

JPM

65.77

0.00(0.00%)

222243

McDonald's Corp

MCD

115.2

0.01(0.0087%)

750

Merck & Co Inc

MRK

63.64

0.06(0.0944%)

261822

Microsoft Corp

MSFT

57.9

0.01(0.0173%)

5849

Nike

NKE

59.84

0.22(0.369%)

7307

Pfizer Inc

PFE

35.33

0.24(0.684%)

5792

Procter & Gamble Co

PG

87.59

0.19(0.2174%)

180

Starbucks Corporation, NASDAQ

SBUX

56.86

0.46(0.8156%)

25501

Tesla Motors, Inc., NASDAQ

TSLA

226

1.16(0.5159%)

8398

The Coca-Cola Co

KO

43.9

0.05(0.114%)

1967

Travelers Companies Inc

TRV

116.63

0.00(0.00%)

25934

Twitter, Inc., NYSE

TWTR

18.79

0.10(0.5351%)

30241

United Technologies Corp

UTX

108.03

0.03(0.0278%)

43919

UnitedHealth Group Inc

UNH

142

-0.01(-0.007%)

150

Verizon Communications Inc

VZ

52.64

0.01(0.019%)

2924

Visa

V

80.96

0.16(0.198%)

2200

Wal-Mart Stores Inc

WMT

72.12

0.15(0.2084%)

1852

Walt Disney Co

DIS

96

0.03(0.0313%)

350

Yahoo! Inc., NASDAQ

YHOO

42.53

-0.07(-0.1643%)

658

Yandex N.V., NASDAQ

YNDX

22.44

0.00(0.00%)

1125

-

14:19

European session review: the pound continues to rise against the dollar

The following data was published:

(Time / country / index / period / previous value / forecast)

6:00 Germany GDP q / q (final data) II quarter 0.7% 0.4% 0.4%

6:00 Germany GDP y / y (final data) II quarter 1.5% 3.1% 3.1%

8:30 UK approved applications for mortgage loans on the BBA figures, thousand. July 39.76 37.66 38.5

The dollar rose strongly against the euro, approaching a week high, helped by expectations of Friday's speech by Fed Janet Yellen, which may shed light on the prospects of the Fed's monetary policy. Investors still believe the rate hike this year is unlikely against the backdrop of weak data on production and GDP. However, recent comments by Fed leaders have increased the likelihood of further rate hikes. According to the futures market, the probability of Fed rate increase in September is 18% against 21% the previous day and at the December meeting is estimated at 43.1% versus 41.1% yesterday.

A slight impact on the course of trading has also provided statistics for Germany. The final report, published by the Statistical Office Destatis, showed that the German economy in the 2nd quarter increased by 0.4% compared to the previous three months, when GDP grew by 0.7%. In annual terms, the economy has added 3.1%. The last change (as in the quarterly and on an annual basis) in line with expectations. At the end of the 2nd quarter, German exports increased by 1.2% and imports decreased by 0.1%. Meanwhile, consumer spending rose by 0.2% after rising 0.3% in the 1st quarter.

Later today, the focus will be on housing sales in the secondary market in the US, which may well turn out to be quite strong as yesterday's statistics on sales of new buildings.

The pound has appreciated significantly against the dollar, updating the 3-week high. The catalyst for such dynamics was renewed fall in EUR / GBP. At the same time, data from the British Bankers Association (BBA), showed that the number of approved applications for mortgage loans decreased by the end of July, reaching its lowest level since the beginning of 2015. According to the report, the number of approved mortgage loans decreased in to a level of 37,662 units compared to 39,763 units in June (revised from 40,100). The latter figure was the lowest since January 2015, when the number of mortgage approvals was 36,649 units. In addition, it was reported that the number of permits approved for house purchase was approximately 19% lower than in July 2015. The total volume of mortgage loans amounted was 12.6 billion pounds, an increase of 6% compared with July last year. Meanwhile, consumer loans continued to show an annual growth of more than 6%, reflecting strong retail sales and, in the case of personal loans and overdrafts, favorable interest rates.

