Noticias del mercado

-

21:04

DJIA 17929.51 -0.48 0%, NASDAQ 4852.04 9.36 0.19%, S&P 500 2099.09 0.23 0.01%

-

18:05

European stocks closed: FTSE 6577.83 73.50 1.13%, DAX 9776.12 96.03 0.99%, CAC 4273.96 36.48 0.86%

-

17:54

Wall Street. Major U.S. stock-indexes rose

Major U.S. stock-indexes rose for the fourth straight day as increased prospects of central bank stimulus around the world bolstered investor confidence. Investors were also taking stock of their holdings after a tumultuous week in the wake of Britain's vote to leave the European Union. The vote sparked a two-day panic selloff, but markets clawed back their losses in the last three days.

Most of all Dow stocks in positive area (20 of 30). Top looser - JPMorgan Chase & Co. (JPM, -1,13%). Top gainer - The Home Depot, Inc. (HD, +1,85%).

Most of all S&P sectors also in positive area. Top looser - Utilities (-0,3%). Top gainer - Services (+1,0%).

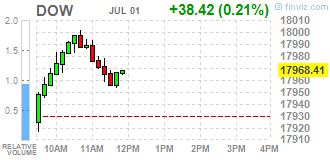

At the moment:

Dow 17857.00 +38.00 +0.21%

S&P 500 2095.50 +5.25 +0.25%

Nasdaq 100 4433.75 +26.75 +0.61%

Oil 48.33 0.00 0.00%

Gold 1339.50 +18.90 +1.43%

U.S. 10yr 1.46 -0.03

-

17:37

WSE: Session Results

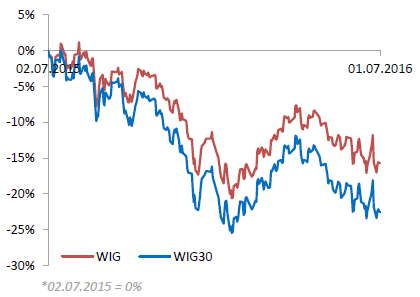

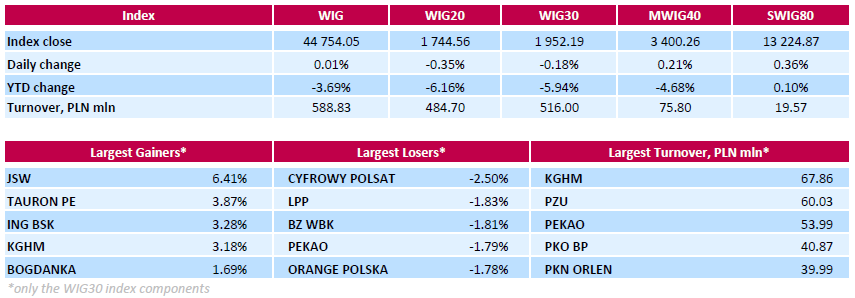

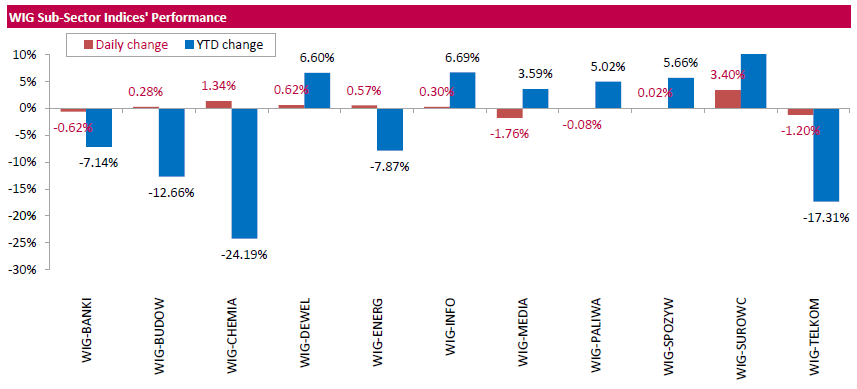

Polish equity market closed flat on Friday. The broad market measure, the WIG Index, inched up 0.01%. Sector performance within the WIG Index was mixed. Media (-1.76%) and telecoms (-1.20%) recorded the most notable declines, while materials (+3.40%) and chemicals (+1.34%) fared the best.

The large-cap stocks' measure, the WIG30 Index fell by 0.18%. Within the Index components, media group CYFROWY POLSAT (WSE: CPS), clothing retailer LPP (WSE: LPP), telecommunication services provider ORANGE POLSKA (WSE: OPL) and two banking sector names BZ WBK (WSE: BZW) and PEKAO (WSE: PEO) were the weakest performers, returning losses between 1.83% and 2.5%. On the other side of the ledger, coking coal miner JSW (WSE: JSW) led the advancers pack with a 6.41% growth, bouncing back after yesterday's sharp decline. It was followed by genco TAURON PE (WSE: TPE), bank ING BSK (WSE: ING) and copper producer KGHM (WSE: KGH), gaining 3.87%, 3.28% and 3.18% respectively.

