Noticias del mercado

-

21:01

Dow +0.15% 16,989.89 +25.79 Nasdaq +0.51% 4,672.34 +23.51 S&P +0.44% 1,987.87 +8.61

-

18:04

WSE: Session Results

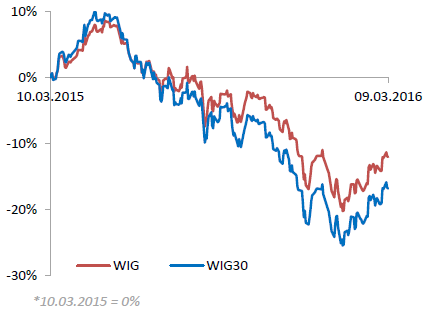

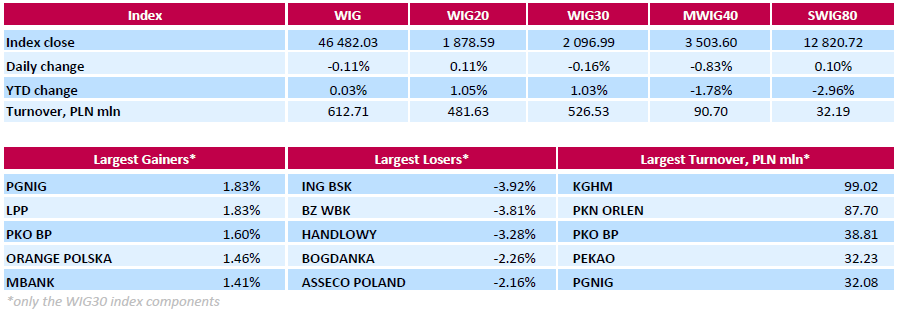

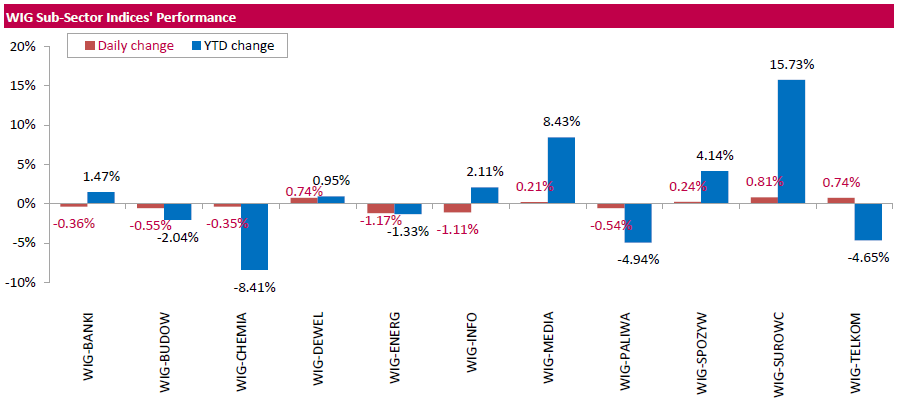

Polish equity market closed lower on Wednesday. The broad market benchmark, the WIG Index, lost 0.11% on low trading turnover. Sector performance within the WIG Index was mixed. Materials sector (+0.81%) recorded the biggest increase, while utilities (-1.17%) lagged behind.

The large-cap stocks slid down 0.16%, as measured by the WIG30 Index. Within the index components, banks ING BSK (WSE: ING), BZ WBK (WSE: BZW) and HANDLOWY (WSE: BHW) were the weakest performers, slumping by 3.28%-3.92%, after Poland's financial regulator KNF announced that the cost of a foreign exchange loans conversion bill proposed by President Andrzej Duda is to be known this month. Other major laggards were thermal coal miner BOGDANKA (WSE: LWB), IT-company ASSECO POLAND (WSE: ACP) and genco ENERGA (WSE: ENG), dropping 2.26%, 2.16% and 2.05% respectively. On the other side of the ledger, clothing retailer LPP (WSE: LPP) and gas company PGNIG (WSE: PGN) were the growth leaders, with each adding 1.83%.

