Notícias do Mercado

-

23:53

NZD/USD seesaws above 0.6200 on RBNZ’s Orr, Fed’s preferred inflation, Powell in focus

- NZD/USD consolidates recent gains around weekly top, sidelined of late.

- RBNZ Governor Orr favored multiple rate hikes but appears cautious over economic growth.

- China’s stimulus, US data and Fedspeak favored buyers previously.

- US Core PCE Price Index, Fed Chair Jerome Powell’s Jackson Hole Speech are crucial for fresh impulse.

NZD/USD fades the upside momentum as it declines to 0.6215 after the Reserve Bank of New Zealand (RBNZ) Governor Adrian Orr sounds cautious during his speech at the Jackson Hole on early Friday morning in Asia. Also exerting downside pressure on the Kiwi pair are the latest geopolitical headlines, as well as a cautious mood ahead of Fed Chair Jerome Powell’s speech at the aforementioned symposium event.

RBNZ Governor Orr initially mentioned that we think there will be at least another two rate hikes. The policymaker also said, “Our core view is we won't see a technical recession.” However, his comments like, “Central banks may need to push towards zero growth,” seemed to have weighed on the NZD/USD prices.

Also read: RBNZ Orr: At least another couple of rate hikes to come

Additionally favoring the NZD/USD sellers are the geopolitical headlines surrounding China, the US and Iran. The US has suspended 26 Chinese carrier flights in response to China's action, per Reuters. On the other hand, a letter got viral quoting US President Joe Biden as saying, “The US struck Iran-backed forces in Syria in order to safeguard American civilians both at home and abroad.”

It should be noted that China’s heavy stimulus and mildly firmer US data, as well as Fedspeak, favored the NZD/USD buyers previously. China’s nearly one trillion yuan worth of stimulus and a holistic approach by the domestic institutions to safeguard the world’s second-largest economy renewed market optimism earlier.

That said, New Zealand’s ANZ Consumer Confidence for August rose to 85.4 versus 81.9 but failed to impress the pair buyers. As per the US data, the second estimate of the US Gross Domestic Product (GDP) Annualized improved to -0.6% in the second quarter (Q2) versus -0.9% flash estimations and -0.8% market forecasts. Further, US Initial Jobless Claims dropped to the lowest levels in seven weeks, to 243K for the week ended on August 19 versus 253K expected and a revised down prior of 245K.

Moving on, Kansas City Fed President Esther George said on Thursday, "For the near-term thinking about higher interest rates seems reasonable to me." The policymaker also mentioned that (it’s) too soon to say what to expect in September (as) more key data coming. Philadelphia Fed President Patrick Harker was on the same line while he noted, per Reuters, that he wants to see the next inflation reading before deciding on the September rate decision but added that a 50 basis points rate hike would still be a substantial move. Further, Philadelphia Fed President Patrick Harker noted on Thursday that he wants to see the next inflation reading before deciding on the September rate decision but added that a 50 basis points rate hike would still be a substantial move, per Reuters.

Against this backdrop, Wall Street marked the biggest daily jump in a week while the US 10-year Treasury yields dropped back to 3.03%, after rising to 3.10% the previous day.

Moving on, the US Core Personal Consumption Expenditure (PCE) Price Index, the Fed’s preferred inflation gauge, may entertain the markets. Forecasts suggest that the YoY print is to ease to 4.7% from 4.8% while the monthly figures may drop to 0.3% while 0.6% prior. However, more important will be Fed Chair Powell’s speech at the Jackson Hole.

Also read: Jackson Hole Symposium Preview: Will Powell power dollar bulls?

Technical analysis

NZD/USD pulls back from a 50-DMA level surrounding 0.6235 but the bears remain cautious until witnessing a clear break of the 0.6150 horizontal support.

-

23:35

RBNZ Orr: At least another couple of rate hikes to come

Adrian Orr, the governor of the Reserve Bank of New Zealand has stated that he thinks there will be at least another couple of rate hikes. This is being reported by Bloomberg TV covering Jackson Hole.

Key comments

- Retail Sales decline a sign higher rates are biting.

- Our core view is won't see a technical recession.

Federal Reserve chair Jerome Powell’s speech is going to be key, but the bears are moving into the kiwi currently. The onus is on the chairman to strike a tone that is hawkish enough to allay fears of an inflation blowout. However, it will need to be a well-balanced delivery so as not to stoke recession fears.

-

23:31

New Zealand ANZ – Roy Morgan Consumer Confidence rose from previous 81.9 to 85.4 in August

-

23:29

AUD/USD bulls attack 0.7000, US PCE Inflation, Powell’s showdown at Jackson Hole eyed

- AUD/USD grinds higher at weekly top, steady after rising the most in two weeks.

- Market sentiment improves on mostly firmer data, China stimulus and mixed Fedspeak.

- Yields dropped but Wall Street pleased buyers amid hopes of Powell’s not-so-hawkish remarks.

- US Core PCE Inflation numbers may entertain traders ahead of Fed Chair Powell’s speech at Jackson Hole.

AUD/USD floats in the air around 0.6980 after posting the biggest daily jump in a fortnight. The Aussie pair’s gains could be linked to the market’s optimism led by multiple factors surrounding China and the US. However, the latest geopolitical headlines and cautious mood ahead of Fed Chair Jerome Powell’s appearance at the Jackson Hole Symposium seems to have probed the bulls.

China’s one more stimulus and a holistic approach by the domestic institutions to safeguard the world’s second largest economy renewed market optimism earlier. On the same line could be the mildly positive US data and the Federal Reserve (Fed) policymakers’ speeches that sounded cautiously optimistic. It’s worth noting, however, that the US-China political tussles and US President Joe Biden’s response to Iran seems to have tamed the market’s optimism, as well as the AUD/USD prices, of late.

Talking about the US data, the second estimate of the US Gross Domestic Product (GDP) Annualized improved to -0.6% in the second quarter (Q2) versus -0.9% flash estimations and -0.8% market forecasts. Further, US Initial Jobless Claims dropped the lowest levels in seven weeks, to 243K for the week ended on August 19 versus 253K expected and a revised down prior of 245K.

Elsewhere, Kansas City Fed President Esther George said on Thursday, "For the near-term thinking about higher interest rates seems reasonable to me." The policymaker also mentioned that (it’s) too soon to say what to expect in September (as) more key data coming. Philadelphia Fed President Patrick Harker was on th same line while he noted, per Reuters, that he wants to see the next inflation reading before deciding on the September rate decision but added that a 50 basis points rate hike would still be a substantial move. Further, Philadelphia Fed President Patrick Harker noted on Thursday that he wants to see the next inflation reading before deciding on the September rate decision but added that a 50 basis points rate hike would still be a substantial move, per Reuters.

It’s worth noting that the US has suspended 26 Chinese carrier flights in response to China action, per Reuters. On the other hand, A letter got viral quoting US President Joe Biden as saying, “The US struck Iran-backed forces in Syria in order to safeguard American civilians both at home and abroad.”

Amid these plays, Wall Street marked the biggest daily jump in a week while the US 10-year Treasury yields dropped back to 3.03%, after rising to 3.10% the previous day.

Looking forward, the AUD/USD pair traders may witness a choppy session amid the market’s anxiety ahead of Fed Chair Powell’s speech. However, the US Core Personal Consumption Expenditure (PCE) Price Index, the Fed’s preferred inflation gauge, may entertain the markets. Forecasts suggests, the YoY print to ease to 4.7% from 4.8% while the monthly figures may drop to 0.3% while 0.6% prior.

Also read: Jackson Hole Symposium Preview: Will Powell power dollar bulls?

Technical analysis

An impending bear cross on the four-hour chart keeps AUD/USD sellers hopeful to witness the latest swing low around 0.6855. However, the early-month top near 0.7050 guards the pair’s immediate upside.

-

23:28

Gold Price Forecast: XAU/USD resumes upside journey after a correction to near $1,750, Fed’s Powell eyed

- Gold price is eyeing a break above $1,760.00 for more upside.

- The Fed has the luxury to scale down its hawkish tone on policy guidance.

- The US Core PCE data is expected to trim by 10 bps to 4.7% on an annual basis.

Gold price (XAU/USD) is advancing gradually higher after correcting to $1,752.30 on Thursday. The precious metal witnessed a vertical fall as the FX domain turned volatile ahead of Jackson Hole Economic Symposium. The yellow metal has rebounded and has advanced to near $1,758.00, however, more gains will be recorded if the asset oversteps the immediate hurdle of $1,760.00.

The gold prices are likely to dance to the tunes of commentary from Fed chair Jerome Powell at Jackson Hole on Friday. After a steep contraction in the US economic activities and a slump in overall demand indicated by weak US Durable Goods Orders, the street believes that the Fed should scale down the pace of hiking interest rates.

Fed policymakers have evidence of exhaustion in the price pressures and also the global supply chain risks have trimmed sharply. Therefore, the Fed has the luxury to scale down its hawkish tone slightly till the time the US economic activities could get to a restoration level.

Apart from that, investors will focus on the US Core Personal Consumption Expenditure (PCE) data, which is expected to decline to 4.7% from the prior print of 4.8%. This may weaken the US dollar index (DXY) further.

