Notícias do Mercado

-

20:00

DJIA 15,681.80 152.09 0.98%, S&P 500 1,720.85 16.09 0.94%, NASDAQ 3,781.07 35.38 0.94%

-

19:00

U.S.: Fed Interest Rate Decision , 0.25% (forecast 0.25%)

-

18:21

European stocks close

European stocks advanced, sending the Stoxx Europe 600 Index near a five-year high, as investors awaited the Federal Reserve’s decision on reducing monthly bond purchases.

The Federal Open Market Committee wraps up a two-day policy meeting today, at which it will probably decide to lower its $85 billion of monthly bond purchases. Among 64 economists surveyed by Bloomberg News, 33 predicted the Fed will reduce its buying of Treasuries by $5 billion or less, with 31 projecting a cut of $10 billion or more.

Earlier this month, a Bloomberg News survey of 34 economists forecast a $10 billion reduction. In a July poll, half of the 54 respondents predicted a $20 billion cut.

The FOMC releases both its policy statement and forecasts for economic growth, inflation and unemployment at 2 p.m. New York time, after the European markets close. Chairman Ben S. Bernanke will hold a press conference half an hour later.

The Bank of England today released the minutes from its Sept. 4-5 meeting, which showed that officials unanimously concluded there was no need for additional stimulus given an improving outlook for the British economy.

National benchmark indexes rose in 15 of the 18 western European markets today. Germany’s DAX advanced 0.5 percent. The U.K.’s FTSE 100 slipped 0.2 percent. France’s CAC 40 increased 0.6 percent.

Siemens gained 1.3 percent to 89.70 euros, the highest price since July 2011. Europe’s biggest engineering company appointed SAP AG’s co-Chief Executive Officer Jim Hagemann Snabe to its supervisory board and named Ralf Thomas CFO.

HeidelbergCement gained 1.4 percent to 58.20 euros as Goldman Sachs raised its rating on the cement maker to buy from sell, saying increased spending will drive growth opportunities. The stock is trading at 16.6 times projected earnings, compared with 16.5 times for the Stoxx 600 Construction and Materials Index.

Smiths Group Plc advanced 2.6 percent to 1,412 pence. The U.K. producer of security scanners increased its final dividend to 27 pence a share and announced an additional payout of 30 pence per share.

Lanxess AG fell 2.8 percent to 49.95 euros. The synthetic-rubber maker said it will cut 1,000 jobs and curb management bonuses as part of a plan to save about 100 million euros ($134 million) annually from 2015. Citigroup Inc. said the proposal will put additional pressure on the company’s cash flow in the short term. Goldman said investors may sell the stock in the absence of a more significant plan. Baader Bank AG analyst Norbert Barth, who has a sell rating on the stock, said Lanxess may lower its dividend from last year’s 1 euro per share.

-

17:00

European stocks closed in different ways: FTSE 100 6,558.82 -11.35 -0.17%, CAC 40 4,170.4 +24.89 +0.60%, DAX 8,636.06 +39.11 +0.45%

-

16:45

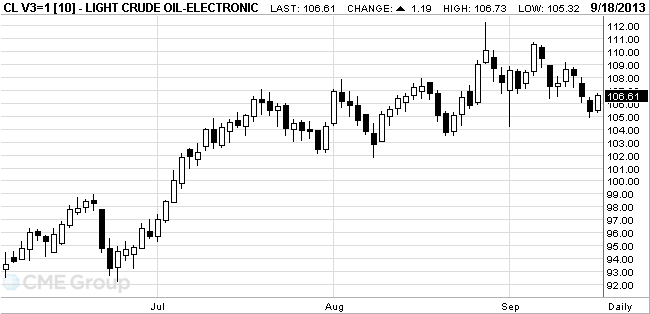

Oil rose

West Texas Intermediate crude advanced after a government report showed that

Futures rose after the Energy Information Administration said nationwide stockpiles dropped 4.37 million barrels to 355.6 million. A 1.2 million-barrel decline was projected in a Bloomberg survey. Inventories at

WTI crude for October delivery increased 98 cents, or 0.9 percent, to $106.40 a barrel at 10:42 a.m. on the New York Mercantile Exchange. The contract traded at $105.74 before the release of the report at 10:30 a.m. in

Brent oil for November settlement rose 32 cents, or 0.3 percent, to $108.51 a barrel on the London-based ICE Futures Europe exchange. The European benchmark grade’s premium to WTI slipped to as little as $2.70 a barrel, the narrowest gap since Aug. 19, as some supplies returned in Libya and concern that a U.S.-led attack on Syria would affect Middle East exports waned.

