Noticias del mercado

-

22:07

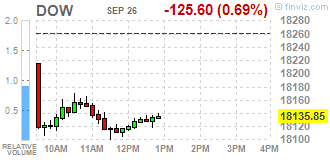

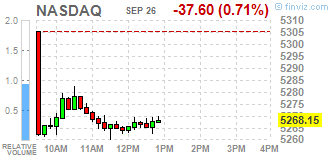

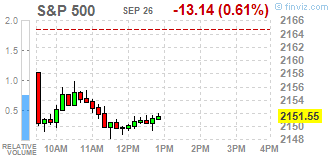

Major US stock indexes finished trading below zero

Major Wall Street stock indexes fell as investors anxiously await the first presidential debate in the United States, to assess how candidates plan to shape the economy and politics.

While the race for the seat in the White House still does not have an appreciable impact on the market, this may change after the first debate between Hillary Clinton and Donald Trump. Just six weeks before election day, some investors note volatility in certain sectors, including among health insurance companies, drug manufacturers and industrialists.

As it became known today, sales of new single-family homes in the US fell less than expected in August, while prices fell and stocks rose. The Commerce Department reported that new home sales fell by 7.6% to a seasonally adjusted annual rate reached 609,000 units last month. Sales rose by 20.6 percent compared to last year. Economists had forecast that sales will fall to 597 000 units in the last month.

Oil has risen dramatically today as the largest manufacturers in the world have gathered in Algiers to discuss ways to support the market. Recall, today in Algeria launched the International Energy Forum. On the sidelines of the forum members of the Organization of Petroleum Exporting Countries will meet in an informal setting to discuss a possible deal to curb oil production. Iran, which is still ramping up production, diminishes the chances of the deal, although several other members of the group said they still hope that will be reached some kind of agreement that will solve the problem of global excess oil.

Almost all the components of DOW index closed in negative territory (27 of 30). More rest up shares The Procter & Gamble Company (PG, + 0.42%). Outsider were shares of The Goldman Sachs Group, Inc. (GS, -2.29%).

All business sectors S & P index showed a decline. the health sector fell the most (-1.2%).

At the close:

Dow -0.91% 18,095.99 -165.46

Nasdaq -0.91% 5,257.49 -48.26

S & P -0.86% 2,146.18 -18.51

-

21:00

DJIA -0.85% 18,106.85 -154.60 Nasdaq -0.82% 5,262.38 -43.37 S&P -0.80% 2,147.36 -17.33

-

18:58

Wall Street. Major U.S. stock-indexes fell

Major U.S. stock-indexes lower on Monday morning as investors anxiously await the first U.S. presidential debate to gauge how the candidates plan to shape the economy and policy. While the White House race has so far had little discernible effect on the market, that may soon change as polls show a tightening race ahead of the first debate between Hillary Clinton and Donald Trump.

Almost all of Dow stocks in negative area (25 of 30). Top gainer - Apple Inc. (AAPL, +0.27%). Top loser - The Goldman Sachs Group, Inc. (GS -1.87%).

All S&P sectors also in negative area. Top loser - Healthcare (-1.1%).

At the moment:

Dow 18044.00 -146.00 -0.80%

S&P 500 2144.00 -14.00 -0.65%

Nasdaq 100 4821.25 -35.25 -0.73%

Oil 46.08 +1.60 +3.60%

Gold 1344.00 +2.30 +0.17%

U.S. 10yr 1.58 -0.04

-

18:00

European stocks closed: FTSE 100 -91.39 6818.04 -1.32% DAX -233.26 10393.71 -2.19% CAC 40 -80.84 4407.85 -1.80%

-

17:52

The price of oil rose more than 3 percent as the largest manufacturers in the world have gathered in Algiers to discuss ways to support the market

Oil futures rose dramatically today as the largest manufacturers in the world have gathered in Algiers to discuss ways to support the market.

Recall, today in Algeria the International Energy Forum starts. On the sidelines of the forum members of the Organization of Petroleum Exporting Countries will meet in an informal setting to discuss a possible deal to curb oil production.

Iran, which is still ramping up production, diminishes the chances of the deal, although several other members of the group said they still hope that will be reached some kind of agreement that will solve the problem of global excess oil.

However, skepticism about the possibility of concluding any agreement prompted money managers and hedge funds to cut their bullish bets on oil to one-month low last week, when prices fell nearly 5 percent. This was reported by the US Commodity Futures Trading Commission.

The cost of the November futures for US light crude oil WTI (Light Sweet Crude Oil) rose to 45.91 dollars per barrel on the New York Mercantile Exchange.

November futures price for North Sea petroleum mix of Brent crude rose to 47.98 dollars a barrel on the London Stock Exchange ICE Futures Europe.

-

17:42

Gold rose slightly

Gold prices rose slightly pdating the Friday's high, helped by a weaker dollar and expectations of the first television debate between the candidates for the US presidency.

