Noticias del mercado

-

21:01

DJIA 17778.40 93.31 0.53%, NASDAQ 4906.55 36.70 0.75%, S&P 500 2069.93 10.19 0.49%

-

18:30

Wall Street. Major U.S. stock-indexes little changed

Major U.S. stock-indexes recouped early losses on Friday, helped by healthcare stocks, as investors assessed data pointing to a strong recovery in the U.S. economy. Gains were limited by a nearly 4 percent fall in crude prices amid increasing skepticism around a deal to freeze crude production. The Labor Department's report showed solid gains in nonfarm payrolls in March, underscoring the economy's resilience amid risks from a weak global economy. While the unemployment rate rose to 5% from an eight-year low of 4.9%, it was because more Americans continued to return to the labor force. A separate report showed the U.S. manufacturing sector resumed growth in March, bolstered by strength in new orders.

Most of Dow stocks in positive area (17 of 30). Top looser - Chevron Corporation (CVX, -1,25%). Top gainer - The Goldman Sachs Group, Inc. (GS, +1,26%).

Most of S&P sectors in negative area. Top looser - Basic Materials (-1,6%). Top gainer - Healthcare (+0,6%).

At the moment:

Dow 17631.00 +36.00 +0.20%

S&P 500 2053.75 +2.25 +0.11%

Nasdaq 100 4498.75 +22.50 +0.50%

Oil 36.99 -1.35 -3.52%

Gold 1217.30 -18.30 -1.48%

U.S. 10yr 1.78 -0.01

-

18:03

European stocks close: stocks closed lower on a fall in oil prices

Stock indices closed lower on drop in oil prices. Oil prices fell on news that Saudi Arabia might not agree to freeze its oil output. Saudi Arabia's deputy crown prince Mohammed bin Salman said in an interview with Bloomberg that the country would only freeze its oil output if Iran and other major oil producers will participate in such deal.

The U.S. labour market data was mixed. According to the U.S. Labor Department's data on Friday, the U.S. economy added 215,000 jobs in March, exceeding expectations for a rise of 205,000 jobs, after a gain of 245,000 jobs in February. February's figure was revised up from a rise of 242,000 jobs.

The U.S. unemployment rate rose to 5.0% in March from 4.9% in February. Analysts had expected the unemployment rate to remain unchanged at 4.9%.

Average hourly earnings in the U.S. increased 0.3% in March, beating forecasts of a 0.2% gain, after a 0.1% decline in February.

As the U.S. labour market continues to strengthen, the Fed could raise its interest rate gradually this year.

Market participants also eyed the economic data from the Eurozone. Markit Economics released its final manufacturing purchasing managers' index (PMI) for the Eurozone on Friday. Eurozone's final manufacturing purchasing managers' index (PMI) climbed to 51.6 in March from 51.2 in February, up from the preliminary reading of 51.4.

The rise was driven by a faster growth in production and new orders.

"Although the PMI ticked higher, March still saw the second-weakest improvement in manufacturing conditions seen for just over a year. The data suggest manufacturing grew by only around 0.2% in the first quarter, acting as a drag on the wider economy," Chris Williamson, Chief Economist at Markit said.

"Policymakers will also be worried by the further intensification of deflationary pressures in manufacturing supply chains, with prices charged at the factory gate falling at the steepest rate since late-2009," he added.

Germany's final Markit/BME manufacturing purchasing managers' index (PMI) rose to 50.7 in March from 50.5 in February, up from the preliminary reading of 50.4. The index was mainly driven by rises in output and new business. Employment declined in March.

France's final manufacturing purchasing managers' index (PMI) decreased to 49.6 in March from 50.2 in February, in line with the preliminary reading. The index was driven by drops in new business and output prices. Output rose slightly.

Markit Economics released its manufacturing purchasing managers' index (PMI) for the U.K. on Friday. The Markit/Chartered Institute of Procurement & Supply manufacturing PMI for the U.K. increased to 51.0 in March from 50.8 in February, missing expectations for a rise to 51.2.

The increase was driven by a rise in new business.

"The UK manufacturing sector remained in the doldrums during the opening quarter of the year. Although March saw modest improvements in the trends for production and new orders, industry is still hovering close to the stagnation mark and will struggle to make a meaningful contribution to the next set of GDP growth figures," Markit's Senior Economist Rob Dobson said.

