Noticias del mercado

-

18:00

European stocks close: stocks closed higher, leading by a rise in shares of mining and commodities trading company Glencore

Stock indices closed higher as shares of mining and commodities trading company Glencore increased after announcing its plans to cut debt.

U.S. markets will be closed for a public holiday on Monday.

Meanwhile, the economic data from the Eurozone was mixed. Market research group Sentix released its investor confidence index for the Eurozone on Monday. The index dropped to 13.6 in September from 18.4 in August. It was the lowest level since February.

A reading above 0.0 indicates optimism, below indicates pessimism.

The decline was driven by a slowdown in the Chinese economy.

"Investors now see the slowdown in China as well as in other emerging markets as a significant burden for the euro zone's economy, which can no longer be compensated by good developments in the domestic euro zone economy or the United States," Sentix said.

Destatis released its industrial production data for Germany on Monday. German industrial production rose 0.7% in July, missing expectations for a 1.0% gain, after a 0.9% decline in June. June's figure was revised up from a 1.4% drop.

The output of capital goods increased 2.8% in July, energy output climbed 1.9%, and the production in the construction sector was up 3.2%, while the production of intermediate goods fell 0.8%.

The output of consumer goods decreased 3.7%.

Indexes on the close:

Name Price Change Change %

FTSE 100 6,074.52 +31.60 +0.52 %

DAX 10,108.61 +70.57 +0.70 %

CAC 40 4,549.64 +26.56 +0.59 %

-

17:50

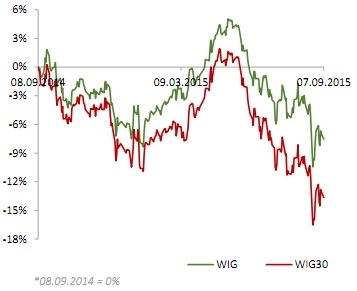

WSE: Session Results

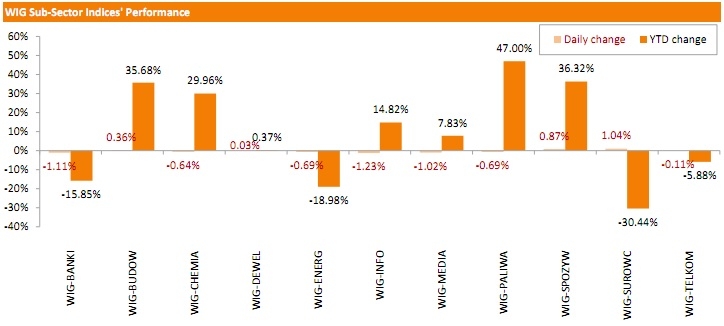

Polish equity market closed lower on Monday. The broad market measure, the WIG Index, lost 0.58%. Sector-wise, information technologies (-1.23%) fared the worst, while materials (+1.04%) outperformed.

The large-cap stocks' measure, the WIG30 Index, fell by 0.66%. Within the WIG30 Index components, JSW (WSE: JSW) was hit the hardest, tumbling 9.64% on news that the company's board member resigned and that Polish ING unit demanded earlier redemption of JSW's bonds worth PLN 26.3 mln. It was followed by ENERGA (WSE: ENG) and PEKAO (WSE: PEO), declining by 2.31% and 2.16% respectively. On the other side of the ledger, SYNTHOS (WSE: SNS), KGHM (WSE: KGH) and GTC (WSE: GTC) recorded the strongest daily performance, soaring by 2.93%, 1.83% and 1.56% respectively.

-

17:11

French President Francois Hollande: the French economy is expected to grow 1% this year and 1.5% next year

French President Francois Hollande said on Monday that the French economy is expected to grow 1% this year and 1.5% next year. But he added that this year's growth would not be enough to reduce unemployment.

Hollande noted that the country's budget deficit is expected to be 3.8% of gross domestic product (GDP) this year and 3.3% in 2016.

The French president also said that he expects the Chinese economy to expand in the long-term period.

-

16:52

European Central Bank purchases €51.6 billion of public and private debt in August

The European Central Bank (ECB) purchased €51.6 billion of public and private debt under its quantitative-easing program in August, compared to €61.3 billion in July.

ECB'S asset buying programme is intended to run to September 2016.

The ECB bought €42.8 billion of government and agency bonds in July, €7.5 billion of covered bonds, and €1.3 billion of asset-backed securities.

The central purchased €11.9 billion of government and agency bonds, €1.0 billion of covered bonds, and €382 million of asset-backed securities last week.

-

16:15

China’s foreign-exchange reserves drop by $93.9 billion in August

According to data released by the People's Bank of China PBoC), China's foreign-exchange reserves declined by $93.9 billion to $3.56 trillion at the end of August, compared with $3.65 trillion in July. Currency reserves have been falling from $3.99 trillion in June 2014.

