Noticias del mercado

-

21:01

Dow -0.35% 17,658.35 -62.63 Nasdaq -0.50% 5,082.55 -25.39 S%P -0,40% 2070.05 -8.31

-

18:12

Wall Street. Major U.S. stock-indexes fell

Major U.S. stock-indexes lower on Wednesday as crude oil slid back towards the 11-year low it hit last week. Crude oil gave up its gains from Tuesday after forecasts of a short winter in North America and Europe piled pressure on the oversupplied commodity. Trading volumes are expected to remain thin on the last trading days of the year.

Most of all of Dow stocks in negative area (19 of 30). Top looser - Chevron Corporation (CVX, -1,21%). Top gainer - Caterpillar Inc. (CAT, +0.43%).

All S&P sectors also in red area. Top looser - Conglomerates (-1.3%).

At the moment:

Oil 36.71 -1.16 -3.06%

Gold 1060.10 -7.90 -0.74%

Dow 17584.00 -54.00 -0.31%

S&P 500 2064.00 -8.75 -0.42%

Nasdaq 100 4665.50 -25.00 -0.53%

U.S. 10yr 2.31 +0.01

-

18:06

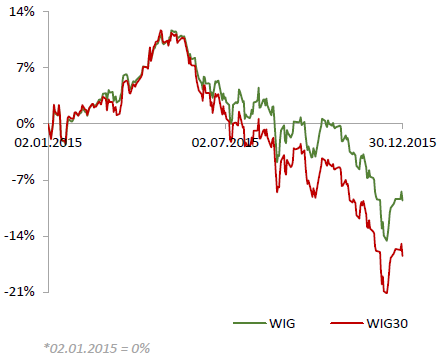

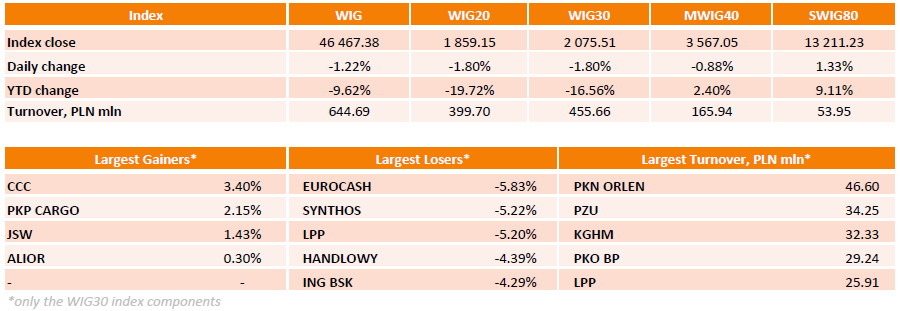

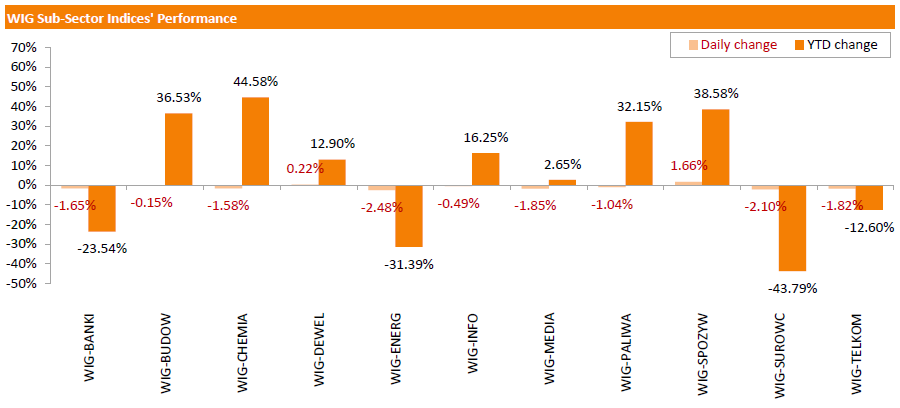

WSE: Session Results

Polish equity market closed lower on Wednesday. The broad market measure, the WIG Index, lost 1.22%. Except for food sector (+1.66%) and developers (+0.22%), every sector in the WIG Index declined, with utilities (-2.48%) lagging behind.