Indexes on the close:

Name Price Change Change %

FTSE 100 6,146.05 -28.85 -0.47 %

DAX 9,794.64 -170.87 -1.71 %

CAC 40 4,322.24 -62.82 -1.43 %

-

18:00

European stocks closed: FTSE 6146.05 -28.85 -0.47%, DAX 9794.64 -170.87 -1.71%, CAC 40 4322.24 -62.82 -1.43%

-

17:57

Italy’s unemployment rate climbs to 11.7% in February

The Italian statistical office Istat released its unemployment data on Friday. The seasonally adjusted unemployment rate increased to 11.7% in February from 11.6% in January. January's figure was revised up from 11.5%.

The number of unemployed people was 2.980 million in February, up 0.3% from the month before.

The youth unemployment rate decreased to 39.1 in February from 39.2% in January.

The employment rate fell to 56.4% in February from 56.6% in January.

-

17:56

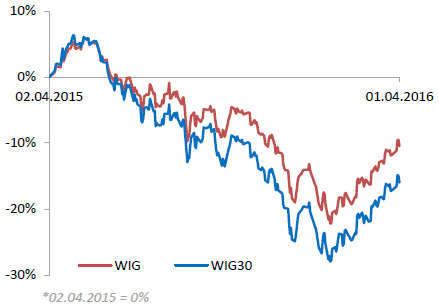

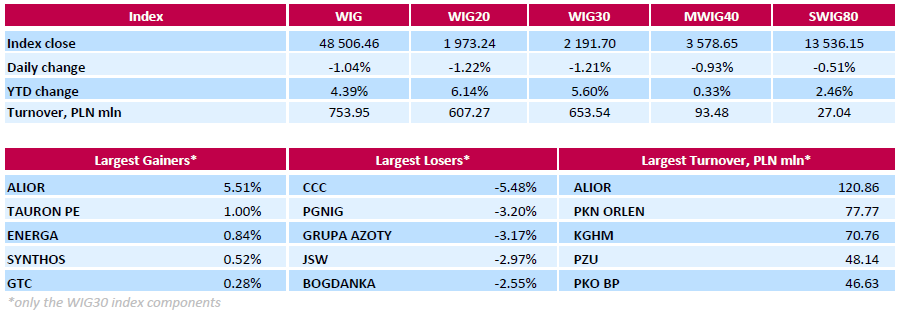

WSE: Session Results

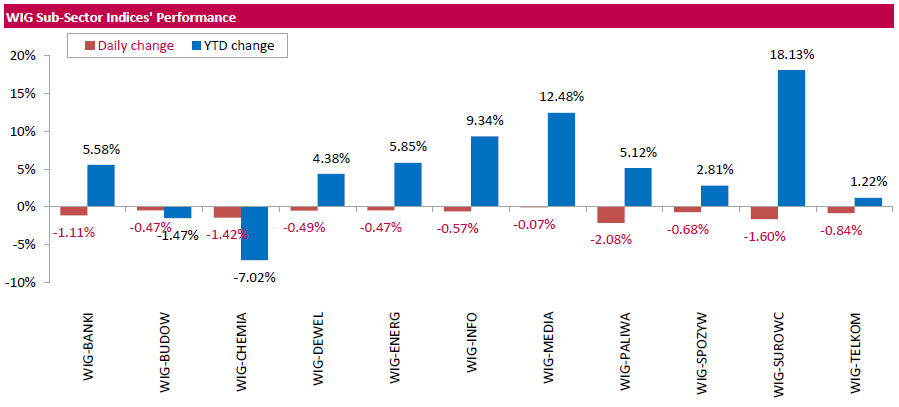

Polish equity market closed lower on Friday. The broad market measure, the WIG Index, fell by 1.04%. All sectors in the WIG retreated, with oil and gas sector (-2.08%) lagging behind.

The large-cap stocks' measure, the WIG30 Index, dropped by 1.21%. Within the WIG30 Index components, footwear retailer CCC (WSE: CCC) recorded the biggest decline, slumping by 5.48% as the company's monthly report showed its sales growth in March was weaker compared to the previous month. Other major laggards were oil and gas company PGNIG (WSE: PGN), chemical producer GRUPA AZOTY (WSE: ATT) and coking coal miner JSW (WSE: JSW), losing 3.2%, 3.17% and 2.97% respectively. On the other side of the ledger, bank ALIOR (WSE: ALR) led the gainers, advancing 5.51% on news the bank agreed to buy core business of Bank BPH in Poland from GE Capital for PLN 1.225 bln ($329 mln). It was followed by gencos TAURON PE (WSE: TPE) and ENERGA (WSE: ENG), adding 1% and 0.84% respectively.

