Noticias del mercado

-

23:59

Schedule for today, Tuesday, Jul 28’2015:

(time / country / index / period / previous value / forecast)

08:30United Kingdom GDP, y/y (Preliminary) Quarter II 2.9% 2.6%

08:30 United Kingdom GDP, q/q (Preliminary) Quarter II 0.4% 0.7%

12:30 Canada Industrial Product Price Index, y/y June -1.3%

12:30 Canada Industrial Product Price Index, m/m June 0.5% 0.4%

12:30 Canada Raw Material Price Index June 4.4%

13:00 U.S. S&P/Case-Shiller Home Price Indices, y/y May 4.9% 5.6%

13:45 U.S. Services PMI (Preliminary) July 54.8 55.0

14:00 U.S. Richmond Fed Manufacturing Index July 6

14:00 U.S. Consumer confidence July 101.4 100

20:30 U.S. API Crude Oil Inventories July 2.3

23:50 Japan Retail sales, y/y June 3.0% 0.5%

-

21:00

DJIA 17436.72 -131.81 -0.75%, S&P 500 2069.18 -10.47 -0.50%, NASDAQ 5043.92 -44.71 -0.88%

-

20:20

American focus: the dollar fell

The US dollar fell against the euro and the yen, as investors took profits after recent gains amid fears that China's stock market volatility may deter the Federal Reserve from raising interest rates in the United States in the coming months.

The Chinese stock market on Monday suffered the biggest losses since 2007. Stock indexes have fallen by 8.5% on concerns that the government will postpone the implementation of measures to support the market. Some investors believe that the instability of the stock market in China will make the Fed more cautious when it comes to the matter of tightening monetary policy. This prompted them to sell dollars and buy euros and yen. The prospect of a rate hike in September to support the dollar in recent weeks, as the higher cost of borrowing makes the dollar more attractive to investors seeking to return.

Investors are waiting for the completion of the Fed meeting on Wednesday, as they look for new clues about the timing of rate increases. Fed Chairman Janet Yellen, speaking in Congress earlier this month, stressed that it expects the central bank will raise the fed funds rate at some point before the end of the year.

Little support for the dollar during trading had strong data on orders for durable goods. The volume of orders for durable goods increased significantly in June, offsetting with the fall in the previous two months. This was reported in the statement of the Ministry of Commerce.

According to data seasonally adjusted new orders for durable goods rose in June by 3.4% compared with a decrease of 2.2% in the previous month (revised from -1.8%). Economists had expected orders to increase by 3.0%.

Recall data on orders for durable goods are highly volatile and often revised, making them difficult to analyze. However, other recent reports indicate that the manufacturing sector improves.

The Ministry of Commerce said that the June change partly reflects the increase in demand for airplanes. Orders for non-military aircraft and parts rose 66.1% in June. Separately, Boeing Corporation announced that it has received 161 orders for the aircraft in June to 11 in May.

Excluding the transportation sector, orders rose by 0.8%, recording the largest increase since August 2014. Meanwhile, with the exception of the defense sector, orders rose 3.8%.

A key indicator of business investment also improved in June - orders for non-military capital goods excluding aircraft rose 0.9% after falling 0.4% in May.

Today's report adds to signs that US manufacturers can overcome the difficulties of the strong dollar, harsh winter weather and a drop in oil prices. However, the data also showed that in the first half of 2015, new orders were down 2% compared to the same period in 2014.

Meanwhile, support for the euro has had a report on Germany. The research results presented by the Munich institute IFO, have shown that the index of business sentiment in Germany rose unexpectedly in July, recording the first increase since April. According to the data, the July business climate index rose to 108.0 level against 107.5 in June (revised from 107.4). The latter value was the highest since May this year. Analysts had expected the index to fall to 107.2 points. The current conditions index from the IFO rose in July by 0.8 points, to 113.9 points, while the expectations index jumped to 102.4 points from 102.1 (revised from 102.0). It forecasts a decline of data rate to 113 and 101.8, respectively. "Business expectations were somewhat more optimistic, after declining for three consecutive months. The recent easing concerns about Greece helped to improve sentiment," - said in a press release IFO.

