Noticias del mercado

-

22:45

New Zealand: Visitor Arrivals, January 13.6%

-

21:00

Dow -0.14% 16,409.49 -22.29 Nasdaq +0.32% 4,518.15 +14.57 S&P -0.02% 1,920.92 -0.35

-

20:20

American focus: the pound has updated a seven-year low against the dollar

The dollar significantly weakened against the euro, reaching a minimum of yesterday's session, the cause of which were technical factors, as well as weak US data. The preliminary report submitted at Markit, showed that activity in the US service sector deteriorated sharply in February, reaching a 28-month low and completing the 27-month series of sustainable expansion. Pre-Purchasing Managers Index (PMI) for the services sector fell in February to 49.8 points versus 53.2 points in January. Economists had expected the index to rise to 53.5. Recall index value below 50 indicates contraction in activity in the sector. Respondents reported that the weak growth in new orders and uncertainty were the main cause of the deterioration of the activity of the economic outlook in February. Negative impact also had outages related to the heavy snowfall on the east coast of the country. The data showed that new orders growth slowed for the third consecutive time. Meanwhile, the employment index dropped to the lowest level since the end of 2009. Seasonally adjusted, the composite PMI index was 50.1 points against 53.2 in January.

Another report from the Commerce Department showed that sales of new buildings in the US fell in January to a 10-month high against the background of falling sales in the Western region, but in general the housing market recovery remains intact. Sales fell 9.2 percent to a seasonally adjusted annual rate reached 494,000 units, after a sharp increase in December. December sales rates have not been revised (544,000 units). Economists had forecast that sales of new homes, which account for about 8.3 percent of the housing market, will drop to 520 000 last month. Sales in the West, who noted a sharp increase in housing prices on the background of moderate reserves, fell by 32.1 percent to 110,000, the lowest level since July, 2014. Moreover, the percentage decline was the largest since May 2010. Last month, inventories of new homes on the market increased by 2.1 percent to 238 000 units, the highest level since October 2009. However, the housing is restrained.

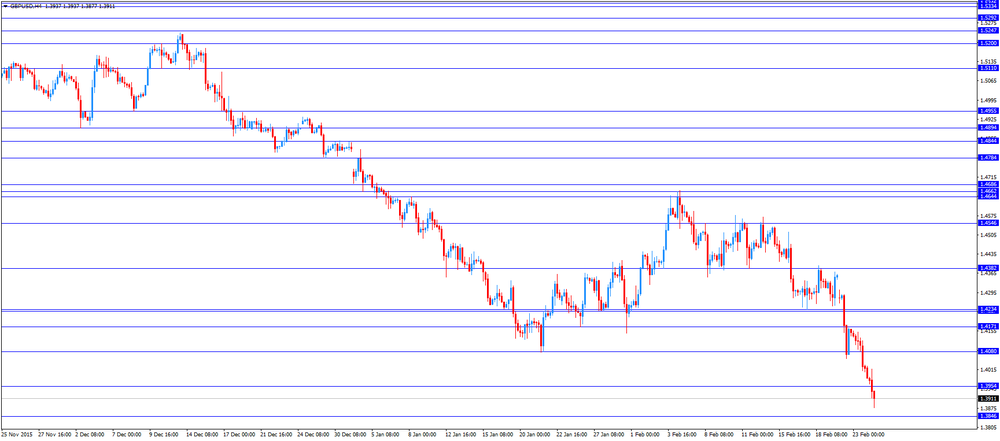

The British pound continued to fall today, updating the seven-year low against the dollar. The pressure on the currency has a British exit from the EU perspective. Analysts believe that because of the uncertainty about the upcoming vote, investors will abandon the investment in UK assets. Analysts at HSBC said that voting for a way out of the EU would lead to a further drop in the pound by 15% -20% against the dollar. The Bank believes that the likelihood of such a development of events is equal to one-third.

Little also had the effect of today's data on Britain. British Bankers' Association reported that the number of mortgage approvals increased to 47,509 in January to 43,660 in December. It was the highest since February 2014 and well above the expected level of 45 200 Gross mortgage borrowing rose to 13.6 billion pounds from 12.4 billion pounds. This was 38 percent higher than a year ago and the highest since mid-2008. Borrowing to buy a house amounted to 8.6 billion pounds, compared with 7.7 billion pounds in the last month.

In addition, a quarterly survey from the Confederation of British Industry showed that retail sales balance fell to 10 percent in February. It was predicted drop in the next month to 2 percent, which would be the slowest since May 2013. "In general, conditions remain challenging for retailers - Raine said Newton-Smith, director of economics at the CBI -. While sales continued to grow and increased optimism expectations of sales growth are weak and retailers are still afraid to invest. " However, respondents expect a decent improvement in business conditions within 3 months.

The Swiss franc strengthened against the US dollar, reaching a peak on 16 February that it was due to the widespread weakening of the US currency and the publication of positive data on Switzerland. The results of the poll of investment bank UBS showed that consumer activity indicator rose again at the beginning of the year, mainly led by the improvement in consumer sentiment in the conditions of low oil prices and a marked increase in vehicle registrations. The indicator of consumer activity in Switzerland rose to 1.66 points from 1.61 in December, revised from 1.62, which was reported previously. Thus, the index extended its upward trend in the new year. "Improvement of the UBS indicator of consumer activity sends a positive signal to private consumption, - stated in the UBS bank -. However, unemployment may rise in the first half of this year, in response to the slowdown in GDP growth last year, thus holding back private consumption . " Investment bank UBS expects the labor market to recover in the second half of the year, which can lead to an increase in private consumption of 1.4 percent this year.

-

18:10

Wages in Australia rise 0.6% in the fourth quarter

The Australian Bureau of Statistics released its wage price data on Wednesday. Wages in Australia rose at a seasonally adjusted rate of 0.6% in the fourth quarter, missing forecasts of a 0.6% gain, after a 0.6% increase in the previous quarter.

Both public and private wages increased 0.5% in the fourth quarter.

On a yearly basis, wages climbed 2.2% in the fourth quarter, missing expectations for a 2.3% increase, after a 2.3% gain in the third quarter.

On a yearly basis, private wages were up 2.0% in the fourth quarter, while public wages jumped 2.6%.

-

18:08

Wall Street. Major U.S. stock-indexes fell

Major U.S. stock-indexes lower on Wednesday, as energy stocks took a hit from a slide in oil prices after Saudi Arabia ruled out a cut in output to help tackle a global glut.

Almost all Dow stocks in negative area (27 of 30). Top looser - The Boeing Company (BA, -2,93%). Top gainer - United Technologies Corporation (UNH, +1,40%).

All S&P sectors in negative area. Top gainer - Financial (-1,5%).

