Notícias do Mercado

-

20:02

DJIA 15,239.40 103.54 0.68%, S&P 500 1,640.97 9.08 0.56%, NASDAQ 3,482.79 3.42 0.10%

-

20:00

U.S.: Consumer Credit , May 19.6 (forecast 13.2)

-

19:20

American focus: the dollar weakened against major currencies

Euro showed moderate gains against the dollar amid ECB President. Mario Draghi's speech in the European Parliament reiterated that monetary policy of the Bank will remain accommodative for as long as necessary, and that interest rates will be maintained at low levels for a long time. Although the situation in the euro zone has not yet stabilized and the downside risks to the economy persist, the ECB expects that in the 2nd half of 2013 in the region will begin a gradual recovery of the economy. The decisive factor in this process will be stable banking system. Draghi said that the ECB's policy has helped stabilize financial conditions in the euro area. Meanwhile, the actions of the EU governments have stimulated the growth of confidence in the eurozone, and sentiment indicators have risen recently.

Note also that break the euro did not help even weak data for the euro area and Germany. Recall that today was presented indicator of investor confidence Sentix. According to reports, in June, the index of confidence of European investors Sentix fell to around -12.6 from -11.6 in May result.

Meanwhile, data from the Federal Ministry of Economics and Technology showed that by the end of May the volume of industrial production in Germany fell significantly more than expected, which was associated with a significant reduction in the construction and energy sectors. Apparently, the recovery of Europe's largest economy remains fragile in the face of uncertain prospects for foreign trade. According to the report, on a monthly basis in May, industrial production fell by 1%, thus showing the biggest drop since October 2012. It is worth noting that many economists had expected a drop in production was 0.5%, after rising 2% in April. In addition, it was reported that on an annualized basis, industrial output fell by 1%, offsetting an increase of 0.9%, which was recorded in April.

The yen against the dollar fluctuates, due to the lack of important publications and events. Note that in part influenced by the currency data from the Ministry of Finance of Japan, which showed that by the end of May a positive current account balance declined in May, but, nevertheless, continued to remain in positive territory for the fourth consecutive month, after fixing the deficit in the current three consecutive months. According to a report by the end of May current account surplus decreased to the level of 540.7 billion yen, compared with a surplus of 750.0 billion yen in April. It is worth noting that according to the average forecasts of experts the value of this index was to drop to 600.0 billion yen. In addition, it was reported that the surplus jumped in May by 58.1 percent on an annualized basis, which was also below expectations for a jump of 91.6 percent after a surge 100.8 percent in the previous month. The Ministry of Finance also reported that the trade deficit in the month of May totaled 906.7 billion yen compared to the predictions of experts at the level of 902.1 billion yen deficit, and after a deficit of 818.8 billion yen in the previous month. We add that the volume of exports increased by 9.1 percent per year, reaching at the same level of 5.526 trillion. yen, compared with 5.568 trillion. yen in April. Meanwhile, imports grew by 9.6 per cent per annum - up to 6433 billion yen after reaching 6,387 billion a month earlier.

-

18:20

European stocks close

European stocks rose, rebounding from their biggest decline in almost two weeks, amid speculation that economic data will improve and as Portugal’s politicians reached an agreement to hold the governing coalition together.

In Portugal, Prime Minister Pedro Passos Coelho proposed that Paulo Portas, leader of the junior party in the governing coalition, become vice premier. The appointment helps cement a deal to hold the coalition together. Portugal’s PSI 20 Index retreated 2.7 percent last week when Portas resigned after Coelho appointed a new finance minister.

Euro-area finance ministers meeting in Brussels discussed Greece’s progress in meeting the conditions needed to obtain further aid from the International Monetary Fund, European Central Bank and European Commission.

Approval of an agreement at the meeting of euro-area finance ministers in Brussels would allow Greece, which has been unable to tap bond markets since 2010, to obtain a loan of 8.1 billion euros ($10.4 billion).

In Germany, a report showed that industrial production declined 1 percent in May, more than the 0.5 percent drop, which was the median forecast of 38 economists in a Bloomberg News survey. It surged a revised 2 percent in April.