-

18:01

European stocks close: stocks closed higher, driven by expectations for further stimulus measures by the ECB

Stock indices closed higher, driven by expectations for further stimulus measures by the European Central Bank (ECB) also supported stocks. Market participants expect the central bank to cut its deposit further or/ and to expand its monthly asset purchases. The ECB's is -0.3%, and monthly asset purchases total €60 billion.

No major economic reports were released today.

Higher oil prices also supported stocks.

The Office for National Statistics (ONS) released its manufacturing and industrial production figures for the U.K. on Wednesday. Industrial production in the U.K. rose 0.3% in January, missing forecasts of a 0.5% increase, after a 1.1% decline in December.

The increase was mainly driven by a gain in water supply, sewerage & waste management, which soared 9.3% in January.

On a yearly basis, industrial production in the U.K. increased 0.2% in January, in line with expectations, after a 0.2% decrease in December. December's figure was revised up from a 0.4% fall.

Manufacturing production in the U.K. climbed 0.7% in January, exceeding expectations for a 0.2% gain, after a 0.3% decrease in December. December's figure was revised down from a 0.2% drop.

Manufacturing output was mainly driven by a rise in other manufacturing and repair, which climbed by 4.8% in January.

On a yearly basis, manufacturing production in the U.K. decreased 0.1% in January, beating forecast of a 0.7% fall, after a 1.7% drop in December.

Indexes on the close:

Name Price Change Change %

FTSE 100 6,146.32 +20.88 +0.34 %

DAX 9,723.09 +30.27 +0.31 %

CAC 40 4,425.65 +21.63 +0.49 %

-

18:00

European stocks closed: FTSE 100 6,146.32 +20.88 +0.34% CAC 40 4,425.65 +21.63 +0.49% DAX 9,723.09 +30.27 +0.31%

-

18:00

Wall Street. Major U.S. stock-indexes rose

Major U.S. stock-indexes slightly rose on Wednesday as a rise in energy shares from recovering oil prices were capped by a fall in biotech stocks. Biotechs came under pressure after the U.S. government proposed a test program aimed at lowering Medicare drug costs. Brent crude extended gains above $40 a barrel, after U.S. crude stockpiles rose in line with estimates last week and gasoline inventories fell more than expected.

Most of Dow stocks in positive area (19 of 30). Top looser - NIKE, Inc. (NKE, -2,01%). Top gainer - Chevron Corporation (CVX, +5,63%).

Almost all of S&P sectors in positive area. Top looser - Healthcare (-0,2%). Top gainer - Basic Materials (+1,8%).

At the moment:

Dow 17014.00 +42.00 +0.25%

S&P 500 1987.75 +6.75 +0.34%

Nasdaq 100 4281.50 +11.00 +0.26%

Oil 37.92 +1.42 +3.89%

Gold 1254.90 -8.00 -0.63%

U.S. 10yr 1.87 +0.04

-

17:32

The Japanese government could delay a second planned sales tax hike

The Japanese government could delay a second planned sales tax hike in April. Prime Minister Shinzo Abe's economic adviser Etsuro Honda said to Reuters on Wednesday that a delay was favourable due to the weakness in the Japanese economy.

-

16:40

NIESR’s gross domestic product rises by 0.3% in three months to February

The National Institute of Economic and Social Research (NIESR) released its estimate of gross domestic product (GDP) for the U.K. on Wednesday. The GDP estimate rose by 0.3% in three months to February, after a 0.4% growth in three months to January.

A softer growth was partly driven by a slight decline in the production and private services sector.

According to the NIESR, the U.K. economy is expected to expand 2.3% in 2016 and 2.7% in 2017.

"It looks as if output growth at the start of 2016 has been subdued. However, it appears that December 2015 may have been a low point for GDP and as this drops out of the calculation of quarterly growth rates, output growth for the first quarter may strengthen slightly," Jack Meaning, NIESR Research Fellow, said.