At the moment:

Dow 16264.00 -132.00 -0.81%

S&P 500 1903.00 -13.00 -0.68%

Nasdaq 100 4130.25 -29.00 -0.70%

Oil 31.81 -0.06 -0.19%

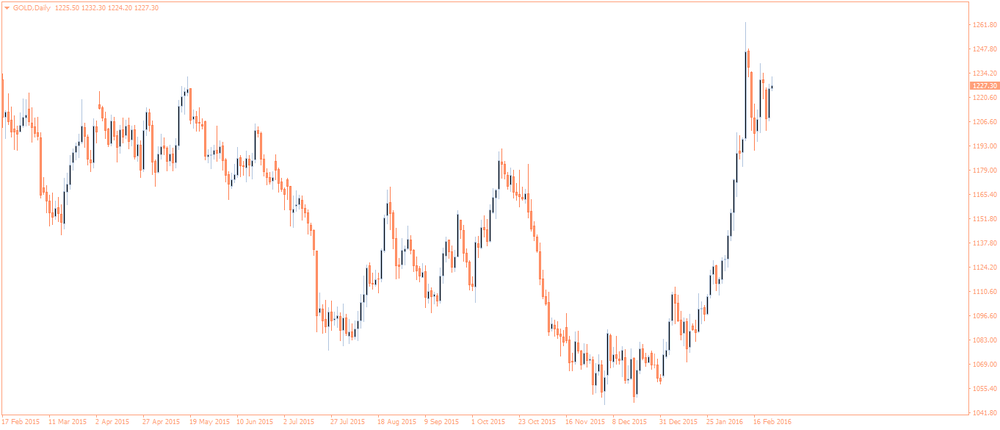

Gold 1245.50 +22.90 +1.87%

U.S. 10yr 1.69 -0.06

-

18:07

Construction work done in Australia drops 3.6% in the fourth quarter

The Australian Bureau of Statistics released its construction work done figures on Wednesday. Construction work done in Australia dropped 3.6% in the fourth quarter, missing forecasts of a 2.0% fall, after a 1.8% decrease in the previous quarter. The third quarter's figure was revised up from a 3.6% decline.

The seasonally adjusted estimate of total building work done rose 2.7% in the fourth quarter, while engineering work slid 9.5%.

On a yearly basis, total construction work plunged 4.3% in the fourth quarter.

-

18:00

European stocks close: stocks closed lower on a drop in oil prices

Stock indices closed lower as oil prices continued to decline. Oil prices fell on the U.S. crude oil inventories data and on comments by Saudi Arabian Oil Minister Ali Al-Naimi. He said that there will be no cut in oil output.

European Central Bank (ECB) Governing Council member and Deutsche Bundesbank President Jens Weidmann said Wednesday that the economic recovery would continue this year. He noted that the German economy was in good shape. Weidmann warned that further stimulus measures could entail longer-term risks and side-effects "that it would be dangerous to simply ignore".

Meanwhile, market participants eyed the economic data from France. French statistical office INSEE released its consumer confidence index for France on Wednesday. French consumer confidence index fell to 95 in February from 97 in January. Analysts had expected the index to remain unchanged at 97.

The British Bankers' Association (BBA) released the number of mortgage approvals in the U.K. on Wednesday. The number of mortgage approvals rose to 47,509 in January from 43,660 in December, exceeding expectations for a rise to 45,200. It was the highest level since February 2014.

The Confederation of British Industry (CBI) released its retail sales balance data on Wednesday. The CBI retail sales balance plunged to +10% in February from +16% in January. It was the lowest level since May 2013. Sales growth is expected to slow next month, while orders are expected to decline.

Indexes on the close:

Name Price Change Change %

FTSE 100 5,867.18 -95.13 -1.60 %

DAX 9,167.8 -248.97 -2.64 %

CAC 40 4,155.34 -83.08 -1.96 %

-

18:00

European stocks closed: FTSE 100 5,867.18 -95.13 -1.60% CAC 40 4,155.34 -83.08 -1.96% DAX 9,167.8 -248.97 -2.64%

-

17:49

Oil prices continue to decline

Oil prices slid on the U.S. crude oil inventories data and on comments by Saudi Arabian Oil Minister Ali Al-Naimi. He said that there will be no cut in oil output.

The U.S. Energy Information Administration (EIA) released its crude oil inventories data on Wednesday. U.S. crude inventories rose by 3.5 million barrels to 507.6 million in the week to February 19.

Analysts had expected U.S. crude oil inventories to rise by 3.17 million barrels.

Gasoline inventories decreased by 2.2 million barrels, the first decline since November, according to the EIA.

Crude stocks at the Cushing, Oklahoma, increased by 333,000 barrels.

U.S. crude oil imports decreased by 117,000 barrels per day.

Refineries in the U.S. were running at 87.3% of capacity, down from 88.3% the previous week.

WTI crude oil for April delivery decreased to $31.00 a barrel on the New York Mercantile Exchange.

Brent crude oil for April rose to $32.70 a barrel on ICE Futures Europe.

-

17:45

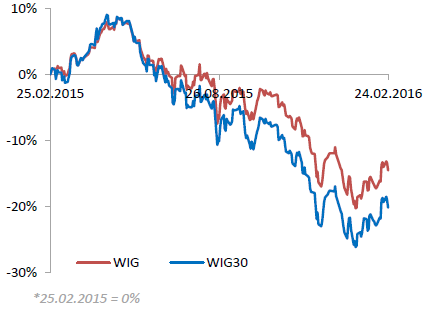

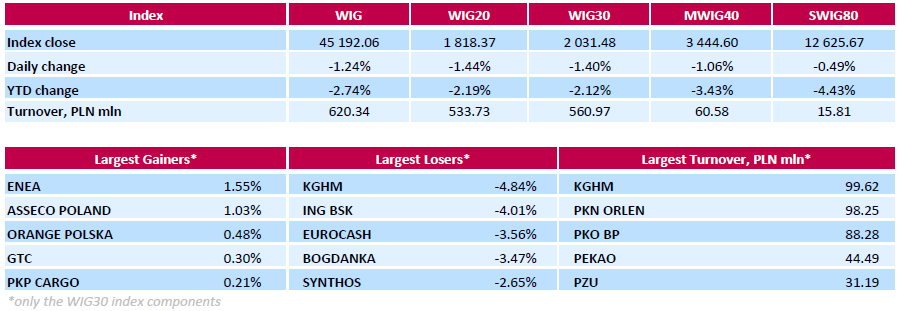

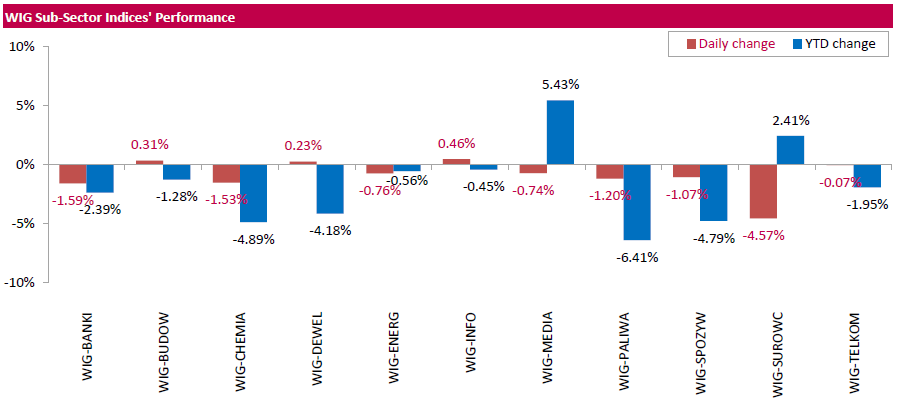

WSE: Session Results

Polish equity market closed lower on Wednesday. The broad market measure, the WIG index, fell by 1.24%. Sector-wise, materials (-4.57%) fared the worst, while informational technology sector (+0.46%) was the best-performer.

