Notícias do Mercado

-

23:49

USD/JPY oscillates around 149.20s after Fed’s commentaries, US Housing Starts eyed

- USD/JPY refreshed 32-year highs, around 149.39, on Tuesday.

- US economic data showed mixed signals, with NY Fed Mfg. Index missing estimates, while Industrial Production rose.

- Minnesota Fed Kashkari: Expects the Federal funds rate (FFR) to hit 4.50% at least.

The USD/JPY oscillates around the 149.00 figure amidst a risk-on impulse caused by Britain’s new Finance Minister Jeremy Hunt, scrapping the PM Liz Truss economic draft alongside better-than-estimated US corporate earnings. At the time of writing, the USD/JPY is trading at 149.20, almost flat as the Asian session begins.

USD/JPY advances slightly as Japanese authorities extended their verbal interventions

US equities finished Tuesday’s session in the green, while Asian stocks are set for a mixed open. According to sources cited by Bloomberg, “A better-than-feared earnings season may well be the catalyst the market needs to see a break in the steady grind lower.”

US economic data released during the New York session showed positive signals, contrary to Monday’s New York Fed Manufacturing Index, which is contracting further. US Industrial Production exceeded estimates for the third straight month amidst one of the most aggressive tightening cycles by the US Federal Reserve.

In the meantime, Fed officials led by Minnesota’s Fed President Neil Kashkari adhere to the Fed’s current narrative. Kashkari said that inflation remains high and that data is showing mixed signals. Furthermore, he commented that he could see rates up to mid-4%, and if inflation has not peaked, he doesn’t “see why rates should not go higher.”

Elsewhere, the US Dollar Index, a gauge of the buck’s value, edges lower by 0.06%, dragged down by a risk-on impulse, at 111.994, while the US 10-year benchmark note rate, is flat, at 4%, a headwind for the USD/JPY.

On the Japanese front, Japanese authorities verbal intervention put a lid on the yen’s weakness but could not stop the USD/JPY from printing a fresh 32-year high above 149.00.

Data-wise, an absent Japanese economic docket, will leave traders adrift to pure US dollar dynamics, on the US front, the calendar will feature tier 3 info with Housing Starts, Building Permits, the Fed Beige Book, and Fed speaking.

USD/JPY Key Technical Levels

-

23:45

USD/CAD Price Analysis: 21-DMA challenges rising wedge confirmation above 1.3700

- USD/CAD struggles to extend the bounce off 21-DMA near fortnight low.

- Confirmation of bearish chart pattern, downbeat MACD signals favor sellers.

- Recovery remains elusive unless crossing three-week-old resistance line.

USD/CAD fades bounce off a short-term moving average while keeping the bearish break of a rising wedge around 1.3740 during Wednesday’s Asian session. In doing so, the Loonie pair stays depressed near the two-week low.

Given the bearish MACD signals and the confirmation of the five-week-old rising wedge formation on Monday, USD/CAD is likely to remain on the bear’s radar unless successfully crosses the 1.3850 immediate hurdle comprising the wedge’s lower line.

Even if the quote rises past 1.3850, the 1.4000 psychological magnet and the upper line of the bearish chart pattern, around 1.4030 by the press time, will challenge the upside momentum.

However, a clear run-up beyond 1.4030 won’t hesitate to challenge the May 2020 peak surrounding 1.4175.

Alternatively, the 21-DMA level near 1.3690 restricts the immediate downside of the USD/CAD pair before directing the sellers toward the monthly low of around 1.3500.

It should be noted that the 50-DMA, close to 1.3320 at the latest, appears strong support for the bears to conquer past 1.3500.

Overall, USD/CAD is likely to remain on the bear’s radar despite the latest rebound from the 21-DMA support.

USD/CAD: Daily chart

Trend: Pullback expected

-

23:27

EUR/USD pokes key hurdle to the north below 0.9900 ahead of EU inflation

- EUR/USD bulls attack five-week-old resistance while taking rounds to fortnight high.

- US dollar traces subdued yields amid firmer sentiment, mixed data.

- EU/German ZEW numbers were upbeat for October, European Commission proposed ‘dynamic cap’ to gas price.

- Final readings of EU inflation, second-tier US housing data to entertain traders.

EUR/USD bulls take a breather around an important resistance as it seesaws near 0.9860-65 during Wednesday’s Asian session. That said, the major currency pair refreshed a two-week high of 0.9875 as a risk-on mood and sluggish yields weighed on the US dollar the previous day.

US Dollar Index (DXY) remains mildly offered near the lowest levels since October 06 during the second loss-making day on Tuesday. In doing so, the greenback’s gauge versus the six major currencies traced the sluggish Treasury yields amid the risk-on mood.

However, firmer US Industrial Production for September and softer NAHB Housing Market Index for October, respectively around 0.4% MoM and 38 versus the market expectations of 0.1% and 43 in that order, pushed back the bears during the later hours of the day.

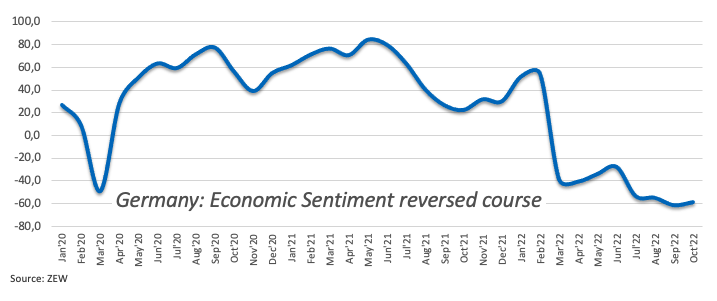

At home, the German ZEW Economic Sentiment Index improved to -59.2 for October versus forecast of -65.7 and -61.9 previous. Further, the same gauge for Eurozone stood at -59.7 for the said period as compared to the -60.6 expected and -60.7 previous reading.

The risk profile remains rosy as equities cheered the absence of the UK’s market collapse, even if the political plays are fishy in Britain. Also likely to have gained little response is the European Commission’s (EC) proposal to purchase gas in bulk and cap the prices in case of extreme volatility. Amid these plays, the US 10-year Treasury yields remained sidelined around the 4.0% threshold.

Looking forward, final readings of September inflation data for the bloc, expected to confirm the initial 10.0% figure, as per the HICP figure, could entertain the EUR/USD traders ahead of the US Building Permits and Housing Starts.

Above all, risk catalysts will be more important for the pair traders to watch for fresh impulses amid a lack of major data and the US dollar’s pullback from the multi-day high.

Technical analysis

The first daily closing beyond the 21-DMA, around 0.9775 by the press time, keeps EUR/USD buyers hopeful of overcoming the immediate trend line hurdle surrounding 0.9860-65, which in turn could propel the quote towards the 50-DMA resistance of 0.9925.

-

23:24

AUD/USD aims an establishment above 0.6300, focus shifts to Australian employment

- AUD/USD is aiming to shift its business above 0.6300 amid a cheerful market mood.

- A decline in US Housing Starts could weigh pressure on the DXY.

- Employment opportunities in Australia are rising at a diminishing rate amid a solid labor market.

The AUD/USD pair picked bids after dropping to near 0.6266 and reclaimed the round-level hurdle of 0.6300 in the late New York session. The pair is oscillating above 0.6300 in early Asia and is expected to shift business higher amid positive market sentiment.

On Tuesday, S&P500 witnessed topsy-turvy moves but settled the traded session around the day’s high. Back-to-back positive trading sessions in the US market are signaling that an all-around risk-on profile is gaining traction. Meanwhile, the US dollar index (DXY) is displaying a sluggish price action around the cushion of 112.00 and is preparing for further weakness.

An upside momentum will be triggered for the aussie bulls if they manage to counter the critical hurdle of 0.6344 confidently. The antipodean may gain strength ahead of the employment data, which will release on Thursday. As per the projections, the Employment Change for September will decline to 25k vs. the prior release of 33.5k. Australia’s tight labor market has left less room for growth in employment opportunities. While the Unemployment Rate will remain steady at 3.5%.

Apart from that, the People’s Bank of China (PBOC)’s monetary policy will be keenly watched. Considering the continuation of the no-tolerance Covid-19 policy and weak real estate demand, the central bank may adopt a ‘dovish’ tone on Prime Lending Rate (PLR). It is worth noting that Australia is a leading trading partner of China.

In the US docket, investors will focus on Wednesday’s Housing Starts data, which reflects retail demand for real estate. The economic data is expected to decline by 1.475M against the former release of 1.575M. It seems that accelerating interest rates by the Federal Reserve (Fed) have started displaying their consequences.

-

22:56

Fed’s Kashkari: Not ready to declare a pause in rate hikes

“Until I see some compelling evidence that core inflation has at least peaked, not ready to declare a pause in rate hikes,” Minneapolis Federal Reserve Bank President Neel Kashkari on Tuesday per Reuters.

Additional comments

Without help from supply side, Fed needs to do more.

Inflation is much too high.

We are getting a lot of mixed signals.

There is some evidence job market is slowing down.

Fed needs to be aware of feedback to the US economy from the strong dollar and other global feedback loops.

Fed does not set monetary policy for the world.

My confidence in where inflation will be in six months is very low.

EUR/USD grinds higher

The news failed to get any major response from the market, may be due to the usual inactive hours of trading, while the EUR/USD pair remains sidelined near the five-week-old resistance surrounding 0.9860.

-

22:54

Gold Price Forecast: XAU/USD turns sideways around $1,650, eyes yields action for further guidance

- Gold price is juggling in a limited territory amid lackluster DXY.

- The precious metal has underperformed against risk-perceived currencies amid firmer yields.

- Solid bets for a hawkish Fed policy have kept the 10-year US yields above 4%.

