Noticias del mercado

-

22:12

U.S. stocks closed

U.S. stocks fluctuated as China's signal that it may add to stimulus boosted metals prices from copper to gold. Brent crude slipped to an 11-year low on signs the global glut will persist, while Treasuries advanced.

The Standard & Poor's 500 Index pared gains to 0.1 percent, after earlier rallying as much as 0.9 percent. The U.S. benchmark recovered from a 3.3 percent rout over two days after the Federal Reserve raised interest rates. Ten-year Treasury notes erased losses for December, while the dollar slipped. Brent futures in London fell to the weakest intraday level since July 2004, with drilling in the U.S. increasing. Emerging-market equities headed for the fourth gain in five days.

The rout in crude prices has pushed oil to the lowest levels since before financial crisis, threatening to keep inflation from rising to levels targeted by central banks in Europe and America. Equities have tumbled since the Fed's tightening on concern that U.S. growth could slow without zero-percent interest rates. China's government said monetary policy must be more "flexible" and fiscal policy more "forceful" to combat slowing growth in the world's second-largest economy.

Brent crude futures were 1.9 percent lower at $36.19 a barrel, after a 2.8 percent decline last week. It fell as low as $36.04 on Monday, the lowest since July 2004. West Texas Intermediate crude in New York was little changed at $34.74 a barrel.

Gas, which has been battered by widespread warmth in the eastern half of the country, headed for the biggest one-day gain in seven weeks as forecasts showed mild weather fading in the U.S. Midwest. Gas futures for January delivery rose 7.9 percent, to $1.907 per million British thermal units on the New York Mercantile Exchange.

-

21:00

DJIA 17172.95 44.40 0.26%, NASDAQ 4942.67 19.59 0.40%, S&P 500 2011.72 6.17 0.31%

-

20:21

American focus: the US dollar fell

The US dollar fell against other major currencies, as trading volumes are likely to remain low for the Christmas holidays, but demand for the dollar rose to a recent decision of the Federal Reserve System.

The dollar showed an increase last week after the Federal Reserve raised interest rates by a quarter percentage point to 0.25% -0.5%, as many expected.

Commenting on the statement of the Fed, Janet Yellen head of the bank promised that the Fed will not rush to the tightening of monetary policy, and the future rate hikes will be gradual and will depend on economic indicators.

According to a National Activity Index Chicago Fed, economic activity in the US fell in November.

The index, which is weighted value of the 85 individual indicators, since data on production and sales and ending salaries and expenses in November fell to -0.30 from -0.17 in October. A reading above zero indicates that the national economy is growing at a rate of long-term trend, while values below zero indicate growth below average.

The moving average of the index in three months, which smooths volatility of the monthly index in November fell to -0.20 from -0.18 in October. In November 2014, the index was equal to 0.77, while the moving average stood at 0.42.

These figures are not terrible, but they are a warning to all those who believe that the pace of US economic growth in 2016 will be strong, but also point to the fact that at the end of 2015 the economy lost momentum for growth.

Little impact on the dynamics of the euro earlier had data for Germany. The Federal Statistics Office Destatis reported that the producer price index fell in November by 0.2% compared to October and 2.5% per annum. The index showed the biggest annual fall in nearly six years, helped by lower energy prices. Economists had forecast a drop of 0.2% compared to October and 2.5% per annum. Excluding energy prices, producer prices fell by 0.2% in monthly terms and 0.7% per annum.

Also today, the ECB's chief economist, Peter Pret said that the economic outlook had improved in terms of low interest rates and a sharp drop in oil prices. "The positive effects of structural reforms in a number of countries such as Spain and Ireland, should also be highlighted. These factors had a positive effect on the labor market and economic recovery. Fiscal policy will be more neutral, even slightly expansionary. In fact, these measures will promote the growth of the eurozone's GDP by 0.1% in 2016 and 2017 "- added Pret. "There have been attached huge financial effort, although debt levels are still too high. However, we must bear in mind that the real GDP in the euro area in the first quarter of 2016 just come back to the level of the beginning of 2008. This means that for the past eight years, the euro zone's GDP did not grow in real terms on average, while countries such as Germany recorded a moderate expansion. Other countries, however, experienced a serious recession, "- said the politician.

