Notícias do Mercado

-

23:45

New Zealand: Current Account , Quarter I 1.40 (forecast 1.42)

-

16:33

Foreign exchange market. American session: the U.S. dollar traded higher against the most major currencies after the better-than-expected U.S. consumer inflation

The U.S. dollar traded higher against the most major currencies after the better-than-expected U.S. consumer inflation. The consumer price index in the U.S. rose 0.4% in May, exceeding expectations for a 0.2% gain, after a 0.3% increase in April. Food prices had shown the biggest increase since August 2011.

On a yearly basis, the U.S. consumer price index increased 2.1% in May, after a 2.0% gain in April. That was the biggest rise since October 2012. Analysts had expected the consumer price index to remain unchanged at 2.0%.

The U.S. core consumer prices excluding food and energy climbed 0.3% in May, slightly exceeding expectations for a 0.2% rise, after a 0.2% increase in April. On a yearly basis, the U.S. core consumer prices increased 2.0% in May, after a 1.8% gain in April. That was the fastest pace since February 2013.

The higher inflation could weigh on Federal Reserve’s decision when to raise short-term interest rates.

There is a weakness in the U.S. housing sector. The U.S. housing starts declined by 6.5% to a seasonally adjusted 1.001 million units in May from 1.071 million in April. Analysts had expected a decline of 3.7% to 1.034 million units.

The number of building permits in the U.S. fell by 6.4% to a seasonally adjusted 991,000 units in May from 1.059 million units in April. Analysts had forecasted building permits to decrease by 0.1% to 1.05 million units.

The euro traded lower against the U.S. dollar after the weaker-than-expected ZEW economic sentiment and the better-than-expected U.S. consumer inflation. The German economic sentiment dropped by 3.3 points to 29.8 in June from 33.1 in May. Analysts had expected an increase by 1.9 points to 35.0.

Eurozone’s ZEW economic sentiment climbed to 58.4 in June from 55.2 in May, missing expectations for a gain to 59.6.

The British pound traded slightly lower against the U.S. dollar. The unexpected decline in inflation in the U.K. and the stronger consumer inflation in the U.S. weighed on the British currency. The annual rate of inflation declined 1.5% in May, after 1.8% in April. That was the lowest level since October 2009. Analysts had expected the annual inflation rate to decrease to 1.7%.

On a monthly basis, inflation in the U.K. fell 0.1%, missing expectations for a 0.2% gain, after a 0.4% increase.

The decline was driven by falls in the price of bread, cereals and vegetables. Food prices declined 0.6%.

Core consumer price index excluding food costs in the U.K. climbed at annual rate by 1.6%, missing expectations for a 1.7% rise.

The Retail Prices Index (RPI) decreased to 2.4% in May from 2.5% in April.

U.K. house prices surged by 9.9% in the 12 months to April and reached a new high of £260,000.

The Swiss franc traded lower against the U.S. dollar. The producer & import prices in Switzerland rose 0.1% in May, after a 0.3% decline in April. Analysts had expected the producer & import prices to be flat.

On a yearly, producer & import prices in Switzerland declined 0.8% in May, meeting expectations, after a 1.2% fall.

The Canadian dollar traded lower against the U.S. dollar in the absence of any major economic reports in Canada. The better-than-expected U.S. consumer inflation weighed on the Canadian dollar.

The New Zealand dollar declined against the U.S dollar in the absence of any major economic reports in New Zealand. Concerns over the violence in Iraq weighed on the kiwi.

The Australian dollar dropped against the U.S. dollar due to concerns over the violence in Iraq and comments by the Reserve Bank of Australia.

The Reserve Bank of Australia (RBA) released minutes from its latest meeting. The RBA said that the current stimulus measures continue to be appropriate and the economic growth is expected to remain slightly below trend. Australia’s central bank added inflation in Australia is to remain within the target range of 2% to 3%.

New motor vehicle sales in Australia increased 0.3% in May, after a flat reading in April. On a yearly basis, new motor vehicle sales in Australia declined 2.0% in May, after a 1.9% drop in April.