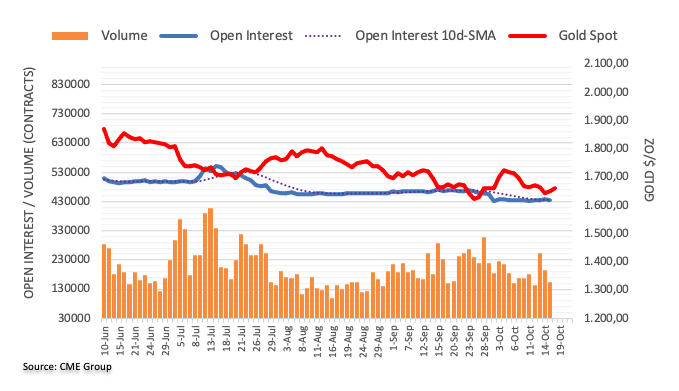

Gold price (XAU/USD) is displaying back-and-forth moves after defending the downside bias below the critical support of $1,650.00. The precious metal is oscillating in a narrow range of $1,645.91-1,657.33 range in early Tokyo. Firmer risk-on sentiment in the market has failed to underpin the yellow metal.

S&P500 has delivered back-to-back bullish trading sessions as the quarterly earnings season has kicked off. Apart from that, risk-perceived currencies have also capitalized on every pullback. The US dollar index (DXY) has logged losses and is hovering around 112.00. The mighty DXY is expected to surrender the 112.00 support further.

The catalyst which is restricting a reversal in the gold prices is the firmer yields that have not surrendered their elevated levels. The 10-year US Treasury yields are holding above the critical hurdle of 4% as the odds for a 75 basis point (bps) rate hike by the Federal Reserve (Fed) are extremely solid. As per the CME FedWatch tool, chances of an increment in the interest rates by 75 bps consecutively for the fourth time stand at around 95%.

Gold technical analysis

Gold prices are auctioning in a symmetrical triangle on an hourly scale as volatility has contracted amid the absence of a trigger in the economic calendar. The downward-sloping trendline is placed from Thursday’s high at $1,682.53 while the upward-sloping trendline is plotted from Friday’s low at $1,640.23.

The precious metal is overlapping with the 20-period Exponential Moving Average (EMA) at $1,652.30, which indicates a consolidation ahead.

Also, the Relative Strength Index (RSI) (14) is oscillating in a 40.00-60.00 range, which indicates the unavailability of a potential trigger.

Gold hourly chart

-

22:45

GBP/JPY Price Analysis: Retraces from weekly highs, meandering around YTD highs

- The GBP/JPY tumbled 0.17% on Tuesday due to waning GBP demand.

- The cross-currency daily chart suggests the GBP/JPY might print a leg-down before resuming its uptrend.

- Short term, the GBP/JPY is upward biased, and if it cleats 169.50, a test of 170.00 is on the cards.

The GBP/JPY surpasses the previous YTD high of around 168.73 but retraces from daily highs at about 169.80, below its opening price by a minimal 0.19%, despite a risk-on impulse. At the time of writing, the GBP/JPY is trading at 168.89.

Sentiment remains upbeat, with US equities registering gains between 0.90% - 1.14%, while the greenback registers slight losses of 0.03%, as shown by the US Dollar Index. In the FX space, the Japanese yen is the laggard, while the British pound is still appreciating after UK’s U-turn on Liz Truss’s minimal budget.

GBP/JPY Price Forecast

Given the backdrop, the GBP/JPY is gaining 1.63% so far in the week. The GBP/JPY daily chart portrays the pair as upward biased, but Tuesday’s price action formed a hanging-man candle pattern, meaning that additional downward pressure is expected. Therefore, GBP/JPY key support lies at 167.58, which, once cleared, could send the GBP/JPY sliding toward the October 17 daily low at 166.43.

The GBP/JPY hourly chart is also upward biased, though price action fluctuates above/below the 20-EMA with no clear trend. However, below the exchange rate, the rest of the EMAs suggest that the upside is warranted, but firstly it will need to clear some hurdles on its way north.

Hence the GBP/JPY first resistance would be the 169.00 figure, followed by the R1 pivot at 169.97, ahead of the 170.00 mark.

GBP/JPY Key Technical Levels

-

22:12

United States API Weekly Crude Oil Stock declined to -1.27M in October 14 from previous 7.054M

-

21:13

Will the US dollar come back by popular demand?

- US dollar is not going down without a fight, supported at key levels.

- The embded fundamentals could see the greenback resurge this week.

The greenback, as measured by the DXY index vs. a basket of currencies, moved a touch higher against a basket of currencies on Tuesday, resurging from the lows seen in the prior day, although there was little conviction from a technical perspective as shown below.

Meanwhile, it's been a mixed day in terms of risk appetite as investors weigh up the earnings outlook against rising interest rates. The narrative surrounding the Federal Reserve remains the key driver, which continues to weigh on the global financial markets. Wall Street's main indexes gapped to the upside at Tuesday's open as strong earnings from Goldman Sachs and Johnson & Johnson that lifted hopes that upbeat corporate reports could soothe market worries about a potential recession due to rising inflation and interest rates. However, at the time of writing, the S&P was up just 1.00%, but still up from the lows of 3,686.53 and down from the 3,762 highs. US treasuries were little changed, with the 10-year yield at 4.01%. The DXY was trading flat at 112.07 and had moved between a low of 111.773 and 112.455.

UK politics in the spotlight

In fundamentals, the Bank of England and UK politics remained front and centre, although there was a sense of calm in the sentiment that gave some stability to markets, The BoE announced its plans to start bond sales on 1 November. however, these won’t include the longer-dated debt recently purchased in the wake of the mini-budget saga. Size and frequency are expected to be similar to that announced prior to the delay, but the BoE will be watching market conditions closely.

The UK's Chancellor, Jeremy Hunt, has announced that he was scrapping "almost all" of the tax cuts announced by the government last month, in a bid to stabilise the financial markets. However, uncertainties remain over the leadership qualities of PM Liz Truss who was said to be hiding "under a desk" after the prime minister did not attend a clash with Sir Keir Starmer in the Commons. Five of her own MPs have now called on her to resign and that does not bode well for the pound. Many more Conservative MPs are calling on the prime minister to quit in anonymous briefings the BBC reported that wrote in an article that Tuss intends to lead the Conservatives into the next general election and apologised for making mistakes.

US dollar remains in demand

With the geopolitical strife happening, the US dollar remains under demand and especially so due to the rates advantage it yields for investors due to the Federal Reserve's hawkish stance. On Tuesday, Raphael Bostic, the head of the central bank’s Atlanta district said that inflation is too high and they have to get it under control. such rhetoric has led to speculators’ net long USD index positions edging higher for the third consecutive week on the back of a persistent string of hawkish Fed speak. Even so, net longs remained below recent averages which would allow for additional length in the coming days and weeks.

Meanwhile, US Industrial Production lifted 0.4% in September, stronger than expected, and driven largely by a solid rise in manufacturing output (+0.4%). ''These results go against the signal in the ISM data, which has been on a softening trajectory for some months now,'' analysts at ANZ Bank explained.

''Part of the strength in manufacturing of late has been an auto production catch-up story, and therefore isn’t expected to persist. But nonetheless, resilience in these data in the face of rapidly tightening monetary policy remains clear. Stepping back, solid growth in goods production as the demand impulse continues to slow will help contain goods inflation, but for the Fed it’s services inflation that tends to be sticky, and currently causing the most concern.''

US yields and the dollar's technical analysis

The 2-year yield is under pressure which has left the US dollar hanging out to dry below last week's low. However, should both of their trendline supports hold up, we could see some upward pressure in both assets.

The US 10-Year Treasury yield, which ended Friday at 4.006%, being its highest weekly finish since July 2008, remains close to the mark which is a supportive factor for the greenback longer term, with the yield closing up for an 11th-straight week last week. Since the yield's March 2020 record-low, pronounced weekly winning streaks have marked some significant highs and only a reversal below 3.81% can put the 3.5620%/3.4980% area at risk, with potential for a much deeper, surprise decline. For now, the W-formations and necklines remain a supportive feature for both the yield and the greenback:

-

21:08

Forex Today: Market steady ahead of inflation updates

What you need to take care of on Wednesday, October 19:

The American Dollar finished Tuesday mixed across the FX board, not far from its daily opening levels. Financial markets lacked clear direction, as government bond yields remained steady, while macroeconomic data was mixed.

The main focus was once again on the United Kingdom. During London trading hours, the Financial Times suggested the Bank of England could delay the start of the quantitative tightening bond-selling program, sending the Pound up and adding pressure on the greenback. However, the BOE quickly denied the headline, saying it was “inaccurate.” As a result, the dollar ticked marginally higher but was unable to retain gains amid rising equities and stable government bond yields.

The GBP/USD pair seesawed with the headlines, ending the day with modest losses at around 1.1320. EUR/USD extended its weekly advance by a few pips to 0.9875 to settle around 0.9850.

The USD/JPY pair kept rallying and surpassed 149.00, its highest in over 30 years. It suffered a near-term knee-jerk during European trading hours, shedding some 100 pips before bouncing back. It is now trading at around 149.20. The 20-year Japanese government bond yield is up to its highest since 2015.

AUD/USD ticked higher, now battling with 0.6300, while USD/CAD also advanced and stands at 1.3740. The Loonie was affected by further slides in crude oil prices, with WTI now trading at around $82.40 a barrel. Gold was also under pressure but finished the day little changed at around $1,650 a troy ounce.

On Wednesday, the EU, the UK, and Canada will publish updated inflation data that could spur volatile moves.

Top 3 Price Prediction Bitcoin, Ethereum, Ripple: Crypto season no more

Like this article? Help us with some feedback by answering this survey:

Rate this content -

21:03

GBP/CAD wavers around 1.5600 after failure to break beyond 1.5700

- The pound treads water at 1.5600 after rejection at 1.5700.

