Noticias del mercado

-

22:08

US stocks closed

The increased prospect that six years of near-zero borrowing costs in the U.S. may end next month rippled through global markets, as companies hurt most by the strengthening dollar led a selloff in American equities and bonds fell with emerging-market assets.

The Standard & Poor's 500 Index sank the most in a month, with large caps from Caterpillar Inc. to Nike Inc. pacing the drop. European stocks lost 1.1 percent. The dollar traded near the highest in a decade, as a gauge of emerging-market currencies slumped toward a five-week low. Treasury 10-year note rates climbed to 2.34 percent.

Global investors continue to adjust to the increased likelihood that America's benchmark rate will rise this year, a move that would end an unprecedented era of record-low borrowing costs. Concern that capital outflows from developing nations will worsen sent emerging assets lower, while dollar-denominated resources slumped with shares of American multinational companies. Treasuries pared losses with gold on haven demand.

Investors shrugged off the threat of higher rates on Friday, focusing instead on a blowout jobs report that signaled the U.S. economy may be ready to withstand tighter monetary policy. That sentiment reversed Monday in the absence of any additional data and after American equities ended last week near the highest level in three months.

"People sort-of stewed on it over the weekend that we're facing a rate hike in December," said Robert Pavlik, who helps oversee $9.1 billion as chief market strategist at Boston Private Wealth. "I don't think it's the 25 basis points that's necessarily leading the market down, but what comes after. How fast and furious do the rate hikes come now that this cheap money environment is coming to an end?"

The S&P 500 fell 1.2 percent at 2:54 p.m. in New York, the most since Oct. 2. The gauge is coming off its longest run of weekly gains this year, a streak that pushed it within 1.5 percent below its May record.

Consumer-discretionary stocks had the biggest declines among 10 groups in the S&P 500, falling 1.9 percent. Macy's Inc. and Kohl's Corp. declined more than 5.5 percent after Citigroup Inc. cut its earnings estimates for the companies, saying the industry is suffering from a sales slowdown and inventory glut.

There is an "absence of any real, compelling reason to step in and buy a lot right now," Peter Tuz, who helps manage $400 million as president of Chase Investment Counsel Corp. in Charlottesville, Virginia. "I don't think anyone came into work today figuring that they had to load up on stocks."

European stocks fell, after rising four times in the past five days, as investors weighed the outlook for global economic growth and stimulus. The Stoxx Europe 600 Index lost 1.1 percent. Shares of exporters fell after worse-than-forecast Chinese trade data.

-

21:00

DJIA 17705.76 -204.57 -1.14%, NASDAQ 5084.25 -62.87 -1.22%, S&P 500 2074.93 -24.27 -1.16%

-

20:20

American focus: the US dollar moderately lower against major currencies

The US dollar was moderately lower against other major currencies in subdued trade as investors take profits after a rally on Friday to seven-month high on positive US statistics on employment in October.

Dollar fully appreciated after the US Labor Department reported on Friday that the US economy added 271,000 jobs last month against the expected 182,000, the highest since December. The unemployment rate fell to 7.5-year low of 5.0%.

Reliable figures increased the chances that the Fed will raise interest rates at the December meeting, with the result that the dollar will become more attractive for investors looking for profit.

Data on jobs came after the Fed chief Janet Yellen said that the economy is showing good momentum and that the rise of interest rates in December, is a "real possibility" if it will save the vector of development.

Euro moved away from session highs after Livesquawk, quoting informed sources, reported that the ECB is now considering the option of reducing the interest rates on deposits in December, contrary to most forecasts suggesting an increase in QE.

According to the source, currently an emerging consensus on the issue of lowering rates, and the debate is around the size of this reduction. Markets expect the ECB to increase the size of the program QE (now it is 60 billion euros per month).

Reduced rates on deposits would make it more accessible to a greater number of bond purchases under the program of QE.

Markets were assessed comments by the Fed Rosengren, who commented on the latest data and prospects for December's increase.

The president of the Federal Reserve Bank of Boston Eric Rosengren said on Monday that the improvement in the US economy may increase the likelihood of raising key interest rates at the next meeting of the Federal Reserve in December.

"December may be appropriate time to raise rates if the economic situation will correspond to forecasts", - stated in the materials prepared for the speech Rosengren on Monday before the Chamber of Commerce in Portsmouth.

Rosengren pointed to the wording of the Fed statement after a meeting in October, which made it clear that interest rates in December may be increased if Fed officials see the progress in achieving the objectives of the central bank to achieve price stability and employment. Rosengren added that he generally supports the decision.

"I want to emphasize that recent economic data were positive and reflect real improvement in the economy", - said in the text of the speech.

Previously, support for the euro have data for the euro area and Germany. As it became known today, foreign trade surplus in Germany in September rose to 22.9 billion euros. Thus the index jumped in August against 1.5. Exports from Germany amounted to 105.9 billion euros, 4.4% more than in September 2014. With the exception of seasonal and calendar factors exports compared with the previous month increased by 2.6%. Imports increased by 3.9% compared to the same period in 2014 - up to 83 billion euros. With the exception of seasonal and calendar factors imports in September compared to August increased by 3.6%. Economists had expected a surplus of 20 billion euros.

Meanwhile, the Sentix survey results showed that the mood among investors in the euro zone improved considerably in November, exceeding in this case, despite a migration crisis in Europe. According to the index of investor confidence rose in November to a level of 15.1 points compared to 11.7 points in October. The latter value was the highest for the last three months. Economists had expected the index to improve to only 12.7 points. It also became known that the index of current conditions rose in November 16 from 13 in the previous month. Likewise, the expectations index rose to 14.3 points from 10.5 points in October.