-

16:32

Wholesale inventories in the U.S. rise 0.3% in January

The U.S. Commerce Department released wholesale inventories on Wednesday. Wholesale inventories in the U.S. rose 0.3% in January, beating expectations for a 0.2 decline, after a flat reading in December. December's figure was revised up from a 0.1% decline.

The rise was driven by an increase in inventories of non-durable goods. Inventories of non-durable goods increased 1.1% in January, while inventories of durable goods fell 0.3%.

Wholesale sales slid 1.3% in January, after a 0.6% fall in December.

-

16:13

Bank of Canada keeps its interest rate unchanged at 0.50% in March

The Bank of Canada (BoC) released its interest rate decision on Wednesday. The central bank kept its interest rate unchanged at 0.50%, noting that the current monetary policy was appropriate. This decision was expected by analysts.

The BoC said that financial market volatility seemed to dissipate, while the downside risks remained.

The BoC noted that the Canadian economic growth was better than expected in the fourth quarter. Employment improved, the central bank added.

According to the central bank, inflation was evolving broadly as anticipated.

Risks around the inflation are roughly balanced, the central bank said.

The BoC added that "vulnerabilities in the household sector continue to edge higher".

-

15:56

After start on Wall Street

Today's unusually stable behavior of the WIG20 rests on essentially symbolic PLN 300 mln turnover at this time, and lack of major news which could introduce variability in investors' expectations and result in reassessment of quotations. It looks as if bigger players temporarily withdrew from the trading.

Contracts for US indices and oil indicated that the opening of Wall Street will look for a moderate rise. There was no surprises, and it appears that there will be no new impetus from that side.

To the end of the session in Warsaw, oil quotations and Wall Street will shape sentiment.

-

15:34

U.S. Stocks open: Dow +0.41%, Nasdaq +0.40%, S&P +0.49%

-

15:27

Before the bell: S&P futures +0.34%, NASDAQ futures +0.30%

U.S. stock-index futures rose.

Global Stocks:

Nikkei 16,642.2 -140.95 -0.84%

Hang Seng 19,996.26 -15.32 -0.08%

Shanghai 2,862.13 -39.26 -1.35%

FTSE 6,159.67 +34.23 +0.56%

CAC 4,453.08 +49.06 +1.11%

DAX 9,809.61 +116.79 +1.20%

Crude oil $37.02 (+1.42%)

Gold $1254.30 (-0.68%)

-

15:01

Italian economy is expected to expand 0.1% in the first quarter

The Italian statistical office Istat released its gross domestic product (GDP) forecast data for Italy on Wednesday. The Istat expects the Italian economy to expand moderately in the first quarter. The Italian GDP is expected to rise 0.1% in the first quarter, after a 0.1% growth in the fourth quarter of 2015.

The Istat said that domestic demand was expected to be the main driver of the economic growth, exports were expected to fall, while investment will remain stable.

In 2016 as a whole, the Italian economy is expected to grow 0.4%, after a 0.8% rise in 2015.

-

14:59

Wall Street. Stocks before the bell

(company / ticker / price / change, % / volume)

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

8.89

2.66%

77.2K

ALCOA INC.

AA

9.48

1.61%

41.8K

Twitter, Inc., NYSE

TWTR

18.62

1.58%

68.5K

Yandex N.V., NASDAQ

YNDX

13.90

1.31%

6.5K

Tesla Motors, Inc., NASDAQ

TSLA

204.99

1.18%

12.7K

Pfizer Inc

PFE

29.70

1.16%

36.2K

Chevron Corp

CVX

89.60

0.97%

3.7K

Exxon Mobil Corp

XOM

83.41

0.94%

4.4K

Ford Motor Co.

F

13.35

0.91%

16.0K

Cisco Systems Inc

CSCO

27.29

0.89%

1.0K

Goldman Sachs

GS

152.90

0.86%

0.7K

General Motors Company, NYSE

GM

30.56

0.86%

1.6K

Amazon.com Inc., NASDAQ

AMZN

565.00

0.85%

7.3K

Citigroup Inc., NYSE

C

41.35

0.73%

41.8K

Home Depot Inc

HD

127.60

0.69%

0.1K

Starbucks Corporation, NASDAQ

SBUX

58.00

0.69%

0.7K

Wal-Mart Stores Inc

WMT

68.00

0.68%

0.1K

Apple Inc.

