Notícias do Mercado

-

20:00

Dow +67.87 15,368.51 +0.44% Nasdaq +5.17 3,721.14 +0.14% S&P +4.1 1,687.52 +0.24%

-

19:20

American focus: the British pound rose against the dollar significantly

Dollar Mixed trend against the euro , moving from growth to decline. Note that the weak retail sales data , coupled with denials of prospects for the appointment of Larry Summers as the new head of the Federal Reserve, sent EUR / USD pair beyond $ 1.3320 , after which the euro has lost momentum , making it possible to show a sharp rise in the dollar , which also plays out.

The White House was forced to issue an official denial excited the market rumors that President Obama intends to nominate Larry Summers to head the Federal Reserve .

President Obama has not yet made a decision on the issue of successor Ben Bernanke as head of the Fed , said White House spokesman Amy Brundage , who wrote on his Twitter account that the " morning reports in the Japanese press are not true ." As for the data, they showed that retail sales rose by a seasonally adjusted 0.2 % in August compared with the previous month , showing a smaller increase than the 0.5 % growth forecast of economists and the smallest increase since April. Most of the increase was due to a surge in car sales, which tend to be unstable and to recover from the recession, while households have made a long-awaited purchase of new cars .

Excluding autos, retail sales rose by only 0.1 %, which is a sign of weakness for the broader discretionary spending .

At the same time, the report contains some positive points : sales in July were stronger than previously thought , and showed an increase of 0.4 % compared to the initial 0.2 %.

We add that the current dynamics of trading is also associated with the upcoming Fed meeting , which is scheduled for next week.

Value of the pound has increased significantly against the dollar, which continues to help the previously reported rate of unemployment . Note that the unemployment rate / p at 7.7 % was lower than expected and made a positive contribution to the overall economic picture of the country. Earlier today it was announced that in the month of July, the volume of production in the construction sector rose a seasonally adjusted 2.2 per cent ( on a monthly basis ) , while recovering from the 1.1 - percent decline, which was recorded in June. Add that led recovery volumes stood 3.2 percentage increase in new construction, as well as an increase of 0.6 percent as repair and maintenance. In addition, the data showed that the annualized construction output rose in July by 2 percent, which was slightly slower than the 2.2 - percent growth , marked by a month earlier . The volume of new work increased by 5.8 percent per year, while the repair work fell by 3.6 per cent .

Despite the downward revisions in the June data , the total score for the 2 nd quarter was revised to increase , but it was not enough to make an impact on GDP. Meanwhile, America has published a statistics block , which was generally negative. The index of consumer sentiment University of Michigan was 76.8 vs. 82.0 .

-

18:20

European stock close

European stocks advanced, extending a second weekly gain for the Stoxx Europe 600 Index, as companies from Fresenius SE to Kabel Deutschland Holding AG rallied following mergers-and-acquisitions activity.

The Stoxx 600 rose 0.2 percent to 311.43 at 4:30 p.m. in London after earlier dropping as much as 0.4 percent. The equity benchmark has gained 1.7 percent this week as investors awaited the next Federal Reserve meeting, while a report showed that Chinese exports grew at a faster-than-expected pace.

The Stoxx 600 fell from its highest level in more than five years yesterday as a report showed the euro area’s industrial output contracted more than forecast.

U.S. Secretary of State John Kerry meets with Russian counterpart Sergei Lavrov in Geneva to discuss a deal to remove Syria’s chemical weapons. Syrian President Bashar al-Assad said that the administration of President Barack Obama must stop its military threats and cease arming rebel groups for the nation to give up its chemical arsenal. Obama delayed a decision on military action after Russia proposed putting the chemical weapons under international control.

In the U.S., a Commerce Department report showed that retail sales rose at a slower pace in August. Purchases climbed 0.2 percent, after increasing a revised 0.4 percent in July. The median forecast survey had called for sales to increase 0.5 percent.

The retail report was one of the last pieces of data before the Fed meeting on Sept. 17-18 when policy makers will discuss whether to reduce their monthly bond purchases. Chairman Ben S. Bernanke has said that the central bank may consider tapering if the economy continues to grow in line with its forecasts.

National benchmark indexes climbed in 11 of the 18 western-European markets.

