Noticias del mercado

-

23:59

Schedule for today, Wednesday, Feb 24’2016:

(time / country / index / period / previous value / forecast)

00:30 Australia Wage Price Index, q/q Quarter IV 0.6% 0.6%

00:30 Australia Wage Price Index, y/y Quarter IV 2.3% 2.3%

00:30 Australia Construction Work Done Quarter IV -3.6% -2%

05:00 Japan Leading Economic Index (Finally) December 103.2 102

05:00 Japan Coincident Index (Finally) December 111.9

07:00 Switzerland UBS Consumption Indicator January 1.62

07:45 France Consumer confidence February 97 97

09:30 United Kingdom BBA Mortgage Approvals January 43.98

12:00 U.S. MBA Mortgage Applications February 8.2%

14:45 U.S. Services PMI (Preliminary) February 53.2 53.5

15:00 U.S. New Home Sales January 544 520

15:30 U.S. Crude Oil Inventories February 2.147

21:45 New Zealand Visitor Arrivals January 10.5%

-

21:00

Dow -1.10% 16,437.47 -183.19 Nasdaq -1.23% 4,514.45 -56.16 S&P -1.10% 1,924.09 -21.41

-

20:22

American focus: The pound continued to fall against major currencies

The pound depreciated significantly against the dollar, approaching to the psychological mark of $ 1.4000. The cause of this trend was the increased demand for the US currency and the neutral tone of the statements of the Bank of England Governor Mark Carney and the representatives of the Central Bank of Huila and Shafiq. Carney said that the Bank started the development of an emergency scenario in case Brekzita and said he had enough room to maneuver, he is ready to lower rates or extend the program of QE. It is also noted that the Committee had not formulated an opinion on the most likely outcome of the referendum and its implications for the exchange rate of the national currency. "It seems that in recent years the dynamics of the pound affect the upcoming vote From the perspective of monetary policy the most important is the stability of the national currency and the dynamics of its conditional factors." - Carney said.

Meanwhile, representatives of the Bank of England said they did not consider it necessary to increase interest rates in response to the decline in the pound on the eve of the referendum. The weakening of the pound should lead to an increase in import prices and to help ensure that the Central Bank inflation target of 2%.

In addition, the deputy. the head of the Bank of England Shafiq said that wage growth should accelerate. "It is advisable to abstain from voting in favor of a rate hike as long as wage growth is not sufficiently convincing and relevant inflation target after eliminating uncertainties, it is expected that the economy will support more rapid rate increase than the estimated market yield curve." - Said Shafiq.

Earlier, the Bank of England this month made it clear that the first since 2007, the rate hike will happen quite soon, the cause of which is the deterioration of prospects for the global economy and fluctuations in the financial markets caused by the slowdown in emerging economies.

The Swiss franc fell more than 100 points against the US dollar, reaching a minimum on 22 February. The demand for the franc rose after the head of the SNB's Jordan said that unconventional policy measures can not be used indefinitely, if the Central Bank plans to achieve the desired. "A set of monetary instruments has expanded, but did not become infinite. The effect of monetary policy may weaken over time, and the use of unconventional measures potentially entail costs. It is necessary to constantly evaluate the ratio of costs and effects of monetary instruments. If the tool is no longer have the desired effect on the background of changed circumstances, it is necessary to adjust policy ", - said Jordan. Also the head of the SNB reiterated that the Swiss franc is still significantly overvalued against the euro in real terms.

In the course of trading was also influenced by mixed US data. As it became known, housing prices in major metropolitan areas have continued to rise in December, although the increase was slightly less than expected. Composite House Price Index for the 20 mega-cities of the S & P / Case-Shiller increased by 5.7 percent compared to the previous year, compared with analysts' estimates, is expected to increase by 5.8 percent.

Another report showed that the consumer confidence indicator from the Conference Board declined in February. The index is currently 92.2 (1985 = 100) as compared to 97.8 in January. the current situation index fell to 112.1 from 116.6, while the expectations index fell from 85.3 to 78.9 in February.

It was also reported that home sales in the secondary market increased by 0.4 percent and reached a seasonally adjusted annual rate of 5.47 million in January from a revised down figure of 5.45 million in December. Sales are now 11.0 per cent higher than a year ago - the largest increase compared to the previous year since July of 2013.

The euro partially recovered against the dollar, returning to the levels of the opening, which was caused by the publication of a controversial US statistics. Previously, pressure on the euro have provided data on the business climate in Germany. the business climate index of the Ifo fell to 105.7 in February from 107.3 in January. According to the forecasts it was expected to decline to 106.7. Meanwhile, the current conditions index rose to 112.9, while economists had forecast it to fall to 112 from 112.5. The expectations index fell to 98.8 from the initial estimate of 102.4 in January. The expected result was 101.6. In turn, the gross domestic product grew by 0.3 percent compared to the third quarter, when it grew at the same pace. Sequential growth rates correspond to the preliminary assessment. Taking into account the calendar of amendments GDP increased by 1.3 percent year on year, followed by expansion of 1.7 percent in the previous quarter. The unadjusted GDP grew by 2.1 per cent per annum in the fourth quarter after increasing 1.7 percent in the previous three months. For the whole 2015, GDP grew by 1.7 percent compared to the previous year, as expected.

-

18:17

European stocks close: stocks closed lower on corporate earnings and a drop in oil prices

Stock indices closed lower on corporate earnings and as oil prices dropped again. Oil prices fell on concerns over the global oil oversupply.

Meanwhile, market participants eyed the economic data from Germany. German Ifo Institute released its business confidence figures for Germany on Tuesday. German business confidence index declines to 105.7 in February from 107.3 in January, missing expectations for a fall to 106.7.

"The majority of companies were pessimistic about their business outlook for the first time in over six months. Assessments of the current business situation, by contrast, were slightly better than last month. German businesses expressed growing concern, especially in manufacturing," Ifo President Hans-Werner Sinn said.

The Ifo current conditions index increased to 112.9 from 112.5. Analysts had expected the index to decline to 112.0.

The Ifo expectations index dropped to 98.8 from 102.3, missing expectations for a decrease to 101.6. January's figure was revised down from 102.4.

Destatis released its final gross domestic product (GDP) growth for Germany on Tuesday. Germany's final GDP gained by 0.3% in the fourth quarter, in line with the preliminary reading, after a 0.3% increase in the third quarter.

The increase was driven by domestic final consumption expenditure. Household consumption expenditure rose by 0.2% in the fourth quarter, while government spending increased by 1.0%.

Exports of goods and services were down 0.6% in fourth quarter, while imports climbed 0.5%.

On a yearly basis, Germany's final GDP rose to 2.1% in the fourth quarter from 1.8% in the third quarter, in line with the preliminary reading.

In 2015 as whole, the economy expanded 1.7%, in line with the preliminary reading.

The Bank of England (BoE) Governor Mark Carney said on Tuesday that the outcome of Britain's referendum was treated like "any other political event which is not to make a judgement on the outcome and assume status quo continues" by the BoE. He added that the central bank wasn't making any judgment on the outcome of the referendum.

Carney noted that a weak pound could help to boost inflation in the U.K., noting that he believed that the recent drop in the pound was caused by the upcoming referendum.

The BoE governor pointed out that the central bank could add further stimulus measures if needed to stimulate the economy.

