Noticias del mercado

-

22:14

U.S. stocks rallied

U.S. stocks rallied, with the Standard & Poor's 500 Index closing at its highest level in more than two weeks, as retail sales data showed a resilient consumer before the Federal Reserve decides on Thursday whether to raise interest rates.

The S&P 500 gained 1.3 percent to 1,978.11 at 4 p.m. in New York, its highest since Aug. 28.

A report today showed retail sales climbed for a second straight month, a sign consumers may be looking past recent volatility in financial markets. Although confidence has taken a hit from stock-market turmoil and global-growth concerns, the data show households are still putting their savings from cheap energy to work.

Other data showed that while consumers are holding up, factories are struggling. U.S. factory production declined in August by the most since January 2014 as automakers scaled back after a surge the month before and a stronger dollar weighed on demand from overseas customers.

Meanwhile, a quarterly survey said chief executive officers of large U.S. companies are becoming less optimistic about the prospects for the world's largest economy, with more leaders planning to cut capital spending and employment in the next six months. The Business Roundtable CEO Economic Outlook Index fell to the lowest level since 2012, according to results compiled by Bloomberg.

Speculation has increased that the Fed will delay raising rates as China ignited concern that its slowdown could weigh on global growth. While investors remain confident the central bank will increase borrowing costs this year, traders are pricing in just a 30 percent chance of action on Thursday, down from 48 percent before China's currency devaluation last month. Odds of a move at the December gathering are 62 percent, according to data compiled by Bloomberg.

Equities have been particularly volatile recently, with the Chicago Board Options Exchange Volatility Index jumping a record 135 percent in August amid the first 10 percent correction in U.S. equities in four years. Since 1990, the measure of market turbulence known as the VIX has averaged 16.9 when U.S. policy makers started raising rates. If the Fed increases rates this week, it would be the first time since 1946 it has done so within a month of a correction.

The bull market that began in March 2009 is the third longest in history, but it's the longest ever to go without an increase by the Fed, eclipsing the nearest competitor by more than eight months. Economists are evenly split on whether there will be a hike, with about half the 81 surveyed by Bloomberg predicting a rate increase.

After sliding into a correction, the S&P 500 has rallied 5.9 percent since Aug. 25, though the benchmark is still down 7.2 percent from its all-time high set in May. The gauge has lost 3.9 percent this year.

-

21:00

DJIA 16623.73 252.77 1.54%, NASDAQ 4866.13 60.37 1.26%, S&P 500 1981.05 28.02 1.43%

-

18:21

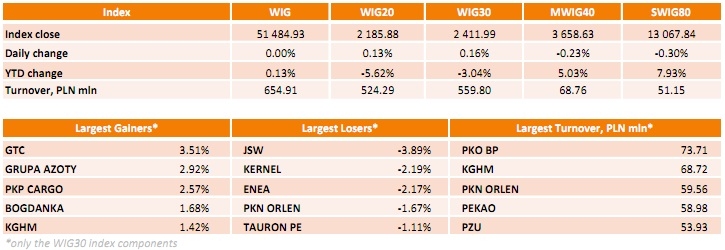

WSE: Session Results

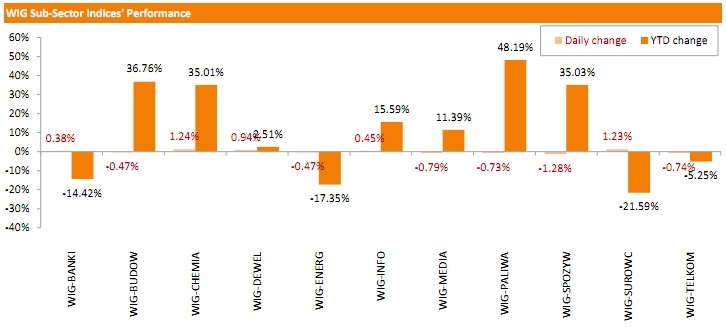

Polish equity market finished unchanged on Tuesday, as measured by the WIG index. From a sector perspective, food sector (-1.28%) was the weakest group, while chemicals (+1.24%) and materials (+1.23%) outperformed.

