Noticias del mercado

-

18:28

WSE: Session Results

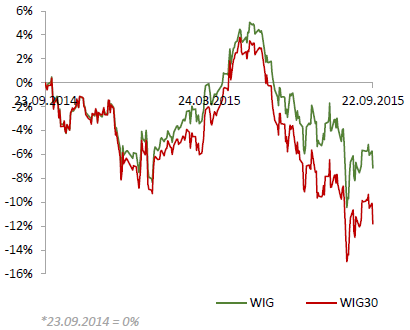

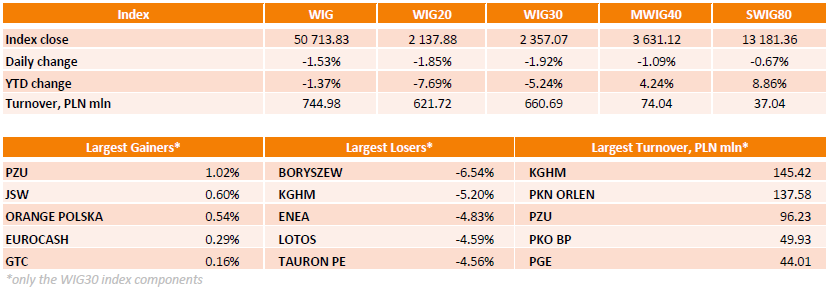

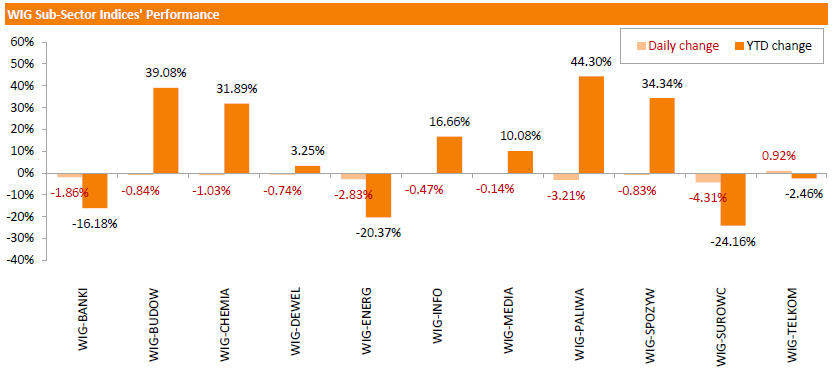

Polish equity market retreated on Tuesday. The broad market measure, the WIG Index, lost 1.53%. All sectors, but for telecommunications (+0.92%), were down. Materials (-4.31%) fared the worst, followed by oil and gas sector (-3.21%) and utilities (-2.83%).

The large-cap stocks' measure, the WIG30 Index, fell by 1.92%. There were only a few gainers among the index components. PZU (WSE: PZU) posted the strongest advance, up 1.02%. Other gainers, namely, JSW (WSE: JSW), ORANGE POLSKA (WSE: OPL), EUROCASH (WSE: EUR), GTC (WSE: GTC) and PKP CARGO (WSE: PKP), added less than 1%. On the other side of the ledger, BORYSZEW (WSE: BRS) was the biggest decliner, plunging by 6.54%. It was followed by KGHM (WSE: KGH), slumping 5.20% on weaker copper prices. ENEA (WSE: ENA), LOTOS (WSE: LTS), TAURON PE (WSE: TPE) and PKN ORLEN (WSE: PKN) were also among top fallers, losing more than 4% each.

-

18:11

Wall Street. Основные фондовые индексы США теряют более полутора процента

Major U.S. stock-indexes fell more than 1.5% on Tuesday morning amid a decline in commodity prices and continuing uncertainty about when the Federal Reserve will raise interest rates. Copper prices hit a three-week low, while oil was down more than 2 percent on persistent worries about demand, especially in China. The Fed last week kept rates at near-zero levels, citing the turbulence in a tightly linked global economy, including slowing growth in China. But, Atlanta Fed President Dennis Lockhart said on Monday a rate hike later this year was still possible.