Indexes on the close:

Name Price Change Change %

FTSE 100 5,962.31 -75.42 -1.25 %

DAX 9,416.77 -156.82 -1.64 %

CAC 40 4,238.42 -60.28 -1.40 %

-

18:12

Oil prices plunge more than 4%

Oil prices slid on concerns over the global oil oversupply. Saudi Arabian Oil Minister Ali Al-Naimi said on Tuesday that the country was not ready to cut its oil output.

Iranian Oil Minister Bijan Namdar Zanganeh said the initiative to freeze the oil production at January level is unrealistic demand on Iran. Iran plans to boost its oil output.

Market participants are awaiting the release of U.S. crude oil inventories data. The American Petroleum Institute (API) is scheduled to release its U.S. oil inventories data later in the day, and U.S. oil inventories data from the U.S. Energy Information Administration is expected on Wednesday.

WTI crude oil for April delivery decreased to $31.75 a barrel on the New York Mercantile Exchange.

Brent crude oil for April rose to $33.29 a barrel on ICE Futures Europe.

-

18:00

European stocks closed: FTSE 100 5,962.31 -75.42 -1.25% CAC 40 4,238.42 -60.28 -1.40% DAX 9,416.77 -156.82 -1.64%

-

17:46

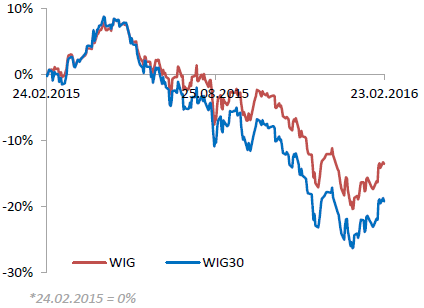

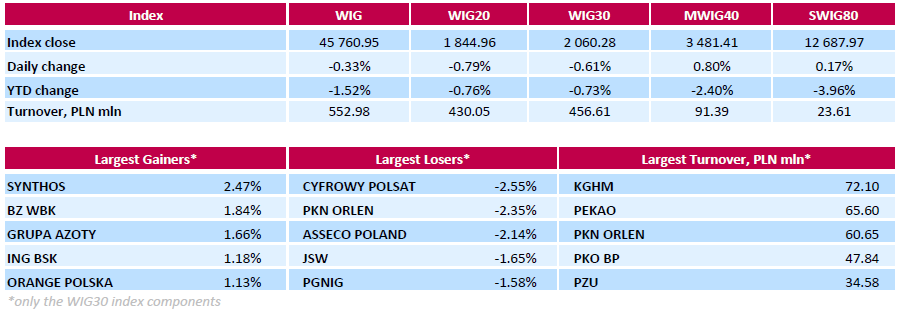

WSE: Session Results

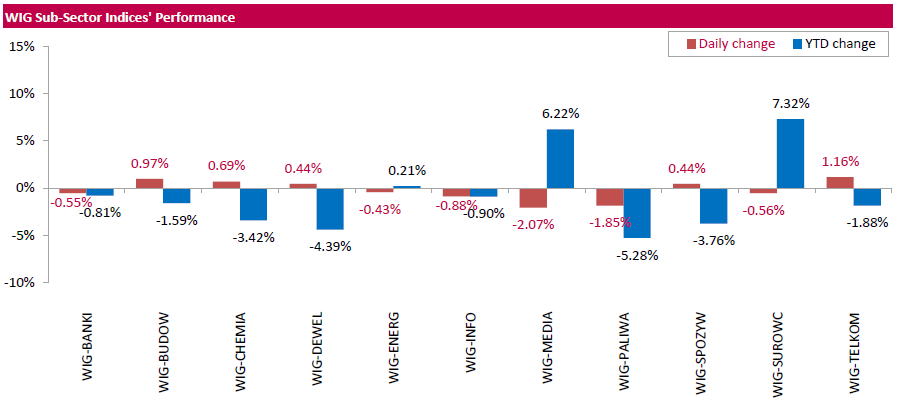

Polish equities closed lower on Tuesday. The broad market measure, the WIG Index, declined by 0.64%. Sector performance within the WIG Index was mixed. Media segment (-2.07%) was the weakest group, while telecoms (+1.16%) outperformed.

Large-cap stocks measure, the WIG30 Index suffered a 0.61% drop. In the index basket, media group CYFROWY POLSAT (WSE: CPS) and oil refiner PKN ORLEN (WSE: PKN) were the sharpest decliners, tumbling by 2.55% and 2.35% respectively. Other biggest laggards were IT-company ASSECO POLAND (WSE: ACP), coking coal producer JSW (WSE: JSW), oil and gas producer PGNIG (WSE: PGN) and FMCG wholesaler EUROCASH (WSE: EUR), plunging by 1.52%-2.14%. On the other side of the ledger, two chemicals names SYNTHOS (WSE: SNS) and GRUPA AZOTY (WSE: ATT), and bank BZ WBK (WSE: BZW) were recorded as the biggest gainers, advancing 2.47%, 1.66% and 1.84% respectively.

-

17:30

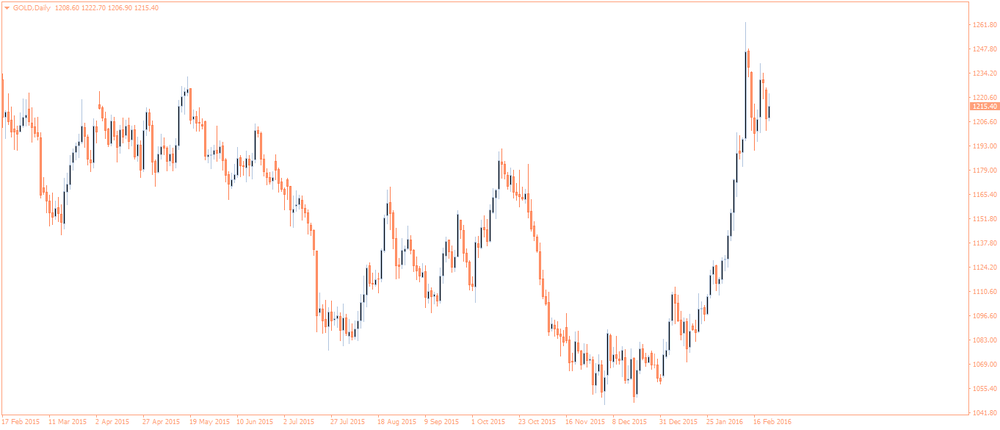

Gold increases more than 1%

Gold price rose on increasing demand for safe-haven assets.

Market participants speculate that the Fed will not raise its interest rate in March. They are focussed on the incoming U.S. economic data. The Conference Board released its consumer confidence index for the U.S. on Tuesday. The index dropped to 92.2 in February from 97.8 in January, missing expectations for a fall to 97.0. The present conditions index dropped to 112.1 in February from 116.6 in January. The Conference Board's consumer expectations index for the next six months decreased to 78.9 in February from 85.3 in January. The percentage of consumers expecting more jobs in the coming months was down to 22.1% in February from 23.0% in January.

The National Association of Realtors released existing homes sales figures in the U.S. on Tuesday. Sales of existing homes rose 0.4% to a seasonally adjusted annual rate of 5.47 million in January from 5.45 in December. Analysts had expected a decrease to 5.32 million units.