According to a survey conducted by broadcaster ABC and the newspaper Washington Post, Clinton ahead Trump's popularity by 2%. Studies have shown that if you had to choose between two candidates, 46% of respondents would vote for Clinton and 44% for Trump. According to analysts, if Trump's support will increase, the price of gold may rise in the short term against the backdrop of highly volatile.

However, uncertainty about the US monetary policy outlook and sluggish demand for physical metal in Asia held back a further increase in prices. This week, investors will focus on recent comments of Fed Yellen, which may shed further light on the timing of the next increase in US interest rates. Market participants will closely follow the performances on other high-ranking officials Fed, as well as statistics on the US economy.

"Gold is trading in a relatively narrow range for the third day in a row - Ole Hansen said, the head of commodity research at Saxo Bank -. Meanwhile, demand from hedge funds and investors absent in recent weeks, despite the favorable prospects for Fed policy. Trump increased support in the polls, a weaker dollar and today's drop in the stock market, driven by losses in the banking sector. "

Data published by Commodity Futures Trading Commission US, showed that last week (to September 20), hedge funds and money managers reduced their net long positions in gold for the second time in a row.

The cost of the October futures for gold on COMEX rose to $ 1340.2 per ounce.

-

17:35

WSE: Session Results

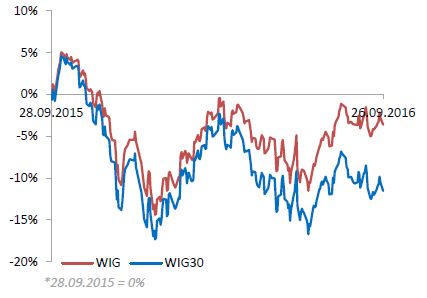

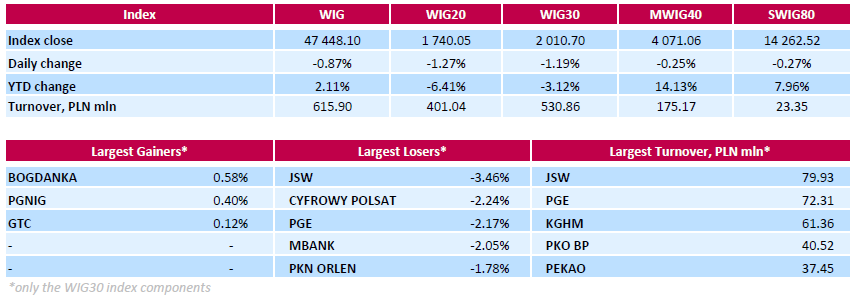

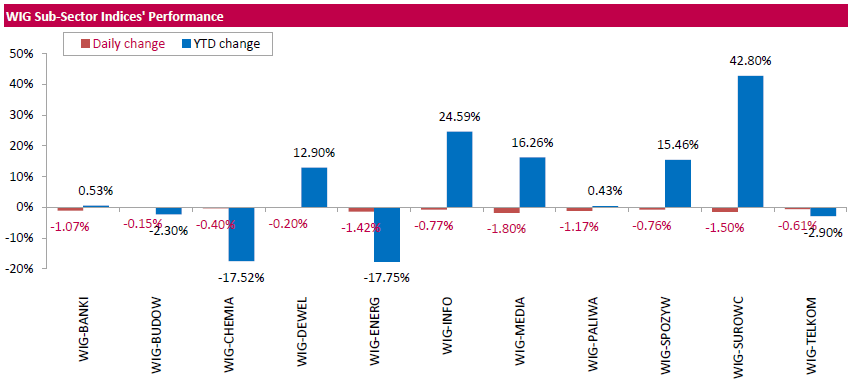

Polish equity closed lower on Monday. The broad market measure, the WIG Index, fell by 0.87%. All sectors in the WIG generated negative returns, with media (-1.80%) and materials (-1.50%) underperforming.

The large-cap stocks' benchmark, the WIG30 Index, slumped by 1.19%. There were only three gainers among the index components. Thermal coal miner BOGDANKA (WSE: LWB) recorded the biggest advance of 0.58%. Other outperformers were oil and gas producer PGNIG (WSE: PGN) and property developer GTC (WSE: GTC), adding 0.4% and 0.12% respectively. On the other side of the ledger, coking coal producer JSW (WSE: JSW) topped the list of laggards, tumbling by 3.46%. It was followed by media group CYFROWY POLSAT (WSE: CPS), genco PGE (WSE: PGE) and bank MBANK (WSE: MBK), declining by 2.24%, 2.17% and 2.05% respectively.

-

16:02

US new home sales up slightly in August

Sales of new single-family houses in August 2016 were at a seasonally adjusted annual rate of 609,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 7.6 percent (±10.7%)* below the revised July rate of 659,000, but is 20.6 percent (±14.8%) above the August 2015 estimate of 505,000.

The median sales price of new houses sold in August 2016 was $284,000; the average sales price was $353,600. The seasonally adjusted estimate of new houses for sale at the end of August was 235,000. This represents a supply of 4.6 months at the current sales rate.

