Notícias do Mercado

-

23:51

Japan Trade Balance - BOP Basis above expectations (¥-2110.9B) in November: Actual (¥-1537.8B)

-

23:50

Japan Bank Lending (YoY) came in at 2.7% below forecasts (2.8%) in December

-

23:50

Japan Current Account n.s.a. above forecasts (¥471.1B) in November: Actual (¥1803.6B)

-

23:42

GBP/JPY tumbles to near 160.20 as BoJ to review the impact of decade-long easy policy

- GBP/JPY has witnessed a sell-off and has dropped vertically to near 160.20.

- The announcement of the review of secular loose monetary policy by the BoJ has strengthened the Japanese Yen.

- Pessimism for Pound Sterling and the UK economy seems over, which will be brighter for London in CY2023.

The GBP/JPY pair has sensed immense pressure after failing to shift its auction profile above the immediate resistance of 161.00 in the early Asian session. The cross has slipped sharply to near 160.40 as the Bank of Japan (BoJ) has announced that it will review the negative impact of ultra-loose monetary policy from a secular period next week, reported Yomiuri.

Chatters over exit from decade-long ultra-loose monetary policy in the Japanese region has gained strength amid difficulties in expanding wages and supporting the Japanese yen against the strengthening US Dollar. Earlier, Michio Saito, Director-General of the Financial Bureau at Japan’s Ministry of Finance (MoF), said in a statement early Wednesday, “interest rates remain low but the current situation won't last indefinitely.”

On the United Kingdom front, the UK economy faced sheer volatility amid poor risk-management systems by commercial banks and political instability led by the debacle of former Prime Ministers Boris Johnson and Liz Truss in CY2022. The current year seems brighter for the Pound Sterling after current UK PM Rishi Sunak held a higher position.

In the view of economists at MUFG Bank, we may have reached “peak pessimism” for the UK and the Pound. Much greater political stability this year than last is one factor here and we can very likely assume that PM Sunak will bring greater credibility after the turmoil of 2022. “Another consequence of having Rishi Sunak at No. 10 is the prospect of better relations with the EU and with that a possible deal to break the deadlock regarding the Northern Ireland Protocol.”

On the economic data front, investors will keep an eye on the UK Production data, which is scheduled for Friday. On an annual basis, Industrial Production is expected to contract by 3.0% and Manufacturing Production may contract by 4.8%. This might impact harshly on the United Kingdom economy but will delight the Bank of England (BOE) as it will trim inflation projections.

-

23:38

EUR/JPY Price Analysis: Struggles at 142.00 and drops, extending its losses beneath the 100-DMA

- EUR/JPY stalls its rally and clashes with a confluence of technical indicators.

- A break below the 20-day EMA could pave the way toward the 200-day EMA at 140.24.

- EUR buyers reclaiming 142.00 would set the stage to challenge the 100-day EMA.

The EUR/JPY gained some traction during the Wednesday session and reached a new two-week high at 142.85 before reversing its course and closed at 142.39. As Thursday’s Asian Pacific session begins, the EUR/JPY continues the late downtrend, registering decent losses of 0.14%, and trades at 142.12 at the time of writing.

EUR/JPY Price Analysis: Technical outlook

After piercing the EUR/JPY 50-day Exponential Moving Average (EMA) at 142.50, and the 100-day at 142.21, the cross-currency reversed its course, snapping four days of straight gains. Nevertheless, to resume its downtrend in the short-term, the EUR/JPY needs to clear the 20-day EMA at 141.65, which, once surpassed, the pair could fall towards the 141.00 mark, ahead of the 200-day EMA at 140.24.

The previously-mentioned scenario is backed by oscillators, with the Relative Strength Index (RSI), although at bullish territory, its slope is downwards, about to cross under the 50-midline. In contrast, the Rate of Change (RoC) portrays upside volatility as higher. Therefore, EUR/JPY traders might refrain from opening fresh EUR short positions until the RoC shifts bearish.

As an alternative scenario, if the EUR/JPY resumes its uptrend, key resistance levels are the 100-day EMA at 142.21, followed by the 50-day EMA at 142.50, and then the 143.00 mark.

EUR/JPY Key Technical Levels

-

23:36

Silver Price Analysis: 200-SMA, monthly support line defends XAG/USD bulls above $23.00

- Silver price picks up bids to snap three-day uptrend.

- RSI, MACD conditions also favor the rebound from the key support line, 200-SMA, suggesting further advances.

- Three-week-old horizontal support zone appears crucial for bulls.

Silver price (XAG/USD) licks its wounds around $23.40 amid early Thursday in Asia, printing the first daily gains in four as of late.

In doing so, the bright metal bounces off a one-month-long ascending trend line, as well as the 200-SMA.

The commodity’s recovery moves also take clues from the above 40.0 RSI (14), as well as recently improving MACD signals.

As a result, the XAG/USD is likely to extend the latest recovery moves toward the $22.00 round figure.

However, a horizontal area comprising multiple levels marked since December 21, near $24.30, could challenge the quote’s further upside.

It should be observed that the monthly high near $24.55 could act as the last defense of the XAG/USD bears past $24.30, a break of which won’t hesitate to direct Silver price towards the April 2022 high near $26.25.

On the contrary, the aforementioned support line and the 200-SMA restrict the immediate downside of the Silver price near $23.30 and $23.20 in that order.

Following that, the monthly low of $23.10 and the mid-December trough surrounding $22.55 will be in focus.

Overall, the Silver price is likely to remain firmer but the road toward the north is long and bumpy.

Silver price: Four-hour chart

Trend: Further upside expected

-

23:17

BoJ to review side effects of its massive monetary easing at its policy meetings next week – Yomiuri

Japanese media Yomiuri came out with the news suggesting another hawkish move by the Bank of Japan (BoJ) during its next week’s monetary policy meeting. The news signaled that the Japanese central bank is up for reviewing the side effects of massive monetary easing in the monetary policy meeting next week.

“BoJ reviews due to skewed interest rates in markets even after last month's tweak in bond yield control policy,” adds Yomiuri per Reuters.

USD/JPY slides

Following the news, the USD/JPY pair dropped around 50 pips to 131.90, close to 132.10 by the press time.

Also read: USD/JPY bulls eye a break of key daily resistance with US CPI eyed

-

23:14

USD/CHF Price Analysis: 0.9400 looks into the picture after a firmer recovery

- USD/CHF has turned sideways after a firmer recovery move from around 0.9200.

- A follow-up buying after a Double Bottom formation indicates the strength of the US Dollar.

- The RSI (14) has comfortably shifted into the bullish range of 60.00-80.00, which indicates more upside ahead.

The USD/CHF pair has picked strength after a minor correction to near 0.9300 in the Asian session. The Swiss franc asset faced barricades near 0.9325 in an attempt to extend its upside journey. On Wednesday, the major displayed a responsive buying action after dropping to near 0.9204.

The major could remain inside the woods ahead of the release of the United States inflation data. Meanwhile, the risk appetite of investors is significantly improved as S&P500 has displayed back-to-back bullish trading sessions despite anxiety ahead of the release of the US Consumer Price Index (CPI) data. The US Dollar Index (DXY) is hovering around 103.00.

On an hourly scale, USD/CHF witnessed a sharp bullish reversal after forming a Double Bottom chart pattern near the round-level support of 0.9200. After sensing weak selling interest near the aforementioned support, bulls made a comeback and pushed the asset higher vigorously.

The 20-and 50-period Exponential Moving Averages (EMAs) at 0.9283 and 0.9260 are upward-sloping now, which adds to the upside filters.

Meanwhile, the Relative Strength Index (RSI) (14) has comfortably shifted into the bullish range of 60.00-80.00 from the 40.00-60.00 range, which indicates that the bullish momentum has been triggered.

Going forward, a break above Wednesday’s high at 0.9332 will drive the asset towards December 12 high at 0.9367 followed by the round-level resistance at 0.9400.

Alternatively, a slippage below Monday’s low at 0.9167 will result in a fresh downside journey toward the March low at 0.9150. A downside move below the March low will expose the asset to January 17 low at 0.9117.

USD/CHF hourly chart

-638090755921242397.png)

-

23:07

GBP/USD looks to regain 1.2200 amid downbeat expectations from US inflation

- GBP/USD picks up bids to snap two-day downtrend.

- Fears from UK’s public sector workers’ strike challenge bulls despite broadly softer US Dollar.

- Dovish Fedspeak, market’s optimism adds strength to Cable’s recovery moves.

- US CPI for December will be crucial for near-term directions, softer print could add to weekly gains.

GBP/USD buyers flex muscles around the mid-1.2100s, following the downbeat performance in the last two days, as markets await the key US Consumer Price Index (CPI) for December during early Thursday. In doing so, the Cable pair remains well-set for the biggest weekly gains since late November.

The quote’s latest weakness could be linked to the likely increase in the UK’s economic hardships due to the fears emanating from the strikes of the British public sector workers. To solve the same, UK Prime Minister Rishi Sunak eased his front to come to a mid-point but the situation didn’t improve and the unions are warning over a much bigger protest starting from February 01. “Britain's Public and Commercial Services (PCS) union said on Wednesday 100,000 of its members across 124 government departments would take strike action on Feb. 1 in a dispute over pay, pensions and job security,” reported Reuters.