AAPL

101.67

0.63%

63.7K

American Express Co

AXP

59.80

0.62%

2.0K

Facebook, Inc.

FB

106.55

0.59%

66.1K

Google Inc.

GOOG

697.88

0.56%

0.8K

Visa

V

71.01

0.55%

0.4K

Yahoo! Inc., NASDAQ

YHOO

33.11

0.55%

1.0K

Walt Disney Co

DIS

98.35

0.54%

1.7K

Microsoft Corp

MSFT

51.92

0.52%

3.2K

JPMorgan Chase and Co

JPM

59.04

0.44%

8.8K

General Electric Co

GE

30.18

0.40%

11.3K

Verizon Communications Inc

VZ

52.67

0.40%

0.4K

Caterpillar Inc

CAT

72.00

0.38%

2.6K

E. I. du Pont de Nemours and Co

DD

63.76

0.36%

0.5K

AT&T Inc

T

38.21

0.32%

2.4K

ALTRIA GROUP INC.

MO

62.49

0.30%

0.6K

Johnson & Johnson

JNJ

106.50

0.26%

0.8K

Boeing Co

BA

122.50

0.12%

3.1K

AMERICAN INTERNATIONAL GROUP

AIG

51.98

0.10%

0.1K

Hewlett-Packard Co.

HPQ

11.06

0.09%

0.2K

Nike

NKE

59.81

0.00%

9.6K

FedEx Corporation, NYSE

FDX

141.93

-0.42%

0.6K

Barrick Gold Corporation, NYSE

ABX

13.15

-1.35%

22.4K

-

12:34

WSE: Mid-Session Comment

The first hours of the session reinforced the key factors that were visible at the opening - domination of KGHM and low turnover in the remaining companies. As a result, the WIG20 index has not produced any considerable changes to yesterday's close and today's opening. Low turnover indicates the market is shallow. Calm stock market is paralleled by consolidating EUR/USD pair in the currency market. On such a low turnover of the stock market, the 0.4 percent decline of the WIG20 up to now can be treated with reservation. Markets seems to be waiting for the results of the tomorrow's ECB meeting. Blank macro calendar also favors cautious strategies and prompts to look for continuation of a peaceful session in Warsaw.

On 12:30 (Warsaw time) index WIG20 stood at 1,868 points (-0.40% ) and the March series of future contracts for WIG20 (FW20H16) were at level of 1874 points (+0,16%).

-

12:00

European stock markets mid session: stocks traded higher

Stock indices traded higher, driven by a rise in banking and telecom shares. Expectations for further stimulus measures by the European Central Bank (ECB) also supported stocks. Market participants expect the central bank to cut its deposit further or/ and to expand its monthly asset purchases. The ECB's is -0.3%, and monthly asset purchases total €60 billion.

No major economic reports were released today.

The Office for National Statistics (ONS) released its manufacturing and industrial production figures for the U.K. on Wednesday. Industrial production in the U.K. rose 0.3% in January, missing forecasts of a 0.5% increase, after a 1.1% decline in December.

The increase was mainly driven by a gain in water supply, sewerage & waste management, which soared 9.3% in January.

On a yearly basis, industrial production in the U.K. increased 0.2% in January, in line with expectations, after a 0.2% decrease in December. December's figure was revised up from a 0.4% fall.

Manufacturing production in the U.K. climbed 0.7% in January, exceeding expectations for a 0.2% gain, after a 0.3% decrease in December. December's figure was revised down from a 0.2% drop.

Manufacturing output was mainly driven by a rise in other manufacturing and repair, which climbed by 4.8% in January.

On a yearly basis, manufacturing production in the U.K. decreased 0.1% in January, beating forecast of a 0.7% fall, after a 1.7% drop in December.