-

18:55

Wall Street. Major U.S. stock-indexes fell

Major U.S. stock-indexes fell 1% on Monday, their biggest fall in six weeks, as weak Chinese trade data and a cut in the OECD's global growth forecast sparked fears about a global economic slowdown. Data from China, one of the one of the U.S.'s biggest trade partners, showed a fall in exports and imports in October left it with a record high trade surplus. The Organisation for Economic Co-operation and Development cut its 2015 global growth forecast again.

All Dow stocks in negative area (30 of 30). Top looser - Caterpillar Inc. (CAT, -2.88%).

All S&P index sectors also in negative area. Top looser - Services (-1.9%).

At the moment:

Dow 17657.00 -186.00 -1.04%

S&P 500 2069.00 -24.75 -1.18%

Nasdaq 100 4638.50 -64.50 -1.37%

Oil 43.81 -0.48 -1.08%

Gold 1089.10 +1.40 +0.13%

U.S. 10yr 2.34 +0.01

-

18:18

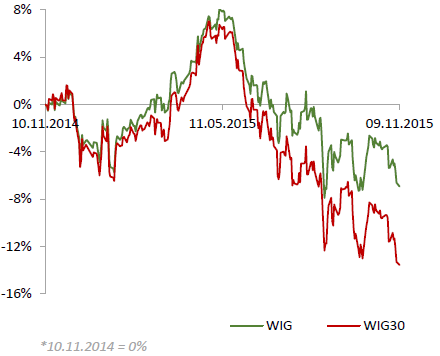

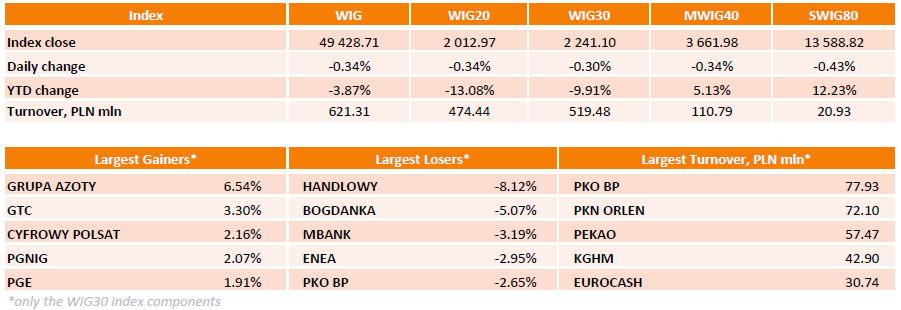

WSE: Session Results

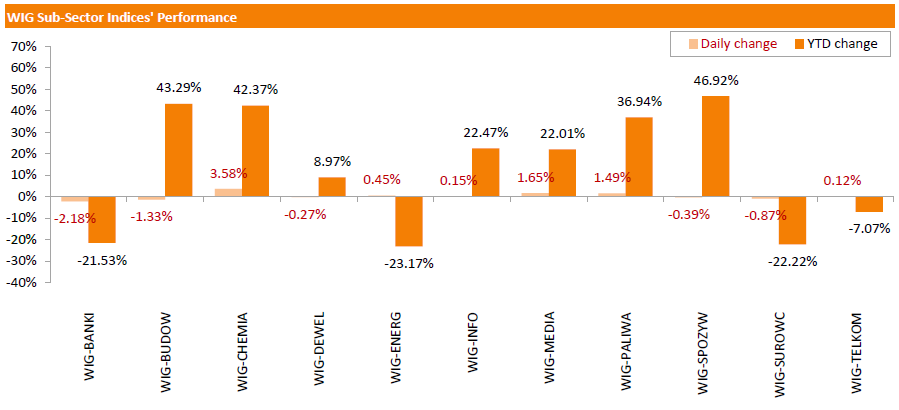

Polish equity market declined on Monday. The broad market measure, the WIG Index, slumped by 0.34%. Sector performance in the WIG Index was mixed. Banking sector (-2.18%) recorded the sharpest decline as the Polish president's office announced on Friday that President Andrzej Duda believes it would be equitable if banks bore between 50% and 90% of the cost of conversion of Swiss franc-denominated mortgages into zlotys at historical rates.

The large-cap stocks fell by 0.3%, as measured by the WIG30 Index. Within the index components, HANDLOWY (WSE: BHW) led the decliners, tumbling 8.12% on the back of worse-than-expected 3Q earnings (its Q3 profit was PLN140.9 mln versus consensus of PLN145.6 mln). It was followed by BOGDANKA (WSE: LWB), sliding down 5.07%. The other biggest losers were MBANK (WSE: MBK), ENEA (WSE: ENA), PKO BP (WSE: PKO), KERNEL (WSE: KER) and CCC (WSE: CCC), losing 2.24%-3.19%. On the other side of the ledger, GRUPA AZOTY (WSE: ATT) led the risers, climbing by 6.54% as the company's 3Q results beat analysts' expectations (its revenues accounted PLN 2401 mln versus consensus of PLN 2179 mln and its net income was PLN 73.6 mln versus consensus of PLN 39.8 mln). GTC (WSE: GTC), CYFROWY POLSAT (WSE: CPS) and PGNIG (WSE: PGN) were also noteworthy performers, gaining 3.3%, 2.16% and 2.07% respectively.