The large-cap stocks' measure, the WIG30 Index, added 0.16%. Within the index components, GTC (WSE: GTC) managed to record the best daily result, advancing by 3.51%. It was followed by GRUPA AZOTY (WSE: ATT) and PKP CARGO (WSE: PKP), which climbed by 2.92% and 2.57% respectively. On the other side of the ledger, JSW (WSE: JSW) fared the worst, slumping 3.89%. KERNEL (WSE: KER) lost 2.19%, retreating after two days of gains. Utilities names ENEA (WSE: ENA) and TAURON PE (WSE: TPE) also generated solid losses, sliding down 2.17% and 1.11% respectively.

-

18:17

Wall Street. Major U.S. stock-indexes rose

Major U.S. stock-indexes rose on Tuesday after data showed retail sales continued to climb in August but investors remained cautious ahead of this week's Federal Reserve meeting. U.S. consumer spending appeared to grow at a healthy pace halfway through the third quarter, pointing to solid domestic demand that could persuade the Fed to raise interest rates. Analysts said an interest rate hike would remove the uncertainty that has dogged the market for several weeks.

Almost all of Dow stocks in positive area (29 of 30). Top looser - The Walt Disney Company (DIS, -1.08%). Top gainer - Chevron Corporation (CVX, +2.27).

All S&P index sectors in positive area. Top gainer - Industrial goods (+0,9%).

At the moment:

Dow 16423.00 +144.00 +0.88%

S&P 500 1958.25 +14.25 +0.73%

Nasdaq 100 4333.75 +34.00 +0.79%

10 Year yield 2,23% +0,05

Oil 45.00 +1.00 +2.27%

Gold 1103.70 -4.00 -0.36%

-

18:00

European stocks close: stocks closed higher after the mixed economic data from the Eurozone

Stock indices closed higher after the mixed economic data from the Eurozone. The ZEW Center for European Economic Research released its economic sentiment index for Germany and the Eurozone on Tuesday. Germany's ZEW economic sentiment index declined to 12.1 in September from 25.0 in August, missing expectations for a fall to 18.4.

"The weakening economic development in emerging markets dampens the economic outlook for Germany's export-oriented economy. While economic growth in the second quarter was largely driven by external demand, it is becoming less likely that exports will stimulate growth in the near future," the ZEW President Clemens Fuest.

Eurozone's ZEW economic sentiment index decreased to 33.3 in September from 47.6 in August.

Eurozone's unadjusted trade surplus jumped to €31.4 billion in July from €26.4 billion in June.

Exports rose at an annual rate of 7.0% in July, while imports increased at 1.0%.

Eurozone's employment increased by 0.3% in the second quarter, after a 0.2% rise in the first quarter. The first quarter's figure was revised up from a 0.1% gain.

The Office for National Statistics (ONS) released the consumer price inflation data for the U.K. on Tuesday. The U.K. consumer price index declined to 0.0% in August from 0.1% in July, in line with expectations.

The decline was driven by low petrol prices.

On a monthly basis, U.K. consumer prices rose 0.2% in August, in line with expectations, after a 0.2% decline in July.

Consumer price inflation excluding food, energy, alcohol and tobacco prices fell to 1.0% in August from 1.0% the month before.

The Retail Prices Index remained climbed to 1.1% in August from 1.0% in July, beating expectations for a decrease to 0.9%.

The consumer price inflation is below the Bank of England's 2% target.

The U.K. house price index rose at a seasonally adjusted rate of 0.8% in July, faster than a 0.6% in June.

The increase was mainly driven by a rise in prices in the east and south-east of England.

On a yearly basis, the U.K. house price index increased at a seasonally adjusted rate of 5.2% in July, down from a 5.7% gain in June. It was the lowest rise since September 2013.

The lower house price inflation was mainly driven by a decline in prices in Scotland and the north-east of England.

Indexes on the close:

Name Price Change Change %

FTSE 100 6,137.6 +53.01 +0.87 %

DAX 10,188.13 +56.39 +0.56 %

CAC 40 4,569.37 +51.22 +1.13 %

-

18:00

European stocks closed: FTSE 6137.60 53.01 0.87%, DAX 10188.13 56.39 0.56%, CAC 40 4569.37 51.22 1.13%

-

17:17

Fiscal spending in China rises 25.9% in August

China's Ministry of Finance said on Tuesday that fiscal spending in China rose 25.9% in August from a year earlier. It was biggest increase since April.