The British pound fell slightly against the dollar, updating the at least Friday. Experts point out that in recent years the pound is under pressure as markets no longer expect a rate hike of the Bank of England in 2016. Today, representatives of the Bank of England Martin Weale said that a pause in the growth of wages and a further decline in commodity prices have made the need for tighter monetary policy, "a little less urgent." Recall, according to the latest forecasts of the Central Bank, inflation will remain below 1 percent until the second half of next year. We also add the interest rate remains unchanged at the current record low of 0.50% since the beginning of 2009. During the interview, Will said that the growth of the pound against the euro has been a significant factor hampering the rate increase. He believes that the rate should be increased before the beginning of 2017, to keep inflation from rising above the target level of the Central Bank.

In addition, the survey results Confederation of British Industry (CBI) showed that retail sales in the country grew slightly less than expected in the run up to Christmas. According to the data, the balance of retail sales rose to 19 in December from a nine-month low of seven in November. Nevertheless, the latter value was slightly less than forecasts of experts at around 21. In addition, the index of expected sales next month fell to its lowest level since May 2012.

-

18:00

European stocks closed: FTSE 6034.84 -17.58 -0.29%, DAX 10497.77 -110.42 -1.04%, CAC 40 4565.17 -60.09 -1.30%

-

17:59

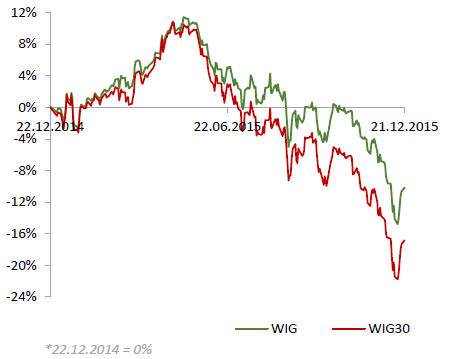

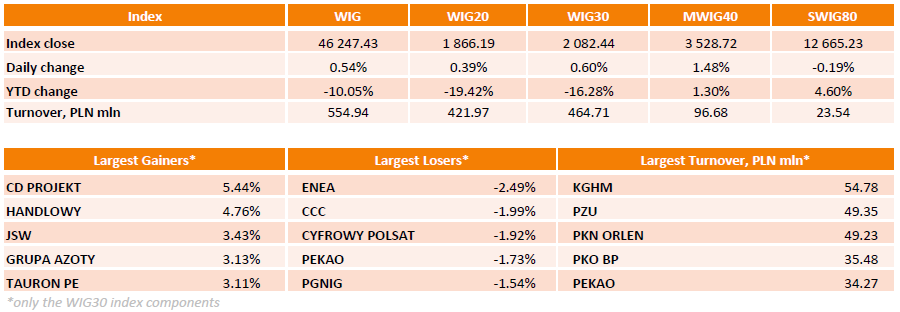

WSE: Session Results

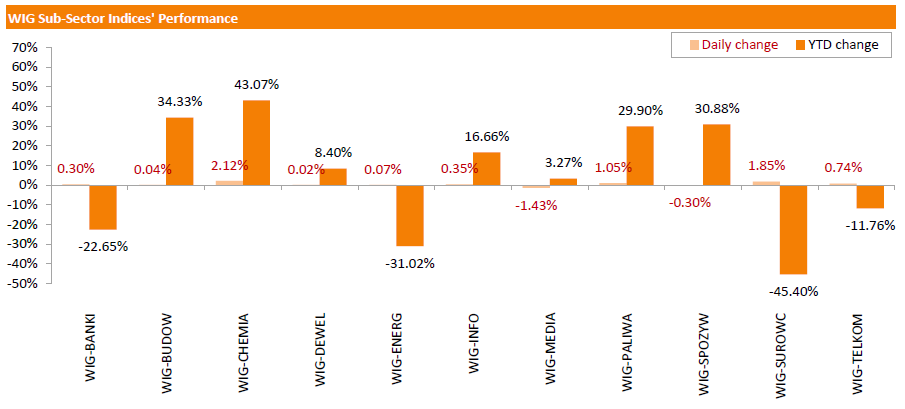

Polish equity market surged on Monday. The broad market measure, the WIG Index, added 0.54%. Except for media (-1.43%) and food sector (-0.30%), every sector in the WIG Index gained, with chemicals (+2.12%) outperforming.