-

18:00

European stocks closed: FTSE 6295.16 -58.67 -0.92%, DAX 10815.45 -172.58 -1.57%, CAC 40 4911.17 -72.98 -1.46%

-

16:46

Bank of France’s new governor and European Central Bank (ECB) Governing Council member Francois Villeroy de Galhau: the inflation expectations in the Eurozone is still too low and uncertain

Bank of France's new governor and European Central Bank (ECB) Governing Council member Francois Villeroy de Galhau said in an interview with the German newspaper Handelsblatt that the inflation expectations in the Eurozone is still too low and uncertain since summer as concerns over the

"The (inflation) expectations are still too low, and uncertain since the summer," he noted.

Galhau pointed that the ECB will add further stimulus measures if needed.

"There are still margins to make monetary policy more effective -- the instruments are available," he said.

-

16:27

Chairman of the state-owned Saudi Arabian Oil Company Khalid al-Falih: the country will not cut its oil production

Chairman of the state-owned Saudi Arabian Oil Company (Saudi Aramco), Khalid al-Falih, said in an interview with the Financial Times that the country will not cut its oil production.

"The only thing to do now is to let the market do its job. There have been no conversations here that say we should cut production now that we've seen the pain," he said.

-

16:12

European Central Bank purchases €12.93 billion of government and agency bonds last week

The European Central Bank (ECB) purchased €12.93 billion of government and agency bonds under its quantitative-easing program last week.

The European Central Bank's (ECB) President Mario Draghi said at a press conference in October that the value of the ECB's asset-buying programme will be discussed at the monetary policy meeting in December.

ECB'S asset buying programme is intended to run to September 2016.

The ECB bought €1.38 billion of covered bonds, and €176 million of asset-backed securities.

-

16:01

U.S.: Labor Market Conditions Index, October 1.6

-

15:35

U.S. Stocks open: Dow -0.46%, Nasdaq -0.46%, S&P -0.42%

-

15:29

Before the bell: S&P futures -0.01%, NASDAQ futures 0.00%

U.S. stock-index futures were flat.

Global Stocks:

Nikkei 19,642.74 +377.14 +1.96%

Hang Seng 22,726.77 -140.56 -0.61%

Shanghai Composite 3,647.14 +57.10 +1.59%

FTSE 6,354.29 +0.46 +0.01%

CAC 4,963.63 -20.52 -0.41%

DAX 10,970.49 -17.54 -0.16%

Crude oil $44.64 (+0.79%)

Gold $1091.60 (+0.36%)

-

15:10

OECD’s leading composite leading indicator declines to 99.8 in September

The Organization for Economic Cooperation and Development (OECD) released its leading indicators on Monday. The composite leading indicator decreased to 99.8 in September from 99.9 in August.

The leading indicators of Canada, France and Italy rose in September, while the indicators of China, the U.S., Japan, Germany and the U.K. declined.

Eurozone's leading indicator remained unchanged in September.

-

15:05

Labour cash earnings in Japan rise 0.6% in September

Japan's Ministry of Health, Labour and Welfare released its labour cash earnings data on Monday. Labour cash earnings in Japan rose at an annual rate of 0.6% in September, after a 0.4% rise in August.

August's figure was revised down from a 0.5% gain.

Summer bonuses in the June-August period slid 2.8% year-on-year. It was the biggest decline since 2009.

Total real wages climbed 0.5% in September, after a 0.1% gain in August.

-

14:57

Wall Street. Stocks before the bell

(company / ticker / price / change, % / volume)

General Motors Company, NYSE

GM

36.05

0.84%

8.8K

Yahoo! Inc., NASDAQ

YHOO

34.35

0.44%

3.3K

McDonald's Corp

MCD

113.7

0.34%

2.8K

Nike

NKE

132.2

0.32%

0.9K

JPMorgan Chase and Co

JPM

68.66

0.30%

0.2K

Hewlett-Packard Co.

HPQ

14.05

0.29%

2.0K

Barrick Gold Corporation, NYSE

ABX

7.07

0.28%

3.7K

Citigroup Inc., NYSE

C

56

0.23%

12.1K

Twitter, Inc., NYSE

TWTR

28.33

0.18%

32.0K

Goldman Sachs

GS

199.5

0.17%

5.5K

Apple Inc.

AAPL

121.25

0.16%

92.6K

Amazon.com Inc., NASDAQ

AMZN

660.25

0.13%

10.7K

Facebook, Inc.

FB

107.16

0.06%

60.5K

Exxon Mobil Corp

XOM

83.77

0.04%

1.8K

ALTRIA GROUP INC.

MO

57.09

0.00%

15.5K

AMERICAN INTERNATIONAL GROUP

AIG

61.9

-0.05%

37.4K

International Business Machines Co...

IBM

138.15

-0.07%

1.1K

Home Depot Inc

HD

125.88

-0.08%

9.7K

Starbucks Corporation, NASDAQ

SBUX

61.7

-0.11%

0.2K

Intel Corp

INTC

33.8

-0.12%

0.6K

Visa

V

78.65

-0.13%

1.3K

Ford Motor Co.

