Notícias do Mercado

-

18:27

European stocks close

European stocks dropped the most in more than a week as Portugal's coalition government splintered and crude oil surged above $100 a barrel amid rising political unrest in Egypt.

National benchmark indexes retreated in all the 18 western European markets except Iceland. The U.K.'s FTSE 100 lost 1.2 percent. France's CAC 40 fell 1.1 percent and Germany's DAX also retreated 1 percent.

Espirito Santo, Portugal's biggest bank by market capitalization, tumbled 11 percent to 54.5 euro cents. Banco Comercial plunged 13 percent to 8.1 euro cents. The country's bonds slumped, pushing the 10-year yield above 8 percent, as two ministers resigned amid austerity fatigue.

Prime Minister Pedro Passos Coelho said in a televised speech yesterday he's trying to hold his government together after losing both his finance minister and his foreign minister.

Secretary of State for Treasury Maria Luis Albuquerque replaced Vitor Gaspar at the Ministry of Finance. That prompted Paulo Portas, who leads the smaller CDS party in the coalition government, to quit, saying the new minister would offer "mere continuity" of the country's deficit-cutting plans.

Banks also fell as Barclays Plc, Deutsche Bank AG and Credit Suisse Group AG had their credit ratings lowered by S&P's as new rules and "uncertain market conditions" threaten their business.

Long-term counterparty credit ratings for Barclays and Deutsche Bank were cut to A from A+, while Credit Suisse Group was reduced to A- from A.

Barclays declined 0.8 percent to 280.75 pence, Deutsche Bank dropped 1.4 percent to 31.46 euros and Credit Suisse slid 2.6 percent to 25.04 Swiss francs.

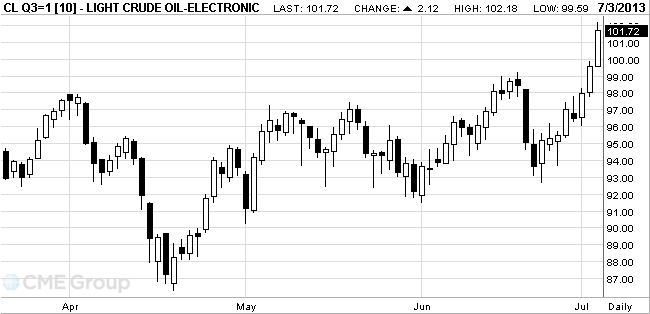

Airlines fell after West Texas Intermediate crude surged to as high as $102.18, its highest price since May 1, 2012, as political uncertainty in Egypt escalated and an industry report showed U.S. stockpiles shrank the most this year.

Air France, Europe's largest airline, dropped 1.6 percent to 6.74 euros. Deutsche Lufthansa AG slid 3.9 percent to 15.27 euros and International Consolidated Airlines Group SA, the owner of British Airways, declined 1.3 percent to 263.9 pence.

Chr. Hansen A/S dropped 4.8 percent to 191.1 kroner after the world's biggest maker of dairy enzymes cut its full-year sales forecast on lower prices for the red pigment carmine. Sales will probably rise 6 percent to 7 percent on a like- for-like basis, down from an earlier targeted range of 7 percent to 9 percent, the company said.

-

18:00

American focus: the euro and the pound rose

The euro rose against the dollar ahead of tomorrow's ECB meeting and against the closure of short positions in the pair. Contributed to the strengthening of the single currency weak data on activity in the U.S. service sector. The index of business activity in the U.S. service sector (ISM Non-Manufacturing) in June dropped to 52.2 from 53.7 the previous month. Experts predicted an increase to 54.3 index points. The indicator above 50 indicates growth in business activity, and the value of the index below 50 points - about the decline of activity. ISM index calculates the ISM Non-Manufacturing corporations on the basis of the 62 segments of the service sector, which accounts for about 90% of the U.S. economy.

