Notícias do Mercado

-

20:00

DJIA 15,536.50 41.68 0.27%, S&P 500 1,705.05 7.45 0.44%, NASDAQ 3,744.74 26.90 0.72%

-

19:20

American focus: the euro rose

The euro rose against the dollar, which , first of all , due to the anticipation of the announcement of the outcome of meetings of the Open Market Committee of the Federal Reserve , which begins today and will end tomorrow . According to the median forecast of economists , the majority of the voting committee may decide to reduce the amount of monthly purchases of bonds to $ 75 billion to $ 85 billion

Today published data on U.S. inflation. At the end of last month , consumer prices rose less than expected , continuing with a series of "soft" reports on inflation, which will affect the decision of the Federal Reserve officials on future policy. According to the report , the August consumer price index rose by 0.1 %, compared with an increase of 0.2 % in the previous month. Core CPI , which excludes food prices and energy costs , also rose by 0.1 % added that the CPI was slightly below forecasts of experts - at the level of 0.2 % , while the growth of the underlying index confirmed their expectations. In addition, it was reported that on an annual basis , consumer prices rose in August by 1.5 %, which was followed after increasing by 2.0 % a month earlier. Meanwhile, the core consumer price index rose by 1.8 %, compared with growth of 1.7 % in July. According to experts , the value of these indicators would grow by 1.6 % and 1.8% , respectively.

The euro had data on the index of sentiment in the business environment. As shown by recent research , which was published today institute ZEW, the German index of sentiment in the business environment has grown significantly in the month of September , registering with the second monthly increase and exceeded the estimates of many experts. According to a report this month, the indicator of economic sentiment for Germany's business climate rose to 49.6 , up from 42 in August. We add that according to the average estimate of economists this indicator had improved only to the level of 45.3 . Note also that the last result index was the highest since April 2010 , when he was 53 , and well above its historical average of 23.8 points. Meanwhile, studies have shown that the current conditions index also rose , registering the third consecutive monthly gain . The value of this index in September rose to the level of 30.6 , up from 18.3 last month. It was the best figure since June last year.

At the same time, did not prevent the growth of the European currency submitted data for the euro area , which were worse than expected .

The European Central Bank said that by the end of July profit Eurozone current account decreased again , registering with the fourth monthly decline in a row, which was due mainly to a sharp drop in income . According to the report , the seasonally adjusted balance of payments surplus fell in July to the level of 16.9 billion euros, compared with the upwardly revised figure for the previous month at 19.8 billion euros. Add that to the experts according to the average surplus would rise to the level of 18.3 billion euros from 16.9 billion , which was originally reported last month .

In addition, the Statistical Office Eurostat reported that the trade surplus of the euro zone unexpectedly , and at the same time is drastically reduced in the month of July , which was associated with a marked drop in exports (for the third time in four months ) , and almost the same volume of imports . According to the report , the seasonally adjusted trade surplus fell in July to a level of 11.1 billion euros, compared with a revised downward from the previous month at 13.5 billion euros. Add that to the experts according to the average surplus in trade in goods had increased to 15.3 billion from 14.9 billion , which was originally reported. In addition , the data showed that exports in July totaled 155.9 billion billion, down 1.6% from June , while imports reached 144.8 billion euros, which is 0.1 % less than in the previous month.

The pound rose slightly against the dollar, although it has lost some of the previously captured positions . Note that this trend was accompanied by a release of weak data on Britain. It is learned from the Office for National Statistics , at the end of last month, the growth of annual inflation slowed again , registering the second monthly decline in a row, which was primarily due to a slower increase in transportation costs.

According to the report , in the month of August consumer price index rose by 2.7 % per annum , compared with an increase of 2.8 % in July. Add that final reading fully confirmed the experts' forecasts . In addition, it was reported that on a monthly basis the consumer price index rose 0.4 % , after the previous month, it remained unchanged. Many experts expect that the value of this index will rise by 0.5 %.

Meanwhile, core inflation, which excludes the cost of energy , food, alcoholic beverages and tobacco products remained unchanged in August - at the level of 2 % , confounding economists' expectations for a moderate increase to 2.1 %.