F

14.5

-0.14%

0.5K

E. I. du Pont de Nemours and Co

DD

66

-0.17%

1.9K

Verizon Communications Inc

VZ

45.7

-0.17%

0.4K

AT&T Inc

T

33.09

-0.21%

8.3K

Procter & Gamble Co

PG

75.4

-0.22%

5.1K

Wal-Mart Stores Inc

WMT

58.65

-0.22%

1.8K

Walt Disney Co

DIS

115.35

-0.27%

5.8K

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

10.72

-0.28%

23.1K

Chevron Corp

CVX

93.72

-0.33%

0.3K

Microsoft Corp

MSFT

54.73

-0.35%

14.0K

Cisco Systems Inc

CSCO

28.34

-0.39%

8.9K

General Electric Co

GE

29.8

-0.40%

43.2K

Caterpillar Inc

CAT

73.52

-0.43%

12.6K

Johnson & Johnson

JNJ

101.44

-0.47%

0.2K

Pfizer Inc

PFE

33.76

-0.49%

29.2K

Tesla Motors, Inc., NASDAQ

TSLA

231.1

-0.54%

1.8K

ALCOA INC.

AA

9.04

-0.55%

62.0K

American Express Co

AXP

73.73

-0.77%

0.5K

UnitedHealth Group Inc

UNH

113.9

-0.79%

3.9K

Yandex N.V., NASDAQ

YNDX

15.67

-1.01%

1.0K

HONEYWELL INTERNATIONAL INC.

HON

102

-1.92%

0.1K

-

14:51

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Alcoa (AA) downgraded to Neutral from Buy at Nomura

Other:

Walt Disney (DIS) target raised to $129 from $123 at Argus

Wal-Mart (WMT) initiated with a Neutral at Citigroup

-

14:50

Option expiries for today's 10:00 ET NY cut

USD/JPY 122.00 (USD 305m)

EUR/USD 1.0800 (EUR 909m)

GBP/USD 1.5400 (GBP 478m)

USD/CHF 0.9925 (USD 525m)

USD/CAD 1.3200 (USD 610m) 1.3300 (825m)

AUD/USD 0.7000 ( AUD 391m)

NZD/USD 0.6600 (NZD 915m)

-

14:34

OECD downgrades its global growth outlook

The Organization for Economic Cooperation and Development (OECD) released its growth forecast on Monday. The OECD downgraded its global growth outlook.

"The slowdown in global trade and the continuing weakness in investment are deeply concerning. Robust trade and investment and stronger global growth should go hand in hand," the OECD Secretary-General Angel Gurria.

The OECD expect the global economy to grow at 2.9% in 2015, down from the previous estimate of 3.0%, and at 3.3% in 2016, down from the previous estimate of 3.6%.

The global economy is expected to expand 3.6% in 2017.

The U.S. economy is expected to grow at 2.4% in 2015, 2.5% in 2016, down from the previous estimate of 2.6%, and 2.4% in 2017.

Japan's economy is expected to grow at 0.6% in 2015 and at 1.0% in 2016, down from its previous estimate of 1.2%, and 0.5% for 2017.

Eurozone's forecasts were downgraded to 1.5% in 2015 from the previous estimate of 1.6% and to 1.8% in 2016 from the previous estimate of 1.9%. Eurozone's economy is expected to expand 1.9%.

China is expected to expand at 6.8% in 2015, up from the previous estimate of 6.7%. Growth forecast for 2016 remained unchanged at 6.5%, while 2017 forecast was 6.2%.

-

14:22

Housing starts in Canada declines to a seasonally adjusted annualized rate of 198,065 units in October

The Canada Mortgage and Housing Corporation (CMHC) released housing starts data on Monday. Housing starts in Canada fell to a seasonally adjusted annualized rate of 198,065 units in October from a revised reading of 231,304 units in September.

Housing starts were driven by a rise in new condominium and rental starts.

"Rental starts across urban centres are poised to reach their highest level since 1992 due to low vacancy rates in recent years," the CMHC's Chief Economist Bob Dugan said.

-

14:14

Canada: Housing Starts, October 198.1 (forecast 200)

-

14:00

Foreign exchange market. European session: the euro traded higher against the U.S. dollar on the positive economic data from the Eurozone

Economic calendar (GMT0):

(Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual)

00:30 Australia ANZ Job Advertisements (MoM) October 3.8% Revised From 3.9% 0.4%

01:30 Japan Labor Cash Earnings, YoY September 0.4% Revised From 0.5% 0.6%

07:00 Germany Current Account September 13.3 Revised From 12.3 25.1

07:00 Germany Trade Balance September 15.3 Revised From 15.4 22.9

09:30 Eurozone Sentix Investor Confidence November 11.7 15.1

13:15 Canada Housing Starts October 230.7 200

The U.S. dollar traded mixed against the most major currencies in the absence of any U.S. major economic reports.

The greenback declined on profit taking after the Friday's significant rise on the U.S. labour market.

The euro traded higher against the U.S. dollar on the positive economic data from the Eurozone. Market research group Sentix released its investor confidence index for the Eurozone on Monday. The index climbed to 15.1 in November from 11.7 in October. It was the lowest level since February.

A reading above 0.0 indicates optimism, below indicates pessimism.

"Reason for rising economic expectations is gaining confidence in Asian markets," Sentix said in its statement.

Destatis released its trade data for Germany on Monday. Germany's seasonally adjusted trade surplus declined to €19.4 billion in September from 19.4 in August.

Exports rose 4.4% year-on-year in September, while imports climbed 3.9% year-on-year.

On a yearly basis, German exports increased at a seasonally and calendar-adjusted 2.6% in September, while imports rose by 3.6%.

Germany's current account surplus was at €25.1 billion in September, up from €13.3 billion in August. August's figure was revised up from €12.3 billion.

The British pound traded higher against the U.S. dollar in the absence of any major economic reports from the U.K.