"The housing market has shown promising resilience in recent months, but home prices are still rising too fast because of ongoing supply constraints. Despite the global economic slowdown, the housing sector continues to recover and will likely help the U.S. economy avoid a recession," the NAR chief economist Lawrence Yun said.

March futures for gold on the COMEX today rose to 1226.40 dollars per ounce.

-

17:23

Wall Street. Major U.S. stock-indexes fell

Major U.S. stock-indexes lower on Tuesday, failing to sustain yet another rally in what has been a turbulent year so far, as prices of oil and other commodities resumed their declines. Stocks have moved in tandem with volatile oil prices, which are hovering near multi-year lows, as investors see tepid demand for energy as a sign of broader global economic weakness.

Almost all Dow stocks in negative area (26 of 30). Top looser - JPMorgan Chase & Co. (JPM, -3,62%). Top gainer - The Home Depot, Inc. (HD, +1,38%).

Almost all S&P sectors also in negative area. Top gainer - Basic Materials (-2,4%). Top gainer - Conglomerates (+0,7%).

At the moment:

Dow 16421.00 -118.00 -0.71%

S&P 500 1920.25 -16.00 -0.83%

Nasdaq 100 4170.50 -44.25 -1.05%

Oil 31.76 -1.63 -4.88%

Gold 1226.70 +16.60 +1.37%

U.S. 10yr 1.73 -0.03

-

17:16

Bank of England's Monetary Policy Committee member Martin Weale: the strong pound weighed in inflation in the U.K.

The Bank of England's (BoE) Monetary Policy Committee (MPC) member Martin Weale said on Tuesday that the strong pound weighed in inflation in the U.K.

"The fall of the exchange rate does weaken one of the factors holding inflation down. In that sense, it's good news," he commented on the recent drop in the pound.

-

17:10

Bank of England's Monetary Policy Committee member Gertjan Vlieghe: the recent decline in the pound was caused by the uncertainty around the upcoming referendum

The Bank of England's (BoE) Monetary Policy Committee (MPC) member Gertjan Vlieghe said on Tuesday that the recent decline in the pound was caused by the uncertainty around the upcoming referendum.

"It is possible that at some point that increased uncertainty from foreign exchange investors also ends up manifesting itself in increased uncertainty by households and businesses which may or may not reduce or delay their spending," he added.

Vlieghe pointed out that he could vote for an interest rate cut if the downside risks increase.

-

17:02

Bank of England's Deputy Governor Minouche Shafik: the next monetary policy action is likely to be an interest rate hike than an interest rate cut

The Bank of England's (BoE) Deputy Governor Minouche Shafik said on Tuesday that the next monetary policy action was likely to be an interest rate hike than an interest rate cut.

She also said that she expected wages to rise if the U.K. labour market continues to improve. But she could not say when wages would start to pick up.

-

16:57

Richmond Fed Manufacturing Index falls to -4 in February

The Federal Reserve Bank of Richmond released its survey of manufacturing activity on Tuesday. The composite index for manufacturing declined to -4 in February from 2 in January. Analysts had expected the index to remain unchanged at 2.

The decrease was mainly driven by declines in shipments and new orders.

Shipments sub-index slid to -11 in February from -6 in January.

New orders sub-index was down to -6 from 4.

The employment sub-index remained unchanged at 9.

"Shipments and the volume of new orders decreased modestly this month. Manufacturing hiring continued to increase at a modest pace, while average wages grew mildly and the average workweek lengthened slightly. Prices of raw materials and finished goods rose at a slower pace this month, compared to January," the survey said.

-

16:48

U.S. consumer confidence index drops to 92.2 in February

The Conference Board released its consumer confidence index for the U.S. on Tuesday. The index dropped to 92.2 in February from 97.8 in January, missing expectations for a fall to 97.0. January's figure was revised down from 98.1.

The present conditions index dropped to 112.1 in February from 116.6 in January.

The Conference Board's consumer expectations index for the next six months decreased to 78.9 in February from 85.3 in January.

The percentage of consumers expecting more jobs in the coming months was down to 22.1% in February from 23.0% in January.

"Consumers' assessment of current conditions weakened, primarily due to a less favourable assessment of business conditions. Consumers' short-term outlook grew more pessimistic, with consumers expressing greater apprehension about business conditions, their personal financial situation, and to a lesser degree, labour market prospects," the director of economic indicators at The Conference Board, Lynn Franco, said.

-

16:39

U.S. existing homes sales increase 0.4% in January

The National Association of Realtors released existing homes sales figures in the U.S. on Tuesday. Sales of existing homes rose 0.4% to a seasonally adjusted annual rate of 5.47 million in January from 5.45 in December. December's figure was revised down from 5.46 million units.

Analysts had expected a decrease to 5.32 million units.

"The housing market has shown promising resilience in recent months, but home prices are still rising too fast because of ongoing supply constraints. Despite the global economic slowdown, the housing sector continues to recover and will likely help the U.S. economy avoid a recession," the NAR chief economist Lawrence Yun said.

Sales to first-time buyers remained unchanged at 32% in January.

"The spring buying season is right around the corner and current supply levels aren't even close to what's needed to accommodate the subsequent growth in housing demand. Home prices ascending near or above double-digit appreciation aren't healthy - especially considering the fact that household income and wages are barely rising," Yun said.

-

16:00

U.S.: Consumer confidence , February 92.2 (forecast 97.0)

-

16:00

U.S.: Existing Home Sales , January 5.47 (forecast 5.32)

-

15:59

U.S.: Richmond Fed Manufacturing Index, February -4 (forecast 2)

-

15:40

S&P/Case-Shiller home price index rises 5.7% in December

The S&P/Case-Shiller home price index increased 5.7% year-on-year in December, missing expectations for a 5.8% rise, after a 5.7% gain in November. November's figure was revised down from a 5.8% increase.

Portland, San Francisco and Denver were the largest contributors to the rise, where prices climbed by 11.4%, 10.3% and 10.2%, respectively.

"While home prices continue to rise, the pace is slowing a bit," chairman of the index committee at S&P Dow Jones Indices David Blitzer said.

On a monthly basis, the S&P/Case-Shiller home price index was flat in December.

The S&P/Case-Shiller home price index measures single-family home prices in 20 U.S. cities.

-

15:35

U.S. Stocks open: Dow -0.38%, Nasdaq -0.48%, S&P -0.47%

-

15:29

Before the bell: S&P futures -0.01%, NASDAQ futures -0.18%

U.S. stock-index futures fluctuated.

Global Stocks:

Nikkei 16,052.05 -59.00 -0.37%

Hang Seng 19,414.78 -49.31 -0.25%

Shanghai Composite 2,903.95 -23.22 -0.79%

FTSE 6,009.38 -28.35 -0.47%

CAC 4,283.04 -15.66 -0.36%

DAX 9,510.16 -63.43 -0.66%

Crude oil $33.03 (-1.08%)

Gold $1224.50 (+1.19%)

-

15:01

Bank of England Governor Mark Carney: the outcome of Britain's referendum is treated like any other political event by the BoE

The Bank of England (BoE) Governor Mark Carney said on Tuesday that the outcome of Britain's referendum was treated like "any other political event which is not to make a judgement on the outcome and assume status quo continues" by the BoE. He added that the central bank wasn't making any judgment on the outcome of the referendum.