The Japanese yen declined against the U.S. dollar in the absence of any major economic reports in Japan. The better-than-expected U.S. consumer inflation weighed on the yen.

-

15:27

U.S. inflation rose 0.4% in May

The U.S. Labor Department released the consumer price index. The index rose 0.4% in May, exceeding expectations for a 0.2% gain, after a 0.3% increase in April. Food prices had shown the biggest increase since August 2011.

On a yearly basis, the U.S. consumer price index increased 2.1% in May, after a 2.0% gain in April. That was the biggest rise since October 2012. Analysts had expected the consumer price index to remain unchanged at 2.0%.

The U.S. core consumer prices excluding food and energy climbed 0.3% in May, slightly exceeding expectations for a 0.2% rise, after a 0.2% increase in April. On a yearly basis, the U.S. core consumer prices increased 2.0% in May, after a 1.8% gain in April. That was the fastest pace since February 2013.

The higher inflation could weigh on Federal Reserve’s decision when to raise short-term interest rates.

-

15:08

U.S. housing starts dropped 6.5% in May

The U.S. Commerce Department released the U.S. housing starts and building permits figures. The U.S. housing starts declined by 6.5% to a seasonally adjusted 1.001 million units in May from 1.071 million in April. Analysts had expected a decline of 3.7% to 1.034 million units.

Many Americans are still struggling to afford new houses due to the high mortgage rates. Single-family houses, the largest part of the housing market, declined 5.9% in May.

Apartments gained 9.4% over the past 12 months. It seems that more Americans prefer to rent a house instead of owning homes.

The number of building permits in the U.S. fell by 6.4% to a seasonally adjusted 991,000 units in May from 1.059 million units in April. Analysts had forecasted building permits to decrease by 0.1% to 1.05 million units.

-

14:40

Option expiries for today's 1400GMT cut

EUR/USD $1.3500, $1.3540/45, $1.3600

USD/JPY Y101.40/50, Y101.65

USD/CAD Cad1.0975/85, Cad1.1000

AUD/USD $0.9375, $0.9435

USD/CHF Chf0.8925, Chf0.8950, Chf0.9100

-

13:31

U.S.: CPI excluding food and energy, Y/Y, May +2.0% (forecast +1.8%)

-

13:31

U.S.: Housing Starts, mln, May 1.00 (forecast 1.04)

-

13:31

U.S.: Building Permits, mln, May 0.99 (forecast 1.07)

-

13:30

U.S.: CPI, m/m , May +0.4% (forecast +0.2%)

-

13:30

U.S.: CPI excluding food and energy, m/m, May +0.3% (forecast +0.2%)

-

13:30

U.S.: CPI, Y/Y, May +2.1% (forecast +2.0%)

-

13:00

Foreign exchange market. European session: the U.S. dollar traded slightly lower against the most major currencies ahead of the release of consumer price index in the U.S.

Economic calendar (GMT0):