The Canadian dollar traded higher against the U.S. dollar ahead the Canadian housing starts data. Housing starts in Canada are expected to drop 200,000 in October from 230,700 in September.

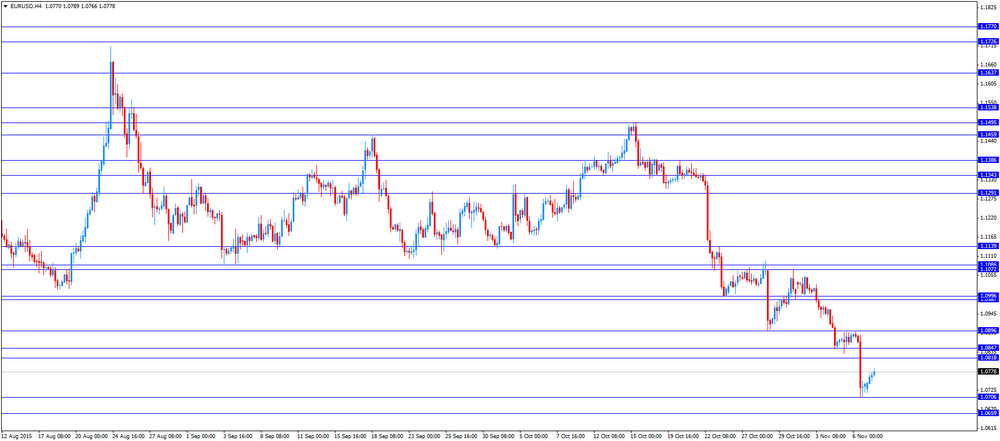

EUR/USD: the currency pair rose to $1.0789

GBP/USD: the currency pair was up to $1.5114

USD/JPY: the currency pair increased to Y123.60

The most important news that are expected (GMT0):

13:15 Canada Housing Starts October 230.7 200

15:00 U.S. Labor Market Conditions Index October 0

23:50 Japan Current Account, bln September 1653 2235.2

-

13:45

Orders

EUR/USD

Offers 1.0780-85 1.0800 1.0820 1.0845-50 1.0885 1.0900 1.0925-30 1.0960 1.0980 1.1000

Bids 1.0745-50 1.0725-30 1.0700 1.0685 1.0665 1.0650 1.0630 1.0600

GBP/USD

Offers 1.5085 1.5100 1.5120 1.5140 1.5175-80 1.5200 1.5220 1.5245-50

Bids 1.5060 1.5045 1.5025-30 1.5000 1.4985 1.4965 1.4950 1.4930 1.4900

EUR/GBP

Offers0.7150 0.7170 0.7185 0.7200 0.7225-30 0.7250 0.7275 0.7300

Bids 0.7130-35 0.7100 0.7085 0.7050 0.7030-35 0.7020 0.7000

EUR/JPY

Offers 133.00 133.20 133.50-60 133.75-80 134.00 134.30 134.50

Bids 132.60 132.25-30 132.00 131.80 131.50 131.30 131.00

USD/JPY

Offers 123.50 123.75-80 124.00 124.30 124.50 124.75 125.00

Bids 123.20-25 123.00 122.80 122.50 122.25 122.00 121.80 121.50-60

AUD/USD

Offers 0.7075-80 0.7100 0.7125-30 0.7150 0.7180-85 0.7200 0.7220 0.7250

Bids 0.7035-40 0.7020 0.7000 0.6985 0.6965 0.6950 0.6930 0.6900

-

13:09

Greek industrial production declines 1.8% in September

The Hellenic Statistical Authority released its preliminary industrial production data for Greece on Monday. Greek industrial production fell 1.8% in September.

On a yearly basis, industrial production in Greece increased at an adjusted rate of 2.8% in September, after a 4.1% rise in August. August's figure was revised down from a 4.5% gain.

Production in the manufacturing sector rose at an annual rate of 2.6% in September, output in the mining and quarrying sector slid 4.4%, while electricity production jumped by 6.3%.

-

12:55

Building permits in Canada drops 6.7% in September

Statistics Canada released housing market data on Friday. Building permits in Canada fell 6.7% in September, missing expectations for a 1.3% rise, after a 3.6% drop in August. August's figure was revised up from a 3.7% decrease.

The decline was mainly driven by lower construction intentions for residential buildings and commercial structures in Ontario.

Building permits for non-residential construction gained 1.6% in September, while permits in the residential sector slid 11.6%.

-

12:44

Canada’s unemployment rate falls to 7.0%in October

Statistics Canada released the labour market data on Friday. Canada's unemployment rate fell to 7.0% in October from 7.1% in September. Analysts had expected the unemployment rate to remain unchanged at 7.1%.

The increase was driven by higher labour participation. The labour participation rate increased slightly to 66.0% in October from 65.9% in September.

The number of employed people climbed by 44,400 jobs in October, beating expectations for a rise of 10,000 jobs, after a 12,100 increase in September.

The increase was driven by a rise in full-time work. Full-time employment was up by 14,587 in October, while part-time employment increased by 3,436 jobs.

The Bank of Canada monitors closely the labour participation rate.

-

12:23

Bank of France expects the country’s economy to expand at 0.4% in the fourth quarter

The Bank of France released its gross domestic product (GDP) forecasts for France on Monday. French economy is expected to expand at 0.4% in the fourth quarter.

The economy is expected to grow 0.2% in the third quarter.