The large-cap stocks' measure, the WIG30 Index, advanced by 0.6%. Videogame developer CD PROJEKT (WSE: CDR) closed its first day as WIG30 Index component with a 5.44% boost. CDR replaced the shares of auto components producer BORYSZEW (WSE: BRS). Other major gainers included bank HANDLOWY (WSE: BHW), coal miner JSW (WSE: JSW), chemical producer GRUPA AZOTY (WSE: ATT) and genco TAURON PE (WSE: TPE), advancing between 3.11% and 4.76%. On the other side of the ledger, genco ENEA (WSE: ENA) was the weakest name, retreating by 2.49% after two consecutive sessions of gains. Retailer CCC (WSE: CCC) and media group CYFROWY POLSAT (WSE: CPS) posted declines of 1.99% and 1.92% respectively.

-

17:34

Wall Street. Major U.S. stock-indexes rose

Major U.S. stock-indexes started the Christmas holiday week on a positive note, led by tech and financials, but energy stocks lagged as Brent crude hit an 11 year low. Trading volumes are expected to be relatively light this week, with U.S. stock markets operating a shortened session on Thursday and closing on Friday for Christmas.

Oil prices have been sliding under continued pressure from global oversupply and tepid demand.

Most of Dow stocks in positive area (24 of 30). Top looser - The Walt Disney Company (DIS, -1,33%). Top gainer - JPMorgan Chase & Co. (JPM, +1.18%).

All S&P index sectors in positive area. Top looser - Conglomerates (+0,7%).

At the moment:

Dow 17087.00 +70.00 +0.41%

S&P 500 2004.00 +12.00 +0.60%

Nasdaq 100 4530.50 +26.00 +0.58%

Oil 35.57 -0.49 -1.36%

Gold 1078.30 +13.30 +1.25%

U.S. 10yr 2.19 -0.01

-

16:00

Eurozone: Consumer Confidence, December -5.7 (forecast -5.85)

-

15:34

U.S. Stocks open: Dow +0.79%, Nasdaq +0.84%, S&P +0.80%

-

15:23

Before the bell: S&P futures +0.84%, NASDAQ futures +0.83%

U.S. stock-index futures were rose.

Global Stocks:

Nikkei 18,916.02 -70.78 -0.37%

Hang Seng 21,791.68 +36.12 +0.17%

Shanghai Composite 3,642.63 +63.67 +1.78%

FTSE 6,108.01 +55.59 +0.92%

CAC 4,644.48 +19.22 +0.42%

DAX 10,696.51 +88.32 +0.83%

Crude oil $34.57 (-0.46%)

Gold $1073.70 (+0.82%)

-

15:01

Wall Street. Stocks before the bell

(company / ticker / price / change, % / volume)

Barrick Gold Corporation, NYSE

ABX

7.40

2.35%

1.4K

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

6.31

1.61%

24.9K

Hewlett-Packard Co.

HPQ

11.68

1.48%

0.1K

Walt Disney Co

DIS

109.25

1.42%

73.5K

ALCOA INC.

AA

9.33

1.08%

15.0K

Apple Inc.

AAPL

107.16

1.07%

246.7K

Microsoft Corp

MSFT

54.70

1.05%

87.1K

Goldman Sachs

GS

177.30

1.03%

0.1K

Citigroup Inc., NYSE

C

51.72

1.00%

10.7K

Intel Corp

INTC

34.20

0.99%

8.6K

Starbucks Corporation, NASDAQ

SBUX

59.20

0.99%

1.0K

Nike

NKE

129.68

0.90%

0.5K

Visa

V

77.00

0.89%

2.1K

Chevron Corp

CVX

90.60

0.88%

1.1K

Yahoo! Inc., NASDAQ

YHOO

33.24

0.88%

3.3K

ALTRIA GROUP INC.

MO

57.61

0.84%

9.7K

Boeing Co

BA

140.70

0.80%

0.3K

JPMorgan Chase and Co

JPM

64.90

0.78%

1.0K

E. I. du Pont de Nemours and Co

DD

63.88

0.76%

2.3K

Facebook, Inc.

FB

104.81

0.74%

45.0K

AT&T Inc

T

33.80

0.60%

6.7K

Amazon.com Inc., NASDAQ

AMZN

667.80

0.55%

4.0K

Home Depot Inc

HD

131.00

0.54%

0.5K

Johnson & Johnson

JNJ

102.50

0.54%

0.5K

Exxon Mobil Corp

XOM

77.69

0.53%

0.9K

Pfizer Inc

PFE

32.16

0.53%

45.6K

Ford Motor Co.