01:30 Australia RBA Meeting's Minutes

01:30 Australia New Motor Vehicle Sales (MoM) May 0.0% 0.3%

01:30 Australia New Motor Vehicle Sales (YoY) May -1.9% -2.0%

05:45 Switzerland SECO Economic Forecasts Quarter III

07:15 Switzerland Producer & Import Prices, m/m May -0.3% 0.0% +0.1%

07:15 Switzerland Producer & Import Prices, y/y May -1.2% -0.8% -0.8%

08:30 United Kingdom Retail Price Index, m/m May +0.4% +0.2% +0.1%

08:30 United Kingdom Retail prices, Y/Y May +2.5% +2.5% +2.4%

08:30 United Kingdom RPI-X, Y/Y May +2.6% +2.5%

08:30 United Kingdom Producer Price Index - Input (MoM) May -1.1% +0.1% -0.9%

08:30 United Kingdom Producer Price Index - Input (YoY) May -5.5% -4.1% -5.0%

08:30 United Kingdom Producer Price Index - Output (MoM) May 0.0% +0.1% 0.0%

08:30 United Kingdom Producer Price Index - Output (YoY) May +0.6% +0.8% +1.0%

08:30 United Kingdom HICP, m/m May +0.4% +0.2% -0.1%

08:30 United Kingdom HICP, Y/Y May +1.8% +1.7% +1.5%

08:30 United Kingdom HICP ex EFAT, Y/Y May +2.0% +1.6%

09:00 Eurozone ZEW Economic Sentiment June 55.2 59.6 58.4

09:00 Germany ZEW Survey - Economic Sentiment June 33.1 35.2 29.8

The U.S. dollar traded slightly lower against the most major currencies ahead of the release of consumer price index in the U.S. The lowering forecast of the U.S. economic growth by the International Monetary Fund (IMF) still weighed on the U.S. The IMF expects the U.S. economy to grow 2% in 2014, down from its forecast of 2.8% in April.

The consumer price index in the U.S. should climb 0.2% in May, after a 0.3% increase. The core consumer price index in the U.S. should remain unchanged at 2.0% in May.

The euro traded mixed against the U.S. dollar after the weaker-than-expected ZEW economic sentiment. The German economic sentiment dropped by 3.3 points to 29.8 in June from 33.1 in May. Analysts had expected an increase by 1.9 points to 35.0.

Eurozone’s ZEW economic sentiment climbed to 58.4 in June from 55.2 in May, missing expectations for a gain to 59.6.

The British pound traded slightly higher against the U.S. dollar. The annual rate of inflation declined 1.5% in May, after 1.8% in April. That was the lowest level since October 2009. Analysts had expected the annual inflation rate to decrease to 1.7%.

On a monthly basis, inflation in the U.K. fell 0.1%, missing expectations for a 0.2% gain, after a 0.4% increase.

The decline was driven by falls in the price of bread, cereals and vegetables. Food prices declined 0.6%.

Core consumer price index excluding food costs in the U.K. climbed at annual rate by 1.6%, missing expectations for a 1.7% rise.

The Retail Prices Index (RPI) decreased to 2.4% in May from 2.5% in April.

U.K. house prices surged by 9.9% in the 12 months to April and reached a new high of £260,000.

The Swiss franc traded mixed against the U.S. dollar. The producer & import prices in Switzerland rose 0.1% in May, after a 0.3% decline in April. Analysts had expected the producer & import prices to be flat.

On a yearly, producer & import prices in Switzerland declined 0.8% in May, meeting expectations, after a 1.2% fall.

