Noticias del mercado

-

21:00

DJIA 18438.51 -42.97 -0.23%, NASDAQ 5204.77 -12.93 -0.25%, S&P 500 2170.47 -4.97 -0.23%

-

18:59

Wall Street. Major U.S. stock-indexes little changed

Major U.S. stock-indexes little changed on Thursday morning as financial stocks gained after two more Federal Reserve officials said the case for an interest rate hike was strengthening. Their comments followed the hawkish tone set by key Fed policymakers in recent days and came ahead of Fed Chair Janet Yellen's speech on Friday at Jackson Hole, which will be assessed to see if she takes an aggressive stance.

Most of Dow stocks in positive area (18 of 30). Top gainer - Cisco Systems, Inc. (CSCO, +0.98%). Top loser - Wal-Mart Stores Inc. (WMT, -1.34%).

Most of S&P sectors also in positive area. Top gainer - Technology (+0.3%). Top loser - Services (-0.1%).

At the moment:

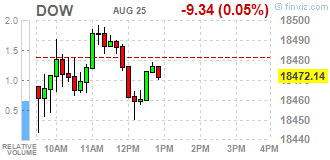

Dow 18454.00 -18.00 -0.10%

S&P 500 2175.25 +0.25 +0.01%

Nasdaq 100 4790.00 +3.75 +0.08%

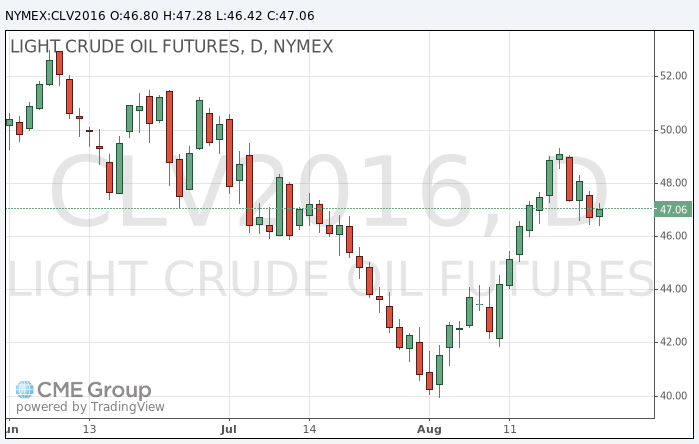

Oil 47.12 +0.35 +0.75%

Gold 1325.20 -4.50 -0.34%

U.S. 10yr 1.56 +0.01

-

18:00

European stocks closed: FTSE 6816.90 -18.88 -0.28%, DAX 10529.59 -93.38 -0.88%, CAC 4406.61 -28.86 -0.65%

-

17:55

Oil rose slightly today

US National Center for tracking hurricanes issued a warning about the formation in the next couple of days of a tropical storm.

This news, as well as some weakness of the US dollar on the currency market will support oil quotes and become drivers of growth observed today. If a tropical storm is indeed formed, and will go towards the United States, it will happen on the weekend. Investors do not want to stay in such conditions in short positions and prefer to partially or completely reduce the risks by cutting the volume of shorts.

Earlier, Iran's oil minister said he will participate in an informal meeting of OPEC in September in Algeria. It is also a favorable factor for the price, although the prevailing majority of experts did not believe that the results of the meeting will be of any effective agreements.

Many analysts and traders believe that the production freeze will not signed. Even in the case of the signing of such agreement strong doubts remain about the implementation.

It is difficult to keep a large amount of short positions, says Kyle Cooper of Ion Energy Group. " Is in the interest of OPEC to make at least some statement on the results of the meeting, so that prices may continue to grow", - adds the analyst.

However, the rise in oil prices on Thursday is relatively small, and the overall trend of the market over the last four trading sessions is down.

-

17:40

WSE: Session Results

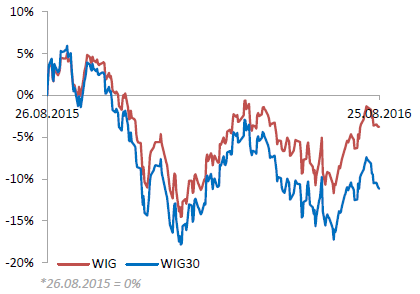

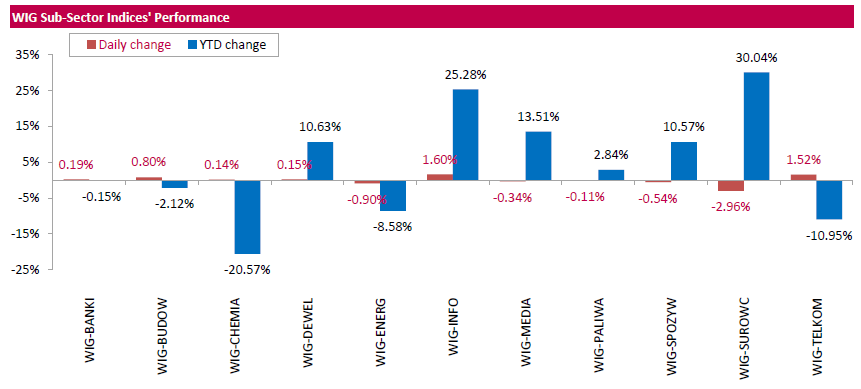

Polish equity market closed flat on Thursday. The broad market measure, the WIG Index, inched down 0.03%. Sector performance in the WIG index was mixed. Information technology (+1.60%) outperformed, while materials (-2.96%) lagged behind.