F

13.87

0.51%

1.0K

Tesla Motors, Inc., NASDAQ

TSLA

231.62

0.50%

3.2K

Twitter, Inc., NYSE

TWTR

23.10

0.48%

6.8K

The Coca-Cola Co

KO

42.70

0.47%

22.3K

Google Inc.

GOOG

742.52

0.43%

1.1K

Procter & Gamble Co

PG

78.45

0.41%

1.0K

General Electric Co

GE

30.40

0.40%

0.2K

Cisco Systems Inc

CSCO

26.37

0.38%

2.3K

Verizon Communications Inc

VZ

45.72

0.35%

0.4K

Caterpillar Inc

CAT

65.32

0.32%

31.7K

International Business Machines Co...

IBM

135.31

0.30%

0.5K

Wal-Mart Stores Inc

WMT

59.02

0.29%

0.3K

American Express Co

AXP

67.94

0.10%

0.1K

Deere & Company, NYSE

DE

75.03

0.08%

0.1K

Yandex N.V., NASDAQ

YNDX

15.30

-0.13%

0.5K

-

14:49

Option expiries for today's 10:00 ET NY cut

USD/JPY: 120.35 (USD 600m) 122.50 (360m) 122.70-85 (685m)

EUR/USD: 1.0750 (EUR 380m) 1.0785 (343m) 1.0810 (559m) 1.0900 (761m)

GBP/USD: 1.5050 (GBP 279m)

USD/CAD:1.3600 (USD 1.1bln)

AUD/USD: 0.7195 (AUD 750m) 0.7270 (307m)

NZD/USD: 0.6600 (NZD 300m) 0.6850 (297m)

-

14:46

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Other:

Alphabet (GOOG) target raised to $850 from $820 at Pacific Crest

-

14:09

Orders

EUR/USD

Offers 1.0885 1.0900 1.0930 1.0960 1.0985 1.1000 1.1025-30 1.1050

Bids 1.0845-50 1.0830 1.0800 1.0780-85 1.0750 1.0730 1.0700 1.0685 1.0670 1.0650

GBP/USD

Offers 1.4925-30 1.4950-55 1.4980-85 1.5000 1.5030 1.5050 1.5075-80 1.5100

Bids 1.4900 1.4885 1.4865 1.4850 1.4830 1.4800 1.4785 1.4765 1.4750

EUR/GBP

Offers 0.7300 0.7320 0.7350 0.7375 0.7400 0.7420 0.7450

Bids 0.7275-80 0.7250 0.7225-30 0.7200 0.7180 0.7165 0.7150

EUR/JPY

Offers 132.10 132.25 132.50 132.80 133.00 133.20 133.50 133.85 134.00

Bids 131.75-80 131.50 131.00 130.80 130.50 130.30 130.00

USD/JPY

Offers 121.50-55 121.80 122.00 122.20 122.50 122.65 122.80 123.00

Bids 121.20-25 121.00 120.85 120.60-65 120.50 120.30 120.00

AUD/USD

Offers 0.7200 0.7220 0.7255-60 0.7280 0.7300 0.7320-25 0.7345-50

Bids 0.7150 0.7120-25 0.7100 0.7085 0.7065 0.7050 0.7020 0.7000

-

12:00

United Kingdom: CBI retail sales volume balance, December 19 (forecast 21)

-

09:22

Option expiries for today's 10:00 ET NY cut

USD/JPY: 120.35 (USD 600m) 122.50 (360m) 122.70-85 (685m)

EUR/USD: 1.0750 (EUR 380m) 1.0785 (343m) 1.0810 (559m) 1.0900 (761m)

GBP/USD: 1.5050 (GBP 279m)

USD/CAD:1.3600 (USD 1.1bln)

AUD/USD: 0.7195 (AUD 750m) 0.7270 (307m)

NZD/USD: 0.6600 (NZD 300m) 0.6850 (297m)

-

08:26

Oil prices plunged

West Texas Intermediate futures for January delivery, which expires today, fell to $35.73 (-0.92%), while Brent crude dropped to $36.40 (-1.30%). Prices of both types of crude fell to levels not seen since 2009 and 2004 respectively.

Investors are concerned over the persistent supply glut and prospects of exports from the U.S. after elimination of a forty-year old export ban. Iran is also preparing to boost production now that the sanctions are lifted.