The manufacturing business confidence index increased to 99 in October 98 in September, driven by rises in the automobile and chemical sectors. Services companies expect an increase in activity in November.

The services business sentiment index rose to 98 in October from 97 in September. Services companies expect a rise in activity in November.

The construction business sentiment index was up to 96 in October from 95 in September.

-

12:10

NIESR’s gross domestic product rises by 0.6% in three months to October

The National Institute of Economic and Social Research (NIESR) released its estimate of gross domestic product (GDP) for the U.K. on Friday. The GDP estimate rose by 0.6% in three months to October, in line with forecasts, after a 0.5% growth in three months to September.

"This implies that reasonable economic growth has continued into the fourth quarter of 2015," the NIESR said.

-

12:05

China's trade surplus climbs to $61.64 billion in October

The Chinese Customs Office released its trade data on Sunday. China's trade surplus rose to $61.64 billion in October from $60.34 billion in September.

Exports fell at an annual rate of 6.9% in October, while imports slid at an annual rate of 18.8%, the twelfth consecutive decline.

-

12:00

European stock markets mid session: stocks traded mixed on the weak Chinese trade data

Stock indices traded mixed on the weak Chinese trade data. The Chinese Customs Office released its trade data on Sunday. Exports fell at an annual rate of 6.9% in October, while imports slid at an annual rate of 18.8%, the twelfth consecutive decline.

Meanwhile, the economic data from the Eurozone was positive. Market research group Sentix released its investor confidence index for the Eurozone on Monday. The index climbed to 15.1 in November from 11.7 in October. It was the lowest level since February.

A reading above 0.0 indicates optimism, below indicates pessimism.

"Reason for rising economic expectations is gaining confidence in Asian markets," Sentix said in its statement.

Destatis released its trade data for Germany on Monday. Germany's seasonally adjusted trade surplus declined to €19.4 billion in September from 19.4 in August.

Exports rose 4.4% year-on-year in September, while imports climbed 3.9% year-on-year.

On a yearly basis, German exports increased at a seasonally and calendar-adjusted 2.6% in September, while imports rose by 3.6%.

Germany's current account surplus was at €25.1 billion in September, up from €13.3 billion in August. August's figure was revised up from €12.3 billion.

Current figures:

Name Price Change Change %

FTSE 100 6,356.02 +2.19 +0.03 %

DAX 10,952.71 -35.32 -0.32 %

CAC 40 4,956.6 -27.55 -0.55 %

-

11:54

St. Louis Fed President James Bullard: the risk of the slowdown in China and other concerns over the global economy, which led to the delay of the Fed’s interest rate hike in September, almost dissipated

St. Louis Fed President James Bullard said on Friday that the risk of the slowdown in China and other concerns over the global economy, which led to the delay of the Fed's interest rate hike in September, almost dissipated.

"The probability of a hard landing in China is no higher today than it was earlier this year," he noted.

Regarding the U.S. economy, Bullard said that U.S. labour markets have largely normalized, and it is likely that the inflation will return to 2% target when oil prices will stabilise.

-

11:46

Sentix investor confidence index for the Eurozone is up to 15.1 in November

Market research group Sentix released its investor confidence index for the Eurozone on Monday. The index climbed to 15.1 in November from 11.7 in October. It was the lowest level since February.

A reading above 0.0 indicates optimism, below indicates pessimism.

"Reason for rising economic expectations is gaining confidence in Asian markets," Sentix said in its statement.

The current conditions index rose to 16.0 in November from 13.0 in October.

The expectations index jumped to 14.3 in November from 10.5 in October from 12.3 in September.

German investor confidence index increased to 20.1 from 17.8.

-

11:37

European Central Bank Governing Council member Ardo Hansson: there is no need for further stimulus measures

The European Central Bank (ECB) Governing Council member Ardo Hansson said in an interview with Bloomberg on Friday that there is no need for further stimulus measures.

"I would see even less reason to make changes now," he said.

-

11:35

European Central Bank Executive Board member Peter Praet: the central bank will run its asset-buying programme until the Eurozone reaches sustained adjustment in the path of inflation

The European Central Bank (ECB) Executive Board member Peter Praet said on Friday that the central bank will run its asset-buying programme until the Eurozone reaches sustained adjustment in the path of inflation.

The ECB President Mario Draghi said that the ECB will review the volume of its asset-buying programme at its December monetary policy meeting.

-

10:08

Option expiries for today's 10:00 ET NY cut

USD/JPY 122.00 (USD 305m)

EUR/USD 1.0800 (EUR 909m)

GBP/USD 1.5400 (GBP 478m)

USD/CHF 0.9925 (USD 525m)

USD/CAD 1.3200 (USD 610m) 1.3300 (825m)

AUD/USD 0.7000 ( AUD 391m)

NZD/USD 0.6600 (NZD 915m)

-

09:26

Germany’s manufacturing turnover declines by 1.1% in September

Destatis released its manufacturing turnover data for Germany on Monday. Manufacturing turnover declined on seasonally adjusted and on adjusted for working days basis by 1.1% in September, after a 1.0% fall in August. August's figure was revised down up a 1.3% decrease.

Meanwhile, domestic turnover decreased by 1.2% in September, while the business with foreign customers dropped 1.1%.

Sales to euro area countries rose 1.6% in September, while sales to other countries were down 2.9%.

On a yearly basis, manufacturing turnover in Germany was up on seasonally adjusted and on adjusted for working days basis by 0.7% in September.