Carney noted that a weak pound could help to boost inflation in the U.K., noting that he believed that the recent drop in the pound was caused by the upcoming referendum.

The BoE governor pointed out that the central bank could add further stimulus measures if needed to stimulate the economy.

"We could cut interest rates towards zero. We could engage in additional asset purchases, including a variety of assets. We could also provide a perspective where we could adjust our policy horizon," he said.

Carney noted that he was against negative interest rates.

-

15:00

Belgium: Business Climate, February -6.6 (forecast -3.6)

-

15:00

U.S.: S&P/Case-Shiller Home Price Indices, y/y, December 5.7% (forecast 5.8%)

-

14:56

Wall Street. Stocks before the bell

(company / ticker / price / change, % / volume)

Home Depot Inc

HD

127

3.38%

70.7K

Barrick Gold Corporation, NYSE

ABX

13.15

2.57%

14.6K

Twitter, Inc., NYSE

TWTR

18.52

1.20%

67.8K

HONEYWELL INTERNATIONAL INC.

HON

105

0.41%

0.2K

Merck & Co Inc

MRK

50.95

0.35%

1.5K

ALTRIA GROUP INC.

MO

61.37

0.26%

1.1K

General Motors Company, NYSE

GM

29.63

0.00%

160.4K

Yahoo! Inc., NASDAQ

YHOO

31.14

-0.10%

22.6K

United Technologies Corp

UTX

92.24

-0.14%

19.1K

Starbucks Corporation, NASDAQ

SBUX

58.78

-0.15%

1K

McDonald's Corp

MCD

117.4

-0.23%

0.1K

Pfizer Inc

PFE

29.97

-0.27%

3.6K

FedEx Corporation, NYSE

FDX

135

-0.29%

0.1K

Nike

NKE

59.98

-0.32%

0.6K

Procter & Gamble Co

PG

81.87

-0.32%

3.8K

Facebook, Inc.

FB

106.74

-0.39%

57.7K

Citigroup Inc., NYSE

C

39.36

-0.40%

6.3K

Ford Motor Co.

F

12.51

-0.40%

6.7K

AT&T Inc

T

36.7

-0.43%

5.0K

Johnson & Johnson

JNJ

104.3

-0.43%

1K

Wal-Mart Stores Inc

WMT

65.35

-0.43%

1.4K

General Electric Co

GE

29.28

-0.44%

22.8K

Exxon Mobil Corp

XOM

82

-0.47%

13.8K

Caterpillar Inc

CAT

66.97

-0.51%

0.2K

Visa

V

72.68

-0.52%

0.8K

International Business Machines Co...

IBM

133.05

-0.54%

4.9K

Amazon.com Inc., NASDAQ

AMZN

556.36

-0.56%

13.4K

Apple Inc.

AAPL

96.31

-0.59%

69.7K

Walt Disney Co

DIS

95.78

-0.61%

8.7K

Verizon Communications Inc

VZ

50.75

-0.63%

5.1K

Goldman Sachs

GS

147.83

-0.65%

1.3K

Intel Corp

INTC

29.16

-0.65%

38.7K

Chevron Corp

CVX

88.2

-0.70%

1.7K

The Coca-Cola Co

KO

43.62

-0.73%

72.6K

Cisco Systems Inc

CSCO

26.43

-0.75%

17.7K

Microsoft Corp

MSFT

52.25

-0.76%

10.1K

Yandex N.V., NASDAQ

YNDX

13.22

-0.83%

1.0K

Google Inc.

GOOG

700.5

-0.84%

0.6K

UnitedHealth Group Inc

UNH

120.05

-1.01%

0.1K

JPMorgan Chase and Co

JPM

57.96

-1.04%

5.0K

Tesla Motors, Inc., NASDAQ

TSLA

175.55

-1.23%

4.9K

ALCOA INC.

AA

8.79

-1.35%

114.7K

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

7.46

-5.93%

341.1K

-

14:51

Upgrades and downgrades before the market open

Upgrades:

Twitter (TWTR) upgraded to Outperform from Market Perform at Raymond James; target $25

Downgrades:

Freeport-McMoRan (FCX) downgraded to Sell from Neutral at Citigroup

Other:

FedEx (FDX) resumed with a Equal-Weight at Morgan Stanley

-

14:49

Swiss National Bank Chairman Thomas Jordan: the options of the monetary policy are not unlimited

The Swiss National Bank (SNB) Chairman Thomas Jordan said in Frankfurt on Tuesday that the options of the monetary policy were not unlimited.

"Despite the expanded set of instruments available, the extent of the monetary policy can achieve is not unlimited," he said.

"The effects of monetary policy measures can wane with duration and dosage, especially when the solution to structural problems lies in adjustments to economic policy," Jordan noted, adding that "central banks must continually weigh the short-term benefits against long-term costs".

He pointed out that the Swiss franc was still overvalued.

-

14:45

Option expiries for today's 10:00 ET NY cut

USD/JPY: 111.00 (USD 250m) 114.50 (500m) 115.00 (570m)

EUR/USD: 1.0700 (EUR 163m) 1.0750 (150m) ) 1.1000 (794m) 1.1140 (436m) 1.1160 (178m)

GBP/USD: 1.4200-05 (GBP 168m)

USD/CHF 0.9920 (USD 200m)

EUR/GBP 0.7825 (EUR 180m) 0.7870 (225m)

AUD/USD: 0.7150 (AUD 241m) 0.7200 (255m)

USD/CAD 1.3840 (USD 310m)

USD/CNY 6.4000 (USD 1.55bln) 6.5000 (1.33bln) 6.5725 (1.1bln)

-

14:33

Foreign exchange market. European session: the euro traded lower against the U.S. dollar after the release of the weak Ifo data from Germany

Economic calendar (GMT0):

(Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual)

07:00 Germany GDP (YoY) (Finally) Quarter IV 1.8% 2.1% 2.1%

07:00 Germany GDP (QoQ) (Finally) Quarter IV 0.3% 0.3% 0.3%

09:00 Germany IFO - Expectations February 102.3 Revised From 102.4 101.6 98.8

09:00 Germany IFO - Business Climate February 107.3 106.7 105.7

09:00 Germany IFO - Current Assessment February 112.5 112.0 112.9

11:15 Switzerland SNB Chairman Jordan Speaks

The U.S. dollar traded mixed against the most major currencies ahead of the release of the U.S. economic data. The S&P/Case-Shiller home price index is expected to rise by 5.8% in December, after a 5.8% gain in November.

The U.S. consumer confidence is expected to decline to 97.0 in February from 98.1 in January.

The existing home sales in the U.S. are expected to fall to 5.32 million units in January from 5.46 million units in December.

The euro traded lower against the U.S. dollar after the release of the weak Ifo data from Germany. German Ifo Institute released its business confidence figures for Germany on Tuesday. German business confidence index declines to 105.7 in February from 107.3 in January, missing expectations for a fall to 106.7.

"The majority of companies were pessimistic about their business outlook for the first time in over six months. Assessments of the current business situation, by contrast, were slightly better than last month. German businesses expressed growing concern, especially in manufacturing," Ifo President Hans-Werner Sinn said.

The Ifo current conditions index increased to 112.9 from 112.5. Analysts had expected the index to decline to 112.0.