The large-cap stocks' benchmark, the WIG30 Index, fell by 1.8%. There were only four gainers among the index components. Footwear retailer CCC (WSE: CCC) posted the strongest advance, up 3.4%. Other outperformers were railway freight transport operator PKP CARGO (WSE: PKP), coking coal producer JSW (WSE: JSW) and bank ALIOR (WSE: ALR), gaining 2.15%, 1.43% and 0.3% respectively. On the other side of the ledger, FMCG wholesaler EUROCASH (WSE: EUR) topped the list of underperformers, tumbling by 5.83%. It was followed by chemical producer SYNTHOS (WSE: SNS) and clothing retailer LPP (WSE: LPP), slumping by 5.22% and 5.20% respectively.

For the year, the market lost 9.62%, suffering from weak performance of materials (-43.79%), utilities (-31.39%) and banking (-23.54%) sectors.

The market will be closed on Thursday and Friday.

-

18:02

European stocks closed: FTSE 100 6,274.05 -40.52 -0.64% CAC 40 4,677.14 -24.22 -0.52% DAX 10,743.01 -117.13 -1.08%

-

16:30

U.S.: Crude Oil Inventories, December 2.629 (forecast -2.5)

-

16:00

U.S.: Pending Home Sales (MoM) , November -0.9% (forecast 0.5%)

-

15:33

U.S. Stocks open: Dow -0.16%, Nasdaq -0.16%, S&P -0.20%

-

15:23

Before the bell: S&P futures -0.27%, NASDAQ futures -0.18%

U.S. stock-index futures slipped.

Global Stocks:

Nikkei 19,033.71 +51.48 +0.27%

Hang Seng 21,882.15 -117.47 -0.53%

Shanghai Composite 3,572.69 +8.96 +0.25%

FTSE 6,275.88 -38.69 -0.61%

CAC 4,685.27 -16.09 -0.34%

DAX 10,743.01 -117.13 -1.08%

Crude oil $36.83 (-2.75%)

Gold $1060.90 (-0.66%)

-

14:58

Wall Street. Stocks before the bell

(company / ticker / price / change, % / volume)

Hewlett-Packard Co.

HPQ

11.93

0.59%

13.0K

Merck & Co Inc

MRK

53.54

0.37%

0.1K

Intel Corp

INTC

35.45

0.03%

4.7K

Ford Motor Co.

F

14.23

0.00%

0.5K

Pfizer Inc

PFE

32.82

-0.03%

1.2K

International Business Machines Co...

IBM

139.70

-0.06%

0.4K

Wal-Mart Stores Inc

WMT

61.56

-0.08%

2.1K

UnitedHealth Group Inc

UNH

119.66

-0.13%

6.0K

Starbucks Corporation, NASDAQ

SBUX

61.05

-0.13%

2.1K

Visa

V

79.10

-0.14%

0.1K

Walt Disney Co

DIS

106.92

-0.15%

2.0K

ALTRIA GROUP INC.

MO

58.82

-0.17%

0.5K

Microsoft Corp

MSFT

56.45

-0.18%

1.1K

General Electric Co

GE

31.22

-0.19%

23.7K

Cisco Systems Inc

CSCO

27.70

-0.25%

0.6K

McDonald's Corp

MCD

119.73

-0.28%

0.4K

Apple Inc.

AAPL

108.42

-0.29%

39.4K

Boeing Co

BA

146.90

-0.31%

2.6K

Twitter, Inc., NYSE

TWTR

22.40

-0.31%

3.4K

Nike

NKE

64.05

-0.33%

0.6K

Citigroup Inc., NYSE

C

52.80

-0.34%

6.0K

Facebook, Inc.