-

16:00

U.S.: New Home Sales, August 609 (forecast 597)

-

15:55

WSE: After start on Wall Street

The afternoon trading phase has not changed the balance of power on the Warsaw market. The turnover in the segment of blue chips is still meager and the mood in Warsaw and across Europe is declining today. The German DAX was deepened morning intraday lows and consequently descends falling more than 2%. Thus the weakness of the German market today is basically indisputable. The start of the day on Wall Street was inscribed in the mood already set by Europe and the S&P500 index began testing support. So far, we may see that the vision of the upcoming elections and the real possibility of Trump victory quite effectively inhibits bulls aspirations.

An hour before the end of trading, the WIG20 was at the level of 1,734 points (-1.60%).

-

15:46

Option expiries for today's 10:00 ET NY cut

EUR/USD: 1.1170 (367m) 1.1250 (224m) 1.1325 (207m)

USD/JPY: 99.00 (USD 610m) 99.80-81 (640m) 100.00 (627m) 100.50-60 (USD 220m) 101.00 (411m) 102.00 (262m) 102.21 (360m)

AUD/USD 0.7500 (AUD 610m)

NZD/USD 0.7300 (248m) 0.7335-41 (249m)

USD/CAD 1.3300 (USD 590m)

EUR/JPY 113.15 (798m)

AUD/JPY 75.50-60 (531m)

-

15:28

Before the bell: S&P futures -0.47%, NASDAQ futures -0.59%

U.S. stock-index futures fell, tracking declines in European shares spurred by weakness in banks, while investors awaited a presidential debate and a meeting between major oil producers this week.

Global Stocks:

Nikkei 16,544.56 -209.46 -1.25%

Hang Seng 23,317.92 -368.56 -1.56%

Shanghai 2,981.25 -52.65 -1.74%

FTSE 6,828.82 -80.61 -1.17%

CAC 4,411.49 -77.20 -1.72%

DAX 10,427.91 -199.06 -1.87%

Crude $45.05 за баррель (+1.28%)

Gold $1342.00 за унцию (+0.02%)

-

15:11

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

9.73

-0.03(-0.3074%)

3899

ALTRIA GROUP INC.

MO

63.72

-0.15(-0.2349%)

1034

Amazon.com Inc., NASDAQ

AMZN

802

-3.75(-0.4654%)

26077

Apple Inc.

AAPL

111.5

-1.21(-1.0736%)

399552

AT&T Inc

T

41.4

0.12(0.2907%)

2798

Barrick Gold Corporation, NYSE

ABX

18.05

-0.06(-0.3313%)

15346

Caterpillar Inc

CAT

82.39

-0.05(-0.0607%)

474

Chevron Corp

CVX

99.41

0.19(0.1915%)

725

Cisco Systems Inc

CSCO

31.2

-0.14(-0.4467%)

2379

Citigroup Inc., NYSE

C

46.64

-0.51(-1.0817%)

20760

Exxon Mobil Corp

XOM

83.55

0.10(0.1198%)

2850

Facebook, Inc.

FB

127.51

-0.45(-0.3517%)

100529

Ford Motor Co.

F

12.11

-0.06(-0.493%)

21663

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

10.66

0.03(0.2822%)

53836

General Electric Co

GE

29.76

-0.13(-0.4349%)

6251

General Motors Company, NYSE

GM

32.05

-0.07(-0.2179%)

1099

Goldman Sachs

GS

164

-1.13(-0.6843%)

2460

Google Inc.

GOOG

784.23

-2.67(-0.3393%)

1423

Home Depot Inc

HD

127.2

-0.59(-0.4617%)

938

Intel Corp

INTC

37.06

-0.13(-0.3496%)

27261

International Business Machines Co...

IBM

154.43

-0.55(-0.3549%)

455

Johnson & Johnson

JNJ

118.7

-0.11(-0.0926%)

406

McDonald's Corp

MCD

117.01

-0.16(-0.1366%)

250

Microsoft Corp

MSFT

57.28

-0.15(-0.2612%)

3288

Nike

NKE

54.72

-0.43(-0.7797%)

4861

Pfizer Inc

PFE

33.78

-0.48(-1.4011%)

21301

Starbucks Corporation, NASDAQ

SBUX

54.02

-0.41(-0.7533%)

1927

Tesla Motors, Inc., NASDAQ

TSLA

206.26

-1.19(-0.5736%)

5498

Twitter, Inc., NYSE

TWTR

21.71

-0.91(-4.023%)

1559989

Verizon Communications Inc

VZ

52.5

-0.06(-0.1142%)

303

Visa

V

82.2

-0.34(-0.4119%)

2477

Wal-Mart Stores Inc

WMT

72.2

-0.15(-0.2073%)

830

Walt Disney Co

DIS

92.6

-0.67(-0.7183%)

8644

Yahoo! Inc., NASDAQ

YHOO

42.3

-0.50(-1.1682%)

17268

Yandex N.V., NASDAQ

YNDX

21.52

-0.05(-0.2318%)