For the first eight months of 2015, fiscal expenditure rose by 14.8% compared with the same period last year. Spending on education jumped 15.8% in the January-August period, healthcare was up by 19.5%, energy conversation and clean technology increased by 22.7% while social security and employment gained by 21.7%.

-

16:40

U.K. leading economic index falls 0.3% in July

The Conference Board (CB) released its leading economic index for the U.K. on Tuesday. The leading economic index decreased 0.3% in July, after a 0.3% decline in June.

The coincident index was up 0.1% in July, after a flat reading in July.

"The current behaviour of the composite indexes suggests that the economy is likely to continue to grow in the short-term, but the pace is unlikely to pick up," the CB said.

-

16:23

U.S. business inventories rise 0.1% in July

The U.S. Commerce Department released the business inventories data on Tuesday. The U.S. business inventories rose 0.1% in July, in line with expectations, after a 0.7% gain in June. It was the smallest rise since March.

June's figure was revised down from a 0.8% increase.

The increase was partly driven by a rise in retail inventories. Retail inventories climbed 0.6% in July, wholesale inventories were down 0.1%, while manufacturing inventories fell 0.1%.

Business sales climbed 0.1% in July, while retail sales increased 0.8%.

The business inventories/sales ratio remained unchanged at 1.36 months in July. The business inventories /sales ratio is a measure of how long it would take to clear shelves.

-

15:50

U.S. industrial production declines 0.4% in August

The Federal Reserve released its industrial production report on Tuesday. The U.S. industrial production fell 0.4% in August, missing expectations for a 0.2% decrease, after a 0.9% gain in July. July's figure was revised up from a 0.6% rise.

The drop was driven by a fall in the manufacturing output, which plunged by 0.5% in August. It was the biggest drop since January 2014.

Mining output was down 0.6% in August, while utilities production increased 0.6%.

Capacity utilisation rate decreased to 77.6% in August from 78.0% in July, missing expectations for a decline to 77.8%.

-

15:32

U.S. Stocks open: Dow +0.31%, Nasdaq +0.24%, S&P +0.31%

-

15:26

Before the bell: S&P futures +0.21%, NASDAQ futures +0.20%

U.S. stock-index futures were little changed as data showed retail sales climbed for a second straight month, a sign consumers may be looking past recent volatility in financial markets.

Global Stocks:

Nikkei 18,026.48 +60.78 +0.34%

Hang Seng 21,455.23 -106.67 -0.49%

Shanghai Composite 3,004.36 -110.44 -3.55%

FTSE 6,080.4 -4.19 -0.07%

CAC 4,538.8 +20.65 +0.46%

DAX 10,142.61 +10.87 +0.11%

Crude oil $44.46 (+1.07%)

Gold $1106.40 (-0.12%)

-

15:08

Wall Street. Stocks before the bell

(company / ticker / price / change, % / volume)

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

11.30

1.25%

24.0K

ALCOA INC.

AA

9.42

0.43%

15.1K

General Motors Company, NYSE

GM

30.84

0.39%

0.6k

Chevron Corp

CVX

76.01

0.32%

1.3K

Apple Inc.

AAPL

115.63

0.28%

139.9K

Exxon Mobil Corp

XOM

72.67

0.25%

1.5K

Amazon.com Inc., NASDAQ

AMZN

522.00

0.12%

3.1M

Microsoft Corp

MSFT

43.08

0.09%

23.7M

Facebook, Inc.

FB

92.39

0.09%

23.4K

General Electric Co

GE

24.79

0.08%

0.7k

Twitter, Inc., NYSE

TWTR

26.92

0.07%

24.6K

Intel Corp

INTC

29.40

0.03%

24.1M

Visa

V

70.01

0.00%

0.4k

Barrick Gold Corporation, NYSE

ABX

6.23

0.00%

0.4k

Hewlett-Packard Co.

HPQ

27.04

0.00%

0.3k

ALTRIA GROUP INC.

MO

52.44

-0.02%

0.1k

Cisco Systems Inc

CSCO

25.69

-0.04%

21.6M

AT&T Inc

T

32.53

-0.06%

21.9K

Google Inc.

