Market news

-

22:29

Stocks. Daily history for Oct 19’2016:

(index / closing price / change items /% change)

Nikkei 225 16,998.91 +35.30 +0.21%

Shanghai Composite 3,085.32 +1.45 +0.05%

S&P/ASX 200 5,435.36 +24.61 +0.45%

FTSE 100 7,021.92 +21.86 +0.31%

CAC 40 4,520.30 +11.39 +0.25%

Xetra DAX 10,645.68 +14.13 +0.13%

S&P 500 2,144.29 +4.69 +0.22%

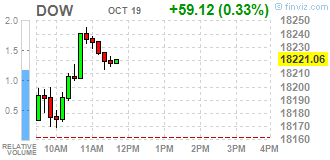

Dow Jones Industrial Average 18,202.62 +40.68 +0.22%

S&P/TSX Composite 14,840.49 +88.24 +0.60%

-

19:02

DJIA 18232.71 70.77 0.39%, NASDAQ 5250.65 6.81 0.13%, S&P 500 2146.90 7.30 0.34%

-

16:01

European stocks closed: FTSE 7021.92 21.86 0.31%, DAX 10645.68 14.13 0.13%, CAC 4520.30 11.39 0.25%

-

15:52

WSE: Session Results

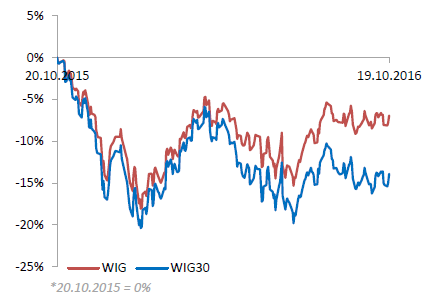

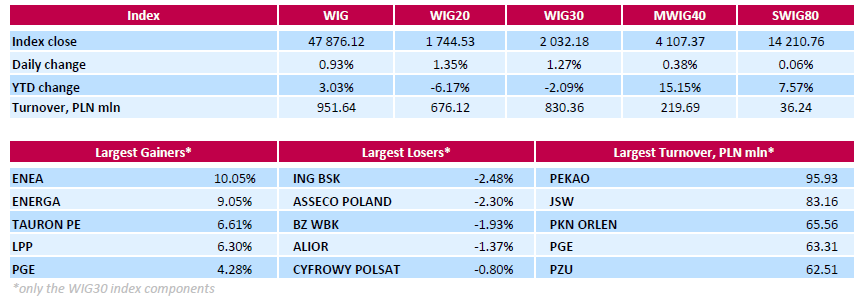

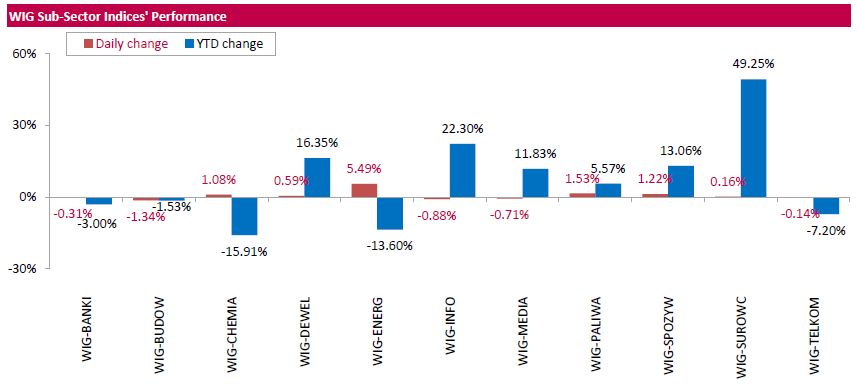

Polish equity market closed higher on Wednesday. The broad market measure, the WIG index, added 0.93%. Sector performance within the WIG Index was mixed. Utilities stocks (+5.49%) were the strongest group, while construction sector names (-1.34%) lagged behind.