Data showed on Friday that despite plunging prices U.S. rig count rose by 17 to 541 after four weeks of declines.

-

08:10

Foreign exchange market. Asian session: the dollar little changed

Economic calendar (GMT0):

Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual

04:30 Japan All Industry Activity Index, m/m October -0.2% 1.0%

05:00 Japan BoJ monthly economic report

07:00 Germany Producer Price Index (MoM) November -0.4% -0.2% -0.2%

07:00 Germany Producer Price Index (YoY) November -2.3% -2.5% -2.5%

The U.S. dollar traded range-bound against major currencies ahead of Christmas at the end of the current working week. Trading is not expected to be dynamic. At the same time many traders have already closed their positions ahead of the end of the year, which increases market volatility. On Thursday, December 24, markets in Germany and Italy will be closed. On December 25 markets in other European countries as well as in Canada, the U.S., Australia and New Zealand will be on holiday.

The pound also traded range-bound. Market participants are waiting for data on U.K. budged deficit. The report is expected to show that the deficit rose to £11.7 billion ($17.4 billion) in November. This would suggest that Osborne will face difficulties fulfilling his pledge to balance the budget by 2020.

The New Zealand dollar climbed on positive data. Visitor arrivals rose by 11.1% in November. Meanwhile Westpac consumer sentiment rose to 110.7 in the fourth quarter from 106 reported previously (the best quarterly increase in two years).