1400

-

15:08

Upgrades and downgrades before the market open

Upgrades:

AT&T (T) upgraded to Hold from Reduce at HSBC Securities

Downgrades:

Walt Disney (DIS) downgraded to Hold from Buy at Drexel Hamilton

Twitter (TWTR) downgraded to Underperform from Perform at Oppenheimer

Other:

NIKE (NKE) removed from Focus List at JP Morgan

Amazon (AMZN) target raised to $960 from $900 at Cowen; maintain Outperform

-

15:08

FOMC, Lacker: I thought the case was strong this past week for another increase

"I thought the case was strong this past week for another increase. Given how tight labor markets are, given how close we are to our inflation target, our benchmarks point to interest rates that are substantially higher than they are now and I think we need to get on with it."

-

15:05

Shares of Deutsche Bank (DB) in premarket trading dropped to 20-year low

Deutsche Bank shares recorded a decline of 6.5%, reaching the lowest value in more than 20 years. According to the information by CNNMoney, the cause of the collapse was the message of the German government that will not interfere in the dispute with the United States Department of Justice, which requires from Deutsche Bank (DB) compensation in the amount of $ 14 billion, for dubious operations of mortgage loans, which led to the housing market crisis and the fall of 2008.

The German government refused to comment on the information.

DB's shares fell in premarket trading to $ 12.00 (-5.88%).

-

13:53

Orders

EUR/USD

Offers : 1.1250-55 1.1280 1.1300 1.1320 1.1350

Bids : 1.1220 1.1200 1.1185 1.1150 1.1130 1.1100 1.1080 1.1050

GBP/USD

Offers : 1.2950 1.2980-85 1.3000 1.3020-251.3050-55 1.3080-85 1.3100

Bids : 1.2915 1.2900 1.2880 1.2865 1.2850 1.2830 1.2800

EUR/GBP

Offers : 0.8700 0.8720-25 0.8750 0.8765 0.8785 0.8800

Bids : 0.8680 0.8665 0.8645-50 0.8630 0.8600 0.8580 0.8565 0.8540 0.8520 0.8500

EUR/JPY

Offers : 113.30 113.50 113.85 114.00 114.20 114.50 114.80-85 115.00

Bids : 112.80-85 112.50 112.35 112.00 111.80 111.50 111.30 111.00

USD/JPY

Offers : 100.85 101.00 101.25-30 101.50 101.80 102.00

Bids : 100.45-50 100.20 100.00 99.80 99.65 99.50-55 99.30 99.00

AUD/USD

Offers : 0.7630 0.7650-55 0.7680 0.7700 0.7725-30 0.7750

Bids : 0.7600 0.7585 0.7565 0.7550 0.7530-35 0.7500

-

13:47

This Can Trigger A Sharp EUR Rally Next Year; How To Position? - SocGen

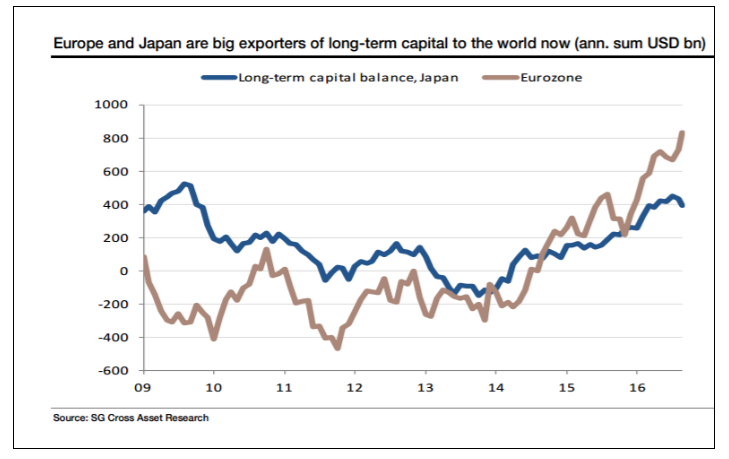

"The chart below shows net annual long-term (direct and portfolio investment) capital outflows from Japan, in US dollars. The switch from net importer of capital to exporter in 2014 helped weaken the Yen and the Euro. It still provides a lot of fuel for risk assets everywhere.

But if massive capital outflows merely keep EUR/USD in a stifling range, isn't the risk at some point in the next year, that any hiccup in those flows triggers a sharp Euro rally?

A Euro surge would catch just as many people off guard as the yen move did. The best way to position for this is to be long EUR/GBP".

Copyright © 2016 Societe Generale, eFXnews™

-

13:45

Arab members of OPEC are working to help the oil market - UAE energy minister

-

13:12

WSE: Mid session comment

The first half of today's trading on the Warsaw Stock Exchange was marked by deepening, following by similar behavior of environment, discounts.

The September reading of the German Ifo index surprised positively with respect to forecasts and the index has gained significantly in relation to the level a month ago. The impact of these data on the market was not significant, although the euro slightly strengthened. Today, new historical lows reached the shares of Deutsche Bank after the press releases, that Angela Merkel does not agree on a plan support the bank by the state.