Elsewhere, the market’s cautious optimism amid the risk-positive headlines surrounding China, as well as receding fears of hawkish Fed actions seemed to have kept the GBP/USD buyers hopeful.

Recently, Federal Reserve’s Boston President Susan Collins backed the smaller rate increases while stating that she leans at this stage to a 25 bps hike. However, she also mentioned that it is very data-dependent.

On other hand, China’s total reopening and early signals of heavy holiday shopping join the chatters that the People’s Bank of China (PBOC) will adhere to rate cuts in 2023 to spread the Beijing-inspired optimism.

It should be noted that the firmer prints of equities and downbeat US Treasury yields also restricted GBP/USD downside despite not-so-positive headlines from the UK. That said, the US 10-year Treasury yields dropped nearly eight basis points (bps) 3.54% while Wall Street closed in the green.

Looking forward, GBP/USD traders are likely to witness further recovery moves amid downbeat expectations from the US CPI data, expected 6.5% YoY versus 7.1% prior. Considering this, analysts at Australia and New Zealand Banking Group (ANZ) said, “Current price action indicates that the market wants and is expecting a fairly benign data print. The consensus is that core CPI rose 0.3% m/m; we are forecasting 0.4% m/m.”

Technical analysis

Wednesday’s Dragonfly Doji and the GBP/USD pair’s ability to remain firmer past 21-DMA, around 1.2085 by the press time, keeps buyers hopeful.

-

22:41

NZD/USD Price Analysis: Fades bounce off 200-SMA below 0.6390 resistance confluence

- NZD/USD struggles to defend weekly gains despite keeping recent technical breakouts.

- Convergence of weekly resistance line, 61.8% Fibonacci retracement level guards immediate upside amid bearish MACD signals.

- Sustained trading beyond 200-SMA, previous resistance line from early December keeps buyers hopeful.

NZD/USD retreats to 0.6370 as bulls take a breather ahead of the key inflation data from China and the US on early Thursday.

In doing so, the Kiwi pair fades the previous day’s bounce off the 200-Simple Moving Average (SMA). Also adding strength to the pullback moves could be the bearish MACD signals.

Even so, the NZD/USD buyers defend Friday’s upside break of the one-month-old descending resistance line, now support, as well as the 200-SMA. On the same line is the firmer RSI (14) line, not overbought.

Hence, the NZD/USD price is likely to struggle despite keeping the latest bullish signals.

That said, a convergence of the weekly descending trend line joins the 61.8% Fibonacci retracement level of the pair’s December-January downturn, around 0.6390, appears a tough nut to crack for the NZD/USD bulls.

Following that, the monthly high around 0.6415 appears additional upside filter for the quote to cross to justify the traders’ bullish bias.

In a case where the NZD/USD remains firmer past 0.6415, the odds of witnessing a run-up toward the previous monthly peak of 0.6514 can’t be ruled out.

Meanwhile, the 200-SMA and the aforementioned resistance-turned-support line, close to 0.6335 and 0.6295 in that order, restrict the short-term downside of the NZD/USD pair.

If the Kiwi pair sellers keep the reins past 0.6295, the recent hopes of witnessing a north-run take a backseat as prices could challenge the monthly low of 0.6190.

NZD/USD: Four-hour chart

Trend: Pullback expected

-

22:39

AUD/JPY aims to re-test 92.00 as focus shifts to China's Inflation

- AUD/JPY is expected to re-test 92.00 but is inside the woods following cues from AUD/USD.

- Investors are awaiting China’s inflation data for fresh impetus.

- It seems that few days of sunlight left for the ultra-loose monetary policy approach in Japan.

The AUD/JPY pair is struggling to come out of the woods as investors are awaiting the release of China’s Consumer Price Index (CPI) data for fresh impetus. The risk barometer has shifted sideways around 91.50, following footprints of AUD/USD ahead of the release of the United States inflation data.

According to the estimates, annual CPI (Dec) is set to improve to 1.8% from the former release of 1.6%. While the monthly figure may contract by 0.1% against the prior release of -0.2%. Also, the Producer Price Index (PPI) could contract by 0.1%. The Chinese economy is operating at lower inflation levels after remaining locked for a lengthy period due to the Covid-19 epidemic. This might force the People’s Bank of China (PBOC) to announce some policy-easing measures to spurt the level of economic activities.

On Wednesday, the cross turned sideways after a bullish action supported by the release of the higher-than-projected Australian inflation and upbeat Retail Sales data. The monthly price index (Nov) in the Australian economy landed at 7.4% vs. the consensus of 7.3% and the former release of 6.9%. Apart from that, monthly Retail Sales (Nov) jumped to 1.4% against the projections of 0.6%.

Stronger-than-anticipated inflation and retail demand by households are going to compel the Reserve Bank of Australia (RBA) to continue hiking interest rates further to tame soaring inflation. Currently, the Official Cash Rate (OCR) of the RBA is at 3.10%.

On the Tokyo front, Michio Saito, Director-General of the Financial Bureau at Japan’s Ministry of Finance (MoF), said in a statement early Wednesday, “interest rates remain low but the current situation won't last indefinitely.” Japanese administration and the Bank of Japan (BoJ) are looking to review their decade-long ultra-loose monetary policy to conclude deflation and an easy policy approach.

-

22:17

AUD/USD dribbles around 0.6900 as traders await Aussie Trade Balance, China Inflation

- AUD/USD awaits fresh clues to extend recent gains, eyes fourth weekly upside.

- Dovish Fed talks, upbeat Aussie data allowed bulls to keep the reins.

- Wait for inflation data from China, US joined light calendar elsewhere to restrict moves.

- Markets anticipate mixed data but improvement in China CPI could favor bulls.

AUD/USD portrays pre-data anxiety as it struggles to extend the previous day’s run-up, taking rounds to 0.6900 during the initial hours of Thursday’s Asian session. Even so, the Aussie pair stays on the way to post four consecutive weekly gains while staying around the highest levels since late August 2022.

The quote’s latest gains could be linked to the market’s cautious optimism amid the risk-positive headlines surrounding China, as well as receding fears of hawkish Fed actions. Adding strength to the AUD/USD upside could be the recently firmer data from Australia.

That said, Australia’s seasonally adjusted Retail Sales grew 1.4% MoM versus 0.6% expected and -0.2% prior while the Monthly Consumer Price Index rose 7.4% compared to -5.7% market forecasts and -3.9% previous readings.

Elsewhere, Federal Reserve’s Boston representative Susan Collins reiterated her support for the smaller rate increases. The policymaker said that she leans at this stage to a 25 bps hike. However, she also mentioned that it is very data-dependent.

Talking about China, the dragon nation’s total reopening and early signals of heavy holiday shopping join the chatters that the People’s Bank of China (PBOC) will adhere to rate cuts in 2023 to spread the Beijing-inspired optimism. On the same line, the recent improvement in the Sino-Aussie ties also helps AUD/USD to remain firmer.

It should be observed that the easing of the US Treasury bond yields and an upbeat performance by equities also added strength to the AUD/USD upside, due to the pair’s risk-barometer status.

On Wednesday, the US 10-year Treasury yields dropped nearly eight basis points (bps) 3.54% while Wall Street closed in the green.

Moving on, Australian trade numbers for November will precede China’s inflation data for December to direct immediate AUD/USD moves. Given the likely easing in the Aussie Trade Balance to 10,500M versus 12,217M prior, the quote may witness a pullback in the initial hours before the expectedly firmer China Consumer Price Index (CPI) and Producer Price Index (PPI) figures could favor the bulls. Above all, US CPI will be crucial as the Fed hawks run out of steam.

Technical analysis

AUD/USD grinds higher between a two-month-old resistance line and the 200-DMA, respectively near 0.6960 and 0.6830.

-

22:13

USD/CAD Price Analysis: Subdued around 1.3420s as a doji emerges

- USD/CAD extends its losses after sliding below a five-month-old support trendline that surpasses 1.3500.

- USD/CAD Price Analysis: A breach below 1.3357 could pave the way for further downside; otherwise, a test of 1.3500 is on the cards

USD/CAD reverses its uptrend and drops below the 100-day Exponential Moving Average (EMA) at 1.3427, set to finish Wednesday’s session with losses of almost 0.01%. At the time of writing, the USD/CAD is trading at 1.3423 after hitting a daily high of 1.3445.

USD/CAD Price Analysis: Technical outlook

From a daily chart perspective, the USD/CAD is still neutral-biased, though slightly skewed to the downside. Once USD/CAD’s price action broke below a five-month-old upslope support trendline drawn from August 2022 lows on January 6, the USD/CAD resumed its downtrend, which stalled around the current week’s low of 1.3357.

To extend its downtrend, the USD/CAD needs to break below 1.3357 to extend its losses to the November 24 daily low of 1.3316, ahead of the 1.3300 mark. Once hurdled, the USD/CAD would be poised to test the 200-day EMA at 1.3238.