EUR/USD: the pair fluctuated within $1.0855-85 in Asian trade

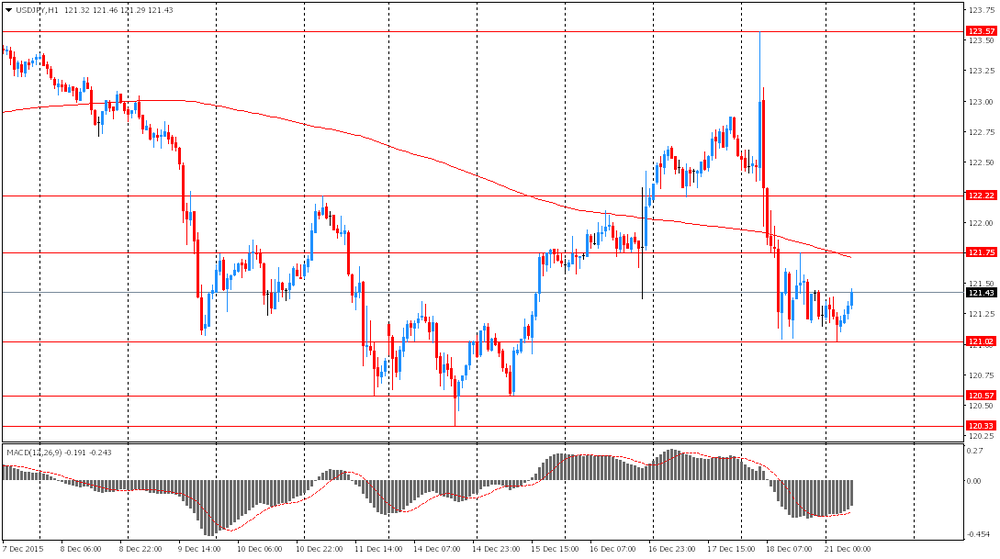

USD/JPY: the pair traded within Y121.00-50

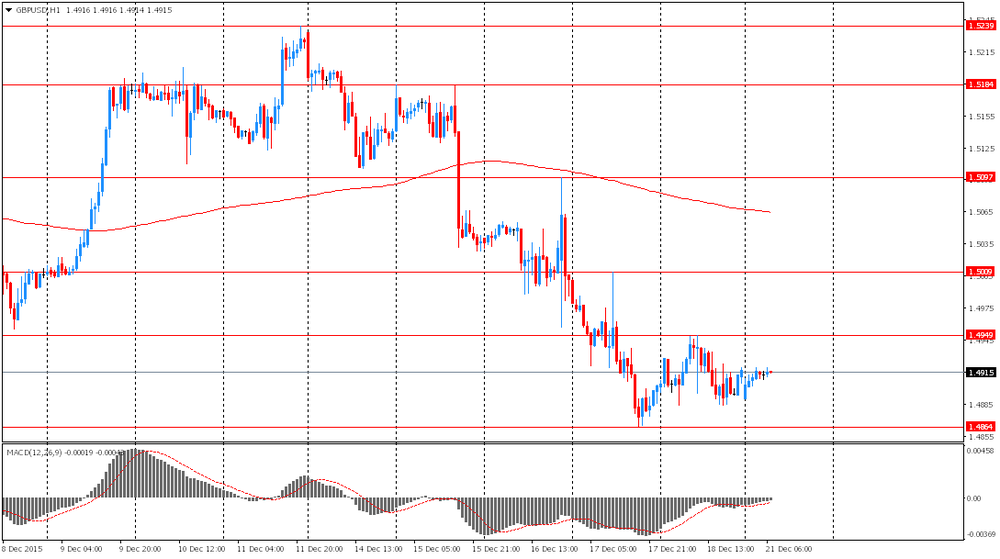

GBP/USD: the pair traded within $1.4885-20

The most important news that are expected (GMT0):

(time / country / index / period / previous value / forecast)

11:00 United Kingdom CBI retail sales volume balance December 7 21

11:00 Germany Bundesbank Monthly Report

15:00 Eurozone Consumer Confidence (Preliminary) December -5.9 -5.85

-

08:00

Germany: Producer Price Index (MoM), November -0.2% (forecast -0.2%)

-

08:00

Germany: Producer Price Index (YoY), November -2.5% (forecast -2.5%)

-

07:44

Gold climbed slightly

Gold climbed to $1,068.50 (+0.33%) following gains in the previous session amid a softer dollar and weaker stocks. However gains are limited due to concerns that higher interest rates in the U.S. will hit demand for the non-interest-paying precious metal. The Federal Reserve is likely to raise rates further in 2016.

Assets in SPDR Gold Trust, the biggest gold-backed exchange-traded fund in the world, climbed 2.98% to 648.92 tonnes on Friday, marking the first increase in two months.

Physical demand may improve in China in a couple of weeks due to the Lunar New Year celebrations in February.

-

07:30

Global Stocks: U.S. stock indices fell amid declines in oil prices

U.S. stock indices fell on Friday weighed by declines in oil prices.

The Dow Jones Industrial Average fell 367.39 points, or 2.1%, to 17,128.45 (-0.8% over the week). The S&P 500 dropped 36.37 points, or 1.8%, to 2,005.52 (-0.3% over the week; financials led declines with a 2.5% fall). The Nasdaq Composite lost 79.47 points, or 1.6% to 4,923.08 (-0.2% over the week).

Earlier in the week Fed's decision to raise interest rates spurred a rally in stocks. Normally higher rates steepen the spread between ten-year and 2-year yields, but this effect is not seen yet this time. That's why investors focused on concerns over bank's exposure to energy companies.

This morning in Asia Hong Kong Hang Seng climbed 0.40%, or 86.09, to 21,841.65. China Shanghai Composite Index advanced 1.98%, or 70.42, to 3.649.88. The Nikkei fell by 0.41%, or 78.19, to 18,908.61.

Asian indices outside Japan rose.

Japanese stocks fell reacting to declines in Wall Street on Friday.

The People's Bank of China strengthened the daily fix for the yuan by 0.09% to 6.4753 per dollar avoiding an unprecedented 11th weakening in a row.