FB

106.90

-0.34%

9.9K

Tesla Motors, Inc., NASDAQ

TSLA

236.30

-0.38%

4.7K

Yahoo! Inc., NASDAQ

YHOO

33.91

-0.38%

2.3K

Verizon Communications Inc

VZ

47.01

-0.42%

0.5K

FedEx Corporation, NYSE

FDX

148.57

-0.45%

2.2K

Amazon.com Inc., NASDAQ

AMZN

690.50

-0.50%

3.3K

Caterpillar Inc

CAT

68.69

-0.72%

0.8K

Chevron Corp

CVX

90.15

-1.21%

2.5K

Exxon Mobil Corp

XOM

78.20

-1.21%

10.4K

ALCOA INC.

AA

10.00

-1.28%

51.6K

Barrick Gold Corporation, NYSE

ABX

7.46

-1.71%

1.7K

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

6.77

-2.87%

60.3K

-

14:50

Option expiries for today's 10:00 ET NY cut

USD/JPY 120.00 (USD 284m) 121.00 (120m) 122.00 (926m)

EUR/USD 1.0875 (EUR200m) 1.0880 (383m) 1.1000 ( 597m)

GBP/USD 1.4700 (GBP 492m) 1.4725 (169m) 1.4940-50 (GBP 129m)

AUD/USD 0.7225 (AUD 210m) 0.7290 (AUD 375m) 0.7300 (142m) 0.7315 (131m) 0.7350 (306m)

NZD/USD 0.6750 (148m)

USD/CNY 6.5000 (USD 400m)

USD/SGD 1.4050 (USD 600m) 1.4100 (397m)

-

14:44

Upgrades and downgrades before the market open

Upgrades:

Downgrades:

Other:

Intel (INTC) target raised to $38 from $37 at Needham

FedEx (FDX) target set at $182 at Goldman Sachs

-

11:19

Option expiries for today's 10:00 ET NY cut

USD/JPY 120.00 (USD 284m) 121.00 (120m) 122.00 (926m)

EUR/USD 1.0875 (EUR200m) 1.0880 (383m) 1.1000 ( 597m)

GBP/USD 1.4700 (GBP 492m) 1.4725 (169m) 1.4940-50 (GBP 129m)

AUD/USD 0.7225 (AUD 210m) 0.7290 (AUD 375m) 0.7300 (142m) 0.7315 (131m) 0.7350 (306m)

NZD/USD 0.6750 (148m)

USD/CNY 6.5000 (USD 400m)

USD/SGD 1.4050 (USD 600m) 1.4100 (397m)

-

10:16

Eurozone: Private Loans, Y/Y, November 1.4% (forecast 1.3%)

-

10:00

Eurozone: M3 money supply, adjusted y/y, November 5.1% (forecast 5.4%)