The large-cap stocks lost 0.18%, as measured by the WIG30 Index. Within the index components, copper producer KGHM (WSE: KGH) and coking coal miner JSW (WSE: JSW) recorded the largest declines, tumbling by a respective 3.14% and 2.57%. They were followed by three gencos ENERGA (WSE: ENG), PGE (WSE: PGE) and ENEA (WSE: ENA), losing between 1.36% and 1.72%. At the same time, videogame developer CD PROJEKT (WSE: CDR) and footwear retailer CCC (WSE: CCC) were among growth leaders, climbing by 4.62% and 1.63% respectively, helped by better-than-expected Q2 earnings results. The former reported net income of PLN 102.1 mln (-57.7% y/y) versus analysts' consensus estimate of PLN 77.2 mln, while the latter posted net profit of PLN 131.6 mln (+25% y/y) versus analysts' consensus estimate of PLN 100.9 mln. Other noticeable gainers were railway freight transport operator PKP CARGO (WSE: PKP), IT-company ASSECO POLAND (WSE: ACP) and two banks ING BSK (WSE: ING) and PEKAO (WSE: PEO), which added between 0.84% and 2.87%.

-

17:30

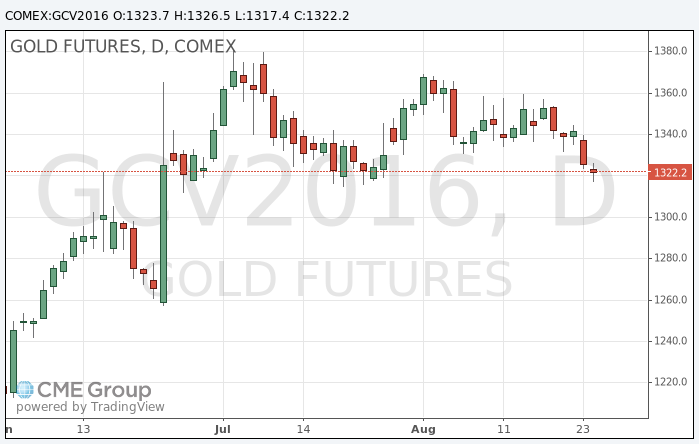

Gold price moderately lower

Gold is slightly cheaper, but traded in a narrow range in anticipation os Fed's Janet Yellen speech tomorrow which could give clues about the prospects for US monetary policy.

Investors are hoping that Yellen will give a clear signal about the timing of interest rate increases, when she will speak on Friday at a meeting of leaders of the world's central bankers in Jackson Hole, Wyoming.

Strong US employment data gave grounds to assume that rates could rise in September, although the views of officials of the central bank in the United States during the last session are divided.

"After the publication of the Fed meeting minutes the gold reacted very well, but after a few days there were comments of some officials, who believe that in fact the Fed has time to raise interest rates - said Capital Economics analyst Simon Gambarini -. This led to a decrease in the price of gold . Now all took a wait and see atitude for further comments, which will be able to move the market. "

CME FedWatch showed that the futures market estimates a 18 percent chance of the Fed hike next month, and about 50 percent in December.

The cost of the October futures for gold on the COMEX fell to $ 1317.4 per ounce.

-

16:38

Fed, Kaplan: Case for hiking rates 'strengthening'

-

Bond market predominantly driven by global search for yield

-

We are making progress on employment, slow progress on inflation

-

Case for hiking rates 'strengthening'

-

Hesitant to raise Fed's 2% inflation target

-

Debate about Fed monetary policy and targets is 'healthy'

-

Liquidity is fundamental force driving bond market

-

Case for removing accommodation in strengthening

-

-

15:57

Weakest rise in US services activity since February - Markit

According to Markit Economics, payroll numbers expand at slowest pace for 20 months Business expectations remain stronger than the survey-record low seen in June

U.S. service providers indicated another month of lacklustre growth in August, with business activity, new orders and employment all rising at a slower pace than in July. Survey respondents generally cited subdued underlying demand conditions and uncertainty ahead of the presidential election as factors that had dampened growth in August. Nonetheless, the balance of service sector firms expecting a rise in business activity over the year ahead remained well above the survey-record low seen in June.

-

15:52

Option expiries for today's 10:00 ET NY cut

USDJPY 98.00, 98.85 99.05, 99.25/30, 99.50/59, 99.75, 99.85 100.00, 100.30, 100.50, 100.60 101.00 (843m), 101.20/25/30/35 (785m), 101.45, 101.55, 101.60 102.00/05, 102.50 103.00/05 103.50

EURUSD 1.0950 (640m), 1.0975 (517m) 1.1000/03, 1.1040, 1.1090 1.1100, 1.1115, 1.1160, 1.1180, 1.1190 1.1200, 1.1240, 1.1260 1.1350 (652m), 1.1385/90 1.1400 1.1470

GBPUSD 1.2800 1.2900 1.3100, 1.3140

EURGBP 0.8125 (710m) 0.8200 0.8300 0.8620 (499m), 0.8650

AUDUSD 0.7400 (441m), 0.7450, 0.7470/75 (538m) 0.7595 0.7750

NZDUSD 0.8285

AUDNZD 1.0710 (330m)

USDCAD 1.3010/20/25

EURJPY 112.20

-

15:50

WSE: After start on Wall Street

The series of US data brought favorable news. While the good behavior of the labor market should no longer surprise anyone, information on orders for durable goods are more suggestive. The data, however, passed unnoticed, because everyone is waiting now to Yellen. The data was also overlap by words of the Fed head in Kansas City, Esther George, who said that it is time for a rate hike.

The market in the United States opened with a slight decrease of 0.12%. Investors clearly begins to fear of tomorrow's words of Janet Yellen.

An hour before the close of trading, the WIG20 index was at the level of 1,777 points (-0,48%).