The large-cap stocks' gauge, the WIG30 Index, dropped by 1.4%. A majority of the index components recorded declines. Copper producer KGHM (WSE: KGH) posted the biggest drop, down by 4.84%, amid sliding prices for copper. Other most prominent losers were FMCG wholesaler EUROCASH (WSE: EUR), thermal coal miner BOGDANKA (WSE: LWB), chemical producer SYNTHOS (WSE: SNS) and two banks ING BSK (WSE: ING) and PKO BP (WSE: PKO), which lost between 2.64% and 4.01%. At the same time, genco ENEA (WSE: ENA) and IT-company ASSECO POLAND (WSE: ACP) led a handful of gainers, adding 1.55% and 1.03% respectively.

-

17:30

Gold increases around 2%

Gold price rose on increasing demand for safe-haven assets as global stocks and oil prices declined. A weaker U.S. dollar also supported gold. The U.S. dollar fell against other currencies after the release of the weak U.S. economic data. Markit Economics released its preliminary services purchasing managers' index (PMI) for the U.S. on Wednesday. The U.S. preliminary services purchasing managers' index (PMI) dropped to 49.8 in February from 53.2 in January. It was the lowest level since October 2013. Analysts had expected the index to rise to 53.5.

The U.S. Commerce Department released new home sales data on Wednesday. New home sales slid 9.2% to a seasonally adjusted annual rate of 494,000 units in January from 544,000 units in December. Analysts had expected new home sales to reach 520,000 units.

March futures for gold on the COMEX today rose to 1247.50 dollars per ounce.

-

17:15

European Central Bank Governing Council member and Deutsche Bundesbank President Jens Weidmann: the economic recovery would continue this year

European Central Bank (ECB) Governing Council member and Deutsche Bundesbank President Jens Weidmann said Wednesday that the economic recovery would continue this year.

"The euro area's gradual economic recovery is likely to continue in the rest of this year and in 2017," he said.

Weidmann noted that the German economy was in good shape.

"While wage growth was marked, inflation remained subdued; this led to a distinct rise in real disposable income," Bundesbank president added.

Weidmann warned that further stimulus measures could entail longer-term risks and side-effects "that it would be dangerous to simply ignore".

-

16:51

U.S. crude inventories rise by 3.5 million barrels to 507.6 million in the week to February 19

The U.S. Energy Information Administration (EIA) released its crude oil inventories data on Wednesday. U.S. crude inventories rose by 3.5 million barrels to 507.6 million in the week to February 19.

Analysts had expected U.S. crude oil inventories to rise by 3.17 million barrels.

Gasoline inventories decreased by 2.2 million barrels, the first decline since November, according to the EIA.

Crude stocks at the Cushing, Oklahoma, increased by 333,000 barrels.

U.S. crude oil imports decreased by 117,000 barrels per day.

Refineries in the U.S. were running at 87.3% of capacity, down from 88.3% the previous week.

-

16:37

Richmond Fed President Jeffrey Lacker: interest rate hikes are still possible this year

Richmond Fed President Jeffrey Lacker said in a speech on Wednesday that interest rate hikes are still possible this year. He noted that the Fed's federal-funds rate, adjusted for inflation, was below the natural rate.

"In fact, this perspective would bolster the case for raising the federal funds rate target," Lacker said.

He pointed out that the monetary policy's effect on real economic activity was limited and temporary.

Lacker is not a voting member of the Federal Open Market Committee (FOMC) this year.

-

16:30

U.S.: Crude Oil Inventories, February 3.502 (forecast 3.165)

-

16:26

Kansas City Fed President Esther George: the Fed should consider to raise its interest rate at its monetary policy meeting in March

Kansas City Fed President Esther George said in an interview with Bloomberg Radio on Tuesday that the Fed should consider to raise its interest rate at its monetary policy meeting in March.

"It absolutely should be on the table," she said.

Kansas City Fed president added that there was no fundamental shift in the outlook.

George is a voting member of the Federal Open Market Committee (FOMC) this year.

-

16:18

New home sales in the U.S. slide 9.2% in January

The U.S. Commerce Department released new home sales data on Wednesday. New home sales slid 9.2% to a seasonally adjusted annual rate of 494,000 units in January from 544,000 units in December.

Analysts had expected new home sales to reach 520,000 units.

The decrease was mainly driven lower sales in the West region. New home sales in the West region plunged 32.1% in January.

-

16:13

U.S. preliminary services purchasing managers' index drops to 49.8 in February, the lowest level since October 2013

Markit Economics released its preliminary services purchasing managers' index (PMI) for the U.S. on Wednesday. The U.S. preliminary services purchasing managers' index (PMI) dropped to 49.8 in February from 53.2 in January. It was the lowest level since October 2013.

Analysts had expected the index to rise to 53.5.

A reading below 50 indicates contraction in economic activity.

The drop was driven by a softer growth in new work, the slowest since late-2009.

"The PMI survey data show a significant risk of the US economy falling into contraction in the first quarter. The flash PMI for February shows business activity stagnating as growth slowed for a third successive month. Slumping business confidence and an increased downturn in order book backlogs suggest there's worse to come," Markit Chief Economist Chris Williamson said.

-

16:00

U.S.: New Home Sales, January 494 (forecast 520)

-

15:45

U.S.: Services PMI, February 49.8 (forecast 53.5)

-

15:34

U.S. Stocks open: Dow -1.02%, Nasdaq -1.27%, S&P -1.06%

-

15:26

Before the bell: S&P futures -0.84%, NASDAQ futures -1.17%

U.S. stock-index futures dropped.

Global Stocks:

Nikkei 15,915.79 -136.26 -0.85%

Hang Seng 19,192.45 -222.33 -1.15%

Shanghai Composite 2,929.57 +26.24 +0.90%

FTSE 5,878.01 -84.30 -1.41%

CAC 4,150.01 -88.41 -2.09%

DAX 9,191.62 -225.15 -2.39%

Crude oil $30.92 (-2.98%)

Gold $1241.80 (+1.57%)

-

14:59

Japan's final leading index declines to 102.1 in December, the lowest level since January 2013

Japan's Cabinet Office released its final leading index data on Wednesday. The leading index decreased to 102.1 in December from 103.2 in November, up from the preliminary estimate of 102.0. It was the lowest level since January 2013.

November's figure was revised down from 103.5.