Meanwhile, another report from the Office for National Statistics showed that producer prices inflation slowed markedly in August , indicating a weakening of inflationary pressures.

The data showed that the index of producer prices rose in August by 1.6 % per annum , compared with an increase of 2.1% a month earlier. Experts estimate the growth of this index was up 1.8%. In monthly terms, wholesale prices rose by 0.1 %, which followed a 0.2 percent increase in July. It was assumed that the growth will be 0.2 %. As for the input price inflation , it declined in August to 2.8 % per year from 5.1 % last month , and lower than forecast at 3% . On a monthly basis , raw materials prices fell 0.2 % , registering the first decline in three months .

-

18:20

European stocks close

European stocks declined from a five-year high as investors sold holdings in companies from Lloyds Banking Group Plc to Continental AG.

In Germany, a report showed that investor confidence in Europe’s largest economy increased in September to the highest level since April 2010. An index compiled by the ZEW Center for European Economic Research, which aims to predict economic developments six months in advance, rose to 49.6 from 42 in August. That exceeded the median economist projection for a reading of 45.

National benchmark indexes dropped in 14 of the 18 western-European markets today. Germany’s DAX and France’s CAC 40 fell 0.2 percent. The U.K.’s FTSE 100 declined 0.8 percent.

Lloyds retreated 3.5 percent to 74.7 pence after UK Financial Investments Ltd. sold a 6 percent stake in Britain’s largest mortgage lender. The body, which oversees the government’s holdings in banks, said it sold 4.28 billion shares at 75 pence apiece. The transaction reduced the government’s stake in Lloyds to 32.7 percent from 38.7 percent.

Continental fell 3.1 percent to 123 euros after Schaeffler AG and Schaeffler Verwaltungs GmbH sold a combined stake of 4 percent in Europe’s second-largest maker of auto parts. Schaeffler and its holding company sold 7.8 million shares at 122.50 euros a share, according to a statement.

A gauge of carmakers slipped 1.4 percent from its highest level in at least 26 years after a report showed European car sales fell 4.9 percent in August. Volkswagen AG lost 1.5 percent to 180.25 euros. PSA Peugeot Citroen and Renault SA, France’s biggest automobile manufacturers, dropped 2.5 percent to 12.32 euros and 2.4 percent to 58.15 euros, respectively.

-

17:00

European stocks closed in minus: FTSE 100 6,578.68 -44.18 -0.67%, CAC 40 4,147.26 -4.96 -0.12%, DAX 8,599.75 -13.25 -0.15%

-

16:40

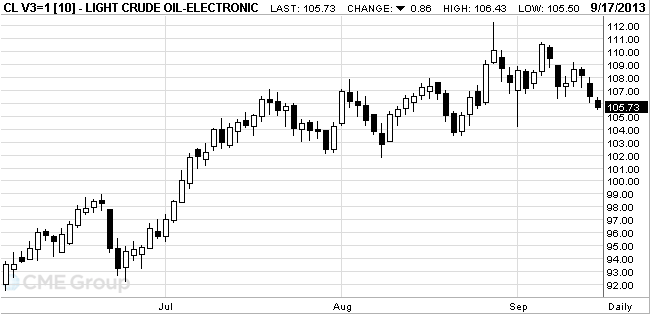

Crude falls for third day

West Texas Intermediate crude slid for a third day as a

Prices fell as much as 1 percent. Secretary of State John Kerry said the

WTI for October delivery dropped 73 cents, or 0.7 percent, to $105.86 a barrel at 10:50 a.m. on the New York Mercantile Exchange. The volume of all futures traded was 6.4 percent above the 100-day average.

Brent for November settlement slid $1.53, or 1.4 percent, to $108.54 a barrel on the London-based ICE Futures Europe exchange. Volume was 8.7 percent above the 100-day average. The European benchmark’s premium to WTI shrank to $3.20 from $3.88 yesterday.

-

16:20

Gold stabilized

Gold prices have stabilized slightly above the five-week low , as investors await news from the Fed about the reduction incentive program .

From the beginning, gold fell by more than 20 per cent as the growing U.S. economy has made the precious metal less attractive as a low-risk assets .