Gold technical analysis

On an hourly scale, gold prices are struggling to surpass 38.2% Fibonacci retracement (placed from the August 10 high at $1,807.93 to Monday’s low at $1,727.87) at $1,758.40. The gold prices are entirely focusing on sustaining above the 200-period Exponential Moving Average (EMA) at $1,757.18, which will bolster the odds of a bullish reversal.

Also, the 50-period EMA at $1,754.00 has remained a major supportive tool for the asset.

Meanwhile, the Relative Strength Index (RSI) (14) has shifted into the 40.00-60.00 range, which indicates that bulls are not strengthened enough for a while. However, a break above 60.00 will kick-start a fresh bullish impulsive wave.

Gold hourly chart

-

23:11

Sources: Decision to end ECB reinvestments take back seat to rate hikes

The European Central Bank (ECB) could soon start talks on ending reinvestments of cash maturing in its 3.3 trillion euro ($3.3 trillion) Asset Purchase Programme (APP), but a decision is not urgent and is unlikely to be taken next month, sources close to the discussion said to Reuters on Thursday.

Key quotes

The sources said that discussions on ending redemptions have yet to start and policymakers have not even had a seminar on the issue, which is normally a precursor to any decision.

‘There is just no urgency,’ one of the sources said. ‘I think interest rates are our main focus right now.’

A decision on rates coupled with reinvestments may be too much for markets and there's no point in taking that risk right now.

EUR/USD retreats

EUR/USD remains sidelines, recently retreating towards 0.9950, as traders await Fed Chair Powell’s key speech at the Jackson hole Symposium.

-

23:10

EUR/USD Price Analysis: Range-bound around 0.9900-0.9980, on traders in wait-and-see mode

- The shared currency extended its gains in the week, though closed below parity for the fourth consecutive day.

- EUR/USD rejection at parity sent the pair towards its daily lows before climbing towards 0.9970.

The EUR/USD begins the Asian session on the right foot, carrying on Thursday’s upbeat sentiment of the pair after posting gains of 0.11%. However, price action in the last week shows thin liquidity conditions, as traders remained on the sidelines until Fed’s Chief Jerome Powell hits the stand at the Jackson Hole symposium on Friday. At the time of writing, the EUR/USD is trading at 0.9976.

On Thursday, the EUR/USD price action witnessed the shared currency opening around the 0.9960s area. The major climbed towards its daily high at 1.0000 before erasing its gains, retreating towards current exchange rates.

EUR/USD Price Analysis: Technical outlook

The daily scale shows that the EUR/USD is in a consolidation phase. After hitting a year-to-date low at 0.9899, the EUR/USD reclaimed the 0.990 figure and hasn’t looked back, posing threats of reclaiming parity. The lack of strength keeps the major hovering around the 0.9960-90 area. It is worth noting that in reclaiming parity, its first resistance would be the 1.0100 figure, immediately followed by the 20-day EMA at 1.0137. On the flip side, a fall towards the YTD low at 0.9998 is on the cards, ahead of December 2002 lows at 0,9859, ahead of the October 2002 lows at 0.9685.

EUR/USD Key Technical Levels

-

22:58

USD/CAD sees a downside below 1.2900 as DXY sets for a bumpy ride, Jackson Hole buzz

- USD/CAD is likely to display more losses if the asset drops below 1.2900.

- Fed’s Powell is expected to adopt a less-hawkish tone while discussing over policy guidance.

- Oil prices have turned into a correction mode after printing a high near $95.00.

The USD/CAD pair is displaying a lackluster performance after slipping below the crucial support of 1.2940 in the late New York session. The asset is expected to extend its losses if it surrenders the round-level support of 1.2900. The pair is attracting a lot of offers as the US dollar index (DXY) is likely to display more weakness amid uncertainty over Jackson Hole Economic Symposium.

As the investing community is expecting that the Federal Reserve (Fed) will choose a less-hawkish tone while discussing the guidance over interest rates at Jackson Hole, the DXY is losing its strength. No doubt, the asset displayed a decent pullback move on Thursday after refreshing a two-day low at 108.00. But that short-lived pullback could turn into a fresh bearish impulsive wave if Fed chair Jerome Powell’s commentary matches street expectations.

The consequences of using a higher pace for hiking interest rates are visible to the market participants. US private sector has contracted, especially the service sector, which carries the potential of accelerating fears of a slowdown in tech companies globally. Also, a decline in US Durable Goods Orders indicates that the overall demand is going through a bumpy ride.

Meanwhile, oil prices have witnessed a mild correction after a juggernaut rally over the past few trading sessions. The black gold has surrendered more than 3% after printing a high to near $95.00 as the announcement of production cuts by OPEC has started fading away and investors are realizing that dismal global Purchasing Managers Index (PMI) numbers are the outcome of a slowdown in overall demand.

Investors should be aware of the fact that Canada is a leading exporter of oil to the US. And, higher oil prices will bring higher revenues to Canada and will strengthen its fiscal balance sheet.

-

22:19

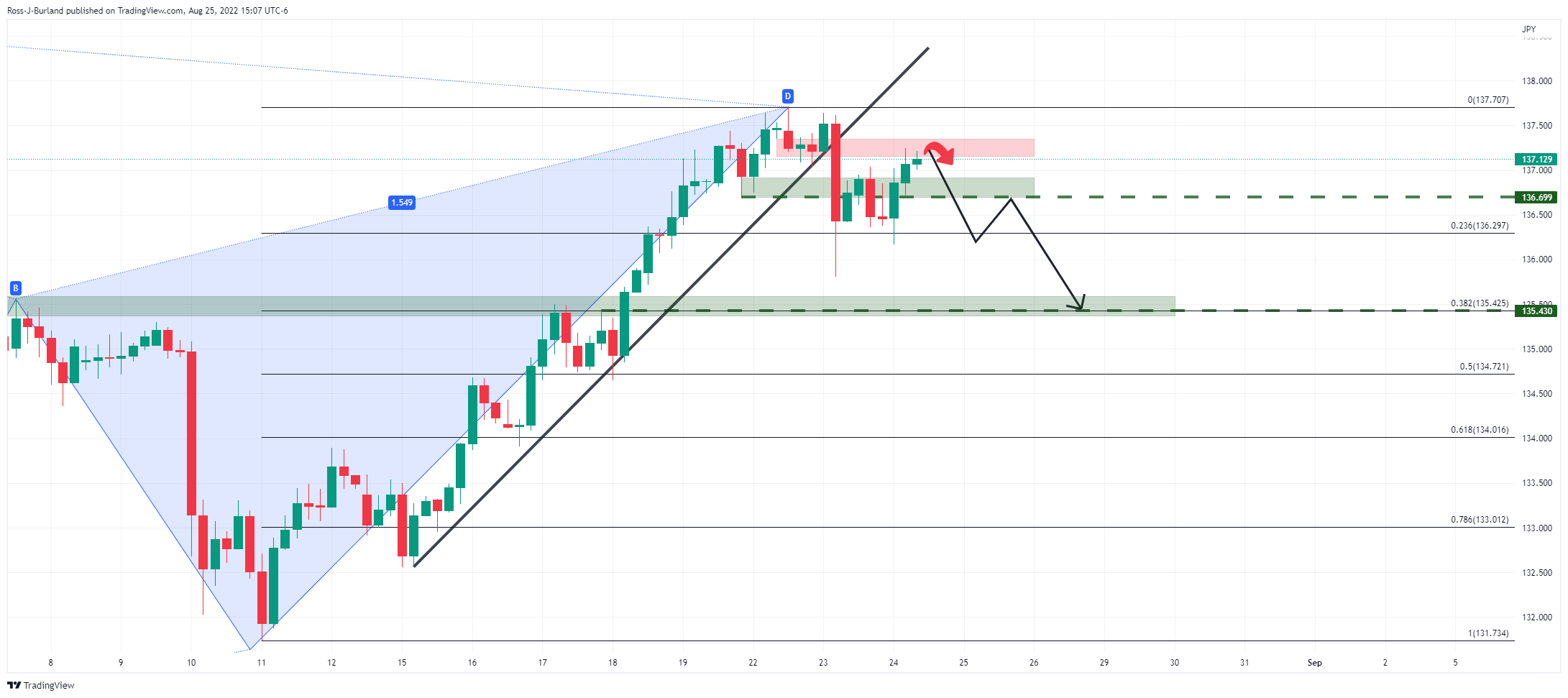

USD/JPY Price Analysis: Bears back on the prowl, eyes on 135.50 still

- USD/JPY weekly W-formation is a reversion pattern (the lower time frame H4 Gartley), which leaves a bearish tendency on the charts.

- The neckline of the formation opens risk to a move below 38.2% and towards the 50% mean reversion point near 134.70.

As per the prior analysis, USD/JPY Price Analysis: Bears are stepping on the gas and a move to 135.50 could be on the cards, the bears stepped in and remain in charge while below critical resistance as per the following analysis:

USD/JPY H4 chart

The Gartley is a reversion pattern that predicts that the price will reverse from point D. The price, in this instance, is finding resistance and could be above to make a significant move to the downside as follows:

The price has met the resistance of an M-formation and is now decelerating there with sights on a move to test the W-formation's neckline near 136.70. A break of that will open prospects of a move to test the recent lows of the last bullish leg around 136.20 that is guarding the 38.2% Fibonacci level of the weekly bullish impulse near 135.50:

USD/JPY weekly chart

The weekly W-formation is a reversion pattern (the lower time frame H4 Gartley). The neckline of the formation opens risk to a move below 38.2% and towards the 50% mean reversion point near 134.70. This makes 135 a compelling round-figure target for the week ahead.