All of Dow stocks in negative area (30 of 30). Top looser - United Technologies Corporation (UTX, -3.70%).

All of S&P index sectors also in positive area. Top looser - Healthcare (-2.2%).

At the moment:

Dow 16150.00 -306.00 -1.86%

S&P 500 1924.50 -38.50 -1.96%

Nasdaq 100 4237.00 -104.25 -2.40%

10 Year yield 2,13% -0,08

Oil 45.76 -1.20 -2.56%

Gold 1124.90 -7.90 -0.70%

-

18:03

European stocks close: stocks closed lower as shares of miners and automakers dropped due to a decline in commodity prices

Stock indices closed lower as shares of miners and automakers dropped due to a decline in commodity prices.

The European Central Bank (ECB) Chief Economist Peter Praet said on Monday that the central bank will expand its asset-buying programme to defend its inflation objective if needed.

Meanwhile, the economic data from the Eurozone was mixed. The European Commission released its preliminary consumer confidence figures for the Eurozone on Tuesday. Eurozone's preliminary consumer confidence index fell to -7.1 in September from -6.9 in August, missing expectations for a decline to -7.0.

European Union's consumer confidence index declined by 0.8 points to -5.5 in September.

Destatis released its real wages growth data for Germany on Tuesday. Real wages in Germany rose by 2.7% year-on-year in the second quarter, after a 2.5% growth in the first quarter. It was the biggest increase since the series began in 2008.

Nominal earnings climbed 3.2% year-on-year in the second quarter. In the same period, German consumer price index increased 0.5%.

The Office for National Statistics released public sector net borrowing for the U.K. on Tuesday. The public sector net borrowing in the U.K. rose to £11.31 billion in August from £0.07 billion in July. July's figure was revised up from -£2.07 billion. Analysts had expected an increase to £8.65 billion.

Public sector net borrowing excluding public sector banks totalled £12.1 billion in August, up by £1.4 billion from last year. It was the highest level for August since 2012.

Total debt was £1,506 billion in August, up £68.9 billion from last year. It was equal to 80.6% of GDP.

The increase in debt was driven by a decline in income tax paid.

The Confederation of British Industry (CBI) released its industrial order books balance on Tuesday. The CBI industrial order books balance dropped to -7% in September from -1% in August, missing expectations for a rise to 0%.

The decrease was partly driven by a fall in export order book balance. The export order book balance plunged to -24% in September from -8% in August.

The balance for output volumes for the next three months was 0% in September, down from +14% in August. It was the lowest level since October 2013.

Indexes on the close:

Name Price Change Change %

FTSE 100 5,935.84 -172.87 -2.83 %

DAX 9,570.66 -377.85 -3.80 %

CAC 40 4,428.51 -156.99 -3.42 %

-

18:00

European stocks closed: FTSE 100 5,935.84 -172.87 -2.83% CAC 40 4,428.51 -156.99 -3.42% DAX 9,570.66 -377.85 -3.80%

-

17:02

Asian Development Bank cut its growth forecasts for China and India

The Asian Development Bank (ADB) lowered growth forecasts for China and India. According to the ADB, China is expected to expand by 6.8% in 2015, down from July estimate of a 7.0% rise, and 6.7% in 2016, down from July estimate of a 6.8% increase.

India is expected to rise by 7.4% in the financial year 2015 ending March 2016, down from July estimate of a 7.8% rise, and 7.8% in the fiscal year 2016 ending March 2017, down from July estimate of a 8.2% increase.

The downgrade of the Indian growth was driven by a weak external demand and a slower-than-expected pace of reform implementation.

The economic growth of developing Asia is expected to be 5.8% this year, down from July estimate of a 6.1% increase, and 6% in 2016, down from July estimate of a 6.2% rise.