The large-cap stocks' measure, the WIG30 Index, surged by 1.27%. A majority of the index components rose. All four energy generating sector's names ENEA (WSE: ENA), ENERGA (WSE: ENG), TAURON (WSE: TPE) and PGE (WSE: PGE) delivered solid advances, climbing by 4.28%-10.05%, helped by the announcement the Energy Minister Krzysztof Tchorzewski stated he did not see a need of raising capital in state-run utilities this year to get extra taxes from them. Recall, Poland's government plan, which was announced in September, implied raising capital in utilities by increasing the nominal value of their shares, which triggers the need of paying of flat-rate income tax of 19 percent on the increased nominal value. Thermal coal miner BOGDANKA (WSE: LWB) as well as two retailers LPP (WSE: LPP) and CCC (WSE: CCC) also recorded significant gains, up 4.06%, 6.3% and 3.45% respectively. On the other side of the ledger, IT-company ASSECO POLAND (WSE: ACP) and three banking names ING BSK (WSE: ING), BZ WBK (WSE: BZW) and ALIOR (WSE: ALR) bank were the major laggards, losing 1.37%-2.48%.

-

15:44

Wall Street. Major U.S. stock-indexes slightly rose

Major U.S. stock-indexes little changed on Wednesday as gains in energy and financial stocks were offset by a drop in technology shares, led by Intel. Intel (INTC) fell 4,7%, the biggest drag on all three indexes, after the chipmaker's disappointing current-quarter revenue forecast.

Most of Dow stocks in positive area (20 of 30). Top gainer - Chevron Corporation (CVX, +1.44%). Top loser - Intel Corporation (INTC, -5.60%).

Most of S&P sectors also in positive area. Top gainer - Basic Materials (+1.2%). Top loser - Healthcare (-0.3%).

At the moment:

Dow 18136.00 +72.00 +0.40%

S&P 500 2138.75 +6.75 +0.32%

Nasdaq 100 4831.00 +4.00 +0.08%

Oil 52.05 +1.43 +2.82%

Gold 1272.90 +10.00 +0.79%

U.S. 10yr 1.74 -0.01

-

13:31

U.S. Stocks open: Dow +0.10%, Nasdaq -0.06%, S&P +0.06%

-

13:17

Before the bell: S&P futures +0.20%, NASDAQ futures +0.07%

U.S. stock-index futures edged higher amid corporate earnings and as crude oil rose for a second day.

Global Stocks:

Nikkei 16,998.91 +35.30 +0.21%

Hang Seng 23,304.97 -89.42 -0.38%

Shanghai 3,085.32 +1.45 +0.05%

FTSE 7,000.60 +0.54 +0.01%

CAC 4,512.91 +4.00 +0.09%

DAX 10,644.37 +12.82 +0.12%

Crude $51.00 (+1.41%)

Gold $1272.40 (+0.75%)

-

12:56

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

26.54

0.03(0.1132%)

967

ALTRIA GROUP INC.

MO

62.65

-0.01(-0.016%)

505

Amazon.com Inc., NASDAQ

AMZN

821

3.35(0.4097%)

8609

American Express Co

AXP

60.45

0.37(0.6158%)

1407

Apple Inc.

AAPL

117.41

-0.06(-0.0511%)

135776

AT&T Inc

T

39.37

0.01(0.0254%)

665

Barrick Gold Corporation, NYSE

ABX

16.64

0.27(1.6494%)

64432

Chevron Corp

CVX

102.3

0.51(0.501%)

948

Citigroup Inc., NYSE

C

49.13

0.14(0.2858%)

1310

Facebook, Inc.

FB

128.71

0.14(0.1089%)

33032

Ford Motor Co.

F

11.9

0.01(0.0841%)

8248

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

9.85

0.13(1.3375%)

38358

General Electric Co

GE

29

0.02(0.069%)

2922

Goldman Sachs

GS

172.78

0.15(0.0869%)

4830

Google Inc.

GOOG

797.94

2.68(0.337%)

2023

Intel Corp

INTC

36

-1.75(-4.6358%)

1468938

International Business Machines Co...

IBM

151

0.28(0.1858%)

1852

Johnson & Johnson

JNJ

115.5

0.09(0.078%)

4961

JPMorgan Chase and Co

JPM

67.85

0.15(0.2216%)

3800

McDonald's Corp

MCD

112.04

0.79(0.7101%)

701

Microsoft Corp

MSFT

57.5

-0.16(-0.2775%)

19746

Nike

NKE

51.31

0.09(0.1757%)

120

Pfizer Inc

PFE

32.99

0.30(0.9177%)

4444

Procter & Gamble Co

PG

87

0.2195(0.2529%)

1276

Starbucks Corporation, NASDAQ

SBUX

52.9

0.29(0.5512%)

7287

Tesla Motors, Inc., NASDAQ

TSLA

199.5

0.40(0.2009%)

14337

The Coca-Cola Co

KO

42.05

0.08(0.1906%)