Current figures:

Name Price Change Change %

FTSE 100 6,131.6 +6.16 +0.10 %

DAX 9,737.97 +45.15 +0.47 %

CAC 40 4,426.72 +22.70 +0.52 %

-

11:39

Home loans in Australia drop 3.9% in January

The Australian Bureau of Statistics released its home loans data on Wednesday. Home loans in Australia dropped 3.9% in January, missing expectations for a 2.3% decline, after 2.7% increase in December. December's figure was revised up from a 2.6% rise.

The value of owner occupied loans plunged at a seasonally adjusted 4.3% in January, investment lending decreased 1.6%, while the number of loans for the construction of dwellings slid 2.8%.

-

11:33

House prices in Spain decline 0.1% in the fourth quarter

The Spanish statistical office INE released its house prices data on Wednesday. House prices in Spain declined 0.1% in the fourth quarter, after a 0.7% increase in the third quarter.

Prices for new houses climbed 1.3% in the fourth quarter, while prices for second-hand houses fell 0.3%.

On a yearly basis, house prices rose 4.2% in the fourth quarter, after a 4.5% gain in the third quarter.

Prices for new houses soared 5.8% year-on-year in the fourth quarter, while prices for second-hand houses increased 4.0%.

-

11:19

Bank of France cuts its growth forecast for the first quarter

The Bank of France cuts its growth forecast for the first quarter on Wednesday. The central bank expects the French economy to expand 0.3% in the first quarter, down from the previous estimate of a 0.4% growth.

The manufacturing business confidence index fell to 98 in February from 101 in January.

The services business sentiment index remained unchanged at 96 in February.

The construction business sentiment index remained unchanged at 96 in February.

-

11:09

U.K. industrial production rises 0.3% in January

The Office for National Statistics (ONS) released its manufacturing and industrial production figures for the U.K. on Wednesday. Industrial production in the U.K. rose 0.3% in January, missing forecasts of a 0.5% increase, after a 1.1% decline in December.

The increase was mainly driven by a gain in water supply, sewerage & waste management, which soared 9.3% in January.

On a yearly basis, industrial production in the U.K. increased 0.2% in January, in line with expectations, after a 0.2% decrease in December. December's figure was revised up from a 0.4% fall.

Manufacturing production in the U.K. climbed 0.7% in January, exceeding expectations for a 0.2% gain, after a 0.3% decrease in December. December's figure was revised down from a 0.2% drop.

Manufacturing output was mainly driven by a rise in other manufacturing and repair, which climbed by 4.8% in January.

On a yearly basis, manufacturing production in the U.K. decreased 0.1% in January, beating forecast of a 0.7% fall, after a 1.7% drop in December.

-

11:09

TAURON PE Approves Efficiency Improvement Program

Tauron PE (WSE: TPE) approved an efficiency improvement program of a total of PLN 1.3 bln in years 2016-2018 which is expected to boost EBITDA by around PLN 1 bln in 2016-2018, including PLN 400 mln in 2018.

Tauron Polska Energia SA is the parent company of Tauron Group - one of the largest economic entities in Poland, a vertically integrated producer of electricity with capital of about PLN 18 billion and employing more than 26,000 workers. The main activity of the Tauron Group is a coal mining, power generation, distribution and sale of electricity and heat to end-users.

-

10:40

Bank of England's Monetary Policy Committee member Martin Weale: the central bank will likely hike its interest rate than lower it over the next two years

The Bank of England's (BoE) Monetary Policy Committee (MPC) member Martin Weale said in a speech on Tuesday that the central bank will likely hike its interest rate than lower it over the next two years.

"It is appreciably more likely that monetary tightening rather than monetary easing will be needed in the United Kingdom over the next two years," he said.

Weale pointed out that the BoE could buy more assets if there is need for more monetary policy easing.

"Should the need for further easing arise because of a sharp weakening in the outlook for inflation, the scope for further asset purchases is substantial, while the obstacles we saw to reducing Bank Rate below 0.5 per cent are no longer material," MPC member said.

He also said that negative interest rates could lead to a currency war (competitive exchange rate devaluations).