Inflation in developing Asia is expected to decline to 2.3% in 2015 from 3% in 2014 due to low global commodity prices.

Southeast Asia is expected to grow 4.4% in 2015 and 4.9% in 2016.

"The combination of a moderating prospect in China and India, together with delayed recovery of advanced countries, weighed on our forecast for the region as a whole," ADB Chief Economist Shang-Jin Wei said.

-

16:37

Eurozone’s preliminary consumer confidence index declines to -7.1 in September

The European Commission released its preliminary consumer confidence figures for the Eurozone on Tuesday. Eurozone's preliminary consumer confidence index fell to -7.1 in September from -6.9 in August, missing expectations for a decline to -7.0.

European Union's consumer confidence index declined by 0.8 points to -5.5 in September.

-

16:29

Richmond Fed Manufacturing Index drops to -5 in September

The Federal Reserve Bank of Richmond released its survey of manufacturing activity on Tuesday. The composite index for manufacturing dropped to -5 in September from 0 in August.

The decline was driven by decreases in new orders. New orders subindex was down to -12 from 1.

Shipments subindex rose to -3 in September from -4 in August.

"Order backlogs and new orders decreased, while shipments declined. Average wages continued to increase at a moderate pace this month, however manufacturing employment grew mildly. Prices of raw materials and prices of finished goods rose, although at a slightly slower pace compared to last month," the survey said.

-

15:49

U.S. house price index rise 0.6% in July

The Federal Housing Finance Agency (FHFA) released its monthly house price index for the U.S. on Tuesday. The U.S. house price index rose 0.6% on a seasonally adjusted basis in July, after a 0.2% gain in June.

On a yearly basis, U.S. house prices climbed 5.8% in July.

-

15:37

U.S. Stocks open: Dow -0.96%, Nasdaq -1.33%, S&P-0.97%

-

15:27

Before the bell: S&P futures -1.71%, NASDAQ futures -1.98%

U.S. stock-index futures fell, with raw-material shares dragged lower as commodities retreated and Volkswagen AG's diesel-emissions cheating scandal continued to rattle global auto stocks.

Hang Seng 21,796.58 +39.65 +0.18%

Shanghai Composite 3,186.32 +29.78 +0.94%

FTSE 5,960.88 -147.83 -2.42%

CAC 4,431.32 -154.18 -3.36%

DAX 9,628.12 -320.39 -3.22%

Japan Stock Market was closed.

Crude oil $45.20 (-3.17%)

Gold $1126.10 (-0.59%)

-

15:01

Wall Street. Stocks before the bell

(company / ticker / price / change, % / volume)

E. I. du Pont de Nemours and Co

DD

48.34

0.21%

1.9K

UnitedHealth Group Inc

UNH

123.75

-0.15%

0.1K

3M Co

MMM

139.39

-0.46%

0.1K

ALTRIA GROUP INC.

MO

54.41

-0.69%

8.9K

McDonald's Corp

MCD

97.11

-0.81%

0.7K

International Paper Company

IP

40.00

-0.84%

2.7K

HONEYWELL INTERNATIONAL INC.

HON

96.91

-0.85%

0.1K

Procter & Gamble Co

PG

70.00

-0.92%

4.2K

AT&T Inc

T

32.25

-0.95%

17.0K

Verizon Communications Inc

VZ

44.36

-0.98%

0.9K

Johnson & Johnson

JNJ

92.21

-0.99%

0.3K

The Coca-Cola Co

KO

38.80

-1.00%

0.4K

Wal-Mart Stores Inc

WMT

63.07

-1.02%

4.5K

Walt Disney Co

DIS

102.33

-1.04%

5.3K

Visa

V

69.99

-1.12%

6.1K

Deere & Company, NYSE

DE

78.26

-1.14%

0.3K

International Business Machines Co...