-

17:51

New York Federal Reserve President William Dudley: the Fed should be cautious in raising its interest rate

New York Federal Reserve President William Dudley said on Thursday that he agreed with Fed Chairwoman Janet Yellen and the Fed should be cautious in raising its interest rate. He noted that the Fe should hike its interest rate gradually.

-

17:47

Cleveland Federal Reserve Bank President Loretta Mester: gradual interest rate hikes are appropriate

Cleveland Federal Reserve Bank President Loretta Mester said in an interview with Fox Business on Friday that gradual interest rate hikes were appropriate. She noted that she did not know how she would vote in April, adding that she wanted to see the incoming economic data.

Mester also said that she downgraded its forecast slightly compared to December, due to a slower economic growth in the fourth quarter.

-

16:43

Canadian manufacturing PMI rises to 51.5 in March

Royal Bank of Canada (RBC), the Supply Chain Management Association (SCMA) and Markit Economics released their RBC Canadian manufacturing PMI on Friday. The index rose to 51.5 in March from 49.4 in February. It was the highest level since December 2014.

The rise was mainly driven by stronger export demand.

"The low Canadian dollar contributed to further improvement in export volumes during the first quarter of 2016 and a return to growth in the manufacturing sector. In the remainder of 2016, we expect manufacturing conditions to continue to improve, driven by firm U.S. domestic demand and a weaker Canadian dollar which will drive demand for exports of autos, consumer goods, machinery, equipment and lumber," RBC senior vice-president and chief economist, Craig Wright, said.

-

16:36

Greece’s manufacturing PMI rises to 49.0 in March

Markit Economics released its manufacturing purchasing managers' index (PMI) for Greece on Friday. Greece's manufacturing purchasing managers' index (PMI) rose to 49.0 in March from 48.4 in February.

New orders and production remained below 50 in March, while employment rose slightly.

"Survey data for March signals a further deterioration of operating conditions in the manufacturing sector of Greece. However, the downturn has eased considerably from the lows of last summer," Markit economist Samuel Agass said.

-

16:28

Thomson Reuters/University of Michigan final consumer sentiment index declines to 91.0 in March

The Thomson Reuters/University of Michigan final consumer sentiment index decreased to 91.0 in March from 91.7 in February, up from the preliminary estimate of 90.0 and beating expectations a fall to 90.5.

"Despite the recent small monthly variations, the overall level of confidence has remained largely unchanged during the past nine months," the Surveys of Consumers chief economist at the University of Michigan Richard Curtin.

"Consumers anticipated that the slower pace of economic growth will more than likely put an end to further declines in the unemployment rate. What was surprising was that the expectations of higher gas prices and higher unemployment have not caused an increase in uncertainty about personal financial prospects," he added.

The current economic conditions index fell to 105.6 in March from 106.8 in February, in line with the preliminary reading.

The index of consumer expectations declined to 81.5 in March from 81.9 in February, up from a preliminary reading of 80.0.

The one-year inflation expectations increased to 2.7% in March from 2.5% in February, in line with the preliminary reading.

-

16:21

Construction spending in the U.S. is down 0.5% in February

The U.S. Commerce Department released construction spending data on Friday. Construction spending in the U.S. fell 0.5% in February, missing expectations for a 0.1% gain, after a 2.1% increase in January. January's figure was revised up from a 1.5% rise.

The decrease was mainly driven by a drop in total public spending. Total public construction spending slid 1.7% in February, while total spending on private construction projects decreased 0.1%.

-

16:15

ISM manufacturing purchasing managers’ index rises to 51.8 in March

The Institute for Supply Management released its manufacturing purchasing managers' index for the U.S. on Friday. The index rose to 51.8 in March from 49.5 in February. Analysts had expected the index to increase to 50.7.

A reading above 50 indicates expansion, below indicates contraction.

The increase was mainly driven by rises in production and new orders. The production index increased to 55.3 in March from 52.8 in February, while the new orders index jumped to 58.3 from 51.5.

The employment index was down to 48.1 in March from 48.5 in February.

The price index increased to 51.5 in March from 38.5 in February.

-

15:58

WSE: After start on Wall Street

Data from the labor market of the United States turned out to be quite good and were initially seen as increasing the chances of a rate hike in the US, which strengthened the dollar.

From the point of view of exchanges, data can be received in two ways and can be used both for bulls and bears. But certainly today's mood will not be changed.

The US market opens from discounts of 0.5% and takes the form of negative reaction to the good data from the labor market. This means that will for further growth may be subside by wish to implement considerable gains from recent weeks.