EUR / USD: during the European session, the pair fell to $ 1.1255

GBP / USD: during the European session, the pair has risen to $ 1.3248

USD / JPY: during the European session, the pair fell to Y100.08 and then rebounded

-

14:04

Bundesbank's member, Dombret: main reason for weakness of German banks is the high uncertainty about their structural profitability

-

banks should cut costs and work on their business model to adapt to the new environment

-

banks are right to consider imposing account fees, charge on deposits unlikely to become widespread

-

the drope in German banks' market cap is a reason for concern

-

-

13:50

Orders

EUR/USD

Offers 1.1300 1.1320-25 1.1350-55 1.1380-85 1.1400 1.1425-30 1.1450

Bids 1.1280 1.1250 1.1230 1.1200 1.1185 1.1150 1.1130 1.1100

GBP/USD

Offers 1.3200 1.3230-25 1.3250 1.3280 1.3300 1.3320 1.3350

Bids 1.3160 1.3150 1.3130 1.3100 1.3085 1.3050 1.3025-30 1.3000

EUR/GBP

Offers 0.8580 0.8600 0.8625-30 0.8655-60 0.8685 0.8700

Bids 0.8550 0.8530 0.8500 0.8480 0.8465 0.8450

EUR/JPY

Offers 113.60 113.80 114.00 114.30 114.50 114.75 115.00

Bids 113.00 112.75-80 112.50 112.30 112.00-10

USD/JPY

Offers 100.50 100.85 101.00 101.25-30 101.50 101.75-80 102.00

Bids 100.20 100.00 99.85 99.6599.50 99.30 99.00 98.80 98.50

AUD/USD

Offers 0.7620-25 0.7650-55 0.7680 0.7700 0.7725-30 0.7750-55

Bids 0.7600 0.7585 0.7565 0.7550 0.7500

-

13:06

WSE: Mid session comment

The morning trading phase brought recovery on European markets. The market in Frankfurt rebounded from a session bottom of around 1 percent and helps bulls in Warsaw. On the Warsaw market is worth to note reflection on PZU and Pekao shares. These leaders of the morning supply grow by approx. 1 per cent and correct a negative impact of Tuesday's session. Investor activity focuses today on the values of PZU, which account for almost half of today's trading on the WIG20. As we approach the mid-session, the demand side has become more daring. Contribute to the general sentiment is also persistent approach in Euroland.

In the mid-session, the WIG20 index was at the level of 1,788 points (-0.13%) and with the turnover of PLN 300 million.

-

13:02

Major stock indices in Europe little changed

European stock indices show a predominantly positive trend, heading to third consecutive session increases. The growth of indices helps to gradually improve investor confidence.

The final report, published by the Statistical Office Destatis, showed that the German economy in the 2nd quarter increased by 0.4% compared to the previous three months, when GDP grew by 0.7%. In annual terms, the economy has added 3.1%. The last change (as in the quarterly and on an annual basis) in line with expectations. At the end of the 2nd quarter, German exports increased by 1.2% and imports decreased by 0.1%. Meanwhile, consumer spending rose by 0.2% after rising 0.3% in the 1st quarter.

A certain pressure on the index has decline of oil prices, due to concerns about growth in US oil inventories. Recent data from API revealed that for the past week US crude inventories rose by 4.5 mln barrels. Analysts had forecast a decline to 0.5 mln barrels. Gasoline inventories fell by 2.2 million barrels, while distillates -. 834 million barrels.. Later, the official statistics from the US Department of Energy will be released today. It is predicted that crude oil inventories fell by 0.85 million barrels

The composite index of Europe's largest enterprises Stoxx 600 added 0.5 percent. volatility gauge shows the minimum monthly fluctuations since March 2015, as traders await clarity from the Fed regarding the prospects for a rate hike.

While most industry groups showing growth, shares of commodity producers falling on the background of the renewed drop in oil prices.

Quotes of Glencore Plc tumbled 5.7 percent after the company reported a drop in profit margins in the first half of this year.

The cost of Svenska Cellulosa AB increased by 11 percent on news that the company will be divided into two parts.

Shares of H. Lundbeck A / S rose 2.5 percent after the Danish pharmaceutical company raised its forecasts for sales and earnings for 2016.