Earlier, the euro fell against the dollar under the influence of weak PMI data in the service sector in the eurozone. Only Spain and France was able to make positive note in today's report services PMI, but the Germany and the euro area as a whole disappointed investors. As the results of the final studies, which were presented to Markit Economics, the results of last month to reduce activity in the private sector of the euro area has slowed down, which was associated with a slower decline in employment and the number of new orders. According to the report, the composite output index, that measures activity in the manufacturing and services sectors, rose in June to a level of 48.7, up from 47.7 in May. However, despite this significant improvement, the latter figure, after all, was slightly below the pre-assessment at the level of 48.9, indicating that the rate of decline was greater than anticipated. Recall that the value of this index is below 50 suggests contraction in activity. The composite index remains below this threshold for 17 consecutive month, but recent rate of decline in business activity in the private sector were the weakest in the past 15 months. Meanwhile, the data showed that the index of business activity in the services sector rose in June to the level of 48.3 from 47.2 in May, which was lower than the preliminary estimate at around 48.6.

Also note that the recent events in Portugal and Greece have added a negative. News about the growth of bond yields in the debt markets boosted concern among traders ahead of tomorrow's ECB meeting. As it became known, the yield on 10-year Portuguese bonds exceeded the psychologically important level of 7% (after Monday was less than 6.5%) and continues to grow, now residing at 8%. Portugal shares lost 5.6% this morning.

Value of the pound has increased significantly against the U.S. dollar, which has helped to publish a report on Britain. As the results of recent studies that have been presented Markit Economics and the Chartered Institute of Purchasing and Supply, at the end of last month, the growth in the British service sector accelerated to the highest level in more than two years, which was supported by a significant increase in new orders, which was the highest since 2007. According to the report, in June, the index of business activity in the services sector climbed to 56.9 - the highest level since March 2011. Note that by the end of May, the index rose to a level of 54.9. A reading above 50 indicates expansion in the sector of activity. We also add that with the last read it already was the sixth consecutive month extension. Many economists had forecast a slight drop in the index - to 54.6.

The data also showed that the growth in the number of new orders were the highest since June 2007, which encouraged the company to increase the number of jobs. It should be noted that this growth was the highest since August 2007. Meanwhile, it was reported that the level of trust between service providers in June reached a 14-month high. Note also that the increase in purchase and selling prices accelerated during the last month. But despite the increase in selling prices inflation was moderate, and was much lower than the cost price.

-

17:00

European stocks closed in minus: FTSE 100 6,229.87 -74.07 -1.17 %, CAC 40 3,702.01 -40.56 -1.08 %, DAX 7,829.32 -81.45 -1.03 %

-

16:40

Oil rose

Crude oil surged, with West Texas Intermediate surpassing $100 a barrel for the first time in nine months, as the government reported that

WTI climbed as much as 2.6 percent. The Energy Information Administration said that supplies fell 10.3 million barrels to 383.8 million. The report was projected to show a 2.25 million-barrel decline, according to a survey. Prices also rose after

WTI crude for August delivery gained $1.97, or 2 percent, to $101.57 a barrel at 10:34 a.m. on the New York Mercantile Exchange. The contract traded at $101.45 before the release of the EIA report at 10:30 a.m. in

There will be no floor trading in the Nymex tomorrow because of the U.S. Independence Day holiday. Any electronic trades will be booked for July 5.

Brent oil for August settlement rose $1.47, or 1.4 percent, to $105.47 a barrel on the London-based ICE Futures Europe exchange. The European benchmark grade was at a $3.90 premium to WTI after falling to as little as $3.10 today. The spread was $4.40 yesterday, the narrowest based on closing prices since Jan. 4, 2011. It was more than $23 in February.

-

16:20

Gold rises for third time in four sessions

Gold price shows a moderate growth after a decline on the eve associated with the strengthening of the dollar.

Today, the U.S. dollar shows a reverse trend after weak data on activity in the U.S. service sector. Data released on Wednesday by the Institute for Supply Management (ISM), showed that the rate of growth of activity in the U.S. non-manufacturing sector slowed in June, but employment grew. Reported Purchasing Managers Index (PMI) for the non-production sphere of the United States in June fell to 52.2 from 53.7 in May. Economists had forecast the index in June was 54.3. . Reading above 50 indicates expanding activity.