According to economists, the two-day meeting, which will begin on Tuesday , the Fed will reduce the amount of buying bonds of at least $ 10 billion a month from the current $ 85 billion .

Given the current economic situation in the U.S., experts expect only a small reduction in incentives. Therefore, gold will continue to receive support . At the same time, if the Fed does not reduce incentives this year , experts believe that gold at the end of the year will cost $ 1.400-1.500 per ounce.

A peaceful solution to the Syrian problem had a negative impact on the gold market , but the message that former U.S. Treasury Secretary Lawrence Summers , withdrew his candidacy for the post of chairman of the Fed, prices will rise , analysts said.

The cost of the October futures on the COMEX gold is trading today in the range of $ 1306.70 - $ 1323.60 per ounce.

-

15:00

U.S.: NAHB Housing Market Index, September 58 (forecast 59)

-

14:45

Option expiries for today's 1400GMT cut

EUR/USD $1.3200, $1.3220, $1.3250, $1.3300, $1.3350, $1.3355, $1.3360

USD/JPY Y98.75, Y98.90, Y99.00, Y99.10, Y99.35, Y99.50, Y100.00,

GBP/USD $1.5800, $1.5980

AUD/USD $0.9200, $0.9300, $0.9315, $0.9355, $0.9400

UAD/CAD C$1.0220, C$1.0245, C$1.0450

-

14:35

U.S. Stocks open: Dow 15,522.81 +28.03 +0.18%, Nasdaq 3,727.04 +9.19 +0.25%, S&P 1,700.66 +3.06 +0.18%

-

14:24

Before the bell: S&P futures +0.03%, Nasdaq futures +0.15%

U.S. stock-index futures were little changed as Federal Reserve policy makers prepared to begin a two-day policy meeting.

Global Stocks:

Nikkei 14,311.67 -93.00 -0.65%

Hang Seng 23,180.52 -71.89 -0.31%

Shanghai Composite 2,185.56 -45.84 -2.05%

FTSE 6,590.43 -32.43 -0.49%

CAC 4,143.28 -8.94 -0.22%

DAX 8,597.81 -15.19 -0.18%

Crude oil $105.81 -0.73%

Gold $1315.00 -0.21%

-

14:01

U.S.: Total Net TIC Flows, July 56.7

-

14:00

U.S.: Net Long-term TIC Flows , July -31.1 (forecast -45.3)

-

13:32

U.S.: CPI, Y/Y, August +1.5% (forecast +1.6%)

-

13:32

U.S.: CPI excluding food and energy, Y/Y, August +1.8% (forecast +1.8%)

-

13:31

Canada: Manufacturing Shipments (MoM), July +1.7% (forecast +0.6%)

-

13:31

U.S.: CPI, m/m , August +0.1% (forecast +0.2%)

-

13:31

U.S.: CPI excluding food and energy, m/m, August +0.1% (forecast +0.1%)

-

13:15

European session: the euro rose against the dollar

Data

01:30 Australia RBA Meeting's Minutes

01:30 Australia New Motor Vehicle Sales (MoM) August -3.6% Revised From -3.5% +1.8% +0.8%

01:30 Australia New Motor Vehicle Sales (YoY) August +3.0% +0.2%

02:00 China Leading Index August +1.4% +0.7%

08:00 Eurozone Current account, adjusted, bln August 19.8 Revised From 16.9 18.3 16.9

08:30 United Kingdom Retail Price Index, m/m August 0.0% +0.4% +0.5%

08:30 United Kingdom Retail prices, Y/Y August +3.1% +3.2% +3.3%

08:30 United Kingdom Producer Price Index - Input (MoM) August +1.1% +0.3% -0.2%

08:30 United Kingdom Producer Price Index - Input (YoY) August +5.0% +3.0% +2.8%

08:30 United Kingdom Producer Price Index - Output (MoM) August +0.2% +0.2% +0.1%

08:30 United Kingdom Producer Price Index - Output (YoY) August +2.1% +1.8% +1.6%