U.S. Stocks open: Dow -0.51%, Nasdaq -0.59%, S&P -0.58%

-

15:50

U.S. final manufacturing purchasing managers' index (PMI) increases to 51.5 in March

Markit Economics released its final manufacturing purchasing managers' index (PMI) for the U.S. on Friday. The U.S. final manufacturing purchasing managers' index (PMI) increased to 51.5 in March from 51.3 in February, up from the previous estimate of 51.4.

A reading above 50 indicates expansion in economic activity.

The index was driven by a faster pace of growth in new business.

"March's survey highlights sustained weakness across the US manufacturing sector, meaning that overall growth through the first quarter slowed to its lowest since late-2012," Markit's Senior Economist Tim Moore said.

-

15:44

Bank of Japan board member Makoto Sakurai: the downside risks to the Japanese economy increased in the recent six months

Bank of Japan (BoJ) board member Makoto Sakurai said on Friday that the downside risks to the Japanese economy increased in the recent six months. He supported the central bank's monetary policy easing, saying that bold monetary policy measures should be used.

"When you need to take steps, you obviously want to do something effective so you need to take bold steps," he said.

Sakurai also said that new tools were needed to ease the monetary policy further.

-

15:33

U.S. Stocks open: Dow -0.51%, Nasdaq -0.59%, S&P -0.58%

-

15:26

Australian Industry Group’s manufacturing purchasing managers’ index for Australia rises to 58.1 in March, the highest level since April 2004

The Australian Industry Group (AiG) released its manufacturing purchasing managers' index (PMI) for Australia on the late Thursday evening. The index rose to 58.1 in March from 53.5 in February. It was the highest level since April 2004.

A reading above 50 indicates expansion in the sector, while a reading below 50 indicates contraction in the sector.

Main contributor to the rise was new orders.

-

15:23

Before the bell: S&P futures -0.51%, NASDAQ futures -0.51%

U.S. stock-index fell.

Global Stocks:

Nikkei 16,164.16 -594.51 -3.55%

Hang Seng 20,498.92 -277.78 -1.34%

Shanghai Composite 3,008.98 +5.06 +0.17%

FTSE 6,091.28 -83.62 -1.35%

CAC 4,275.64 -109.42 -2.50%

DAX 9,713.2 -252.31 -2.53%

Crude oil $37.21 (-2.95%)

Gold $1229.50 (-0.49%)

-

15:18

Final Markit/Nikkei manufacturing purchasing managers' index for Japan declines to 49.1 in March

The final Markit/Nikkei manufacturing Purchasing Managers' Index (PMI) for Japan declined to 49.1 in March from 50.1 in February, in line with the preliminary reading.

A reading above 50 indicates expansion, a reading below 50 indicates contraction of activity.

The index was driven by drops in output and in new orders. New export orders slid at the fastest rate since January 2013.

"Manufacturing conditions in Japan worsened at the end of the first quarter of 2016. Both production and new orders contracted, with total incoming work declining at the sharpest rate in nearly two years," economist at Markit, Amy Brownbill, said.

-

15:08

Spain’s manufacturing PMI drops to 53.4 in March

Markit Economics released its manufacturing purchasing managers' index (PMI) for Spain on Friday. Spain's manufacturing purchasing managers' index (PMI) declined to 53.4 in March from 54.1 in February.

The decrease was driven by a slower growth in output and new orders, while input costs dropped.

"Although growth in the Spanish manufacturing sector has slowed from the start of the year, the latest monthly improvements in output and new orders were still respectable and there is little sign at this stage of a move towards stagnation," a senior economist at Markit Andrew Harker said.

-

15:03

Italy’s manufacturing PMI increases to 53.5 in March

Markit Economics released its manufacturing purchasing managers' index (PMI) for Italy on Friday. Italy's Markit/ADACI manufacturing PMI increased to 53.5 in March from 52.2 in February.

The increase was driven by a faster growth in output, new orders and exports.

"The manufacturing sector ended the first quarter on a solid footing, according to the latest PMI data, with March seeing accelerated growth in output and inflows of new orders. Moreover, with inventories of finished goods falling sharply, there's a good chance that production will be ramped up further to replenish stock," Markit economist Phil Smith said.

-

14:52

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

9.5

-0.08(-0.8351%)

33845

ALTRIA GROUP INC.

MO

62.51

-0.15(-0.2394%)

1050

Amazon.com Inc., NASDAQ

AMZN

590.89

-2.75(-0.4632%)

8950

American Express Co

AXP

60.86

-0.54(-0.8795%)

16815

Apple Inc.