Investors are closely watching the changes in the monetary policy of both the United States and in other countries, as well as studying the economic data in the U.S. seeking guidance regarding the fate of the Fed's stimulus program.

Gold prices have been supported by the stimulus the Fed. Investors feared that the bond purchases will lead to higher inflation and a weakening dollar invested in precious metals as a hedge. However, most recently, fears that the Fed will soon complete these programs lowered the price of gold to near 3-year lows as traders were concerned about a possible decline in demand in the absence of these risks.

The cost of the August gold futures on COMEX today rose to 1259.30 dollars an ounce.

-

15:30

U.S.: Crude Oil Inventories, June -10.3

-

15:00

U.S.: ISM Non-Manufacturing, June 52.2 (forecast 54.3)

-

14:46

Option expiries for today's 1400GMT cut

EUR/USD $1.2930, $1.2950, $1.2955, $1.3000, $1.3025, $1.3035, $1.3050,$1.3055

USD/JPY Y99.50, Y100.00, Y100.20, Y100.30, Y100.40, Y100.50,Y101.00

EUR/JPY Y131.00

GBP/USD $1.5200, $1.5300

EUR/GBP stg0.8550, stg0.8585, stg0.8600

USD/CHF Chf0.9450, Chf0.9500, Chf0.9525, Chf0.9540, Chf0.9600

EUR/CHF Chf1.2400

EUR/SEK Sek8.7150

AUD/USD $0.9000, $0.9050, $0.9145, $0.9170

NZD/USD $0.7900

USD/CAD C$1.0550

-

14:41

U.S. Stocks open: Dow 14,875.43 -56.98 -0.38%, Nasdaq 3,420.98 -12.42 -0.36%, S&P 1,605.92 -8.16 -0.51%

-

14:29

Before the bell: S&P futures -0.31%, Nasdaq futures -0.17%

U.S. stock futures fell as turmoil in Egypt and political uncertainty in Portugal overshadowed better-than-estimated data on jobs growth and unemployment claims.

Global Stocks:

Nikkei 14,055.56 -43.18 -0.31%

Hang Seng 20,147.31 -511.34 -2.48%

Shanghai Composite 1,994.27 -12.29 -0.61%

FTSE 6,216.13 -87.81 -1.39%

CAC 3,694.92 -47.65 -1.27%

DAX 7,803.13 -107.64 -1.36%

Crude oil $101.41 (+1.82%)

Gold $1250.60 (+0.58%)

-

14:01

Upgrades and downgrades before the market open:

Upgrades:

Downgrades:

Alcoa (AA) downgraded to Neutral from Overweight at JP Morgan

Other: -

13:31

U.S.: Initial Jobless Claims, June 343 (forecast 345)

-

13:31

Canada: Trade balance, billions, May -0.3 (forecast -0.7)

-

13:31

U.S.: International trade, bln, May -45.0 (forecast -40.3)

-

13:15

U.S.: ADP Employment Report, June 188 (forecast 161)

-

13:00

European session: the British Pound has increased markedly

Data

01:00 Australia HIA New Home Sales, m/m May +3.9% +1.6%

01:30 Australia Retail sales (MoM) May +0.2% +0.4% +0.1%

01:30 Australia Retail Sales Y/Y May +3.1% +2.3%

01:30 Australia Trade Balance May 0.03 0.05 0.67

01:45 China HSBC Services PMI June 51.2 51.3

07:50 France Services PMI (Finally) June 46.5 46.5 47.2

07:55 Germany Services PMI (Finally) June 51.3 51.3 50.4

08:00 Eurozone Services PMI (Finally) June 48.6 48.6 48.3

08:30 United Kingdom Purchasing Manager Index Services June 54.9 54.6 56.9

08:30 United Kingdom BOE Credit Conditions Survey Quarter II

The euro exchange rate fell sharply against the dollar, but later was able to recover some lost positions. Note that the dynamics of trading was influenced by weak PMI data in the service sector in the eurozone. Only Spain and France was able to make positive note in today's report services PMI, but the Germany and the eurozone as a whole have disappointed investors, which helped strengthen the bearish sentiment.