-

22:02

NZD/USD Price Analysis: Bottoms around 0.6150 and reclaims 0.6200, refreshing weekly highs

- NZD/USD appears to have bottomed after seesawing around 0.6150 for three days.

- Despite trading in the green, the NZD/USD daily chart shows oscillators and moving averages tilted to the downside.

- The NZD/USD is neutral-upwards and might retest the 0.6300 figure if it conquers 0.6260; otherwise, a fall towards 0.6100 is on the cards.

The NZD/USD rose to fresh weekly highs around 0.6251 on Thursday, spurred by broad US dollar weakness courtesy of a fall in US T-bond yields, ahead of Powell’s keynote on Friday at the Jackson Hole Symposium. At the time of writing, the NZD/USD is trading at 0.6223, above its opening price by 0.63%.

Wall Street finished with solid gains, reflecting an upbeat mood. Nevertheless, trading liquidity conditions remained thin as investors prepared for other Fed policymakers’ remarks.

NZD/USD Price Analysis: Technical outlook

The NZD/USD edged higher during the day, briefly piercing the 50-day EMA at 0.6248 but retraced towards current exchange rates. Even though the NZD/USD trades positive in the week, moving averages above the price action, with a downward slope, suggest the opposite, further reinforced by the RSI in negative territory.

Short term, the NZD/USD 4-hour scale illustrates the major bottoming around the 0.6160 area, though as of writing, the major is trading below August’s 23 daily high at 0.6264. A breach of the latter is needed so the pair can retest the figure at 0.6300. Once cleared, the next resistance area will be the August 16 swing high at 0.6383. On the other side, the NZD/USD first support would be the 20-day EMA at 0.6197, below the 0.6200 figure. Break below will expose the August 22 daily low at 0.6156, followed by the psychological 0.6100.

NZD/USD Key Technical Levels

-

21:02

Forex Today: Financial markets about to wake up

What you need to take care of on Friday, August 26:

The greenback ended Thursday mixed across the FX board, although there were no significant changes among major pairs. Investors are mildly optimistic as macroeconomic figures were upbeat but cautious ahead of central banks' governors, set to speak within the Jackson Hole Economic Symposium.

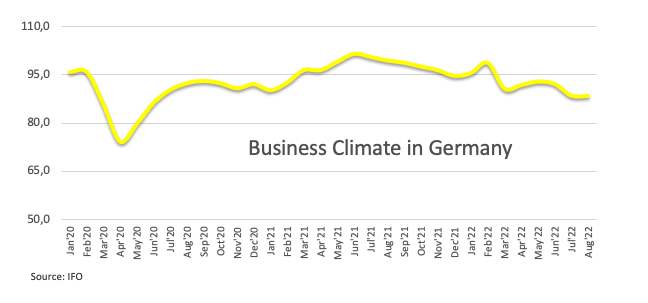

Germany reported that the Q2 Gross Domestic Product rose by 1.7% YoY, better than the 1.4% previously estimated. In the quarter, it was up by 0.1%, revised from 0% previously. Also, the August IFO survey showed the Business Climate reached 88.5, better than the 86.8 expected. Expectations and the assessment of the current situation were better than anticipated.

The European Central Bank released the minutes of its latest meeting, which showed that a "very large number" of Governing Council members agreed that it was appropriate to raise key rates by 50 basis points while also noting that members agreed that it was "appropriate to take further steps on the path of monetary policy normalisation."

The US published the second estimate of the Q2 GDP, which was upwardly revised from -0.9% to -0.6%. Additionally, Initial Jobless Claims for the week ended August 19 declined to 243K, beating the market expectations.

The EUR/USD pair briefly traded above parity but could not retain gains and stabilised around 0.9970, unchanged for a third consecutive day. GBP/USD holds above the 1.1800 figure. The USD/CAD pair is at around 1.2920, while the Australian dollar was the best performer vs the greenback, now trading at around 0.6980.

Spot gold is up for a third consecutive day and currently trades at around $1,757 a troy ounce. Crude oil prices, on the other hand, gave back some ground, and WTI stands at $93.10 a barrel.

Bitcoin Price Prediction: How Biden's debt relief program could trigger the next BTC rally

Like this article? Help us with some feedback by answering this survey:

Rate this content -

20:30

EUR/JPY holds in familiar territories as investors get set for the Jackson Hole

- EUR/JPY consolidates into the Jackson Hole at a key point in financial markets.

- The focus turns to the BoJ, ECB and Fed as central banks throw the kitchen sink at inflation risks.

EUR/JPY is down 0.38% at the time of writing and has fallen from a high of 136.98 to a low of 136.01 on the day so far as the market consolidated in the main ahead of keynote speeches at the Jackson Hole that started today. The dollar index and the euro both slipped on Thursday in choppy trading as investors waited on a speech by Federal Reserve Chairman Jerome Powell on Friday for further clues about the ongoing pace of the US central bank’s rate hikes.

Meanwhile, despite the economic difficulties, the inflationary implications of higher energy prices in the eurozone are keeping the euro bulls in check despite prospects of higher rates. Another rate hike is widely expected in September but is only likely to provide fleeting support for the EUR given the stagflation fears.

This makes for a very compelling Jackson Hole this year, considering Much of the world is facing many of the same problems as the early 1980s with strong price growth and the fears of a repeat of that era's wage-price spiral phenomenon and double-digit interest rates. The outlook is probably much worse for the energy-importing Europe which may give the yen the edge as the US dollar continues to pick up the safe haven bid. Russia's invasion of Ukraine has led to sky-rocketing energy prices that look set to keep on accelerating. This has led to the ECB last month needing to raise interest rates for the first time in 11 years.

As for the Bank of Japan, considering the current increase in headline inflation readings, the central bank is expected to exit its unsustainable policy, Yield Curve Control, or YCC. However, due to the rise of commodity prices and Japanese imports, an exit may only be temporary as wages struggle to keep up with the pace, leading to a deflationary environment. With Japanese interest rates still at minus 0.1 per cent, a divergence in global yields earlier this year sent the yen to a 24-year low against the US dollar and there could be more to go as the BoJ continues its effort to hit and sustain its 2% inflation target.

-

20:28

Gold Price Forecast: XAU/USD climbs above $1750 as traders expect a hawkish Powell speech

- Gold price advances almost 0.30% on Thursday, courtesy of an upbeat sentiment and overall buck’s weakness.

- Investors mulled on mixed US economic data, released ahead of Powell’s speech.

- Fed officials expect a 50 or 75 bps rate hike at the next meeting; awaiting September’s data.

- Gold Price Forecast (XAU/USD): Neutral above $1800; otherwise, a re-test of the YTD lows below $1700 is on the cards.

Gold price trades in the green, spurred by overall US dollar weakness across the board, and falling US Treasury bond yields, amidst an upbeat trading session. XAU/USD opened near the day’s lows, around $1750, and rallied towards the high of the day at $1763.71 before retracing to current price levels. At the time of writing, XAU/USD is trading at $1755.93, above its opening price.

Global equities portray an upbeat sentiment. Incoming economic data from the US revealed that growth in the country improved but is stills in contractionary territory. The Gross Domestic Product (GDP) for the second quarter dropped 0.6%, less than estimates of minus 0.8%. That said, if the final reading comes negative, it would confirm that the US is in a technical recession, though today’s figures are still susceptible to revision.

In the meantime, the US Department of Labor revealed unemployment claims for the week ending on August 20. Initial Jobless Claims rose by 243K, less than the estimated 253K. This week’s report and the previous one further confirmed the robust labor market, as mentioned by some Fed officials, which had emphasized the need for further rate hikes amidst a high inflation environment.

The US Dollar Index, a gauge of the buck’s value vs. a six currencies basket, creeps lower by 0.12%, down at 108.476, undermined by the US 10-year Treasury bond yield dip to 3.028%, losing eight bps, ahead of Fed’s Chair Powell Jackson Hole speech.

Meanwhile, some Fed officials crossing wires have opened the door for additional rate hikes, led by Kansas City’s Fed Esther George, who said that she foresees rates above 4%.

Earlier, Atlanta’s Fed President Raphael Bostic commented that he’s undecided about going 50 or 75 but added that a Fed pivot is misguided. Contrary to Esther George’s opinion, Patrick Harker of the Philadelphia Fed noted that he expects to raise and hold rates at 3.4% while supporting a 50 bps increase for September.

Later, the St, Louis Fed President James Bullard reiterated that he expects the Federal funds rate (FFR) around 3.75% to 4% for 2022, adding that risks may have to be higher for longer.

What to watch

The US economic calendar will release the Fed’s favorite measure of inflation, July’s PCE, headline, and core figures before Wall Street opens. Later, the US Federal Reserve Chair Jerome Powell will hit the stand.

Gold Price Forecast (XAU/USD): Technical outlook

XAU/USD remains neutral-to-downward biased, confirmed by several factors. The daily moving averages (DMAs) above the spot price, and the Relative Strength Index (RSI) at 47.08, in the negative territory, are just two signs confirming the previously-mentioned. Also, gold buyers need to reclaim the $1800 figure to test the 100 and 200-day EMAs, around $1822-$1838. Failure to achieve the aforementioned will pave the way for further downside, opening the door for a fall to August’s 22 daily low at $1727.90, followed by $1700.