AAPL

108.83

-0.16(-0.1468%)

151811

AT&T Inc

T

38.79

-0.38(-0.9701%)

131544

Barrick Gold Corporation, NYSE

ABX

13.56

-0.02(-0.1473%)

59801

Boeing Co

BA

126.75

-0.19(-0.1497%)

1050

Caterpillar Inc

CAT

76.1

-0.44(-0.5749%)

1944

Chevron Corp

CVX

94.42

-0.98(-1.0273%)

3791

Cisco Systems Inc

CSCO

28.33

-0.14(-0.4917%)

1400

Citigroup Inc., NYSE

C

41.67

-0.08(-0.1916%)

9606

Deere & Company, NYSE

DE

76.7

-0.29(-0.3767%)

5063

Exxon Mobil Corp

XOM

82.94

-0.65(-0.7776%)

16011

Facebook, Inc.

FB

113.84

-0.26(-0.2279%)

99080

FedEx Corporation, NYSE

FDX

162.72

0.00(0.00%)

1440

Ford Motor Co.

F

13.45

-0.05(-0.3704%)

52022

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

10.1

-0.24(-2.3211%)

37528

General Electric Co

GE

31.62

-0.17(-0.5348%)

29475

General Motors Company, NYSE

GM

31.32

-0.11(-0.35%)

2009

Google Inc.

GOOG

742.03

-2.92(-0.392%)

744

Home Depot Inc

HD

133.1

-0.33(-0.2473%)

231

Intel Corp

INTC

32.29

-0.06(-0.1855%)

91965

International Business Machines Co...

IBM

151.25

-0.20(-0.1321%)

1790

Johnson & Johnson

JNJ

108.2

-0.00(-0.00%)

2511

JPMorgan Chase and Co

JPM

59.1

-0.12(-0.2026%)

20457

McDonald's Corp

MCD

125.21

-0.47(-0.374%)

3558

Microsoft Corp

MSFT

55

-0.23(-0.4164%)

27065

Nike

NKE

61.27

-0.20(-0.3254%)

4618

Pfizer Inc

PFE

29.47

-0.17(-0.5736%)

26230

Starbucks Corporation, NASDAQ

SBUX

59.39

-0.31(-0.5193%)

29082

Tesla Motors, Inc., NASDAQ

TSLA

244

14.23(6.1931%)

527550

The Coca-Cola Co

KO

46.25

-0.14(-0.3018%)

5560

Twitter, Inc., NYSE

TWTR

16.45

-0.10(-0.6042%)

8734

Verizon Communications Inc

VZ

53.7

-0.38(-0.7027%)

96137

Visa

V

76.25

-0.23(-0.3007%)

9392

Wal-Mart Stores Inc

WMT

68.4

-0.09(-0.1314%)

1500

Walt Disney Co

DIS

98.89

-0.42(-0.4229%)

36216

Yahoo! Inc., NASDAQ

YHOO

36.46

-0.35(-0.9508%)

1979

Yandex N.V., NASDAQ

YNDX

15.05

-0.27(-1.7624%)

1250

-

14:49

U.S. unemployment rate rises to 5.0% in March, 215,000 jobs are added

The U.S. Labor Department released the labour market data on Friday. The U.S. economy added 215,000 jobs in March, exceeding expectations for a rise of 205,000 jobs, after a gain of 245,000 jobs in February. February's figure was revised up from a rise of 242,000 jobs.

The increase was driven by rises in retail trade, construction, and health care.

The retail trade added 47,700 jobs in March, while the manufacturing sector shed 29,000 jobs.

Construction added 37,000 in March, while mining sector shed 12,400 jobs.

The U.S. unemployment rate rose to 5.0% in March from 4.9% in February. Analysts had expected the unemployment rate to remain unchanged at 4.9%.

Average hourly earnings increased 0.3% in March, beating forecasts of a 0.2% gain, after a 0.1% decline in February.

The labour-force participation rate increased to 63.0% in March from 62.9% in February.

As the U.S. labour market continues to strengthen, the Fed could raise its interest rate gradually this year.

-

14:42

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

AT&T (T) downgraded to Sell from Neutral at MoffettNathanson

Verizon (VZ) downgraded to Neutral at MoffettNathanson

Other:

IBM (IBM) target raised to $155 from $135 at RBC Capital Mkts

-

13:03

WSE: Mid session comment

The mood in Europe, with the entry into the southern phase of trading, have not improved and indices oscillate at trading minima, or deepen as in the case of France.