- The GBP loses momentum on Tuesday.

- Lower oil prices have weighed on the Canadian Dollar's demand.

The pound has been trading back and forth, both sides of 1.5600 on Tuesday, after Monday’s rejection from the 2, 1/2-month highs at 1.5700. The pair, however, remains steady above 1.5500 after having bounced from 1.5100 last week.

Sterling loses traction on Tuesday

The cable lost momentum on Tuesday following a sharp rally on Monday after the new UK finance minister, Jeremy Hunt announced that he will scrap most of the aspects of the tax cuts plan presented by his predecessor last month. The British Government’s U-turn has dampened hopes of an aggressive rate hike by the Bank of England, which has undermined GBP’s upside momentum.

Furthermore, the pound saw some positive price action after the Financial Times suggested earlier today that the Bank of England might be considering delaying the start of its quantitative tightening (QT). The report was denied by the bank later on, which sent the GBP lower again.

On the other end, the lower oil prices have kept CAD bulls subdued. WTI oil plunged 4% on Tuesday, weighed by global recession fears and increased selling pressure on the commodity-linked loonie.

GBP/CAD: capped below resistance at 1.5625

From a technical perspective, the pair’s recovery is facing resistance at 1.5625 (October 13, and 14 highs) which is closing the path toward the October 17 high at 1.5705. Above here, the next target would be the August 2 high at 1.5770.

On the downside the pair remains contained above 1.5500 (session low) with a next potential support area at the 100-day SMA, currently around 1.5445 ahead of the 50-day SMA at 1.5260.

Technical levels to watch

-

21:00

United States Total Net TIC Flows: $275.6B (August) vs $153.5B

-

21:00

United States Net Long-Term TIC Flows increased to $197.9B in August from previous $21.4B

-

20:19

USD/CAD climbs above 1.3770s on overall US dollar strength, falling oil prices

- USD/CAD marches 1.3770s due to a risk-on appetite and falling oil prices.

- US September Industrial Production surprisingly exceeded estimates, though Monday’s NY Fed Manufacturing Index contracted for the third month.

- Despite BoC’s rate hike cycle, Canada’s housing starts jumped to its highest levels in almost a year.

The USD/CAD trims some of its Monday’s losses and rises back above the 1.3700 figure after hitting a daily low of 1.3657, below the 20-day EMA, but recovered some ground amid a risk-on impulse, as shown by US equities rising. At the time of writing, the USD/CAD is trading at 1.3774, up by 0.43%.

USD/CAD climbs from under 1.3700, on falling oil prices, and some US dollar strength

Investors’ mood is upbeat, improving their appetite for risk-perceived assets. However, in the case of the USD/CAD, falling crude oil prices keep the loonie on the defensive vs. the greenback. Positive US Industrial Production in September, improving for the third consecutive month, underpinned the greenback.

The Federal Reserve reported that manufacturing production jumped 0.4% MoM, above 0.2% estimates by economists polled by Reuters. Regarding Capacity, Utilization ticked up 2 points, from 80% to 80.3%. Albeit manufacturing production was better than expected, Monday’s New York Fed Empire State Index fell for the third consecutive month, with the survey showing that businesses are pessimistic regarding the future economic outlook.

In the meantime, the US Dollar Index, a measure of the buck against six currencies, edges up 0.06%, at 112.132, underpinning the USD/CAD. Meanwhile, WTI plunges 3.30%, with US crude oil hitting $82.86 PB, a tailwind for the major.

Of late crossing newswires was the Atlanta Fed President Raphael Bostic, who said the Fed couldn’t solve all the problems causing actual inflation.

On the Canadian front, housing starts jumped 11% in September, its highest level in 10 months. The SAAR of housing starts rose by 299,589 units in the last month from an upwardly revised 270,397. Even though data is positive, the Bank of Canada (BoC) BOS survey showed that companies upwardly revised their inflation expectations in Q3, though long-term inflation remains anchored to the BoC’s target.

Analysts at TD Securities are pricing in another rate hike by the BoC. They noted, “While the Bank can draw some comfort that long-term inflation expectations have not become unanchored, we do not expect them to change course amid further erosion to shorter-term measures and ongoing price pressures, particularly in light of recent hawkish comments from Governor Macklem. We think this report supports a 50bp move in October, but recent BoC rhetoric very clearly suggests a 75bp move is in play.”

USD/CAD Key Technical Levels

-

20:11

EUR/USD eases to 0.9850 after rejection at 0.9880

- The euro retreats below 0.9850 after failure at 0.9880.

- The positive market sentiment has acted as a tailwind for the euro.

- EUR/USD correction seen capped below 0.9980/1.0000 – ING.

Eurodollar’s recovery from last week’s lows at 0.9635 has lost steam right below 0.9900 and the pair pulled back to 0.9850 on Tuesday’s afternoon US Trading session. The euro, however, remains moderately positive on the daily chart.

The euro, favoured by the risk-on mood

The common currency managed to extend gains in the early European session, pushing the pair to session highs at 0.9875. European and US stock markets have advanced for the second consecutive day as the enthusiasm for Britain’s U-turn on the tax cuts plan is offsetting concerns about the deterioration in the global economic perspectives.

The mixed German ZEW report, which has shown better than expected sentiment readings in Germany and the Eurozone, while the current situation view has deteriorated beyond expectations, has not dented the EUR recovery.

In the US, a brighter-than-expected industrial report has offered some respite to the USD. Industrial production increased 0.4% in September, beating expectations of a 0.1% increment, while capacity utilization reached a level of 80.3% against the market consensus of 80.0%.

EUR/USD correction to be limited at 0.9980/1.0000 – ING

Currency analysts at ING observe the current euro recovery as a mere correction, which is expected to be capped below 1.0000: Energy shock is temporarily going into reverse as European gas prices drop sharply on the warmer weather and European governments having largely achieved their gas storage targets (…) “A quiet week for US data (just soft US housing) creates a corrective window for EUR/USD, where an obvious target is the top of this year's bear channel at around the 0.9980/1.0000 area. We would assume that this continues to hold the correction.”

Technical levels to watch

-

19:30

Fitch: More aggressive interest rate policy and higher inflation pose risks to consumer spending in 2023

Fitch, on the US, says it expects a very strong consumer balance sheet, the strongest labour market in decades to cushion the impact of likely recession starting in the second quarter, of 2023.

Key notes

- Fitch, on the US says the Fed’s aggressive tightening cycle will increasingly weigh on job growth and consumer demand in 2023.

- Says a drag on real wages from high inflation will prove to be too much of a drain on aggregate household income and consumer spending.

- Says more aggressive interest rate policy and higher inflation pose risks to consumer spending in 2023.

- Says a slowdown in job growth and rising unemployment in 2023 will take a wider toll on consumer spending.

US dollar and yields update

The 2-year yield is under pressure which has left the US dollar hanging out to dry below last week's low. However, should both of their trendline supports hold up, we could see some upward pressure in both assets.

-

19:29

NZD/USD, steady near 0.5700, downside attempts capped at 0.5645

- New Zealand dollar's reversal from 0.5720, contained at 0.5645.

- The kiwi remains moderately positive amid a risk-on mood.

- NZD/USD is expected to consolidate between 1.5570 and 1.5755 – UOB.

The New Zealand dollar remains bid for the second consecutive day on Tuesday. The pair’s reversal from the 0.5700 area has found support at the mid-0.5600, before picking up again to the 0.5685 area.

The kiwi extends recovery as risk appetite prevails

Monday’s positive market sentiment seems to have extended into Tuesday. European stock markets closed with advances between 0.2% and 0.9%, while the US indexes are posting gains beyond 1%, which is underpinning New Zealand dollar's moderate positive tone.

In the macroeconomic docket, the higher-than-expected New Zealand Consumer Price Index has fed hopes of further monetary tightening by the Reserve Bank of New Zealand, which has provided some support to the NZD.

Kiwi bulls, however, seem to be capped below 0.5700 as hopes of another aggressive Fed rate hike in September, are keeping USD weakness on a leash. The market is pricing in a nearly 100% chance that the Fed will hike rates by 75 basis points in November which provides significant support to the USD.

NZD/USD expected to consolidate between 0.5570 and 0.5755 – UOB

Regarding the near-term perspective, FX analysts at UOB expect the pair to consolidate at current levels: “The breach of our ‘strong resistance’ level at 0.5560 indicates that the weakness in NZD has ended. NZD appears to have moved into a consolidation phase and is likely to trade between 0.5570 and 0.5755 for the time being.”

Technical levels to watch

-

19:18

Fed's Bostic: Inflation too high, have to get it under control

Raphael Bostic, the head of the central bank’s Atlanta district has said that inflation is too high and they have to get it under control.

Key comments

There is a need for stable prices for maximum employment growth.

More to come...

-

19:14

Gold Price Forecast: XAU/USD bears hover over the edge of the abyss, preparing to take the leap

- Gold prices remain under pressure below a key dominant bearish trendline.

- The US dollar could find support from a resurgence in US yields.

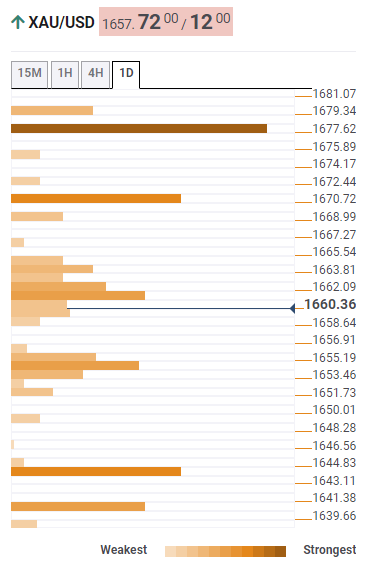

The spot gold price is trading at $1,650.57 and flat on the day at the time of writing. The yellow metal has been trading within a $1,645 / $1,660.93 range on the day so far while the US dollar remains pressured towards the middle of the week which hit its lowest level since Oct. 6, making bullion cheaper for overseas buyers.