-

20:02

US: Upward revisions to Q2 growth weaken the current recession argument – Wells Fargo

The second estimate of Q2 GDP showed the US economy contracted at a slower-than-expected rate of 0.6%. Upward revisions to underlying demand and a first read from the income side weakens the argument that the economy is currently in recession, point out analysts at Wells Fargo.

Key Quotes:

“The U.S. economy contracted at a 0.6% annualized rate in the second quarter according to the second estimate of GDP, which is slightly better than previously thought. While Q2 still marks the second-consecutive decline in real GDP growth, the upward revisions weaken the current recession argument.”

“Despite some upward revisions, second quarter weakness still reflects a genuine slowing in economic activity. Real final sales to domestic purchasers, an indication of underlying demand, still came in negative, contracting at a 0.2% annualized pace during the quarter.”

“But when measured from the income side, real GDI grew at an annualized rate of 1.4% in the second quarter, suggesting an expansion in economic activity. In theory, growth in GDP and GDI should be identical, but they rarely are due to data errors and omissions. Growth on the income side of the national income and product accounts (NIPA) is more in line with the "core" parts of the spending side, and further adds to the argument that the economy is slowing but not yet broadly contracting.”

-

19:25

AUD/USD bulls holding on as US dollar remains soft ahead of Powell speeh

- AUD/USD bulls are hanging in there following a very strong move to the upside.

- China stimulus boosted risk sentiment and the proxy AUD.

- The Jackson Hole is now the main focus that started today.

AUD/USD is 1% higher on the day as the US dollar continues to find sellers ahead of a keynote speech from the Federal Reserve chairman, Jerome Powell. At the time of writing, AUD/USD is trading at 0.6976 and has been moving between a low of 0.6902 and a high of 0.6991.

The Australian and New Zealand dollars were trying to pick up on Thursday as a buoyant greenback paused for breath amid caution ahead of the US Federal Reserve's Jackson Hole conference this week. The antipodeans were supported further as China's stimulus announcement in the Tokyo session boosted risk sentiment.

China announced a massive CNY1 trln stimulus package to help shore up the economy. The State Council outlined a 19-point package that is mostly focused on infrastructure spending, including another CNY300 bln that state banks can invest in infrastructure projects which comes on top of another CNY300 bln that was already announced in June. This accompanied the weakest fix in the yuan vs the US dollar since August 2020. In turn, the Aussie rallied to a key target area on the hourly chart, 0.6945, and then burst through it to print highs in London of 0.6991.

However, while the measures will help at the margin, ''we can’t help but feel that policymakers there are pushing on a string,'' analysts at Brown Brothers Harriman argued. ''Infrastructure spending is the tried and true method that has helped China muddle through in the past but we suspect it won’t be enough to truly offset the impact of Covid Zero lockdowns, persistent energy shortages from drought, and strains on the financial system from the collapsing property market.''

Meanwhile, it will soon come back to domestic data and next week will see the release of retail trade, building approvals, private sector credit and some of the building blocks for the Q2 22 national accounts. For now, however, the focus is on the Jackson Hole Economic Symposium has begun today.

All eyes on the US economy

In the build-up to the event, there has been a plethora of US economic data that has been less inflationary, including today's first revision for the second quarter Gross Domestic Product which fell by 0.6% annualized and not by the 0.9% previously thought during the second quarter, following a 1.6% retreat in the first quarter. The market expectations in a Bloomberg survey were for a decline of 0.7%.

The first round of data that moved the needle in financial markets came in a report on Tuesday that showed US private sector activity contracted for a second-straight month in August. Then, data on Wednesday showed that new orders for US-made capital goods increased at a slower pace in July from the prior month, suggesting that business spending on equipment could struggle to rebound after contracting in the second quarter. Due to the less inflationary data, Fed funds futures traders were pricing in a 59% chance that the Fed will hike rates by another 75 basis points at its September meeting, and a 41% probability of a 50 basis points increase.

Fed Chair Powell gives his keynote speech tomorrow at 10 AM ET. In the past, the Fed has used this symposium to announce or hint at policy shifts. However, analysts at Brown Brothers Harriman argue that this year is very different and they do not think the Fed will paint itself into a corner ahead of the September 20-21 FOMC meeting.

''Rather, we expect Powell to try and manage market expectations by maintaining the Fed’s hawkish tone. Between now and the September 20-21 FOMC meeting, we will get all the major August data and some of the early September surveys such as the preliminary S&P Global PMI readings and regional Fed surveys. The Fed will also have a better idea then of how the economy is doing in Q3.''

-

19:10

Fed's Bullard: Rates aren't high enough now

Federal Reserve's president and CEO of the Federal Reserve Bank of St. Louis James Bullard: in a CNBC interview has said rates aren't high enough now.

Key notes

- 3.75% - 4% is my target for this year.

- Says he likes the idea of front loading; it ‘shows you are serious about inflation fight’.

- Rates aren't high enough now.

- Labour market is strong right now.

- Front loading shows you are serious about the inflation fight.

- Rates aren't high enough now.

- Need to get the policy rate to where it pushes downward pressure on inflation.

- After rates get above 3.75%-4%, not quite sure what's next.

- My baseline is that inflation will be more persistent than many expect.

- Inflation will be higher for longer.

- That risk is underpriced in the market.

- Markets are showing outstanding confidence in the Fed, hope they are right.

- The risk is that we may have to be higher for longer.

- Asked about the stock market, says he tries to stay away from equity pricing.

- I don't want to take too much signal from the stock market.

- Bond markets give a little better pricing of the risk we will have to do more.

- You should be able to hit the inflation target even if there are factors out of Fed's control.

- Recessions are not that predictable.

- We are of course taking recession risk, but we don't know one way or the other.

- GDP was positive for the 2Q, consistent with what businesses say about hard-to-hire

- After the pandemic, we set out a path on asset-buying that was 'overboard'.

- Now we have to switch back; the Fed has to get inflation back to 2%.

Meanwhile, Fed funds futures traders are pricing in a 59% chance that the Fed will hike rates by another 75 basis points at its September meeting, and a 41% probability of a 50 basis points increase. The US dollar slipped on Thursday in choppy trading as investors waited on a speech by Federal Reserve Chairman Jerome Powell on Friday for further clues about the ongoing pace of the US central bank’s rate hikes.

-

18:21

United States 7-Year Note Auction rose from previous 2.73% to 3.13%

-

18:16

USD/CHF Price Analysis: Subdued around 0.9635, despite forming a bearish-harami candle pattern

- USD/CHF exchanges hands under its opening price, despite recovering from daily lows.

- The USD/CHF is range-bound through a break of the top of the range will pave the way above the 0.9700 figure; otherwise, a fall towards 0.9550 is on the cards.

The USD/CHF drops into negative territory after refreshing five-week highs around 0.9650s, courtesy of broad US dollar weakness across the board, amidst an upbeat market mood. After hitting a daily high at 0.9626, the USD/CHF dived below the 50-day EMA at 0.9612, the day’s lows, before jumping to current price levels. At the time of writing, the USD/CHF trades at 0.9645, below its opening price.

USD/CHF Price Analysis: Technical outlook

A bearish-harami candle chart pattern emerged in the USD/CHF daily chart. Even though the pattern has bearish implications, oscillators and moving averages (MAs) portray the opposite. Albeit the RSI has a downslope, it remains in positive territory. Meanwhile, all the daily Exponential Moving Averages are below the USD/CHF spot price, suggesting that buyers are in charge.

In the near term, the USD/CHF one-hour chart depicts the pair as range-bound within the 0.9603-0.9692 area for the last three days. Further confirmation of the previously mentioned is that the 20, 50, and 100 exponential moving averages (EMAs), are located within the 0.9632-46 area. Also, the Relative Strength Index (RSI) at 52 is almost flat.

Therefore, if the USD/CHF breaks above the range, the first resistance would be the 0.9700 figure. Once cleared, the next resistance would be the R2 daily pivot at 0.9733, followed by 0.9800. On the flip side, the USD/CHF first support would be the 0.9600 mark, followed by the confluence of the 200-EMA and the S2 pivot at 0.9570, and then the August 19 daily low at 0.9553.

USD/CHF Key Technical

-

17:34

GBP/USD subdued around the figure at 1.1800 posts mixed US data, awaiting Powell’s speech

- GBP/USD fluctuates during the day, with traders waiting for Powell to take the stand on the sidelines.

- US growth in the second quarter improved but remains below the 0% threshold; a US recession looms.

- Money market futures expect the BoE to hike rates 250 bps by May of 2023.

The GBP/USD slightly advanced in the North American session, staying a comeback after piercing below the 1.1800 figure for the fourth time in the week, but a shift in sentiment augmented the appetite for the Sterling. Factors like China’s stimulus to the housing and construction markets underpinned worldwide stocks.

The GBP/USD reached a daily low of around 1.1783 during the Asian session before climbing towards the day’s high at 1.1864. Nevertheless, it retreated towards current exchange rates. At the time of writing, the GBP/USD trades at 1.1817, registering marginal gains of 0.18%.