Japan's coincident index was down to 110.9 in December from 111.9 in November, down from the preliminary reading of 111.2.

-

14:59

Wall Street. Stocks before the bell

(company / ticker / price / change, % / volume)

Barrick Gold Corporation, NYSE

ABX

14.12

4.28%

136.1K

AT&T Inc

T

36.64

-0.27%

7.6K

International Business Machines Co...

IBM

131.84

-0.42%

0.2K

ALTRIA GROUP INC.

MO

61.26

-0.42%

1.8K

McDonald's Corp

MCD

116.35

-0.47%

1K

Pfizer Inc

PFE

29.81

-0.50%

1.2K

The Coca-Cola Co

KO

43.47

-0.50%

3.6K

Merck & Co Inc

MRK

50.27

-0.53%

0.3K

Procter & Gamble Co

PG

81.3

-0.62%

1.1K

Yandex N.V., NASDAQ

YNDX

12.83

-0.62%

7.2K

AMERICAN INTERNATIONAL GROUP

AIG

50.74

-0.63%

0.1K

Wal-Mart Stores Inc

WMT

66.05

-0.65%

6.1K

Verizon Communications Inc

VZ

50.28

-0.69%

0.6K

Yahoo! Inc., NASDAQ

YHOO

30.45

-0.72%

6.5K

Travelers Companies Inc

TRV

107.12

-0.73%

0.2K

Walt Disney Co

DIS

94.65

-0.77%

1.4K

American Express Co

AXP

54.68

-0.78%

0.3K

United Technologies Corp

UTX

90.85

-0.82%

0.9K

Nike

NKE

59.7

-0.85%

0.3K

General Electric Co

GE

28.97

-0.86%

28.4K

Johnson & Johnson

JNJ

103.11

-0.93%

1.0K

Intel Corp

INTC

28.53

-0.94%

10.7K

Hewlett-Packard Co.

HPQ

10.21

-0.97%

0.1K

Cisco Systems Inc

CSCO

25.85

-1.03%

2.0K

Microsoft Corp

MSFT

50.65

-1.04%

61.7K

Boeing Co

BA

115.65

-1.07%

0.5K

Apple Inc.

AAPL

93.67

-1.08%

157.4K

Facebook, Inc.

FB

104.28

-1.12%

32.0K

Google Inc.

GOOG

687.75

-1.16%

0.8K

Caterpillar Inc

CAT

65

-1.19%

2.9K

Home Depot Inc

HD

123

-1.23%

3.2K

Goldman Sachs

GS

143.01

-1.31%

9.3K

Exxon Mobil Corp

XOM

80.11

-1.38%

2.8K

Chevron Corp

CVX

83.55

-1.60%

7.8K

Amazon.com Inc., NASDAQ

AMZN

544.1

-1.60%

9.0K

Starbucks Corporation, NASDAQ

SBUX

57.52

-1.61%

0.6K

JPMorgan Chase and Co

JPM

55.21

-1.62%

31.9K

Citigroup Inc., NYSE

C

37.6

-1.62%

15.1K

Visa

V

70.81

-1.86%

3.6K

General Motors Company, NYSE

GM

28.83

-1.87%

4.1K

Twitter, Inc., NYSE

TWTR

17.92

-2.08%

39.7K

Tesla Motors, Inc., NASDAQ

TSLA

173

-2.38%

8.1K

Ford Motor Co.

F

12.05

-2.98%

150.4K

ALCOA INC.

AA

8.27

-3.05%

55.3K

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

6.75

-6.77%

194.3K

-

14:50

Option expiries for today's 10:00 ET NY cut

USD/JPY: 110.10 (USD 205m) 112.00 (USD 135m) 114.00 (284m) 115.00 (245m)

EUR/USD: 1.0800-15 (EUR 1.8bln) 1.0900 (383m) 1.1000 (425m) 1.1010-15 (361m) 1.1025-35 (1.1bln) 1.1050 (744m) 1.1075 (198m) 1.1140-50 (877m) 1.1190-112.00 (551m) 1.1250 (2.03bln)

EUR/GBP 0.7750 (EUR 777m)

AUD/USD: 0.6950 (AUD 151m) 0.7050 (290m) 0.7150 (425m) 0.7200 (191m)

USD/CAD 1.3500 (USD 600m) 1.3950 (570m)

USD/CNY 6.5000 (1.97bln) 6.55 (1.47bln)

-

14:48

Upgrades and downgrades before the market open

Upgrades:

Deere (DE) upgraded to Buy at Argus; target $85

Downgrades:

Ford Motor (F) downgraded to Underperform from Neutral at Credit Suisse; target $13

Other:

AT&T (T) initiated with a Buy at Deutsche Bank

Verizon (VZ) initiated with a Hold at Deutsche Bank

JPMorgan Chase (JPM) reiterated with an Outperform at FBR & Co.

-

14:38

CBI retail sales balance slides to +10% in February

The Confederation of British Industry (CBI) released its retail sales balance data on Wednesday. The CBI retail sales balance plunged to +10% in February from +16% in January. It was the lowest level since May 2013.

Sales growth is expected to slow next month, while orders are expected to decline.

"Overall, conditions remain challenging for retailers. Although sales have continued to grow and optimism has risen, expectations for sales growth are lacklustre and retailers are still wary of investing," CBI Director of Economics, Rain Newton-Smith, said.

-

14:25

Foreign exchange market. European session: the British pound traded lower against the U.S. dollar on the possible Britain’s exit from the European Union

Economic calendar (GMT0):

(Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual)

00:30 Australia Wage Price Index, q/q Quarter IV 0.6% 0.6% 0.5%

00:30 Australia Wage Price Index, y/y Quarter IV 2.3% 2.3% 2.2%

00:30 Australia Construction Work Done Quarter IV -1.8% Revised From -3.6% -2% -3.6%

05:00 Japan Leading Economic Index (Finally) December 103.2 102 102.1

05:00 Japan Coincident Index (Finally) December 111.9 110.9

07:00 Switzerland UBS Consumption Indicator January 1.61 Revised From 1.62 1.66

07:45 France Consumer confidence February 97 97 95

09:30 United Kingdom BBA Mortgage Approvals January 43.66 Revised From 43.98 45.2 47.5

12:00 U.S. MBA Mortgage Applications February 8.2% -4.3%

The U.S. dollar traded mixed to higher against the most major currencies ahead of the release of the U.S. economic data. The preliminary U.S. services PMI is expected to rise to 53.5 in February from 53.2 in January.

New home sales in the U.S. are expected to decline to 520,000 units in January from 544,000 units in December.

The euro traded lower against the U.S. dollar in the absence of any major economic data from the Eurozone.

French statistical office INSEE released its consumer confidence index for France on Wednesday. French consumer confidence index fell to 95 in February from 97 in January. Analysts had expected the index to remain unchanged at 97.

The British pound traded lower against the U.S. dollar on the possible Britain's exit from the European Union.