FTSE 100 6,583.8 -5.18 -0.08% CAC 40 4,114.5 +7.87 +0.19% DAX 8,509.42 +15.42 +0.18%

Fresenius increased 3.6 percent to 91.10 euros and Rhoen-Klinikum rallied 11 percent to 19.45 euros. The boards of both German companies endorsed the deal for Fresenius’s Helios unit to buy 43 hospitals from Rhoen-Klinikum. The deal requires regulatory approval and the support of minority shareholders and the former owners of some of the hospitals. Fresenius said that the purchase will add 2 billion euros in annual revenue and 250 million euros in earnings before interest, taxes, depreciation and amortization.

Kabel Deutschland jumped 6.3 percent to 91.82 euros, the highest price since its initial public offering in March 2010. Vodafone Group Plc said that at least 75 percent of the German company’s shareholders supported its 7.7 billion-euro bid before yesterday’s deadline expired. Kabel Deutschland investors who haven’t tendered their shares will get a second chance to do so from Sept. 17 to Sept. 30.

Carlsberg A/S gained 1.6 percent to 579 kroner. The brewer predicted that it will sustain the 5 percent organic-sales growth in the China from the first half. Separately, Goldman Sachs Group Inc. raised the stock to neutral, the equivalent of hold, from sell. The brokerage cited the improving economy in Europe and cost-saving measures.

BHP Billiton slid 2 percent to 1,885 pence and Anglo American, the world’s largest platinum producer, lost 3.2 percent to 1,568.5 pence as a gauge of mining companies posted the biggest decline of the 19 industry groups in the Stoxx 600.

TDC dropped 3.1 percent to 46.41 kroner as a group of private-equity firms sold its stake in the company for 4.17 billion-krone ($744 million). NTC sold 90 million shares at 46.30 kroner apiece. That amounted to an 11 percent stake in TDC, (TDC) according to JPMorgan Chase & Co. which managed the sale.

-

17:00

European stock close: FTSE 100 6,583.8 -5.18 -0.08% CAC 40 4,114.5 +7.87 +0.19% DAX 8,509.42 +15.42 +0.18%

-

16:40

Oil: an overview of the market situation

Oil prices declined moderately today , closer to $ 112 per barrel (Brent) and $ 108 (WTI), after the foreign ministers of the United States and Russia have agreed that it is worth the effort to end the civil war in Syria. Note that the settlement of the question for the elimination of chemical weapons just raised hopes for a more meaningful negotiations .

Expectations of an imminent U.S. attack on Syria helped overcome Brent crude above $ 117 at the end of August, as investors were concerned that the conflict may cause a decrease in the volume of production in the Middle East region , which holds about one third of the world 's oil reserves. But this tension eased somewhat over the past few days , as U.S. Secretary of State , John Kerry, and Russian Foreign Minister Sergey Lavrov is trying to resolve the prevailing conflict in a peaceful way, namely to remove chemical weapons in Syria.

Although world oil markets remain under stress , and the amount of Libyan exports decreased more than 1 million barrels per day due to civil unrest and strikes, investors expect supply growth already in the next few months.

Meanwhile , we add that a partial influence on the bidding had U.S. data . As it became known, retail sales rose by a seasonally adjusted 0.2 % in August compared with the previous month , showing a smaller increase than the 0.5 % growth forecast of economists and the smallest increase since April.

Most of the increase was due to a surge in car sales, which tend to be unstable and to recover from the recession, while households have made a long-awaited purchase of new cars

Excluding autos, retail sales rose by only 0.1 %, which is a sign of weakness for the broader discretionary spending .

At the same time, the report contains some positive points : sales in July were stronger than previously thought , and showed an increase of 0.4 % compared to the initial 0.2 %.

Consumers account for over two-thirds of demand in the U.S. economy , and they have been the main driving force behind the recovery that remains weak by historical standards .

The cost of the October futures on U.S. light crude oil WTI (Light Sweet Crude Oil) fell to $ 107.93 a barrel on the New York Mercantile Exchange.

October futures price for North Sea Brent crude oil mixture rose $ 0.89 to $ 112.07 a barrel on the London exchange ICE Futures Europe.