On the Warsaw market, the half of the session brought a turnover of barely PLN 146 million in the segment of blue chips, while the WIG20 index was at the level of 1,739 points (-1.31%).

-

13:07

Major European stock indices trading in the red zone

European stock markets started trading with a negative dynamic, since the reduction in the shares of major banks and energy companies weighed on the stock exchange in the region.

Investors evaluate data on German business climate, as well as the expected long-awaited presidential debate in the United States.

According to Ifo institute IFO the index of confidence of German businessmen rose to 109.5 points - the highest level since May 2014 - as compared with 106.3 points a month earlier.

Tonight at Hofstra University in New York will be the first debate of the US presidential candidates Hillary Clinton and Donald Trump.

The composite index of the largest companies in the region Stoxx Europe 600 fell during trading on 1,5% - to 340.29 points.

Shares of Deutsche Bank collapsed in price to a record low of 10.65 euros, to the 08:40 GMT decrease their value exceeded 5%.

Earlier, the German magazine Focus reported that German Chancellor Angela Merkel ruled out the possibility of granting state aid to Deutsche Bank, from which US regulators require the payment of $ 14 billion as part of the settlement of claims in the case of manipulating prices for mortgage securities in the period before the 2008 crisis.

On Friday, ratings agency Fitch said that the key risks for the banking sector in Germany are ultra-low interest rates, putting pressure on the profits of banks, as well as regulatory pressures and stiff competition.

In the case of Deutsche Bank agency also noted the problems associated with significant costs and expenses.

Shares of other European banks also fell today. Quotes Commerzbank Securities, BNP Paribas and Lloyds Banking Group fell by 4.5%, 4.3% and 3.1%.

Shares of oil companies are also cheaper in the course of trading on the background of the high volatility of oil prices before the upcoming meeting of oil producing countries in Algiers.

The cost of BP shares fell to 1,6%, Royal Dutch Shell - by 1.6%.

Oil prices, which rose in the morning about 1%, sharply reduced growth during the session amid experts doubt the success of the upcoming talks between the oil-producing countries.

"We are skeptical about the possibility of reaching an agreement this week", - said a senior analyst at IronFX Global Charalambos Pissuros.

German Lanxess shares rose 7.9%. German specialty chemicals group announced the purchase of its US Chemtura Corp., the transaction amount will be about 2.4 billion euros ($ 2.7 billion).

At the moment:

FTSE 6838.24 -71.19 -1.03%

DAX 10479.33 -147.64 -1.39%

CAC 4418.23 -70.46 -1.57%

-

13:03

Iran wants to regain market share by next OPEC meeting - Livesquawk

-

11:45

Jordan: Financial market infrastructures: Walking the line between stability and innovation

"Financial market infrastructures are vital for various Swiss National Bank (SNB) activities, including the implementation of monetary policy. This part of the financial sector also stands to be affected by the rapid changes currently taking place in financial technology. Technological innovations are thus highly relevant for the SNB. The SNB's task is to strike the right balance between maintaining stable conditions and promoting useful innovation.

Although the financial industry's core functions - funding new investments, offering investment and asset protection strategies, and executing payments - will remain largely unchanged, the technologies and channels by which it delivers these services are changing. The challenge for regulators and central banks is to make sure they fully understand the effects - and side-effects - of these new mechanisms at an early stage. Central banks and regulators have a duty to protect the safety of financial market infrastructures, but they also have a duty to ensure that they operate efficiently.

Until recently, financial market infrastructures had been moving towards centralisation. However, technological progress could reverse this trend, making decentralisation the new paradigm. The keywords here are 'distributed ledger' and 'blockchain'. There will nevertheless continue to be a role for centralised infrastructures, which already operate at low cost and meet high safety standards. It is, however, possible that we will see conventional and new technologies co-existing or even blending in the future. Such new technology is particularly relevant for central banks in the context of the ongoing debate about central bank money potentially being issued via a distributed ledger. This issue raises a host of central bank-specific questions that will need to be examined in more detail. The SNB is following and analysing developments in this arena closely and is actively involved in discussions with market participants, regulators and other central banks.

Certain other developments are already having a tangible effect on financial market infrastructures - for instance on cashless payment systems - and, this, in turn, has ramifications for the SNB. According to its mandate, the SNB is obliged to facilitate and secure the operation of such systems. In April of this year, the latest generation of the Swiss Interbank Clearing (SIC) system, which operates under the strategic guidance of the SNB, was launched. Support for emerging messaging standards and plans to extend SIC's operating hours next year will set the stage for cashless payment innovations which will ultimately benefit companies as well as private customers.

For financial market infrastructure innovations to be successful, market participants, regulators and central banks must all be convinced they are both safe and efficient. It is therefore essential that these parties maintain an active dialogue".