The British Bankers' Association (BBA) released the number of mortgage approvals in the U.K. on Wednesday. The number of mortgage approvals rose to 47,509 in January from 43,660 in December, exceeding expectations for a rise to 45,200. It was the highest level since February 2014.

The Confederation of British Industry (CBI) released its retail sales balance data on Wednesday. The CBI retail sales balance plunged to +10% in February from +16% in January.

The Swiss franc traded mixed against the U.S. dollar. UBS released its consumption index for Switzerland on Wednesday. The UBS consumption index increased to 1.66 in January from 1.61 in December. December's figure was revised down from 1.62. The increase was driven by an improved business sentiment in the retail sector.

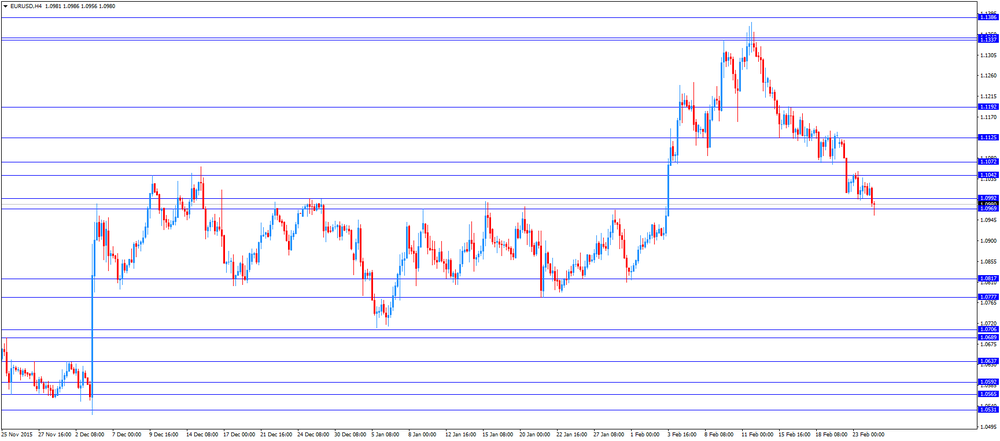

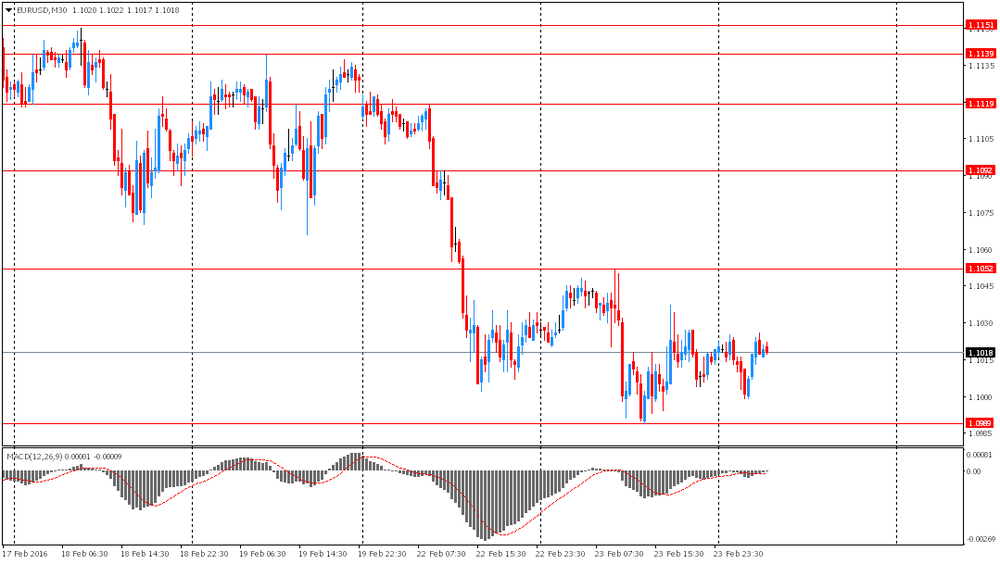

EUR/USD: the currency pair decreased to $1.0956

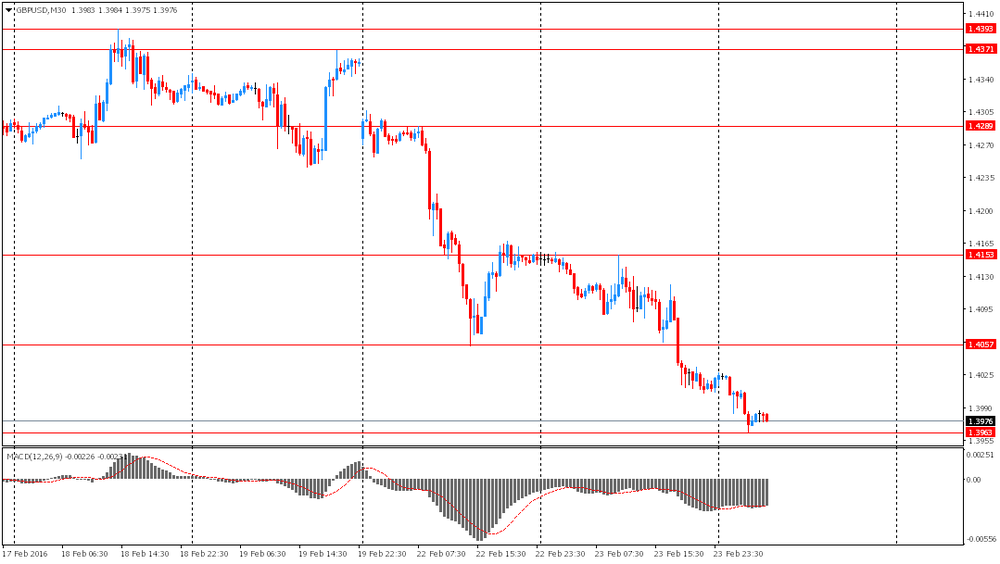

GBP/USD: the currency pair dropped to $1.3877

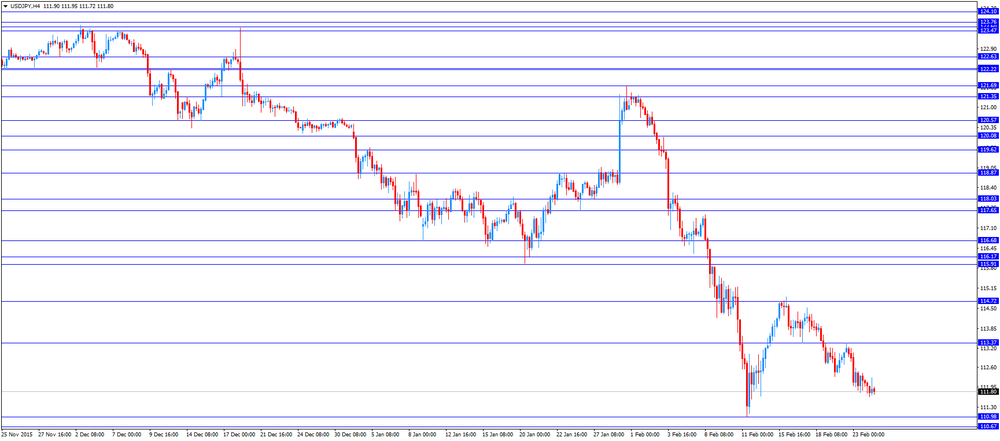

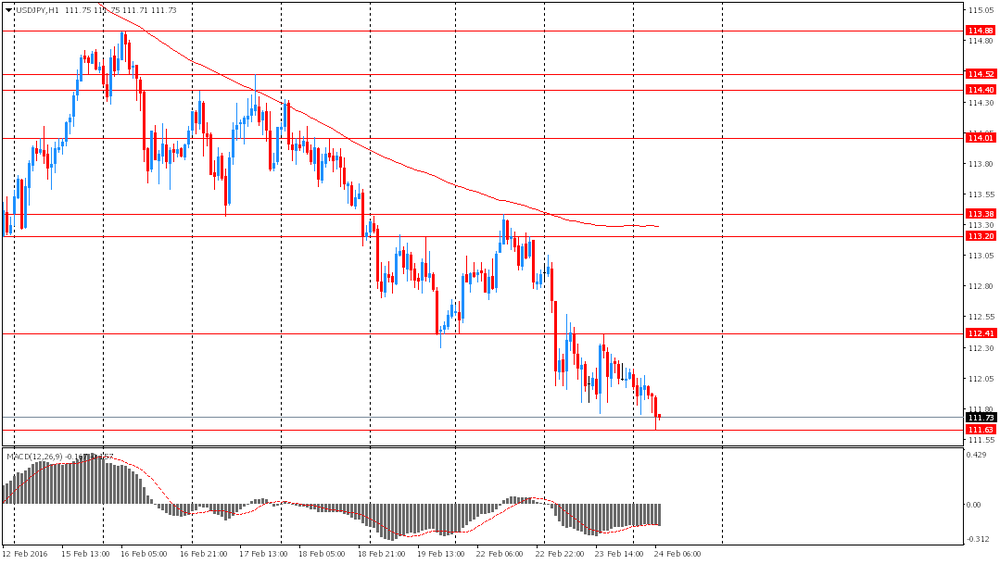

USD/JPY: the currency pair fell to Y111.72

The most important news that are expected (GMT0):

14:45 U.S. Services PMI (Preliminary) February 53.2 53.5

15:00 U.S. New Home Sales January 544 520

15:30 U.S. Crude Oil Inventories February 2.147 3.165

17:50 Canada BOC Deputy Governor Lawrence Schembri Speaks

18:10 United Kingdom BOE Deputy Governor for Financial Stability Jon Cunliffe speaks

-

14:10

European stock markets mid session: stocks traded lower on a further decline in oil prices

Stock indices traded lower as oil prices continued to decline. Oil prices fell on comments by Saudi Arabian Oil Minister Ali Al-Naimi. He said on Tuesday that the country was not ready to cut its oil output.

Meanwhile, market participants eyed the economic data from France. French statistical office INSEE released its consumer confidence index for France on Wednesday. French consumer confidence index fell to 95 in February from 97 in January. Analysts had expected the index to remain unchanged at 97.

The British Bankers' Association (BBA) released the number of mortgage approvals in the U.K. on Wednesday. The number of mortgage approvals rose to 47,509 in January from 43,660 in December, exceeding expectations for a rise to 45,200. It was the highest level since February 2014.

Current figures:

Name Price Change Change %

FTSE 100 5,887.46 -74.85 -1.26 %

DAX 9,229.74 -187.03 -1.99 %

CAC 40 4,170.15 -68.27 -1.61 %

-

13:49

Orders

EUR/USD

Offers: 1.1020 1.1035 1.1050 1.1080 1.1100 1.1120 1.1135 1.1150

Bids: 1.0985 1.0965 1.0950 1.0920 1.0900 1.0880 1.0860 1.0830 1.0800

GBP/USD

Offers: 1.4020-25 1.4050 1.4080 1.4100 1.4120 1.4135 1.4150-55 1.4180 1.4200

Bids: 1.3950-55 1.3925-30 1.3900 1.3885 1.3865 1.3850