-

15:45

U.S.: Services PMI, August 50.9 (forecast 52.0)

-

15:34

U.S. Stocks open: Dow -0.12%, Nasdaq -0.18%, S&P -0.14%

-

15:12

Before the bell: S&P futures -0.17%, NASDAQ futures -0.17%

U.S. stock-index futures slipped as investors awaited Friday's speech from Federal Reserve Chair Janet Yellen for clues on when to expect higher borrowing costs.

Global Stocks:

Nikkei 16,555.95 -41.35 -0.25%

Hang Seng 22,814.95 -5.83 -0.03%

Shanghai 3,068.23 -17.65 -0.57%

FTSE 6,825.58 -10.20 -0.15%

CAC 4,402.86 -32.61 -0.74%

DAX 10,526.05 -96.92 -0.91%

Crude $46.61 (-0.34%)

Gold $1322.00 (-0.58%)

-

14:52

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

3M Co

MMM

179.41

0.00(0.00%)

44687

ALCOA INC.

AA

10.11

0.07(0.6972%)

40326

ALTRIA GROUP INC.

MO

66.67

0.51(0.7709%)

114

Amazon.com Inc., NASDAQ

AMZN

756.2

-1.05(-0.1387%)

1270

American Express Co

AXP

64.99

-0.17(-0.2609%)

999

AMERICAN INTERNATIONAL GROUP

AIG

58.91

0.00(0.00%)

18614

Apple Inc.

AAPL

107.66

-0.37(-0.3425%)

40642

AT&T Inc

T

40.83

-0.04(-0.0979%)

2170

Barrick Gold Corporation, NYSE

ABX

18.15

-0.02(-0.1101%)

111399

Boeing Co

BA

133.29

0.00(0.00%)

15559

Caterpillar Inc

CAT

83

-0.15(-0.1804%)

16499

Chevron Corp

CVX

102.17

-0.03(-0.0294%)

326859

Cisco Systems Inc

CSCO

30.94

-0.12(-0.3863%)

708

Citigroup Inc., NYSE

C

46.6

-0.06(-0.1286%)

5130

Deere & Company, NYSE

DE

87.02

-0.40(-0.4576%)

462

E. I. du Pont de Nemours and Co

DD

70.37

0.00(0.00%)

118086

Exxon Mobil Corp

XOM

88.15

0.13(0.1477%)

2682

Facebook, Inc.

FB

123.27

-0.21(-0.1701%)

15512

FedEx Corporation, NYSE

FDX

168.23

0.00(0.00%)

14358

Ford Motor Co.

F

12.32

0.02(0.1626%)

14668

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

11.02

-0.06(-0.5415%)

183292

General Electric Co

GE

31.26

0.04(0.1281%)

6756

General Motors Company, NYSE

GM

31.78

0.00(0.00%)

483

Goldman Sachs

GS

165.19

-0.11(-0.0665%)

1020

Google Inc.

GOOG

770

0.36(0.0468%)

478

Hewlett-Packard Co.

HPQ

13.55

-0.85(-5.9028%)

310098

Home Depot Inc

HD

134.85

-0.21(-0.1555%)

647

HONEYWELL INTERNATIONAL INC.

HON

116.76

0.00(0.00%)

133134

Intel Corp

INTC

35.08

-0.07(-0.1991%)

700

International Business Machines Co...

IBM

158.7

-0.35(-0.2201%)

300

International Paper Company

IP

46.56

0.00(0.00%)

4795

Johnson & Johnson

JNJ

118.56

-0.15(-0.1264%)

278555

JPMorgan Chase and Co

JPM

66.08

0.13(0.1971%)

86095

McDonald's Corp

MCD

114.87

0.00(0.00%)

500

Merck & Co Inc

MRK

62.35

-0.38(-0.6058%)

1086

Microsoft Corp

MSFT

57.95

0.00(0.00%)

1630271

Nike

NKE

59.84

-0.38(-0.631%)

5104

Pfizer Inc

PFE

34.7

-0.12(-0.3446%)

31921

Procter & Gamble Co

PG

87.31

0.00(0.00%)

372941

Starbucks Corporation, NASDAQ

SBUX

57.19

0.10(0.1752%)

84478

Tesla Motors, Inc., NASDAQ

TSLA

223.5

0.88(0.3953%)

5015

The Coca-Cola Co

KO

43.85

0.00(0.00%)

62952

Travelers Companies Inc

TRV

117.11

0.00(0.00%)

13965

Twitter, Inc., NYSE

TWTR

18.41

0.16(0.8767%)

106064

United Technologies Corp

UTX

108.0278

0.0678(0.0628%)

53427

UnitedHealth Group Inc

UNH

139.87

0.00(0.00%)

76678

Verizon Communications Inc

VZ

52.75

0.22(0.4188%)

645

Visa

V

79.74

-0.55(-0.685%)

424

Wal-Mart Stores Inc

WMT

72.1

-0.13(-0.18%)

3735

Walt Disney Co

DIS

95.82

0.00(0.00%)

31194

Yahoo! Inc., NASDAQ

YHOO

41.86

-0.05(-0.1193%)

425

Yandex N.V., NASDAQ

YNDX

22.54

0.17(0.76%)