Price of WPP Plc shares increased by 5.6 percent as sales beat forecasts in the first half.

At the moment:

FTSE 100 6852.59 -15.92 -0.23%

DAX +26.68 10619.56 + 0.25%

CAC 40 +19.74 4441.19 + 0.45%

-

11:37

-

11:35

Reserve Bank of South Africa: too much inflation to lower rates

- South Africa running out of room to borrow

- less nominal wage pressure on prices would help lower CPI

- government has duty to support the unemployed

- underlying inflation "reasonably well contained"

- local institutions could be less hostile to small firms

*via forexlive

-

10:38

UK, BBA: Data does not currently suggest borrowing patterns have been significantly affected by the Brexit vote

- Gross mortgage borrowing of £12.6bn in the month was 6% higher than in July 2015.

- Net mortgage borrowing is 3% higher than a year ago.

- Consumer credit continues to show annual growth of over 6% reflecting strong retail sales and in the case of personal loans and overdrafts favourable interest rates.

Dr Rebecca Harding, BBA Chief Economist, said:

"This month's BBA High Street Banking statistics are the first set of borrowing figures gathered since the EU referendum. The data does not currently suggest borrowing patterns have been significantly affected by the Brexit vote, but it is still early days. Many borrowing decisions will also have been taken before the referendum vote."

-

10:31

United Kingdom: BBA Mortgage Approvals, July 37.66 (forecast 38.5)

-

10:29

Turkish tanks reported to have crossed into Syria in offensive to drive IS from border area - BBC

-

10:27

Oil is trading lower

This morning, New York crude oil futures for WTI fell by 1.50% to $ 47.37 and Brent oil futures were down -1.18% to $ 49.35 per barrel. Thus, the black gold is trading lower on the background of growth in US oil inventories, which put pressure on the market, along with fears of slowing demand in China. Beijing will take measures in respect of the alleged tax evasion in the petroleum industry. Growing demand in China supported by independent refiners, who have started to import oil in June 2015, received a quota and license from the government. US crude stocks rose last week, according to the American Petroleum Institute, reinforcing concern about the market glut.

-

10:03

Option expiries for today's 10:00 ET NY cut

EUR/USD 1.1100, 1.1160/65/70 (650m), 1.1190,1.1200/05, 1.1270,1.1375, 1.1450

USD/JPY 98.20,99.95,100.75,101.00,102.25/30

GBP/USD 1.2880,1.3400

AUD/USD 0.7435/40, 0.7450, 0.7460/65

NZD/USD 0.7325 (318m)

USD/CHF 0.9715/20,0.9875/80

EUR/CHF 1.0700, 1.0825

-

09:55

EUR/USD: En-Route To 1.16; USD/JPY: En-Route To 97 - Morgan Stanley

"USD levels keeping us bearish: We continue to expect further 4% weakness in USD on the Fed's broad trade-weighted measure. The DXY has failed to break back into a trend channel formed since June, with the lower end around 94.80. Staying below the 95.30 area should keep the bearish momentum for USD.

One of our favourite ways to play for USD weakness is via EUR. From a technical basis, EURUSD is currently behaving in textbook fashion, and we think shouldn't be met with much resistance when going through the 1.14 level. We still target 1.16 for the end of this quarter. Dovish academic debate on the shape of future monetary policy from the Fed should support our currency views.

The Fed and inflation: To analyse USD we are paying particular attention to the relationship between market expectations for the pace of rate hikes (MSP0KE Index) and the US 5y5y inflation swap. Any hawkish Fed commentary in the coming weeks would lower inflation expectations from their already weak 1.9%Y level. Hawkish commentary could also weaken the equity market, which could then drive the Fed towards a less hawkish tone. The dynamic we describe and commentary this week should show how trapped the Fed is. The Fed's Williams' suggestion to raise rates and the inflation target should flatten the curve and thus weaken USD. Implicitly he wants to lower the terminal real rate by aiming for a higher inflation target. The fact that inflation expectations are not moving higher, currently at 1.9%Y, suggests that the market regards the Williams paper as a theoretical exercise with no practical impact yet. USD should weaken should the higher inflation targeting debate gain substance in Jackson Hole.