EUR/JPY

Offers: 123.30 123.50 123.80 124.00 124.50 124.75 125.00 125.50 126.00

Bids: 122.75-80 122.50 122.30 122.00 121.50 121.00

EUR/GBP

Offers: 0.7830-35 0.7885 0.7900 0.7925 0.7950

Bids: 0.7850 0.7830-35 0.7800 0.7785-90 0.7765 0.7750

USD/JPY

Offers: 112.20-25 112.50 112.80 113.00 113.20-25 113.40 113.65 113.85 114.00

Bids: 111.80 111.65-70 111.50 111.30 111.00 110.80 110.50 110.30 110.00

AUD/USD

Offers: 0.7220 0.7250 0.7265 0.7285 0.7300 0.7320 0.7350

Bids: 0.7180-85 0.7160 0.7140-45 0.7120 0.7100

-

13:01

U.S.: MBA Mortgage Applications, February -4.3%

-

11:47

NBB business climate for Belgium slides to -6.6 in February

The National Bank of Belgium (NBB) released its business survey on Tuesday. The business climate dropped to -6.6 in February from -3.0 in January. Analysts had expected the index to decline to -3.6.

2 of 4 indicators dropped in February, while 2 indicators rose.

The business climate index for the manufacturing sector fell to -11.2 in February from -6.3 in January due to a less favourable assessments of total order books.

The business climate index for the services sector was up to 10.5 in February from 10.2 in January due to a more favourable assessment of the current activity.

The business climate index for the building sector slid to -4.1 in February from 0.5 in January due to a downward revision of all the demand-side components.

The business climate index for the trade sector increased to -5.1 in February from -8.6 in January due to more positive demand expectations.

-

11:39

Industrial orders in Italy decline at a seasonally adjusted rate of 2.8% in December

The Italian statistical office Istat released its industrial orders data for Italy on Wednesday. Industrial orders in Italy declined at a seasonally adjusted rate of 2.8% in December, after a 1.5% rise in November. November's figure was revised down from a 1.6% gain.

Domestic orders slid 4.8% in December, while non-domestic orders were up 0.2%.

On a yearly basis, the unadjusted industrial orders in Italy rose 1.5% in December, after a 12.1% rise in November.

The seasonally adjusted industrial turnover in Italy fell 1.6% in December, after a 1.1% decrease in November.

Domestic turnover decreased 1.7% in December, while non-domestic turnover plunged 1.4%.

On a yearly basis, the adjusted industrial turnover in Italy declined 3.0% in December, after a 0.8% increase in November.

-

11:31

Number of mortgage approvals in the U.K. rises to 47,509 in January

The British Bankers' Association (BBA) released the number of mortgage approvals in the U.K. on Wednesday. The number of mortgage approvals rose to 47,509 in January from 43,660 in December, exceeding expectations for a rise to 45,200. It was the highest level since February 2014.