300

-

14:48

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

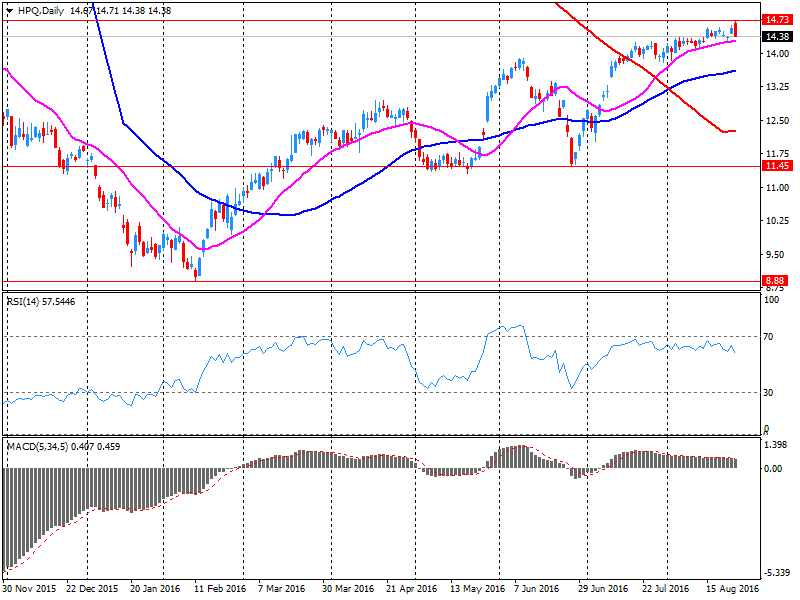

HP (HPQ) downgraded to Hold from Buy at Maxim Group; target lowered to $15 from $17

Other:

HP (HPQ) reiterated with Sector Perform with a target $14 at RBC Capital Mkts

-

14:40

Durable goods orders in US up 4.4% in July

New orders for manufactured durable goods in July increased $9.7 billion or 4.4 percent to $228.9 billion, the U.S. Census Bureau announced today. This increase, up following two consecutive monthly decreases, followed a 4.2 percent June decrease. Excluding transportation, new orders increased 1.5 percent. Excluding defense, new orders increased 3.8 percent. Transportation equipment, also up following two consecutive monthly decreases, led the increase, $7.5 billion or 10.5 percent to $78.9 billion.

Inventories of manufactured durable goods in July, up following six consecutive monthly decreases, increased $1.2 billion or 0.3 percent to $383.0 billion. This followed a 0.1 percent June decrease - US Census Bureau.

-

14:36

Canadian corporate profits declined less than the previous month

According to Statcan, Canadian corporations earned $72.9 billion in operating profits in the second quarter, down 3.4% from the previous quarter. The decrease was attributable to a $3.2 billion decline in profits for insurance carriers.

Year over year, overall operating profits for Canadian corporations fell 15.3% compared with the second quarter of 2015.

The oil and gas extraction industry reported an operating loss of $4.2 billion in the second quarter.

Petroleum and coal product manufacturing posted its second consecutive quarterly operating loss, recording an operating loss of $788 million in the second quarter, following an operating loss of $858 million in the first quarter.

-

14:33

US initial unemployment claims continue to decline

In the week ending August 20, the advance figure for seasonally adjusted initial claims was 261,000, a decrease of 1,000 from the previous week's unrevised level of 262,000. The 4-week moving average was 264,000, a decrease of 1,250 from the previous week's unrevised average of 265,250.

There were no special factors impacting this week's initial claims. This marks 77 consecutive weeks of initial claims below 300,000, the longest streak since 1970.

-

14:30

U.S.: Initial Jobless Claims, 261 (forecast 265)

-

14:30

U.S.: Durable Goods Orders , July 4.4% (forecast 3.3%)

-

14:30

U.S.: Continuing Jobless Claims, 2145 (forecast 2153)

-

14:30

U.S.: Durable Goods Orders ex Transportation , July 1.5% (forecast 0.5%)

-

14:30

U.S.: Durable goods orders ex defense, July 3.8%

-

14:24

Company News: HP Inc. (HPQ) Q3 results beat analysts’ expectations

HP Inc. reported Q3 FY 2016 earnings of $0.48 per share, beating analysts' consensus estimate of $0.45.

The company's quarterly revenues amounted to $11.892 bln (-3.8% y/y), beating analysts' consensus estimate of $11.492 bln.

HP issued downside guidance for Q4, projecting EPS of $0.34-0.37 versus analysts' consensus estimate of $0.40. It also lowered FY16 EPS to $1.59-1.62 from $1.59-1.65 versus analysts' consensus of $1.61.

HPQ fell to $13.60 (-5.56%) in pre-market trading.