-

08:24

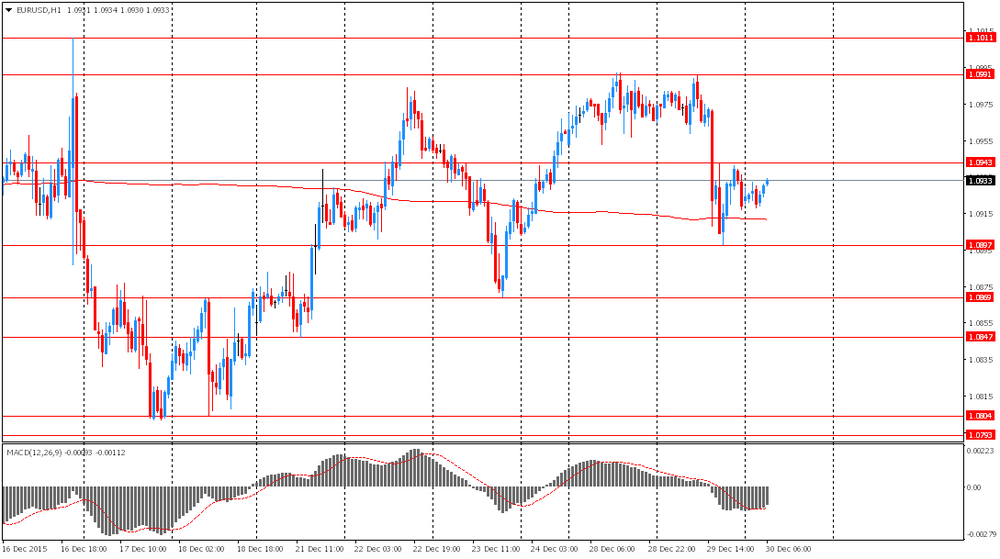

Options levels on wednesday, December 30, 2015:

EUR / USD

Resistance levels (open interest**, contracts)

$1.1050 (4750)

$1.1003 (5522)

$1.0978 (2627)

Price at time of writing this review: $1.0931

Support levels (open interest**, contracts):

$1.0888 (1906)

$1.0858 (3670)

$1.0823 (2766)

Comments:

- Overall open interest on the CALL options with the expiration date January, 8 is 55813 contracts, with the maximum number of contracts with strike price $1,1100 (7418);

- Overall open interest on the PUT options with the expiration date January, 8 is 73007 contracts, with the maximum number of contracts with strike price $1,0450 (8000);

- The ratio of PUT/CALL was 1.31 versus 1.30 from the previous trading day according to data from December, 29

GBP/USD

Resistance levels (open interest**, contracts)

$1.5101 (2726)

$1.5002 (506)

$1.4905 (222)

Price at time of writing this review: $1.4823

Support levels (open interest**, contracts):

$1.4794 (1776)

$1.4697 (1130)

$1.4599 (804)

Comments:

- Overall open interest on the CALL options with the expiration date January, 8 is 19712 contracts, with the maximum number of contracts with strike price $1,5100 (2726);

- Overall open interest on the PUT options with the expiration date January, 8 is 19449 contracts, with the maximum number of contracts with strike price $1,5100 (3084);

- The ratio of PUT/CALL was 0.99 versus 0.99 from the previous trading day according to data from December, 29

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

08:01

United Kingdom: Nationwide house price index, y/y, December 4.5% (forecast 3.8%)

-

08:01

United Kingdom: Nationwide house price index , December 0.8% (forecast 0.5%)