December's figure was revised up from 43,979.

"The start of the year has seen a significant rise in mortgage borrowing. It seems that this has been driven, in part, by borrowers looking to get ahead of the increases in stamp duty for buy-to-let and second home buyers scheduled to come into effect in April," the chief economist at the BBA, Richard Woolhouse, said.

-

11:18

French consumer confidence index falls to 95 in February

French statistical office INSEE released its consumer confidence index for France on Wednesday. French consumer confidence index fell to 95 in February from 97 in January. Analysts had expected the index to remain unchanged at 97.

The index of the outlook on consumers' saving capacity rose to -5 in February from -6 in January.

The index of households' assessment of their financial situation in the past twelve months declined to -25 in February from -24 in January.

The index of the outlook on consumers' financial situation for next twelve months decreased to -10 in February from -8 in January.

The index of the outlook on unemployment rising in coming months climbed to 46 in February from 33 in January.

The index for future inflation expectations was down to -38 in February from -39 in January.

-

11:09

UBS consumption index rises to 1.66 in January

UBS released its consumption index for Switzerland on Wednesday. The UBS consumption index increased to 1.66 in January from 1.61 in December. December's figure was revised down from 1.62.

The increase was driven by an improved business sentiment in the retail sector.

The bank noted that the outlook for retail remained subdued.

"The improvement of the UBS Consumption Indicator sends a positive signal for private consumption. However, unemployment could rise in the first half of the year as a delayed response to last year's weaker GDP growth, thereby dampening private consumption," the bank said.

The bank noted that private consumption could rise 1.4% in 2016, driven by the labour market recovery in the second half of the year.

-

11:04

Option expiries for today's 10:00 ET NY cut

USD/JPY: 110.10 (USD 205m) 112.00 (USD 135m) 114.00 (284m) 115.00 (245m)

EUR/USD: 1.0800-15 (EUR 1.8bln) 1.0900 (383m) 1.1000 (425m) 1.1010-15 (361m) 1.1025-35 (1.1bln) 1.1050 (744m) 1.1075 (198m) 1.1140-50 (877m) 1.1190-112.00 (551m) 1.1250 (2.03bln)

EUR/GBP 0.7750 (EUR 777m)

AUD/USD: 0.6950 (AUD 151m) 0.7050 (290m) 0.7150 (425m) 0.7200 (191m)

USD/CAD 1.3500 (USD 600m) 1.3950 (570m)

USD/CNY 6.5000 (1.97bln) 6.55 (1.47bln)

-

11:03

Fed Vice Chairman Stanley Fischer: the economic growth in the U.S. picked up in the first quarter

The Fed Vice Chairman Stanley Fischer said on Tuesday that the economic growth in the U.S. picked up in the first quarter.

"The spending indicators that we have in hand for January point to a pickup in economic growth this quarter," he said.

Fischer noted that a tightening of financial conditions could mean a slowdown in the global economy that could have a negative impact on the economic growth and inflation in the U.S.

"If the recent financial market developments lead to a sustained tightening of financial conditions, they could signal a slowing in the global economy that could affect growth and inflation in the United States," the Fed vice chairman said.

He said nothing new about further interest rate hikes.

-

10:44

Germany’s Deutsche Börse is in talks to merge with the London Stock Exchange

Germany's Deutsche Börse is in talks to merge with the London Stock Exchange (LSE). It would be a £21bn deal. In case of a successful merger, Deutsche Börse shareholders will own 54.4% of the combined company, while LSE shareholders will hold 45.6%.

Both companies expect to strengthen their market position, to generate extra revenues and to save costs.

-

10:34

U.S. banks’ aggregate net income increases by 11.9% in the fourth quarter of 2015

The U.S. Federal Deposit Insurance Corporation (FDIC) said on Tuesday that the U.S. banks' aggregate net income increased by 11.9% year-on-year to $40.8 billion in the fourth quarter. The rise was mainly driven by an increase in net operating revenue and a fall in noninterest expenses.

-

10:30

United Kingdom: BBA Mortgage Approvals, January 47.5 (forecast 45.2)

-

10:22

World Bank: the economy in the European Union continued to improve in 2015

World Bank released its European Union Regular Economic Report (EU RER) on Tuesday. The bank said that the economy in the European Union (EU) continued to improve in 2015. The growth is estimated to be 2% in 2015.

Central Europe showed the highest growth, driven by the Czech Republic, Poland, and Romania, while Southern Europe expanded 1.4% in 2015, driven by an improvement in labour markets.

"The story in the region is positive. Unemployment rates are reaching pre-crisis levels in many EU countries and unemployment among the young - who suffered the largest increase in poverty during the crisis - is finally declining," World Bank Lead Economist and co-author of the latest report, Doerte Doemeland, said.

-

10:12

Minneapolis Federal Reserve President Neel Kashkari expects the U.S. economy to expand moderately

Minneapolis Federal Reserve President Neel Kashkari said on Tuesday that he expected the U.S. economy to expand moderately.

"The moderate economic outlook is still the base case for the U.S.," he said.

Kashkari noted that further labour market improvement could lead to a rise in wages.

Kashkari is not a voting member of the Federal Open Market Committee (FOMC) this year.

-

08:45

France: Consumer confidence , February 95 (forecast 97)

-

08:28

Options levels on wednesday, February 24, 2016:

EUR / USD

Resistance levels (open interest**, contracts)

$1.1219 (4273)

$1.1141 (3955)

$1.1082 (5190)

Price at time of writing this review: $1.1009

Support levels (open interest**, contracts):

$1.0932 (7045)

$1.0870 (7017)

$1.0831 (3496)

Comments:

- Overall open interest on the CALL options with the expiration date March, 4 is 66670 contracts, with the maximum number of contracts with strike price $1,1000 (5190);

- Overall open interest on the PUT options with the expiration date March, 4 is 92033 contracts, with the maximum number of contracts with strike price $1,1000 (7045);

- The ratio of PUT/CALL was 1.38 versus 1.41 from the previous trading day according to data from February, 23

GBP/USD

Resistance levels (open interest**, contracts)

$1.4303 (1458)

$1.4205 (375)

$1.4108 (358)

Price at time of writing this review: $1.4011

Support levels (open interest**, contracts):

$1.3893 (1401)

$1.3796 (409)

$1.3698 (174)

Comments:

- Overall open interest on the CALL options with the expiration date March, 4 is 27895 contracts, with the maximum number of contracts with strike price $1,4650 (1652);

- Overall open interest on the PUT options with the expiration date March, 4 is 29241 contracts, with the maximum number of contracts with strike price $1,4350 (2954);

- The ratio of PUT/CALL was 1.05 versus 1.03 from the previous trading day according to data from February, 23

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

08:00

Switzerland: UBS Consumption Indicator, January 1.66

-

07:55

Foreign exchange market. Asian session: the Australian dollar fell

Economic calendar (GMT0):

Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual

00:30 Australia Wage Price Index, q/q Quarter IV 0.6% 0.6% 0.5%

00:30 Australia Wage Price Index, y/y Quarter IV 2.3% 2.3% 2.2%

00:30 Australia Construction Work Done Quarter IV -1.8% Revised From -3.6% -2% -3.6%

05:00 Japan Leading Economic Index (Finally) December 103.2 102 102.1

05:00 Japan Coincident Index (Finally) December 111.9 110.9

The pound extended declines amid fears of the U.K.'s exit from the European Union. Moody's warned that the country's rating could be revised in case it leaves the union. Some economists believe that U.K. exit would result in capital outflows and weaker economic growth. A referendum on EU membership will be held on June 23.