The USD/CAD downward bias in the near term is supported by the Relative Strength Index (RSI) in bearish territory, while the Rate of Change (RoC) portrays steady downward volatility, meaning that sellers remain in charge.

USD/CAD Key Technical Levels

-

22:12

Gold Price Forecast: XAU/USD bearish head and shoulders in play, eyes on $1,850

- Gold Price is steady ahead of crucial United States of America Consumer Price Index (CPI) inflation data due Thursday.

- US Dollar pressured vs. risk markets that performed well ahead of the December CPI report.

- Gold price has dropped below key structure following the test of equal highs and is now printing prospects of a bearish head and shoulders.

Gold price was capped at the highest in more than eight months on Wednesday, while investors anticipate the United States of America Consumer Price Index (CPI) inflation data due Thursday. At the time of writing, Gold price is flat on the day at $1,876 but it had travelled between a low of $1,867.22 and reached a high of $1,886.69.

US Consumer Price Index is key for Gold price

The moves come ahead of the December inflation report, which is expected to show US prices rose by an annualized 6.5%. This is lower than November's 7.1% pace. Investors are monitoring the Consumer Price Index closely as the expectations are that if it were to continue to decelerate, so too will the Federal Reserve's pace of rate hikes.

In this regard, analysts at TD Securities explained that they are looking for the core Consumer Price Index to have edged higher on a monthly basis in December, ''closing out the year on a relatively stronger footing,'' they said.

''Indeed, we forecast a firm 0.3% MoM increase, as services inflation likely gained momentum. In terms of the headline, we expect the Consumer Price Index inflation to register a slight decline on an unrounded basis in December, but rounded up to flat MoM, as energy prices offered large relief again. Our MoM projections imply that headline and core CPI inflation likely lost speed on a YoY basis in December.''

US Dollar could depend on US CPI

As for the US Dollar, the analysts said, ''unless the core measure significantly surprises to the upside, US Dollar rallies should be sold into. We think the bar is high to compel a reversal of fortune despite the US Dollar tactically stretched.''

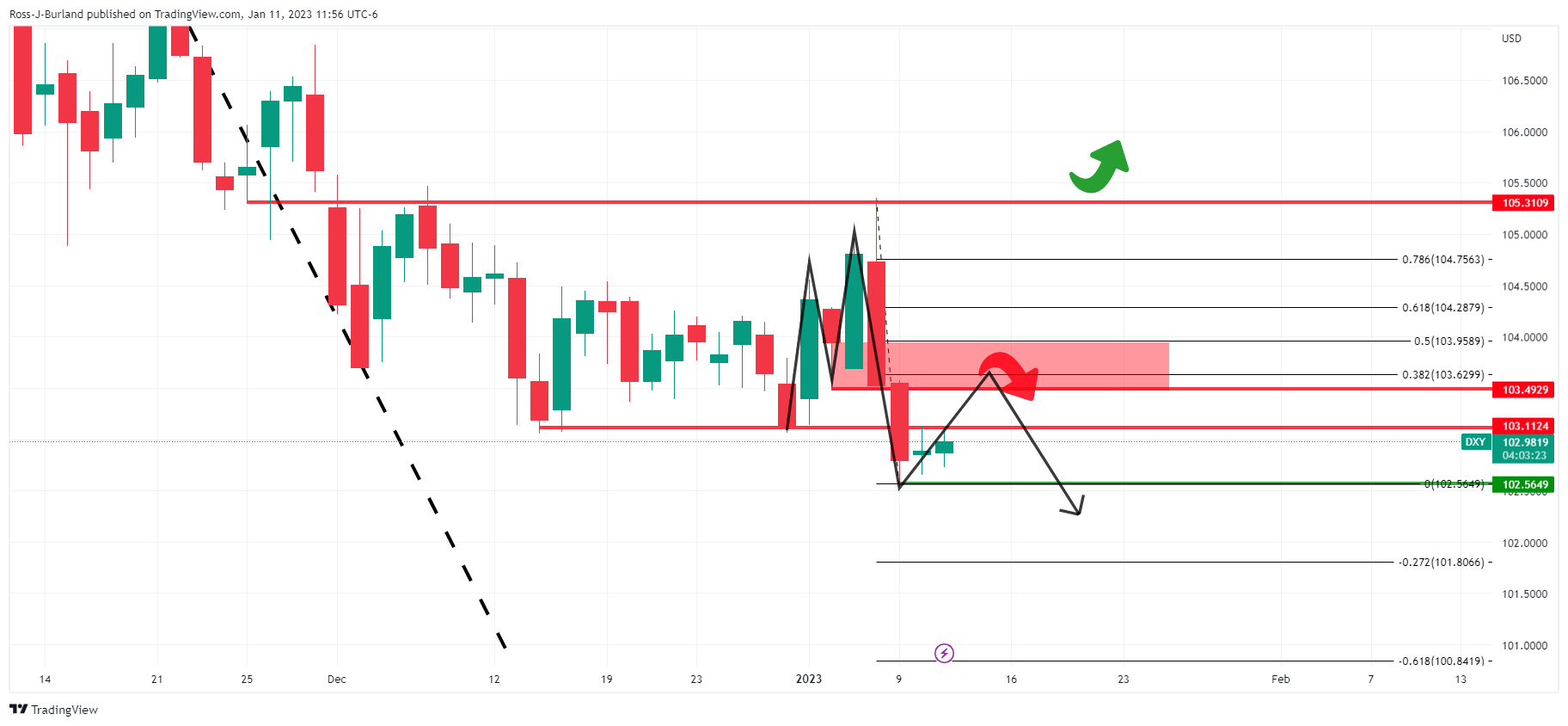

Meanwhile, the DXY index, which measures the US Dollar vs. a basket of currencies, is trading flat near 103.24 after meeting a new cycle low Monday near 102.944. The next target to the downside is the May low near 101.297. However, the US Dollar is poised for a bullish continuation technically speaking where an M-formation is in play:

The M-formation on the US dollar chart is a reversion pattern and the price would be expected to move in for the restest of the resistance structures and neckline of the pattern between 103.50 and 104.00. Such a move in the US Dollar would align with a 38.2% Fibonacci retracement and a 50% mean reversion at the extreme, a major weight for Gold price.

China has been on the bid, supporting Gold price higher

Analysts at TD Securities argued that ''the strength in Gold price is inconsistent with the bearish macro backdrop, as highlighted by its diverging relationship with real rates.''

The analysts explained that ''under the hood, relentless buying from China has fueled a squeeze on CTA trend follower positioning over the past months, and has yet to show signs of abating.'' The analysts said ''mysterious large-scale Chinese purchases of gold have single-handedly catalyzed a $150/oz rally.''

''Our tracking of positioning for the top ten traders in China highlights a continued accumulation of gold, with this cohort adding another 2.4 tonnes of notional gold to their net length overnight,'' the analysts at TD Securities added.

''CTA trend followers could still exacerbate upside flows with a break north of the $1,900/oz mark likely to spark a sizeable buying program equivalent to nearly +8% of algos' maximum historical position size,'' the analysts explained.

Gold price technical analysis

However, Gold price has started to show signs that its four-day bullish impulse is starting to decelerate given Wednesday's doji:

The following technical analysis of the Gold price arrives at a bearish conclusion, at least for the near term:

In the prior day's analysis, it was explained that on the daily Gold price chart, we could see prior equal highs finally being tested and ''swept'' as follows:

The phenomenon occurs on a fractal basis whereby the equal levels are ''swept'' only to fuel a reversal in the Gold price. We are still in this process and the Gold price moved in on liquidity in the $1,886s on Wednesday. This was an area of expected resistance highlighted the prior day on the 4-hour chart:

Gold price, H4 chart update

As per the prior analysis, the Gold price has indeed dropped below the structure following the test of the equal highs. The Gold price is now printing prospects of a bearish head and shoulders pattern as potential peak formation into the US consumer Price Index. Gold price bears will need to break the $1,870 structure that ultimately guards the target area some $20/oz below to test the $1,850s.

-

22:07

EUR/USD shows sheer volatility contraction around 1.0750 ahead of US Inflation

- EUR/USD is demonstrating volatility contraction as the focus has shifted to the US inflation data.

- A consecutive bullish session reported by S&P500 indicates that the risk profile is extremely solid.

- Improved risk appetite has weighed down the 10-year US Treasury yields to 3.54%.

The EUR/USD pair is displaying back-and-forth moves around 1.0750 in the early Tokyo session. The major currency major is showing extreme volatility contraction, which indicates that investors are not ready to build fresh positions before the release of the United States inflation data.

The risk profile seems extremely solid as S&P500 has recorded two consecutive bullish trading sessions. It seems that investors are optimistic on CY2023. Also, the demand for US government bonds remained upbeat, which led to a significant fall in the 10-year US Treasury yields to 3.54%. The US Dollar Index (DXY) continued its sideways profile around 103.00 ahead of the US Consumer Price Index (CPI) data.