-

08:00

Switzerland: UBS Consumption Indicator, November 1.66

-

07:53

Foreign exchange market. Asian session: the Australian dollar edged down

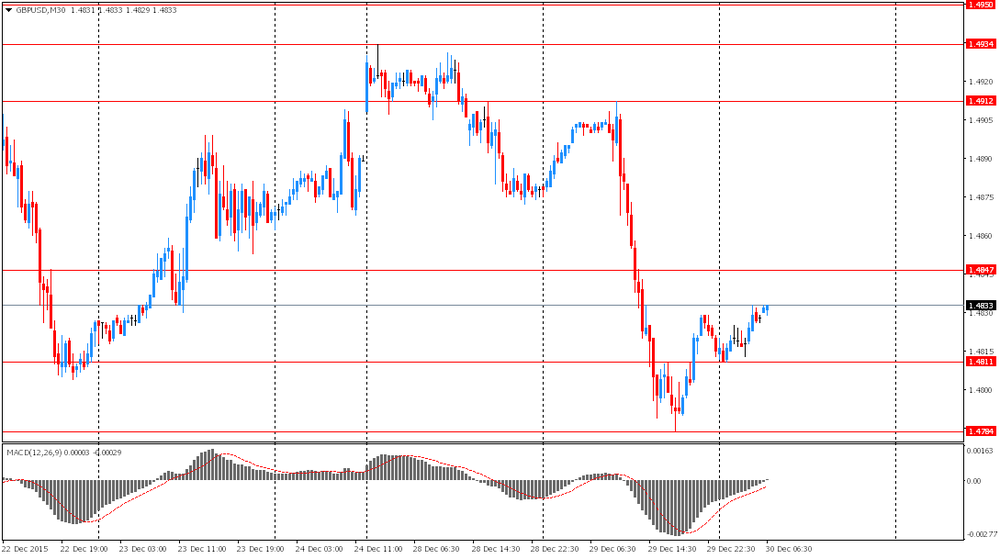

The pound climbed after yesterday's decline to an eight-month low against the U.S. dollar. Investors shifted expectations of a BOE rate hike to the second half of 2016. Market participants are also cautious ahead of a probable referendum on UK's EU membership. An exit from the European Union could harm investment, which supports the pound.

The Australian dollar edged down amid ongoing declines in oil prices. An industry group the American Petroleum Institute said yesterday that U.S. oil inventories likely rose by 2.9 million barrels last week.

EUR/USD: the pair fluctuated within $1.0915-35 in Asian trade

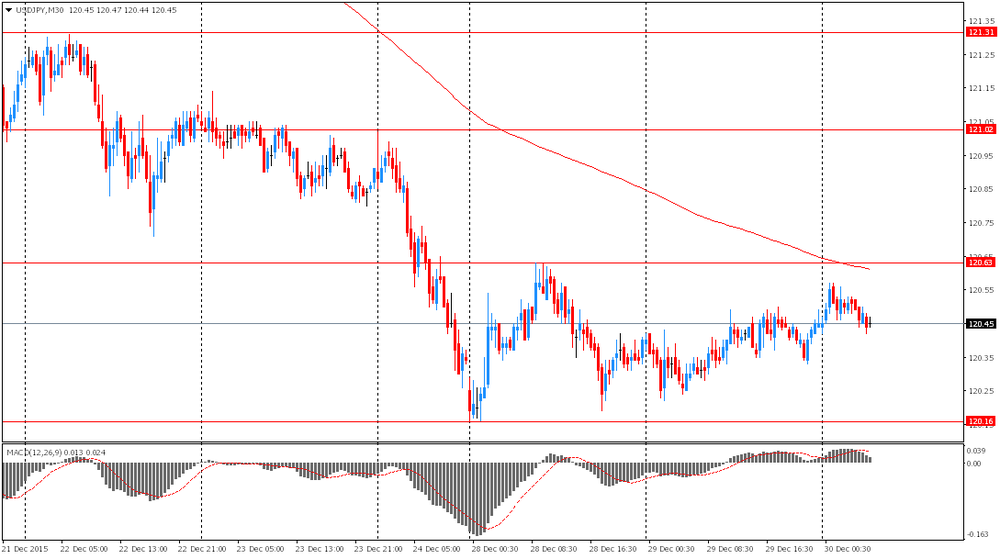

USD/JPY: the pair fell to Y120.35

GBP/USD: the pair rose to $1.4840

The most important news that are expected (GMT0):

(time / country / index / period / previous value / forecast)

07:00 United Kingdom Nationwide house price index, y/y December 3.7% 3.8%

07:00 United Kingdom Nationwide house price index December 0.1% 0.5%

07:00 Switzerland UBS Consumption Indicator November 1.6

09:00 Eurozone Private Loans, Y/Y November 1.2% 1.3%

09:00 Eurozone M3 money supply, adjusted y/y November 5.3% 5.4%

12:00 U.S. MBA Mortgage Applications December 7.3%

15:00 U.S. Pending Home Sales (MoM) November 0.2% 0.5%

15:30 U.S. Crude Oil Inventories

-

07:38

Oil prices declined

West Texas Intermediate futures for February delivery fell to $37.22 (-1.72%), while Brent crude declined to $37.47 (-0.85%) amid supply glut concerns after posting substantial gains in the previous session.

The Energy Information Administration will release its U.S. crude oil inventories data later today. Analysts expect to see a decline. Nevertheless Bloomberg News said that supplies would still be over 120 million barrels above the five-year average for this season.