Before Wall Street opened, the US Department of Commerce reported that the US Gross Domestic Product for Q2 improved, by -0.6%, higher than estimates of -0.8%, and above the advanced reading. At the same time, the Bureau of Labor Statistics (BLS) revealed that Initial Jobless Claims for the week ending on August 20 were lower than foreseen, at 243K from 253K.

Elsewhere, Fed policymakers led by Kansas City Fed Esther George said that the US central bank would hold rates above 4% and wanted to see a full quarter of consistent inflation data to know where things are going.

Earlier, Atlanta’s Fed Raphael Bostic said he’s undecided to go 50 or 75 bps and emphasized that expectations of a Fed pivot are “misguided.” Echoing his comments was Philadelphia’s Fed Patrick Harker, who said that he likes to see the Federal funds rate (FFR) at 3.4%, and then perhaps stay for a while there. He supports a 50 bps increase but wants to see the next inflation report.

Meanwhile, a gloomy economic outlook in the UK, with energy bills pushing higher, Bank of England (BoE) recession projections for at least 18 months, and a slowing economy, would make BoE’s job harder, with inflation levels at double digits. Nevertheless, as shown by STIRs, money market futures expect 250 bps of further hikes by May of 2023, meaning investors expect the Bank’s Rate to hit 4.25%.

What to watch

The US economic calendar will release the Fed’s favorite measure of inflation, July’s PCE, headline, and core figures before Wall Street opens. Later, the US Federal Reserve Chair Jerome Powell will hit the stand.

GBP/USD Price Analysis: Technical outlook

The GBP/USD trades below the midline of a parallel descending channel, pierced earlier in the day but retraced, trading below August’s 24 daily close. Even though the major trades above its opening price, a daily close below 1.1795, would pave the way for a re-test of the YTD lows at around 1.1716. Otherwise, a break above 1.1878, the high of the week, will pave the way towards 1.1900.

-

17:05

NZD/USD unable to break 0.6250, holds in a consolidation range

- US dollar gains momentum after US data and as Wall Street trims gains.

- Market participants await Fed Chair Powell’s speech.

- NZD/USD moving between 0.6250 and 0.6150.

The NZD/USD peaked at 0.6250, the highest level since August 19, then pulled back toward 0.6200. The decline from the multi-day high took place amid a recovery of the US dollar.

The greenback started to gain momentum following the release of US economic data. The second reading of Q2 GDP showed the economy contracted at a 0.6% annualized rate, better than the previous estimate of -0.9%. A different report showed Jobless Claims (initial and continuing) dropped to the lowest level in weeks.

The Jackson Hole symposium started on Thursday. The key event will be Jerome Powell’s speech on Friday. His words are likely to have a significant impact across financial markets. Market participants will look for clues about the trajectory of the Fed’s monetary policy. Philadelphia Fed President Patrick Harker said on Thursday that he wants to see the next inflation reading before deciding what to do on the September FOMC meeting.

Earlier on Thursday, a report showed retail sales in New Zealand declined 2.3% in the second quarter. “It was the second straight quarter of weaker sales and raises the odds that the overall economy will also contract. Q2 GDP data will be reported on September 15. There is no consensus yet but the contraction will likely be worse than the -0.2% q/q posted in Q1”, mentioned analysts at Brown Brothers Harriman.

Short-term outlook

The NZD/USD continues to trade near the weekly low and the crucial support at 0.6150. If broken, a bearish acceleration seems likely. On the upside, the recovery found resistance at 0.6250 containing the 200-hour Simple Moving Average.

Ahead of the Asian session, a slide below 0.6200 would expose the daily low at 0.6175 and then the recent low. While a break above 0.6250 should clear the way for an extension of the recovery.

Technical indicators in the daily chart as still biased to the downside, despite the consolidation of the last four days. Under 0.6150, a test of the year-to-date low at 0.6057 seems likely.

Technical levels

-

16:39

USD/CAD slides below 1.2950 on soft US dollar ahead of Powell’s speech

- USD/CAD dropped 0.15% on Thursday as market players prepare for further hawkish rhetoric by the Fed.

- US GDP Q2 figure, albeit better than expected, is still in recessionary territory.

- USD/CAD Price Analysis: Traders reclaiming 1.3000 to open the door for YTD high tests; otherwise, a fall towards 1.2800 is feasible.

The USD/CAD slides towards new weekly lows in the North American session amidst a positive market mood, spurred by China’s 1 trillion CNY stimulus, aimed to fix the housing and construction crisis. Meanwhile, traders prepare for Fed Chair Jerome Powell’s Jackson Hole speech on Friday.

The USD/CAD hit a daily high of around 1.2975, before diving, towards its daily low, around 1.2895, while crude oil prices edged higher. However, it bounced off the lows, above the 1.2900 psychological figure. At the time of writing, the USD/CAD is trading at 1.2947, down 0.15%.

The USD/CAD slid on broad US dollar weakness. The US Dollar Index, a gauge of the buck’s value vs. a basket of peers, loses 0.18%, down at 108.405, courtesy of market participants moving to the sidelines or profit taking before Powell’s speech. In the meantime, US Treasury bond yields receded from weekly highs, particularly the 10-year T-note rate down one bps, at 3.095%.

Growth in the US, as measured by the Gross Domestic Product (GDP) for the second quarter of 2022, on its second reading, beat expectations. Still, flashes recessionary signs at -0.6%, higher than 0.8% estimates.

At the same time, Initial Jobless Claims for the week ending on August 20 came lower than estimates, at 243K, vs. 253K expected by market analysts. The fall in unemployment claims continued showing a robust labor market, further fueling expectations of a 75 bps Federal Reserve rate hike.

In the meantime, Fed officials led by Kansas City Fed Esther George said that the US central bank would hold rates above 4%, and want to see a full quarter of consistent inflation data to know where things are going.

Earlier, Atlanta’s Fed Raphael Bostic said he’s undecided to go 50 or 75 bps and emphasized that expectations of a Fed pivot are “misguided.” Echoing his comments was Philadelphia’s Fed Patrick Harker, who said that he likes to see the Federal funds rate (FFR) at 3.4%, and then perhaps stay for a while there. He supports a 50 bps increase but wants to see the next inflation report.

What to watch

With Jerome Powell’s speech at Jackson Hole, an absent Canadian docket will leave traders leaning on US dollar dynamics. Still, earlier, US inflation figures, namely the PCE Price Index and core PCE, would shed some light, as it’s the Fed’s favorite gauge of inflation.

USD/CAD Price Analysis: Technical outlook

The USD/CAD exchanges hands nearby the 50-day EMA, at around 1.2912, even though it reached a daily low of 1.2864. From a daily chart perspective, the USD/CAD remains tilted upwards, despite the Relative Strength Index (RSI) aiming down towards the 50-midline, signaling selling pressure gathering momentum. However, if the RSI breaks the midline, expect some downward pressure, putting into play the 50 and 20-day EMAs, each at 1.2912 and 1.2883, respectively. On the other side, if the USD/CAD breaks above 1.3000, a retest of the YTD highs is on the cards.

-

16:35

United States 4-Week Bill Auction rose from previous 2.15% to 2.31%

-

16:14

EUR/USD sideways, supported by 0.9950 ahead of Fed Chair Powell’s speech

- US dollar moving sideways on Thursday, DXY post marginal losses.

- Market participants await Powell’s speech on Friday.

- EUR/USD rejected from above 1.0000, supported by 0.9950.

The EUR/USD is moving without a clear direction on Thursday ahead of a key speech from Jerome Powell at the Jackson Hole symposium. The pair failed to hold above parity and then pulled back, finding support above 0.9950.

The US dollar gained momentum following the release of US economic data. The Q2 GDP growth rate was revised higher from -0.9% to -0.6% and jobless claims declined more than expected. US yields peaked after the reports and then retreated.

Despite the numbers, market participants await Powell’s speech to be delivered on Friday. His words could bring clary regarding the path of the Fed’s monetary policy. “We expect Powell to try and manage market expectations by maintaining the Fed’s hawkish tone. Between now and the September 20-21 FOMC meeting, we will get all the major August data and some of the early September surveys such as the preliminary S&P Global PMI readings and regional Fed surveys. The Fed will also have a better idea then of how the economy is doing in Q3”, explained analysts at Brown Brothers Harriman.

Regarding the European Central Bank, the minutes from the latest meeting showed a “large number” of members agreed it was appropriate to raise interest rates by 50 basis points. “The ECB is now fully in a data-dependent mode with chains from past guidance severed. Most Governing Council members are preoccupied with inflation risks, and large rate hikes are set to continue”, said Jan von Gerich, Chief Analyst at Nordea.

Unable to recover 1.0000

The EUR/USD shows no clear signs in the very short term. The euro continues to show weakness by being unable to hold above 1.0000. A recovery surpassing 1.0030 would add support to the euro. On the flip side, the immediate support stands at 0.9950. A slide below would expose the next barrier around 0.9900.

The main trend in EUR/USD remains bearish and the euro still looks vulnerable. It is on its way to the second weekly slide in a row, and the lowest close since November 2002.

Technical levels

-

16:00

United States Kansas Fed Manufacturing Activity below forecasts (3) in August: Actual (-9)

-

15:30

United States EIA Natural Gas Storage Change came in at 60B, above forecasts (58B) in August 19

-

15:09

Fed's Harker: 50 bps hike in September would still be a substantial move

Philadelphia Fed President Patrick Harker noted on Thursday that he wants to see the next inflation reading before deciding on the September rate decision but added that a 50 basis points rate hike would still be a substantial move, per Reuters.