-

09:15

Germany's seasonally adjusted trade surplus declines to €19.4 billion in September

Destatis released its trade data for Germany on Monday. Germany's seasonally adjusted trade surplus declined to €19.4 billion in September from 19.4 in August.

Exports rose 4.4% year-on-year in September, while imports climbed 3.9% year-on-year.

On a yearly basis, German exports increased at a seasonally and calendar-adjusted 2.6% in September, while imports rose by 3.6%.

Germany's current account surplus was at €25.1 billion in September, up from €13.3 billion in August. August's figure was revised up from €12.3 billion.

-

09:05

Chicago Federal Reserve Bank President Charles Evans: the Fed should delay the interest rate hike despite the strong U.S. labour market data

Chicago Federal Reserve Bank President Charles Evans said in an interview with CNBC on Friday that the Fed should delay the interest rate hike despite the strong U.S. labour market data until the inflation in the U.S. will be on the track to achieve the Fed's 2% target.

He noted that the strong U.S. labour market data in October was "very good news".

"We've indicated that conditions look like they could be ripe of an increase," Evans said.

-

08:55

U.S. unemployment rate falls to 5.0% in October, 271,000 jobs are added

The U.S. Labor Department released the labour market data on Friday. The U.S. economy added 271,000 jobs in October, exceeding expectations for a rise of 180,000 jobs, after a gain of 137,000 jobs in September. It was the largest increase since December 2014.

September's figure was revised down from a rise of 142,000 jobs.

The increase was mainly driven by a rise in the services sector. The services sector added 241,000 jobs in October, while the manufacturing sector added no jobs.

The strong U.S. dollar weighed on the manufacturing sector.

Professional and business services sector added 78,000 jobs in October.

The U.S. unemployment rate declined to 5.0% in October from 5.1% in September. It was the lowest level since April 2008.

Analysts had expected the unemployment rate to remain unchanged at 5.1%.

Average hourly earnings climbed 0.4% in October, beating forecasts of a 0.2% gain, after a flat reading in September.

The labour-force participation rate remained unchanged at 62.4% in October. It was the lowest level since October 1977.

These figures indicate that the interest rate by the Fed in December is likely if November's labour market data will be strong enough and there will be no surprises.

-

08:37

The number of active U.S. rigs falls by 6 rigs to 572 last week

The oil driller Baker Hughes reported on Friday that the number of active U.S. rigs declined by 6 rigs to 572 last week. It was the tenth consecutive decrease and the lowest level since June 118, 2010.

Combined oil and gas rigs declined by 4 to 771. It was the lowest level since April 2002.

-

08:00

Germany: Current Account , September 35.1

-

08:00

Germany: Trade Balance, September 19.4

-

07:48

Foreign exchange market. Asian session: the euro rose slightly

Economic calendar (GMT0):

Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual

00:30 Australia ANZ Job Advertisements (MoM) October 3.8% Revised From 3.9% 0.4%

01:30 Japan Labor Cash Earnings, YoY September 0.4% Revised From 0.5% 0.6%

The euro slightly rebounded after Friday's fall, which was caused by U.S. employment data. It's worth to remind that the U.S. economy exceeded expectations for 180,000 jobs and generated 271,000 jobs outside the farming sector in October, the biggest monthly gain this year, while the unemployment rate fell to 5% from 5.1%. Hourly wages rose 9 cents or 2.5% y/y at the fastest year-over-year pace since 2009.

The yen declined despite favorable data on Japanese wages. Labor Cash Earnings rose by 0.6% in September compared to a 0.4% rise in September 2014. Higher earnings stimulate consumption making earnings an inflation factor.

The New Zealand dollar rose despite Fonterra chief executive officer Theo Spierings' words that the company may lose its market share in China. Dairy products are key exports for New Zealand, that's why concerns over Fonterra may weigh on the NZD.

EUR/USD: the pair rose to $1.0770 in Asian trade

USD/JPY: the pair traded within Y123.15-45

GBP/USD: the pair rose to $1.5075

The most important news that are expected (GMT0):

(time / country / index / period / previous value / forecast)

07:00 Germany Current Account September 12.3

07:00 Germany Trade Balance September 15.3

09:30 Eurozone Sentix Investor Confidence November 11.7

13:15 Canada Housing Starts October 230.7 200

15:00 U.S. Labor Market Conditions Index October 0

23:50 Japan Current Account, bln September 1653 2235.2

-

07:32

Oil prices climbed

West Texas Intermediate futures for December delivery rose to $44.79 (+1.13%), while Brent crude advanced to $47.94 (+1.10%), however gains were limited by a stronger dollar, which rose on strong U.S. jobs data released Friday. A stronger greenback makes crude oil more expensive for importers using other currencies.

Bloomberg News reported that according to data from the Beijing-based General Administration of Customs China's crude imports declined to about 6.23 million barrels a day in October. China is the second-biggest consumer of oil in the world and this report put pressure on oil's gains.

Meanwhile Saudi Oil Minister Ali al-Naimi said low oil prices are favorable for Asian costumers and demand "will soon reflect the attractiveness of the current prices." He expects Asia to account for most of demand growth. However Russia and producers in Africa and South America also raised shipments to the region increasing competition. Russian Energy Minister Alexander Novak said his country intends to more than double oil exports to Asian customers by 2035.

-

07:08

Gold near three-month low

Gold slightly climbed to $1,092.60 (+0.45%) on Monday morning, but remained near a three-month low as strong jobs data from the U.S. intensified expectations for an interest rate hike by the Federal Reserve in December. Some analysts say that the precious metal is likely to remain under pressure until the Federal Open Market Committee announces its monetary policy decision next month.