However, as the following technical analysis will show, DXY remains on the front side of a key trendline, although further weakness, from a technical standpoint below last week's lows, should serve to support the precious metal. US yields, in that regard, remain around 4% in the 10-year yields with a daily bullish structure which should serve to prop up the US dollar. The 2-year yield is pulling back slightly from the daily highs of 4.53%. This is weighing on the greenback this week and supporting gold as rising interest rates dim gold's appeal as they increase the opportunity cost of holding the non-yielding asset.

Slightly further afield, gold has also been subject to the UK's money markets and the shenanigans in UK politics this month. The UK government's decision to u-turn on vast unfunded fiscal stimulus seemed to boost investors' confidence and some stability is being priced back into the gilt market. The yield on Britain’s 10-year gilt stabilized around 3.9%, but it remains well below the 14-year high of 4.6% reached on October 12th.

The good news, however, came with the New Chancellor Jeremy Hunt saying on Monday that he was reversing almost all tax measures announced in the mini-budget, including cutting the basic rate of income tax from 20% to 19% from April next year. Traders also got the news that

Meanwhile, traders also took note of the Bank of England announcing that sales of government bonds are set to go ahead as planned for November 1. This rebutted an article by the Financial Times that warned that another postponement was likely because of the turmoil in the money markets. While this is important news, the main driver for gold remains with the Federal Reserve.

Its all about the Fed

''Inflation's increasing persistence is a constraint for the Fed, which suggests that a restrictive rates regime may persist for longer than historical precedents. In this context, gold prices are unlikely to rise with a deteriorating growth outlook until the Fed makes progress in the war on inflation,'' analysts at TD Securities explained.

''For the time being, TD Securities has found that US wage growth trends are validating near-term household inflation expectations, but appear to have settled at levels that would sustain a CPI inflation rate of 5%-6% going forward, far removed from the 2.5% rate consistent with the Fed's inflation target. In turn, don't count on investors to grow their appetite in the yellow metal. Physical demand for bullion has remained elevated, but seasonal considerations suggest that this tailwind could soon fade following India's festive season.''

Gold and USD technical analysis

The price of gold is under pressure below the dominant trendline resistance following a retest that failed earlier in the week. A move below $1,650 opens the risk of a significant move towards the recent lows of $1,615, as per the following daily chart:

Meanwhile, this will depend on the outcome of the US dollar:

The trendline support could be tested in the coming day (s) and if this holds, should the index move back above last week's lows, then gold would be respected to crumble as the greenback makes bullish headway from out of key demand area.

-

18:46

GBP/USD is pushing lower and testing levels below 1.1300

- The pound attempts to extend below 1.1300 on retreat from 1.1445.

- Investors scale down hopes of aggressive BoE tightening.

- GBP/USD might decline towards the mid-1.11s – Scotiabank.

The pound is giving away gains on Tuesday, following a 1% rally on Monday as the UK Government ditched most of the tax cuts plan announced in September. The sterling us testing prices sub-1.1300 on retreat from Monday’s highs at 1.1445.

The pound retreats as the market resize BoE hike hopes

UK finance minister’s U-turn on the controversial mini-Budget plan has dampened hopes of aggressive monetary tightening by the Bank of England. This has discouraged GBP buyers, which has been one of the main reasons behind Tuesday’s reversal.

Earlier in the day, the pound saw some positive price action after the Financial Times reported that the Bank of England might be considering delaying the start of its quantitative tightening (QT) gilt sales from the scheduled date of Oct. 31, after having already delayed it from Oct. 6.

The Bank, however, denied the Financial Times ‘report later on. The BoE assured that they do not contemplate any postponement of the start of government bonds’ sales, which has sent the GBP lower again.

GBP/USD: The risk of further decline to the mid-1.11s – ScotiaBank

FX analysts at UBS Scotiabank maintain their negative outlook on the pair, pointing out to targets below 1.1200: “Intraday support in the upper 1.12s is coming under pressure. Below here, cable risks dipping back to the mid-1.11s (…) Political and economic risks for the GBP remain elevated.”

Technical levels to watch

-

18:16

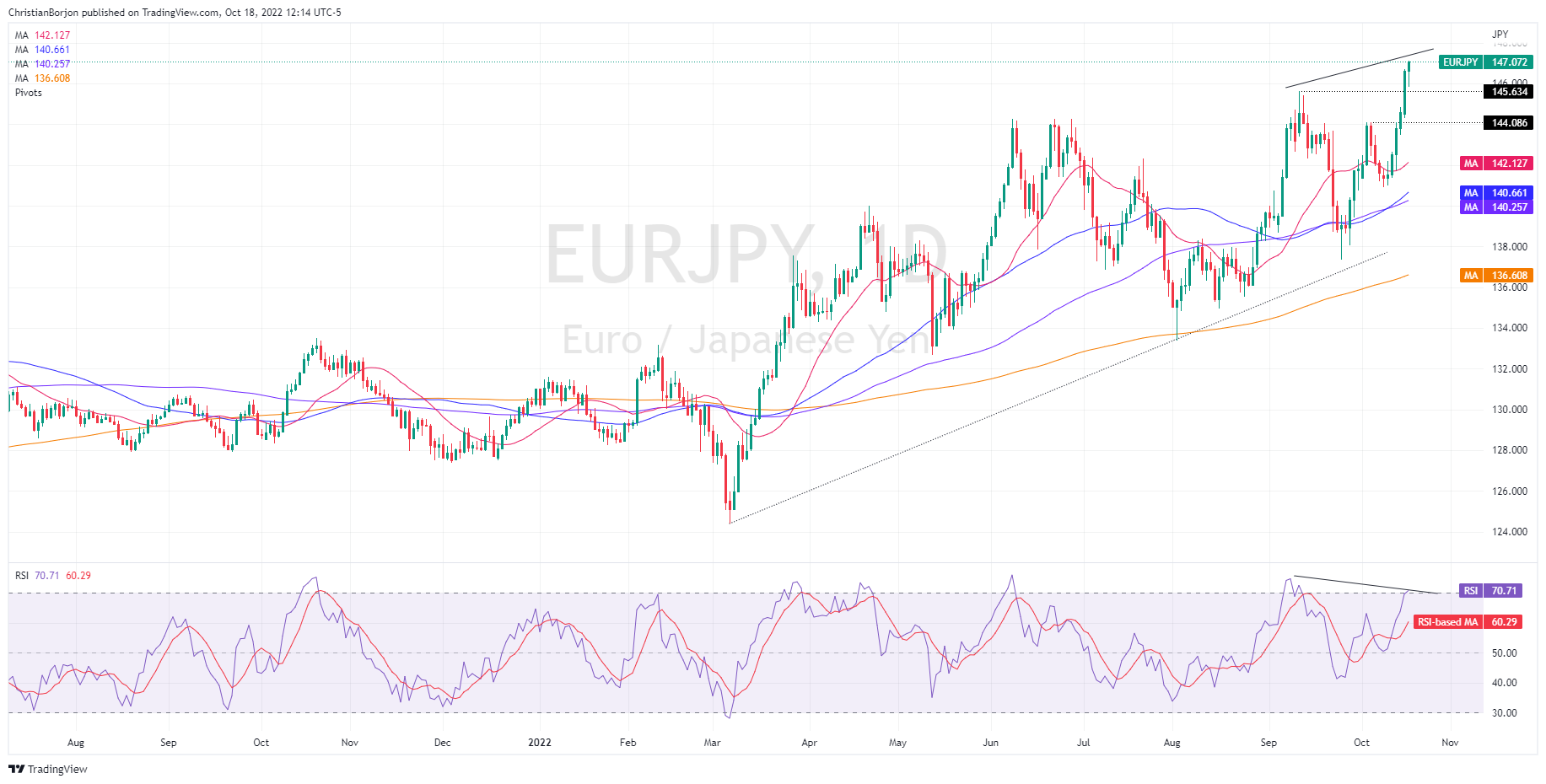

EUR/JPY Price Analysis: Climbs above 147.00, refreshing 8-year highs, as buyers target 150.00

- EUR/JPY printed a fresh YTD high above 147.00 as buyers eye December’s 2014 high.

- A risk-on impulse keeps safe-haven currencies, like the yen, on the defensive.

- EUR/JPY Price Analysis: Negative divergence in the daily and hourly charts to pave the way for a correction towards 145.00.

The EUR/JPY continues extending its gains, eyeing December’s 2013 high of 149.78, while the Japanese yen continues to weaken, despite further verbal interventions by Japanese authorities, which have failed to move the markets in favor of the battered yen. At the time of writing, the EUR/JPY is trading at 147.04. shy of the YTD high of 147.12.

Sentiment-wise, investors’ mood is upbeat, as portrayed by European bourses closing in the green, while US stocks followed suit. Therefore, safe-haven currencies like the Japanese yen, and the Swiss franc, would remain the weakest links in favor of other G8 currencies.

EUR/JPY Price Analysis

The daily chart shows that the EUR/JPY is upward biased. On Monday, the cross-currency pair broke into fresh eight-year highs and, earlier in the North American session, reached a YTD high at 147.12. Of note is that as the EUR/JPY climbs, registering higher highs, the Relative Strength Index (RSI) didn’t, so a negative divergence between RSI and price action could pave the way for a mean-reversion move before continuing to rally.

Hence, the EUR/JPY first support would be the September 12 daily high at 145.63. Break below will expose the October 5 cycle high-turned-support at 144.08, ahead of the 20-day EMA at 142.12.

EUR/JPY Daily chart

In the near term, the EUR/JPY one-hour chart shows price action as overextended, registering higher highs, while the RSI prints lower highs, as in the daily chart. Therefore, a negative divergence surfaced, opening the door for a correction.