-

11:00

Option expiries for today's 10:00 ET NY cut

EUR/USD: 1.1170 (367m) 1.1250 (224m) 1.1325 (207m)

USD/JPY: 99.00 (USD 610m) 99.80-81 (640m) 100.00 (627m) 100.50-60 (USD 220m) 101.00 (411m) 102.00 (262m) 102.21 (360m)

AUD/USD 0.7500 (AUD 610m)

NZD/USD 0.7300 (248m) 0.7335-41 (249m)

USD/CAD 1.3300 (USD 590m)

EUR/JPY 113.15 (798m)

AUD/JPY 75.50-60 (531m)

-

10:45

German business confidence improved in September

According to rttnews, German business confidence improved in September, reports said citing survey data from Ifo institute on Monday.

The business sentiment index rose to 109.5 in September, while the score was forecast to remain unchanged at August's initially estimated value of 106.2.

The current conditions index came in at 114.7 versus 112.8 a month ago. The reading was forecast to rise to 113.

The expectations indicator climbed to 104.5 from 100.1 in August. The expected reading was 100.0.

-

10:44

UK mortgage approvals down slightly

-

Gross mortgage borrowing of £12.4bn in the month was 1% higher than in August 2015.

-

Net mortgage borrowing is just under 3% higher than a year ago.

-

Consumer credit continues to show annual growth of over 6% reflecting fairly strong retail sales and in the case of personal loans and overdrafts favourable interest rates.

Dr Rebecca Harding, Chief Economist at the BBA, said:

"The High Street Banking statistics published today point to a softer housing market, strong consumer credit and slightly weaker business borrowing in August. The data was collected before the Bank of England reduced interest rates to 0.25% and so give an indication of some of the underlying pressures that the MPC was responding to when it made this decision.

"Mortgage borrowing is growing at a slower pace than it has for the last few months reflecting both the slowdown in housing market growth after the April spike and broader trends in the sector".

-

-

10:24

Oil higher in early trading

This morning, New York crude oil futures for WTI rose by + 0.20% to $ 44.60 and Brent crude oil futures rose in price by 0.06% to $ 46.51 per barrel. Thus, the black gold is trading in the green zone on the background of statements by the Algerian Minister of Energy on the informal meeting of OPEC on Monday, who said that all possible options regarding the reduction or freezing of production are open. Recall that the OPEC countries will meet on the sidelines of the International Energy Forum in Algiers on 26-28 September to discuss the potential and the limitation of the production agreement. It will be a close call as Saudi Arabia does not expect the adoption of any decision in Algeria, but it is ready to cut production volumes, if Iran will join the agreement this year, Reuters writes.

-

10:16

Italian retail trade index decreased by 0.3% m/m

The retail trade index measures the monthly evolution of the turnover at current prices of enterprises with retail sale outlets. With effect from January 2013 the indices are calculated with reference to the base year 2010 using the Ateco 2007 classification (Italian edition of Nace Rev. 2). In July 2016 the seasonally adjusted retail trade index decreased by 0.3% with respect to June 2016 (+0.3% for food goods and -0.5% for non-food goods). The average of the last three months increased with respect to the previous three months (+0.2%). The unadjusted index decreased by 0.2% with respect to July 2015.

-

10:00

Germany: IFO - Business Climate, September 109.5 (forecast 106.4)

-

10:00

Germany: IFO - Current Assessment , September 114.7 (forecast 113)

-

10:00

Germany: IFO - Expectations , September 104.5 (forecast 100.2)

-

09:51

Today’s events

At 11:15 GMT the ECB member Yves Mersch will make a speech

At 12:30 GMT The head of the SNB, Thomas Jordan will deliver a speech

At 16:15 GMT the ECB board member Benoit Coeure deliver a speech

At 16:30 GMT FOMC member Neil Kashkari will deliver a speech

At 17:05 GMT the ECB president Mario Draghi will deliver a speech

At 18:45 GMT FOMC Member Daniel Tarullo deliver a speech

At 20:30 GMT FOMC members Robert Kaplan will deliver a speech

-

09:49

Major stock markets trading in the red zone: FTSE -0.2%, DAX -0.7%, CAC40 -0.8%, FTMIB -0.8%, IBEX -0.9%

-

09:17

WSE: After opening

WIG20 index opened at 1756.50 points (-0.34%)*

WIG 47641.42 -0.47%

WIG30 2020.83 -0.69%

mWIG40 4085.75 0.11%

*/ - change to previous close

The futures market started the new week with a discount of 0.63% to 1,738 points. Contract for the DAX also opened up with a downward gap and lost approx. 0.5%.

The cash market opened with discount at modest turnover. After the first transactions the discount worsened, which compensated the optimistic fixing on Friday. Market returns to the level of 1750 points, which attracts like a magnet. The day in whole of Europe begins with declines. The same today's morning quite clearly indicates how dramatically the mood changed in relation to Thursday of the last week.

After fifteen minutes of trade WIG20 index it was at the level of 1,743 points (-1,09%).