This time, the inflation data is getting pivotal for the market participants as wage inflation has shown meaningful signs of deceleration, which Federal Reserve (Fed) policymakers were considering a major threat to the agenda of achieving price stability.

The headline CPI (Dec) is expected to continue its declining spree and may drop to 6.5% from the former figure of 7.1%. While the core CPI that excludes oil and food prices might slip to 5.7% from 6.0% reported earlier. Weaker retail demand, a spree of declining employment additions in the United States economy, a slowdown in economic activities, and now a fall in employment bills have collectively resulted in lower consensus for inflation projections.

On the Eurozone front, after European Central Bank (ECB)'s governing council member Mario Centeno, another ECB member and French central bank governor Francois Villeroy de Galhau said on Wednesday, the central bank should aim to reach the terminal rate by the summer. He further added that ECB needs to be pragmatic about the pace of rate hikes.

-

21:45

New Zealand Building Permits s.a. (MoM) registered at 7% above expectations (-0.1%) in November

-

20:41

GBP/USD Price Analysis: 1.2100 under pressure ahead of key US CPI event

- GBP/USD's 1.2170, 1.2150 and 1.2113 (daily W-formation neckline target area) areas were in focus.

- Meanwhile, key structure target levels have either given out or are being tested, guarding against a full-on capitulation of the bulls.

As per the start of the week's technical analysis for GBP/USD, GBP/USD Price Analysis: Bullish impulse is decelerating, eyes on 1.2150, where the outlook has been bearish while below 1.2400 and 1.2220 nearer-term highs, cable has remained hamstrung to the downside as the following illustrates. Meanwhile, the US Consumer Price Index could be the catalyst to trigger a move below 1.2100 recent lows.

GBP/USD prior analysis

The market was on the back side of the recent supportive trendline at the start of the week and the price broke 1.1900 structure leaving a bearish bias on the charts.

Zoomed in...

The W-formation was supportive of the bearish thesis given that it is a reversion pattern. It was stated that GBP/USD would be expected to move in towards the neckline and day's lows of near 1.2080. So far, we have seen the price dishevelled to test 1.21 the figure and test the structure that guards against a run to the prior broken lows of 1.1900 and 1.1778 below there.

It was stated that the lower time frames can be monitored for a deceleration of the bullish run and signs of distribution as follows:

1.2170, 1.2150 and 1.2113 (daily W-formation neckline target area) areas were meanwhile key structure target levels that have either given out or are being tested, guarding against a full-on capitulation of the bulls and bears taking over towards the 1.1900 target area.

GBP/USD update, daily and H1 charts

-

20:05

ECB's De Cos: Rates to continuing going up 'significantly'

Noting that fiscal policy risk is adding to inflation pressure, European Central Bank policymaker Pablo Hernandez de Cos said on Wednesday that the ECB will continue to raise interest rates significantly at future meetings at a steady pace.

"Keeping interest rates at tight levels will reduce inflation by dampening demand and will also protect against the risk of a persistent upward shift in inflation expectations," De Cos told a financial event in the evening.

EUR/USD update

EUR/USD rose to a seven-month high on Wednesday but is now treading water into the US Consumer Price Index event on Thursday which traders hope to get some clarification of where interest rates are headed. At its highest level since May 31, EUR/USD reached 1.0776 on Wednesday, moving up from a low of 1.0725.

-

19:59

NZD/USD hovers around 0.6360s in choppy trading, eyeing US CPI

- The New Zealand Dollar failed to gain traction despite a risk-on impulse.

- US Dollar remains soft amidst growing speculations for a soft US CPI print.

- China’s reopening could bolster the NZD outlook in the near term.

The NZD/USD prints successive series of doji’s, suggesting that neither buyers nor sellers are in charge, ahead of Thursday’s US Consumer Price Index (CPI) release. Hence, the NZD/USD is trading at 0.6374 above its opening price after hitting a daily high of 0.6388.

Wall Street is set to finish the session with solid gains between 0.56% and 1.24%. The NZD/USD remains in choppy trading as investors brace for the release of crucial US economic data. The consensus estimates that headline inflation in the US, known as the Consumer Price Index (CPI), would drop to 0% MoM, while year-over-year data is expected to decelerate from 7.1% to 6.5%. Excluding volatile items inflation, the so-called core CPI is forecasted to rise 0.3% MoM, while the consensus for annual-based core inflation is 5.7%.

Even though the World Bank’s tweaked its global growth forecasts to the downside, the New Zealand Dollar (NZD) remains linked to China’s economy. China’s reopening could trigger another leg-up in commodities. However, according to ANZ Bank, “tighter global monetary policy in the second half of the year” could help curb commodity inflation.

In the meantime, the US Dollar Index, a gauge of the buck’s value vs. its peers, continues to weaken, down by 0.05%, though it remains hovering around the 103.200 area.

Therefore, the NZD/USD might continue to trade sideways as traders get ready for US economic data releases. However, the New Zealand (NZ) docket will unveil Building Permits for December.

NZD/USD Key Technical Levels

-

19:40

Forex Today: Waiting about to end, does not look good for the US Dollar

What you need to take care of on Thursday, January 12:

Market players held their breath for a second consecutive day, with major pairs holding on to familiar levels. Tensions mounted ahead of the release of the December US Consumer Price Index (CPI), with the focus on central banks’ officials.

European Central Bank (ECB) officials were mostly hawkish, underpinning the EUR. French central bank governor Francois Villeroy de Galhau said the ECB should aim to reach the terminal rate by the summer, confirming they would have to raise rates further in the coming months. Governor of Austria's central bank Robert Holzmann opted for a more aggressive stance, noting that "rates will have to rise significantly further to reach levels that are sufficiently restrictive to ensure a timely return of inflation to target." He finally added that it's too early to discuss a possible terminal rate. Finally, ECB’s Governing Council member Olli Rehn said that rates in the Euro Zone will still have to rise significantly in the next couple of meetings and reach restrictive levels to dampen inflation.

Across the pond, US Federal Reserve’s Boston representative Susan Collins supported smaller rate hikes. Collins said that she thinks 25 bps or 50bps would be reasonable, adding she leans at this stage to a 25 bps hike, but clarifying it is very data-dependent.

The Kremlin restated that President Vladimir Putin is open to talks on Ukraine, although adding that an arrangement should be on Russian terms. A peaceful solution to the conflict remains far away.

EUR/USD keeps hovering around 1.0750, unchanged for a second consecutive day, while GBP/USD settled around 1.2140. The AUD/USD pair started the day on the back foot, but trimmed losses and posted a modest advance, trading just above the 0.6900 level. The USD/CAD pair hovers around 1.3420, while USD/JPY stands at 132.40.

Gold hit a fresh eight-month high of $1,886.63 a troy ounce, but retreated ahead of Wall Street’s opening, ending the day with modest gains at around $1,877.00.

Crude oil prices rallied, helped by a report from the US Energy Information Administration (EIA) as the organism expects global consumption of liquid fuels such as gasoline, diesel, and jet fuel, to set new record highs in 2024. The headline overshadowed a large build in US stockpiles.

Attention on Thursday will be on the United States Consumer Price Index, foreseen up by 6.5% YoY in December. The core reading is seen up by 5.7%, easing from the previous 6%.

BTC Trading Plan: Wait for the fireworks on Thursday and plan for $19,000

Like this article? Help us with some feedback by answering this survey:

Rate this content -

19:35

USD/JPY bulls eye a break of key daily resistance with US CPI eyed

- USD/JPY traders await the US CPI data for the next major scheduled catalyst.

- The price is coiled and an inverse daily head and shoulders could be in the making.

USD/JPY is attempting to move higher during a light schedule in the North American session but has run into offers as US stocks climb to fresh highs for the week. at the time of writing, USD/JPY is trading back to flat for the day at 132.35 but has travelled between a low of 132.06 and 132.87 the high for Tuesday and the week so far.

Wall Street's main indexes are bid as investors keenly await the US consumer price index which seems to have weighed on the US Dollar and US Treasury yields in the recent hours of the session. The 10-year yield is now down by 1.66% and meeting an hourly support structure near 3.563%. If this were to hold, this would offer the greenback some support also and fend off the USD/JPY bears leaving the cross to tread water into the CPI data on Thursday where traders expect to get more clarity on the Federal Reserve's rate hike trajectory.

In this regard, analysts at TD Securities explained that they are looking for core prices to have edged higher on a monthly basis in December, ''closing out the year on a relatively stronger footing,'' they said.

''Indeed, we forecast a firm 0.3% MoM increase, as services inflation likely gained momentum. In terms of the headline, we expect CPI inflation to register a slight decline on an unrounded basis in December, but rounded up to flat MoM, as energy prices offered large relief again. Our MoM projections imply that headline and core CPI inflation likely lost speed on a YoY basis in December.''

As for the US Dollar, the analysts said ''Unless the core measure significantly surprises to the upside, USD rallies should be sold into. We think the bar is high to compel a reversal of fortune despite the USD tactically stretched.''