GOOG

622.80

-0.07%

0.4k

Walt Disney Co

DIS

103.70

-0.12%

5.1K

Ford Motor Co.

F

13.76

-0.15%

1k

Tesla Motors, Inc., NASDAQ

TSLA

252.31

-0.35%

2.9M

Yandex N.V., NASDAQ

YNDX

12.00

-0.41%

12.1M

Verizon Communications Inc

VZ

45.43

-0.48%

0.1k

International Paper Company

IP

41.00

-1.20%

12.6K

Yahoo! Inc., NASDAQ

YHOO

29.69

-2.08%

86.1K

-

15:01

U.S. retail sales increase 0.2% in August

The U.S. Commerce Department released the retail sales data on Tuesday. The U.S. retail sales climbed 0.2% in August, missing expectations for a 0.3% increase, after a 0.7% gain in July. July's figure was revised up from a 0.6% rise.

The increase was partly driven by higher automobiles purchases. Automobiles and car parts sales rose 0.7% in August.

Retail sales excluding automobiles increased 0.3% in August, beating forecasts of a 0.2% rise, after a 0.7% gain in July. July's figure was revised up from a 0.4% increase.

Sales at building material and garden equipment stores dropped 1.8% in August and sales at furniture stores decreased 0.9%.

Sales at clothing retailers were up 0.4% in August.

These figures could add to speculation on that the Fed starts raising its interest rate this month.

-

14:48

NY Fed Empire State manufacturing index rises to -14.67 in September

The New York Federal Reserve released its survey on Tuesday. The NY Fed Empire State manufacturing index rose slightly to -14.67 in September from -14.92 in August, missing expectations for an increase to -0.75. August's reading was the lowest level since April 2009.

The increase was driven by a rise in the new orders and shipments index. The new orders index increased to -12.90 in September from -15.70 in August, while the shipments index climbed to -7.9 from 13.79.

The general business conditions expectations index for the next six months decreased to 23.2 in August from 33.64 in August.

The price-paid index decreased to 4.1 in September from 7.27 in August.

The index for the number of employees fell to -6. 2 in September from 1.82 last month.

-

14:29

UK house price inflation rises 0.8% in July

The Office for National Statistics (ONS) released its house inflation data for the U.K. on Tuesday. The U.K. house price index rose at a seasonally adjusted rate of 0.8% in July, faster than a 0.6% in June.

The increase was mainly driven by a rise in prices in the east and south-east of England.

On a yearly basis, the U.K. house price index increased at a seasonally adjusted rate of 5.2% in July, down from a 5.7% gain in June. It was the lowest rise since September 2013.

The lower house price inflation was mainly driven by a decline in prices in Scotland and the north-east of England.

The average mix-adjusted house price was £282,000 in July, up from £277,000 in June.

-

14:16

Bank of Japan Governor Haruhiko Kuroda: that the country’s exports and production were "affected by the slowdown in emerging economies"

The Bank of Japan (BoJ) Governor Haruhiko Kuroda said at a press conference on Tuesday that the country's exports and production were "affected by the slowdown in emerging economies". But he pointed out that there is no need for further stimulus measures.

"It's true exports and output are being affected by the slowdown in emerging economies. But there's no change to our view that Japan's economy continues to recover moderately," the BoJ governor said.

Kuroda noted that the underlying trend of inflation was increasing.

The BoJ governor expects the Chinese economy to grow due to the support by the Chinese government.

-

12:03

European stock markets mid session: stocks traded mixed on the mixed economic data from the Eurozone

Stock indices traded mixed on the mixed economic data from the Eurozone. The ZEW Center for European Economic Research released its economic sentiment index for Germany and the Eurozone on Tuesday. Germany's ZEW economic sentiment index declined to 12.1 in September from 25.0 in August, missing expectations for a fall to 18.4.

"The weakening economic development in emerging markets dampens the economic outlook for Germany's export-oriented economy. While economic growth in the second quarter was largely driven by external demand, it is becoming less likely that exports will stimulate growth in the near future," the ZEW President Clemens Fuest.

Eurozone's ZEW economic sentiment index decreased to 33.3 in September from 47.6 in August.