-

16:20

Gold fell to a six-week low

Gold prices fell more than 1 percent, as investors expect the Fed to reduce incentives. Market participants expect the U.S. central bank on Wednesday announced a modest - about $ 10 billion a month - reducing the amount of buying bonds from the current $ 85 billion.

Gold rose in price in recent years thanks to the policy of stimulating the central banks of several countries, reaching in 2011 a record high of $ 1,920 an ounce, but this year, some analysts have lowered forecasts for gold due to the expected reduction of incentives for the Fed. According to Goldman Sachs, by the end of the year prices will drop to $ 1,050.

Physical demand in the largest gold consumer India and China is growing slowly due to the volatility of prices. Futures in Shanghai on Wednesday fell by 1 percent.

Government of India has increased the import duty on gold jewelry and 15 percent to 10, setting it higher duty on gold to protect local jewelers.

The cost of the October gold futures on COMEX today dropped to $ 1281.80 per ounce.

-

15:30

U.S.: Crude Oil Inventories, September -4.4

-

14:45

Option expiries for today's 1400GMT cut

EUR/USD $1.3300, $1.3340, $1.3350, $1.3370/75, $1.3400, $1.3410, $1.3450

USD/JPU Y98.00, Y98.75, Y99.00(large), Y99.30/35, Y99.40, Y99.50, Y99.60, Y100.00

GBP/USD $1.5800, $1.5900, $1.5925, $1.6000

GBP/AUD A$1.7080

USD/CHF Chf0.9350

AUD/USD $0.9230, $0.9240, $0.9250, $0.9350, $0.9355

-

14:41

U.S. Stocks open: Dow 15,510.33 -19.40 -0.12%, Nasdaq 3,752.31 +6.61 +0.18%, S&P 1,705.10 +0.34 +0.02%

-

13:59

Upgrades and downgrades before the market open:

Upgrades:

Downgrades:

Procter & Gamble (PG) downgraded to Equal Weight from Overweight at Barclays

Caterpillar (CAT) downgraded to Neutral from Outperform at Robert W. Baird

Other:

AT&T (T) initiated at Outperform at Credit Suisse

Verizon (VZ) initiated at Neutral at Credit Suisse

-

13:31

U.S.: Housing Starts, mln, August 0.891 (forecast 0.923)

-

13:30

U.S.: Building Permits, mln, August 0.918 (forecast 0.950)

-

13:15

European session: the pound against the dollar has increased significantly

Data

00:00 Australia Conference Board Australia Leading Index July -0.2% +0.3%

00:30 Australia Leading Index July 0.0% +0.6%

01:30 Australia RBA Assist Gov Edey Speaks

01:30 China Property Prices, y/y August +7.5% +8.3%

08:30 United Kingdom Bank of England Minutes

09:00 Eurozone Construction Output, m/m July +0.7% +0.3%

09:00 Eurozone Construction Output, y/y July -3.0% -1.2%

09:00 Switzerland Credit Suisse ZEW Survey (Expectations) September 7.2 20.0 16.3

The dollar holds tight against the euro , as many market participants are waiting for the announcement of the results of the two-day meeting of the FOMC. It should be noted that today, the U.S. Federal Reserve is expected to begin a retreat from the ultra - loose monetary policy through the small decline in bond purchases , while stressing that interest rates will remain at a level close to zero for a long time. Most economists expect the Fed will roll monthly purchase by a modest $ 10 billion to total $ 75 billion , which would signal the beginning of the end of an unprecedented monetary expansion , the effect of which is felt throughout the world.

The Fed will announce its decision after a two-day meeting at 18:00 GMT, and half an hour later , Fed Chairman Ben Bernanke will hold a press conference. It is also planned publication of the quarterly forecast.

We also add that the course of trade no tar even have an impact on euro area data , which showed that by the end of July construction output in the euro zone rose again , although recorded at a slower pace than the previous month , but in spite of this, he showed fourth monthly increase in a row. We also add that , combined with the upward revision of indicators over the past two months , we can assume that the sector continues to recover from an unusually cold winter in much of the currency bloc .