USD/JPY technical analysis

As per the prior analysis, USD/JPY Price Analysis: Consolidation into US CPI, bulls on the prowl, the price is coiled and an inverse daily head and shoulders could be in the making:

Such an outcome would take out the daily resistance and tie in with the bullish outlook for DXY as follows, where an M-formation is in play:

The M-formation is a reversion pattern and the price would be expected to move in for the restest of the resistance structures and neckline of the pattern between 103.50 and 104.00. Such a move would align with a 38.2% Fibonacci retracement and a 50% mean reversion at the extreme.

-

19:10

WTI climbs above $77.00 on risk appetite improvement

- WTI rallied more than 3% due to increased optimism on China’s re-opening.

- An increase in US stockpiles was not an excuse for WTI to continue to advance.

- WTI Price Analysis: If it reclaims $78.00, it will exacerbate a rally to $80.00.

Western Texas Intermediate (WTI), the US crude oil benchmark, rises more than 3% Wednesday, breaking above the 20-day Exponential Moving Average (EMA) at $76.55 after erasing Tuesday’s losses. A risk-on impulse, a softer US Dollar (USD), and a jump in US oil inventories are tailwinds for the black gold. At the time of writing, WTI exchanges hand at $77.30.

Traders’ mood remains optimistic, as shown by global equities rising. Estimations that December’s CPI is expected to show annual inflation cooling down to 6.5%, from 7.1% in November, maintained flows ebbing toward risk-perceived assets.

Soft inflation reading in the US would be US Dollar negative, which could boost oil’s demand as the dollar-denominated commodity would be cheaper for buyers holding other currencies.

The US Federal Reserve is expected to raise rates by 25 bps at the February meeting and again in March after a 50 basis point hike in December.

Sources quoted by Reuters said, “China could bounce back strongly, especially if backed by monetary and fiscal stimulus. Central banks may discover they have room to cut rates if inflation falls substantially and economies are in a recession.”

Oil prices rose as hopes for an improved global economic outlook and concern over the impact of sanctions on Russian crude output outweighed a higher-than-expected build in US crude and fuel stocks.

The US Energy Information Administration (EIA) reported that crude inventories rose by 19.0 M barrels last week, the third largest weekly gain ever and the most since stocks rose by a record 21.6 million barrels in February 2021.

WTI Price Analysis: Technical outlook

From a technical perspective, WTI is still neutral-to-downward biased, which, if it continued to rise further, would clash with the confluence of the 50-day EMA and a three-month-old downslope resistance trendline around $79.09. Oscillators like the Relative Strength Index (RSI) suggest that buyers are gathering momentum, but the Rate of Change (RoC), suggests the advance could be gradual as volatility levels remain depressed.

If WTI reclaims $78.00, that could open the door toward the abovementioned confluence of technical indicators, which, once cleared, will exacerbate a WTI’s rally to $80.00 per barrel. On the other hand, failure at $78.00 could keep prices lower, and open the door for sellers, to reclaim the 20-day EMA at $76.56.

-

18:15

Fed's Collins backs a slowdown on rate hikes, but is data dependent

The New York Times reported that the Boston Federal Reserve's Susan Collins backs a slowdown in rate increases.

Collins was reported saying that she was leaning toward a quarter-point move at the central bank’s February 1 meeting.

More to come...

-

18:13

United States 10-Year Note Auction fell from previous 3.625% to 3.575%

-

18:12

Gold Price Forecast: XAU/USD erases earlier gains, falls to $1870s as traders brace for US CPI

- Gold traders bracing for December’s US CPI data weighed on the yellow metal prices.

- The US Dollar rises, contrarily to US Treasury bond yields, dropping.

- Gold Price Analysis: Could test $1900 once it clears $188; otherwise, it could test $1860.

Gold’s rally stalled around $1887 after hitting an eight-month new high, though it erased some of those gains, turning negative on Wednesday amidst an upbeat market sentiment. Speculations that softer-than-estimated US inflation report Thursday could spur a Fed pivot increased. However, the greenback is recovering, a headwind for XAU/USD prices. At the time of writing, the XAU/USD is trading at $1873.68.

Gold Price falls despite risk-on mood, falling yields

US equities continue to advance in the mid-New York session, portraying investors’ mood. The XAU/USD is perceived as traders booked profits ahead of December’s US inflation report. Data is estimated to show the Consumer Price Index (CPI) on a monthly basis, dropping to 0%, while year-over-year data is expected to fall from 7.1% to 6.5%. Excluding volatile items inflation, the so-called core CPI is forecasted to rise 0.3% MoM, while the consensus for annual-based core inflation is 5.7%.

In the meantime, the US Dollar Index, a gauge of the greenback’s value against a basket of six currencies, is erasing earlier losses at 103.371, slightly up by 0.09%. Contrarily, US Treasury bond yields are falling four bps, down to 3.583%. Even though US bond yields extended their losses, XAU/USD continues to edge lower.

On the US monetary policy side, traders’ expectations for a Fed rate hike of 25 bps lie at a 77% chance, as shown by money market futures, while for a 50 bps increase is 23%. Money markets expect the Federal Funds rate (FFR) to peak at around 4.92% in June 2023.

Gold Price Analysis: Technical outlook

After peaking around $1887, XAGU/USD is almost flat. However, a daily close at around the $1876 area, Wednesday’s opening price, could exacerbate a fall toward the current week’s lows of $1865.40. Nevertheless, oscillators like the Relative Strength Index (RSI) and the Rate of Change (RoC) remain in bullish territory and continue to support higher prices, though a consolidation around $1875 ahead of the release of critical US data is on the cards.

XAU/USD will extend its gains towards $1900 if it breaks $1887. On the other hand, a fall beneath $1865.40 could pave the way toward the 20-day EMA at $1830.

-

18:10

AUD/USD Price Analysis: Distribution could be playing out into US CPI critical event

- While below 0.6950, the bias for AUD/USD is to the downside for the near term.

- A break of 0.6870 will open the risk of a move into the 0.6800 figure and the targetted area between 0.6791 and 0.6748.

- US Dollar is also poised for a move higher as per the daily M-formation.

Despite hot domestic economic data that reinforced the case for further increases in interest rates from the Reserve Bank of Australia, AUD/USD has failed to hold onto the knee-jerk gains. At the time of writing, AUD/USD is treading water at 0.69 the figure. The pair has moved between a range of 0.6872 and 0.6925 (highs reached ahead of Frankfurt open, fuelled by data).

As per the prior analysis, AUD/USD Price Analysis: Bears move in on key 0.6905 support structure, higher time frame traders were triggered into the market on the break of the prior week's and month's highs near 0.6890. While some temporary gains were made on a run to 0.6950 (offered) highs, in-the-money longs have been squeezed back to 0.6859 over the course of the week as the US Dollar perked up and recovered from the lowest levels since the summer of 2022 as per the DXY index.

Both the DXY and AUD/USD are coiled markets, treading water into the US Consumer Price Index on Thursday. Therefore, a breakout could be imminent. We have some red news on the calendar for the Aussie ahead of the event, but so long as the US Dollar remains firm, this might do little to steer the bears away from targeting the stubborn longs towards 0.6850 that guards volumes between 0.6790 and 0.6750.

DXY technical analysis

Looking at the DXY index chart, we have a compelling bullish technical outlook that has taken shape as follows:

The hourly chart shows the price in a coil and in the absence of bearish commitments below the initial balance lows, then the bias is to the upside on a strong close above last month's lows. Liquidity above the equal highs opens prospects of mitigation of the price imbalance between 104.05 and 104.90s.

Looking at the daily chart, an upside bias, for the meanwhile, could also be argued, at least for a test of the 103.50s:

The US Dollar's decline is decelerating after moving to the backside of the bearish trendline and stalling at recent lows of 102.56. However, while below 105.31, the dominant bias is bearish. With that being said, and in accordance with the short-term bearish bias for the Aussie, zooming in on the DXY daily chart, an M-formation is in play:

The M-formation is a reversion pattern and the price would be expected to move in for the restest of the resistance structures and neckline of the pattern between 103.50 and 104.00. Such a move would align with a 38.2% Fibonacci retracement and a 50% mean reversion at the extreme. Beyond there, then the mitigation of the price imbalance opens the risk of a test of 105 the figure.

AUD/USD technical analysis

Coming back to the Aussie, a move higher in the greenback would cement the bearish themes for a run towards 0.6750:

While below 0.6950, the bias is to the downside for the near term. That is not to say that the price will automatically fall, and again, there is plenty of red news on tap that could go either way. However, a break of 0.6870 will open the risk of a move into the 0.6800 figure and the targetted area between 0.6791 and 0.6748.

-

16:24

Silver Price Analysis: XAG/USD rejected from $24.00, looks at $23.00

- XAG/USD is under pressure after breaking short-term support levels during the American session.

- The metal is under pressure, approaching the $23.00 level.

- US Dollar mixed as equity prices rises modestly.

Silver is under pressure during Wednesday’s American session, trading at the lowest level since Friday, near $23.20. The white metal is falling by 1.25%, getting closer to January lows.

Earlier on Wednesday, XAG/USD reached levels above $24.00 but it was rejected and started to move lower. The decline gained speed during the American session and after breaking short-term horizontal and dynamic supports.