08:30 United Kingdom HICP, m/m August 0.0% +0.5% +0.4%

08:30 United Kingdom HICP, Y/Y August +2.8% +2.7% +2.7%

08:30 United Kingdom HICP ex EFAT, Y/Y August +2.0% +2.1% +2.0%

09:00 Eurozone Trade Balance s.a. July 13.5 Revised From 14.9 15.3 11.1

09:00 Eurozone ZEW Economic Sentiment September 44.0 47.2 58.6

09:00 Germany ZEW Survey - Economic Sentiment September 42.0 45.3 49.6

The euro rose against the dollar, which , first of all , due to the anticipation of the announcement of the outcome of meetings of the Open Market Committee of the Federal Reserve , which begins today and will end tomorrow . According to the median forecast of economists , the majority of the voting committee may decide to reduce the amount of monthly purchases of bonds to $ 75 billion to $ 85 billion

Meanwhile, we add that did not prevent the growth of the European currency submitted data for the euro area , which were worse than expected .

The European Central Bank said that by the end of July profit Eurozone current account decreased again , registering with the fourth monthly decline in a row, which was due mainly to a sharp drop in income . According to the report , the seasonally adjusted balance of payments surplus fell in July to the level of 16.9 billion euros, compared with the upwardly revised figure for the previous month at 19.8 billion euros. Add that to the experts according to the average surplus would rise to the level of 18.3 billion euros from 16.9 billion , which was originally reported last month .

In addition, the Statistical Office Eurostat reported that the trade surplus of the euro zone unexpectedly , and at the same time is drastically reduced in the month of July , which was associated with a marked drop in exports (for the third time in four months ) , and almost the same volume of imports . According to the report , the seasonally adjusted trade surplus fell in July to a level of 11.1 billion euros, compared with a revised downward from the previous month at 13.5 billion euros. Add that to the experts according to the average surplus in trade in goods had increased to 15.3 billion from 14.9 billion , which was originally reported.

In addition , the data showed that exports in July totaled 155.9 billion billion, down 1.6% from June , while imports reached 144.8 billion euros, which is 0.1 % less than in the previous month.

The pound rose slightly against the dollar, although it has lost some of the previously captured positions . Note that this trend was accompanied by a release of weak data on Britain. It is learned from the Office for National Statistics , at the end of last month, the growth of annual inflation slowed again , registering the second monthly decline in a row, which was primarily due to a slower increase in transportation costs.

According to the report , in the month of August consumer price index rose by 2.7 % per annum , compared with an increase of 2.8 % in July. Add that final reading fully confirmed the experts' forecasts . In addition, it was reported that on a monthly basis the consumer price index rose 0.4 % , after the previous month, it remained unchanged. Many experts expect that the value of this index will rise by 0.5 %.

Meanwhile, core inflation, which excludes the cost of energy , food, alcoholic beverages and tobacco products remained unchanged in August - at the level of 2 % , confounding economists' expectations for a moderate increase to 2.1 %.

Meanwhile, another report from the Office for National Statistics showed that producer prices inflation slowed markedly in August , indicating a weakening of inflationary pressures.

The data showed that the index of producer prices rose in August by 1.6 % per annum , compared with an increase of 2.1% a month earlier. Experts estimate the growth of this index was up 1.8%. In monthly terms, wholesale prices rose by 0.1 %, which followed a 0.2 percent increase in July. It was assumed that the growth will be 0.2 %. As for the input price inflation , it declined in August to 2.8 % per year from 5.1 % last month , and lower than forecast at 3% . On a monthly basis , raw materials prices fell 0.2 % , registering the first decline in three months .

EUR / USD: during the European session, the pair rose to $ 1.3367

GBP / USD: during the European session, the pair rose to $ 1.5936 , and then fell to $ 1.5884

USD / JPY: during the European session, the pair traded in a narrow range of Y99.05-Y99.37

At 12:30 GMT Canada will announce the change of volume of manufacturing sales in July. Also at this time, the U.S. consumer price index will be released and the core consumer price index for August. At 13:00 GMT the United States will be known on net purchases of long-term U.S. securities by foreign investors and the total net amount of purchases of U.S. securities by foreign investors in July. At 14:00 GMT the U.S. will release the housing market index from the NAHB for September. At 22:45 GMT New Zealand will report on the balance of the current account of balance of payments and the ratio of current account deficit to GDP for the 2nd quarter .