Therefore, the EUR/JPY first support would be the 20-EMA at 14.70, which, once cleared, would expose a busy area, with the confluence of the daily low, the 50-EMA, and the central pivot point at around 145.84. A breach of the latter will expose the S1 pivot at around 145.00.

EUR/JPY Hourly chart

EUR/JPY Key Technical Levels

-

18:11

USD/CHF picks up from 0.9920 approaches parity again

- The dollar bounces up at 0.9920 to trim Monday's losses.

- The ongoing risk-on mood is keeping a lid on USD bulls.

- USD/CHF: A break of 0.9876 support will increase downside pressure – Credit Suisse.

The US dollar edged up on Tuesday to pare losses after Monday’s sharp decline. USD/CHF has bounced up from the one-week low at 0.9920 to reach a session high at 0.9975.

The greenback appreciates as US bonds tick up

The uptick in US bond yields seen on Tuesday has provided a fresh boost for the USD to trim previous losses in spite of the positive market sentiment. The risk-on mood seen on Monday, after the historical U-turn on the British Government's mini-Budget plan, seems to have extended into Tuesday.

World stocks have traded higher for the second consecutive day, with the Dow Jones, the S&P, and the Nasdaq, all three appreciating posting advances of about 1% at the time of writing. This positive market mood is keeping a lid on dollar bulls.

On the macroeconomic front, the German ZEW Survey has reflected a larger-than-expected deterioration in the current economic conditions. The report has also revealed higher chances of a decline in the GDP over the next six months, yet without a remarkable impact on the risk-on market mood.

The US dollar has been favoured by a brighter-than-expected performance of the US industrial sector in September. US Industrial Production accelerated at a 0.4% pace, beating expectations of a 0.1% improvement, while the capacity utilization reached 80.3% against market consensus of a mild decline to 80%.

USD/CHF: Breach of 0.9876 will increase downward pressure – Credit Suisse

On the downside, FX analysts at Credit Suisse point out to a key support area at 0.9876: “USD/CHF’s surge was capped at the major resistance at the trendline from 2016 at 1.0075. This strong reversal lower paired with daily RSI holding a bearish divergence continues to strengthen the case for a near-term weakness (…) “Immediate support is seen at the recent low and the 13-day exponential average at 0.9929/13, though only a close below 0.9876 would raise more serious thoughts of the near-term risk shifting lower again.”

Technical levels to watch

-

18:10

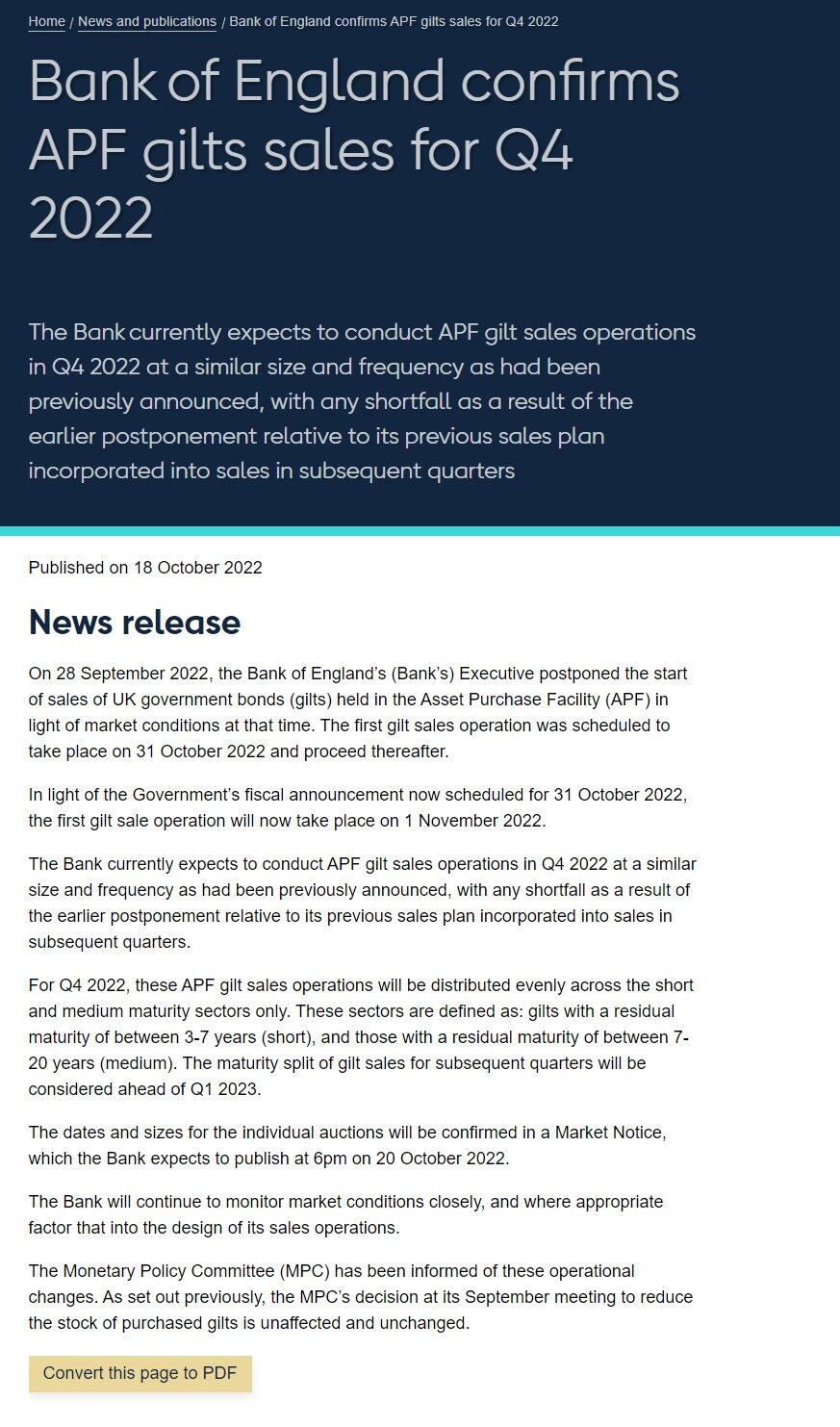

BoE confirms first gilt sale operation will take place Nov. 1

Band of England confirms the first gilt sale operation will take place on November 1 which has put some short-term volatility into GBP/USD.

The Monetary Policy Committee's decision at the September meeting to reduce the stock of purchased gilts is ‘unaffected and unchanged.

This puts to rest the speculation that there would be a delay to the sales and coupled with the U-turn in UK politics, the pound is now driven by the Bank of England's rate hike expectations again. There is less speculation for an aggressive hiking path given the concerns over the economy and cable has been pressured again on Tuesday.

GBP/USD has been as low as 1.1255 on the day, down from 1.1410. It is testing 1.13 at the time of writing.

-

17:43

Silver Price Forecast: XAG/USD oscillates around $18.60s despite high US T-bond yields

- Silver price steadily advances, bouncing off daily lows around $18.55.

- The US 10-year Treasury bond yield rises above 4%, underpinning the buck.

- XAG/USD Price Forecast: Is neutral-downwards, a fall below $18.00 would exacerbate a test of the YTD low.

Silver price climbs as the North American session progresses, trimming earlier losses as US Treasury bond yields rise, as bets that the Federal Reserve would likely hike rates for the fourth time 75 bps increased, putting a lid on the precious metals segment. At the time of writing, XAG/USD is trading at $18.66, above its opening price by 0.33%.

XAG/USD falls as the US 10-year yield rises above 4%

The market sentiment remains upbeat, with most US equities remaining in the green. US Industrial Production exceeded estimates for the third consecutive month in September, increasing 0.4% MoM vs. estimates of 0.1%, while Capacity Utilization ticked up 2 points, from 80% to 80.3%.

Even though Tuesday’s data is encouraging, on Monday, the New York Fed Empire State Manufacturing Index disappointed market participants, contracting for the third straight month, as the survey showed that responders were downbeat about future business conditions.

A reflection of that is the greenback, which dropped more than 1% on Monday, as the US Dollar Index (DXY) portrays. Nevertheless, at the time of typing, the DXY is recovering some ground, gaining 0.12%, at 112.19, underpinned by the 10-year bond yield, which is yielding 4.027%, up one bps.

Hence, XAG/USD hovers around $18.64, pairing some of its earlier losses, while US T-bond yields, namely the 10-year, hold to the 4% threshold. Worth noting that the white metal recovery happened as Fed speakers have not crossed newswires. Silver traders should be aware that Atlanta’s Fed President Raphael Bostic and Minnesota Neil Kashkari would hit wires late in the day.

XAG/USD Price Forecast

XAG/USD remains neutral-to-downward biased, as the daily moving averages (DMAs) reside above the spot price, but with the 20-DMA trapped between the 50 and 100-DMA. Of note, a cross of the 20-DMA below the 50-DMA would mean that sellers gather momentum, further confirmed by the Relative Strength Index (RSI) at bearish territory, which is almost flat. If the 20-DMA crosses below the 50-DMA, and the RSI crosses below its 7-SMA RSI, that could send XAG/USD tumbling towards $18.00, which, once cleared, could pave the way towards a YTD low of $17.56.

-

17:27

GBP/JPY treads water at 169.00 with BoJ intervention looming

- The pound's reversal from 170.00 contained above 168.40.

- The pair trims Monday's gains as hopes of an aggressive BoE hike wane.

- Investors remain wary about a BoJ intervention.

The British pound’s reversal from seven-year highs right above 170.00 seen on Monday found support above 168.40 on Tuesday, before stalling right ahead of 169.00 amid increasing rumors of a BoJ intervention.

The pound gives away Monday’s gains

The new British finance minister’s announcement of the reverse of most of the aspects of its predecessor’s tax cuts plan has generated concern that the Bank of England may not hike rates as aggressively as expected, which has sent the pound moderately lower on Tuesday.