As the results of the final studies, which were presented to Markit Economics, the results of last month to reduce activity in the private sector of the euro area has slowed down, which was associated with a slower decline in employment and the number of new orders.

According to the report, the composite output index, that measures activity in the manufacturing and services sectors, rose in June to a level of 48.7, up from 47.7 in May. However, despite this significant improvement, the latter figure, after all, was slightly below the pre-assessment at the level of 48.9, indicating that the rate of decline was greater than anticipated. Recall that the value of this index is below 50 suggests contraction in activity. The composite index remains below this threshold for 17 consecutive month, but recent rate of decline in business activity in the private sector were the weakest in the past 15 months. Meanwhile, the data showed that the index of business activity in the services sector rose in June to the level of 48.3 from 47.2 in May, which was lower than the preliminary estimate at around 48.6.

Also note that the recent events in Portugal and Greece have added a negative. News about the growth of bond yields in the debt markets boosted concern among traders ahead of tomorrow's ECB meeting. As it became known, the yield on 10-year Portuguese bonds exceeded the psychologically important level of 7% (after Monday was less than 6.5%) and continues to grow, now residing at 8%. Portugal shares lost 5.6% this morning.

Value of the pound has increased significantly against the U.S. dollar, which has helped to publish a report on Britain. As the results of recent studies that have been presented Markit Economics and the Chartered Institute of Purchasing and Supply, at the end of last month, the growth in the British service sector accelerated to the highest level in more than two years, which was supported by a significant increase in new orders, which was the highest since 2007.

According to the report, in June, the index of business activity in the services sector climbed to 56.9 - the highest level since March 2011. Note that by the end of May, the index rose to a level of 54.9. A reading above 50 indicates expansion in the sector of activity.

We also add that with the last read it already was the sixth consecutive month extension. Many economists had forecast a slight drop in the index - to 54.6.

The data also showed that the growth in the number of new orders were the highest since June 2007, which encouraged the company to increase the number of jobs. It should be noted that this growth was the highest since August 2007.

Meanwhile, it was reported that the level of trust between service providers in June reached a 14-month high. Note also that the increase in purchase and selling prices accelerated during the last month. But despite the increase in selling prices inflation was moderate, and was much lower than the cost price.

The Japanese yen strengthened against the dollar and the euro amid renewed tension in the periphery of Europe. Purchasing Managers Index PMI become an additional catalyst. In all countries except Italy, in June was marked improvement in the service sector than in May.

Also, the currency's expectations related to the release of U.S. data on changes in the number of employees from ADP, jobless claims and trade balance. Recall that in April, the U.S. trade deficit widened to $ 40.3 billion from $ 37.1 billion in March. In general, the trade deficit declined last year, which was associated with a slight decrease during the year of import and modest export growth. However, we do not expect that trade can make a significant contribution to overall growth. We add that the EU is mired in recession, and growth in the rest of the world is slowing down, as concerns about the economy of China is growing. Recovery of the U.S. economy also remains modest, keeping the consumer and business demand for imports at bay. Note that inbound and outbound container traffic fell by internal ports, and ISM manufacturing index for May showed that international trade has weakened during the month, especially exports.

EUR / USD: during the European session, the pair fell to $ 1.2921, and then recovered to $ 1.2972

GBP / USD: during the European session, the pair rose to $ 1.5273

USD / JPY: during the European session, the pair fell to Y99.24

At 12:15 in the U.S. will change ADP Employment for June. At 12:30 the U.S. and Canada will publish its trade balance. In the U.S., will be released at 12:30 number of initial applications for unemployment benefits and the number of continuing claims for unemployment benefits in 14:00 - a composite index of ISM non-manufacturing activity in June, and at 14:30 - the data on stocks of crude oil from Department of Energy.