1200

Twitter, Inc., NYSE

TWTR

16.9

0.07(0.4159%)

84153

UnitedHealth Group Inc

UNH

143.35

-0.04(-0.0279%)

157

Verizon Communications Inc

VZ

50.11

-0.16(-0.3183%)

1191

Visa

V

81.6

0.02(0.0245%)

1578

Walt Disney Co

DIS

91

-0.17(-0.1865%)

810

Yahoo! Inc., NASDAQ

YHOO

42.11

0.43(1.0317%)

8385

Yandex N.V., NASDAQ

YNDX

20

0.26(1.3171%)

1100

-

12:54

Upgrades and downgrades before the market open

Upgrades:

Twitter (TWTR) upgraded to Hold from Sell at Loop Capital

Downgrades:

Other:

Intel (INTC) target lowered to $37 from $38 at RBC Capital

Intel (INTC) target lowered to $42 from $43 at Needham

Yahoo! (YHOO) target raised to $48 from $44 at Susquehanna

Yahoo! (YHOO) target raised to $42 from $38 at Mizuho

Yahoo! (YHOO) target raised to $45 from $39 at RBC Capital

Goldman Sachs (GS) target raised to $170 from $160 at RBC Capital

Hewlett Packard Enterprise (HPE) target raised to $26 at Needham

Starbucks (SBUX) target lowered to $64 at RBC Capital Mkts

UnitedHealth (UNH) target raised to $169 at Mizuho

DuPont (DD) initiated with a Buy at Nomura

-

12:11

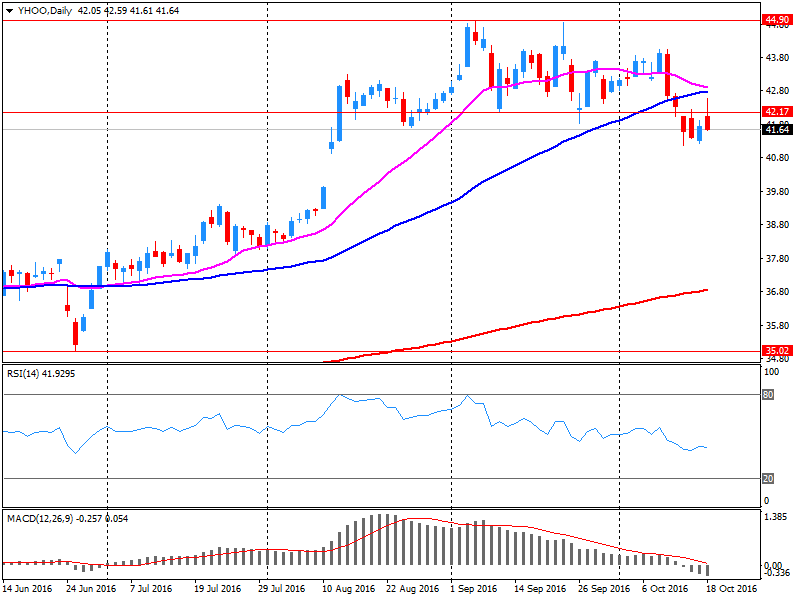

Company News: Yahoo! (YHOO) Q3 EPS beat analysts’ estimates

Yahoo! reported Q3 FY 2016 earnings of $0.20 per share (versus $0.15 in Q3 FY 2015), beating analysts' consensus estimate of $0.14.

The company's quarterly revenues amounted to $0.857 bln (-14.6% y/y), slightly missing analysts' consensus estimate of $0.861 bln.

The company issued downside guidance for Q4, projecting Q4 revenues of $0.88-0.92 bln versus analysts' consensus estimate of $0.939 bln.

YHOO rose to $42.20 (+1.25%) in pre-market trading.