The Ifo expectations index dropped to 98.8 from 102.3, missing expectations for a decrease to 101.6. January's figure was revised down from 102.4.

Destatis released its final gross domestic product (GDP) growth for Germany on Tuesday. Germany's final GDP gained by 0.3% in the fourth quarter, in line with the preliminary reading, after a 0.3% increase in the third quarter.

The increase was driven by domestic final consumption expenditure. Household consumption expenditure rose by 0.2% in the fourth quarter, while government spending increased by 1.0%.

Exports of goods and services were down 0.6% in fourth quarter, while imports climbed 0.5%.

On a yearly basis, Germany's final GDP rose to 2.1% in the fourth quarter from 1.8% in the third quarter, in line with the preliminary reading.

In 2015 as whole, the economy expanded 1.7%, in line with the preliminary reading.

The British pound traded mixed against the U.S. dollar on comments by the Bank of England (BoE) Governor Mark Carney. He said on Tuesday that the outcome of Britain's referendum was treated like "any other political event which is not to make a judgement on the outcome and assume status quo continues".

The Swiss franc traded higher against the U.S. dollar. The Swiss National Bank (SNB) Chairman Thomas Jordan said on Tuesday that the options of the monetary policy were not unlimited. He noted that the Swiss franc was still overvalued.

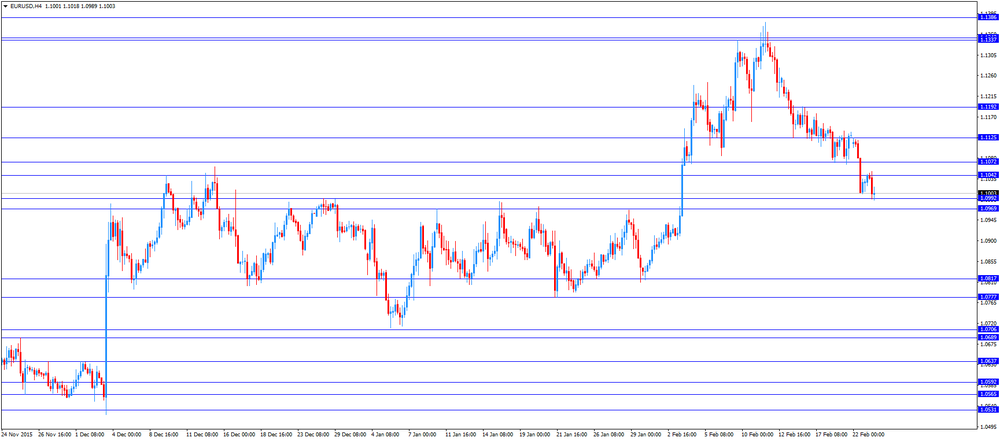

EUR/USD: the currency pair decreased to $1.0989

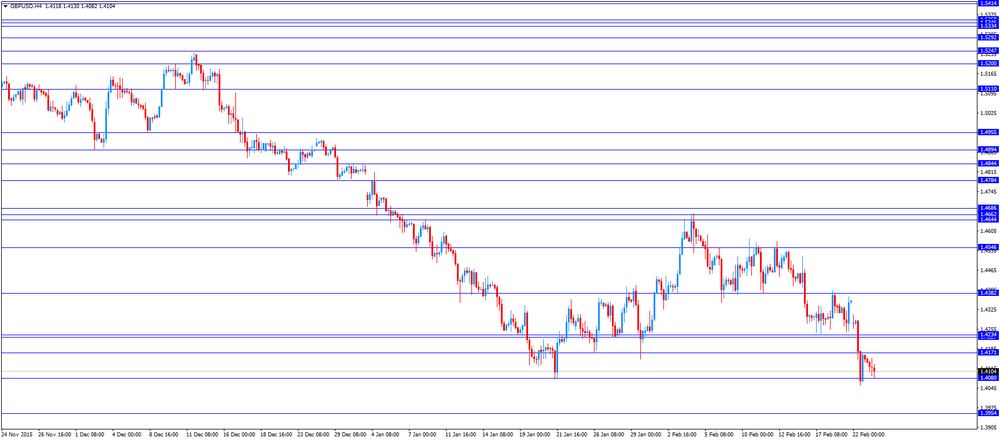

GBP/USD: the currency pair traded mixed

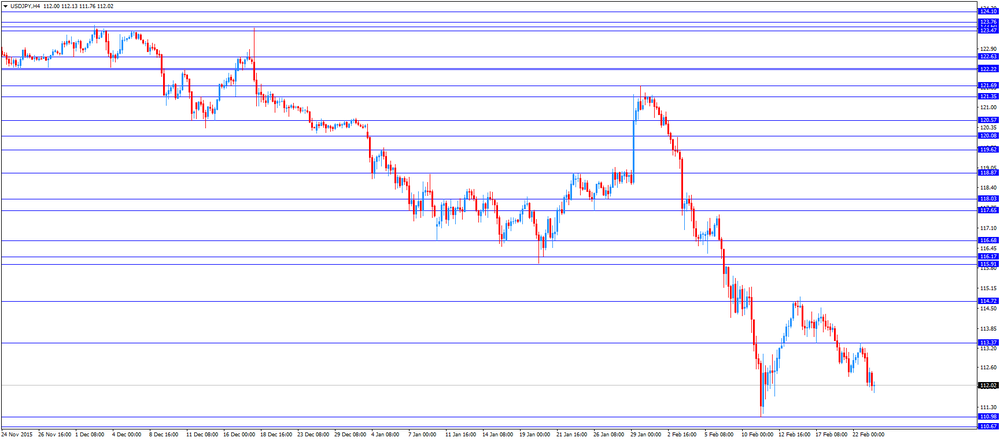

USD/JPY: the currency pair fell to Y111.85

The most important news that are expected (GMT0):

14:00 Belgium Business Climate February -3.0 -3.6

14:00 U.S. S&P/Case-Shiller Home Price Indices, y/y December 5.8% 5.8%

15:00 U.S. Richmond Fed Manufacturing Index February 2 2

15:00 U.S. Existing Home Sales January 5.46 5.32

15:00 U.S. Consumer confidence February 98.1 97.0

17:00 United Kingdom MPC Member Andy Haldane Speaks

-

14:00

Orders

EUR/USD

Offers: 1.1035 1.1050 1.1080 1.1100 1.1120 1.1135 1.1150 1.1165 1.1185 1.1200

Bids: 1.1000 1.0985 1.0965 1.0950 1.0920 1.0900 1.0880 1.0860 1.0830 1.0800

GBP/USD

Offers: 1.4150-55 1.4180 1.4200 1.4220-25 1.4250 1.4265 1.4285 1.4300 1.4325 1.4350

Bids: 1.4100 1.4085-90 1.4070 1.4050 1.4030 1.4000 1.3980 1.3960 1.3925-30 1.3900