Additional takeaways

"We need to get to a restrictive stance, which we'll be by year-end."

"I'd like to see us get to above 3.4% and then perhaps sit for a while."

"But if data keeps indicating we need to raise more, we should do that."

"We need to get inflation under control no matter what."

"I don't think we can call the current environment a recession."

"Supply chain constraints are starting to heal."

"Started to hear very early last fall that inflation was not transitory."

"I'm not in the camp of taking rates way up and then right back down."

"I don't see a risk of sustained recession."

"Medium to long-term neural rate is somewhere around 2.5%."

Market reaction

The US Dollar Index edged slightly lower on these remarks and was last seen losing 0.07% on a daily basis.

-

15:02

AUD/USD Price Analysis: Intraday positive move falters near 50% Fibo., ahead of 0.7000 mark

- AUD/USD meets with some supply at higher levels and trims a part of its intraday gains.

- A goodish USD rebound from the weekly low exerts downward pressure on the major.

- Any subsequent slide is likely to find decent support near the 0.6935-0.6925 confluence.

The AUD/USD pair attracts some selling in the vicinity of the 0.7000 psychological mark and trims a part of its early gains to over a one-week high touched earlier this Thursday.

The US dollar rebounds swiftly from the weekly low following the release of better-than-expected US macro data, which reaffirms hawkish Fed expectations. Apart from this, an intraday turnaround in the equity markets further benefits the greenback's safe-haven status and acts as a headwind for the risk-sensitive aussie.

From a technical perspective, the AUD/USD pair struggles to find acceptance above the 100-period SMA on the 4-hour chart. The intraday positive move stalls near the 50% Fibonacci retracement level of the recent decline witnessed over the past two weeks or so. The latter should now act as a pivotal point for short-term traders.

Meanwhile, neutral oscillators on the daily chart warrant caution before placing aggressive directional bets. This, in turn, suggests any subsequent pullback is more likely to find decent support near the 0.6935-0.6925 confluence support. The said region comprises the 200-period SMA on the 4-hour chart and the 23.6% Fibo. level.

Sustained weakness below the latter will suggest that this week's recovery move has run out of steam and make the AUD/USD pair vulnerable. Spot prices could then break through the 0.6900 mark and test the 0.6860-0.6855 horizontal support. Some follow-through selling will be seen as a fresh trigger for bearish traders.

On the flip side, the 50% Fibo. level, just ahead of the 0.7000 mark, now seems to act as an immediate strong resistance, above which the AUD/USD pair could climb to the 0.7030 area (61.8% Fibo. level). The momentum could further get extended and allow spot prices to aim to reclaim the 0.7100 round-figure mark.

AUD/USD 4-hour chart

Key levels to watch

-

15:01

Mexico Current Account, $ (QoQ) above expectations ($-2800M) in 2Q: Actual ($-704M)

-

15:01

Mexico Accumulated Current Account/GDP: -0.19% (2Q) vs -1.94%

-

14:37

ECB to hike rates by another 50 bps in September, but an even larger hike is not excluded – Nordea

The accounts of the European Central Bank's (ECB) July policy meeting showed that a large number of members agreed it was appropriate to raise rates by 50 basis points (bps). Therefore, economists at Nordea expect the ECB to hike rates by another 50 bps in September.

All doors are open

“The ECB is now fully in a data-dependent mode with chains from past guidance severed.”

“Most Governing Council members are preoccupied with inflation risks, and large rate hikes are set to continue.”

“We continue to think that the ECB will hike rates by another 50 bps at the next meeting on 8 September, but would not exclude an even larger hike.”

“The benchmark rate at zero remains extremely low and the inflation situation is increasingly worrying, so it is not difficult to find arguments in favour of fast hikes at least in the next few monetary policy meetings.”

-

14:26

US Dollar Index trims losses and reclaims the 108.60 region

- The index fully reverses the initial drop to the 108.00 zone.

- US Q2 GDP revision surprised to the upside at -0.6% QoQ.

- All the attention remains on the start of the Jackson Hole Symposium.

The US Dollar Index (DXY), which gauges the greenback vs. a bundle of its main competitors, manages to back-pedal the initial pessimism and returns to the 108.60 area.

US Dollar Index regains composure after data

Following a drop to as low as the 108.00 zone – or weekly lows – the index regains some balance and now flirts with the 108.60 area despite declining US yields and following upbeat results from the US calendar.

Indeed, another revision of the GDP Growth Rate now sees the economy contracting 0.6% QoQ in the April-June period, while Initial Claims rose by 243K in the week to August 20, also surpassing estimates.

In the meantime, the Jackson Hole Symposium will kick in later in the session amidst investors’ preference now tilted towards a 75 bps rate hike in September and expectations of further support for the Fed’s tightening plans from Chief Powell at his speech on Friday.

What to look for around USD

The resumption of the risk-on mood among investors drags the dollar from the recent test of yearly peaks north of the 109.00 barrier.

Bolstering the dollar’s strength appears the firm conviction of the Federal Reserve to keep hiking rates until inflation looks well under control regardless of a likely slowdown in the economic activity and some loss of momentum in the labour market.

DXY, in the meantime, is poised to suffer some extra volatility amidst investors’ repricing of the next move by the Federal Reserve, namely a 50 bps or 75 bps hike in September.

Looking at the macro scenario, the greenback appears propped up by the Fed’s divergence vs. most of its G10 peers (especially the ECB) in combination with bouts of geopolitical effervescence and occasional re-emergence of risk aversion.

Key events in the US this week: Jackson Hole Symposium, Advanced Q2 GDP Growth Rate, Initial Claims (Thursday) - Jackson Hole Symposium, PCE, Personal Income, Personal Spending, Fed Powell, Final Consumer Sentiment (Friday) - Jackson Hole Symposium (Saturday).

Eminent issues on the back boiler: Hard/soft/softish? landing of the US economy. Escalating geopolitical effervescence vs. Russia and China. Fed’s more aggressive rate path this year and 2023. US-China trade conflict.

US Dollar Index relevant levels

Now, the index is retreating 0.06% at 108.53 and faces the next support at 107.99 (weekly low August 25) seconded by 106.21 (55-day SMA) and then 104.63 (monthly low August 10). On the upside, a break above 109.29 (2022 high July 15) would aim for 109.77 (monthly high September 2002) and then 110.00 (round level).

-

14:00

Belgium Leading Indicator fell from previous -2.8 to -5.8 in August

-

14:00

Russia Central Bank Reserves $ fell from previous $580.6B to $574B

-

13:58

GBP/USD pares intraday gains, retreats to 1.1820-15 area post-US GDP/Jobless Claims

- GBP/USD meets with a fresh supply at higher levels amid a modest pickup in the USD demand.

- Mostly upbeat US data, elevated US bond yields, hawkish Fed expectations underpin the USD.

- The UK’s bleak economic outlook acts as a headwind for sterling and favours bearish traders.

The GBP/USD pair struggles to capitalize on its intraday positive move back closer to the weekly high and attracts some sellers near the 1.1865 area on Thursday. The intraday pullback picks up pace during the early North American session and spot prices retreat to the 1.1815-1.1820 region in reaction to the upbeat US macro data.

The Preliminary US GDP report, the second reading, showed that the world's largest economy contracted by 0.6% annualized pace during the second quarter as compared to the 0.9% fall estimated previously. Adding to this, the Weekly Initial Jobless Claims unexpectedly edged lower to 243K in the week ended August 19 from the previous week's downwardly revised print of 245K. Apart from this, elevated US Treasury bond yields, bolstered by hawkish Fed expectations, assists the US dollar to trim a part of its intraday losses to the weekly low. This turns out to be a key factor that exerts some downward pressure on the GBP/USD pair.

The British pound, on the other hand, continues to be underpinned by a bleak outlook for the UK economy. It is worth recalling that the Bank of England earlier this month indicated that a prolonged recession would start in the fourth quarter. This, to a larger extent, overshadows expectations for a 50 bps rate hike by the BoE in September, suggesting that the path of least resistance for the GBP/USD pair is to the downside. Traders, however, might refrain from placing aggressive bearish bets and prefer to wait for a more hawkish message by Fed Chair Jerome Powell's appearance at the Jackson Hole Symposium on Friday.

Powell's comments will be closely scrutinized for clues about the possibility of a supersized 75 bps Fed rate hike move at the September meeting. This, in turn, will play a key role in influencing the near-term USD price dynamics and provide a fresh directional impetus to the GBP/USD pair. In the meantime, the US bond yields and the broader market risk sentiment could drive the greenback demand, allowing traders to grab short-term opportunities.

Technical levels to watch

-

13:52

EUR/USD Price Analysis: Sell the rallies?

- EUR/USD loses upside momentum after climbing to 1.0030.

- Another test of the 0.9900 region appears well on the cards.

EUR/USD quickly fades the earlier uptick to the area north of the parity level, or new 3-day highs.

The lack of conviction of the earlier bullish attempt leaves the door open to the resumption of the downtrend. Against that, another visit to cycle lows around 0.9900 remains in store in the not-so-distant future. A drop below the 2022 low at 0.9899 (August 23) could sponsor a deeper pullback to the December 2002 low at 0.9859.