Silver price is back under the 20-day Simple Moving Average (SMA), today at $23.60. The mentioned SMA is turning south, suggesting some exhaustion to the upside. The short-term bias is turning to the downside. All could change it XAG/USD manages to rise and hold above $24.00, particularly with a daily close above $24.20.

On the downside, the next target is at the January low at $23.10. Below $23.00 the next support level is seen at $22.80.

Silver Daily chart

-638090509364990186.png)

Silver 4-hour chart

-638090509325722473.png)

-

16:14

EUR/USD grinds higher above 1.0750 on ECB’s comments and offered USD

- EUR/USD rallied on a weak US Dollar and ECB hawkish commentary.

- Federal Reserve Chair Jerome Powell’s speech on Tuesday did not provide any guidance ahead of the US CPI report.

- EUR/USD Price Analysis: A break/close above 1.0770 would pave the way to test 1.0800

The Euro (EUR) resumed its uptrend vs. the US Dollar (USD) and rose to an eight-month new high around 1.0776, ahead of the release of the Consumer Price Index (CPI) in the United States (US), which is foreseen to slow down. Hence the EUR/USD is trading at 1.0759 after hitting a daily low of 1.0725.

Euro climbed on hawkish ECB commentary and expectations that US inflation would ease

Wall Street continues its rally ahead of the release of the US CPI report. The lack of US economic data releases and an irrelevant speech by the US Federal Reserve (Fed) Chair Jerome Powell on Tuesday left the EUR/USD adrift to speculations that US inflation would ease, which could pave the way for a less aggressive Fed. Consequently, the EUR/USD rose steadily.

Aside from this, the EUR/USD got a lift courtesy of several European Central Bank (ECB) officials’ hawkish commentaries. On Tuesday, ECB’s Schnabel said that “interest rates will still have to rise significantly” and that “inflation will not subside by itself.” On Wednesday, the Bank of France Governor and ECB Governing Council (GC) member Francois Villeroy said that the ECB should reach its terminal rate by the summer.

Later, the Austrian Central Bank Governor Robert Holtzmann added that “rates will have to rise significantly further to reach levels that are sufficiently restrictive to ensure a timely return of inflation to target.” Echoing some of his comments was Olli Rehn, who added that rates need to rise “significantly” in the next couple of meetings and reach restrictive levels to dampen inflation.

Ahead of the week, the US economic docket will feature the Consumer Price Index (CPI) report Thursday, with estimates at 0% MoM while annual based is estimated at 6.5%. The so-called Core CPI is foreseen at 0.3% MoM, a tick higher than the previous month, while yearly, it is estimated to come at 5.7%.

EUR/USD Price Analysis: Technical outlook

From a daily chart perspective, the EUR/USD break of weekly highs around 1.0750s opened the door for testing the June 2022 highs of 1.0773. Once that price level is broken, the EUR/USD might test the 1.0800 figure in the near term. That scenario is backed by the Relative Strength Index (RSI) being in bullish territory and aiming higher, though the Rate of Change (RoC) suggests that volatility remains unchanged. Therefore, the EUR/USD might continue to advance steadily or consolidate.

On the other hand, EUR/USD failure to crack 1.0800 would expose the pair to selling pressure, which could tumble the pair to 1.0750, followed by a test of the January 10 daily low of 1.0711 and the 1.0700 figure.

-

15:55

US CPI Preview: Forecasts from 10 major banks, price pressures to ease further

The US Bureau of Labor Statistics will release the Consumer Price Index (CPI) figures for December on Thursday, January 12 at 13:30 GMT and as we get closer to the release time, here are the forecasts by the economists and researchers of 10 major banks regarding the upcoming US inflation print.

The annual CPI is expected to decline to 6.5% from 7.1% in November and see the Core CPI, which excludes volatile food and energy prices, edging lower to 5.7% from 6%. On a monthly basis, the CPI is forecast to stay unchanged while the Core CPI is projected to rise 0.3%.

TDS

“Core prices likely edged higher in Dec, with the index rising 0.3% MoM after printing 0.2% in Nov. Shelter inflation likely remained the key wildcard, though we look for goods deflation to act again as a major offset. Importantly, gas prices likely provided new relief to the CPI, as they fell sharply in Dec. All told, our m/m forecasts imply 6.5%/5.7% YoY for total/core prices.”

RBC Economics

“We expect YoY US consumer price growth to slow significantly in December to 6.3% from 7.1% in November. The steep decline in headline price growth is largely thanks to a significant drop in energy prices. We expect ‘core’ (excluding food & energy products) price growth to slow to 5.6% YoY in December from 6.0% in October. Further signs of declining price growth would support further slowing in the pace of hikes from the Fed. We continue to expect 50 bps of additional hikes to the Fed funds target range in Q1 before a pause at a terminal rate of 4.75% to 5.0%.”

SocGen

“We expect the headline CPI to hold flat against November (0.0%) while moderating to a 6.5% YoY increase, down from the 7.1% posted in November. The Core CPI should be up, and we expect a rise of 0.4% MoM.”

NBF

“The food component likely remained relatively strong, but this increase should have been more than compensated by lower gasoline prices. As a result, headline prices could have decreased 0.1% MoM. If we’re right, the yearon-year rate should come down from 7.1% to 6.7%. The Core index, meanwhile, may have continued to be supported by rising rent prices and advanced 0.3% on a monthly basis. This would translate into a two-tick decline of the 12-month rate to 5.8%.”

Deutsche Bank

“In terms of the MoM rate, the headline CPI is expected at -0.15% at DB with Core CPI expected at +0.22% at DB. In terms of YoY, headline is expected to drop from 7.1% to 6.3% at DB with Core falling from 6% to 5.6%.”

ANZ

“We expect US December Core CPI inflation to rise by 0.4% MoM, with headline flat thanks to lower energy prices. YoY, this would mean core eased to 5.8% from 6.0% and headline to 6.7% from 7.0%.”

ING

“We expect to see a further moderation in the annual rate of inflation from 7.1% down to 6.6%, but this is still more than three times faster than the Federal Reserve’s 2% target. Still, a 0.3% MoM print would lead to the annual rate of Core inflation hitting 5.7% versus 6% in November. We expect to see much sharper falls in the annual rate of inflation from the early second quarter onwards.”

Wells Fargo

“We estimate CPI fell 0.2% in December, bringing the YoY rate down to a 14-month low of 6.3%. We expect another sizable decline in energy prices to weigh on the headline and offset further gains in food and core services prices. But the drop in prices should also be helped along by another decline in core goods, led once again by used autos. We expect core inflation to rise 0.2% with the pace of core services prices little changed. While we believe that shelter inflation is close to its peak, continuing strong gains in the price of other core services can really pump the breaks on progress toward 2% inflation.”

CIBC

“There was more relief in the form of lower gasoline prices for households in December, which will be behind the expected 0.1% monthly decline in total prices. That retrenchment will have been limited by pressure in food prices and an expected 0.2% advance in the core group (excluding food and energy), with the latter likely showing strength in core services tied to the tight labor market, against an easing in core goods prices on weaker demand and the improvement in supply chains and inventories. We are a tick below consensus for both total and core inflation, which could nudge bond yields and the USD lower, but be a plus for equities.”

Commerzbank

“In the US, inflation is clearly on the retreat. From its peak of 9.1% in June, the YoY rate most recently fell to 7.1% in November. For December, we forecast a further decline to 6.4%. Used car prices are likely to have fallen by almost 3% in December from November. We therefore also expect the Core inflation rate to decrease from 6.0% to 5.6%. This would mean a continuation of the easing in inflation – a trend that should continue in 2023. However, we stand by our assessment that the fundamental inflation problem will not be solved. A sustained return to 2% inflation is likely to be prevented by demographically induced labor shortages, the costs of climate policy and increasing protectionism.”

-

15:48

USD/CHF surges to 0.9300 as Swiss Franc tumbles

- The Swiss Franc is among the worst performers on Wednesday.

- US Dollar post mixt results during the American session ahead of US CPI.

- USD/CHF rebounds sharply, above the 20-day SMA.

The USD/CHF is rising by more than 70 pips on Wednesday extending the recovery from the multi-month it reached on Monday at 0.9165. The pair rose momentarily above 0.9300 for the first time since Friday.

Following two days of gains, USD/CHF is back above the 20-day Simple Moving Average (SMA) that stands at 0.9285. The bias is still bearish but the 0.9200 area is becoming a strong support.

CHF drops across the board

The Swiss Franc is the worst performer of the American session. Switzerland bonds are soaring. The Swiss 10-year bond yield is falling by more than 10% at the time of writing, at 1.26%, the lowest level since December 19.

The USD/CHF broke above 0.9250 and accelerated to the upside. It peaked at 0.9303 and then pulled back finding support at 0.9285. At the same time EUR/USD trades at fresh multi-month highs above 1.0770. The EUR/CHF is having the best day in months and it hit levels above parity for the first time since July.

The US Dollar is mixed on Wednesday as market participants await the US CPI report due on Thursday. The index is expected to remain unchanged in December with the annual rate falling from 7.1% to 6.5%.