According to the report , the July construction output rose a seasonally adjusted 0.3% ( on a monthly basis ) , compared with a revised upward figure for June and May - to the level of 0.9 % (originally 0.7%) and 0.8 % (initially 0.5 %), respectively .

The pound rose significantly against the dollar, which was associated with the publication of the protocol of the Bank of England. This month, members of the Committee of the Bank of England voted unanimously to maintain the policy unchanged. In August, some members of the Monetary Committee saw a " compelling " case for policy easing , but Minutka meeting, which was held on September 3-4 , showed that " no member believes that additional incentives would be appropriate at the present time ."

In the report , published today, also says that politicians have voted " 9-0 " for the conservation program of bond purchases at around 375 billion pounds ( 598 billion dollars) and for keeping interest rates unchanged at a record low of 0.5 percent.

In recent months, the UK economy has shown signs of strengthening , and employees of the Bank of England is now expected to rise by 0.7 percent in the quarter, compared to 0.5 percent last month . MPC, led by Mark Carney pledged to keep interest rates low for as long as the unemployment rate drops to 7 percent. Investors believe that the MPC will have to increase its key interest rate earlier than projected policy. The Bank of England also noted that there are tentative signs that the amount of spare capacity companies may start to decline.

EUR / USD: during the European session, the pair is trading in a narrow range

GBP / USD: during the European session, the pair rose to $ 1.5978

USD / JPY: during the European session, the pair fell Y9.77, then rebounded to Y99.00

At 12:30 GMT the United States , there are data on the volume of building permits issued and the number of Housing Starts in August. At 18:00 GMT the United States will present an economic forecast from the FOMC in September. At 18:00 GMT the United States will publish the FOMC decision on the basic interest rate as well as the accompanying statement will be released FOMC. At 18:30, the U.S. will be a press conference of the Federal Reserve System . At 22:45 GMT New Zealand will report on changes in the volume of GDP for the 2nd quarter . At 23:50 GMT Japan will release a report on the overall balance of foreign trade in August.

-

13:00

Orders

EUR/USD

Offers $1.3450/55, $1.3410, $1.3385/400, $1.3370

Bids $1.3325/20, $1.3305/00, $1.3290, $1.3260/50, $1.3240/30

GBP/USD

Offers stg0.8520, stg0.8460/65, stg0.8440/50, stg0.8425/30, stg0.8411

Bids stg0.8360, stg0.8350, stg0.8320, stg0.8300

AUD/USD

Offers $0.9500, $0.9470/75, $0.9440-60, $0.9415/20, $0.9400, $0.9370/80

Bids $0.9285/80, $0.9270, $0.9250, $0.9225/20

EUR/GBP

Offers stg0.8520, stg0.8460/65, stg0.8440/50, stg0.8425/30, stg0.83995

Bids stg0.8360, stg0.8350, stg0.8320, stg0.8300

EUR/JPY

Offers Y134.60, Y134.30/40, Y133.80, Y133.50, Y133.00/10, Y132.60/80

Bids Y131.60, Y131.30/20, Y130.80, Y130.00/9.80

USD/JPY

Offers Y100.60/65, Y100.20/50, Y100.00, Y99.98, Y99.40/50

Bids Y98.70/50, Y98.25/20, Y98.00, Y97.65

-

11:30

European stock indices rose

European stocks advanced as investors awaited the Federal Reserve’s decision on reducing its monthly bond purchases. U.S. index futures were little changed, while Asian shares rose.

The Stoxx Europe 600 Index gained 0.3 percent to 312.86 at 9:38 a.m. in London, after yesterday falling from its highest level since June 2008. The gauge has rallied 12 percent so far in 2013 as central banks pressed on with their supportive policies.

The Federal Open Market Committee wraps up a two-day policy meeting today, at which it will probably decide to lower its $85 billion of monthly bond purchases. Among 64 economists, 33 predict the Fed will reduce its buying of Treasuries by $5 billion or less, with 31 forecasting a cut of $10 billion or more.

Earlier this month, the median estimate of 34 economists called for a $10 billion reduction. In a July poll, half of the 54 responses predicted a $20-billion cut.