Traditionally, the strongest is the German market, but it only leads to consolidation. The weakest attitude is characterized by French parquet, where the derivative comes back to the minima from the end of February.

On the Warsaw market declines today have their width, not only among the blue chips, but also among the other, the mWIG40 and the sWIG80 indices.

The problem of departure is so important that it is made exactly from the level of resistance, which yesterday has been cosmetically touched.

-

12:01

European stock markets mid session: stocks traded lower ahead of the U.S. labour market data

Stock indices traded lower ahead of the release of the U.S. labour market data later in the day. Analysts expect that U.S. unemployment rate is expected to remain unchanged at 4.9% in March. The U.S. economy is expected to add 205,000 jobs in March, after adding 242,000 jobs in February.

Market participants also eyed the economic data from the Eurozone. Markit Economics released its final manufacturing purchasing managers' index (PMI) for the Eurozone on Friday. Eurozone's final manufacturing purchasing managers' index (PMI) climbed to 51.6 in March from 51.2 in February, up from the preliminary reading of 51.4.

The rise was driven by a faster growth in production and new orders.

"Although the PMI ticked higher, March still saw the second-weakest improvement in manufacturing conditions seen for just over a year. The data suggest manufacturing grew by only around 0.2% in the first quarter, acting as a drag on the wider economy," Chris Williamson, Chief Economist at Markit said.

"Policymakers will also be worried by the further intensification of deflationary pressures in manufacturing supply chains, with prices charged at the factory gate falling at the steepest rate since late-2009," he added.

Germany's final Markit/BME manufacturing purchasing managers' index (PMI) rose to 50.7 in March from 50.5 in February, up from the preliminary reading of 50.4. The index was mainly driven by rises in output and new business. Employment declined in March.

France's final manufacturing purchasing managers' index (PMI) decreased to 49.6 in March from 50.2 in February, in line with the preliminary reading. The index was driven by drops in new business and output prices. Output rose slightly.

Markit Economics released its manufacturing purchasing managers' index (PMI) for the U.K. on Friday. The Markit/Chartered Institute of Procurement & Supply manufacturing PMI for the U.K. increased to 51.0 in March from 50.8 in February, missing expectations for a rise to 51.2.

The increase was driven by a rise in new business.

"The UK manufacturing sector remained in the doldrums during the opening quarter of the year. Although March saw modest improvements in the trends for production and new orders, industry is still hovering close to the stagnation mark and will struggle to make a meaningful contribution to the next set of GDP growth figures," Markit's Senior Economist Rob Dobson said.

Current figures:

Name Price Change Change %

FTSE 100 6,101.74 -73.16 -1.18 %

DAX 9,799.4 -166.11 -1.67 %

CAC 40 4,309.77 -75.29 -1.72 %

-

11:56

Nationwide: UK house prices rise 0.8% in March

The Nationwide Building Society released its house prices data for the U.K. on Friday. UK house prices were up 0.8% in March, after a 0.4% increase in February.

On a yearly basis, house prices rose to 5.7% in March from 4.8 in February. It was the biggest rise since January 2015.

"There has been a pickup in housing market activity in recent months, with the number of housing transactions and mortgage approvals rising strongly. This is likely to have been driven, at least in part, by upcoming changes to stamp duty on second homes, where buyers have brought forward purchases in order to avoid the additional tax liabilities, Nationwide's Chief Economist, Robert Gardner, said.

-

11:49

Swiss manufacturing PMI climbs to 53.2 in March, the highest level since October 2014

Credit Suisse and procure.ch released their manufacturing purchasing managers' index (PMI) for Switzerland on Friday. The manufacturing purchasing managers' index in Switzerland climbed to 53.2 in March from 51.6 in February, beating expectations for a decrease to 51.0. It was the highest level since October 2014.

A reading above 50 indicates expansion.

The increase was driven by rises in all sub-indexes.

The production increased to 58.0 in March from 56.9 in February, while the backlog of orders sub-index jumped to 54.9 from 53.3, the highest level since July 2014.

Purchase prices were up to 47.0 in March from 43.8 in February.

Employment rose to 46.1 in March from 45.6 in February.

-

11:43

Swiss retail sales decline 0.2% year-on-year in February

The Federal Statistical Office released its retail sales data for Switzerland on Friday. Retail sales in Switzerland were down at an annual rate of 0.2% in February, missing expectations for a 0.5% rise, after a 0.1% decrease in January. January's figure was revised down from a 0.2% increase.

Sales of food, beverages and tobacco climbed at an annual rate of 0.7% in February, while non-food sales climbed 0.9%.