Technical levels

-

15:31

GBP/USD to reach 1.25 by the second half of 2023 after a stable start of the year – Scotiabank

Economists at Scotiabank expect the GBP/USD to stabilize around 1.20 in the first half of the year. A sustained move higher towards 1.25 is likely latter in 2023.

A sizeable correction is likely after the Q4 snap higher from record lows

“We expect stability around current levels through H1 and some modest strength emerging against a generally overvalued USD in H2 as the global monetary policy tightening cycle matures. At this point, we expect investors will be starting to consider the prospect for easier Fed policy and will be ready to re-embrace risk and move out of the USD.”

“From a (broad) technical point of view; we look for firm GBP support on weakness to the 1.14/1.16 range in Q1.

“A sizeable correction is likely after the Q4 snap higher from record lows. Resistance is 1.2450/00, with an extension to the 1.28/1.30 range likely above 1.25.”

-

15:30

United States EIA Crude Oil Stocks Change came in at 18.962M, above forecasts (-2.243M) in January 6

-

15:10

USD is likely to weaken further in 2023 after a choppy end in 2022 – HSBC

The broad US Dollar tore between opposing forces last month, with the USD Index (DXY) ending the month lower. Economists at HSBC look for USD weakness in 2023.

A US economic soft landing should see the USD broadly weaken

“We believe the USD will weaken further in 2023, as its significant overvaluation (based on the real effective exchange rate (REER) can no longer be supported, once the Fed stops hiking, global growth shows signs of troughing and market volatility comes down.”

“We acknowledge there would be ‘safe-haven’ demand for the USD, if the US economy goes into a deep recession. However, we see that as a risk scenario, rather than an inevitable outcome.”

“If the US economy manages a softer descent, the USD is likely to weaken. That is our base case for 2023.”

-

15:07

GBP/USD seesaws around 1.2140s trendless as traders eye US CPI

- GBP/USD is almost flat, unable to capitalize on the US Dollar weakness.

- Fed’s Powell speech did not provide any forward guidance for the February 1 FOMC meeting.

- GBP/USD Price Analysis: In the near term, it could test the 200-DMA.

The Pound Sterling (GBP) failed to hold to earlier gains against the US Dollar (USD) and augmented selling pressure dragged the GBP/USD down after hitting a daily high of 1.2178. An upbeat market sentiment, as portrayed by US equities, failed to propel the risk-perceived Sterling. At the time of writing, the GBP/USD is trading at 1.2145, slightly below its opening price.

GBP/USD traders brace for the US December's CPI report

Wall Street opened with solid gains after US Federal Reserve Fed Chair Jerome Powell’s speech on Tuesday failed to provide any forward guidance. However, according to Rabobank Analysts, “The Chair was, however, able to squeeze in reference to the Fed prioritizing inflation over employment in the near term, when he said that the case for monetary policy independence lies in the benefits of insulating monetary policy decisions from short-term political considerations.”

Investors shrugged off Powell’s words as US equities closed higher Tuesday. In the meantime, the GBP/USD failed to gain traction even though the greenback continued to weaken. The US Dollar Index, a gauge of the buck’s value against its peers, is losing 0.08% at 103.193.

An absent UK economic calendar keeps traders waiting for the release of the US Consumer Price Index (CPI) report Thursday. Street’s estimates of headline inflation are 0% MoM; on an annual basis, a dip to 6.5% is expected. Excluding volatile items, the so-called Core CPI is foreseen at 0.3% MoM, a tick higher than the previous month, while yearly, it is estimated to come at 5.7%.

GBP/USD Price Analysis: Technical outlook

GBP/USD’s price action in the last three days formed a bullish harami candlestick pattern, suggesting that sellers are moving in. But it should be said that the 200-day Exponential Moving Average (EMA) at 1.2107 would be difficult to surpass by sellers. However, if cleared, that could open the door for a GBP/USD retest of 1.2100, closely followed by the 20-day EMA at 1.2080.

-

14:59

Gold Price Forecast: XAU/USD to see a meaningful long-term break higher above $2,070/75 – Credit Suisse

Gold maintains a large base. Strategists at Credit Suisse expect the yellow metal to stretch higher.

Important support is located at $1,729

“We look for further strength to the 61.8% retracement of the 2022 fall and June 2022 high at $1,878/1,896. Whilst we look for this to cap at first, above would raise the prospect of further strength in the broader range to resistance next at $1,973/98, with a fresh cap expected here.” “Only above $2,070/75 would suggest we are seeing a significant and meaningful long-term break higher.”

“Support is seen at $1,780 initially, and then more importantly at the ‘neckline’ to the base at $1,729.”

-

14:55

ECB's Rehn: Rates will still have to rise significantly

European Central Bank (ECB) Governing Council member Olli Rehn said on Wednesday that rates in the Eurozone will still have to rise significantly in the next couple of meetings and reach restrictive levels to dampen inflation, as reported by Reuters.

In December, Rehn had said that he was expecting the ECB to hike the policy rate by 50 basis points in February and March.

Market reaction

EUR/USD pair edged higher with the initial reaction to these comments. As of writing, the pair was trading at its highest level since late May at 1.0768, rising 0.3% on a daily basis.

-

14:35

USD/CAD: Loonie to be an underperformer among the G10 currencies over the medium-term – Wells Fargo

Canada's economy appears to have lost some momentum in recent months. Subsequently, economists at Wells Fargo also expect the Loonie to weaken over the coming months.

USD/CAD seen at 1.35 by Q1-2024

“We believe a contracting Canadian economy and an end to Bank of Canada tightening could contribute to some underperformance by the Canadian Dollar over the short-to-medium term.”

“We see the possibility for some weakness in the Loonie through Q1-2023, and see only a moderate rebound in the CAD over time.”

“Even acknowledging that risks are tilted toward less CAD softness than our base case forecast projects (which targets a USD/CAD exchange rate of 1.35 by Q1-2024), we still expect the Loonie to be an underperformer among the G10 currencies over the medium-term.”

-

14:33

USD Index wobbles around 103.30 ahead of US inflation

- The index alternates gains with losses near 103.30 midweek.

- US yields trade in a mixed fashion ahead of US CPI (Thursday).

- MBA Mortgage Applications expanded 1.2% WoW.

The greenback, in term of the USD Index (DXY), keeps the range bound theme unchanged around 103.30 on Wednesday.

USD Index focuses on US CPI results

The index maintains a narrow trading range amidst the prevailing cautious stance from market participants, all in light of the upcoming release of US inflation figures gauged by the CPI (Thursday).

Indeed, another weak print in the US consumer prices in December could intensify investors’ perception of a Fed’s pivot in its normalization process and add further conviction of a deceleration in inflation.

So far, and according to CME Group’s FedWatch Tool, the probability of a 25 bps rate raise at the February 1 meeting is at nearly 80% (from around 40% a month ago).

Earlier in the US data space, MBA Mortgage Applications expanded 1.2% n the week to January 6.

What to look for around USD

The dollar remains under pressure and trades in a side-lined fashion in the 103.00 region amidst investors’ prudence ahead of US CPI due on Thursday.

The mixed results from the US Nonfarm Payrolls for the month of December (Friday) seem to have reignited the idea of a probable pivot in the Fed’s policy in the next months, which comes in contrast to the message from the latest FOMC Minutes, where the Committee advocated the need to remain within a restrictive stance for longer, at the time when it ruled out any interest rate reduction for the current year.

Furthermore, the tight labour market, still elevated inflation and the resilient economy are also seen supportive of the firm message from the Federal Reserve and its hiking cycle.

Key events in the US this week: MBA Mortgage Applications (Wednesday) – Inflation Rate, Initial Jobless Claims, Monthly Budget Statement (Thursday) – Flash Michigan Consumer Sentiment (Friday).

Eminent issues on the back boiler: Hard/soft/softish? landing of the US economy. Prospects for further rate hikes by the Federal Reserve vs. speculation of a recession in the next months. Fed’s pivot. Geopolitical effervescence vs. Russia and China. US-China trade conflict.

USD Index relevant levels

Now, the index is retreating 0.06% at 103.21 and the breach of 102.94 (monthly low January 9) would open the door to 101.29 (monthly low May 30) and finally 100.00 (psychological level). On the other hand, the next up barrier comes at 105.63 (monthly high January 6) followed by 106.37 (200-day SMA) and then 107.19 (weekly high November 30).

-

14:14

AUD/USD: The mid-0.70s are within reach – SocGen

AUD/USD remains well within the striking distance of its highest level since late August. Economists at Société Générale believe that the pair could reach the mid-0.70s.

Scope for bearish rate surprises is limited for now

“The RBA is still dragging its feet and the monetary/fiscal policy mix isn’t helpful, but the rates market is only pricing another 75 bps of hikes from here, so scope for bearish rate surprises is limited for now.”

“We dream of AUD/USD trading in the 0.80s but while that may be too much, the mid-0.70s are within reach.”