-

10:22

Deputy managing director of the International Monetary Fund David Lipton: the downside risks to the global economic growth increased since January

The first deputy managing director of the International Monetary Fund (IMF), David Lipton, said on Tuesday that the downside risks to the global economic growth increased since January. But he added that the global economic recovery continued.

Lipton pointed out that a combination of monetary and fiscal policy and structural reforms, and collective action was needed to boost the global economy.

-

10:12

Westpac’ consumer confidence index for Australia falls 2.2% in March

Westpac Bank released its consumer confidence index for Australia on late Tuesday evening. The index fell 2.2% in March, after a 4.2% rise in February.

The index was driven by declines in three of the five sub-indexes.

"The Reserve Bank Board next meets on April 5. As we have been successfully arguing since June last year that we expect the Bank will keep rates on hold through 2016," Westpac Chief Economist Bill Evans said.

"Recent dollar strength has been associated with a more positive outlook for China and commodity prices and as such would not be grounds for a policy adjustment. Equally, while most indicators, including our own, one of which is quoted in this survey, point to an overall improvement in the labour market over the last six months, actual jobs growth appears to be running ahead of those indicators," he added.

-

09:11

WSE: Market Opening

Futures contracts on the WIG20 (FW20H16) started the day with a modest rise, increasing by 0.11 % and opening up to the level of 1873 points. (+ 2 points).

The beginning of trading on the Warsaw Stock Exchange is around yesterday's close. The initial phase of the session in only unusual in the low turnover. However, flat opening is exactly what was expected. Most activity is focused on KGHM, a copper exporter, that is adjusting, reflecting recent fluctuations in the commodities markets.

Indices at Opening (Change

WIG 46487.23 -0.10%

WIG20 1875.09 -0.07%

WIG30 2098.72 -0.07%

mWIG40 3524.18 -0.25%

-

08:31

WSE: Pre-Opening

Tuesday's session on Wall Street ended with major indices declining in a uniform fashion. US markets were permeated by the climate of risk aversion that dominated yesterday's sessions in Europe. An important, if not the key element, was contraction of commodity markets, beginning with oil that has been fueling growth of stock markets in the past three weeks.

The current atmosphere of 9:00 maintained, opening in European markets is expected to be flat.

In such environment, WSE is expected to closely follow the performance of core markets. We expect today's WSE session to be devoid any major moves. Investors will be eyeing tomorrow's decisions of the European Central Bank.

-

07:43

Global Stocks: Investors were being cautious ahead of the European Central Bank monetary policy meeting

European stocks were steeped in red Tuesday after a surprise fall in Chinese exports and a drop in oil prices helped drive commodity shares lower.

U.S. stocks snapped their five-day winning streak to close lower on Tuesday as supply woes weighed on oil prices and worries about a prolonged slowdown in China resurfaced.

Stocks in Asia were mostly down Wednesday as investors shied away from risk amid a slump in commodities and oil prices. Investors were being cautious ahead of the European Central Bank monetary policy meeting Thursday. Analysts largely expect the central bank to ease policy, though some investors are concerned that a stimulus expansion could fall short of expectations.

Based on MarketWatch materials

-

03:04

Nikkei 225 16,518.01 -265.14 -1.58 %, Hang Seng 19,846.8 -164.78 -0.82 %, Shanghai Composite 2,824.545 -2.65 %

-

01:02

Stocks. Daily history for Sep Mar 8’2016:

(index / closing price / change items /% change)

Hang Seng 20,011.58 -148.14 -0.73 %

Shanghai Composite 2,899.9 +2.57 +0.09 %

Topix 1,347.72 -14.18 -1.04 %

FTSE 100 6,125.44 -56.96 -0.92 %

CAC 40 4,404.02 -38.27 -0.86 %

Xetra DAX 9,692.82 -86.11 -0.88 %

S&P 500 1,979.26 -22.50 -1.12 %

NASDAQ Composite 4,648.83 -59.43 -1.26 %

Dow Jones Industrial Average 16,964.1 -109.85 -0.64 %

-