-

07:27

Gold little changed

Gold is currently at $1,069.60 (+0.15%) amid low trading volumes. This week trading is likely to remain thin. Gold is expected to be range-bound for the rest of the year tracking oil prices and the dollar.

Some analysts expect gold to trade lower and decline to $1,000 an ounce at the beginning of 2016 amid prospects of further rate hikes by the Federal Reserve.

-

07:05

Global Stocks: U.S. stock indices climbed

U.S. stock indices advanced on Tuesday amid gains in oil prices.

The Dow Jones Industrial Average rose 192.71 points, or 1.1%, to 17,720.98. The S&P 500 rose 21.86 points, or 1.1%, to 2,078.36 (all of its 10 sectors climbed). The Nasdaq Composite gained 66.95 points, or 1.3%, to 5,107.94.

A report from S&P/Case-Shiller showed that U.S. home prices rose at a faster pace in October; however recent data suggest that home sales lost momentum. The home price index rose by 5.2% in the twelve months through October compared to a 4.9% increase in September.

Meanwhile the Conference Board reported that the consumer confidence index improved to 96.5 (1985=100) in December from 92.6 in November. The current assessment index rose to 115.3 from 110.9; the expectations index advanced to 83.9 from 80.4.

This morning in Asia Hong Kong Hang Seng declined 0.54%, or 118.77, to 21,880.85. China Shanghai Composite Index fell 0.70%, or 24.93, to 3,538.81. The Nikkei gained 0.31%, or 58.39, to 19,040.62.

Asian stock indices traded mixed. Japanese stocks rose on higher crude oil prices and a weaker yen, which is favorable for exporters. Nevertheless trading was sluggish ahead of a holiday.

-

03:03

Nikkei 225 19,088.8 +106.57 +0.56 %, Hang Seng 22,024.89 +25.27 +0.11 %, Shanghai Composite 3,568.6 +4.86 +0.14 %

-

01:04

Commodities. Daily history for Dec 29’2015:

(raw materials / closing price /% change)

Oil 37.33 -1.43%

Gold 1,068.50 +0.05%

-

01:03

Stocks. Daily history for Sep Dec 29’2015:

(index / closing price / change items /% change)

Nikkei 225 18,982.23 +108.88 +0.58 %

Hang Seng 21,999.62 +80.00 +0.36 %

Shanghai Composite 3,563.91 +30.13 +0.85 %

FTSE 100 6,314.57 +59.93 +0.96 %

CAC 40 4,701.36 +83.41 +1.81 %

Xetra DAX 10,860.14 +206.23 +1.94 %

S&P 500 2,078.36 +21.86 +1.06 %

NASDAQ Composite 5,107.94 +66.95 +1.33 %

Dow Jones 17,720.98 +192.71 +1.10 %

-

01:03

Currencies. Daily history for Dec 29’2015:

(pare/closed(GMT +2)/change, %)

EUR/USD $1,0919 -0,43%

GBP/USD $1,4815 -0,43%

USD/CHF Chf0,9929 +0,44%

USD/JPY Y120,45 +0,05%

EUR/JPY Y131,55 -0,37%

GBP/JPY Y178,48 -0,36%

AUD/USD $0,7294 +0,63%

NZD/USD $0,6867 +0,32%

USD/CAD C$1,3841 -0,46%

-

00:00

Schedule for today, Wednesday, 30’2015:

(time / country / index / period / previous value / forecast)

07:00 United Kingdom Nationwide house price index, y/y December 3.7% 3.8%

07:00 United Kingdom Nationwide house price index December 0.1% 0.5%

07:00 Switzerland UBS Consumption Indicator November 1.6

09:00 Eurozone Private Loans, Y/Y November 1.2% 1.3%

09:00 Eurozone M3 money supply, adjusted y/y November 5.3% 5.4%

12:00 U.S. MBA Mortgage Applications December 7.3%

15:00 U.S. Pending Home Sales (MoM) November 0.2% 0.5%

15:30 U.S. Crude Oil Inventories December -5.877 -2.5

-