What a weak USD means for JPY: We are still expecting USDJPY to reach 97 this quarter with the current Fed-driven dynamic working more on the USD side of this pair. Local risk-supportive ETF purchases by the BoJ are now causing a large divergence between the currency and equity markets. We think this dynamic can continue as long as the BoJ doesn't cut rates, something our economists now expect, and so doesn't have a large negative impact on the Japanese banks. Japan's Kyodo newspaper reporting that an extra JPY 4.5 trillion of spending was to be approved in a second budget had little impact on USDJPY as it appeared to be another case of repackaging old announcements".

Copyright © 2016 Morgan Stanley, eFXnews

-

09:45

Major stock exchanges began trading mixed: FTSE 100 6,832.55 + 4.01 + 0.06%, DAX 10,521.32-71.56-0.68%

-

09:18

WSE: After opening

WIG20 index opened at 1787.89 points (-0.15%)*

WIG 47376.54 -0.31%

WIG30 2031.57 -0.50%

mWIG40 3840.91 -0.29%

*/ - change to previous close

The September futures series on the WIG20 index (WSE: FW20U1620) started the day losing 0.2 per cent which was affected by moderate cons on European contracts. The Deputy Prime Minister and Development Minister Mateusz Morawiecki announced today that PZU and Polish Development Fund will not conduct negotiations on the purchase of Pekao shares from UniCredit, although it does not reduce the pressure of the supply on yesterday's negative hero - PZU. That company is responsible now for a half of the turnover in the index and it shows that, at least in the first phase of the session, the PZU will determine the mood in the WIG20. Technically looking drop of the WIG20 into area of 1,788 points means that the index draws new downward wave lows.

-

09:01

Today’s events:

At 17:00 GMT the United States will hold an auction of 5-year bonds

-

08:27

Options levels on wednesday, August 24, 2016:

EUR/USD

Resistance levels (open interest**, contracts)

$1.1445 (4612)

$1.1388 (4592)

$1.1352 (4407)

Price at time of writing this review: $1.1292

Support levels (open interest**, contracts):

$1.1230 (2397)

$1.1200 (1918)

$1.1165 (2765)

Comments:

- Overall open interest on the CALL options with the expiration date September, 9 is 52875 contracts, with the maximum number of contracts with strike price $1,1250 (4901);

- Overall open interest on the PUT options with the expiration date September, 9 is 57718 contracts, with the maximum number of contracts with strike price $1,1000 (5763);

- The ratio of PUT/CALL was 1.09 versus 1.08 from the previous trading day according to data from August, 23

GBP/USD

Resistance levels (open interest**, contracts)

$1.3404 (2371)

$1.3307 (2864)

$1.3211 (1706)

Price at time of writing this review: $1.3167

Support levels (open interest**, contracts):

$1.3093 (1003)

$1.2996 (2035)

$1.2898 (1943)

Comments:

- Overall open interest on the CALL options with the expiration date September, 9 is 32575 contracts, with the maximum number of contracts with strike price $1,3300 (2864);

- Overall open interest on the PUT options with the expiration date September, 9 is 26355 contracts, with the maximum number of contracts with strike price $1,2800 (2675);

- The ratio of PUT/CALL was 0.81 versus 0.82 from the previous trading day according to data from August, 23

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

08:26

WSE: Before opening

Tuesday's session on Wall Street ended with modest increases in the major indexes. The main ones gained from 0.1 to 0.3 percent and the wide S&P500 having increased by 0.2 percent. Night trading of contracts on the S&P500 did not bring new impulses. Thus start of sessions in Europe may bring discounts induced by withdrawal on Wall Street at the end of the session but the potential drop will be rather cosmetic.

The macro calendar today is quite empty, therefore, to the rank of events increases the Friday speech of the Fed head, J. Yellen and investors are hoping for a more concrete signal about interest rates hike.

On the Warsaw market, yesterday's session in the basket of blue chips was dominated by discount of PZU and Pekao shares triggered by fears that the first will take over the second. Quite better acted the smaller companies. In conjunction with the breaking of the support in the region of 1,800 points the way to descend the WIG20 into area of 1,750 points was opened. In other words technique supports the continuation of the depreciation of the index of the largest companies, and fears about the future of PZU & Pekao does not help for the demand side for the deceleration of started last week correction.