-

14:00

Orders

EUR/USD

Offers 1.1280 1.1300 1.1320-25 1.1350-55 1.1380-85 1.1400

Bids 1.1250 1.1230 1.1200 1.1185 1.1150 1.1130 1.1100

GBP/USD

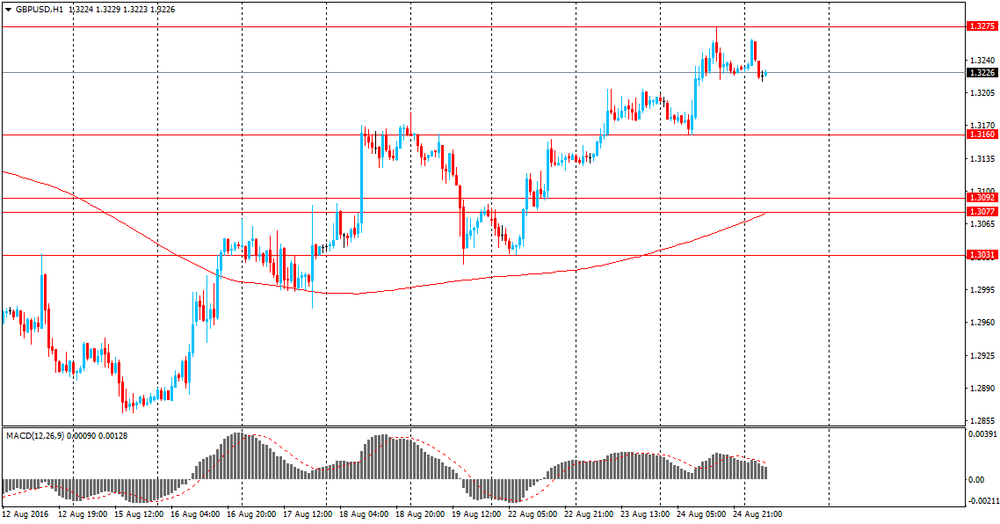

Offers 1.3235 1.3250 1.3280 1.3300 1.3320 1.3350

Bids 1.3200 1.3180 1.3160 1.3150 1.3130 1.3100 1.3085 1.3050

EUR/GBP

Offers 0.8535 0.8550 0.8580 0.8600 0.8625-30 0.8655-60 0.8685 0.8700

Bids 0.8520 0.8500 0.8480-85 0.8465 0.8450 0.8430 0.8400

EUR/JPY

Offers 113.50 113.80 114.00 114.30 114.50 114.75 115.00

Bids 113.00 112.75-80 112.50 112.30 112.00-10

USD/JPY

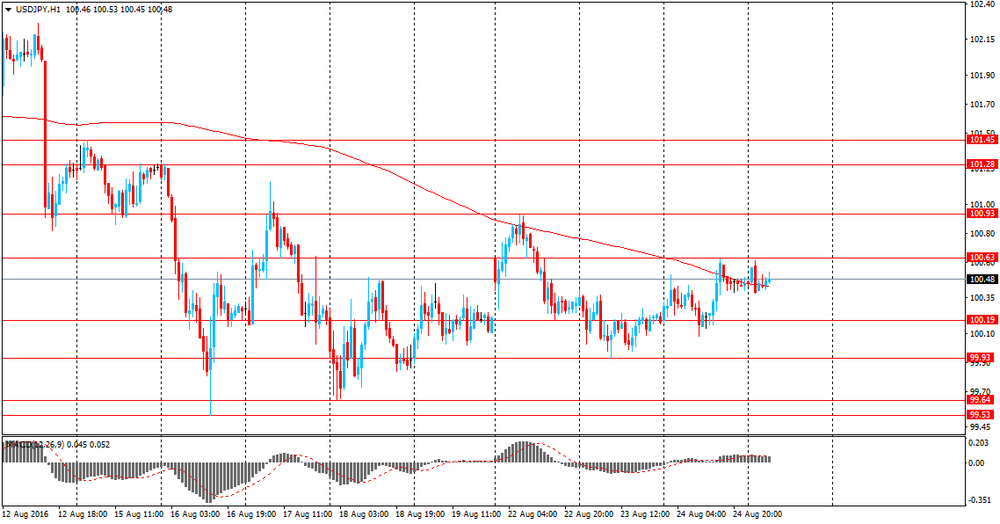

Offers 100.50 100.65 100.85 101.00 101.25-30 101.50 101.75-80 102.00

Bids 100.30 100.25 100.00 99.85 99.6599.50 99.30 99.00 98.80 98.50

AUD/USD

Offers 0.7650-55 0.7680 0.7700 0.7725-30 0.7750-55

Bids 0.7620 0.7600 0.7585 0.7565 0.7550 0.7500

-

13:48

Fed's George: Removing `Some of this Accommodation Would Be Appropriate'

- Inflation `Beginning to Stir'.

- there's every reason to expect 2016 US GDP growth of 2%.

- 3% GDP possible in H2.

-

13:02

WSE: Mid session comment

The reading of the German Ifo index surprised negatively. These data exacerbated the already strained mood and the German DAX lost after reading more than 1%. Weaker data from Germany, combined with the expectation of tomorrow's speech by Janet Yellen noticeably worsened the condition of the environment and stable Stock Exchange in the half of second hour of trading slightly surrendered and the WIG20 quickly went down to yesterday's lows.

In the southern phase of trading European parquets come to slightly higher levels. Thus, the German DAX limited losses to 0.9% and the French CAC40 to 0.8%. The weakest are doing today the companies of raw materials (including our KGHM, which shares lost more than 3% today) and related to the automotive sector. Our market is traditionally less eager to change the chosen direction and the WIG20 from their session lows is not unduly moved away. In the mid-session the WIG20 index reached the level of 1,775 points (-0,61%). The turnover in the basket of the largest companies was amounted to PLN 200 mln.

-

12:54

Major stock indexes in Europe show a negative trend

European stocks are down moderately, ending a three-day rally, due to concerns over the outlook for economic growth and expectations of the Fed speech.

The data published by research institute IFO, showed that the index of business climate in Germany unexpectedly fell in August to 106.2 points from 108.3 points in July. Analysts had expected the index rising to 108.5 points. In addition, the current conditions index fell to 112.8 points from 114.8 points in July, while economists had forecast an improvement to 114.9. The expectations index fell to 100.1 points from 102.1 points, which was lower than expected level of 102.5. Yesterday the Germany's GDP in the 2nd quarter increased by 0.4% compared to the previous 3 months. In annual terms, the economy has added 3.1%.

However, today, the Statistical Office Insee reported that the index of manufacturing sentiment in France fell in August to 101 from 103 in July. Economists had forecast that the index would remain unchanged. A similar low value was recorded for the last time in June 2015. Business managers in the industrial sector were less optimistic about the general prospects of production than in July - the corresponding indicator fell to 2 points from a month earlier.

The composite index of Europe's largest enterprises Stoxx 600 fell 0.7 percent.

Shares of mining companies shows the greatest decline among the 19 industry groups. Shares of Glencore Plc and Anglo American fell 4 percent and 1.5 percent respectively.

Shares of energy companies also in negative territory, as oil traded near a week low. Total SA Quotes decreased by 0.3 percent.

Price of Playtech Plc shares rose 3.4 percent after the supplier of gaming software reported an increase in revenues in the 1st half of the year and announced a special dividend.

Capitalization of Jimmy Choo Plc jumped 5.3 The company noted that it is still optimistic about the prospects for this year.

CRH Plc shares rose by 2.6 per cent, as the Irish construction company recorded higher-than-expected figures for profits and sales in the 1st half of the year.