EUR/JPY

Offers: 123.50 123.80 124.00 124.50 124.75 125.00 125.50 126.00

Bids: 123.00 122.80 122.50 122.30 122.00

EUR/GBP

Offers: 0.7830-35 0.7850-55 0.7875 0.7884 0.7900

Bids: 0.7800 0.7785-90 0.7765 0.7750 0.7725-30 0.7700

USD/JPY

Offers: 112.20-25 112.50 112.80 113.00 113.20-25 113.40 113.65 113.85 114.00

Bids: 111.85 111.65 111.50 111.30 111.00 110.80 110.50 110.30 110.00

AUD/USD

Offers:0.7265 0.7285 0.7300 0.7320 0.7350

Bids: 0.7220 0.7200 0.7185-90 0.7160 0.7140-45 0.7120 0.7100

-

12:44

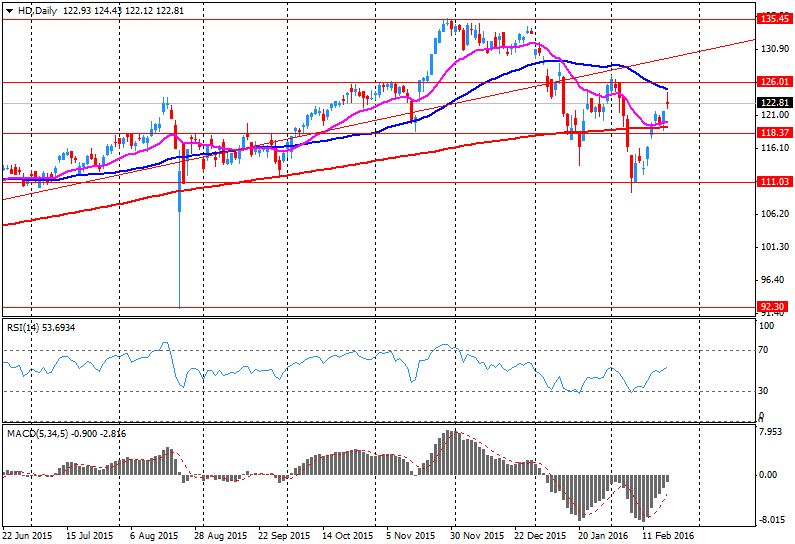

Company News: Home Depot (HD) Q4 Results Beat Analysts’ Expectations

Home Depot reported Q4 FY 2015 earnings of $1.17 per share (versus $1.05 in Q4 FY 2014), beating analysts' consensus of $1.10.

The company's quarterly revenues amounted to $20.980 bln (+9.5% y/y), beating consensus estimate of $20.397 bln.

The company also issued guidance for FY 2016, projecting EPS of $6.12-6.18 versus consensus of $6.15 and revenues of $93.03-93.83 bln (+5.1-6% y/y) versus consensus of $92.92 bln.

Home Depot increased its quarterly dividend by 17% to $0.69/share from $0.59/share.

HD rose to $125.54 (+2.19%) in pre-market trading.

-

12:02

European stock markets mid session: stocks traded lower on corporate earnings and as oil prices fell

Stock indices traded lower on corporate earnings and as oil prices dropped again. Oil prices fell on concerns over the global oil oversupply.

Meanwhile, market participants eyed the economic data from Germany. German Ifo Institute released its business confidence figures for Germany on Tuesday. German business confidence index declines to 105.7 in February from 107.3 in January, missing expectations for a fall to 106.7.

"The majority of companies were pessimistic about their business outlook for the first time in over six months. Assessments of the current business situation, by contrast, were slightly better than last month. German businesses expressed growing concern, especially in manufacturing," Ifo President Hans-Werner Sinn said.

The Ifo current conditions index increased to 112.9 from 112.5. Analysts had expected the index to decline to 112.0.

The Ifo expectations index dropped to 98.8 from 102.3, missing expectations for a decrease to 101.6. January's figure was revised down from 102.4.

Destatis released its final gross domestic product (GDP) growth for Germany on Tuesday. Germany's final GDP gained by 0.3% in the fourth quarter, in line with the preliminary reading, after a 0.3% increase in the third quarter.

The increase was driven by domestic final consumption expenditure. Household consumption expenditure rose by 0.2% in the fourth quarter, while government spending increased by 1.0%.

Exports of goods and services were down 0.6% in fourth quarter, while imports climbed 0.5%.

On a yearly basis, Germany's final GDP rose to 2.1% in the fourth quarter from 1.8% in the third quarter, in line with the preliminary reading.

In 2015 as whole, the economy expanded 1.7%, in line with the preliminary reading.

Current figures:

Name Price Change Change %

FTSE 100 5,992.15 -45.58 -0.75 %

DAX 9,485.24 -88.35 -0.92 %

CAC 40 4,273.61 -25.09 -0.58 %

-

11:52

Bank of Japan (BoJ) Governor Haruhiko Kuroda: the money printing alone would not lead to higher inflation

Bank of Japan (BoJ) Governor Haruhiko Kuroda said before the parliament on Tuesday that the money printing alone would not lead to higher inflation.

"It's not that the monetary base alone will pull up inflation or inflation expectations promptly. We aim to raise prices through an increase in inflation expectations and a tighter gap in supply and demand under QQE [qualitative and quantitative easing measures]," he said.

Kuroda noted that a risk aversion was responsible for the recent market turmoil.

The BoJ Governor pointed out that the central bank's stimulus measures had a positive effect on households and the economic growth.

-

11:31

Japanese Finance Minister Taro Aso: the government could implement additional fiscal stimulus measures

Japanese Finance Minister Taro Aso said before the parliament on Tuesday that the government could implement additional fiscal stimulus measures to support the economy if needed.

"We'll obviously act flexibly on fiscal policy as needed, looking at how the economy performs," he said.

"That will depend on economic conditions," Aso added.

-

11:20

Australia’s leading economic index falls 0.2% in December

The Conference Board (CB) released its leading economic index for Australia on Monday. The leading economic index (LEI) fell 0.2% in December, after a 0.3% rise in November.

The coincident index was increased 0.2% in December, after a 0.5% gain in November.

-

11:07

French manufacturing confidence index remains unchanged at 103 in February

The French statistical office Insee released its manufacturing confidence index for France on Tuesday. The French manufacturing confidence index remained unchanged at 103 in February. January's figure was revised up from 102.

Past change in production index was down to -3 in February from -1 in January.

Personal production expectations index rose to 17 in February from 11 in January, while general production outlook index slid to -4 from 2.

-

10:59

Option expiries for today's 10:00 ET NY cut

USD/JPY: 111.00 (USD 250m) 114.50 (500m) 115.00 (570m)

EUR/USD: 1.0700 (EUR 163m) 1.0750 (150m) ) 1.1000 (794m) 1.1140 (436m) 1.1160 (178m)

GBP/USD: 1.4200-05 (GBP 168m)

USD/CHF 0.9920 (USD 200m)

EUR/GBP 0.7825 (EUR 180m) 0.7870 (225m)

AUD/USD: 0.7150 (AUD 241m) 0.7200 (255m)

USD/CAD 1.3840 (USD 310m)

USD/CNY 6.4000 (USD 1.55bln) 6.5000 (1.33bln) 6.5725 (1.1bln)

-

10:55

German final GDP increases 0.3% in the fourth quarter

Destatis released its final gross domestic product (GDP) growth for Germany on Tuesday. Germany's final GDP gained by 0.3% in the fourth quarter, in line with the preliminary reading, after a 0.3% increase in the third quarter.

The increase was driven by domestic final consumption expenditure. Household consumption expenditure rose by 0.2% in the fourth quarter, while government spending increased by 1.0%.

Exports of goods and services were down 0.6% in fourth quarter, while imports climbed 0.5%.