National benchmark indexes advanced in all 18 western-European markets today. France’s CAC 40 gained 1.9 percent and Germany’s DAX climbed 2.1 percent. The U.K.’s FTSE 100 added 1.2 percent. The PSI 20 rallied 2.3 percent.

Novartis climbed 1.3 percent to 68.50 Swiss francs as the company said its secukinumab drug proved better at clearing the skin of people with plaque psoriasis than Enbrel.

Lloyds advanced 3.8 percent to 67.1 pence. Former Standard Chartered Chairman Mervyn Davies is assembling a group of investors to bid for part of the U.K. government’s 39 percent stake in the lender, according to a person with knowledge of the talks. The group has yet to reach an agreement with the Treasury, the person added.

Bovis Homes Group Plc jumped 7.1 percent to 830 pence after the U.K. housebuilder said that increased volume and higher margins led to a bigger profit in the first half. The company said it will probably report a housing gross margin of about 23 percent, compared with 20.9 percent a year earlier.

Hikma Pharmaceuticals Plc surged 5.6 percent to 1,050 pence, the highest price since its initial public offering in November 2005, after the company raised its full-year revenue forecast. It predicted that revenue will grow by 17 percent in 2013, compared with a previous projection of 13 percent.

-

17:00

European stocks closed in plus: FTSE 100 6,450.07 +74.55 +1.17%, CAC 40 3,823.83 +69.98 +1.86%, DAX 7,968.54 +162.54 +2.08%

-

16:41

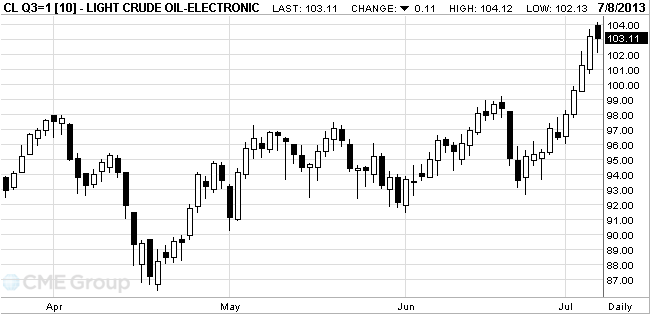

Oil dropped from a 14-month high

West Texas Intermediate crude dropped from a 14-month high after an official said Egypt’s Suez Canal is “secure” and ship traffic through the waterway is “normal,” even as violence escalated in Cairo.

WTI fell as much as 1.1 percent as Tarek Hassanein, a Suez Canal Authority spokesman, said that 55 ships are scheduled to pass through the channel. Prices topped $104 a barrel today as Egyptian security forces fought with supporters of ousted President Mohamed Mursi, leaving at least 50 dead.

WTI crude for August delivery declined 17 cents, or 0.2 percent, to $103.05 a barrel at 11:12 a.m. on the New York Mercantile Exchange. The volume of all futures traded was 25 percent more than the 100-day average. Earlier it rose to $104.12, the highest intraday level since May 3, 2012.

Brent oil for August settlement decreased 28 cents, or 0.3 percent, to $107.44 a barrel on the London-based ICE Futures Europe exchange. The volume for all contracts was 1 percent below the 100-day average. The European benchmark grade traded at a $4.39 premium to WTI, down from $4.50 on July 5.

-

16:20

Gold rose

Gold prices rose after Friday's decline, but growth is constrained by a high dollar.

The spot price fell by 10 percent after Federal Reserve Chairman Ben Bernanke said in June that the pace of U.S. economic growth allows the central bank to reduce the volume of buying up bonds this year. Reducing incentives will increase interest rates and the dollar, making gold less attractive to investors outside the United States.

In the second quarter, gold fell by 23 percent, which was a record quarterly decline, and on June 28 the price dropped to a low of nearly three years, $ 1.180,70 an ounce.

The number of employees in the U.S. economy, excluding the agriculture sector in June increased by 195,000, while analysts had expected growth of 165,000, and the unemployment rate was 7.6 percent, the forecast of 7.5 percent. These data fueled fears that the Fed will soon begin to reduce incentives.