In the longer run, the pair’s bearish view is expected to prevail as long as it trades below the 200-day SMA at 1.0832.

EUR/USD daily chart

-

13:39

US: Weekly Initial Jobless Claims decline to 243K vs. 253K expected

- Initial Jobless Claims fell by 2,000 in the week ending August 20.

- US Dollar Index trades flat on the day above 108.50.

There were 243,000 initial jobless claims in the week ending August 20, the weekly data published by the US Department of Labor (DOL) showed on Thursday. This print followed the previous week's print of 245,000 (revised from 252,000) and came in better than the market expectation of 253,000.

Further details of the publication revealed that the advance seasonally adjusted insured unemployment rate was 1% and the 4-week moving average was 247,000, an increase of 1,500 from the previous week's unrevised average.

"The advance number for seasonally adjusted insured unemployment during the week ending August 13 was 1,415,000, a decrease of 19,000 from the previous week's revised level," the DOL further announced.

Market reaction

The US Dollar Index edged higher after this data and was last seen trading virtually unchanged on the day at 108.56.

-

13:35

US: Real GDP contracts by 0.6% in Q2 vs -0.8% expected

- US Q2 GDP growth got revised higher to -0.6% in the second estimate.

- US Dollar Index trades modestly lower on the day near 108.50.

The US economy contracted at an annualized rate of 0.6% in the second quarter, the US Bureau of Economic Analysis' (BEA) second estimate showed on Thursday. This reading came in higher than the flash estimate of -0.9% and surpassed the market expectation of -0.8%.

"In the advance estimate, the decrease in real GDP was 0.9%," the BEA explained in its publication. "The update primarily reflects upward revisions to consumer spending and private inventory investment that were partly offset by a downward revision to residential fixed investment."

Market reaction

The US Dollar Index edged slightly higher after this data and was last seen losing 0.1% on the day at 108.50.

-

13:31

United States Gross Domestic Product Price Index registered at 9% above expectations (8.7%) in 2Q

-

13:31

United States Core Personal Consumption Expenditures (QoQ) meets forecasts (4.4%) in 2Q

-

13:30

United States Personal Consumption Expenditures Prices (QoQ) meets expectations (7.1%) in 2Q

-

13:30

United States Gross Domestic Product Annualized above forecasts (-0.8%) in 2Q: Actual (-0.6%)

-

13:30

United States Initial Jobless Claims below forecasts (253K) in August 19: Actual (243K)

-

13:30

United States Continuing Jobless Claims came in at 1.415M below forecasts (1.442M) in August 12

-

13:30

United States Initial Jobless Claims 4-week average increased to 247K in August 19 from previous 246.75K

-

13:24

USD/JPY Price Analysis: Remains depressed near mid-136.00s, bulls still have the upper hand

- USD/JPY meets with a fresh supply on Thursday amid broad-based USD weakness.

- The Fed-BoJ policy divergence should continue to act as a tailwind for the major.

- The technical set-up also favours bulls and supports prospects for some dip-buying.

The USD/JPY pair comes under some renewed selling pressure on Thursday and slips back below the mid-136.00s during the mid-European session. The pair is currently hovering around the 23.6% Fibonacci retracement level of the recent rally witnessed over the past two weeks or so.

The US dollar hits a one-week high amid some repositioning trade ahead of the Jackson Hole Symposium and turns out to be a key factor exerting downward pressure on the USD/JPY pair. Bearish traders further take cues from a softer tone surrounding the US Treasury bond yields, though the Fed-BoJ policy divergence should help limit any further losses for the major.

The positive outlook is reinforced by the fact that technical indicators on the daily chart are still holding comfortably in bullish territory. Hence, any subsequent downfall is more likely to attract some buyers near the 136.00 mark. This is closely followed by the weekly low, around the 135.80 region and the 135.65-135.55 resistance breakpoint, now turned support.

The latter marks a confluence - comprising the 50-day SMA and the 38.2% Fibo. level - and should act as a strong base for the USD/JPY pair. A convincing break below would suggest that a two-week-old positive trend has run out of steam and set the stage for further losses. The USD/JPY pair might then slide to the 135.00 psychological mark en route to the 50% Fibo. level.

On the flip side, the 137.00-137.10 region seems to have emerged as immediate resistance. Sustained strength beyond has the potential to lift the USD/JPY pair back towards the monthly high, around the 137.70 area. Some follow-through buying would be seen as a fresh trigger for bullish traders and set the stage for an extension of the positive move beyond the 138.00 mark.

USD/JPY daily chart

-637970267381207758.png)

Key levels to watch

-

13:20

US Dollar Index Price Analysis: Weakness seen as a buying opportunity

- DXY seems to have met quite a decent support around 108.00.

- A visit to the 2002 high should not be ruled out near term.

DXY loses momentum and revisits the area of weekly lows in the 108.00 neighbourhood on Thursday.

Despite the corrective move, further still appears in store for the index. That said, bouts of weakness could be deemed as buying opportunities ahead of a probable retest of 109.00 and a potential new visit to the 2022 high at 109.29 (July 14). Above the latter comes the September 2002 top at 109.77 before the round level at 110.00.

In the meantime, while above the 6-month support line around 105.20, the index is expected to keep the short-term positive stance.

Looking at the long-term scenario, the bullish view in the dollar remains in place while above the 200-day SMA at 100.61.

DXY daily chart

-

13:10

GBP/USD needs to clear 1.1870 to remain attractive to bulls

GBP/USD has reclaimed 1.1800 following Wednesday's choppy action. The pair needs to clear 1.1870 to extend its rebound, FXStreet’s Eren Sengezer reports.

Cable could face stiff resistance at 1.1870

“On the upside, 1.1870 (Fibonacci 23.6% retracement of the latest downtrend) aligns as initial resistance. With a four-hour close above that level, additional recovery gains toward 1.1900 (50-period SMA, psychological level) and 1.1940 (Fibonacci 38.2% retracement) could be witnessed.”

“Key technical support is located at 1.1800 (20-period SMA, psychological level). If that level fails, sellers could take action and drag the pair lower toward 1.1750 (static level, end-point of the downtrend) and 1.1720 (Aug. 23 low).”

-

13:08

AUD/USD: Australia/US terms of trade still supporting the aussie – SocGen

The Australian dollar is Thursday’s top currency. Kit Juckes, Chief Global FX Strategist at Société Générale, expects the aussie to strengthen as Australia’s terms of trade out-performance vs the US persists.

AUD also to outperform European currencies

“We warned at the end of July that August is often a tough month for AUD, and a good month for the dollar. In the event, AUD is only marginally weaker against the dollar than it was at the end of July, and it has done better than the yen (which is unusual for the time of year). However, our desire to get long AUD for the Autumn/|Winter is intact and AUD/USD is still below 0.70.”

“Australia’s terms of trade out-performance vs the US persists. The more the Chinese authorities do to stabilize the economy with fiscal measures, and the less they use a weaker currency to help, the better for the AUD.”

“We’re long-term bulls, vs the USD, but also against the European currencies.”

-

13:04

EUR/JPY Price Analysis: The 200-day SMA holds the downside so far

- EUR/JPY keeps the choppy trade around the 136.00 zone.

- The positive outlook remains unchanged above the 200-day SMA.

EUR/JPY fades Wednesday’s downtick and resumes the downside amidst the prevailing erratic performance so far this week.

Extra weakness now appears in store for the cross, with the immediate support at the weekly low at 134.94 (August 16). The loss of this level should expose a deeper pullback to the 200-day SMA, today at 134.18.

While above the latter, the prospects for the pair should remain constructive.

EUR/JPY daily chart

-

13:03

USD/JPY to target July 14 high near 139.40 as BoJ officials remain dovish – BBH

USD/JPY is trading around 136.50 after it was unable to break above 138 earlier this week. Still, economists at BBH expect the pair to eventually test the July 14 high near 139.40.

Bank of Japan to maintain powerful monetary easing

“With risk sentiment improving from China stimulus plans and the BoJ remaining ultra-dovish, the USD/JPY pair should move higher to eventually test the July 14 high near 139.40.”

“MPC member Nakamura said that the current state of the economy doesn’t allow for a change in the bank’s easing bias. We believe Nakamura’s view represents the consensus and supports our view that current policy will be maintained for the foreseeable future. Next meeting is September 21-22 and no change is expected then.”

-

12:41

When is the Preliminary US GDP report and how could it affect EUR/USD?

US Q2 GDP Overview

Thursday's US economic docket highlights the release of the Preliminary GDP print for the second quarter, scheduled at 12:30 GMT. The first revision is expected to show that the world's largest economy contracted by 0.8% annualized pace during the April-June period as against the 0.9% decline estimated previously.

How Could it Affect EUR/USD?

The backwards-looking data might do little to push back against expectations for a further policy tightening by the Fed and fail to provide any meaningful impetus. That said, a downward revision will add to growing worries about a deeper economic global downturn and take its toll on the already weaker risk sentiment. This, in turn, should support the safe-haven greenback.

Conversely, a stronger-than-expected print should reaffirm hawkish Fed expectations and lift the US Treasury bond yields, along with the USD. Apart from this, concerns about an extreme energy crisis in Europe suggest that the path of least resistance for the EUR/USD pair is to the downside and any positive move runs the risk of fizzling out rather quickly.