-

13:00

Orders

EUR/USD

Offers Y100.60/65, Y100.20/50, Y100.00, Y99.40/50

Bids Y98.70/50, Y98.25/20, Y98.00, Y97.90/80, Y97.65

GBP/USD

Offers $1.6050, $1.6000, $1.5975/95, $1.5945/50

Bids $1.5870, $1.5855/50, $1.5840, $1.5820

AUD/USD

Offers $0.9415/20, $0.9400, $0.9370/80, $0.9345

Bids $0.9285/80, $0.9270, $0.9250, $0.9225/20, $0.9205/00

EUR/GBP

Offers stg0.8550/55, stg0.8520, stg0.8460/65, stg0.8425/30, stg0.8410

Bids stg0.8371, stg0.8357, stg0.8350, stg0.8320

EUR/JPY

Offers Y134.30/40, Y133.80, Y133.50, Y133.00/10, Y132.70

Bids Y132.00/1.90, Y131.50, Y131.30/20, Y130.80

USD/JPY

Offers Y100.60/65, Y100.20/50, Y100.00, Y99.98, Y99.40/50

Bids Y98.70/50, Y98.25/20, Y98.00, Y97.65

-

11:30

European stock indices fell

European stocks declined from a five-year high as investors sold stakes in companies from Lloyds Banking Group Plc (LLOY) to Continental AG. U.S. index futures were little changed, while Asian shares slid.

The Stoxx Europe 600 Index slipped 0.4 percent to 312.06 at 9:04 a.m. in London after yesterday rallying to its highest level in more than five years. Standard & Poor’s 500 Index futures decreased 0.2 percent after the equity benchmark rose to a six-week high yesterday, while the MSCI Asia Pacific Index retreated 0.5 percent from its highest level since May 22.

The Federal Open Market Committee will probably decide at a two-day policy meeting starting today to lower its $85 billion of monthly bond purchases by $10 billion, according to the median estimate of economists survey earlier this month. Economists forecast in a July survey that the Fed would reduce its asset purchases by $20 billion.

Lloyds retreated 2.1 percent to 75.8 pence after UK Financial Investments Ltd. sold a 6 percent stake in the U.K.’s largest mortgage lender. The body, which oversees the government’s holdings in banks, said it sold 4.28 billion shares at 75 pence apiece. The transaction reduced the government’s stake in Lloyds to 32.7 percent from 38.7 percent.

Continental fell 3.9 percent to 122 euros after Schaeffler AG and Schaeffler Verwaltungs GmbH sold a combined stake of about 4 percent in Europe’s second-largest car-parts maker.

A gauge of European carmakers slipped 1.4 percent from its highest level in at least 26 years after a report showed European car sales fell 4.9 percent in August. Volkswagen AG lost 1.9 percent to 179.50 euros, while PSA Peugeot Citroen and Fiat SpA dropped 3.6 percent to 12.18 euros and 1.4 percent to 6.05 euros, respectively.

FTSE 100 6,601.38 -21.48 -0.32%

CAC 40 4,138.58 -13.64 -0.33%

DAX 8,597.67 -15.33 -0.18%

-

10:23

Option expiries for today's 1400GMT cut

EUR/USD $1.3200, $1.3220, $1.3250, $1.3300, $1.3350, $1.3355, $1.3360

USD/JPY Y98.75, Y98.90, Y99.00, Y99.10, Y99.35, Y99.50, Y100.00,

GBP/USD $1.5800, $1.5980

AUD/USD $0.9200, $0.9300, $0.9315, $0.9355, $0.9400

UAD/CAD C$1.0220, C$1.0245, C$1.0450

-

10:01

Eurozone: ZEW Economic Sentiment, September 58.6 (forecast 47.2)

-

10:00

Germany: ZEW Survey - Economic Sentiment, September 49.6 (forecast 45.3)

-

10:00

Eurozone: Trade Balance s.a., July 11.1 (forecast 15.3)

-

09:39

United Kingdom: Retail Price Index, m/m, August +0.5% (forecast +0.4%)