On Monday, the dollar rose to a three-year high against a basket of world currencies. Stocks of the world's largest exchange-traded fund backed by gold (ETF) SPDR Gold Trust on Friday fell 0.3 percent to 30.92 million ounces - the lowest level since February 2009.

The cost of the August gold futures on COMEX today rose to a high of $ 1237.40 an ounce.

-

15:36

Canada: Bank of Canada Senior Loan Officer , Quarter II -12.7 (forecast -5.0)

-

14:46

Option expiries for today's 1400GMT cut

EUR/USD $1.2750, $1.2830, $1.2900, $1.3000, $1.3100, $1.3115

USD/JPY Y100.00, Y100.50, Y101.00, Y101.20, Y101.50, Y101.60

EUR/JPY Y123.00

GBP/USD $1.4900, $1.5000

USD/CHF Chf0.9485

EUR/CHF Chf1.2200

AUD/USD $0.9015, $0.9150, $0.9180

AUD/JPY Y90.15, Y91.55

NZD/JPY Y77.40

CAD/JPY Y95.75

-

14:35

U.S. Stocks open: Dow 15,211.41 +75.57 +0.50%, Nasdaq 3,493.96 +14.58 +0.42%, S&P 1,639.87 +7.98 +0.49%

-

14:28

Before the bell: S&P futures +0.48%, Nasdaq futures +0.45%

U.S. stock futures rose as investors awaited on starts of second-quarter earnings season which kicks off with results after the close from aluminum producer Alcoa (AA).

Global Stocks:

Nikkei 14,109.34 -200.63 -1.40%

Hang Seng 20,582.19 -272.48 -1.31%

Shanghai Composite 1,958.27 -48.93 -2.44%

FTSE 6,460.05 +84.53 +1.33%

CAC 3,827.96 +74.11 +1.97%

DAX 7,990.84 +184.84 +2.37%

Crude oil $102.29 -0.90%

Gold $1232.60 +1.64%

-

13:47

Upgrades and downgrades before the market open:

Upgrades:

Downgrades:

Intel (INTC) downgraded from Equal Weight to Underweight at Evercore

Other:

-

13:30

Canada: Building Permits (MoM) , May +4.5% (forecast +2.6%)

-

13:20

European session: the euro exchange rate rose slightly

Data

01:30 Australia ANZ Job Advertisements (MoM) June -2.4% -1.8%

05:00 Japan Eco Watchers Survey: Current June 55.7 55.6 53.0

05:00 Japan Eco Watchers Survey: Outlook June 56.2 53.6

05:45 Switzerland Unemployment Rate June 3.2% 3.2% 3.2%

06:00 Germany Current Account May 17.6 14.8 11.2

06:00 Germany Trade Balance May 17.7 17.4 14.1

07:15 Switzerland Industrial Production (QoQ) Quarter I +1.7% +1.4% +3.0%

07:15 Switzerland Industrial Production (YoY) Quarter I -2.4% +2.0% +0.6%

08:30 Eurozone Sentix Investor Confidence July -11.6 -11.5 -12.6

09:00 Eurozone Eurogroup Meetings

10:00 Germany Industrial Production s.a. (MoM) May +2.0% -0.5% -1.0%

10:00 Germany Industrial Production (YoY) May +1.0% -0.5% -1.0%

The euro rose against the dollar rebounded slightly after a significant decline Friday, as many market participants are waiting for the speech of President of the European Central Bank Mario Draghi. Earlier, the official said that the interest rate of the European Central Bank will remain at the current low level or near for a long period of time. Statement M.Dragi withholding rates low for a long time is an innovation for the ECB and reflects - both in form and in substance - the wording used by the Federal Reserve System of the USA before moving to forecasting interest rates of its leaders.

Note also that the euro does not break even helped the weak data for the euro area and Germany.

Recall that today was presented indicator of investor confidence Sentix. According to reports, in June, the index of confidence of European investors Sentix fell to around -12.6 from -11.6 in May result.