IBM

144.77

-1.17%

3.5K

Caterpillar Inc

CAT

71.30

-1.19%

5.5K

Pfizer Inc

PFE

32.03

-1.20%

0.3K

Boeing Co

BA

134.34

-1.24%

1.2K

Apple Inc.

AAPL

113.75

-1.27%

294.4K

Nike

NKE

115.05

-1.30%

0.2K

Home Depot Inc

HD

115.05

-1.31%

1.1K

Amazon.com Inc., NASDAQ

AMZN

541.00

-1.35%

13.1K

Yahoo! Inc., NASDAQ

YHOO

30.75

-1.35%

43.5K

Starbucks Corporation, NASDAQ

SBUX

56.75

-1.37%

6.8K

Google Inc.

GOOG

626.70

-1.38%

4.6K

AMERICAN INTERNATIONAL GROUP

AIG

57.22

-1.40%

0.6K

General Electric Co

GE

24.72

-1.47%

29.6K

Merck & Co Inc

MRK

50.21

-1.51%

5.5K

Cisco Systems Inc

CSCO

25.15

-1.53%

6.0K

Twitter, Inc., NYSE

TWTR

26.96

-1.53%

49.6K

Goldman Sachs

GS

180.50

-1.55%

0.6K

American Express Co

AXP

75.50

-1.62%

0.3K

Facebook, Inc.

FB

94.00

-1.62%

97.1K

JPMorgan Chase and Co

JPM

60.44

-1.64%

4.0K

Chevron Corp

CVX

76.80

-1.65%

10.0K

Citigroup Inc., NYSE

C

49.86

-1.68%

28.0K

Exxon Mobil Corp

XOM

72.13

-1.72%

24.6K

Microsoft Corp

MSFT

43.35

-1.72%

3.7K

United Technologies Corp

UTX

89.96

-1.74%

0.1K

Hewlett-Packard Co.

HPQ

25.96

-1.82%

3.0K

Tesla Motors, Inc., NASDAQ

TSLA

258.99

-1.97%

12.3K

Barrick Gold Corporation, NYSE

ABX

6.45

-1.98%

14.5K

Yandex N.V., NASDAQ

YNDX

11.95

-2.05%

6.9K

Intel Corp

INTC

28.55

-2.09%

45.9K

Ford Motor Co.

F

13.96

-2.51%

45.2K

ALCOA INC.

AA

9.62

-2.83%

61.7K

General Motors Company, NYSE

GM

29.70

-3.00%

34.5K

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

9.99

-5.13%

88.5K

-

14:52

Upgrades and downgrades before the market open

Upgrades:

DuPont (DD) upgraded to Buy from Neutral at Citigroup

Downgrades:

Other:

Apple (AAPL) assumed with a Buy at Goldman; target $163

Hewlett-Packard (HPQ) assumed with a Neutral at Goldman; target $30

Johnson & Johnson (JNJ) initiated with a Buy at UBS

NIKE (NKE) target raised to $128 at Telsey Advisory Group

Travelers (TRV) initiated with a Neutral at Sterne Agee CRT

-

14:47

Australian house price index rises 4.7% in the second quarter

The Australian Bureau of Statistics released its house price index on Tuesday. The Australian house price index rose 4.7% in the second quarter, after a 1.6% gain in the first quarter.

On a yearly basis, house prices jumped 9.8% in the second quarter, after a 6.9% rise in the first quarter.

The total value of residential dwellings in Australia totalled A$5.761 trillion in the second quarter, up A$271.939 billion in the first quarter.

-

14:23

CBI industrial order books balance decreases to -7% in September

The Confederation of British Industry (CBI) released its industrial order books balance on Tuesday. The CBI industrial order books balance dropped to -7% in September from -1% in August, missing expectations for a rise to 0%.

The decrease was partly driven by a fall in export order book balance. The export order book balance plunged to -24% in September from -8% in August.

The balance for output volumes for the next three months was 0% in September, down from +14% in August. It was the lowest level since October 2013.