On a monthly basis, retail sales fell by 0.4% in February, after a 0.6% drop in January. January's figure was revised down from a 0.3% fall.

Sales of food, beverages and tobacco declined 0.8% in February, while non-food sales were flat.

-

11:32

France’s final manufacturing PMI decreases to 49.6 in March

Markit Economics released its final manufacturing purchasing managers' index (PMI) for France on Friday. France's final manufacturing purchasing managers' index (PMI) decreased to 49.6 in March from 50.2 in February, in line with the preliminary reading.

The index was driven by drops in new business and output prices. Output rose slightly.

"Although output returned to growth in March, a sharper fall in new orders dragged the PMI below the neutral 50.0 mark and highlighted the ongoing weakness of demand facing manufacturers," Markit Senior Economist Jack Kennedy said.

-

11:28

Germany’s final manufacturing PMI rises to 50.7 in March

Markit Economics released its final manufacturing purchasing managers' index (PMI) for Germany on Friday. Germany's final Markit/BME manufacturing purchasing managers' index (PMI) rose to 50.7 in March from 50.5 in February, up from the preliminary reading of 50.4.

The index was mainly driven by rises in output and new business. Employment declined in March.

"German manufacturers ended their worst quarter in over a year in March, with overall growth in the sector slowing to a crawl. Although production growth was maintained, the pace of expansion was little-changed from February's 14-month low," Markit economist Oliver Kolodseike said.

-

11:24

Eurozone’s final manufacturing PMI climbs to 51.6 in March

Markit Economics released its final manufacturing purchasing managers' index (PMI) for the Eurozone on Friday. Eurozone's final manufacturing purchasing managers' index (PMI) climbed to 51.6 in March from 51.2 in February, up from the preliminary reading of 51.4.

The rise was driven by a faster growth in production and new orders.

"Although the PMI ticked higher, March still saw the second-weakest improvement in manufacturing conditions seen for just over a year. The data suggest manufacturing grew by only around 0.2% in the first quarter, acting as a drag on the wider economy," Chris Williamson, Chief Economist at Markit said.

"Policymakers will also be worried by the further intensification of deflationary pressures in manufacturing supply chains, with prices charged at the factory gate falling at the steepest rate since late-2009," he added.

-

11:12

Markit/Chartered Institute of Procurement & Supply manufacturing PMI for the U.K. increases to 51.0 in March

Markit Economics released its manufacturing purchasing managers' index (PMI) for the U.K. on Friday. The Markit/Chartered Institute of Procurement & Supply manufacturing PMI for the U.K. increased to 51.0 in March from 50.8 in February, missing expectations for a rise to 51.2.

A reading above 50 indicates expansion.

The increase was driven by a rise in new business.

"The UK manufacturing sector remained in the doldrums during the opening quarter of the year. Although March saw modest improvements in the trends for production and new orders, industry is still hovering close to the stagnation mark and will struggle to make a meaningful contribution to the next set of GDP growth figures," Markit's Senior Economist Rob Dobson said.

-

10:45

Bloomberg Consumer Comfort Index: consumers’ expectations for U.S. economy fall to 42.8 in in the week ended March 26

According to data from the Bloomberg Consumer Comfort Index, consumers' expectations for U.S. economy decreased to 42.8 in in the week ended March 26 from 43.6 the prior week.

The decrease was mainly driven by a less favourable assessment of the economy. The measure of views of the economy declined to 32.6 from 34.0, the buying climate index was unchanged, while the personal finances index fell by 1 point to 57.6 from 55.9.

-

10:39

Official data: Chinese manufacturing PMI rises to 50.2 in March

The Chinese manufacturing PMI rose to 50.2 in March from 49.0 in February, according to the Chinese government. February's reading was the lowest reading since November 2011.

Analysts had expected the index to increase to 49.3.

A reading above the 50 mark indicates expansion, a reading below 50 indicates contraction.

The increase was driven by rises in output and new orders, while employment fell.

The services PMI increased to 53.8 in March from 52.7 in February.

-

10:22

Chinese Markit/Caixin manufacturing PMI increases to 49.7 in March

The Chinese Markit/Caixin manufacturing PMI increased to 49.7 in March from 48.0 in February. The increase was driven by rises output, total new orders and output prices. But companies continued to shed jobs.

"All categories of the index showed improvement over the previous month. The output and new order categories rose above the neutral 50-point level, indicating that the stimulus policies the government has implemented have begun to take hold," Dr. He Fan, Chief Economist at Caixin Insight Group, said.