Meanwhile, data from the Federal Ministry of Economics and Technology have shown that up to May, industrial production in Germany fell significantly more than expected, which was associated with a significant reduction in the construction and energy sectors. Apparently, the recovery of Europe's largest economy remains fragile in the face of uncertain prospects for foreign trade. According to the report, on a monthly basis in May, industrial production fell by 1%, thus showing the biggest drop since October 2012. It is worth noting that many economists had expected a drop in production was 0.5%, after rising 2% in April.

In addition, it was reported that on an annualized basis, industrial output fell by 1%, offsetting an increase of 0.9%, which was recorded in April.

The yen against the dollar holds tight, due to the lack of important publications and events. Note that in part influenced by the currency data from the Ministry of Finance of Japan, which showed that up to May, a positive current account balance has decreased in the month of May, but, nevertheless, continued to remain in positive territory for the fourth consecutive month, after fixing the deficit for three consecutive months.

According to a report on the results of May, the current account surplus decreased to the level of 540.7 billion yen, compared with a surplus of 750.0 billion yen in April. It is worth noting that according to the average forecasts of experts the value of this index was to drop to 600.0 billion yen.

In addition, it was reported that the surplus jumped in May by 58.1 percent on an annualized basis, which was also below expectations for a jump of 91.6 percent after a surge 100.8 percent in the previous month.

The Ministry of Finance also reported that the trade deficit in the month of May totaled 906.7 billion yen compared to the predictions of experts at the level of 902.1 billion yen deficit, and after a deficit of 818.8 billion yen in the previous month. We add that the volume of exports increased by 9.1 percent per year, reaching at the same level of 5.526 trillion. yen, compared with 5.568 trillion. yen in April. Meanwhile, imports grew by 9.6 per cent per annum - up to 6433 billion yen after reaching 6,387 billion a month earlier.

EUR / USD: during the European session, the pair rose to $ 1.2860

GBP / USD: during the European session, the pair rose to $ 1.4918

USD / JPY: during the European session, the pair fell to Y100.94

At 12:30 GMT Canada will report on changes in the volume of building permits issued in May, and the 14:30 GMT release indicator of expectations in the area of financial institutions and the indicator of expected growth in trade for the 2nd quarter. At 22:00 GMT New Zealand will present a sentiment indicator of the business environment of the NZIER for the 2nd quarter. At 23:01 GMT Britain will publish the BRC Retail Sales Monitor for June and the balance of the price of RICS House in June.

-

13:00

Orders

EUR/USD

Offers $1.2950/60, $1.2930/35, $1.2880-900, $1.2850

Bids $1.2811, $1.2810/00, $1.2780, $1.2755/45

GBP/USD

Offers $1.5030, $1.4990/5010, $1.4960/65, $1.4940/50, $1.4910/20

Bids $1.4850, $1.4822, $1.4800, $1.4780/70

AUD/USD

Offers $0.9220/25, $0.9200, $0.9175/80, $0.9145/50, $0.9120, $0.9095/00

Bids $0.9025, $0.9000, $0.8950, $0.8915/10, $0.8900

EUR/JPY

Offers Y131.50, Y131.15/20, Y131.00, Y130.50, Y130.15/20

Bids Y129.70/60, Y129.20, Y129.10/00, Y128.55/50

USD/JPY

Offers Y102.75/80, Y102.45/50, Y102.20, Y102.00, Y101.50/60

Bids Y100.80, Y100.60, Y100.55/50, Y100.25/20, Y100.00

EUR/GBP

Offers stg0.8690/95, stg0.8655/65, stg0.8640, stg0.8630, stg0.86275

Bids stg0.8570/65, stg0.8550, stg0.85115, stg0.8500

-

11:30

European stock indices rose

European stocks rose, rebounding from their biggest decline in almost two weeks, amid speculation that economic data will improve and as Portugal’s politicians reached an agreement to hold the governing coalition together. U.S. index futures gained and Asian shares fell.

The Stoxx 600 increased 1.4 percent to 292.26 at 11:10 a.m. in London. Standard & Poor’s 500 Index futures added 0.6 percent after the equity benchmark rose 1 percent on July 5 after a better-than-forecast payrolls report.