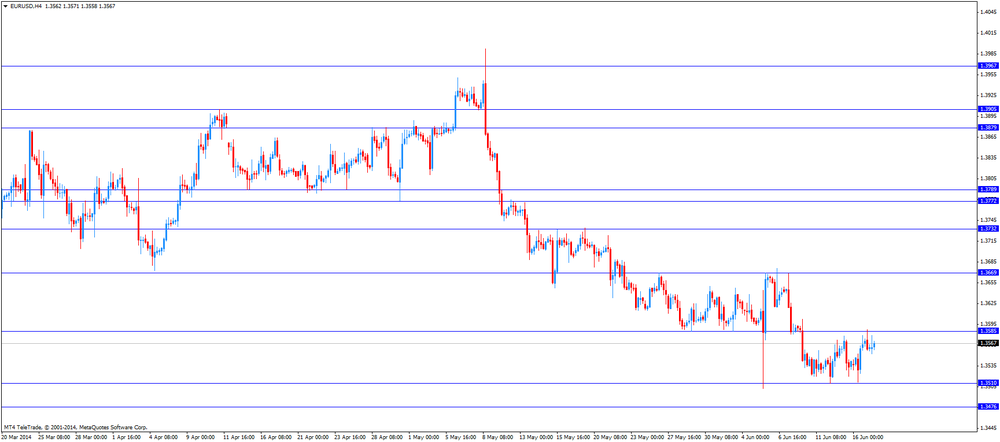

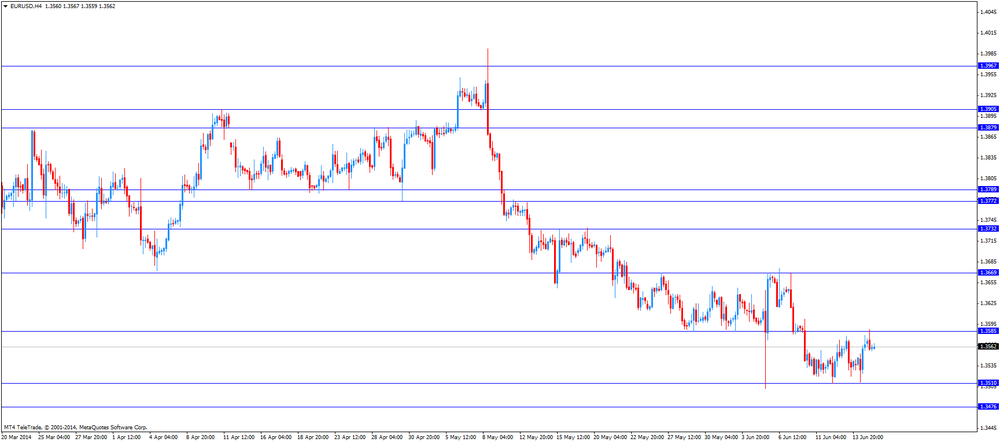

EUR/USD: the currency pair traded mixed

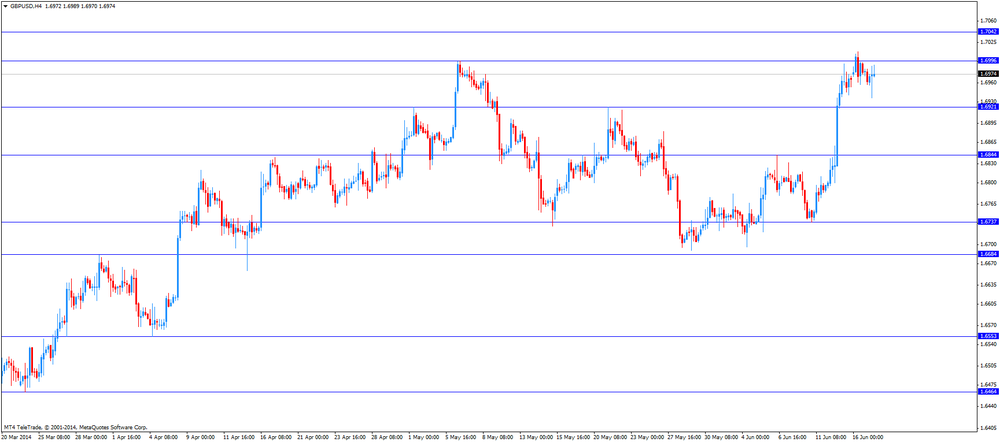

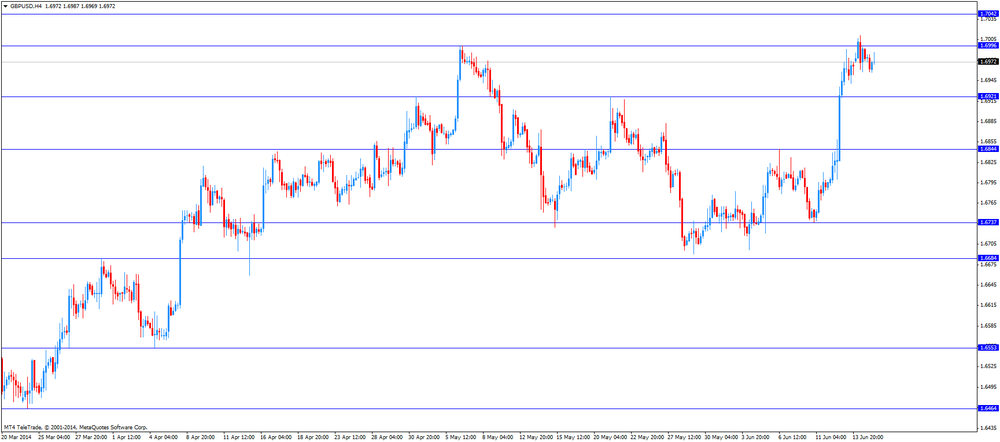

GBP/USD: the currency pair increased to $1.6989

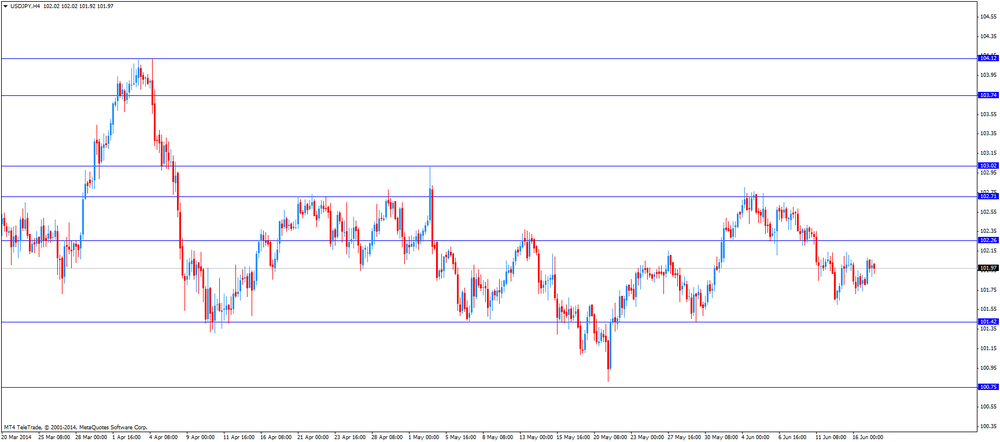

USD/JPY: the currency pair traded mixed

The most important news that are expected (GMT0):

12:30 U.S. Building Permits, mln May 1.08 1.07

12:30 U.S. Housing Starts, mln May 1.07 1.04

12:30 U.S. CPI, m/m May +0.3% +0.2%

12:30 U.S. CPI, Y/Y May +2.0% +2.0%

12:30 U.S. CPI excluding food and energy, m/m May +0.2% +0.2%

12:30 U.S. CPI excluding food and energy, Y/Y May +1.8% +1.8%

22:45 New Zealand Current Account Quarter I -1.43 1.42

23:50 Japan Monetary Policy Meeting Minutes

23:50 Japan Adjusted Merchandise Trade Balance, bln May -808.9 -1100

-

13:00

Orders

EUR/USD

Offers $1.3630-50, $1.3610/15, $1.3600

Bids $1.3550, $1.3535, $1.3515/10, $1.3500, $1.3485/80

GBP/USD

Offers $1.7080/85, $1.7040/50, $1.7015-20, $1.6995/00

Bids $1.6930/20, $1.6910/00, $1.6885/80, $1.6820, $1.6800

AUD/USD

Offers $0.9500, $0.9450

Bids $0.9320, $0.9300, $0.9280

EUR/JPY

Offers Y139.20, Y139.00, Y138.80

Bids Y138.00, Y137.50, Y137.20, Y137.00

USD/JPY

Offers Y102.50

Bids Y101.70, Y101.50, Y101.00

EUR/GBP

Offers stg0.8080, stg0.8050, stg0.8035/40

Bids stg0.7950, stg0.7900

-

11:27

UK inflation rate hits to 1.5% in May, the lowest level since 2009

The Office for National Statistics released inflation in the U.K. The annual rate of inflation declined 1.5% in May, after 1.8% in April. That was the lowest level since October 2009. Analysts had expected the annual inflation rate to decrease to 1.7%.

On a monthly basis, inflation in the U.K. fell 0.1%, missing expectations for a 0.2% gain, after a 0.4% increase.

The decline was driven by falls in the price of bread, cereals and vegetables. Food prices declined 0.6%.

Core consumer price index excluding food costs in the U.K. climbed at annual rate by 1.6%, missing expectations for a 1.7% rise.

The Retail Prices Index (RPI) decreased to 2.4% in May from 2.5% in April.