Focus has also proved statistics for the euro area. A report published by the ECB showed that the growth rate of the monetary aggregate M3 remained in June at 5.0%. Experts expect that this figure will increase by 5.2%. In the period from April to June, the average annual growth rate of M3 was 5.1%. Regarding the main components of M3, the growth rate of M1 increased to 11.8% in June from 11.2% in May. The growth rate of short-term deposits other than overnight deposits (M2-M1) amounted to -4.3% in June, against -4.2% in the previous month. We also learned that the annual growth rate of deposits placed by households stood at 3.0% in June compared with 2.9% in the previous month, while the annual growth rate of deposits placed by non-financial corporations slowed to 4.2% from 4.3% in May. Meanwhile, the ECB reported that the growth rate of credit to the government accelerated to 5.3% from 4.1% in May, while the pace of lending to the private sector slowed to 0.1% from 0.2%.

-

19:20

Europe stocks close 2% down after China rout

European stock closed lower on Monday, after a sharp selloff in Asian shares highlighted concerns about Chinese market volatility and slowing growth.

The pan-European FTSEurofirst 300 provisionally closed 2.1 percent lower, while the Germany's DAX and France's CAC closed respectively 2.4 percent and 2.5 percent lower.

The U.K.'s benchmark FTSE outperformed its euro zone peers, but still closed unofficially down 1.0 percent.

Stocks across Europe, the U.S. and Asia tumbled after China's Shanghai Composite tanked to close 8.5 percent down at a three-week low. This added to the sharp losses seen by the index in recent weeks as the fall in commodity prices saps risk appetite.

Declines in the Shanghai Composite quadrupled during its afternoon session, as official data showed China's industrial profits declined 0.3 percent year-on-year in June, after rising in April and May.

Earnings season continued in Europe, with some companies warning of the impact of the slowing Chinese economy. These included French autos supplier Valeo on Monday, which closed 5.4 percent down at the bottom of the CAC after releasing its first-half earnings.

The FTSE's weakest performers were Pearson and Merlin Entertainments.

The former closed down 4.8 percent after confirming it was in talks to sell its 50 percent stake in The Economist, having announced the sale of the Financial Times Group to Nikkei last week.

Merlin Entertainments shares, meanwhile, closed down 4.3 percent after a profit warning was released. Its shares tumbled as much as 7.8 percent in early trading, its worst ever one-day drop.

Better news came from Swiss banking giant, UBS, which reported better-than-expected earnings. However, shares in the bank closed down around 1.6 percent. UBS results came a day earlier than expected, following a report in Swiss paper Sonntagszeitung.

-

18:29

WSE: Session Results

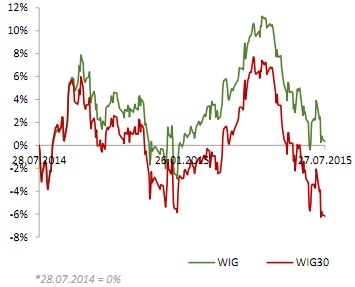

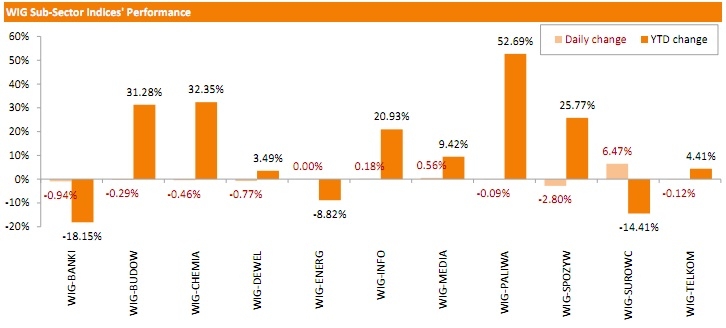

Polish equity market continued to slide on Monday. The broad market measure, the WIG Index, lost 0.23%. Sector-wise, materials (+6.47 %) fared the best, while food sector names (-2.80%) lagged behind.

The large-cap stocks fell by 0.1%. Within the index components, KERNEL (WSE: KER) recorded the biggest drop, down 4.89%. It was followed by banking names HANDLOWY (WSE: BHW) and ING BSK (WSE: ING), plunging by 3.95% and 2.86% respectively. On the other side of the ledger, KGHM (WSE: KGH) became the session's best performer, as its quotations skyrocketed by 8.05%, buoyed by announcement the opposition Law and Justice Party motioned to abolish a mining tax for cooper and silver producers. PGNIG (WSE: PGN), BORYSZEW (WSE: BRS), TAURON PE (WSE: TPE), CYFROWY POLSAT (WSE: CPS) and MBANK (WSE: MBK) did well too, posting 1%-2% gains.