In Portugal, Prime Minister Pedro Passos Coelho proposed that Paulo Portas, leader of the junior party in the governing coalition, become vice premier. The appointment helps cement a deal to hold the coalition together. Portugal’s PSI 20 Index retreated 2.7 percent last week when Portas resigned after Coelho appointed a new finance minister.

ECB President Mario Draghi speaks at the quarterly hearing of the Committee on Economic and Monetary Affairs of the European Parliament at 3 p.m. in Brussels.

In Germany, a report showed that industrial production declined 1 percent in May, more than the 0.5 percent drop, which was the median forecast of economists in. It surged a revised 2 percent in April.

Novartis climbed 1.7 percent to 68.75 Swiss francs, contributing the most to the Stoxx 600’s gain, as the company said its secukinumab drug proved better at clearing the skin of people with plaque psoriasis than Enbrel.

Lloyds Banking Group Plc advanced 2.7 percent to 66.4 pence. Former Standard Chartered Chairman Mervyn Davies is assembling a group of investors to bid for part of the U.K. government’s 39 percent stake in the lender, according to a person with knowledge of the talks. The group has yet to reach an agreement with the Treasury, the person added.

Bovis Homes advanced 4.6 percent to 810.5 pence after the U.K. housebuilder said that increased volume and higher margins led to a bigger profit in the first half. The company said it will probably report a housing gross margin of about 23 percent, compared with 20.9 percent a year earlier.

Hikma Pharmaceuticals Plc surged 8 percent to 1,073 pence, its highest price since at least November 2005, after the company raised its full-year revenue forecast. It predicted that group revenue will grow by about 17 percent in 2013, compared with a previous projection of about 13 percent.

FTSE 100 6,437.26 +61.74 +0.97%

CAC 40 3,821.48 +67.63 +1.80%

DAX 7,977.21 +171.21 +2.19%

-

11:01

Germany: Industrial Production (YoY), May -1.0% (forecast -0.5%)

-

11:00

Germany: Industrial Production s.a. (MoM), May -1.0% (forecast -0.5%)

-

10:32

Option expiries for today's 1400GMT cut

EUR/USD $1.2750, $1.2830, $1.2900, $1.3000, $1.3100, $1.3115

USD/JPY Y100.00, Y100.50, Y101.00, Y101.20, Y101.50, Y101.60

EUR/JPY Y123.00

GBP/USD $1.4900, $1.5000

USD/CHF Chf0.9485

EUR/CHF Chf1.2200

AUD/USD $0.9015, $0.9150, $0.9180

AUD/JPY Y90.15, Y91.55

NZD/JPY Y77.40

CAD/JPY Y95.75

-

10:04

Asia Pacific stocks close

Asian stocks dropped the most in two weeks amid concern a credit squeeze in China will curb growth and after a better-than-forecast U.S. jobs report fueled concern that the Federal Reserve may begin reducing stimulus this year.

Nikkei 225 14,109.34 -200.63 -1.40%

Hang Seng 20,601.75 -252.92 -1.21%

S&P/ASX 200 4,809.5 -32.25 -0.67%

Shanghai Composite 1,958.27 -48.93 -2.44%

BHP Billiton Ltd., the world’s biggest mining company, fell 2.1 percent in Sydney as metals prices retreated the most in two months.

Asiana Airlines Inc. tumbled 5.8 percent in Seoul after one of its planes crashed at San Francisco International Airport.

Zijin Mining Group Co. dropped 7 percent in Hong Kong after China’s biggest gold miner by market value said profit may slump as much as 55 percent.

-

09:25

FTSE 100 6,448.51 +72.99 +1.14%, CAC 40 3,812.48 +58.63 +1.56%, Xetra DAX 7,930.63 +124.63 +1.60%

-

08:15

Switzerland: Industrial Production (YoY), Quarter I +0.6% (forecast +2.0%)

-

07:42

European bourses are initially seen trading sharply higher Monday: the FTSE up 69, the DAX up 64 and the CAC up 39

-

07:25

Asian session: The Dollar Index rose

01:30 Australia ANZ Job Advertisements (MoM) June -2.4% -1.8%

The Dollar Index rose to its highest in three years before Federal Reserve Chairman Ben S. Bernanke speaks this week amid speculation signs of economic growth will impel the central bank to slow stimulus.