On a yearly basis, Germany's final GDP rose to 2.1% in the fourth quarter from 1.8% in the third quarter, in line with the preliminary reading.

In 2015 as whole, the economy expanded 1.7%, in line with the preliminary reading.

-

10:39

German Ifo business confidence index declines to 105.7 in February

German Ifo Institute released its business confidence figures for Germany on Tuesday. German business confidence index declines to 105.7 in February from 107.3 in January, missing expectations for a fall to 106.7.

"The majority of companies were pessimistic about their business outlook for the first time in over six months. Assessments of the current business situation, by contrast, were slightly better than last month. German businesses expressed growing concern, especially in manufacturing," Ifo President Hans-Werner Sinn said.

The Ifo current conditions index increased to 112.9 from 112.5. Analysts had expected the index to decline to 112.0.

The Ifo expectations index dropped to 98.8 from 102.3, missing expectations for a decrease to 101.6. January's figure was revised down from 102.4.

-

10:26

Germany's Bertelsmann Foundation’s study: a Schengen collapse could cost up to €1.4 trillion or 10% of GDP between 2016 and 2025

Germany's Bertelsmann Foundation said in its study on Monday that a Schengen collapse could cost up to €1.4 trillion or 10% of GDP between 2016 and 2025.

"If border controls are reinstated within Europe, already weak growth will come under additional pressure," president of Bertelsmann, Aart De Geus, said.

-

10:20

Citi: the likelihood for Brexit increases

Citi said on Monday that the likelihood for Brexit increased to 30-40% from 20-30%, adding that investors would become nervous.

"The effects of Brexit, if it happens, are likely to be large and painful in economic and political terms, both for the UK and the overall EU," UK economist at Citi, Michael Saunders, wrote.

-

10:12

Italian Prime Minister Matteo Renzi: Brexit would hurt more Britain than the EU

Italian Prime Minister Matteo Renzi said on Monday that Brexit would hurt more Britain than the EU.

"I hope Britain remains inside the EU, but if it leaves, the consequences will be worse for British citizens than for European ones. If Great Britain leaves, the main problem will be for the UK, its businesses and its citizens," he said.

Britain's Prime Minister David Cameron said on Saturday that the referendum will take place on June 23. Cameron secured a deal with the EU, which includes changes to migrant welfare payments, safeguards that Britain would not be a part of the Eurozone and safeguards for Britain's financial sector.

-

10:00

Germany: IFO - Business Climate, February 105.7 (forecast 106.7)

-

10:00

Germany: IFO - Current Assessment , February 112.9 (forecast 112.0)

-

10:00

Germany: IFO - Expectations , February 98.8 (forecast 101.6)

-

08:25

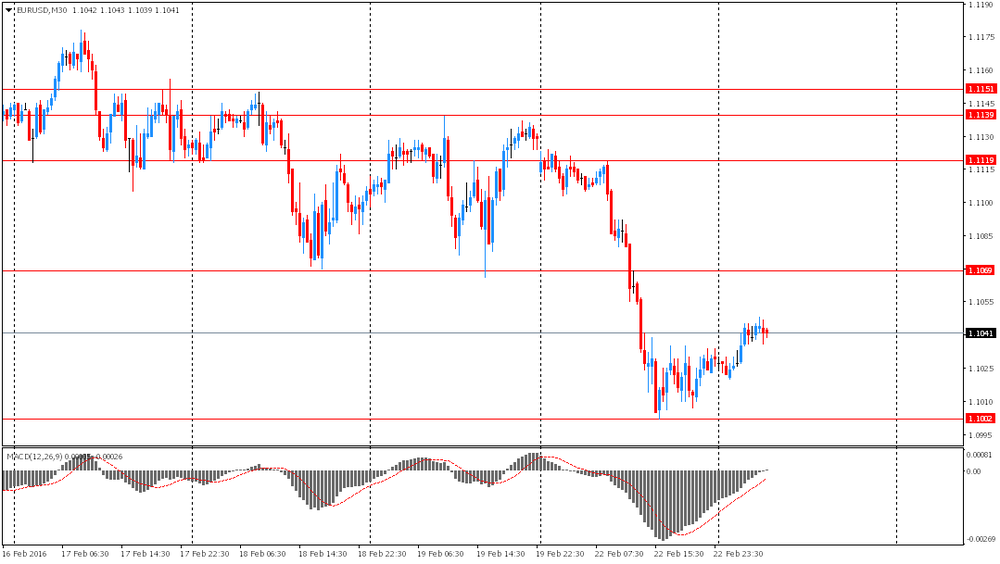

Options levels on tuesday, February 23, 2016:

EUR / USD

Resistance levels (open interest**, contracts)

$1.1226 (4759)

$1.1153 (3872)

$1.1098 (5111)

Price at time of writing this review: $1.1041

Support levels (open interest**, contracts):

$1.0994 (1983)

$1.0958 (3120)

$1.0933 (7818)

Comments:

- Overall open interest on the CALL options with the expiration date March, 4 is 65480 contracts, with the maximum number of contracts with strike price $1,1000 (5111);

- Overall open interest on the PUT options with the expiration date March, 4 is 92014 contracts, with the maximum number of contracts with strike price $1,1000 (7818);

- The ratio of PUT/CALL was 1.41 versus 1.43 from the previous trading day according to data from February, 22

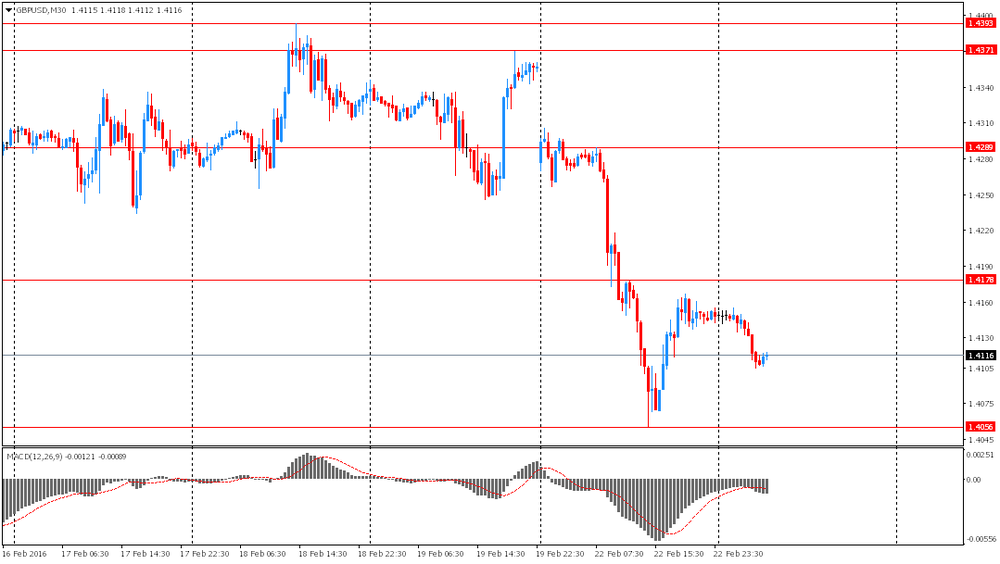

GBP/USD

Resistance levels (open interest**, contracts)

$1.4404 (678)

$1.4306 (1499)

$1.4210 (255)

Price at time of writing this review: $1.4098

Support levels (open interest**, contracts):

$1.3993 (1771)

$1.3896 (1199)

$1.3797 (392)

Comments:

- Overall open interest on the CALL options with the expiration date March, 4 is 27702 contracts, with the maximum number of contracts with strike price $1,4650 (1621);

- Overall open interest on the PUT options with the expiration date March, 4 is 28444 contracts, with the maximum number of contracts with strike price $1,4350 (2956);

- The ratio of PUT/CALL was 1.03 versus 0.96 from the previous trading day according to data from February, 22

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

08:00

Germany: GDP (QoQ), Quarter IV 0.3% (forecast 0.3%)

-

08:00

Germany: GDP (YoY), Quarter IV 2.1% (forecast 2.1%)

-

07:58

Foreign exchange market. Asian session: the euro climbed

The euro climbed after falling on weak economic data yesterday. The single currency is also supported by optimistic expectations for today's publication of final German GDP for the fourth quarter. The German economy is expected to have grown by 0.3% q/q and by 2.1% y/y.