The FOMC releases both its policy statement and forecasts for economic growth, inflation and unemployment at 2 p.m. New York time. Chairman Ben S. Bernanke will hold a press conference half an hour later.

The Bank of England today released the minutes from its Sept 4-5 meeting, which showed that officials had voted unanimously to maintain policy as an improving economic outlook prompted agreement that no more stimulus was needed.

Peugeot, Europe’s second-largest carmaker, climbed 0.6 percent to 12.39 euros. The company may sell a stake to Dongfeng Motor Corp. to raise cash for expansion outside Europe, two people familiar with the matter said. Talks are at an early stage, they said.

HeidelbergCement gained 2 percent to 58.57 euros as Goldman Sachs raised its rating on the cement maker to buy from sell, saying increased spending will drive growth opportunities. The stock is trading at 16.7 times projected earnings, compared with 16.5 times for the Stoxx 600 Construction and Materials Index.

Smiths Group Plc (SMIN) advanced 4 percent to 1,431 pence, its highest price since May. The U.K. producer of security scanners announced an additional dividend of 30 pence per share, as well as increasing its final dividend to 27 pence a share.

Lanxess AG slipped 2.4 percent to 50.18 euros. The synthetic-rubber maker said it will cut 1,000 jobs and curb management bonuses as part of a plan to save about 100 million euros annually from 2015.

Citigroup Inc. said the proposal will put additional pressure on the company’s cash flow in the short term. Goldman Sachs Group Inc. said investors may sell the stock in the absence of a more significant plan. Baader

FTSE 100 6,584.32 +14.15 +0.22%

CAC 40 4,162.58 +17.07 +0.41%

DAX 8,633.92 +36.97 +0.43%

-

10:30

Option expiries for today's 1400GMT cut

EUR/USD $1.3300, $1.3340, $1.3350, $1.3370/75, $1.3400, $1.3410, $1.3450

USD/JPU Y98.00, Y98.75, Y99.00(large), Y99.30/35, Y99.40, Y99.50, Y99.60,

Y100.00

GBP/USD $1.5800, $1.5900, $1.5925, $1.6000

GBP/AUD A$1.7080

USD/CHF Chf0.9350

AUD/USD $0.9230, $0.9240, $0.9250, $0.9350, $0.9355

-

10:20

Asia Pacific stocks close

Asian stocks rose, with the regional benchmark index trading near a four-month high, before the Federal Reserve decides later today whether to slow its $85 billion of monthly asset purchases.

Nikkei 225 14,505.36 +193.69 +1.35%

Hang Seng 23,117.45 -63.07 -0.27%

S&P/ASX 200 5,238.14 -13.10 -0.25%

Shanghai Composite 2,191.85 +6.29 +0.29%

Sharp Corp. climbed 1.6 percent in Tokyo as consumer discretionary companies led gains on the Asia-Pacific benchmark index.

Kawasaki Heavy Industries Ltd. surged 4.7 percent to a six-year high amid unconfirmed reports the Japanese manufacturer secured a 180 billion yen ($1.8 billion) rail-car order.

Kansai Electric Power Co. sank 1.9 percent in Tokyo after the utility halted units at two power plants.

-

10:03

Eurozone: Construction Output, y/y, July -1.2%

-

10:02

Eurozone: Construction Output, m/m, July +0.3%

-

10:00

Switzerland: Credit Suisse ZEW Survey (Expectations), September 16.3 (forecast 20.0)

-

08:40

FTSE 100 6,573.21 +3.04 +0.05%, CAC 40 4,139.14 -6.37 -0.15% Xetra DAХ 8,609.43 +12.48 +0.15%

-

07:40

European bourses are initially seen trading higher Wednesday: the FTSE up 23, the DAX up 35 and the CAC up 13.

-

07:00

Asian session: The dollar held near the lowest in three weeks

00:00 Australia Conference Board Australia Leading Index July -0.2% +0.3%

00:30 Australia Leading Index July 0.0% +0.6%

01:30 Australia RBA Assist Gov Edey Speaks

01:30 China Property Prices, y/y August +7.5% +8.3%

The dollar held near the lowest in three weeks against the euro before the Federal Reserve concludes a two-day meeting today when policy makers will decide whether to slow its $85 billion of monthly asset purchases.