Wednesday's morning trading on the currency market does not bring major changes in the valuation of the zloty against foreign currency. Polish currency is valued by investors as follows: EURPLN 4.3017, USDPLN 3.8150. Polish debt yields amount to 2,684% for 10-year bonds.

-

08:25

Expected positive start of trading on the major stock exchanges in Europe: DAX + 0.5%, CAC40 + 0.4%, FTSE + 0.4%

-

08:14

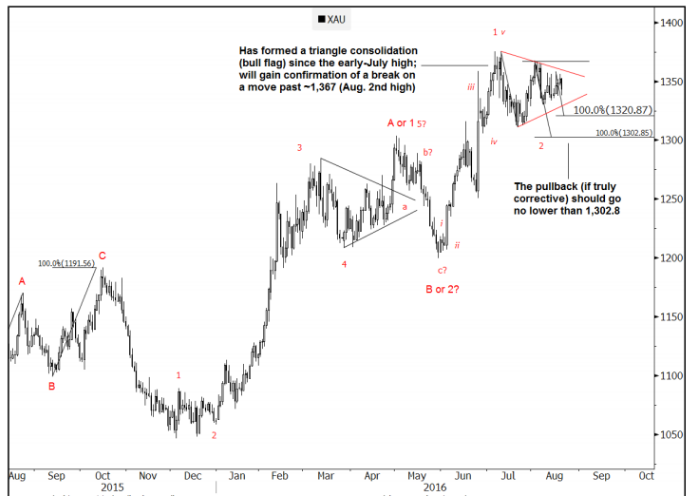

Here’s why Goldman Sachs adds to gold longs above $1367

"Gold has formed a triangle like consolidation since the July 11th high. Initial support comes in at 1,321. If this is truly a corrective pattern, it should go no lower than 1,302.85 (ABC from July 11th).

Will gain confirmation of an upside break through the Aug. 2 nd high which is up at 1,367.

Once a complete correction is in place, the level to target is 1,457; an ABC equality taken from the Dec. '15 low. Will re-assess the impulsive or corrective nature of the rally if/once the market does reach this 1,457 pivot. In other words, breaking past 1,457 will suggest that a more meaningful rally could be developing (i.e. wave III of V).

View: Sideways/ overlapping initially. Add to bullish exposure above 1,367, with an initial upside target at 1,457. Should go no lower than 1,302.85 (ABC from July 11th)".

Copyright © 2016 Goldman Sachs, eFXnews™

-

08:09

The value of construction work done in Australia tumbled

According to rttnews, the total value of construction work done in Australia tumbled a seasonally adjusted 3.7 percent on quarter in the second quarter of 2016, the Australian Bureau of Statistics said on Wednesday - coming in at A$47.419 billion.

That missed forecasts for a decline of 2.0 percent following the 2.6 percent decline in the three months prior.

On a yearly basis, the value of construction work done was down 10.6 percent.

-

08:07

New Zeeland: trade balance lower in July due to meat exports falling

Beef and lamb exports to key markets fell in July, slicing into overall meat exports, Statistics NZ said today. In the month of July 2016, total exports were $4.0 billion and total imports were $4.4 billion.

Overall, meat and edible offal exports in July were down 19 percent on July 2015, to $408 million. The largest fall was in lamb exports, which fell 29 percent in value and 25 percent in quantity.

"The meat export falls this month are partly due to record meat exports this time last year," international statistics senior manager Jason Attewell said. "Meat values in July 2015, off the back of a record high meat season, were 31 percent higher than the average value for the previous five July months."

Dairy exports also fell in July (down $88 million). Milk powder fell $118 million but was partly offset by rises in butter and natural milk constituents. The fall in value of milk powder was price driven, as the quantity rose 0.9 percent.

-

08:03

German GDP Q2 final reading in line with expectations

Germany's economy has continued to grow, but at a slightly slower pace. As the Federal Statistical Office (Destatis) already reported in its first release of 12 August 2016, the gross domestic product (GDP) increased by 0.4% (after price, seasonal and calendar adjustment) in the second quarter of 2016 compared with the first quarter of 2016. At the beginning of 2016, GDP growth had been strong at 0.7%.