-

15:56

WSE: After start on Wall Street

The US market started at neutral level, then began to gain and slightly exceeded the level of 2100 points on the S&P500 index, which is already at the levels of the last Friday opening. The movement from lows was very strong and it seems that today's session can only seal it before the long weekend in the US due to Monday's Independence Day.

Major European indices show good posture and both the DAX-a and the CAC40 are approx. + 0.8%. We also may see very well behavior in the British market, which set new highs this year, and maintains them. At the Warsaw market there is still no major changes, the WIG20 index is currently at the level of 1,744 points (-0.36%).

-

15:32

U.S. Stocks open: Dow -0.04%, Nasdaq -0.06%, S&P -0.03%

-

15:10

Before the bell: S&P futures -0.04%, NASDAQ futures -0.04%

U.S. stock-index futures were little changed.

Global Stocks:

Nikkei 15,682.48 +106.56 +0.68%

Hang Seng Closed

Shanghai Composite 2,932.82 +3.22 +0.11%

FTSE 6,558.17 +53.84 +0.83%

CAC 4,275.23 +37.75 +0.89%

DAX 9,767.78 +87.69 +0.91%

Crude $48.19 (-0.29%)

Gold $1336.90 (+1.23%)

-

14:55

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

9.26

-0.01(-0.1079%)

54839

ALTRIA GROUP INC.

MO

68.96

-0.00(-0.00%)

20584

Amazon.com Inc., NASDAQ

AMZN

716.61

0.99(0.1383%)

20590

American Express Co

AXP

61.18

0.42(0.6912%)

848

AMERICAN INTERNATIONAL GROUP

AIG

52.73

-0.16(-0.3025%)

501

Apple Inc.

AAPL

95.56

-0.04(-0.0418%)

53214

AT&T Inc

T

43.35

0.14(0.324%)

6675

Barrick Gold Corporation, NYSE

ABX

21.85

0.50(2.3419%)

91962

Boeing Co

BA

129.31

-0.56(-0.4312%)

780

Chevron Corp

CVX

104.82

-0.01(-0.0095%)

687

Cisco Systems Inc

CSCO

28.77

0.08(0.2788%)

113087

Citigroup Inc., NYSE

C

42.29

-0.10(-0.2359%)

97861

Deere & Company, NYSE

DE

80.8

-0.24(-0.2961%)

25266

Exxon Mobil Corp

XOM

93.26

-0.48(-0.5121%)

1139

Facebook, Inc.

FB

114.27

-0.01(-0.0088%)

114908

FedEx Corporation, NYSE

FDX

154

2.22(1.4626%)

7568

Ford Motor Co.

F

12.64

0.07(0.5569%)

63611

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

11

-0.14(-1.2567%)

114660

General Electric Co

GE

31.31

-0.17(-0.54%)

58687

General Motors Company, NYSE

GM

28.6

0.30(1.0601%)

16432

Goldman Sachs

GS

148.04

-0.54(-0.3634%)

760

Google Inc.

GOOG

692.1

-0.00(-0.00%)

1138

Intel Corp

INTC

32.71

-0.09(-0.2744%)

107318

JPMorgan Chase and Co

JPM

61.44

-0.22(-0.3568%)

11398

McDonald's Corp

MCD

120

-0.34(-0.2825%)

2040

Merck & Co Inc

MRK

57.53

-0.08(-0.1389%)

582

Microsoft Corp

MSFT

51.21

0.04(0.0782%)

152353

Nike

NKE

55.3

0.10(0.1812%)

4782

Pfizer Inc

PFE

35.21

-0.00(-0.00%)

1115

Procter & Gamble Co

PG

84.64

-0.03(-0.0354%)

28705

Starbucks Corporation, NASDAQ

SBUX

56.7

-0.42(-0.7353%)

6283

Tesla Motors, Inc., NASDAQ

TSLA

208.11

-4.17(-1.9644%)

59588

The Coca-Cola Co

KO

45.37

0.04(0.0882%)

12076

Twitter, Inc., NYSE

TWTR

16.9

-0.01(-0.0591%)

19853

UnitedHealth Group Inc

UNH

142.14

0.94(0.6657%)

509

Verizon Communications Inc

VZ

55.71

-0.13(-0.2328%)

17734

Visa

V

74.5

0.33(0.4449%)

44574

Wal-Mart Stores Inc

WMT

72.41

-0.61(-0.8354%)

38335

Walt Disney Co

DIS

97.82

-0.00(-0.00%)

14511

Yahoo! Inc., NASDAQ

YHOO

37.75

0.19(0.5059%)

3175

Yandex N.V., NASDAQ

YNDX

21.82

-0.03(-0.1373%)

2700

-

13:08

WSE: Mid session comment

After an unsuccessful morning try of clearance over the week high, in the last minutes of the session slightly higher initiative show bears. As a result, the WIG20 index went below 1,740 pts. The behavior of our market presents a detachment from the environment where demand is trying to keep the indexes in the vicinity of neutral. European indexes, the Dax and the CAC40 are listed on delicate pros. In this context, the decline in WIG20 by 0.5%, once again has reflected the weakness of the local market and at the same time resistance to the increases.