-

18:24

Wall Street. Major U.S. stock-indexes fell

Wall Street fell on Monday and fell sharply on concerns about China's slowing growth in the wake of the biggest drop in Shanghai shares in eight years. The Dow Jones industrial average fell to its lowest level in over five months while the Nasdaq composite was at a four-week low and the S&P 500 touched its lowest in more than two weeks. Chinese shares tumbled more than 8% as an unprecedented government rescue plan to prop up valuations abruptly ran out of steam, raising doubts about the viability of Beijing's efforts to stave off a deeper crash.

Almost all of Dow stocks in negative area (24 of 30). Top looser - The Boeing Company (BA, -1.78%). Top gainer - Intel Corporation (INTC, +0.92).

Almost all of S&P index sectors also in negative area. Top looser - Conglomerates (-1.6%). Top gainer - Utilities (+1.1%).

At the moment:

Dow 17363.00 -160.00 -0.91%

S&P 500 2062.75 -14.75 -0.71%

Nasdaq 100 4519.25 -42.50 -0.93%

10 Year yield 2,24% -0,03

Oil 47.60 -0.54 -1.12%

Gold 1095.50 +10.00 +0.92%

-

18:00

European stocks closed: FTSE 100 6,505.13 -74.68 -1.13 %, CAC 40 4,927.60 -129.76 -2.57 %, DAX 11,056.40 -291.05 -2.56 %

-

15:50

Сегодня в 14:00 GMT истекает срок действия следующих опционов:

EUR/USD: $1.0800(E2.0bn), $1.0850(E1.0bn), $1.0900(E1.2bn), $1.0925(E754mn), $1.1000(E1.19bn)

USD/JPY: Y122.50($550mn), Y124.00 ($321mn), Y125.00($300mn)

GBP/USD: $1.5750(Gbp240mn)

NZD/USD: $0.6660(NZ$270mn)

USD/CAD: C$1.3100(250mn), C$1.3200($450mn)

-

15:40

U.S. Stocks open: Dow -0.81%, Nasdaq -1.04%, S&P -0.67%

-

15:29

U.S. stock-index futures fell after the biggest slump in eight years for Chinese equities amid concern over the nation’s economic growth.

Global Stocks:

Nikkei 20,350.1 -194.43 -0.95%

Hang Seng 24,351.96 -776.55 -3.09%

Shanghai Composite 3,725.56 -345.35 -8.48%

FTSE 6,534.28 -45.53 -0.69%

CAC 4,960.44 -96.92 -1.92%

DAX 11,138.09 -209.36 -1.84%

Crude oil $47.34 (-1.66%)

Gold $1090.10 (+0.42%)

-

15:09

Wall Street. Stocks before the bell

(company / ticker / price / change, % / volume)

Microsoft Corp

MSFT

46.05

+0.24%

20.2K

Deere & Company, NYSE

DE

92.75

+0.36%

2.2K

UnitedHealth Group Inc

UNH

117.94

0.00%

0.3K

Merck & Co Inc

MRK

57.41

0.00%

0.3K

McDonald's Corp

MCD

96.01

-0.09%

1.2K

Intel Corp

INTC

28.02

-0.14%

3.9K

Amazon.com Inc., NASDAQ

AMZN

528.70

-0.14%

60.6K

AT&T Inc

T

34.23

-0.18%

56.1K

General Motors Company, NYSE

GM

31.00

-0.19%

10.0K

Johnson & Johnson

JNJ

98.95

-0.20%

0.6K

The Coca-Cola Co

KO

40.34

-0.25%

1.4K

Walt Disney Co

DIS

118.60

-0.26%

8.7K

Nike

NKE

112.69

-0.27%

1.6K

Procter & Gamble Co

PG

80.05

-0.30%

1.7K

United Technologies Corp

UTX

98.98

-0.33%

5.0K

International Business Machines Co...

IBM

159.15

-0.38%

3.9K

3M Co

MMM

148.75

-0.39%

0.2K

Cisco Systems Inc

CSCO

28.29

-0.39%

1.7K

Verizon Communications Inc

VZ

45.86

-0.39%

12.7K

Google Inc.

GOOG

621.13

-0.39%

10.9K

E. I. du Pont de Nemours and Co

DD

56.71

-0.40%

1.5K

Starbucks Corporation, NASDAQ

SBUX

57.06

-0.40%

15.7K

American Express Co

AXP

75.55

-0.46%

2.4K

Pfizer Inc

PFE

34.10

-0.47%

1.0K

Home Depot Inc

HD

113.00

-0.52%

0.1K

ALTRIA GROUP INC.