"Exports are the missing link in the UK recovery at the moment, with the strong pound squeezing manufacturers' margins, even though lower commodity prices are helping to ease cost pressures. Meanwhile manufacturers will have an eye on China's slowdown and its effect on neighbouring markets. Boosting our export performance, alongside innovation, are vital to improving productivity," the CBI director of economics Rain Newton-Smith said.

-

12:00

European stock markets mid session: stocks traded lower as shares of miners and automakers dropped due to a decline in commodity prices

Stock indices traded lower as shares of miners and automakers dropped due to a decline in commodity prices.

The European Central Bank (ECB) Chief Economist Peter Praet said on Monday that the central bank will expand its asset-buying programme to defend its inflation objective if needed.

Meanwhile, the economic data from the Eurozone was positive. Destatis released its real wages growth data for Germany on Tuesday. Real wages in Germany rose by 2.7% year-on-year in the second quarter, after a 2.5% growth in the first quarter. It was the biggest increase since the series began in 2008.

Nominal earnings climbed 3.2% year-on-year in the second quarter. In the same period, German consumer price index increased 0.5%.

The Office for National Statistics released public sector net borrowing for the U.K. on Tuesday. The public sector net borrowing in the U.K. rose to £11.31 billion in August from £0.07 billion in July. July's figure was revised up from -£2.07 billion. Analysts had expected an increase to £8.65 billion.

Public sector net borrowing excluding public sector banks totalled £12.1 billion in August, up by £1.4 billion from last year. It was the highest level for August since 2012.

Total debt was £1,506 billion in August, up £68.9 billion from last year. It was equal to 80.6% of GDP.

The increase in debt was driven by a decline in income tax paid.

Current figures:

Name Price Change Change %

FTSE 100 5,989.13 -119.58 -1.96 %

DAX 9,724.21 -224.30 -2.25 %

CAC 40 4,462.99 -122.51 -2.67 %

-

11:54

European Central Bank Chief Economist Peter Praet: the central bank will expand its asset-buying programme to defend its inflation

The European Central Bank (ECB) Chief Economist Peter Praet said on Monday that the central bank will expand its asset-buying programme to defend its inflation objective if needed.

He noted that the ECB will "certainly do what's necessary".

-

11:44

Public sector net borrowing in the U.K. rises to £11.31 billion in August

The Office for National Statistics released public sector net borrowing for the U.K. on Tuesday. The public sector net borrowing in the U.K. rose to £11.31 billion in August from £0.07 billion in July. July's figure was revised up from -£2.07 billion. Analysts had expected an increase to £8.65 billion.

Public sector net borrowing excluding public sector banks totalled £12.1 billion in August, up by £1.4 billion from last year. It was the highest level for August since 2012.

Total debt was £1,506 billion in August, up £68.9 billion from last year. It was equal to 80.6% of GDP.

The increase in debt was driven by a decline in income tax paid.

-

11:14

Real wages in Germany climb by 2.7% year-on-year in the second quarter

Destatis released its real wages growth data for Germany on Tuesday. Real wages in Germany rose by 2.7% year-on-year in the second quarter, after a 2.5% growth in the first quarter. It was the biggest increase since the series began in 2008.

Nominal earnings climbed 3.2% year-on-year in the second quarter. In the same period, German consumer price index increased 0.5%.

-

11:03

Swiss trade surplus declines to CHF2.87 billion in August

The Swiss Federal Customs Administration released its trade data on Tuesday. The Swiss trade surplus fell to CHF2.87 billion in August from CHF3.58 billion in the previous month. July's figure was revised down from a surplus of CHF3.74 billion.

Exports dropped 2.4% in August, while imports were down 4.0%.

On a yearly basis, exports fell 2.1% in August, while imports decreased 7.4%.

-

10:49

European Central Bank (ECB) Governing Council member Ardo Hansson: low interest rates for a longer period “may lead into unbalances or risks”

European Central Bank (ECB) Governing Council member Ardo Hansson said on Monday that low interest rates for a longer period "may lead into unbalances or risks that-in case they become reality-may become very costly to the society".