U.K. house prices surged by 9.9% in the 12 months to April and reached a new high of £260,000.

-

11:04

German ZEW economic sentiment declined to 18-month low in June

The ZEW Centre for Economic Research released its index for Germany and the Eurozone. The German economic sentiment dropped by 3.3 points to 29.8 in June from 33.1 in May. Analysts had expected an increase by 1.9 points to 35.0.

Eurozone’s ZEW economic sentiment climbed to 58.4 in June from 55.2 in May, missing expectations for a gain to 59.6.

-

10:29

Option expiries for today's 1400GMT cut

EUR/USD $1.3500, $1.3540/45, $1.3600

USD/JPY Y101.40/50, Y101.65

USD/CAD Cad1.0975/85, Cad1.1000

AUD/USD $0.9375, $0.9435

USD/CHF Chf0.8925, Chf0.8950, Chf0.9100

-

10:01

Germany: ZEW Survey - Economic Sentiment, June 29.8 (forecast 35.2)

-

10:01

Eurozone: ZEW Economic Sentiment, June 58.4 (forecast 59.6)

-

09:57

Foreign exchange market. Asian session: the Australian dollar dropped against the U.S. dollar due to concerns over the violence in Iraq and comments by the Reserve Bank of Australia

Economic calendar (GMT0):

01:30 Australia RBA Meeting's Minutes

01:30 Australia New Motor Vehicle Sales (MoM) May 0.0% 0.3%

01:30 Australia New Motor Vehicle Sales (YoY) May -1.9% -2.0%

05:45 Switzerland SECO Economic Forecasts Quarter III

07:15 Switzerland Producer & Import Prices, m/m May -0.3% 0.0% +0.1%

07:15 Switzerland Producer & Import Prices, y/y May -1.2% -0.8% -0.8%

08:30 United Kingdom Retail Price Index, m/m May +0.4% +0.2% +0.1%

08:30 United Kingdom Retail prices, Y/Y May +2.5% +2.5% +2.4%

08:30 United Kingdom RPI-X, Y/Y May +2.6% +2.5%

08:30 United Kingdom Producer Price Index - Input (MoM) May -1.1% +0.1% -0.9%

08:30 United Kingdom Producer Price Index - Input (YoY) May -5.5% -4.1% -5.0%

08:30 United Kingdom Producer Price Index - Output (MoM) May 0.0% +0.1% 0.0%

08:30 United Kingdom Producer Price Index - Output (YoY) May +0.6% +0.8% +1.0%

08:30 United Kingdom HICP, m/m May +0.4% +0.2% -0.1%

08:30 United Kingdom HICP, Y/Y May +1.8% +1.7% +1.5%

08:30 United Kingdom HICP ex EFAT, Y/Y May +2.0% +1.6%

The U.S. dollar traded higher against the most major currencies. The demand for the U.S. currency was supported by the violence in Iraq and the yesterday’s better-than expected economic data.

Concerns over the violence in Iraq and the resulting possible impact of higher oil prices on global economic growth weighed on the risk-related currencies.

The NAHB housing market index in the U.S. increased to 49 in June from 45 in May, exceeding expectations for a gain to 47.

NY Fed Empire State manufacturing index increased to 19.3 in June from 19.0 in May, exceeding expectations from a decline to 15.2.

The New Zealand dollar declined against the U.S dollar in the absence of any major economic reports in New Zealand. Concerns over the violence in Iraq weighed on the kiwi.

The Australian dollar dropped against the U.S. dollar due to concerns over the violence in Iraq and comments by the Reserve Bank of Australia.

The Reserve Bank of Australia (RBA) released minutes from its latest meeting. The RBA said that the current stimulus measures continue to be appropriate and the economic growth is expected to remain slightly below trend. Australia’s central bank added inflation in Australia is to remain within the target range of 2% to 3%.

New motor vehicle sales in Australia increased 0.3% in May, after a flat reading in April. On a yearly basis, new motor vehicle sales in Australia declined 2.0% in May, after a 1.9% drop in April.