MO

53.50

-0.54%

0.4K

Boeing Co

BA

143.18

-0.61%

1.9K

Twitter, Inc., NYSE

TWTR

35.19

-0.65%

5.1K

Wal-Mart Stores Inc

WMT

71.11

-0.66%

0.2K

Goldman Sachs

GS

205.93

-0.68%

1.0K

Travelers Companies Inc

TRV

104.54

-0.69%

0.2K

Ford Motor Co.

F

14.29

-0.69%

37.9K

Facebook, Inc.

FB

96.27

-0.70%

74.2K

HONEYWELL INTERNATIONAL INC.

HON

102.04

-0.71%

0.1K

Exxon Mobil Corp

XOM

79.30

-0.80%

8.7K

JPMorgan Chase and Co

JPM

68.36

-0.80%

4.2K

ALCOA INC.

AA

09.73

-0.82%

17.4K

Chevron Corp

CVX

89.85

-0.83%

12.9K

General Electric Co

GE

25.54

-0.83%

13.5K

Visa

V

74.17

-0.84%

6.8K

AMERICAN INTERNATIONAL GROUP

AIG

63.00

-1.01%

0.1K

Citigroup Inc., NYSE

C

58.11

-1.01%

4.0K

Barrick Gold Corporation, NYSE

ABX

07.17

-1.10%

58.9K

Apple Inc.

AAPL

123.10

-1.12%

446.2K

Caterpillar Inc

CAT

75.11

-1.30%

5.1K

Tesla Motors, Inc., NASDAQ

TSLA

261.21

-1.58%

9.5K

Yahoo! Inc., NASDAQ

YHOO

38.18

-1.72%

61.8K

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

12.03

-2.12%

14.5K

Yandex N.V., NASDAQ

YNDX

14.48

-2.43%

4.0K

-

14:58

Upgrades and downgrades before the market open

Upgrades:

Deere (DE) upgraded from Sell to Neutral at Goldman, target raised from $78 to $94

Downgrades:

Other:

AT&T (T) reiterated at Hold at Canaccord Genuity, target raised from $34 to $35

-

14:32

Earnings Season in U.S.: Major Reports of the Week

July 28

Before the Open:

Ford Motor (F). Consensus EPS $0.37, Consensus Revenue $35435.25 mln.

UPS (UPS). Consensus EPS $1.27, Consensus Revenue $14501.55 mln.

Pfizer (PFE). Consensus EPS $0.52, Consensus Revenue $11418.05 mln.

Merck (MRK). Consensus EPS $0.81, Consensus Revenue $9797.65 mln.

DuPont (DD). Consensus EPS $1.22, Consensus Revenue $8982.75 mln.

After the Close:

Twitter (TWTR). Consensus EPS $0.04, Consensus Revenue $481.24 mln.

July 29

After the Close:

Facebook (FB). Consensus EPS $0.47, Consensus Revenue $3985.62 mln.

July 30

Before the Open:

Procter & Gamble (PG). Consensus EPS $0.95, Consensus Revenue $17952.32 mln.

Yandex N.V. (YNDX). Consensus EPS $7.96, Consensus Revenue $13567.68 mln.

July 31

Before the Open:

Exxon Mobil (XOM). Consensus EPS $1.11, Consensus Revenue $77862.33 mln.

Chevron (CVX). Consensus EPS $1.15, Consensus Revenue $30270.89 mln.

-

14:30

U.S.: Durable Goods Orders , June 3.4% (forecast 3%)

-

14:30

U.S.: Durable goods orders ex defense, 3.8%

-

14:30

U.S.: Durable Goods Orders ex Transportation , June 0.8% (forecast 0.5%)

-

14:15

European session review: the US dollar fell against most major currencies

Data

8:00 Eurozone Change in volume of private sector credit, y / y in June 0.5% 0.6% 0.6%

8:00 Eurozone M3 money supply, y / y in June 5.0% 5.2% 5.0%

8:00 Germany IFO business climate index in July 107.5 107.2 108

8:00 Germany IFO current conditions index in July 113.1 113 113.9

8:00 Germany IFO expectations index July 102.1 101.8 102.4

10:00 UK Balance industrial orders Confederation of British Industry in July -7 -10