At the moment:

FTSE 100 6813.77 -22.01 -0.32%

DAX -100.64 10522.33 -0.95%

CAC 40 4401.39 -34.08 -0.77%

-

12:26

UK: the volume of sales grew modestly - CBI

According to the CBI survey of 131 firms, of which 58 were retailers, showed that the volume of sales grew modestly over the year, beating expectations for a further fall this month. However, sales volumes look set to be broadly flat over the next month.

Investment intentions for the year ahead turned positive following the most negative results since 2013 in the previous quarter. Year-on-year employment was again flat in the year to August, although retailers expect a small cut in headcount in September.

Anna Leach, CBI Head of Economic Analysis and Surveys, said:

"The summer weather has brought shoppers out onto the high street with retailers reporting that sales growth has risen, outdoing expectations, although firms do expect sales growth to ease next month.

"While the fall in Sterling has boosted visitor numbers to the UK, it is likely to push up the price of imported goods over time which will mean households will be more likely to rein back spending on non-essentials."

-

12:00

United Kingdom: CBI retail sales volume balance, August 9 (forecast -5)

-

11:25

Net migration to the UK fell

-

Net migration to the UK was 327k, -9k vs prior year

-

Net EU migration to the UK was 180k, -4k vs last year

*via forexlive -

-

10:40

Option expiries for today's 10:00 ET NY cut

USD/JPY 98.00, 98.85,99.05, 99.25/30, 99.50/59, 99.75, 99.85,100.00,100.30, 100.50, 100.60,101.00 (843m), 101.20/25/30/35,(785m), 101.45, 101.55, 101.60,102.00/05, 102.50,103.00/05,103.50

EUR/USD 1.0950 (640m), 1.0975 (517m)

1.1000/03, 1.1040, 1.1090,1.1100, 1.1115, 1.1160, 1.1180, 1.1190,1.1200, 1.1240, 1.1260,1.1350 (652m), 1.1385/90,1.1400,1.1470

GBP/USD 1.2800,1.2900,1.3100, 1.3140

EUR/GBP 0.8125 (710m),0.8200,0.8300,0.8620 (499m), 0.8650

AUD/USD 0.7400 (441m), 0.7450, 0.7470/75 (538m),0.7595,0.7750

NZD/USD 0.8285

AUD/NZD 1.0710 (330m)

USD/CAD 1.3010/20/25

EUR/JPY 112.20

-

10:28

German Ifo business climate index lower in August

According to rttnews, German business confidence dropped unexpectedly in August, reports said citing survey results from Ifo on Thursday.

The business sentiment index dropped to 106.2 in August from 108.3 in July. The reading was expected to rise to 108.5.

Similarly, the current conditions index fell to 112.8 from 114.8 a month ago, while economists forecast an improvement to 114.9.

The expectations index slid to 100.1 in August, below the expected level of 102.4.

-

10:25

Oil almost flat in early trading

This morning, New York crude oil futures for WTI rose by + 0.13% to $ 46.83 and Brent oil fell slightly to -0.08% to $ 49.02 per barrel. Thus, the black gold is trading without any important changes, showing the preservation of oversupply in the market. According to data published on Wednesday oil inventories in US increased by 2.5 million barrels last week, while analysts expected on average a reduction of 850 thousand. Gasoline stocks rose by 36 thousand barrels, distillates +122 th. barrels, and oil reserves in the United States 8% above last year's levels.

-

10:01

Germany: IFO - Expectations , August 100.1 (forecast 102.5)

-

10:00

Germany: IFO - Business Climate, August 106.2 (forecast 108.5)

-

10:00

Germany: IFO - Current Assessment , August 112.8 (forecast 114.9)

-

09:33

Keep an eye on statements from Jackson Hole. Today is the first day of the meeting

-

09:17

WSE: After opening

WIG20 index opened at 1788.99 points (+0.15%)*

WIG 47535.17 0.12%

WIG30 2039.62 0.17%

mWIG40 3865.46 0.38%

*/ - change to previous close

The futures market opened with increase of 0.11% to 1,789 points.

The cash market opens with slight increase by 0.13% to 1,788 points. The German DAX starts a session low, as already goes down by 0.5%, which means that waiting for Janet Yellen is not generally favorable for the bulls

However it is hard to expect today, on the eve of speech of Janet Yellen, any major changes in indexes and exchange rates. On markets (also on the WSE) should reign waiting. Perhaps a little mess will bring the OCCP (Office of Competition and Consumer Protection), which at 10:00 (Warsaw time) is expected to present its, called as "significant", view on the dispute of owner of currency loans with the banks. It may harm banks.

-

09:10

Today’s events:

At 17:00 GMT the United States will hold an auction on placement of 7-year bonds.

Day 1 of the annual symposium in Jackson Hole.

The Economic Symposium, held in Jackson Hole, Wyoming, is attended by central bankers, finance ministers, academics, and financial market participants from around the world. The meetings are closed to the press but officials usually talk with reporters throughout the day. Comments and speeches from central bankers and other influential officials can create significant market volatility.

-

09:08

Asian session review: the dollar traded in a narrow range

The US dollar traded in a narrow range against the euro and the yen after yesterday's growth, helped by US economic data, as well as the expectation that later this weekthe Federal Reserve will express a tendency to further tighten policy.

Sales in the primary US housing market in July reached the highest level in almost a decade, as evidenced by the data published on Tuesday This indicates the strong momentum of the recovery in the housing market. Positive data boosted expectations of what Fed Chairman Janet Yellen could say in the speech in Jackson.

Futures on interest rates showed that investors see a 24% chance of a rate hike in September, while the probability of such an events was 12%, earlier this month.