"However, considering that current conditions remain uncertain, the government needs to continue with moderate stimulus measures to reinforce market confidence," he added.

-

10:11

Tankan Survey: the large manufacturers’ index drops to +6 in the first quarter

The Bank of Japan released its quarterly Tankan business survey on late Thursday evening. The large manufacturers' index dropped to +6 in the first quarter from +12 in the fourth quarter, missing expectations for a fall to +8.

The outlook fell to +3 in the first quarter from +7 in the fourth quarter.

The large non-manufacturers' index fell to +22 in the first quarter from +25 in the fourth quarter, beating expectations for a decline to +24.

The outlook decreased to +17 from +18.

-

09:52

WSE: Alior Bank

Alior Bank (WSE: ALR) signed an agreement to buy core operations of bank BPH (WSE: BPH) from GE Capital, with the 87.23% stake appraised at PLN 1.255 bln, and will first launch a tender offer on up to 66% of BPH shares.

After the tender offer, BPH will be divided to exclude the mortgage portfolio and investment fund house BPH TFI.

The division plan is to be agreed on by April 30, while the entire transaction should be completed by end-2016.

The sides have agreed that BPH's core operations will have capital adequacy ratio of 13.25%.

Alior Bank will finance the takeover with a rights share issue for existing shareholders. Alior expects to conclude the rights share issue in June 2016, subject to market conditions, and will determine the final number of shares to be issued and issue price "at a later stage of the transaction."

Alior Bank's shares price is rising by more than 6 percent in response to this information and it is the only growing company among the blue chips this morning.

-

09:09

WSE: After opening

The WIG20 futures contracts (WSE: FW20M16) started in difficult market conditions for the bulls, after strong declines in Asia and the explicit discounts contracts for the major European indices. The opening was 14 points below yesterday's closing, at 1,976 points. (-0.7%).

WIG20 index opened at 1985.37 points (-0.62%)*

WIG 48745.62 -0.55%

WIG20 1985.37 -0.62%

WIG30 2202.80 -0.71%

mWIG40 3606.64 -0.16%

*/ - change to previous close

The beginning of the session was a little nervous, but it should be only a foretaste of today's attractions, which the summit of them can be expected in the afternoon after the release of data from the US labor market.

-

08:22

WSE: Before opening

Today's session begins the next month and quarter, which means focusing on PMI / ISM indicators for the major economies, mainly for China and the United States.

In addition, we will know today a monthly report from the US labor market.

In China we observe declines, and Japan's Nikkei index lost more than 3,5%. Some influence on this may have the decision of the S&P Agency, which downgraded the rating outlook of China to negative.

Adding to this picture a slight decline during yesterday's session on Wall Street and bearish morning for future contracts in the United States, morning moods is not so specially favored for the Warsaw bulls to defeat the psychological level of 2,000 points on the WIG20 index.

-

06:20

Global Stocks: investors were cautious on the last day of the quarter

European stocks closed sharply lower on Thursday, deepening losses for the first quarter, with bank shares under pressure while a rise in the euro weighed on exporters.

U.S. stocks finished one of their best-performing months since last October with a whimper, as the main benchmarks closed marginally lower Thursday. Market reaction to a pair of mixed economic reports was muted as investors were cautious on the last day of the quarter as they waited for key labor market data due Friday.

Asian stocks slid as the fresh quarter got under way, with Japanese equities leading losses amid a slump in corporate sentiment. Metals rose after a gauge of Chinese manufacturing expanded for the first time since July.

Based on MarketWatch materials

-

04:04

Nikkei 225 16,419.91 -338.76 -2.02 %, Hang Seng 20,676.2 -100.50 -0.48 %, Shanghai Composite 2,992.2 -11.71 -0.39 %

-

00:30

Stocks. Daily history for Sep Mar 31’2016:

(index / closing price / change items /% change)

Nikkei 225 16,758.67 -120.29 -0.71 %

Hang Seng 20,776.7 -26.69 -0.13 %

S&P/ASX 200 5,082.79 +72.52 +1.45 %

Shanghai Composite 3,004.38 +3.73 +0.12 %

FTSE 100 6,174.9 -28.27 -0.46 %

CAC 40 4,385.06 -59.36 -1.34 %

Xetra DAX 9,965.51 -81.10 -0.81 %

S&P 500 2,059.74 -4.21 -0.20 %

NASDAQ Composite 4,869.85 +0.55 +0.01 %

Dow Jones 17,685.09 -31.57 -0.18 %

-