-

09:14

GBP 'Increasingly Unloved', Consider Long EUR/GBP Over Short GBP/USD - RBS

"GBP is feeling increasingly unloved. Downside pressure has been building just above 1.30 in GBP/USD. This week's break appears to have added to the negative sentiment as has a break up through 0.8635 in EUR/GBP. A break of 0.8676 would add to existing negative sentiment.

We believe the reality of Brexit is sinking in after a summer of less political sound-bites.

GBP has also stopped rallying on better data as the focus has turned to the longer term negatives. This week's current account data (that accompany the final estimate of Q2 GDP) will remind investors of the challenges of financing a large deficit.

We see further trade weighted losses for GBP. Currently we have a slight bias to be long EUR/GBP over short GBP/USD".

Copyright © 2016 RBS, eFXnews™

-

08:52

Markets return to normal at the end of September as the big money come back. More volatile times expected

-

08:43

Negative start of trading expected on the major stock exchanges in Europe: DAX futures -0.7%, CAC 40 -0.7%, FTSE -0.5%

-

08:28

WSE: Before opening

The new week on the markets begins with not very good mood. Poor closure of Wall Street on Friday - a decline of 0.6% and closing at daily minima resulted in clearer discounts in Asia. Such a distribution of forces will put pressure on the supply side of the markets in Europe after and so weak session on Friday.

In the macro calendar macro this morning we will know the reading of the Ifo index in Germany. Today begins also the informal meeting of OPEC countries, which will end on Wednesday and will have a major impact on the prices of crude oil, and thus the shares of oil companies. But the most important event of the day will be the first TV debate of the main candidates for president of the United States. It will be held on 21 am New York time (3:00 am Warsaw time). Positive behavior of the markets to maintain US interest rates unchanged, at very quickly gave way to fear of the elections in the US.

On the Warsaw market, the key element is still the level of 1,750 points on the index of the largest companies and the defeat or the lack of such a defeat will decide on the next trend on the Warsaw parquet.

-

08:15

Former Japan Minister of Finance, Eysuke Sakakibara: Yen slowly but surely to around Y90 in 2017

Today, the former Minister of Finance , Eysuke Sakakibara, known among traders by the nickname "Mr. Yen" gave a short interview. The official said that in his forecast of 2017, the yen will slowly but surely come to around Y90. Sakakibara said the yen to Y95-Y100 range is very favorable for the Japanese economy and can provide the necessary minimum rise of 1% of GDP. Also he supported the recent decision of the Bank of Japan, and said that the regulator is monitoring the situation on the currency market.

-

08:12

3 Reasons Why JPY Will Weaken M-Term On BoJ New Policy Framework - Nomura

"The BOJ's new policy framework aims to improve the sustainability of its easing, as the Bank acknowledges the battle to reach the price target may be more prolonged. The transformation was inevitable sooner rather than later, and the BOJ made the initial step relatively smoothly, avoiding volatility in bond and equity markets. At the same time, the decision does not necessarily add much fresh stimulus to the economy, and we judge this preparation for a prolonged fight means less frequent policy reactions going forward. Thus, we expect the immediate impact on JPY to be limited.

Nonetheless, the improved sustainability under the new policy framework will enable JPY weakness in the medium term, as 1) it avoids the danger of deterioration in risk sentiment by sudden tapering, 2) the policy rate cut will be less harmful for the financial sector, and 3) expectations for joint efforts by the BOJ and the government will continue.

As a result, when positive external developments, such as US rate hikes and a reduction in US political uncertainty, occur, Japanese investment in foreign assets with no FX hedging could accelerate more easily. Carry trade-type JPY selling should also become gradually easier. The BOJ's commitment to maintaining stability in the JGB market will be the key to success".

Copyright © 2016 Nomura, eFXnews™

-

08:09

BOJ's Kuroda: ready to use every possible policy tool if needed

-

there's no limit to monetary policy

-

BOJ to relentlessly pursue innovation

-

can accelerate monetary base expansion if necessary along with more asset purchases

-

main tool for more easing still deepening neg rate cuts and lowering long term rate target

-

shape, locations of yield curve will broadly remain as they are at present

-

large scale monetary easing will be in place until observed CPI stays above 2% in stable manner

*via forexlive -

-

08:08

Saudis Willing to Act on ‘Critical’ Oil Market, Algeria Says - Bloomberg

-

08:07

New Zeeland's trade balance deficit increased more than expected

For August 2016 compared with August 2015:

Goods exports fell $323 million to $3.4 billion.

-

Milk powder, butter, and cheese led the fall, down $135 million (22 percent).

-

Meat and edible offal fell $111 million (26 percent), with falls in beef and lamb.

-

Logs, wood, and wood articles rose $102 million (34 percent), led by untreated logs.

Goods imports fell $148 million to $4.7 billion.

-

Capital goods led the fall in imports, down $195 million (45 percent).

-

Crude oil fell $106 million (38 percent) in value and 16 percent in quantity.

-

Excluding petroleum products and aircraft and parts, goods imports rose $182 million (4.4 percent).