The greenback touched a five-week high versus the yen ahead of minutes of the Fed’s June 18-19 meeting where Bernanke said policy makers may begin slowing bond purchases this year. Data last week showed U.S. employers added more jobs than economists estimated. The U.S. Labor Department reported on July 5 that payrolls increased by 195,000 in June for a second-straight month. A Bloomberg News survey of economists forecast a gain of 165,000 after a previously reported 175,000 rise in May. The jobless rate stayed at 7.6 percent.

The euro held a two-day decline before European Central Bank President Mario Draghi speaks in Brussels today and Germany releases data on industrial production. In Europe, Draghi is due to speak in Brussels today after he made an unprecedented pledge last week to keep interest rates low for an extended period. The ECB’s monetary policy stance will “remain accommodative” for as long as needed to spur growth, he said July 4 after a policy meeting.

Industrial production in Germany probably fell 0.5 percent in May from the previous month, when it gained 1.8 percent, according to the median estimate of economists in surveyed by Bloomberg before the data today.

EUR / USD: during the Asian session the pair traded in the range of $ 1.2810/30

GBP / USD: during the Asian session the pair traded in the range of $ 1.4855/85

USD / JPY: during the Asian session the pair rose to Y101.55

This week's US calendar is light on data, with the latest FOMC minutes likely to be the main event. There is a fuller US data calendar, although the main releases are expected later in the week. Monday's calendar kicks off at 0600GMT with the release of the German May trade balance. Analysts see the balance coming in at E17.8 billion. At 0630GMT, the French June Ban of France business survey will be published at 0630GMT. At 0800GMT, ECB Governing Councilmember Ewald Nowotny will give a press conference on the Financial Stability Report, in Vienna. German May industrial output numbers will cross the wires at 1000GMT. Economist estimates see both the M/M and Y/Y numbers down 0.5%. Also at 1000GMT, the EMU May OECD leading indicator is expected. Across the Atlantic, the calendar gets underway at 1230GMT with the release of the Canadian May Building permits data. In the US, at 1400GMT, the June Employment Trends Index data will cross the wires. At 1900GMT, the May consumer credit numbers will be released. Estimates see the number coming in at $12.5 bn.

-

07:02

Germany: Current Account , May 11.2 (forecast 14.8)

-

07:00

Germany: Trade Balance, May 14.1 (forecast 17.4)

-

06:45

Switzerland: Unemployment Rate, June 3.2% (forecast 3.2%)

-

06:02

Schedule for today, Monday, July 8’2013:

01:30 Australia ANZ Job Advertisements (MoM) June -2.4% -1.8%

05:00 Japan Eco Watchers Survey: Current June 55.7 55.6

05:00 Japan Eco Watchers Survey: Outlook June 56.2

05:45 Switzerland Unemployment Rate June 3.2% 3.2%

06:00 Germany Current Account May 17.6 14.8

06:00 Germany Trade Balance May 17.7 17.4

07:15 Switzerland Industrial Production (QoQ) Quarter I +1.7% +1.4%

07:15 Switzerland Industrial Production (YoY) Quarter I -2.4% +2.0%

08:30 Eurozone Sentix Investor Confidence July -11.6 -11.5

09:00 Eurozone Eurogroup Meetings

10:00 Germany Industrial Production s.a. (MoM) May +1.8% -0.5%

10:00 Germany Industrial Production (YoY) May +1.0% -0.5%

12:30 Eurozone ECB President Mario Draghi Speaks

12:30 Canada Building Permits (MoM) May +10.5% +2.6%

13:30 Eurozone ECB President Mario Draghi Speaks

14:30 Canada Bank of Canada Senior Loan Officer Quarter II -5.8 -5.0

22:00 New Zealand NZIER Business Confidence Quarter II 23

23:01 United Kingdom BRC Retail Sales Monitor y/y June +1.8% +1.9%

23:01 United Kingdom RICS House Price Balance June +5% +10%

-

06:01

Japan: Eco Watchers Survey: Outlook, June 53.0

-

06:00

Japan: Eco Watchers Survey: Current , June 53.0 (forecast 55.6)

-