-

09:35

United Kingdom: HICP, m/m, August +0.4% (forecast +0.5%)

-

09:33

United Kingdom: Producer Price Index - Input (MoM), August -0.2% (forecast +0.3%)

-

09:33

United Kingdom: Retail prices, Y/Y, August +3.3% (forecast +3.2%)

-

09:32

United Kingdom: Producer Price Index - Output (MoM), August +0.1% (forecast +0.2%)

-

09:32

United Kingdom: Producer Price Index - Input (YoY) , August +2.8% (forecast +3.0%)

-

09:30

United Kingdom: Producer Price Index - Output (YoY) , August +1.6% (forecast +1.8%)

-

09:30

United Kingdom: HICP, Y/Y, August +2.7% (forecast +2.7%)

-

09:30

United Kingdom: HICP ex EFAT, Y/Y, August +2.0% (forecast +2.1%)

-

09:00

Eurozone: Current account, adjusted, bln , August 16.9 (forecast 18.3)

-

08:40

FTSE 100 6,608.14 -14.72 -0.22%, CAC 40 4,142.23 -9.99 -0.24%, Xetra DAX 8,603.15 -9.85 -0.11%

-

07:20

European bourses are initially seen trading a touch lower Tuesday: the FTSE down 7, the DAX down 10 and the CAC down 7.

-

07:01

Asian session: The dollar traded 0.4 percent from its lowest level

01:30 Australia RBA Meeting's Minutes

01:30 Australia New Motor Vehicle Sales (MoM) August -3.6% Revised From -3.5% +1.8% +0.8%

01:30 Australia New Motor Vehicle Sales (YoY) August +3.0% +0.2%

02:00 China Leading Index August +1.4% +0.7%

The dollar traded 0.4 percent from its lowest level in almost three weeks against the euro as investors await a decision on U.S. monetary policy from Federal Reserve officials beginning a two-day meeting today. The Federal Open Market Committee will probably decide to slow its monthly bond purchases to $75 billion from $85 billion, according to the median estimate of economists in a Bloomberg News survey on Sept. 6.

The Bloomberg U.S. Dollar Index was near a five-week low after the exit of Lawrence Summers from consideration to be the next Fed chairman fueled speculation the central bank will take a more gradual approach to scaling back bond purchases that tend to debase the currency. Fed Vice Chairman Janet Yellen is the leading candidate to replace Ben S. Bernanke following the withdrawal of Summers from consideration, a person familiar with the process said.

The euro climbed against the yen before a report that may show investor confidence in Germany climbed to a half-year high. The ZEW Center for European Economic Research in Mannheim will probably say today its index of German investor and analyst expectations, which aims to predict economic developments six months in advance, climbed to 45 this month from 42 in August, according to the median forecast in a Bloomberg poll. If confirmed, that would be the highest since March.

EUR / USD: during the Asian session the pair is trading around the $ 1.3330

GBP / USD: during the Asian session, the pair is trading around the $ 1.5900

USD / JPY: during the Asian session the pair rose to Y99.35

There is a full calendar on both sides of the Atlantic Tuesday, although the main event over the next two days is undoubtedly the 2-day FOMC meeting and any announcement Wednesday of any "tapering." The European calendar will see the Spanish second quarter labour cost survey released at 0700GMT. Central bank speakers are then to the fore. At 0730GMT, ECB Governing Council member Erkki Liikanen will hold a press conference on monetary policy, in Helsinki. At 0830GMT, ECB Executive Board member Peter Praet will deliver a speech at an LSE conference on regulation, in London. Further European data is set to be released at 0800GMT, when the EMU July current account numbers will be released. At 0900GMT, the EMU July trade balance will be released. Also due at 0900GMT, Germany's September ZEW survey is set for publication. Expectations are for a rise to 20.0 in the current situation, up from 18.3 in August. Expectations are seen rising to 45 from 42. ECB Governing Council member Ewald Nowotny will sit in on discussions about banking union, in Vienna, starting at 0945GMT. Back in Europe, at 1700GMT, ECB Executive Board member Peter Praet will participate in a panel discussion on the banking union, in Brussels.