The Australian dollar fell on weak domestic data. The wage price index rose by 0.5% in the fourth quarter, while economists had expected it to grow by 0.6%. The index rose by 2.2% y/y marking the slowest growth pace since the index series was launched in 1998. Meanwhile the index of construction work done fell by 3.6% in Q4. Analysts had expected a more modest decline of 2.0%. The third quarter reading was revised to -1.8% from -3.6%.

The yen rose against the U.S. dollar amid growing demand for safe-haven assets, which was triggered by renewed declines in oil prices. Oil prices dropped after Saudi oil minister Ali Al-Naimi clearly said that his country will not implement production cuts, because there is no trust that other producers will follow its example.

EUR/USD: the pair fluctuated within $1.0000-25 in Asian trade

USD/JPY: the pair fell to Y111.65

GBP/USD: the pair fell to $1.3965

The most important news that are expected (GMT0):

(time / country / index / period / previous value / forecast)

07:00 Switzerland UBS Consumption Indicator January 1.62

07:45 France Consumer confidence February 97 97

09:30 United Kingdom BBA Mortgage Approvals January 43.98 45.2

12:00 U.S. MBA Mortgage Applications February 8.2%

14:45 U.S. Services PMI (Preliminary) February 53.2 53.5

15:00 U.S. New Home Sales January 544 520

15:30 U.S. Crude Oil Inventories February 2.147 3.165

21:45 New Zealand Visitor Arrivals January 10.5%

-

07:41

Oil plunged

West Texas Intermediate futures for April delivery tumbled to $31.14 (-2.29%), while Brent crude fell to $32.83 (-1.32%) as hopes for output cuts faded. Speaking on Tuesday at the IHS CERAWeek conference in the U.S., Saudi oil minister Ali Al-Naimi said his country would not take on production cuts, because other producers would not do the same even if they promise. Al-Naimi also said that in the current conditions producers will have to "lower costs, borrow or liquidate". He added that he doesn't know when prices will finally climb.

Signs of rising crude stockpiles in the U.S. also weighed on oil prices. The American Petroleum Institute said on Tuesday inventories likely rose by 7.1 million barrels in the week to February 19, while experts had expected a more modest increase of 3.4 million barrels. Official data from the Energy Information Administration will be published later today.

-

07:09

Gold climbed on weaker stocks

Gold climbed to $1,228.40 (+0.47%) as tumbling equities increased demand for safe-haven assets. Physical demand in top consumers India and China is not impressive; however investor appetite for bullion is quite high as shown by ETF data. Holdings of SPDR Gold Trust, the largest gold-backed exchange-traded-fund are at the highest level in almost a year.

Gold has been one of the best performers this year with a 16% gain.

Some analysts say the precious metal is likely to test its recent high of $1,240 some time soon.

-

06:52

Global Stocks: U.S. stock indices posted declines

U.S. stock indices fell on Tuesday as oil prices tumbled after Saudi Arabia said it wouldn't implement output cuts, because there is no guarantee other producers would do the same. Shares of energy companies and banks exposed to shocks from the oil market led declines.

The Dow Jones Industrial Average fell 189 points, or 1.1%, to 16,431. The S&P 500 lost 24 points, or 1.2%, to 1,921 (its energy sector plunged 3.2%). The Nasdaq Composite fell 67 points, or 1.5%, to 4,503.

Meanwhile the Conference Board reported that consumer confidence declined in the U.S. in February. The corresponding index fell to 92.2 (1985=100) from 97.8 in January. The current situation assessment declined to 112.1 from 116.6, while the expectations sub-index slid to 78.9 from 85.3.

Other data showed real estate prices continued rising in major cities in December, although the pace of growth was slightly below expectations. The S&P/Case-Shiller Home Price composite index rose by 5.7% y/y. Economists had expected prices to add 5.8%.

This morning in Asia Hong Kong Hang Seng dropped 1.78%, or 345.53 points, to 19,069.25. China Shanghai Composite Index fell 0.60%, or 17.46 points, to 2,885.88. Meanwhile the Nikkei declined 1.09%, or 174.31 points, to 15,877.74.

Asian stock indices fell as fresh declines in oil prices intensified concerns over the global economic growth. Energy and financial shares suffered most. Japanese banks on the broader Topix index lost 1.2%. A stronger yen harmed exporters' competiveness.

-

06:01

Japan: Leading Economic Index , December 102.1 (forecast 102)

-

06:01

Japan: Leading Economic Index , December 102.1 (forecast 102)

-

06:01

Japan: Coincident Index, December 110.9

-

03:33

Nikkei 225 15,955.62 -96.43 -0.60 %, Hang Seng 19,327.47 -87.31 -0.45 %, Shanghai Composite 2,906.27 +2.94 +0.10 %

-

01:30

Australia: Wage Price Index, y/y, Quarter IV 2.2% (forecast 2.3%)

-

01:30

Australia: Construction Work Done, Quarter IV -3.6% (forecast -2%)

-

01:30

Australia: Wage Price Index, q/q, Quarter IV 0.5% (forecast 0.6%)

-

00:32

Commodities. Daily history for Feb 23’2016:

(raw materials / closing price /% change)

Oil 31.37 -1.57%

Gold 1,226.00 +0.28%

-

00:31

Stocks. Daily history for Sep Feb 23’2016:

(index / closing price / change items /% change)

S&P/ASX 200 4,979.59 -21.64 -0.43%

TOPIX 1,291.17 -8.83 -0.68%

SHANGHAI COMP 2,903.95 -23.22 -0.79%

HANG SENG 19,414.78 -49.31 -0.25%

FTSE 100 5,962.31 -75.42 -1.25 %

CAC 40 4,238.42 -60.28 -1.40 %

Xetra DAX 9,416.77 -156.82 -1.64 %

S&P 500 1,921.27 -24.23 -1.25 %

NASDAQ Composite 4,503.58 -67.02 -1.47 %

Dow Jones 16,431.78 -188.88 -1.14 %

-

00:31

Currencies. Daily history for Feb 23’2016:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,1029 +0,09%

GBP/USD $1,4021 -0,91%

USD/CHF Chf0,9911 -0,85%

USD/JPY Y112,09 -0,71%

EUR/JPY Y123,51 -0,82%

GBP/JPY Y157,15 -1,62%

AUD/USD $0,7200 -0,36%

NZD/USD $0,6640 -0,86%

USD/CAD C$1,3792 +0,64%

-