-

12:45

Orders

EUR/USD

Offers $1.3100/10, $1.3070-80, $1.3040/50, $1.3020/25, $1.3000, $1.2985

Bids $1.2920, $1.2905/00, $1.2885/80, $1.2860/50, $1.2830/20

GBP/USD

Offers $1.5295/305, $1.5280, $1.5250/60, $1.5249

Bids $1.5200/190, $1.5160/50, $1.5120/10, $1.5100, $1.5080/70, $1.5010/00

AUD/USD

Offers $0.9220/25, $0.9190/00, $0.9145/50, $0.9120, $0.9100

Bids $0.9050, $0.9035, $0.9000, $0.8950, $0.8900

EUR/GBP

Offers stg0.8655/60, stg0.8630/40, stg0.8615-25, stg0.8590/600

Bids stg0.8490, stg0.8465/60, stg0.8445/40, stg0.8420

EUR/JPY

Offers Y131.31, Y131.00, Y130.55/60, Y130.00/20, Y129.75/80

Bids Y129.00, Y128.80, Y128.55/50, Y128.00, Y127.50

USD/JPY

Offers Y101.29/39, Y101.10/20, Y100.60, Y100.35/40, Y100.00

Bids Y99.55/50, Y99.20, Y99.10, Y99.00, Y98.50

-

11:30

European stock indices fell

European stocks dropped the most in more than a week as Portugal's coalition government splintered and crude oil surged above $100 a barrel amid rising unrest in Egypt. Asian shares and U.S. index futures also declined.

The Stoxx Europe 600 Index (SXXP) lost 1.2 percent to 283.8 at 9:57 a.m. in London, extending the retreat from its 2013 high on May 22 to 8.6 percent. Portugal's benchmark PSI-20 Index plunged 7 percent, the most since October 2008. The MSCI Asia Pacific Index slumped 1 percent and S&P 500 Index futures slid 0.6 percent, after the benchmark gauge closed lower yesterday.

The Stoxx 600 (SXXP) slid 0.4 percent yesterday after a report showed U.K. construction expanded less than forecast. Asian stocks fell today as China's services-industry growth slowed in June. Data from the ADP Research Institute at 8:15 a.m. New York time may show U.S. companies hired more workers last month.

Espirito Santo, Portugal's biggest bank by market capitalization, tumbled 12 percent to 53.8 euro cents, its biggest drop since April 2012. Comercial Portugues plunged 15 percent to 7.9 euro cents, the most since June 2012. The country's bonds slumped, pushing the 10-year yield above 8 percent, as two ministers resigned amid austerity fatigue.

Prime Minister Pedro Passos Coelho said in a televised speech yesterday he's trying to hold his government together after losing both his finance minister and his foreign minister.

Secretary of State for Treasury Maria Luis Albuquerque replaced Vitor Gaspar at the Ministry of Finance. That prompted Paulo Portas, who leads the smaller CDS party in the coalition government, to quit, saying the new minister would offer "mere continuity" of the country's deficit-cutting plans.

Banks in Europe fell as Standard & Poor's cut long-term counterparty credit ratings for Barclays and Deutsche Bank to A from A+. Credit Suisse Group was lowered to A- from A.

Barclays declined 3.8 percent to 272.4 pence, Deutsche Bank dropped 3.5 percent to 30.80 euros and Credit Suisse slid 2.9 percent to 24.96 Swiss francs.