The half of the session is behind us, and the turnover on the WIG20 index is only PLN 172 mln. It is clearly seen, that the demand side is absent. Unfortunately, scrubbing in the mid-session on its minima forecasts rather more trouble in the second part of the day.

-

09:22

WSE: After opening

WIG20 index opened at 1756.47 points (+0.33%)*

WIG 44973.52 0.50%

WIG30 1964.32 0.44%

mWIG40 3396.07 0.09%

*/ - change to previous close

The WIG20 futures started trading with a slight indication on a plus, which distinguishes us from other European parquets, where the morning shows indication of contracts rather with cosmetic changes down.

The WIG20 index started from increase by 0.33% to 1,756 points. As might be expected spot market is opening with advantage of increases and the WIG20 is close the peaks of this week. Their eventual break-up would open the way for the closing "after-brexit" gap from last Friday. Unfortunately, a little bothered is the weaker-than-expected reading of the PMI index for Polish industry, which cosmetically falling from 52.1 points. to 51.8 pts., what is slightly disappointing.

-

08:50

Mixed start expected on the major stock exchanges in Europe: DAX + 0,2%, FTSE 100 -0,1%, CAC 40 + 0.1%

-

08:26

WSE: before opening

Today's session begins the next month and the next half-year on the markets. The current week has brought the global improvement in sentiment and yesterday's session on Wall Street was another successful one, which resulted in the increase of the US indexes of more than 1%. The impact on this has probably the situation on the currency market, the weakening of the pound after the speech of Mark Carney, the head of the Bank of England, signaled the need for loosening monetary policy this summer. The Euro also weakened after the news of Bloomberg about the possibility of easing bond purchases conducted by the ECB. As a result of growth in the US market losses from Friday have been almost entirely made up and in the morning it should support the Warsaw Stock Exchange, which had no opportunity to react to it. The index in Shanghai maintains a relatively neutral stance, while other Asian parquets are on the gain. This day will show whether the Warsaw market will react positively to the global improvement or remain resistant, which we experienced in recent days.

-

07:13

Global Stocks

European stocks closed higher Thursday following a choppy session where Deutsche Bank AG and Banco Santander SA shares fell under pressure fell further back into the rearview mirror

European stocks on Wednesday surged 3.1%, marking a second straight day of sharp gains after a two-session rout in the wake of the U.K.'s vote to leave the European Union. Stocks had appeared to have found, at least, a short-term foundation for gains as the U.K. government had yet to formally start the negotiation process for the U.K.'s exit from the 28-member bloc, or Brexit.

Further easing measures may be in the works to deal with heightened uncertainty created by the vote, Bank of England Gov. Mark Carney said in a speech, but he stressed there are limits as to what the central bank can do.

U.S. stocks rose for a third session on Thursday on mounting expectations for more accommodative policies from global central banks following the U.K.'s vote to leave the European Union last week.

The gains were the best three-day climb for the main stock-market gauges since Feb. 17, according to Dow Jones data. All three indexes are near the levels they were trading at ahead of last week's U.K. referendum as initial jitters over Brexit subsided.

July 1 Japan's Nikkei share average rose on Friday for a fifth day as bargain hunting continued and risk appetites remained solid after U.S. and European shares gained.

Japanese stocks have erased about the half of their losses in the wake of Britain's shock vote a week ago to leave the European Union.

For the week, the Nikkei has jumped 4.9 percent, the biggest weekly gain since mid-April.

Shares of securities firm gained ground, with Nomura Holdings rising 2.8 percent and Daiwa Securities advancing 1.2 percent.

Exporters were steady, with Toyota Motor Corp gaining 1.4 percent and Nissan Motor Co adding 1.1 percent.

-

04:04

Nikkei 225 15,657.62 +81.70 +0.52 %, Hang Seng 20,794.37 +358.25 +1.75 %, Shanghai Composite 2,942.4 +12.80 +0.44 %

-

00:32

Stocks. Daily history for Jun 30’2016:

(index / closing price / change items /% change)

Nikkei 225 15,575.92+9.09+0.06%

Hang Seng 20,719.87+283.75+1.39%

S&P/ASX 200 5,233.38+90.98+1.77%

Shanghai Composite 2,929.61-1.99-0.07%

FTSE 100 6,504.33 +144.27 +2.27 %

CAC 40 4,237.48 +42.16 +1.00 %

Xetra DAX 9,680.09 +67.82 +0.71 %

S&P 500 2,098.86 +28.09 +1.36 %

NASDAQ Composite 4,842.67 +63.43 +1.33 %

Dow Jones 17,929.99 +235.31 +1.33 %

-