-

13:52

USD/JPY refreshes weekly high amid modest USD strength, lacks bullish conviction

- USD/JPY edges higher on Wednesday and hits a fresh weekly high amid a modest USD uptick.

- Bets for smaller Fed rate hikes, sliding US bond yields might cap gains for the USD and the pair.

- Traders might also refrain from placing aggressive bets ahead of the US CPI report on Thursday.

The USD/JPY pair gains some positive traction on Wednesday and climbs to the 133.00 neighbourhood, or a fresh weekly top during the early North American session. The uptick, however, lacks bullish conviction and runs the risk of fizzling out rather quickly.

The US Dollar attracts some dip-buying and moves away from a seven-month low touched on Tuesday, which, in turn, is seen lending some support to the USD/JPY pair. Apart from this, a generally positive tone around the equity markets undermines the safe-haven Japanese Yen and provides a modest lift to the major. That said, growing acceptance that the Fed will soften its hawkish stance might hold back bulls from placing aggressive bets and keep a lid on any meaningful upside for spot prices, at least for now.

Friday’s mixed jobs report from the United States (US) showed a slowdown in wage growth and pointed to signs of easing inflationary pressures. Furthermore, business activity in the US services sector hit the worst level since 2009, suggesting that the effect of the Fed's large rate hikes in 2022 is being felt in the economy. This, in turn, lifted bets for smaller Fed rate hikes going forward, which keeps the US Treasury bond yields depressed near a multi-week low and should act as a headwind for the USD.

Apart from this, speculations that the Bank of Japan (BoJ) will eventually phase out its ultra-loose monetary policy settings might further contribute to capping the USD/JPY pair. Traders might also refrain from placing directional bets and prefer to move to the sidelines ahead of the release of the US consumer inflation figures on Thursday. The crucial US CPI report will influence the Fed's policy outlook, which, in turn, will drive the USD and provide a fresh directional impetus to the pair.

In the meantime, the US bond yields, the US price dynamics and the broader market risk sentiment will be looked upon for some short-term trading opportunities around the USD/JPY pair. Nevertheless, the aforementioned fundamental backdrop warrants some caution for bullish traders and positioning for any further appreciating move in the absence of any relevant economic data from the US.

Technical levels to watch

-

13:20

Gold Price Forecast: XAU/USD eases from eight-month high, downside remains cushioned

- Gold price struggles to capitalize on its intraday positive move to a fresh multi-month peak.

- A modest US Dollar strength and a positive risk tone act as a headwind for the commodity.

- Bets for smaller Fed rate hikes help limit losses as the focus remains on the US CPI report.

Gold price surrenders modest intraday gains to a fresh eight-month peak, around the $1,886-$1,887 area touched earlier this Wednesday and turns neutral heading into the North American session. Currently placed just above the $1,875 level, the downside for the XAU/USD remains cushioned amid expectations for a less aggressive policy tightening by the Federal Reserve (Fed).

Bets for less aggressive Federal Reserve lend support to Gold price

Friday’s mixed jobs report from the United States (US) showed a slowdown in wage growth and pointed to signs of easing inflationary pressures. Furthermore, business activity in the US services sector hit the worst level since 2009, suggesting that the effect of the Fed's large rate hikes in 2022 is being felt in the economy. This, in turn, lifted bets for smaller Fed rate hikes going forward, which keeps the US Treasury bond yields depressed near a multi-week low and might continue to lend support to the non-yielding Gold price.

Modest US Dollar strength, positive risk tone caps Gold price

That said, a modest US Dollar (USD) uptick is holding back bullish traders from placing aggressive bets. A stronger Greenback tends to act as a headwind for the US Dollar-denominated Gold price. Apart from this, a generally positive tone around the equity markets further contributes to capping the upside for the safe-haven precious metal, at least for the time being. Traders also seem reluctant and prefer to move to the sidelines ahead of the release of the latest consumer inflation figures from the United States (US), due on Thursday.

Focus remains on consumer inflation figures from United States

The crucial US CPI report will play a key role in influencing the Federal Reserve's rate-hike path and driving Gold price in the near term. Policymakers have indicated that they remain committed to combat high inflation and that rates could remain elevated for longer, or until there is clear evidence that consumer prices are falling. Hence, a stronger US CPI print will lift bets for a more hawkish Fed and push the XAU/USD back down.

Heading into the key data risk, sliding US bond yields could act as a headwind for the Greenback in the absence of any relevant market-moving economic releases from the US. This might continue to lend some support to the Gold price. Apart from this, traders might take cues from the broader risk sentiment to grab short-term opportunities around the XAU/USD.

Gold price technical outlook

From a technical perspective, any meaningful corrective slide is likely to find decent support near the $1,865-$1,860 resistance breakpoint. A sustained break below might prompt some technical selling and drag the Gold price to the $1,835-$1,833 horizontal support. On the flip side, the next level of resistance is pegged near the $1,900 round figure. A sustained strength beyond will be seen as a fresh trigger for bullish traders and pave the way for an extension of the near-term appreciating move.

Key levels to watch

-

13:14

USD/CAD should continue to push lower, scope for gains is limited – Scotiabank

USD/CAD consolidates but still trades shy of fair value, according to economists at Scotiabank.

A drop to the upper 1.32s should play out

“The CAD has corrected some of the more excessive undervaluation our fair value model highlighted last week but spot remains well above its 1.3249 estimated equilibrium, suggesting that the market should continue to push lower and that scope for USD gains is limited in the short run.”

“We spot minor resistance at 1.3450 and stronger resistance at 1.3475/00 intraday. Support is 1.3410 and 1.3355.”

“Broader technical signals suggest a drop to the upper 1.32s should play out after the break under the Dec/Jan range.”

-

12:46

GBP/USD: Consolidation ahead of another push higher – Scotiabank

Sterling is a modest under-performer on the session. Economists at Scotiabank expect the GBP/USD pair to hold above 1.21 to keep the undertone constructive.

Gains back above 1.2175 would be constructive

“Cable’s drift off the early week high just above 1.22 remains limited and could still be construed as a bullish – potentially – consolidation ahead of another push higher.”

“Cable is well-supported in the low 1.21 area but support will have to hold to keep the undertone constructive.”

“Tuesday’s inside range sessions casts a slightly more negative look to the daily chart. Gains back above 1.2175 intraday would be constructive.”

-

12:45

EUR/USD Price Analysis: The continuation of the upside could revisit 1.0800

- EUR/USD keeps the bid tone unchanged near 1.0750 on Wednesday.

- The surpass of recent peaks around 1.0760 exposes a move to 1.0800.

EUR/USD is up for the fourth straight session and revisits the 1.0750 region midweek.

In case bulls remain in control, the breakout of the January high at 1.0760 (January 9) could put the June 2022 peak at 1.0773 (June 27) to the test closely followed by the May 2022 top at 1.0786 (May 30).

Extra gains from here should target the key round level at 1.0800.

In the meantime, further gains remain in store for the pair while above the 200-day SMA at 1.0308.

EUR/USD daily chart

-

12:15

US CPI: USD rallies should be sold into unless Core measure surprises to the upside – TDS

Economists at TD Securities analyze how tomorrow's all important US Consumer Price Index (CPI) print could impact the Dollar and the USD/JPY and EUR/USD pairs.

The bar is high to compel a reversal of fortune

“The market has moved back to fading Fed hawkishness and putting the USD on the back-foot. An on-consensus print does not strike us as a particular threat to the latter. Moreover, it is not evidently clear that a positive surprise on core inflation would tremendously alter the path for the USD either.”

“As much as the USD looks stretched on a tactical basis, we think the bar is high to compel a reversal of fortune. USD rallies should be sold into.”

“With the BoJ meeting next week, USD/JPY is a clear candidate for more downside. Meanwhile, EUR/USD has shown the capacity to rally again; 1.0780/00 is all that stands in the way of another melt-up.”

-

12:11

EUR/GBP climbs to fresh weekly high, bulls flirt with 0.8865-0.8875 strong resistance

- EUR/GBP scales higher for the third straight day and touches a fresh weekly high on Wednesday.

- Dovish BoE expectations weigh on the British Pound and remain supportive of the momentum.

- The recent hawkish ECB rhetoric underpins the Euro and supports prospects for additional gains.

The EUR/GBP cross builds on its goodish rebound from over a two-week low and gains some follow-through traction for the third successive day on Wednesday. The momentum lifts spot prices to a fresh weekly high during the mid-European session, with bulls now eyeing a breakout through the 0.8865-0.8875 supply zone.

The British Pound continues with its relative underperformance, which, along with a modest uptick in the shared currency, acts as a tailwind for the EUR/GBP cross. A bleak outlook for the UK economy has been fueling speculations that the Bank of England (BoE) is nearing the end of the current rate-hiking cycle. This, in turn, is seen as a key factor undermining the Sterling.

Furthermore, hawkish rhetoric from several European Central Bank (ECB) policymakers benefits the Euro and further lends support to the EUR/GBP cross. In fact, the ECB governing council member Robert Holzmann said on Wednesday that rates will have to rise significantly further to reach levels that are sufficiently restrictive to ensure a timely return of inflation to target.