The U.S. economy exceeded expectations for 180,000 jobs and generated 271,000 jobs outside the farming sector in October, the biggest monthly gain this year, while the unemployment rate fell to 5% from 5.1%. Hourly wages rose 9 cents or 2.5% y/y at the fastest year-over-year pace since 2009.

Assets in SPDR Gold Trust, the biggest gold-backed exchange-traded fund in the world, fell 0.40% to 669.09 tonnes on Friday.

-

07:06

Global Stocks: U.S. stock indices posted mixed results on Friday but rose over the week

U.S. stock indices mostly climbed on Friday amid a strong jobs report.

The Dow Jones Industrial Average rose 46.90 points, or 0.3%, to 17,910.33 (+1.4% over the week). The S&P 500 edged down 0.73 points, or 0.03%, to 2,099.20 (+0.95% over the week). The Nasdaq Composite climbed 19.38 points, or 0.4%, to 5,147.12 (+1.9% over the week).

The Labor Department reported the U.S. economy exceeded expectations for 180,000 jobs and generated 271,000 jobs in October, the biggest monthly gain this year, while the unemployment rate fell to 5% from 5.1%. Hourly wages rose 9 cents or 2.5% y/y at the fastest year-over-year pace since 2009.

This morning in Asia Hong Kong Hang Seng climbed 0.12%, or 27.58, to 22,894.91. China Shanghai Composite Index gained 1.63%, or 58.39, to 3.648.42. The Nikkei 225 rose 1.94%, or 372.90, to 19,638.5.

Asian indices rose amid optimistic employment data from the U.S. Japanese stocks rose amid a weaker yen, which is favorable for exporters.

-

07:05

Options levels on monday, November 9, 2015:

EUR / USD

Resistance levels (open interest**, contracts)

$1.0978 (2435)

$1.0917 (1677)

$1.0868 (378)

Price at time of writing this review: $1.0766

Support levels (open interest**, contracts):

$1.0700 (5555)

$1.0672 (4898)

$1.0633 (5953)

Comments:

- Overall open interest on the CALL options with the expiration date December, 4 is 78440 contracts, with the maximum number of contracts with strike price $1,1200 (5413);

- Overall open interest on the PUT options with the expiration date December, 4 is 114161 contracts, with the maximum number of contracts with strike price $1,0700 (8176);

- The ratio of PUT/CALL was 1.46 versus 0.93 from the previous trading day according to data from November, 6

GBP/USD

Resistance levels (open interest**, contracts)

$1.5303 (1502)

$1.5206 (860)

$1.5109 (500)

Price at time of writing this review: $1.5076

Support levels (open interest**, contracts):

$1.4989 (2307)

$1.4893 (1311)

$1.4796 (1170)

Comments:

- Overall open interest on the CALL options with the expiration date December, 4 is 22845 contracts, with the maximum number of contracts with strike price $1,5600 (3634);

- Overall open interest on the PUT options with the expiration date December, 4 is 24919 contracts, with the maximum number of contracts with strike price $1,5000 (2307);

- The ratio of PUT/CALL was 1.09 versus 0.98 from the previous trading day according to data from November, 6

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

03:35

Nikkei 225 19,603.29 +337.69 +1.75 %, Hang Seng 22,850.99 -16.34 -0.07 %, Shanghai Composite 3,625.72 +35.69 +0.99 %

-

02:31

Japan: Labor Cash Earnings, YoY, September 0.6%

-

01:30

Australia: ANZ Job Advertisements (MoM), October 0.4%

-

00:45

Commodities. Daily history for Nov 6’2015:

(raw materials / closing price /% change)

Oil 44.34 +0.11%

Gold 1,089.50 +0.17%

-

00:43

Stocks. Daily history for Sep Nov 6’2015:

(index / closing price / change items /% change)

Nikkei 225 19,265.6 +149.19 +0.78 %

Hang Seng 22,867.33 -183.71 -0.80 %

Shanghai Composite 3,590.03 +67.21 +1.91 %

FTSE 100 6,353.83 -11.07 -0.17 %

CAC 40 4,984.15 +4.11 +0.08 %

Xetra DAX 10,988.03 +100.29 +0.92 %

S&P 500 2,099.2 -0.73 -0.03 %

NASDAQ Composite 5,147.12 +19.38 +0.38 %

Dow Jones 17,910.33 +46.90 +0.26 %

-

00:43

Currencies. Daily history for Nov 6’2015:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,0743 -1,30%

GBP/USD $1,5050 -1,04%

USD/CHF Chf1,0057 +1,06%

USD/JPY Y123,19 +1,18%

EUR/JPY Y132,35 -0,11%

GBP/JPY Y185,4 +0,16%

AUD/USD $0,7046 -1,35%

NZD/USD $0,6522 -1,35%

USD/CAD C$1,3293 +0,94%

-

00:01

Schedule for today, Monday, Nov 9’2015:

(time / country / index / period / previous value / forecast)

00:30 Australia ANZ Job Advertisements (MoM) October 3.9%

01:30 Japan Labor Cash Earnings, YoY September 0.5%

07:00 Germany Current Account September 12.3

07:00 Germany Trade Balance September 15.3

09:30 Eurozone Sentix Investor Confidence November 11.7

13:15 Canada Housing Starts October 230.7 200

15:00 U.S. Labor Market Conditions Index October 0

23:50 Japan Current Account, bln September 1653 2235.2

-