Eren Sengezer, Editor at FXStreet, offered a brief technical outlook for the EUR/USD pair: “On the four-hour chart, the Relative Strength Index (RSI) indicator recovered to 50, suggesting that sellers refrain from committing to additional losses for the time being. Moreover, EUR/USD broke above the descending regression channel coming from August 12 and the last four-hour candles closed above the 20-period SMA, pointing to a bullish shift in the near-term outlook..”

Eren also outlined important levels to trade the EUR/USD pair: “In case the pair manages to hold above parity and starts using that level as support, 1.0020 (Fibonacci 23.6% retracement of the latest downtrend) aligns as immediate resistance ahead of 1.0060 (50-period SMA) and 1.0080 (Fibonacci 38.2% retracement).”

“On the downside, a four-hour close below parity could open the door for an extended slide toward 0.9960 (20-period SMA) and 0.9920 (end-point of the downtrend),” Eren added further.

Key Notes

• EUR/USD Forecast: Parity proves to be a tough resistance to crack

• EUR/USD could still weaken further – UOB

• EUR/USD: The risk is of a short squeeze all the way to 1.0135 – ING

About US GDP

The Gross Domestic Product Annualized released by the US Bureau of Economic Analysis shows the monetary value of all the goods, services and structures produced within a country in a given period of time. GDP Annualized is a gross measure of market activity because it indicates the pace at which a country's economy is growing or decreasing. Generally speaking, a high reading or a better than expected number is seen as positive for equities, while a low reading is negative.

-

12:37

Fed's George: Too soon to say what to expect in September

Kansas City Fed President Esther George said on Thursday that they still had more work to be done on inflation.

Additional takeaways

"You'd want to see at least 3 months of consistent data to know where things are going."

"Too soon to say what to expect in September, more key data coming."

"Full effects of recent rate hikes may not be seen for some time."

"Want to see more broad-based relief in prices to know inflation is coming off its highs."

"Not hearing things that are consistent with what you hear in a recession."

"Bringing inflation back to our target remains the focus."

"For the near-term thinking about higher interest rates seems reasonable to me."

"Unclear if that will be the case in the longer term."

Market reaction

The US Dollar Index edged slightly higher after these comments and was last seen at 108.38, where it was down 0.2% on a daily basis.

-

12:34

ECB Accounts: Large number of members agreed it was appropriate to raise rates by 50 bps

The accounts of the European Central Bank's (ECB) July policy meeting showed that a "very large number" of Governing Council members agreed that it was appropriate to raise key rates by 50 basis points (bps), as reported by Reuters.

Additional takeaways

"Members agreed that it was appropriate to take further steps on the path of monetary policy normalisation."

"Medium-term inflation risks had also increased."

"Persistently high inflation posed an increasing risk of longer-term inflation expectations becoming unanchored."

"Members unanimously supported the TPI."

"A larger than expected increase, a 50 basis point interest rate hike provided more clarity for market participants."

"Decision to raise interest rates by 50 basis points at the present meeting should be regarded as frontloading the exit."

"The Governing Council was not changing its assessment regarding the terminal rate in the hiking cycle."

Market reaction

The EUR/USD pair showed no immediate reaction to this publication and was last seen rising 0.27% on the day at 0.9992.

-

12:00

Mexico Gross Domestic Product (QoQ) meets expectations (0.9%) in 2Q

-

12:00

Mexico Gross Domestic Product (YoY) in line with expectations (2%) in 2Q

-

11:08

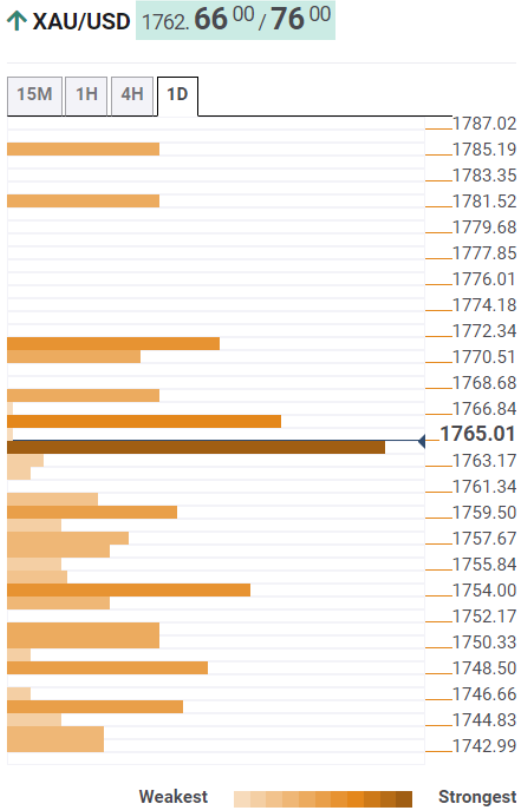

Gold Price Forecast: XAU/USD looks north towards $1,782 ahead of Jackson Hole – Confluence Detector

- Gold price extends its recovery rally into a fourth straight day on Thursday.

- Profit-taking on US dollar longs ahead of Jackson Hole supports the bullion.

- XAU/USD eyes $1,782 on a sustained break above the key $1,765 level.

Gold price is extending its three-day recovery rally on Thursday, capitalizing on the ongoing correction in the US dollar across the board. China announced additional economic stimulus to support growth late Wednesday, which has lifted the overall market mood and reduced the safe-haven demand for the greenback. Further, investors are resorting to position readjustment ahead of the critical US events, in the form of the Fed’s Jackson Hole Symposium and Friday’s Chair Jerome Powell’s speech. The US Treasury yields are retreating from multi-week highs, offering additional support to the non-yielding bullion. Markets are eagerly awaiting the remarks from Powell for fresh clues on the Fed’s tightening path and his outlook on the economy as well as on inflation.

Also read: Gold Price Forecast: Will the XAU/USD recovery extend ahead of Jackson Hole?

Gold Price: Key levels to watch

The Technical Confluence Detector shows that the gold price is challenging powerful resistance at $1,765, the convergence of the Fibonacci 61.8% one-month, pivot point one-day R2 and the previous high four-hour.

The next immediate hurdle is seen at $1,767, the SMA10 one-day, above which the confluence of the SMA50 one-day and the pivot point one-day R3 is aligned at $1,772.

A sustained move above the latter will kickstart a fresh upswing towards the Fibonacci 61.8% one-week at $1,782.

Alternatively, the metal could find some comfort at around $1,759, the Fibonacci 23.6% one-week. The Fibonacci 23.6% one-day at $1,754 could come to the rescue of buyers should the retreat extend.

A dense cluster of support levels around $1,750 will be next on sellers’ radars. That demand area is the intersection of the SMA200 four-hour, SMA5 one-day and Fibonacci 61.8% one-day.

Here is how it looks on the tool

About Technical Confluences Detector

The TCD (Technical Confluences Detector) is a tool to locate and point out those price levels where there is a congestion of indicators, moving averages, Fibonacci levels, Pivot Points, etc. If you are a short-term trader, you will find entry points for counter-trend strategies and hunt a few points at a time. If you are a medium-to-long-term trader, this tool will allow you to know in advance the price levels where a medium-to-long-term trend may stop and rest, where to unwind positions, or where to increase your position size.

-

10:57

Silver Price Analysis: XAG/USD hits one-week high, eyes $19.50 confluence resistance

- Silver catches strong bids on Thursday and jumps to a fresh weekly high.

- Sustained strength beyond the 23.6% Fibo. level favours bullish traders.

- Mixed technical indicators on daily/hourly charts warrant some caution.

Silver gains strong positive traction on Thursday and climbs to a fresh weekly high, around the $19.40 region during the first half of the European session.

The momentum lifts the XAG/USD beyond the 23.6% Fibonacci retracement level of the $20.88-$18.75 slide and supports prospects for additional gains. The constructive outlook is reinforced by the fact that oscillators on hourly charts have been gaining positive traction.

That said, technical indicators on the daily chart are yet to confirm a bullish bias, suggesting that any subsequent move up might confront stiff resistance near the $19.50 confluence. The said barrier comprises 38.2% Fibo. level and the 200-period SMA on the 4-hour chart.

Some follow-through buying, however, will set the stage for an extension of the recent bounce from a multi-week low, around the $18.70 region touched on Monday. The XAG/USD might then test the 50% Fibo. level, around the $19.80 region, aim to reclaim the $20.00 psychological mark.

On the flip side, the $19.20 area (23.6% Fibo. level) now seems to protect the immediate downside ahead of the $19.00 round figure. A decisively break below could make the XAG/USD vulnerable to accelerate the fall back towards the weekly low, around the $18.70 region.

The next relevant support is pegged near the $18.45-$18.40 area, below which the downward trajectory could get extended and drag the XAG/USD to the YTD low, around the $18.15 zone touched in July.

Silver 4-hour chart

-637970181559870198.png)

Key levels to watch

-

10:46

Fed's Bostic: Strong data may make a case for another 75 bps rate hike

In an interview with the Wall Street Journal (WSJ), Atlanta Fed President Raphael Bostic said that “at this point, I'd toss a coin between 50 bps and 75 bps,” adding that “if data remains strong and inflation doesn't soften, it may make a case for another 75 bps.”

Additional quotes

Inflation is a big problem.

Some weakening in the economy is to be expected.