The euro rose sharply against the US currency, updating the maximum of 14 in July and briefly breaking the mark of $ 1.1100, which is mainly explained by the fall in the dollar Friday on weak data on home sales in the United States. Meanwhile, support for the euro has had a report on Germany. The research results presented by the Munich institute IFO, have shown that the index of business sentiment in Germany rose unexpectedly in July, recording the first increase since April. According to the data, the July business climate index rose to 108.0 level against 107.5 in June (revised from 107.4). The latter value was the highest since May this year. Analysts had expected the index to fall to 107.2 points. The current conditions index from the IFO rose in July by 0.8 points, to 113.9 points, while the expectations index jumped to 102.4 points from 102.1 (revised from 102.0). It forecasts a decline of data rate to 113 and 101.8, respectively. "Business expectations were somewhat more optimistic, after declining for three consecutive months. The recent easing concerns about Greece helped to improve sentiment," - said in a press release IFO.

Focus has also proved statistics for the euro area. A report published by the ECB showed that the growth rate of the monetary aggregate M3 remained in June at 5.0%. Experts expect that this figure will increase by 5.2%. In the period from April to June, the average annual growth rate of M3 was 5.1%. Regarding the main components of M3, the growth rate of M1 increased to 11.8% in June from 11.2% in May. The growth rate of short-term deposits other than overnight deposits (M2-M1) amounted to -4.3% in June, against -4.2% in the previous month. We also learned that the annual growth rate of deposits placed by households stood at 3.0% in June compared with 2.9% in the previous month, while the annual growth rate of deposits placed by non-financial corporations slowed to 4.2% from 4.3% in May. Meanwhile, the ECB reported that the growth rate of credit to the government accelerated to 5.3% from 4.1% in May, while the pace of lending to the private sector slowed to 0.1% from 0.2%.

The yen appreciated strongly against the dollar, reaching the highest level since July 15 as the drop in the Chinese stock markets increased the attractiveness of the yen as a currency of refuge. In addition, the decline has intensified due to the reduction in price of the dollar. Also, investors are waiting for the meeting of the US Federal Reserve and the publication of US GDP data. Tomorrow begins a two-day meeting of the Committee on Open Market Federal Reserve, which will discuss the rise in interest rates and the economy. The Central Bank of the United States can provide more information about its intentions regarding the increase in US interest rates. The Fed signaled that interest rates may increase in September, but investors predict that the central bank is likely to take effect at the December meeting. Rising interest rates in the United States will make the dollar more attractive to investors.

The pound has stabilized near the opening levels against the dollar, as investors take a wait and see stance ahead of the release of tomorrow's GDP report Britain. According to economists, the UK economy is likely to grow much more rapidly in the 2nd quarter after a slight delay in the start of the year. According to the forecast, the UK GDP in the 2nd quarter grew by 0.7% against growth of 0.4% in the 1st quarter.

A slight pressure is applied to the data from the CBI, which showed that the expectations of new orders in the industrial sector in Britain fell unexpectedly in July, reaching a minimum value in the past two years, mainly due to the effect of strengthening the pound on export performance. According to the balance of industrial orders fell this month to a level of -10 compared to -7 in July. The last reading was the lowest since July 2013. Economists had expected the balance slightly improved - to -5. However, the rate is still above the long-term average at -15. Quarterly Review of CBI pointed to the gloomy prospects for the manufacturers. Expectations regarding the volume of export orders in the next three months fell to the lowest level since October 2011.

EUR / USD: during the European session, the pair rose to $ 1.1115

GBP / USD: during the European session, the pair has updated the maximum and minimum, and then stabilized near the opening level