A quarter-on-quarter comparison following price, seasonal and calendar adjustment shows that, on the use side of the gross domestic product, positive contributions mainly came from the balance of exports and imports. According to provisional calculations, exports of goods and services rose by a total of 1.2% compared with the first quarter of 2016. Imports declined by 0.1% in the same period. Arithmetically, the balance of exports and imports provided the strongest contribution to GDP growth in the reference period, contributing +0.6 percentage points.

-

08:00

Germany: GDP (QoQ), Quarter II 0.4% (forecast 0.4%)

-

08:00

Germany: GDP (YoY), Quarter II 3.1% (forecast 3.1%)

-

07:21

Global Stocks

European stocks finished higher Tuesday, with strong eurozone economic indicators and advances in the mining and financial sectors pushing the market to a second day of gains.

The Stoxx Europe 600 SXXP, +0.93% picked up 0.9% to close at 343.60, marking its biggest percentage gain since Aug. 5.

U.K. stocks pushed higher Tuesday and posted their biggest gain in nearly two weeks, with mining sector heavyweight BHP Billiton PLC and supermarket chain Tesco PLC among the shares moving firmly higher.

The FTSE 100 UKX, +0.59% rose 0.6% to close at 6,868.51, marking its best day since Aug. 11.

U.S. stocks closed in positive territory on Tuesday, but off the best levels of the session, after upbeat data on U.S. new-home sales and a stronger-than-expected gauge of European private-sector activity.

The Nasdaq Composite briefly hit an all-time intraday high, while the S&P 500 flirted with its own intraday record. Both the S&P 500 and Nasdaq had traded at levels that would have given them new closing highs Tuesday, but fell short by the close.

Asian stocks consolidated recent gains on Wednesday, helped by Wall Street's rise overnight, even as oil prices slid after a surprise build in U.S. crude stocks.

MSCI's broadest index of Asia-Pacific shares outside Japan .MIAPJ0000PUS eased 0.3 percent in early trade. It has risen more than 14 percent since late June to hit a 1-year high last week.

Japan's Nikkei .N225 rose 0.4 percent.

Elsewhere in the region, Hong Kong .HSI slid as investors sold financials, while mainland China markets .SSEC inched higher.

-

07:01

Japan: Leading Economic Index , June 99.2 (forecast 98.4)

-

07:01

Japan: Leading Economic Index , June 99.2 (forecast 98.4)

-

07:01

Japan: Coincident Index, June 111.1 (forecast 110.5)

-

03:30

Australia: Construction Work Done, Quarter II -3.7% (forecast -1.9%)

-

01:05

Commodities. Daily history for Aug 23’2016:

(raw materials / closing price /% change)

Oil 47.57 -1.10%

Gold 1,341.40 -0.35%

-

01:04

Stocks. Daily history for Aug 23’2016:

(index / closing price / change items /% change)

Nikkei 225 16,497.36 -100.83 -0.61%

Shanghai Composite 3,090.63 +5.83 +0.19%

S&P/ASX 200 5,553.77 +38.72 +0.70%

FTSE 100 6,868.51 +39.97 +0.59%

CAC 40 4,421.45 +31.51 +0.72%

Xetra DAX 10,592.88 +98.53 +0.94%

S&P 500 2,186.90 +4.26 +0.20%

Dow Jones Industrial Average 18,547.30 +17.88 +0.10%

S&P/TSX Composite 14,764.77 +16.58 +0.11%

-

01:02

Currencies. Daily history for Aug 23’2016:

(pare/closed(GMT +3)/change, %)

EUR/USD $1,1307 -0,11%

GBP/USD $1,3200 +0,47%

USD/CHF Chf0,9625 +0,05%

USD/JPY Y100,18 -0,13%

EUR/JPY Y113,28 -0,24%

GBP/JPY Y132,24 +0,35%

AUD/USD $0,7614 -0,22%

NZD/USD $0,7291 +0,03%

USD/CAD C$1,2915 -0,17%

-

00:45

New Zealand: Trade Balance, mln, July -433 (forecast -320)

-