The sterling has seen some positive price action during the European session, as the Financial Times suggested that the Bank of England was planning to delay the start of its quantitative tightening (QT) gilt sales from the scheduled date of Oct. 31, after the initial delay from Oct. 6.

The Bank, however, denied the report later on affirming that they do not contemplate any postponement of the start of government bonds’ sales, which sent the GBP lower again.

On the other end, Investors remain on the watch for the possibility of an intervention by the Bank of Japan to strengthen the JPY. The yen has actually exceeded the level that triggered an intervention by the BoJ last month, and the Japanese Government reiterated on Monday their commitment to a “firm response” to avoid rapid yen declines.

Technical levels to watch

-

17:15

EUR/USD: Bearish, seen trading in the 0.9400/1.0200 range over next weeks – MUFG

Analysts at MUFG Bank see the EUR/USD with a bearish bias for the next weeks, trading in the range 0.9400/1.0200. They war the risk/reward balance for the pair moving lower is becoming less complelling.

Key Quotes:

“The deteriorating growth outlook in the euro-zone is not sufficient yet to shift the ECB’s focus from fighting upside risks to inflation. The latest CPI report revealed that headline inflation moved into double digits in September.”

“ECB policymakers have sent a clear signal that they want to lift rates back towards neutral territory (around 2.00%) by the end of this year. They are also set to begin discussions over shrinking their balance sheet by allowing maturing asset holdings to roll off, although those plans are unlikely to be implemented until the 1H of next year. Overall, the developments still favour holding a bearish EUR bias for the month ahead but the risk/reward balance is becoming less compelling.”

“The main upside risk to our bearish EUR/USD bias could be triggered by a further paring back of more acute energy supply concerns in Europe. If the price of natural gas continues to fall/settles at much lower levels over the winter it could help to ease fears over an even sharper slowdown for the euro-zone economies. At the same time, the EUR could strengthen more than expected if the ECB keeps raising rates at a faster pace while the Fed signals that is considering slowing hikes helping to further narrow expectations for monetary policy divergence.”

-

16:58

USD/JPY: Break over 150.00 looks more likely than not over the short term – MUFG

The USD/JPY is trading above 149.30, at fresh multi-decade highs. Analysts at MUFG Bank, see the pair likely to break above 150.00 in the short term. They doubt over the ability of Japanese authorities to turn the weak yen trend.

Key Quotes:

“We are maintaining the unusually wide range we set last month after the Japanese authorities had intervened to stem the depreciation of the yen. We decided against a bearish bias despite the yen-buying intervention on the view that there would be appetite to buy at lower USD/JPY levels. That proved correct and the yen now today is trading at slightly weaker levels than when the intervention took place in September. We expressed doubts over the ability of the Japanese authorities to turn the weak yen trend without a change in fundamentals.”

“We have turned bullish again on USD/JPY based on the fact that the US dollar backdrop dictates a higher USD/JPY and we see the Japan authorities as being reluctant to protect a specific level. Hence a breach to new highs over 150.00 looks more likely than not over the short-term.”

“The threat of intervention is high and hence a risk to our bullish bias is that the authorities conduct intervention that is more aggressive and more persistent than we assume that would then have a bigger impact on driving USD/JPY lower. There are also risks surrounding the FOMC meeting on 2nd November. A risk to our view is that the FOMC decide to slow the pace of tightening by hiking by only 50bps or hikes by 75bps but provides a dovish communication on the outlook going forward. We think after the CPI data last week this is unlikely.”

-

16:51

AUD/USD trims previous gains and retreats below 0.6300

- AUD/USD loses ground and retreats below 0.6300.

- Fed tightening hopes are buoying demand for the USD.

- The dovish RBA minutes weigh on the AUD.

The Australian dollar is giving away gains on the US morning session. The upside attempt featured during the European trading has been unable to break beyond the 0.6340 resistance area, and the pair has pulled back below the 0.6300 level at the time of writing.

The aussie loses steam with the US dollar picking up

The positive risk sentiment seen during the European and early US trading, with the European and US stock indexes in the green, has failed to boost the AUD above recent ranges. The pair remains dangerously close to the 2, 1/2 -year low at 0.6170 as the US dollar crawls higher.

The uptick in US Treasury bonds, with the 10-year benchmark back above 4% has provided a fresh boost to the US dollar, which was trading at one-week lows against a basket of currencies.

Fed tightening hopes are buoying the USD

As the dust from the British U-Turn on its mini-Budget plan settles, the investors seem to have shifted their focus back to the US Federal Reserve’s tightening cycle.

The market is pricing in a practically 100% chance of another 75 basis point rate in November, which is underpinning the US dollar’s strength to the detriment of the AUD, which has depreciated nearly 15% against the US Dollar this year.

On the other hand, the minutes of the latest RBA monetary policy meeting have been dovishly tilted, as the committee members apparently opted to reduce the size of the rate hike and wait to see the impact of monetary tightening on household spending.

Technical levels to watch

-

16:38

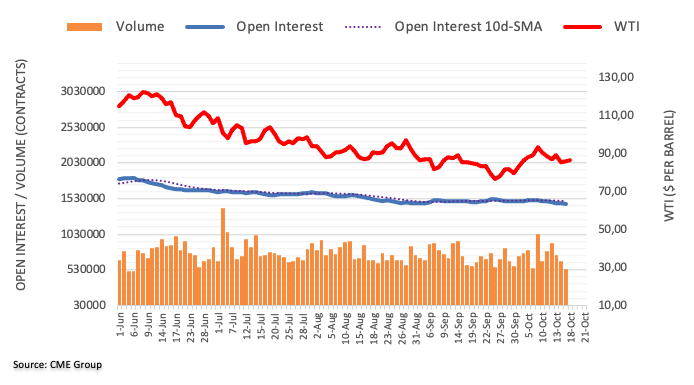

WTI plunges 4% on recession fears mounting, threatening to dampen demand

- WTI drops from daily highs of $86.40s to $82.20s on Tuesday.

- Chinese economic indicators remain delayed, with no rescheduling assigned by the government.

- The US will release oil from its SPR reserve to keep gasoline prices down.

The US crude oil benchmark, also known as Western Texas Intermediate or WTI, dived more than 3% on Tuesday amidst a risk-on impulse on fears that a global economic slowdown might dent oil’s demand. At the same time, the delayed Chinese GDP release weighs on investors’ moods. At the time of writing, WTI is trading at $82.69 per barrel, losing more than 3%.

WTI drops on fears of a global economic slowdown

US equities are trading in the green, supported by earnings. The delay of important Chinese data weighs on WTI traders’ mood, as speculation that growth could have weakened means less demand for black gold. Also, extending its Covid-19 zero-tolerance program might hurt the development of the world’s second-largest economy.

In the meantime, according to Reuters, the US Biden administration plans to sell additional oil from the Strategic Petroleum Reserve (SPR) as the White House tries to control gasoline prices before November’s mid-term elections.

Meanwhile, on Tuesday, OPEC’s secretary general Haitham al-Ghais said that the cartel unanimously decided to cut oil output to prevent a crisis and stem a tide of volatility.

“With macro-economic headwinds forecast for the months ahead and the very real potential for a global recession, which some might say has already started in some parts of the world, there was a consensus amongst the ministers of the need to act now and prevent a crisis later on,” he added.

WTI Price Analysis

WTI is neutral-to-downward biased, as shown by the daily chart. On Tuesday, prices tumbled below the 20-day EMa, extending its losses as sellers eye $80.00 per barrel, which is likely to happen as the Relative Strength Index (RSI), crossed below 50, with enough room before reaching oversold conditions. Therefore, WTI’s first support would be the S3 daily pivot at $82.08, followed by the $81.00 mark, ahead of the S4 pivot point at $80.83, and then the $80.00 mark.

-

16:26

EUR/GBP holds onto daily gains around 0.8700 as pound slides across the board

- Pound among worst performers on Tuesday.

- Bank of England denies it will delay gilts sales.

- EUR/GBP bullish, finds resistance at 0.9730.

The EUR/GBP is rising on Tuesday on the back of a weaker pound, hit by the ongoing political and fiscal drama in the UK. The cross peaked at 0.8731, the highest level since last Thursday and then pulled back toward 0.8700.

UK drama weighs on GBP

The pound is among the worst performers on Tuesday hit by the ongoing political crisis in the United Kingdom. Gilts tumbled after the Bank of England dismissed an Financial Times report that it could delay the sale of bonds, scheduled for October 31. That same day, the government will announce more fiscal plans. With all that is going on, there is a long time until that date and the UK could even have a new PM by then.

Inflation figures are due in the UK on Wednesday and also the final reading of Eurozone September inflation numbers.

Regarding the energy crisis, the European Commission is proposing member countries to buy gas collectively. It also proposed a cap on excessive and volatile gas prices.

EUR/GBP up but unable to break 0.8730

The EUR/GBP is moving with a bullish bias in the very short-term. The upside found resistance at 0.8730. A break higher would open the doors for a recovery above 0.8800. The next crucial area is seen at 0.8810 with a break higher, strengthening the outlook for the euro.

A slide below 0.8660 would be positive for the pound, exposing the 0.8600/10 area. A daily close below should open the doors to more losses in the short-term.

Technical levels

-

15:59

Gold Price Forecast: Do not look at XAU/USD as a safe-haven – TDS

Aggressive Federal Reserve rate hike bets as inflation expectations remain high are set to weigh on gold, strategists at TD Securities report.

Investors unlikely to grow their appetite for gold

“A flat and inverted yield curve has historically been associated with a slowing growth outlook and concurrently rising gold prices. This cycle, however, inflation's increasing persistence is a constraint for the Fed, which suggests that a restrictive rates regime may persist for longer than historical precedents. In this context, gold prices are unlikely to rise with a deteriorating growth outlook until the Fed makes progress in the war on inflation.”