He pointed out that "possible bubbles on financial markets or in real-estate prices are more likely when interest rates are low".

-

10:34

European Central Bank (ECB) Governing Council member Ewald Nowotny: interest rates in the Eurozone are likely to stay low as long as the economic growth stays low

European Central Bank (ECB) Governing Council member Ewald Nowotny said on Monday that interest rates in the Eurozone are likely to stay low as long as the economic growth stays low.

"One should not overestimate the possibilities that central banks have in relation to influencing the long-term interest rate. As long as we have an economy with relatively low growth rates, we will have to live with low interest rates," he said.

Nowotny pointed out that it is dangerous to hike interest rates too soon.

"That's a horror scenario," he noted.

Nowotny also said that the ECB pursues "no particular exchange rate policy".

-

10:24

Atlanta Fed President Dennis Lockhart: the Fed could still start raising its interest rates in 2015

Atlanta Fed President Dennis Lockhart said on Monday that the Fed could still start raising its interest rates in 2015.

"As things settle down, I will be ready for the first policy move on the path to a more normal interest rate environment. I am confident the much-used phrase later this year is still operative," he said.

Lockhart noted that the U.S. economy was "performing solidly".

Atlanta Fed president said that he voted for keeping interest rates unchanged last week.

"I supported the decision last week to hold off. The altered risk picture relative to the economic outlook was decisive in my thinking. I thought it prudent to wait to evaluate whether recent developments change the outlook," he said.

Lockhart is a voting member of the Federal Open Market Committee this year.

-

10:12

Alexis Tsipras' Syriza won 35.46% on Sunday

Alexis Tsipras' Syriza party has won the parliament election on Sunday. Syriza has won 35.46%. That share gives the party 145 seats in the 300-seat parliament. The Conservative New Democracy won 28.1% - 75 seats. The fascist party Golden Dawn came in third place with 6.99% - 18 seats. The Independent Greeks, the coalition partner of Tsipras, won 3.69% - 10 seats.

Tsipras has to form the new government.

-

08:15

Global Stocks: U.S. indices gained

U.S. stock indices closed higher on Monday after a FOMC voting member expressed confidence that there will be a rate hike this year.

The Dow Jones Industrial Average rose 125.61 points, or 0.8%, to 16,510.19. The S&P 500 climbed 8.94 points, or 0.5%, to 1,966.97. The Nasdaq Composite Index added 1.73 point, or less than 0.1% to 4,828.95.

Stocks of health-care companies fell.

This morning in Asia Hong Kong Hang Seng rose 0.73%, or 158.67 points, to 21,915.60. China Shanghai Composite Index gained 0.65%, or 20.48 point, to 3,177.02. Japanese markets are on holiday.

Asian stock indices outside Japan advanced following gains in U.S. equities. However, trading volumes were light due to investors' concerns over global growth and absence of market participants from Japan. Investors will watch data on China's economy closely to assess health of the global economy. Markit Economics will release its preliminary report on China's September Manufacturing PMI on Wednesday.

-

04:01

Hang Seng 21,863.44 +106.51 +0.49% Shanghai Composite 3,161.32 +4.78 +0.15%

-

00:33

Stocks. Daily history for Sep 21’2015:

(index / closing price / change items /% change)

Hang Seng 21,756.93 -163.90 -0.75%

S&P/ASX 200 5,066.24 -104.26 -2.02%

Shanghai Composite 3,157.15 +59.24 +1.91%

FTSE 100 6,108.71 +4.60 +0.08%

CAC 40 4,585.5 +49.65 +1.09%

Xetra DAX 9,948.51 +32.35 +0.33%

S&P 500 1,966.97 +8.94 +0.46%

NASDAQ Composite 4,828.96 +1.73 +0.04%

Dow Jones 16,510.19 +125.61 +0.77%

-