FTSE 100 6,206.67 -97.27 -1.54%

CAC 40 3,683.17 -59.40 -1.59%

DAX 7,788.61 -122.16 -1.54%

-

10:30

Option expiries for today's 1400GMT cut

EUR/USD $1.2930, $1.2950, $1.2955, $1.3000, $1.3025, $1.3035, $1.3050,$1.3055

USD/JPY Y99.50, Y100.00, Y100.20, Y100.30, Y100.40, Y100.50,Y101.00

GBP/USD $1.5200, $1.5300

EUR/GBP stg0.8550

USD/CHF Chf0.9450, Chf0.9500, Chf0.9525, Chf0.9540, Chf0.9600

EUR/SEK Sek8.7150

AUD/USD $0.9000, $0.9145

NZD/USD $0.7900

-

10:02

Eurozone: Retail Sales (YoY), May -0.1% (forecast -1.9%)

-

10:01

Eurozone: Retail Sales (MoM), May +1.0% (forecast +0.4%)

-

09:29

United Kingdom: Purchasing Manager Index Services, June 56.9 (forecast 54.6)

-

09:23

Asia Pacific stocks close

Asian stocks dropped for the first time in six days as resource companies retreated after metals prices slid overnight and an official report showed China's services industry expanded at a slower pace.

Nikkei 225 14,055.56 -43.18 -0.31%

Hang Seng 20,197.19 -461.46 -2.23%

S&P/ASX 200 4,744.13 -89.88 -1.86%

Shanghai Composite 1,994.27 -12.29 -0.61%

BHP Billiton Ltd., the world's largest mining company, sank 3.2 percent.

Tokyo Electric Power Co. led declines on the Asia-Pacific equity benchmark after the Japanese utility soared 19 percent yesterday.

Suntory Beverage & Food Ltd. gained 1.5 percent on its debut in Tokyo after raising almost $4 billion in Asia's largest public offering this year.

-

08:58

Eurozone: Services PMI, June 48.3 (forecast 48.6)

-

08:53

Germany: Services PMI, June 50.4 (forecast 51.3)

-

08:48

France: Services PMI, June 47.2 (forecast 46.5)

-

08:44

FTSE 100 6,242.18 -61.76 -0.98%, CAC 40 3,694.41-48.16 -1.29%, Xetra DAX 7,799.72 -111.05 -1.40%

-

07:24

Asian session: The Dollar Index rose

01:00 Australia HIA New Home Sales, m/m May +3.9% +1.6%

01:30 Australia Retail sales (MoM) May +0.2% +0.4% +0.1%

01:30 Australia Retail Sales Y/Y May +3.1% +2.3%

01:30 Australia Trade Balance May 0.03 0.05 0.67

01:45 China HSBC Services PMI June 51.2 51.3

The Dollar Index rose to the highest level in a month before a report forecast to show companies in the U.S. added more jobs in June. Companies in the U.S. added 160,000 workers last month after increasing positions by 135,000 in May, analysts in a Bloomberg poll predicted before a report today by the Roseland, New Jersey-based ADP Research Institute.

The dollar traded near the strongest in a month versus the euro before data that may show service industries expanded at the fastest pace since March. The Institute for Supply Management's non-manufacturing index climbed to 54 last month from 53.7 in May, a report from the Tempe, Arizona-based group is predicted to show today, according to the median estimate in a Bloomberg News survey. A reading above 50 indicates expansion in the industries that make up almost 90 percent of the economy.

New York Fed President William C. Dudley said yesterday economic growth will probably quicken in 2014, possibly warranting a reduction in the central bank's bond-purchase program, which currently stands at $85 billion a month.

Europe's shared currency weakened against most of its 16 major counterparts before the European Central Bank meets tomorrow. The ECB will keep its main refinancing rate at a record-low 0.5 percent on July 4, according to economists in a Bloomberg survey. Policy "will stay accommodative for the foreseeable future," President Mario Draghi said in Paris on June 26.

Australia's currency declined to its lowest in more than two years after RBA Governor Stevens said the downward phase of the resource investment boom in his country "appears likely to pose significant challenges."