The recent decline is the result of the central bank's intervention to stop to stop the yuan fall and to limit capital outflows from the country.

-

14:38

Bundesbank President Jens Weidmann is elected as board chairman of the Bank for International Settlements (BIS)

The Bundesbank President Jens Weidmann has been elected on Sunday as board chairman of the Bank for International Settlements (BIS).

The BIS is based in Basel, Switzerland. The BIS Board is responsible for determining the strategic and policy direction of the BIS. The board includes the Bank of England Governor Mark Carney, the European Central Bank President Mario Draghi, the People's Bank of China (PBoC) Governor Zhou Xiaochuan and the Federal Reserve Chairwoman Janet Yellen

Weidmann will replace the Bank of France Governor Christian Noyer, who will retire as the Bank of France Governor on October 31.

Weidmann's term will be for three years and begins on November 1.

-

12:00

European stock markets mid session: stocks traded higher as concerns over a slowdown in the global economy eased

Stock indices traded higher as concerns over a slowdown in the global economy eased.

U.S. markets will be closed for a public holiday on Monday.

Meanwhile, the economic data from the Eurozone was mixed. Market research group Sentix released its investor confidence index for the Eurozone on Monday. The index dropped to 13.6 in September from 18.4 in August. It was the lowest level since February.

A reading above 0.0 indicates optimism, below indicates pessimism.

The decline was driven by a slowdown in the Chinese economy.

"Investors now see the slowdown in China as well as in other emerging markets as a significant burden for the euro zone's economy, which can no longer be compensated by good developments in the domestic euro zone economy or the United States," Sentix said.

Destatis released its industrial production data for Germany on Monday. German industrial production rose 0.7% in July, missing expectations for a 1.0% gain, after a 0.9% decline in June. June's figure was revised up from a 1.4% drop.

The output of capital goods increased 2.8% in July, energy output climbed 1.9%, and the production in the construction sector was up 3.2%, while the production of intermediate goods fell 0.8%.

The output of consumer goods decreased 3.7%.

Current figures:

Name Price Change Change %

FTSE 100 6,070.44 +27.52 +0.46 %

DAX 10,067.08 +29.04 +0.29 %

CAC 40 4,531.35 +8.27 +0.18 %

-

11:38

People’s Bank of China (PBoC) Governor Zhou Xiaochuan: there is no reason for the yuan to fall further

The People's Bank of China (PBoC) Governor Zhou Xiaochuan said at G20 summit on Friday that there is no reason for the yuan to fall further.

Zhu Jun, head of the international department at the PBoC, noted that the yuan devaluation was not an attempt to gain an advantage over other exporters. He added that the Chinese government expected the market turbulence in China to be "pretty close to the end".

Chinese Finance Minister Lou Jiwei said on Friday that he expects China's economy to expand about 7% for the next four or five years.

-

11:27

U.S. Treasury Secretary Jacob Lew: China should refrain from competitive devaluation

The U.S. Treasury Secretary Jacob Lew said at G20 summit on Friday that China should refrain from competitive devaluation.

"China should allow its exchange rate to reflect underlying fundamentals, avoid persistent exchange rate misalignments, and refrain from competitive devaluation," he said.

-

11:14

Job advertisements in Australia climb 1.0% in August

The Australian and New Zealand Banking Group (ANZ) released its job advertisements for Australia on Monday. Job advertisements in Australia climbed 1.0% in August, after a 0.5% decline in July. July's figure was revised down from a 0.4% fall.

Internet job advertisements increased 1.0% in August, while newspaper advertisements gained 0.8%.

On a yearly basis, job advertisement rose 8.7% in August, after a 9.2% in July.

"The recent strength in employment growth has been concentrated in a range of labour intensive services industries, however job losses in mining, mining-related construction and manufacturing are likely to weigh on employment growth over the next year,'' ANZ Chief Economist Warren Hogan said.

-

11:02

Sentix investor confidence index for the Eurozone is down to 13.6 in September

Market research group Sentix released its investor confidence index for the Eurozone on Monday. The index dropped to 13.6 in September from 18.4 in August. It was the lowest level since February.

A reading above 0.0 indicates optimism, below indicates pessimism.

The decline was driven by a slowdown in the Chinese economy.

"Investors now see the slowdown in China as well as in other emerging markets as a significant burden for the euro zone's economy, which can no longer be compensated by good developments in the domestic euro zone economy or the United States," Sentix said.

The current conditions index fell to 15.0 in September from 15.3 in August.