"Yellen's speech on Friday could have a serious impact on the dollar, and we still expect to continue to improve," - according to BNP Paribas analysts.

The yen briefly rose after the Nikkei news agency reported that the Japanese government will introduce Y4,52 trillion in the economy in the current fiscal year.

The main infusion will be in the form of public construction projects. a supplementary budget proposal was approved on Wednesday

Japanese investment in foreign bonds fell along with the number of foreign investments in Japanese stocks. According to data released by Japan's Ministry of Finance, foreign bonds investment in August, totaled ¥ 433,1 mld, lower than the previous value of ¥ 1 297,6 mld.

The report estimates the volume of debt securities issued by foreign issuers and placed on the domestic market of Japan. This report reflects the dynamics of capital from the public sector, excluding the Bank of Japan. The net result shows a difference between the rates of inflow and outflow of capital. Despite the positive value, data indicates a decline in the outflow of capital.

Foreign investment in Japanese equities fell in August to ¥ -229,6mlrd after rising ¥ 94mlrd in July.

According to J.P. Of Morgan, after the meeting in Jackson Hole, the US currency will weaken again and USD / JPY is likely to test Y99,55.

EUR / USD: during the Asian session, the pair was trading in the $ 1.1260-80 range

GBP / USD: during the Asian session, the pair was trading in the $ 1.3220-60 range

USD / JPY: during the Asian session, the pair was trading in the Y100.40-65 range

-

08:39

New RBA Governor A Reluctant Rate Cutter - Credit Agricole

"Australian construction work done data show further contraction in the sector as declines in engineering construction continue to more than offset firm growth in residential and non-residential construction. The end to the mining boom remains a significant drag on the economy. Anecdotal evidence about Australia's residential property market is mixed. While auction clearance rates in Melbourne and Sydney remain high, in other centres they are weakening. Sydney's weekend auction clearance rates hit boom-time highs over the recent weekend and even weekday auctions are seeing strong bidding, largely driven by the RBA's latest rate cut.

The bar for further rate cuts in Australia is likely high. New RBA Governor, Phil Lowe, is a system stability expert and likely a reluctant rate cutter.

So AUD's fortunes are increasingly tied to the Fed. AUD/USD continues to rest against trend-line support ahead of Yellen's speech on Friday".

*Credit Agricole maintains a short AUD/USD position from 0.7674.

Copyright © 2016 Credit Agricole CIB, eFXnews™

-

08:36

Japanese investment in foreign bonds fell

Japanese investment in foreign bonds fell along with the number of foreign investments in Japanese stocks. According to data released by Japan's Ministry of Finance, foreign bonds investment in August, totaled ¥ 433,1 mld, lower than the previous value of ¥ 1 297,6 mld.

The report estimates the volume of debt securities issued by foreign issuers and placed on the domestic market of Japan. This report reflects the dynamics of capital from the public sector, excluding the Bank of Japan. The net result shows a difference between the rates of inflow and outflow of capital. Despite the positive value, data indicates a decline in the outflow of capital.

Foreign investment in Japanese equities fell in August to ¥ -229,6mlrd after rising ¥ 94mlrd in July.

-

08:32

Sumitomo Mitsui Banking Corp: USDJPY could undo all the Abenomic gains to fall to 85.00

-

BOJ may drop inflation target time frame at September meeting

-

May flag external factors like oil and slower global growth as impediments to hitting inflation goal, even while saying the correct policy actions have been taken

-

BOJ may change QQE range to ¥70-90tn from current ¥80tn

-

Would be difficult for BOJ to cut rates further into the negative

-

USDJPY could undo all the Abenomic gains to fall to 85.00

-

-

08:31

Options levels on thursday, August 25, 2016:

EUR/USD

Resistance levels (open interest**, contracts)

$1.1433 (4488)

$1.1368 (4542)

$1.1324 (4205)

Price at time of writing this review: $1.1272

Support levels (open interest**, contracts):

$1.1205 (2376)

$1.1150 (2757)

$1.1115 (3258)

Comments:

- Overall open interest on the CALL options with the expiration date September, 9 is 52228 contracts, with the maximum number of contracts with strike price $1,1250 (4638);

- Overall open interest on the PUT options with the expiration date September, 9 is 57754 contracts, with the maximum number of contracts with strike price $1,1000 (5763);

- The ratio of PUT/CALL was 1.11 versus 1.09 from the previous trading day according to data from August, 24

GBP/USD

Resistance levels (open interest**, contracts)

$1.3503 (1942)

$1.3405 (2523)

$1.3308 (2631)

Price at time of writing this review: $1.3219

Support levels (open interest**, contracts):

$1.3094 (1009)

$1.2997 (2023)

$1.2898 (1937)

Comments:

- Overall open interest on the CALL options with the expiration date September, 9 is 32392 contracts, with the maximum number of contracts with strike price $1,3300 (2631);

- Overall open interest on the PUT options with the expiration date September, 9 is 26425 contracts, with the maximum number of contracts with strike price $1,2800 (2675);

- The ratio of PUT/CALL was 0.82 versus 0.81 from the previous trading day according to data from August, 24

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

08:28

Expected negative start of trading on the major stock exchanges in Europe: DAX -0.1%, CAC40 -0,05%, FTSE -0,06%

-

08:21

WSE: Before opening

Yesterday's session on Wall Street ended with slight declines and the S&P500 index ended trading with a discount of 0.5%. In Asia, the mood is not the worst, and only China is clearly dominated by the red color, index in Shanghai discounts up to 1%. The Japanese Nikkei lost cosmetically and on other parquets we may see the light increases. Futures market in the US looks quite stable.

Today begins a symposium in Jackson Hole, and yesterday we could see the first changes in the markets in view of possible incoming impulses from there. Strengthened the US dollar and on equity markets investors have become more cautious.