Eurozone's unadjusted trade surplus jumped to €31.4 billion in July from €26.4 billion in June.

Exports rose at an annual rate of 7.0% in July, while imports increased at 1.0%.

Eurozone's employment increased by 0.3% in the second quarter, after a 0.2% rise in the first quarter. The first quarter's figure was revised up from a 0.1% gain.

The Office for National Statistics (ONS) released the consumer price inflation data for the U.K. on Tuesday. The U.K. consumer price index declined to 0.0% in August from 0.1% in July, in line with expectations.

The decline was driven by low petrol prices.

On a monthly basis, U.K. consumer prices rose 0.2% in August, in line with expectations, after a 0.2% decline in July.

Consumer price inflation excluding food, energy, alcohol and tobacco prices fell to 1.0% in August from 1.0% the month before.

The Retail Prices Index remained climbed to 1.1% in August from 1.0% in July, beating expectations for a decrease to 0.9%.

The consumer price inflation is below the Bank of England's 2% target.

Current figures:

Name Price Change Change %

FTSE 100 6,054.19 -30.40 -0.50 %

DAX 10,114.66 -17.08 -0.17 %

CAC 40 4,518.82 +0.67 +0.01 %

-

11:58

Eurozone's employment increases by 0.3% in the second quarter

Eurostat released its employment growth data for the Eurozone on Tuesday. Eurozone's employment increased by 0.3% in the second quarter, after a 0.2% rise in the first quarter. The first quarter's figure was revised up from a 0.1% gain.

Main contributors were Portugal (+1.3%) and Greece (+1.2%).

On a yearly basis, employment in the Eurozone increased by 0.8% in the second quarter.

-

11:53

Eurozone's unadjusted trade surplus rises to €31.4 billion in July

Eurostat released its trade data for the Eurozone on Tuesday. Eurozone's unadjusted trade surplus jumped to €31.4 billion in July from €26.4 billion in June.

Exports rose at an annual rate of 7.0% in July, while imports increased at 1.0%.

-

11:45

Germany's ZEW economic sentiment index drops to 12.1 in September

The ZEW Center for European Economic Research released its economic sentiment index for Germany and the Eurozone on Tuesday. Germany's ZEW economic sentiment index declined to 12.1 in September from 25.0 in August, missing expectations for a fall to 18.4.

"The weakening economic development in emerging markets dampens the economic outlook for Germany's export-oriented economy. While economic growth in the second quarter was largely driven by external demand, it is becoming less likely that exports will stimulate growth in the near future," the ZEW President Clemens Fuest.

Eurozone's ZEW economic sentiment index decreased to 33.3 in September from 47.6 in August.

-

11:41

UK consumer price inflation is down to 0.0% in August

The Office for National Statistics (ONS) released the consumer price inflation data for the U.K. on Tuesday. The U.K. consumer price index declined to 0.0% in August from 0.1% in July, in line with expectations.

The decline was driven by low petrol prices.

On a monthly basis, U.K. consumer prices rose 0.2% in August, in line with expectations, after a 0.2% decline in July.

Consumer price inflation excluding food, energy, alcohol and tobacco prices fell to 1.0% in August from 1.0% the month before.

The Retail Prices Index remained climbed to 1.1% in August from 1.0% in July, beating expectations for a decrease to 0.9%.

The consumer price inflation is below the Bank of England's 2% target.

-

10:50

French consumer price inflation rises 0.3% in August

The French statistical office Insee released its consumer price inflation for France on Tuesday. The French consumer price inflation increased 0.3% in August, after a 0.4% decrease in July.

On a yearly basis, the consumer price index was flat in August, after a 0.2% rise in July.

Fresh food prices rose 8.0% year-on-year in August, while petroleum products prices dropped by 12.5%.

-

10:38

September’s Reserve Bank of Australia monetary policy meeting: there is a downside risk to the outlook for global growth

The Reserve Bank of Australia (RBA) released its minutes from September monetary policy meeting on Tuesday. The RBA said that the accommodative monetary policy was appropriate, adding that the monetary policy decision will depend on the incoming economic data.

The central bank noted that there is a downside risk to the outlook for global growth.

"But it was too early to assess the extent to which this would materially alter the forecast for GDP growth in Australia's trading partners," the RBA said.