The expectations index plunged to 12.3 in September from 21.5 in August, the lowest level since December 2014

German investor confidence index declined to 20.6 from 25.7

-

10:12

Ai Group/HIA Australian Performance of Construction Index is up to 53.8 in August

The Australian Industry Group (AiG) released its construction data for Australia on late Sunday evening. The Ai Group/HIA Australian Performance of Construction Index rose to 53.8 in August from 47.1 in July.

A reading above 50 indicates expansion in the sector.

The increase was driven by a rise in new orders, which jumped to 57.6 in August from 45.4 in July.

"A healthy August update for commercial construction is encouraging, but needs to be sustained. As new housing activity remains strong rather than achieving further growth, commercial construction and infrastructure investment needs to pick up the baton," HIA Chief Economist, Harley Dale, said.

-

09:44

Japan's leading index declines to 104.9 in July

Japan's Cabinet Office released its preliminary leading index data on Monday. The leading index declined to 104.9 in July from 106.5 in June. It was the lowest level since March.

Japan's coincident index was down to 112.2 in July from 112.3 in June.

-

09:33

Swiss National Bank's foreign exchange reserves increase to 540.460 billion Swiss francs in August

The Swiss National Bank's foreign exchange reserves increased to 540.416 billion Swiss francs in August from 531.201 billion francs in July.

July's figure was revised down from 531.820 billion francs.

-

09:22

German industrial production rises 0.7% in July

Destatis released its industrial production data for Germany on Monday. German industrial production rose 0.7% in July, missing expectations for a 1.0% gain, after a 0.9% decline in June. June's figure was revised up from a 1.4% drop.

The output of capital goods increased 2.8% in July, energy output climbed 1.9%, and the production in the construction sector was up 3.2%, while the production of intermediate goods fell 0.8%.

The output of consumer goods decreased 3.7%.

-

09:11

China lowers its GDP for 2014 to 7.3% from 7.4%

China's National Bureau of Statistics (NBS) revised its gross domestic product (GDP) on Monday. The Chinese economy expanded 7.3% in 2014, down from a 7.4% growth reported earlier. It was the lowest growth since 1990.

The downward revision was driven by a weaker rise in the services sector than previously reported. The services sector rose by 7.8% in 2014, down from the previous estimate of a 8.1% increase.

The agriculture sector grew 4.1% in 2014, while the secondary sector increased by 7.3%.

China's economy expanded 7% in the first half of 2015.

-

08:23

Global Stocks: U.S. stock indices fell amid mixed employment data

U.S. stock indices fell on Friday after a key employment report showed mixed data. The U.S. economy created 173,000 jobs in August vs 220,000 expected. Meanwhile the unemployment rate fell to 5.1% from 5.3% reported previously. Average hourly earnings rose 2.2% beating expectations. The contradicting data failed to clarify probability of a rate increase when Fed policymakers meet on September 16-17.

Richmond Fed President Jeffrey Lacker said that the payrolls number was still strong even though it missed forecasts. "It didn't change the picture for monetary policy," he said.

The Dow Jones Industrial Average fell 272.38 points, or 1.7%, to 16102.38 (-3.3% over the week). The S&P 500 declined 29.91 points, or 1.5%, to 1,921.22 (-3.4% over the week). The Nasdaq Composite lost 49.58 points, or 1.1%, to 4,683.92 (-3% over the week).

This morning in Asia Hong Kong Hang Seng added 0.22%, or 45.13 points, to 20,885.74. China Shanghai Composite Index rose 0.88%, or 27.66 points, to 3,187.82. The Nikkei climbed 0.34%, or 60.70 points, to 17,852.86.

Asian stock indices climbed in this volatile session. However investors remained concerned over China's economy. On Monday China's National Bureau of Statistics revised down 2014 gross domestic product growth to 7.3% from a previously reported 7.4%.

People's Bank of China Governor Zhou Xiaochuan said at the G-20 meeting in Turkey that China's stock market has almost completed its correction after a bubble formed earlier this year.

-

04:02

Nikkei 225 17,948.22 +156.06 +0.88 %, Hang Seng 21,013.94 +173.33 +0.83 %, Shanghai Composite 3,149.38 -10.79 -0.34 %

-

02:32

Stocks. Daily history for Sep 4’2015:

(index / closing price / change items /% change)

S&P/ASX 200 5,040.6 +12.80 +0.25%

TOPIX 1,444.53 -30.45 -2.06%

FTSE 100 6,042.92 -151.18 -2.44 %

CAC 40 4,523.08 -130.71 -2.81 %

Xetra DAX 10,038.04 -279.80 -2.71 %

S&P 500 1,921.22 -29.91 -1.53 %

NASDAQ Composite 4,683.92 -49.58 -1.05 %

Dow Jones 16,102.38 -272.38 -1.66 %

-