The monthly trade balance was a deficit of $1.3 billion (37 percent of exports).

The trade weighted index rose 9.2 percent from August 2015.

Milk powder exports fell in August 2016 to the lowest level since August 2009, contributing to a large 8.7 percent fall in the monthly value of exports when compared with August 2015, Statistics New Zealand said today.

-

-

07:16

Japan: Coincident Index, July 112.1 (forecast 112.8)

-

07:06

Options levels on monday, September 26, 2016:

EUR/USD

Resistance levels (open interest**, contracts)

$1.1341 (2636)

$1.1316 (2222)

$1.1288 (1073)

Price at time of writing this review: $1.1228

Support levels (open interest**, contracts):

$1.1173 (3927)

$1.1134 (3243)

$1.1090 (7019)

Comments:

- Overall open interest on the CALL options with the expiration date October, 7 is 36626 contracts, with the maximum number of contracts with strike price $1,1400 (4957);

- Overall open interest on the PUT options with the expiration date October, 7 is 39349 contracts, with the maximum number of contracts with strike price $1,1100 (7019);

- The ratio of PUT/CALL was 1.07 versus 1.05 from the previous trading day according to data from September, 23

GBP/USD

Resistance levels (open interest**, contracts)

$1.3202 (1398)

$1.3105 (996)

$1.3009 (542)

Price at time of writing this review: $1.2981

Support levels (open interest**, contracts):

$1.2894 (914)

$1.2797 (1761)

$1.2698 (1424)

Comments:

- Overall open interest on the CALL options with the expiration date October, 7 is 26547 contracts, with the maximum number of contracts with strike price $1,3500 (3374);

- Overall open interest on the PUT options with the expiration date October, 7 is 22321 contracts, with the maximum number of contracts with strike price $1,3000 (3590);

- The ratio of PUT/CALL was 0.84 versus 0.85 from the previous trading day according to data from September, 23

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

07:06

Global Stocks

European stocks moved decisively lower on Friday, giving back a chunk of the prior day's rally after economic data painted a mixed picture of the region's recovery. The week's gains came as the U.S. Federal Reserve refrained from raising interest rates and indicated it would keep monetary policy loose for at least another few months. Traders in Europe and the U.K. closely watch where U.S. interest rates are headed, as they are a major driver for the global economy and currency markets.

U.S. stocks closed near session lows Friday, with investor sentiment hit by a renewed slide in crude-oil prices. Reports that major oil producers are not likely to reach an agreement to freeze production at a meeting this weekend resulted in the largest one-day loss for oil futures since mid-July.

Asian shares were broadly lower Monday, following declines in U.S. stocks on Friday and amid nervousness about the state of global oil markets. The Organization of the Petroleum Exporting Countries gathers for an informal meeting this week in Algiers, with production cuts likely up for discussion.

-

07:02

Japan: Leading Economic Index , July 100 (forecast 100)

-

00:45

New Zealand: Trade Balance, mln, August -1265

-

00:31

Commodities. Daily history for Sep 23’2016:

(raw materials / closing price /% change)

Oil 44.72 +0.54%

Gold 1,341.50 -0.01%

-

00:30

Stocks. Daily history for Sep 23’2016:

(index / closing price / change items /% change)

Nikkei 225 16,754.02 -53.60 -0.32%

Shanghai Composite 3,033.79 -8.52 -0.28%

S&P/ASX 200 5,431.30 +56.84 +1.06%

FTSE 100 6,909.43 -1.97 -0.03%

CAC 40 4,488.69 -21.13 -0.47%

Xetra DAX 10,626.97 -47.21 -0.44%

S&P 500 2,164.69 -12.49 -0.57%

Dow Jones Industrial Average 18,261.45 -131.01 -0.71%

S&P/TSX Composite 14,697.93 -99.25 -0.67%

-

00:28

Currencies. Daily history for Sep 23’2016:

(pare/closed(GMT +3)/change, %)

EUR/USD $1,1228 +0,19%

GBP/USD $1,2963 -0,87%

USD/CHF Chf0,9703 +0,18%

USD/JPY Y100,99 +0,21%

EUR/JPY Y113,40 +0,40%

GBP/JPY Y130,92 -0,65%

AUD/USD $0,7621 -0,26%

NZD/USD $0,7243 -0,95%

USD/CAD C$1,3165 +0,90%

-

00:01

Schedule for today,Monday, Sep 26’2016

05:00 Japan Coincident Index (Finally) July 111.1 112.8

05:00 Japan Leading Economic Index (Finally) July 99.2 100

08:00 Germany IFO - Current Assessment September 112.8 113

08:00 Germany IFO - Expectations September 100.1 100.2

08:00 Germany IFO - Business Climate September 106.2 106.4

09:30 Switzerland SNB Chairman Jordan Speaks

14:00 Eurozone ECB President Mario Draghi Speaks

14:00 U.S. New Home Sales August 654 597

23:10 Canada BOC Gov Stephen Poloz Speaks

-