-

07:05

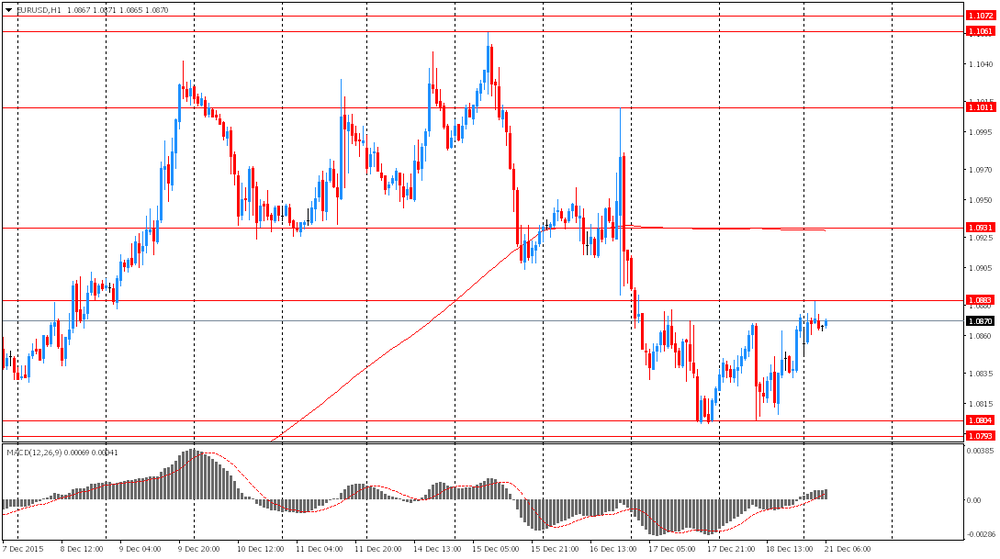

Options levels on monday, December 21, 2015:

EUR / USD

Resistance levels (open interest**, contracts)

$1.1076 (3222)

$1.1036 (4395)

$1.0968 (4838)

Price at time of writing this review: $1.0873

Support levels (open interest**, contracts):

$1.0794 (1855)

$1.0762 (2515)

$1.0714 (5958)

Comments:

- Overall open interest on the CALL options with the expiration date January, 8 is 54387 contracts, with the maximum number of contracts with strike price $1,1100 (6852);

- Overall open interest on the PUT options with the expiration date January, 8 is 72346 contracts, with the maximum number of contracts with strike price $1,0450 (8108);

- The ratio of PUT/CALL was 1.33 versus 1.28 from the previous trading day according to data from December, 17

GBP/USD

Resistance levels (open interest**, contracts)

$1.5201 (1168)

$1.5103 (2623)

$1.5005 (527)

Price at time of writing this review: $1.4918

Support levels (open interest**, contracts):

$1.4794 (1520)

$1.4696 (1049)

$1.4598 (561)

Comments:

- Overall open interest on the CALL options with the expiration date January, 8 is 18640 contracts, with the maximum number of contracts with strike price $1,5100 (2623);

- Overall open interest on the PUT options with the expiration date January, 8 is 18595 contracts, with the maximum number of contracts with strike price $1,5100 (3086);

- The ratio of PUT/CALL was 1.00 versus 1.00 from the previous trading day according to data from December, 17

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

05:32

Japan: All Industry Activity Index, m/m, October 1.0%

-

03:05

Nikkei 225 18,717.49 -269.31 -1.4 %, Hang Seng 21,775.39 +19.83 +0.1 %, Shanghai Composite 3,568.34 -10.63 -0.3 %

-

01:04

Commodities. Daily history for Dec 18’2015:

(raw materials / closing price /% change)

Oil 34.55 -0.52%

Gold 1,065.60 +0.06%

-

01:03

Stocks. Daily history for Sep Dec 18’2015:

(index / closing price / change items /% change)

Nikkei 225 18,986.8 -366.76 -1.90 %

Hang Seng 21,755.56 -116.50 -0.53 %

Shanghai Composite 3,579.49 -0.51 -0.01 %

FTSE 100 6,052.42 -50.12 -0.82%

CAC 40 4,625.26 -52.28 -1.12%

Xetra DAX 10,608.19 -129.93 -1.21%

S&P 500 2,005.55 -36.34 -1.78%

NASDAQ Composite 4,923.08 -79.47 -1.59%

Dow Jones 17,128.55 -367.29 -2.10%

-

01:02

Currencies. Daily history for Dec 18’2015:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,0872 +0,43%

GBP/USD $1,4917 +0,11%

USD/CHF Chf0,9914 -0,47%

USD/JPY Y121,24 -1,07%

EUR/JPY Y131,82 -0,64%

GBP/JPY Y180,85 -0,96%

AUD/USD $0,7179 +0,75%

NZD/USD $0,6736 +0,53%

USD/CAD C$1,3942 +0,05%

-

00:00

Schedule for today, Monday, 21’2015:

(time / country / index / period / previous value / forecast)

04:30 Japan All Industry Activity Index, m/m October -0.2%

05:00 Japan BoJ monthly economic report

07:00 Germany Producer Price Index (MoM) November -0.4% -0.2%

07:00 Germany Producer Price Index (YoY) November -2.3% -2.5%

11:00 United Kingdom CBI retail sales volume balance December 7 21

11:00 Germany Bundesbank Monthly Report

15:00 Eurozone Consumer Confidence (Preliminary) December -5.9 -5.85

-