EUR / USD: during the Asian session the pair traded in the range of $ 1.2965/85

GBP / USD: during the Asian session the pair traded in the range of $ 1.5140/60

USD / JPY: during the Asian session the pair traded in the range Y100.45/85

There is a full calendar on both sides of the Atlantic Wednesday, with some US data releases pushed forward by 24 hours ahead of the Independence Day holiday on Thursday. The European calendar gets underway with a string of service sector survey data, starting at 0713GMT with the release of the Spanish June service sector PMI numbers. At 0730GMT, Sweden's Riksbank releases the June Monetary Policy Report. More service sector PMI numbers come through at 0743GMT when Italian numbers cross the wires, followed by French data at 0748GMT, German at 0753GMT and the collated EMU data at 0758GMT. Economists are looking for a tick up across the data following the slightly better than expected manufacturing numbers seen earlier in the week. There is further EMU data set for release at 0900GMT when the May retail sales data will cross the wires. EC Jose Manuel is scheduled to attend the Youth Unemployment Summit, in Berlin, from 1000GMT. Back in Europe, Buba Board member Joachim Nagel speech on internationalising the renminbi, in Frankfurt from 1240GMT. Angela Merkel will give a press conference after the European conference on youth unemployment, in Berlin from 1515GMT.

-

07:23

European bourses are initially seen trading lower Wednesday: the FTSE down 378, the DAX down 45 and the CAC down 24.

-

06:22

Commodities. Daily history for Jul 2’2013:

Change % Change Last

GOLD 1,241.90 -13.80 -1.10%

OIL (WTI) 99.37 1.38 1.41%

-

06:22

Stocks. Daily history for Jul 2’2013:

Nikkei 225 14,098.74 246,24 1,78%

Hang Seng 20,775.35 -27,94 -0,13%

S & P / ASX 200 4834 123,71 2,63%

Shanghai Composite 2,006.24 +11.00 +0.55%

FTSE 100 6,303.94 -3.84 -0.06%

CAC 40 3,742.57 -24.91 -0.66%

DAX 7,910.77 -73.15 -0.92%

Dow -42.78 14,932.18 -0.29%

Nasdaq -1.09 3,433.40 -0.03%

S&P -0.89 1,614.07 -0.06%

-

06:21

Currencies. Daily history for Jul 2'2013:

(pare/closed(00:00 GMT +02:00)/change, %)

EUR/USD $1,2982 -0,61%

GBP/USD $1,5154 -0,42%

USD/CHF Chf0,9504 +0,56%

USD/JPY Y100,64 +1,02%

EUR/JPY Y130,62 +0,39%

GBP/JPY Y152,46 +0,58%

AUD/USD $0,9145 -0,96%

NZD/USD $0,7762 -0,75%

USD/CAD C$1,0547 +0,49%

-

06:00

Schedule for today, Wednesday, July 3’2013:

01:00 Australia HIA New Home Sales, m/m May +3.9% +1.6%

01:30 Australia Retail sales (MoM) May +0.2% +0.4% +0.1%

01:30 Australia Retail Sales Y/Y May +3.1% +2.3%

01:30 Australia Trade Balance May 0.03 0.05 0.67

01:45 China HSBC Services PMI June 51.2 51.3

07:00 United Kingdom Halifax house price index 3m Y/Y June +2.6% +3.6%

07:50 France Services PMI June 46.5 46.5

07:55 Germany Services PMI June 51.3 51.3

08:00 Eurozone Services PMI June 48.6 48.6

08:30 United Kingdom Purchasing Manager Index Services June 54.9 54.6

08:30 United Kingdom BOE Credit Conditions Survey Quarter II

09:00 Eurozone Retail Sales (MoM) May -0.5% +0.4%

09:00 Eurozone Retail Sales (YoY) May -1.1% -1.9%

12:15 U.S. ADP Employment Report June 135 161

12:30 Canada Trade balance, billions May -0.6 -0.7

12:30 U.S. International trade, bln May -40.3 -40.3

12:30 U.S. Initial Jobless Claims June 346 345

14:00 U.S. ISM Non-Manufacturing June 53.7 54.3

14:00 U.S. Treasury Sec Lew Speaks

14:30 U.S. Crude Oil Inventories June 0.0

-