“US wage growth trends are validating near-term household inflation expectations, but appear to have settled at levels that would sustain a CPI inflation rate of 5%-6% going forward, far removed from the 2.5% rate consistent with the Fed's inflation target. In turn, don't count on investors to grow their appetite for the yellow metal.”

“Physical demand for bullion has remained elevated, but seasonal considerations suggest that this tailwind could soon fade following India's festive season.”

-

15:47

New Zealand GDT Price Index came in at -4.6%, below expectations (0.6%)

-

15:36

Canadian CPI Preview: Forecasts from seven major banks, signs of easing price pressures?

Statistics Canada will release September Consumer Price Index (CPI) data on Wednesday, October 19 at 12:30 and as we get closer to the release time, here are the forecasts by the economists and researchers of seven major banks regarding the upcoming Canadian inflation data.

Headline is seen falling two ticks to 6.8% year-on-year, while Core, which excludes volatile food and energy prices, is expected to fall one tick to 5.6% YoY. On a monthly basis, Canadian CPI is seen flat.

RBC Economics

“The backward-looking September CPI numbers should confirm that current price pressures are still too high and broadly based to take the BoC off its rate hiking path. Headline inflation readings have been declining since early summer as gasoline and oil prices retrench. We expect the rate to tick lower again, to 7% in September. But measures of ‘core’ inflation (measures designed to provide a better gauge of underlying inflation pressures) were likely stickier. We expect YoY price growth excluding food and energy products increased in September and the Bank of Canada’s preferred ‘median’ and ‘trim’ core CPI measures are not expected to repeat the small dip in August. That contrast between ‘headline’ and ‘core’ inflation measures will persist in the near-term. Indeed, core inflation isn’t likely to meaningfully slow until December. Upside surprises, either from little improvements in inflation expectations or a worsening reading in the actual CPI, risk tilting that to a bigger 75 bps increase.”

TDS

“We look for inflation to edge 0.2% lower to 6.8% as a large drag from energy leaves prices unchanged from August. A rebound in rents and motor vehicles will offset the drag from energy, and core inflation should edge lower by ~0.1%. Even though a 6.8% inflation rate remains uncomfortably high for the Bank of Canada, our forecast would leave the Q3 average ~0.9pp below projections from the July MPR at 7.1%, and we should also see some modest improvement across core inflation measures.”

NBF

“While price increases could still have been sustained in the services sector, we expect goods inflation to have continued to weaken on lower prices for transportation and thanks to an easing of supply chain issues. Slumping gasoline prices might also have helped cooling price pressures. As a result, the headline index could have decreased by 0.2% MoM before adjustments for seasonality, allowing the YoY rate to drop from 7.0% to 6.6%. The annual rate of trim (from 5.2% to 5.0%) and median CPI (from 4.8% to 4.6%) might have declined as well.”

Citibank

“We expect a modest -0.1% MoM decline in September CPI, with the YoY measures moderating further to 6.6%. Most important will be the trend in core inflation measures after the first signs of a pullback in August. Continued moderation in core CPI measures would be consistent with leading survey indicators that suggest further easing into year-end. These will be key for BoC’s decision in October. We expect a further easing in inflation data to support a shift to a 50 bps pace of hikes by the BoC in October.”

CIBC

“Unadjusted prices are expected to drop by 0.2% MoM with the annual rate easing to 6.5%, from 7.0% in the prior month. Food prices, including another rise in dairy prices, will partly offset the decline in energy costs. The trend in ex-food/energy prices is once again likely to be more subdued in Canada than in the US, thanks largely to the differing treatment of shelter costs. With house prices continuing to fall and building costs no longer escalating, the homeowner replacement and other housing components of CPI will remain weak MoM. These components combined account for roughly 11% of the overall CPI basket. While mortgage interest costs will continue to escalate, this area is a smaller 3% of the basket and tends to be looked past by the Bank of Canada in its policy setting deliberations.”

BMO

“The sudden spill in the Canadian dollar complicates the Canadian inflation outlook – the loonie is now down more than 10% from a year ago, its sharpest yearly drop in almost seven years. This weakness will almost instantaneously translate into higher food and energy prices, and will also seep into a wide variety of other imported costs. Still, we expect CPI to ease to below 7% on lower gasoline prices, while we also look for some further retreat in core inflation.”

Wells Fargo

“The release of Canada's September CPI is expected to show a further deceleration of inflation, with the consensus forecast calling for headline inflation to slow to 6.6% YoY, from 7.0% in August. That would mark the third straight slowdown in inflation, a trend that has been driven in particular by falling gasoline prices, which could also decline further in September. It is not yet apparent whether broader price pressures are showing a significant slowdown, with food prices, in particular, continuing to quicken in August. In fact, the consensus forecast is for the trimmed mean CPI to remain steady at 5.2% YoY. While the slowing in headline inflation might be enough for the Bank of Canada to slow the pace of rate increases, we don't think it will be enough to dissuade the central bank from further tightening. As of now, we expect the BoC to raise its policy rate by 50 bps in late October, which would be less than the 75 bps increase it delivered in September.”

-

15:14

USD/CAD: Move below 1.30 will have to wait until 2024 – Scotiabank

Economists at Scotiabank update their USD/CAD forecast. The pair is now expected to trade above 1.30 throughout next year.

Q4 forecast lifted to 1.35

“We are marking the Q4 forecast for USD/CAD to 1.35 (from 1.30) and lifting the 2023 profile for the USD somewhat.”

“We now only anticipate the USD weakening below the 1.30 the year after next.”

“Relatively firm growth, a hawkish central bank and elevated commodity prices have done little to slow the USD/CAD rise this year and it is hard seeing any of those drivers delivering any additional support to the CAD right now.”

“The CAD retains a very tight, positive correlation with US equities at present and weak risk appetite seems likely to persist while inflationary pressures are elevated and geo-political tensions are high. This will keep the CAD tone soft.”

-

15:08

NZD/USD eases from over one-week high, struggles to find acceptance above 0.5700 mark

- NZD/USD rallies on hotter-than-expected Q3 inflation figures from New Zealand.

- The risk-on mood weighs on the USD and further benefits the risk-sensitive kiwi.

- Hawkish Fed expectations help limit the USD downside and seem to cap the pair.

The NZD/USD pair gains strong positive traction for the second successive day on Tuesday and climbs to a fresh one-and-half-week high during the early North American session. Spot prices, however, struggle to find acceptance above the 0.5700 mark and retreat a few pips from the daily peak.

The New Zealand dollar gets a strong boost in reaction to hotter domestic consumer inflation for the third quarter, which lifts bets for more rate hikes by the Reserve Bank of New Zealand. On the other hand, the ongoing rally in the equity markets undermines the safe-haven US dollar and offers additional support to the risk-sensitive kiwi.

The USD downtick, however, remains cushioned amid firming expectations that the Federal Reserve will stick to its aggressive policy tightening path to combat stubbornly high inflation. In fact, the current market pricing indicates a nearly 100% chance of another supersized 75 bps rate hike in November, which acts as a tailwind for the USD.

Furthermore, better-than-expected US Industrial Production data, which recorded a growth of 0.4% in September as compared to -0.1% previous, offers some support to the greenback. This turns out to be a key factor capping the upside for the NZD/USD pair and warrants some caution before positioning for any further near-term appreciating move.

Market participants now look forward to a slew of important Chinese macro data, due for release during the Asian session on Wednesday. This will play a key role in influencing the broader market risk sentiment. Apart from this, the USD price dynamics should provide a fresh impetus to the NZD/USD pair and help determine the near-term trajectory.

Technical levels to watch

-

15:00

United States NAHB Housing Market Index below forecasts (43) in October: Actual (38)

-

14:49

EUR/USD remains firm and advances to multi-day highs near 0.9880

- EUR/USD keeps the optimism well and sound near 0.9870.

- EMU, Germany Economic Sentiment surprised to the upside.

- US Industrial Production expanded 0.4% MoM in September.

The buying interest in the single currency gathers extra impulse and lifts EUR/USD to the area of multi-session highs past 0.9870 on Tuesday.

EUR/USD stronger on USD-selling, risk appetite

EUR/USD remains well bid in the upper-0.9800s as the selling pressure around the greenback seems to have picked extra pace on Tuesday.

In addition, the prevailing risk-on mood continues to support the pair’s upside bias despite German yields now give away initial gains and return to the negative territory, adding to Monday’s decline.

Extra support for the European currency also came after the Economic Sentiment measured by the ZEW institute in Germany and the Euroland unexpectedly came in above estimates in October, reversing at the same time the previous downtrend.

In the US, Industrial Production expanded at a monthly 0.4% in September and 5.3% from a year earlier. Next in the calendar comes the NAHB Index, TIC flows and the speech by Minneapolis Fed N.Kashkari (2023 voter, dove).

What to look for around EUR

EUR/USD remains in recovery-mode and now set sails to the 0.9900 neighbourhood amidst faltering price action surrounding the dollar.

In the meantime, price action around the European currency is expected to closely follow dollar dynamics, geopolitical concerns and the Fed-ECB divergence. Following latest results from key economic indicators, the latter is expected to extend further amidst the ongoing resilience of the US economy.

Furthermore, the increasing speculation of a potential recession in the region - which looks propped up by dwindling sentiment gauges as well as an incipient slowdown in some fundamentals – adds to the sour sentiment around the euro

Key events in the euro area this week: EMU, Germany ZEW Economic Sentiment (Tuesday) – EMU Final Inflation Rate, European Council Meeting (Thursday) - European Council Meeting, EMU Flash Consumer Confidence (Friday).

Eminent issues on the back boiler: Continuation of the ECB hiking cycle vs. increasing recession risks. Impact of the war in Ukraine and the persistent energy crunch on the region’s growth prospects and inflation outlook.