-

12:00

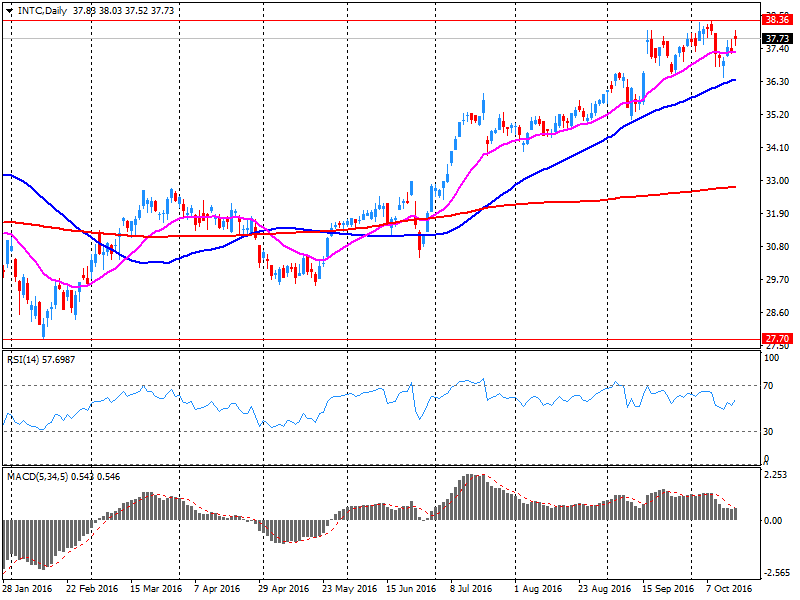

Company News: Intel (INTC) Q3 results beat analysts’ estimates

Intel reported Q3 FY 2016 earnings of $0.80 per share (versus $0.64 in Q3 FY 2015), beating analysts' consensus estimate of $0.72.

The company's quarterly revenues amounted to $15.778 bln (+9.1% y/y), beating analysts' consensus estimate of $15.605 bln.

The company also issued in-line guidance for Q4, projecting Q4 revenues of $15.2-16.2 bln versus analysts' consensus estimate of $15.88 bln; gross margin 63% +/- a couple percent. This revenue forecast is lower than the average seasonal increase for the fourth quarter.

INTC fell to $36.10 (-4.34%) in pre-market trading.

-

10:49

Major European stock indices trading lower

European stock indices show a negative trend, as investors assessed mixed Chinese statistical data, as well as preparing for the ECB meeting. However, some support had moderate increase in oil prices.

As expected, China's GDP grew by 6.7% in the 3rd quarter. A similar increase was observed in the 2nd quarter. However, although the pace of growth was in line with expectations, the signs of the weakness of exports and investments was recorded together with the growth in sales of new homes. These promote the growth of fears of further slowdown. Early next year pressure on the economy will increase, since the real estate market cycle will go on the decline.

The composite index of the largest companies in the region Stoxx Europe 600 trading lower by 0.2 percent. Yesterday the index recorded the maximum increase in nearly a month on optimism that monetary policy will remain favorable for growth.

Shares of Reckitt Benckiser Group fell 2.7 percent after the company reported disappointing figures in terms of sales in the third quarter.

Quotes of Travis Perkins Plc fell 5.1 percent as adjusted annual earnings forecast was slightly below consensus.

The cost of ASML Holding NV shares rose 3.9 percent after Europe's biggest maker of semiconductor equipment announced the updated projections of profitability in the 4th quarter, which exceeded analysts' expectations.

Carrefour share rose 1.6 percent as France's largest retailer reported higher earnings in the third quarter, than experts predicted.

At the moment:

FTSE 100 -7.81 -0.11% 6992.25

DAX -19.49 10612.06 -0.18%

CAC 40 -4.86 4504.05 -0.11%

-

07:43

Major stock markets trading in the green zone: FTSE flat, DAX -0.1%, CAC40 + 0.1%, FTMIB flat, IBEX + 0.3%

-

06:44

Positive start of trading expected on the major stock exchanges in Europe: DAX futures flat, CAC40 + 0.1%, FTSE + 0.2%

-

05:30

Global Stocks

European stocks slumped Monday, led by a pullback in oil shares, as investors entered the trading week with the dollar sitting at a seven-month high while they waited to hear what's next for monetary policy at the European Central Bank.

U.S. stocks on Tuesday gained as the latest round of corporate earnings came in ahead of Wall Street's estimates, helping to buoy market sentiment. The S&P 500 SPX, +0.62% rose 13 points, or 0.6%, to finish at 2,139 while the Dow Jones Industrial Average DJIA, +0.42% climbed 75 points, or 0.4%, to close at 18,161. The Nasdaq Composite COMP, +0.85% advanced 44 points, or 0.9%, to finish at 5,243. Closely watched companies like Goldman Sachs Group Inc. GS, +2.15% Netflix Inc.

Asian shares were broadly higher early Wednesday, tracking overnight gains on Wall Street, while key data out of China met market expectations. The world's second-biggest economy expanded 6.7% in the third quarter from a year earlier, matching growth in the previous quarter, official data showed Wednesday. The figure was also in line with a forecast by economists polled by The Wall Street Journal.

-