The Japanese yen traded lower against the U.S. dollar in the absence of any major economic reports in Japan.

EUR/USD: the currency pair declined to $1.3560

GBP/USD: the currency pair decreased to $1.6960

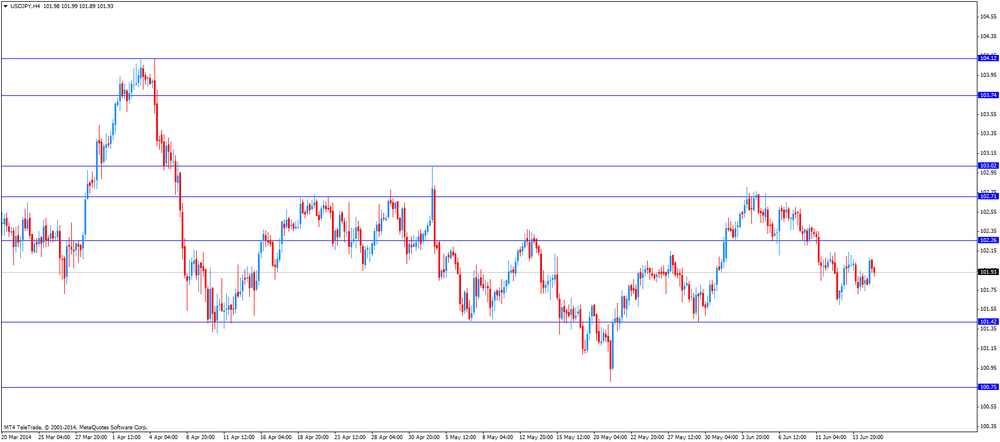

USD/JPY: the currency pair increased to Y102.10

The most important news that are expected (GMT0):

12:30 U.S. Building Permits, mln May 1.08 1.07

12:30 U.S. Housing Starts, mln May 1.07 1.04

12:30 U.S. CPI, m/m May +0.3% +0.2%

12:30 U.S. CPI, Y/Y May +2.0% +2.0%

12:30 U.S. CPI excluding food and energy, m/m May +0.2% +0.2%

12:30 U.S. CPI excluding food and energy, Y/Y May +1.8% +1.8%

22:45 New Zealand Current Account Quarter I -1.43 1.42

23:50 Japan Monetary Policy Meeting Minutes

23:50 Japan Adjusted Merchandise Trade Balance, bln May -808.9 -1100

-

09:32

United Kingdom: HICP ex EFAT, Y/Y, May +1.6%

-

09:32

United Kingdom: Retail Price Index, m/m, May +0.1% (forecast +0.2%)

-

09:32

United Kingdom: Retail prices, Y/Y, May +2.4% (forecast +2.5%)

-

09:31

United Kingdom: Producer Price Index - Output (MoM), May 0.0% (forecast +0.1%)

-

09:31

United Kingdom: Producer Price Index - Output (YoY) , May +1.0% (forecast +0.8%)

-

09:31

United Kingdom: Producer Price Index - Input (MoM), May -0.9% (forecast +0.1%)

-

09:31

United Kingdom: Producer Price Index - Input (YoY) , May -5.0% (forecast -4.1%)

-

09:30

United Kingdom: HICP, m/m, May -0.1% (forecast +0.2%)

-

09:30

United Kingdom: HICP, Y/Y, May +1.5% (forecast +1.7%)

-

08:15

Switzerland: Producer & Import Prices, m/m, May +0.1% (forecast 0.0%)

-

08:15

Switzerland: Producer & Import Prices, y/y, May -0.8% (forecast -0.8%)

-

06:25

Options levels on tuesday, June 17, 2014:

EUR / USD

Resistance levels (open interest**, contracts)

$1.3655 (3053)

$1.3630 (1779)

$1.3597 (71)

Price at time of writing this review: $ 1.3558

Support levels (open interest**, contracts):

$1.3537 (1013)

$1.3517 (3650)

$1.3492 (4506)

Comments:

- Overall open interest on the CALL options with the expiration date July, 3 is 28911 contracts, with the maximum number of contracts with strike price $1,3700 (3645);

- Overall open interest on the PUT options with the expiration date July, 3 is 41226 contracts, with the maximum number of contracts with strike price $1,3500 (4793);

- The ratio of PUT/CALL was 1.43 versus 1.44 from the previous trading day according to data from June, 16

GBP/USD

Resistance levels (open interest**, contracts)

$1.7201 (1427)

$1.7103 (1729)

$1.7006 (2172)

Price at time of writing this review: $1.6972

Support levels (open interest**, contracts):

$1.6895 (977)

$1.6798 (1558)

$1.6699 (1931)

Comments:

- Overall open interest on the CALL options with the expiration date July, 3 is 17812 contracts, with the maximum number of contracts with strike price $1,7000 (2172);

- Overall open interest on the PUT options with the expiration date July, 3 is 21450 contracts, with the maximum number of contracts with strike price $1,6750 (2253);

- The ratio of PUT/CALL was 1.20 versus 1.20 from the previous trading day according to data from June, 16

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

02:31

Australia: New Motor Vehicle Sales (YoY) , May -2.0%

-

02:31

Australia: New Motor Vehicle Sales (MoM) , May 0.3%

-

00:20

Currencies. Daily history for June 16'2014:

(pare/closed(GMT +2)/change, %)EUR/USD $1,3571 +0,22%

GBP/USD $1,6979 +0,08%

USD/CHF Chf0,8970 -0,31%

USD/JPY Y101,81 -0,21%

EUR/JPY Y138,17 +0,03%

GBP/JPY Y172,86 -0,13%

AUD/USD $0,9398 -0,02%

NZD/USD $0,8676 +0,12%

USD/CAD C$1,0841 -0,10%

-

00:00

Schedule for today, Tuesday, June 17’2014:

(time / country / index / period / previous value / forecast)01:30 Australia RBA Meeting's Minutes

01:30 Australia New Motor Vehicle Sales (MoM) May 0.0%

01:30 Australia New Motor Vehicle Sales (YoY) May -1.9%

05:45 Switzerland SECO Economic Forecasts Quarter III

07:15 Switzerland Producer & Import Prices, m/m May -0.3% 0.0%

07:15 Switzerland Producer & Import Prices, y/y May -1.2% -0.8%

08:30 United Kingdom Retail Price Index, m/m May +0.4% +0.2%

08:30 United Kingdom Retail prices, Y/Y May +2.5% +2.5%

08:30 United Kingdom RPI-X, Y/Y May +2.6%

08:30 United Kingdom Producer Price Index - Input (MoM) May -1.1% +0.1%

08:30 United Kingdom Producer Price Index - Input (YoY) May -5.5% -4.1%

08:30 United Kingdom Producer Price Index - Output (MoM) May 0.0% +0.1%

08:30 United Kingdom Producer Price Index - Output (YoY) May +0.6% +0.8%

08:30 United Kingdom HICP, m/m May +0.4% +0.2%

08:30 United Kingdom HICP, Y/Y May +1.8% +1.7%

08:30 United Kingdom HICP ex EFAT, Y/Y May +2.0%

09:00 Eurozone ZEW Economic Sentiment June 55.2 59.6

09:00 Germany ZEW Survey - Economic Sentiment June 33.1 35.2

12:30 U.S. Building Permits, mln May 1.08 1.07

12:30 U.S. Housing Starts, mln May 1.07 1.04

12:30 U.S. CPI, m/m May +0.3% +0.2%

12:30 U.S. CPI, Y/Y May +2.0% +2.0%

12:30 U.S. CPI excluding food and energy, m/m May +0.2% +0.2%

12:30 U.S. CPI excluding food and energy, Y/Y May +1.8% +1.8%

20:30 U.S. API Crude Oil Inventories June +1.5

22:45 New Zealand Current Account Quarter I -1.43 1.42

23:50 Japan Monetary Policy Meeting Minutes

23:50 Japan Adjusted Merchandise Trade Balance, bln May -808.9 -1100

-