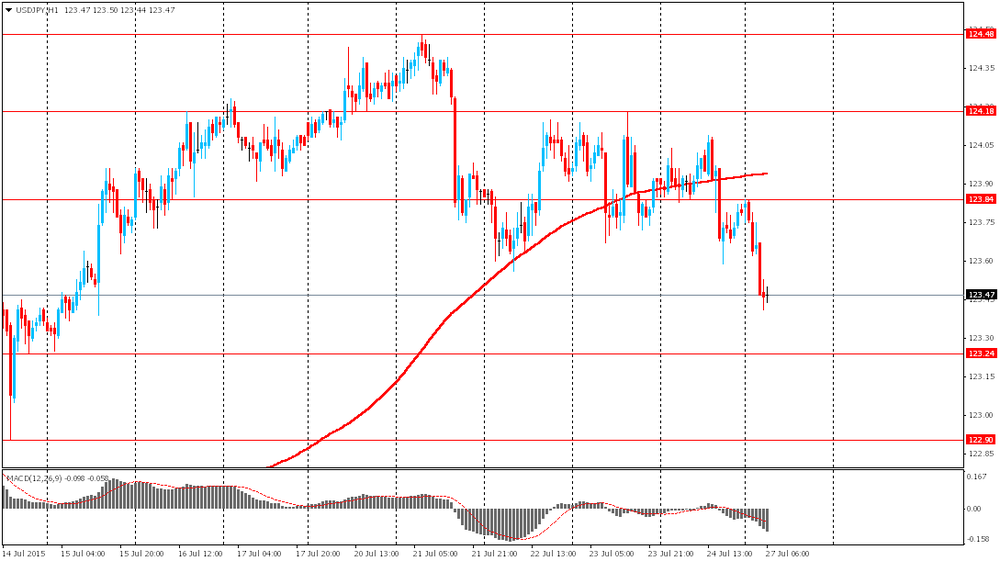

USD / JPY: during the European session the pair fell to Y123.15

At 12:30 GMT the United States will report on orders for durable goods, including excl rd transport in June.

-

14:00

Orders

EUR/USD

Offers 1.1120 1.1160 1.1185 1.1200

Bids 1.1000 1.0980 1.0965 1.0940 1.0900 1.0880 1.0860 1.081.0820-25 1.0800 1.0785 1.0750

GBP/USD

Offers 1.5520-25 1.5550 1.5580 1.5600 1.5625 1.5640-50 1.5680 1.5700-10

Bids 1.5485 1.5450 1.5425-30 1.5400 1.5360 1.5330 1.5300

EUR/GBP

Offers 0.7150-55 0.7180-85 0.7225-30 0.7260 0.7285 0.7300

Bids 0.7120 0.7100 0.7085 0.7065 0.7030 0.7000 0.6975-80

EUR/JPY

Offers 136.85 137.00 137.30 137.50 137.80 138.00

Bids 136.25 136.00 135.80 135.50 135.00 134.85 134.40 134.00

USD/JPY

Offers 123.50-55 123.85 124.00 124.25-30 124.50 124.75 125.00

Bids 123.25-30 123.00 122.80 122.50-60 122.00 121.75 121.50

AUD/USD

Offers 0.7300 0.7325 0.7360 0.7385 0.7400 0.7420-25 0.7450

Bids 0.7265 0.7250 0.7230 0.7200 0.7180 0.7150

-

12:30

Major stock indexes in Europe show a negative trend

European stocks traded in negative territory, approaching its fifth consecutive sessional fall. In the course of trading influence news from the Asia-Pacific region, as well as corporate reports.

"The fall is mainly due to China. I think that many investors expect that the growth of the Chinese economy will continue to slow down, and this slowdown is not yet fully reflected in the quotations of European shares," - said the expert Peregrine & Black Markus Huber. Recall Chinese stocks fell today by 8.5%. In addition, the data showed that the profits of Chinese industrial companies in June decreased by 0.3% per year, after rising 0.6% in May.

Meanwhile, the market was supported by the German statistics. These Munich institute IFO, showed that the index of business sentiment in Germany rose unexpectedly in July, recording the first increase since April. According to the report, the July business climate index rose to a level of 108.0 compared with 107.5 in June (revised from 107.4). The latter value was the highest since May this year. Analysts had expected the index to fall to 107.2 points. The current conditions index from the IFO rose in July by 0.8 points, to 113.9 points, while the expectations index jumped to 102.4 points from 102.1 (revised from 102.0). It forecasts a decline of data rate to 113 and 101.8, respectively. "Business expectations were somewhat more optimistic, after declining for three consecutive months. The recent easing concerns about Greece helped to improve sentiment on the German economy," - said in a press release IFO.

Shares of Swiss bank UBS AG fell 1.2 percent, despite the unexpectedly high quarterly profit. Meanwhile, analysts Citigroup Inc. They noted that a higher than expected amount of profit is likely to be a one-off.

The gauge of banks' shares shows the largest decline among the 19 industry groups. Quotes of German Deutsche Bank and Commerzbank fell 1.7 percent and 2.3 percent, respectively.

The cost of Ryanair Holdings Plc - Europe's largest budget airline - decreased by 0.9 percent since the company announced that the surplus of transport capacity could put pressure on the price of tickets. In the last quarter of the average cost of a ticket on the routes Ryanair declined by 4%.

Paper Merlin Entertainments Plc fell 3.8 percent, which was associated with a decrease in earnings forecast for the current year.