The pound continued declining amid growing fears of the U.K.'s exit from the European Union. Moody's warned that the country's rating could be revised in case it leaves the union. Some economists believe that U.K. exit would result in capital outflows and weaker economic growth.

The Australian dollar is supported by weekly consumer confidence data from ANZ Roy Morgan.The corresponding index rose by 0.6% to 114.3 in the week ending February 21 from 113.6 reported previously. Analysts explain this increase by weaker influence from financial markets instability.

EUR/USD: the pair rose to $1.1045 in Asian trade

USD/JPY: the pair fell to Y111.95

GBP/USD: the pair fell to $1.4105

The most important news that are expected (GMT0):

(time / country / index / period / previous value / forecast)

07:00 Germany GDP (YoY) (Finally) Quarter IV 1.8% 2.1%

07:00 Germany GDP (QoQ) (Finally) Quarter IV 0.3% 0.3%

09:00 Germany IFO - Expectations February 102.4 101.6

09:00 Germany IFO - Business Climate February 107.3 106.7

09:00 Germany IFO - Current Assessment February 112.5 112.0

11:15 Switzerland SNB Chairman Jordan Speaks

14:00 Belgium Business Climate February -3.0 -3.6

14:00 U.S. S&P/Case-Shiller Home Price Indices, y/y December 5.8% 5.8%

15:00 U.S. Richmond Fed Manufacturing Index February 2 2

15:00 U.S. Existing Home Sales January 5.46 5.32

15:00 U.S. Consumer confidence February 98.1 97.0

17:00 United Kingdom MPC Member Andy Haldane Speaks

-

07:41

Oil retreated

West Texas Intermediate futures for April delivery fell to $32.79 (-1.80%), while Brent crude dropped to $34.12 (-1.64%) as market participants assessed a generally bearish report from the International Energy Agency. The agency estimates that U.S. oil output will decline by 600,000 barrels per day by the end of 2016. Nevertheless oil prices are unlikely to sustain gains as the supply glut will persist in the near-term future. Analysts believe that it will take more time to stabilize the market.

-

07:24

Gold climbed on weaker Asian stocks

Gold climbed to $1,217.90 (+0.64%) after Asian stocks reversed gains on lower oil prices. Analysts say that a rally in stocks could put pressure on the precious metal. Meanwhile physical demand in top consumers India and China struggled. Prices in both countries fell.

Nevertheless inflows data suggest that investors are interested in gold. Holdings of SPDR Gold Trust, the largest gold-backed exchange-traded-fund, rose by 2.64% to 752.29 tonnes on Monday. This year's inflows have already outrun outflows for the whole of 2015.

-

07:10

Global Stocks: U.S. stock indices gained

U.S. stock indices rose on Monday amid an increase in oil prices underlining persistent connection between oil and stocks.

The Dow Jones Industrial Average gained 228.67 points, or 1.4%, to 16,620.66 29 out its 30 components advanced). The S&P 500 rose 27.72 points, or 1.4%, to 1,945.50 (its oil prices rose 2.2%). The Nasdaq Composite rose 66.18 points, or 1.5%, to 4,570.61.

Data from Markit Economics showed that the U.S. manufacturing PMI slid to 51.0 in February on a seasonally adjusted basis from 52.4 in January. The country's manufacturing sector lost momentum after a modest recovery at the beginning of 2016. Weaker output and new orders sub-indices weighed on the PMI.

This morning in Asia Hong Kong Hang Seng lost 0.39%, or 76.05 points, to 19,388.04. China Shanghai Composite Index fell 0.98%, or 28.75 points, to 2,898.43. Meanwhile the Nikkei declined 0.35%, or 56.74 points, to 16,054.31.

Asian stock indices retreated as investors took profits from a 2% rally in the previous session. However analysts note that stocks should climb as they normally do before China's National People's Congress, which starts on March 5 this year.

-

03:02

Nikkei 225 16,178.02 +66.97 +0.42 %, Hang Seng 19,482.77 +18.68 +0.10 %, Shanghai Composite 2,920.15 -7.02 -0.24 %

-

00:32

Commodities. Daily history for Feb 22’2016:

(raw materials / closing price /% change)

Oil 31.43 -0.16%

Gold 1,208.90 -0.10%

-

00:31

Stocks. Daily history for Sep Feb 22’2016:

(index / closing price / change items /% change)

S&P/ASX 200 5,001.22 +48.43 +0.98%

TOPIX 1,300 +8.18 +0.63%

SHANGHAI COMP 2,927.73 +67.71 +2.37%

HANG SENG 19,464.09 +178.59 +0.93%

FTSE 100 6,037.73 +87.50 +1.47 %

CAC 40 4,298.7 +75.66 +1.79 %

Xetra DAX 9,573.59 +185.54 +1.98 %

S&P 500 1,945.5 +27.72 +1.45 %

NASDAQ Composite 4,570.61 +66.18 +1.47 %

Dow Jones 16,620.66 +228.67 +1.40 %

-

00:30

Currencies. Daily history for Feb 22’2016:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,1029 -0,91%

GBP/USD $1,4148 -1,48%

USD/CHF Chf0,9995 +0,94%

USD/JPY Y112,89 +0,22%

EUR/JPY Y124,52 -0,67%

GBP/JPY Y159,7 -1,26%

AUD/USD $0,7226 +1,08%

NZD/USD $0,6697 +0,96%

USD/CAD C$1,3704 -0,46%

-

00:00

Schedule for today, Tuesday, Feb 23’2016:

(time / country / index / period / previous value / forecast)

07:00 Germany GDP (YoY) (Finally) Quarter IV 1.8% 2.1%

07:00 Germany GDP (QoQ) (Finally) Quarter IV 0.3% 0.3%

09:00 Germany IFO - Expectations February 102.4 101.6

09:00 Germany IFO - Business Climate February 107.3 106.7

09:00 Germany IFO - Current Assessment February 112.5 112.1

14:00 Belgium Business Climate February -3.0 -3.7

14:00 U.S. S&P/Case-Shiller Home Price Indices, y/y December 5.8% 5.8%

15:00 U.S. Richmond Fed Manufacturing Index February 2

15:00 U.S. Existing Home Sales January 5.46 5.35

15:00 U.S. Consumer confidence February 98.1 97.3

-