EUR/USD levels to watch

So far, the pair is gaining 0.23% at 0.9860 and expects the next resistance at 0.9875 (weekly high October 18) followed by 0.9999 (monthly high October 4) and finally 1.0050 (weekly high September 20). On the other hand, a breach of 0.9631 (monthly low October 13) would target 0.9535 (2022 low September 28) en route to 0.9411 (weekly low June 17 2002).

-

14:40

EUR/USD: Break above 0.9970 needed to extend the rally meaningfully – Scotiabank

EUR/USD holds a tight range above 0.98. The pair needs to break past 0.9970 in order to see further gains, economists at Scotiabank report.

Broader downtrend remains very much intact

“Yesterday’s EUR gains through the low 0.98s was a technical positive for the EUR, in our opinion, but the broader downtrend in this market remains very much intact; a break above 0.9970 – major trend resistance – is needed for the EUR rally to really extend meaningfully.”

“Intraday support is 0.9825/30. Resistance is 0.9880.”

-

14:38

GBP/USD Price Analysis: Recovers a few pips from daily low, lacks follow-through

- GBP/USD stages a modest intraday recovery, though lacks any follow-through buying.

- Subdued USD demand offers support; the UK political uncertainty caps the upside.

- A move beyond the 1.1400 handle is needed to support prospects for additional gains.

The GBP/USD pair rebounds a few pips from the daily low and climbs back above the 1.1300 mark during the early North American session. The modest recovery is sponsored by the emergence of some US dollar selling, though lacks bullish conviction amid the UK political uncertainty.

In fact, rebels within the ruling Tory Party are coming together to replace the newly-elected UK Prime Minister Liz Truss in the wake of the recent tax cut fiasco. Apart from this, reports that the Bank of England is set to further delay quantitative tightening to help stabilize bond markets act as a headwind for sterling and cap the GBP/USD pair.

Moreover, oscillators on the daily chart have been struggling to gain any traction, suggesting that any subsequent move up might confront resistance near the 1.1400-1.1410 area. This is followed by the overnight swing high, around the 1.1440 area, above which the GBP/USD pair could climb to the monthly peak, just ahead of the 1.1500 psychological mark.

The latter coincides with the 50-day SMA, which if cleared decisively should pave the way for an extension of the recent recovery from an all-time low touched in September. The GBP.USD pair might then accelerate the momentum towards the 1.1555-1.1560 intermediate resistance before eventually climbing to the 1.1600 round-figure mark.

On the flip side, weakness below the 1.1300 mark now seems to find some support near the daily low, around the 1.1255 region. Some follow-through selling would expose the 1.1200 level, below which the GBP/USD pair could slide to the next relevant support near the mid-1.1100s. The latter should now act as a pivotal point for spot prices.

Failure to defend the mentioned support levels will negate any near-term positive bias and shift the bias back in favour of bearish traders. The GBP/USD pair could then accelerate the fall towards testing the 1.1100 mark and the 1.1055-1.1050 support zone.

GBP/USD daily chart

-638016964889977496.png)

Key levels to watch

-

14:24

GBP/USD: At risk of dipping back to the mid-1.11s – Scotiabank

GBP/USD weakens as it fades an uptick above 1.1400. Economists at Scotiabank expect the pair to slump to the mid-1.11s on failure to hold support in the upper 1.12s.

Resistance aligns at the 1.1340/50 area

“Intraday support in the upper 1.12s is coming under pressure. Below here, cable risks dipping back to the mid-1.11s.”

“Resistance is 1.1340/50 and then 1.1450/60.”

“Political and economic risks for the GBP remain elevated.”

See – GBP/USD: 1.15 is not realistic without a further round of dollar selling – SocGen

-

14:15

United States Industrial Production (MoM) came in at 0.4%, above expectations (0.1%) in September

-

14:15

United States Capacity Utilization above forecasts (80%) in September: Actual (80.3%)

-

13:55

United States Redbook Index (YoY) declined to 8% in October 14 from previous 8.3%

-

13:49

USD/CAD surrenders modest intraday recovery gains, retreats to 1.3700 mark

- USD/CAD struggles to capitalize on its goodish rebound from over a one-week low.

- The risk-on impulse is weighing on the safe-haven buck and acting as a headwind.

- Bearish oil prices undermine the loonie and should help limit any meaningful slide.

The USD/CAD pair stages a goodish recovery from a one-and-half-week low touched earlier this Tuesday, though the momentum falters near the 1.3780 region. Spot prices retreat to the 1.3700 mark during the early North American session and remain at the mercy of the US dollar price dynamics.

The prevalent risk-on mood - as depicted by a strong follow-through rally in the equity markets - fails to assist the safe-haven buck to capitalize on its modest intraday gains. This, in turn, acts as a headwind for the USD/CAD pair, though a combination of factors warrants caution for bearish traders and before positioning for deeper losses.

The prospects for a more aggressive policy tightening by the Fed might continue to lend support to the greenback and warrant some caution before placing bearish bets around the USD/CAD pair. In fact, the current market pricing indicates a nearly 100% chance of the fourth successive supersized 75 bps Fed rate hike move in November.

Furthermore, worries that a deeper global economic downturn will dent fuel demand weigh on crude oil prices. This could undermine the commodity-linked loonie and further contribute to limiting the downside for the USD/CAD pair. Hence, it will be prudent to wait for strong follow-through selling before confirming that spot prices have topped out.

Market participants now look to Industrial Production data and Capacity Utilization Rate for some impetus. This, along with the US bond yields and the broader risk sentiment, will drive the USD demand. Traders will further take cues from oil price dynamics, though the focus will remain on the Canadian consumer inflation figures on Wednesday.

Technical levels to watch

-

13:39

Canada Canadian Portfolio Investment in Foreign Securities down to $-1.41B in August from previous $4.3B

-

13:30

Canada Foreign Portfolio Investment in Canadian Securities rose from previous $14.83B to $22.01B in August

-

13:30

Canada Canadian Portfolio Investment in Foreign Securities declined to $1.41B in August from previous $4.3B

-

13:23

EUR/USD Price Analysis: There is an interim hurdle at the 55-day SMA

- EUR/USD trades without conviction around the 0.9830 region.

- Next on the upside aligns the 55-day SMA at 0.9956.

EUR/USD gives away the initial advance to the 0.9870 region and deflates to the 0.9830 area on Tuesday

Further recovery in the pair looks probable in the very near term. Against that, the 55-day SMA at 0.9956 emerges as the next temporary hurdle prior to the more relevant October top at 0.9999 (October 4).

In the longer run, the pair’s bearish view should remain unaltered while below the 200-day SMA at 1.0561.

EUR/USD daily chart

-

13:15

Canada Housing Starts s.a (YoY) came in at 299.6K, above forecasts (263K) in September

-

13:05

Gold Price Forecast: XAU/USD could rebound benefiting from sluggish yields

Gold ended up snapping a two-week winning streak, losing over 2% on a weekly basis. Chinese growth data and action in the US bond market will be watched closely this week, FXStreet’s Eren Sengezer reports.

Gold to remain sensitive to fluctuations in US bond yields

“The Chinese economy is forecast to expand at an annualized rate of 3.4% in the third quarter following the dismal 0.2% growth recorded in the second quarter. In case the GDP data comes in below the market expectation, gold could have a hard time finding demand and vice versa.”

“Wednesday may be important as September Housing Starts will be featured in the US economic docket. A significant decline in this data could cause the dollar to lose strength, helping gold higher. September Existing Home Sales on Thursday could also have a similar impact on the greenback’s market valuation.”

“Since markets are already fully pricing in another 75 bps Fed rate hike in November, US yields might not have a lot of room on the upside. Hence, XAU/USD could see that as an opportunity to make a technical rebound/correction.”

-

12:41

USD Index Price Analysis: No changes to the consolidative theme

- DXY attempts a mild rebound after bottoming out near 111.80.

- Further range bound remains on the cards for the time being.

DXY bounces off multi-session lows in the 111.80/75 band on Tuesday.

So far, the index looks poised to keep navigating within a 112.00-114.00 range at least until the next FOMC event.

The prospects for extra gains in the dollar should remain unchanged as long as the index trades above the 8-month support line near 108.00.

In the longer run, DXY is expected to maintain its constructive stance while above the 200-day SMA at 103.43.

DXY daily chart

-

12:31

USD Index could see another 2% fall – SocGen

The US dollar has stayed lower. In the opinion of economists at Société Générale, the US Dollar Index (DXY) could see a fall of another 2%.

DXY unable to revisit last month’s high of 114.78

“The DXY has not managed to revisit last month’s high of 114.78 despite the new high for 2Y UST yields, and that’s certainly not positive.”

“There could be another 1.5-2% in this down-move if we follow the logic of early October, but cheaper levels could attract buyers before the November FOMC.”

-

12:09

EUR/JPY Price Analysis: Extra gains look likely near term

- EUR/JPY advances to new highs around the 147.00 mark.

- Next on the upside comes the December 2014 high at 149.78.

EUR/JPY accelerates the upside momentum and reaches fresh tops around the 147.00 hurdle, an area last seen back in December 2014.

Considering the current price action, further gains remain favoured. That said, the immediate target now emerges at the December 2014 peak at 149.78 (December 8).

In the short term the upside momentum is expected to persist while above the October lows around 141.00.

In the longer run, while above the key 200-day SMA at 136.60, the constructive outlook for the cross should remain unchanged.

EUR/JPY daily chart

-

12:04

AUD/USD flirts with daily low, just below 0.6300 mark amid resurgent USD demand

- AUD/USD surrenders its modest gains amid the emergence of fresh USD buying.

- Aggressive Fed rate hike bets, elevated US bond yields offer support to the buck.

- The risk-on mood limits the downside for the risk-sensitive aussie, at least for now.