The Federal Open Market Committee will reduce Treasury purchases to $40 billion, while continuing to buy $40 billion of mortgage backed securities, according to the median estimates of economists surveyed by Bloomberg News. Fed policy makers have pledged to keep the benchmark interest rate near zero at least as long as unemployment exceeds 6.5 percent and the outlook for inflation is no more than 2.5 percent. The central bank will release its 2016 economic projections today, including the outlook for the benchmark rate.

The pound held a two-day loss against the euro before the Bank of England releases minutes of its last meeting. In the U.K., the Monetary Policy Committee on Sept. 5 held the target for asset purchases at 375 billion pounds ($596 billion) and kept its key interest rate at a record low 0.5 percent. Governor Mark Carney and colleagues provided an assessment of forward guidance last month and said they don’t intend to raise the rate until unemployment falls to 7 percent, adding that they don’t see that happening before late-2016.

The yen weakened against most major peers as stock gains curbed demand for haven assets.

EUR / USD: during the Asian session the pair is trading around the $ 1.3350

GBP / USD: during the Asian session, the pair is trading around the $ 1.5900

USD / JPY: during the Asian session the pair rose to Y99.30

The UK calendar sees the release of the BOE minutes from the September meet and will underline whether the MPC remains inline with Governor Carney on forward guidance. The numbers are expected at 0830GMT. The MPC decided to leave Bank Rate on hold at its record low level of 0.5% and quantitative easing unchanged at Stg375 billion at the meeting. It will be interesting to see if the minutes show any MPC members leaning towards voting for more QE.

-

06:22

Commodities. Daily history for Sep 17’2013:

GOLD 1,310.40 -7.40 -0.56%

OIL (WTI) 105.48 -1.11 -1.04%

-

06:21

Stocks. Daily history for Sep 17’2013:

Nikkei 225 14,311.67 -93.00 -0.65%

Hang Seng 23,180.52 -71,89 -0,31%

S & P / ASX 200 5,251.24 +3.25 +0.06%

Shanghai Composite -2,05 -45,84 2,185.56%

FTSE 100 6,578.68 -44.18 -0.67%

CAC 40 4,147.26 -4.96 -0.12%

DAX 8,599.75 -13.25 -0.15%

DJIA 15,529.70 34.95 0.23%

S&P 500 1,704.50 6.90 0.41%

NASDAQ 3,745.70 27.85 0.75%

-

06:20

Currencies. Daily history for Sep 17'2013:

(pare/closed(00:00 GMT +02:00)/change, %)

EUR/USD $1,3358 +0,17%

GBP/USD $1,5907 +0,07%

USD/CHF Chf0,9257 -0,16%

USD/JPY Y99,12 +0,04%

EUR/JPY Y132,43 +0,21%

GBP/JPY Y157,66 +0,10%

AUD/USD $0,9355 +0,38%

NZD/USD $0,8233 +0,73%

USD/CAD C$1,0296 -0,25%

-

06:00

Schedule for today, Wednesday, Sep 18’2013:

00:00 Australia Conference Board Australia Leading Index July -0.2%

00:30 Australia Leading Index July 0.0%

01:30 Australia RBA Assist Gov Edey Speaks

01:30 China Property Prices, y/y August +7.5%

08:30 United Kingdom Bank of England Minutes

09:00 Eurozone Construction Output, m/m July +0.7%

09:00 Eurozone Construction Output, y/y July -3.0%

09:00 Switzerland Credit Suisse ZEW Survey (Expectations) September 7.2 20.0

12:30 U.S. Building Permits, mln August 0.943 0.950

12:30 U.S. Housing Starts, mln August .896 0.923

14:30 U.S. Crude Oil Inventories September -0.2

14:40 Canada BOC Gov Stephen Poloz Speaks

18:00 U.S. Fed Interest Rate Decision 0.25% 0.25%

18:00 U.S. FOMC Economic Projections

18:00 U.S. FOMC Statement

18:30 U.S. Federal Reserve Press Conference

22:45 New Zealand GDP q/q Quarter II +0.3% +0.2%

22:45 New Zealand GDP y/y Quarter II +2.4% +2.3%

23:50 Japan Adjusted Merchandise Trade Balance, bln August -0.94 -0.82

-