Capitalization of Royal Philips NV - the manufacturer of consumer electronics - increased by 5.0 percent due to higher profit than analysts had expected.

The cost of Reckitt Benckiser Group Plc rose 2.2 percent. The company said that the increase in revenues in the second quarter exceeded the forecasts of experts.

Currently:

FTSE 100 6,568.95 -10.86 -0.17%

CAC 40 4,985.68 -71.68 -1.42%

DAX 11,195.84 -151.61 -1.34%

-

12:00

United Kingdom: CBI industrial order books balance, July -10

-

11:20

Option expiries for today's 10:00 ET NY cut

EUR/USD: $1.0800(E2.0bn), $1.0850(E1.0bn), $1.0900(E1.2bn), $1.0925(E754mn), $1.1000(E1.19bn)

USD/JPY: Y122.50($550mn), Y124.00 ($321mn), Y125.00($300mn)

GBP/USD: $1.5750(Gbp240mn)

NZD/USD: $0.6660(NZ$270mn)

USD/CAD: C$1.3100(250mn), C$1.3200($450mn)

-

10:00

Germany: IFO - Business Climate, July 108 (forecast 107.2)

-

10:00

Eurozone: M3 money supply, adjusted y/y, June 5.0% (forecast 5.2%)

-

10:00

Germany: IFO - Current Assessment , July 113.9 (forecast 113)

-

10:00

Germany: IFO - Expectations , July 102.4 (forecast 101.8)

-

10:00

Eurozone: Private Loans, Y/Y, June 0.6% (forecast 0.6%)

-

09:27

Oil prices remain low

West Texas Intermediate futures for September delivery slid to $48.12 (-0.04%), while Brent crude climbed to $54.74 (+0.22%). Prices of both types of crude remain low amid oversupply concerns. However a weaker dollar limited declines.

Recently the U.S. and Iraq intensified global glut concerns. Baker Hughes reported that U.S. oil producers added 21 drilling rigs last week, marking the biggest rise since April 2014.

Meanwhile Iraq is on track to export a record amount of crude from its southern oilfields in July. It has already topped 3 million barrels per day this month.

Considering these data the National Australia Bank said it expects oil prices to stay below $70 a barrel for the rest of 2015 and 2016.

-

09:09

Gold partly recovered

Gold advanced to $1,102.00 (+1.52%); however it failed to reach far beyond its 5 year-low as the Fed two-day meeting is scheduled for this week. It will end on Wednesday. The central bank of the U.S. is preparing to raise its interest rates; this would weigh on non-interest-paying bullion. Investors expect the Fed to provide some clues on the timing of a rate hike.

HSBC analyst James Steel believes that gold's recovery from last week's declines appears to be mostly driven by short-covering. "So while we think prices may firm near-term, the sell-off does not look as if it's entirely over as we do not yet detect a notable change in investor sentiment." Last week the metal lost more than 3%.

Data from the International Monetary Fund showed Germany cut its gold holdings by 2.395 tonnes last month, while Russia and Kazakhstan continued to add to their reserves.

-

08:49

Global Stocks: U.S. indices weighed on Asian stocks

U.S. stock indices fell on Friday with biotechnology companies leading declines this time.

Biogen dropped 22% on weak sales outlook.

The Dow Jones Industrial Average fell 163.39 points, or 0.9%, to 17568.53 Friday. The S&P 500 declined 22.50 points, or 1.1%, to 2079.65, and the Nasdaq Composite lost 57.78 points, or 1.1%, to 5088.63.

For the week, the Dow Jones lost 2.9%, while the S&P 500 tumbled 2.2%.

In Asia this morning Hong Kong Hang Seng fell 2.67%, or 671.42 points, to 24,457.09. China Shanghai Composite Index fell 3.09%, or 125.63 points, to 3,945.28. The Nikkei lost 1.19%, or 244.77 points, to 20,299.76.

Stocks fell across Asia amid declines in U.S. indices, which were caused by corporate earnings reports. Chinese stocks were also influenced by concerns over activity in the industrial sector of the country's economy. Official data showed that revenues of Chinese industrial companies fell by 0.7% in the first half of the current year compared to last year.

-

08:46

Foreign exchange market. Asian session: the euro gained

The euro advanced against the dollar ahead of German business climate data by IFO. Economists expect the index to come in at 107.2 in July. The index is based on results of survey of 7000 business executives. A reading above 100 suggests that economic growth improves amid business optimism.