There is a raft of UK data set for release at 0830GMT, focusing on both CPI and PPI inflation data. CPI inflation is likely to have moved a little closer to the Bank of England's 2% target in August after British Retail Consortium data showed prices fell during the month. A fall to 2.7% would take the CPI rate below the 2.8% forecast for August in the BOE's most recent Inflation Report. In terms of producer prices, both input and output price growth is likely to have eased slightly in August as a result of the recent rise in sterling. Also expected is the official UK July house price data.

-

06:21

Commodities. Daily history for Sep 16’2013:

GOLD 1,308.60 0.20 0.02%

OIL (WTI) 106.20 -2.01 -1.86%

-

06:21

Stocks. Daily history for Sep 16’2013:

Nikkei 225 14,404.67 17,40 0,12%

Hang Seng 23,219.19 303,91 1,33%

S & P / ASX 200 5,247.99 28,36 0,54%

Shanghai Composite -4,82 -0,22 2,231.4%

FTSE 100 6,621.7 +37.90 +0.58 %

CAC 40 4,151.22 +36.72 +0.89 %

DAX 8,612.4 +102.98 +1.21 %

DJIA 15,494.90 118.80 0.77%

S&P 500 1,696.66 8.67 0.51%

NASDAQ 3,717.85 -4.34 -0.12%

-

06:20

Currencies. Daily history for Sep 16'2013:

(pare/closed(00:00 GMT +02:00)/change, %)

EUR/USD $1,3335 +0,60%

GBP/USD $1,5896 +0,57%

USD/CHF Chf0,9272 -0,33%

USD/JPY Y99,08 -0,41%

EUR/JPY Y132,15 -0,12%

GBP/JPY Y157,50 +0,16%

AUD/USD $0,9319 +0,61%

NZD/USD $0,8173 +0,46%

USD/CAD C$1,0322 -0,04%

-

06:00

Schedule for today, Tuesday, Sep 17’2013:

01:30 Australia RBA Meeting's Minutes

01:30 Australia New Motor Vehicle Sales (MoM) August -3.6% Revised From -3.5% +1.8% +0.8%

01:30 Australia New Motor Vehicle Sales (YoY) August +3.0% +0.2%

02:00 China Leading Index August +1.4% +0.7%

08:00 Eurozone Current account, adjusted, bln August 16.9 18.3

08:30 United Kingdom Retail Price Index, m/m August 0.0% +0.4%

08:30 United Kingdom Retail prices, Y/Y August +3.1% +3.2%

08:30 United Kingdom Producer Price Index - Input (MoM) August +1.1% +0.3%

08:30 United Kingdom Producer Price Index - Input (YoY) August +5.0% +3.0%

08:30 United Kingdom Producer Price Index - Output (MoM) August +0.2% +0.2%

08:30 United Kingdom Producer Price Index - Output (YoY) August +2.1% +1.8%

08:30 United Kingdom HICP, m/m August 0.0% +0.5%

08:30 United Kingdom HICP, Y/Y August +2.8% +2.7%

08:30 United Kingdom HICP ex EFAT, Y/Y August +2.0% +2.1%

09:00 Eurozone Trade Balance s.a. July 14.9 15.3

09:00 Eurozone ZEW Economic Sentiment September 44.0 47.2

09:00 Germany ZEW Survey - Economic Sentiment September 42.0 45.3

12:15 U.S. Treasury Sec Lew Speaks

12:30 Canada Manufacturing Shipments (MoM) July -0.5% +0.6%

12:30 U.S. CPI, m/m August +0.2% +0.2%

12:30 U.S. CPI, Y/Y August +2.0% +1.6%

12:30 U.S. CPI excluding food and energy, m/m August +0.2% +0.1%

12:30 U.S. CPI excluding food and energy, Y/Y August +1.7% +1.8%

13:00 U.S. Total Net TIC Flows July -19.0

13:00 U.S. Net Long-term TIC Flows July -66.9 -45.3

14:00 U.S. NAHB Housing Market Index September 59 59

15:30 United Kingdom MPC Member Tucker Speaks

20:30 U.S. API Crude Oil Inventories September -2.9

22:30 New Zealand Current Account Quarter II -0.66 -1.87

-