In today's macro calendar in the morning will be announced macro data from Germany in the form of the Ifo institute index. In the afternoon in the US will be announced orders for durable goods.

The Warsaw market is fighting to stop the downward movement. Upcoming speech by Janet Yellen will not help, but on the other hand, the global situation is not so tense to seriously interfered with at least stabilization of the market over the level of 1,775 points.

Thursday morning trading on the currency market does not bring any significant changes to the valuation of the zloty against foreign currency. Polish currency is valued by the market as follows: PLN 4.3084 per euro, 3.8230 PLN against the US dollar. Yields on Polish debt amounts to 2,663% for 10-year bonds.

-

08:21

Reuters: 60% of economists expect the Bank of Japan easing policy in September

60% of economists surveyed by Reuters expected easing of monetary policy from the Bank of Japan in September and 40% of respondents take a neutral position on this issue.

More than 50% of economists predict the introduction of a flexible inflation target.

-

08:19

Producer prices in Japan were up 0.4 percent in July

According to rttnews, producer prices in Japan were up 0.4 percent on year in July, the Bank of Japan said on Thursday.

That beat expectations for an increase of 0.1 percent following the 0.2 percent gain in June.

On a monthly basis, process also jumped 0.4 percent following the flat reading in the previous month.

Among the individual components, prices increased for advertising, communications and leasing - while they were down for transportation and postal activities.

-

07:21

Global Stocks

European stocks advanced on Wednesday after a choppy start to the day, as a rally for banks and advertising giant WPP PLC outweighed pressure from falling commodity prices.

The Stoxx Europe 600 index SXXP, +0.39% gained 0.4% to 344.93, closing in positive for a third straight session.

U.K. stocks closed in the red Wednesday, with resource companies leading the charge south on the back of a slide in commodity prices and a mixed earnings report from mining giant Glencore PLC.

The FTSE 100 UKX, -0.48% dropped 0.5% to finish at 6,835.78, partly erasing a 0.6% gain from Tuesday.

The S&P 500 and Dow industrials on Wednesday finished at their lowest levels since early August as selling in health-care shares, sparked by intensifying outrage over the pricing of a lifesaving drug by Mylan, put pressure on the broader market.

The slump in Mylan nudged the health-care sector lower and weighed on the exchange-traded iShares Nasdaq Biotechnology ETF IBB, -3.36% which was down 3.4%-its worst daily slide in two months, according to FactSet data.

The Nasdaq Composite Index COMP, -0.81% suffered the brunt of the market's retreat, trading down 42.38 points, or about 0.8%, to close at 5,217.69. The tech-heavy index closed at its lowest level since Aug. 8., and experienced its worst daily slump in three weeks.

Asian stocks edged higher on Thursday but clung to recent well-worn trading ranges while the greenback held firm against regional currencies ahead of a speech by Federal Reserve Chair Janet Yellen at a global central bankers' meeting.

Market expectations have increased that Yellen might indicate a clearer timeframe for the next U.S. rate hike after strong housing data this week and hawkish comments by other Fed officials, but many analysts expect her to strike a more neutral stance.

On Wednesday, futures markets were indicating just an 18 percent chance the U.S. central bank would hike rates at its policy meeting next month, and roughly 50 percent odds of a rate increase in December, according to CME Group's FedWatch tool.

-

00:31

Commodities. Daily history for Aug 24’2016:

(raw materials / closing price /% change)

Oil 46.79 +0.04%

Gold 1,327.80 -0.14%

-

00:29

Stocks. Daily history for Aug 24’2016:

(index / closing price / change items /% change)

Nikkei 225 16,597.30 +99.94 +0.61%

Shanghai Composite 3,085.82 -3.88 -0.13%

S&P/ASX 200 5,561.67 +7.90 +0.14%

FTSE 100 6,835.78 -32.73 -0.48%

CAC 40 4,435.47 +14.02 +0.32%

Xetra DAX 10,622.97 +30.09 +0.28%

S&P 500 2,175.44 -11.46 -0.52%

Dow Jones Industrial Average 18,481.48 -65.82 -0.35%

S&P/TSX Composite 14,626.24 -138.53 -0.94%

-

00:29

Currencies. Daily history for Aug 24’2016:

(pare/closed(GMT +3)/change, %)

EUR/USD $1,1262 -0,40%

GBP/USD $1,3230 +0,23%

USD/CHF Chf0,9668 +0,44%

USD/JPY Y100,45 +0,27%

EUR/JPY Y113,13 -0,13%

GBP/JPY Y132,88 +0,48%

AUD/USD $0,7610 -0,05%

NZD/USD $0,7305 +0,19%

USD/CAD C$1,2927 +0,09%

-

00:00

Schedule for today, Thursday, Aug 25’2016

(time / country / index / period / previous value / forecast)

01:30 Australia Private Capital Expenditure Quarter II -5.2%

08:00 Germany IFO - Business Climate August 108.3 108.5

08:00 Germany IFO - Current Assessment August 114.7 114.9

08:00 Germany IFO - Expectations August 102.2 102.5

10:00 United Kingdom CBI retail sales volume balance August -14 -5

12:30 U.S. Continuing Jobless Claims 2175 2153

12:30 U.S. Durable Goods Orders July -4% 3.3%

12:30 U.S. Durable Goods Orders ex Transportation July -0.5% 0.5%

12:30 U.S. Durable goods orders ex defense July -3.9%

12:30 U.S. Initial Jobless Claims 262 265

23:30 Japan Tokyo Consumer Price Index, y/y August -0.4%

23:30 Japan Tokyo CPI ex Fresh Food, y/y August -0.4% -0.3%

23:30 Japan National Consumer Price Index, y/y July -0.4%

23:30 Japan National CPI Ex-Fresh Food, y/y July -0.5% -0.4%

-