The yen rose against the dollar amid declines in Asian stocks and growing demand for this safe-haven currency. Investors are waiting for the Federal Reserve meeting and U.S. GDP data.

A two-day Federal Open Markets Committee meeting starts tomorrow. The central bank of the U.S. may provide more information on its intension regarding the future of interest rates. The Fed signaled that it may raise rates in September, but investors are convinced that the Fed will take this step in December. Higher rates in the U.S. would make the greenback more attractive for investors.

EUR/USD: the pair rose to $1.1015 in Asian trade

USD/JPY: the pair fell to Y123.40

GBP/USD: the pair traded around $1.5515-35

The most important news that are expected (GMT0):

(time / country / index / period / previous value / forecast)

08:00 Eurozone Private Loans, Y/Y June 0.5% 0.6%

08:00 Eurozone M3 money supply, adjusted y/y June 5.0% 5.2%

08:00 Germany IFO - Business Climate July 107.4 107.2

08:00 Germany IFO - Current Assessment July 113.1 113

08:00 Germany IFO - Expectations July 102.0 101.8

10:00 United Kingdom CBI industrial order books balance July -7

12:30 U.S. Durable goods orders ex defense -2.1%

12:30 U.S. Durable Goods Orders June -1.8% 3%

12:30 U.S. Durable Goods Orders ex Transportation June 0.5% 0.5%

-

07:01

Options levels on monday, July 27, 2015:

EUR / USD

Resistance levels (open interest**, contracts)07

$1.1119 (2454)

$1.1068 (1120)

$1.1033 (433)

Price at time of writing this review: $1.1003

Support levels (open interest**, contracts):

$1.0920 (1696)

$1.0871 (3088)

$1.0840 (5713)

Comments:

- Overall open interest on the CALL options with the expiration date August, 7 is 54217 contracts, with the maximum number of contracts with strike price $1,1200 (4082);

- Overall open interest on the PUT options with the expiration date August, 7 is 62849 contracts, with the maximum number of contracts with strike price $1,0800 (5835);

- The ratio of PUT/CALL was 1.16 versus 1.17 from the previous trading day according to data from July, 24

GBP/USD

Resistance levels (open interest**, contracts)

$1.5802 (1805)

$1.5703 (1138)

$1.5606 (2159)

Price at time of writing this review: $1.5527

Support levels (open interest**, contracts):

$1.5394 (1338)

$1.5297 (1373)

$1.5198 (1338)

Comments:

- Overall open interest on the CALL options with the expiration date August, 7 is 22218 contracts, with the maximum number of contracts with strike price $1,5750 (3212);

- Overall open interest on the PUT options with the expiration date August, 7 is 22651 contracts, with the maximum number of contracts with strike price $1,5250 (2086);

- The ratio of PUT/CALL was 1.02 versus 1.03 from the previous trading day according to data from July, 24

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

04:08

Nikkei 225 20,424.69 -119.84 -0.58 %, Hang Sengт24,716.31ь-412.20 -1.64 %, Shanghai Composite 4,004.26 -66.64 -1.64 %

-

00:57

Commodities. Daily history for Jul 24’2015:

(raw materials / closing price /% change)

Oil$47.97-0.35%

Gold$1,098.50+1.20%

-

00:55

Stocks. Daily history for Jul 24’2015:

(index / closing price / change items /% change)

Nikkei 225 20,544.53 -139.42 -0.67 %

Hang Seng -270.34 -1.06 %

S&P/ASX 200 5,566.1 -24.18 -0.43 %

Shanghai Composite 4,070.83 -53.09 -1.29 %

FTSE 100 6,579.81 -75.20 -1.13 %

CAC 40 5,057.36 -29.38 -0.58 %

Xetra DAX 11,347.45 -164.66 -1.43 %

S&P 500 2,079.65 -22.50 -1.07 %

NASDAQ Composite 5,088.63 -57.78 -1.12 %

Dow Jones 17,568.53 -163.39 -0.92 %

-

00:54

Currencies. Daily history for Jul 24’2015:

(pare/closed(GMT +3)/change, %)

EUR/USD $1,0981 -0,02%

GBP/USD 1,5508 -0,04%

USD/CHF Chf0,9626 +0,31%

USD/JPY Y123,79 -0,10%

EUR/JPY Y135,97 -0,09%

GBP/JPY Y191,99 -0,13%

AUD/USD $0,7281 -0,96%

NZD/USD $0,6575 -1,89%

USD/CAD C$1,3045 +0,05%

-