Board members pointed out that mining investment will stabilise at lower level.

"Members discussed the implications of the recent emphasis on cost cutting in the mining sector, noting that it would probably lead to mining investment eventually stabilising at a lower level than had previously been expected," the minutes said.

The central bank also said that the Fed's interest rate hike "could have significant effects on financial markets despite the fact that it had been well telegraphed".

The RBA kept unchanged its interest rate at 2.00% in September.

-

10:29

Bank of Japan keeps its monetary policy unchanged in September

The Bank of Japan (BoJ) released its interest rate decision on Tuesday. The BoJ kept its monetary policy unchanged (interest rate: 0.00-0.10%, monetary base target: 275 trillion yen). The central bank will expand its monetary base at an annual pace of 80 trillion yen. This decision was expected by analysts.

The BoJ board members voted 8-1 to keep monetary policy unchanged.

The BoJ noted that the country's economy continued to recover moderately.

The central bank said that the annual inflation in Japan was flat, but inflation expectations seems to be rising.

The BoJ pointed out that exports and production were "affected by the slowdown in emerging economies".

-

10:21

Fitch Ratings: the interest rate hike by the Fed could have a negative impact on emerging economies

Fitch Ratings said in its report "Fed Lift-off Matters for Emerging Markets" that the interest rate hike by the Fed could have a negative impact on emerging economies, despite the fact that the Fed's interest rate hike is widely expected.

"Part of the rationale for ultra-loose monetary policies from global central banks has been to depress risk and term premiums via a portfolio-rebalancing effect. This is consistent with the emergence of pressure on emerging markets as Fed lift-off approaches," Fitch said.

The agency noted that the future path of interest rate hikes remains unclear and that "an outcome closer to the Fed's guidance could be a significant shock".

-

10:11

Chinese government seizes up to 1 trillion yuan from local governments who did not spend their budget

Sources that are close to the government said that the Chinese government seized up to 1 trillion yuan ($157 billion) from local governments who did not spend their budget to stimulate the country's growth. The money should be used for other investments.

"Investments were not realised, and the money will be reallocated," the source said.

-

08:22

Global Stocks: U.S. indices declined

U.S. stock indices declined on Monday as investors were cautious ahead of a two-day Federal Reserve meeting, which starts on Wednesday. Some analysts say that fundamental headlines will continue to drive markets until the next earnings season.

The Dow Jones Industrial Average fell 62.13 points, or 0.4%, to 16,370.96. The S&P 500 lost 8.02 points, or 0.4%, to 1,953.03. The Nasdaq Composite Index declined 16 points, or 0.3%, to 4,805.76.

This morning in Asia Hong Kong Hang Seng slid 0.29%, or 61.51 points, to 21,500.39. China Shanghai Composite Index fell 2.53%, or 78.65 point, to 3,036.15. The Nikkei gained 0.90%, or 162.15 points, to 18,127.85.

Asian stock indices outside Japan declined ahead of the Federal Reserve's meeting.

Japanese stocks rose after the Bank of Japan's meeting. The central bank has left its monetary policy unchanged and pledged to increase monetary base at annual pace of 80 trillion yen. The BOJ cut assessment of overseas economies, exports and output and reiterated that the economy of Japan continued to improve moderately.

-

04:31

Nikkei 225 18,222.7 +257.00 +1.43 %, Hang Seng 21,590.45 +28.55 +0.13 %, Shanghai Composite 3,056.33 -58.46 -1.88 %

-

00:31

Stocks. Daily history for Sep 14’2015:

(index / closing price / change items /% change)

Nikkei 225 17,965.7 -298.52 -1.63 %

Hang Seng 21,561.9 +57.53 +0.27 %

S&P/ASX 200 5,096.47 +25.39 +0.50 %

Shanghai Composite 3,114.87 -85.37 -2.67 %

FTSE 100 6,084.59 -33.17 -0.54 %

CAC 40 4,518.15 -30.57 -0.67 %

Xetra DAX 10,131.74 +8.18 +0.08 %

S&P 500 1,953.03 -8.02 -0.41 %

NASDAQ Composite 4,805.76 -16.58 -0.34 %

Dow Jones 16,370.96 -62.13 -0.38 %

-