-

16:20

Gold: an overview of the market situation

Gold prices fell markedly today , reaching a five-week low at the same time , and lead to the largest weekly decline ha last two months, the prospects that the United States will reduce the amount of stimulus measures in the near future . Also on the bidding influences decrease fears of a military operation against Syria. However, after the price of gold rose slightly , departing from the minimum values , but in spite of this, is still trading lower.

U.S. and Russia have begun talks on Thursday , trying to flesh out a plan for the disposition of Moscow mimic weapons Syria.

Meanwhile, today it was reported that Syria has become a full member of the International Convention on the Prohibition of Chemical Weapons . This was stated by the authorized representative to the UN, Bashar Jaafar . The move , he said , was made pursuant to an agreement that would allow to avoid being hit on Syria by the United States .

However, several UN functionaries told the press on condition of anonymity that can not yet be definitely state that Syria has fulfilled all the conditions for accession to the convention. According to the official representative of the United Nations , the Syrian application for accession to the Convention is " pending ."

According to Jaafari , the Syrian chemical weapons were part of a system of deterrence against Israel. "Despite the fact that the weapons of deterrence , it is time to join the international agreement. This is a gesture that demonstrates our commitment to ban all weapons of mass destruction ," - said the Syrian diplomat . Recall that Syria was one of the seven countries that have not acceded in 1997 to the Convention on the Prohibition of Chemical Weapons , which requires all participants to eliminate stocks of chemical warfare agents .

Earlier, the UN said yesterday that they had received a request Syria to join the Convention on the prohibition of chemical weapons .

In addition, we add that many market participants are waiting for the meeting FOMC, which will take place next week, and will be able to shed light on the future program of quantitative easing. It is expected that the U.S. Federal Reserve may announce a reduction of monthly purchases of bonds at the end of its two-day meeting on September 18.

The cost of the October gold futures on COMEX today dropped to $ 1316.30 per ounce.

-

15:00

U.S.: Business inventories , July +0.4% (forecast +0.4%)

-

14:55

U.S.: Reuters/Michigan Consumer Sentiment Index, September 76.8 (forecast 82.6)

-

14:46

Option expiries for today's 1400GMT cut

EUR/USD $1.3250, $1.3300, $1.3310, $1.3350

USD/JPY Y98.65, Y99.00, Y99.50, Y99.75, Y99.80, Y100.00

EUR/JPY Y132.50, Y132.75

GBP/USD $1.5800

EUR/GBP stg0.8400

GBP/JPY Y157.50

EUR/CHF Chf1.2355

AUD/USD $0.9200, $0.9205, $0.9210, $0.9220, $0.9230, $0.9300, $0.9330, $0.9350

USD/CAD C$1.0335, C$1.0400

-

14:37

U.S. Stocks open: Dow 15,331.06 +30.42 +0.20%, Nasdaq 3,719.64 +3.67 +0.10%, S&P 1,685.45 +2.03 +0.12%

-

14:27

Before the bell: S&P futures -0.34%, Nasdaq +0.06%

U.S. stock-index futures were little changed as retail sales rose less than forecast and investors awaited a Federal Reserve meeting that may lead to stimulus cuts.

Global Stocks:

Nikkei 14,404.67 +17.40 +0.12%

Hang Seng 22,915.28 -38.44 -0.17%

Shanghai Composite 2,236.22 -19.39 -0.86%

FTSE 6,572.84 -16.14 -0.24%

CAC 4,102.6 -4.03 -0.10%

DAX 8,500.83 +6.83 +0.08%

Crude oil $107.88 -0.66%

Gold $1318.00 -0.95%

-

13:31

U.S.: PPI excluding food and energy, Y/Y, August +1.1% (forecast +1.3%)

-

13:31

Canada: Capacity Utilization Rate, Quarter II 80.6% (forecast 81.3%)

-

13:30

U.S.: Retail sales, August +0.2% (forecast +0.5%)

-

13:30

U.S.: Retail sales excluding auto, August +0.1% (forecast +0.3%)

-

13:30

U.S.: PPI, m/m, August +0.3% (forecast +0.2%)

-

13:30

U.S.: PPI excluding food and energy, m/m, August 0.0% (forecast +0.2%)

-

13:30

U.S.: PPI, y/y, August +1.4% (forecast +1.3%)

-

13:14

European session: the euro rose

07:15 Switzerland Producer & Import Prices, m/m August 0.0% +0.2% +0.2%

07:15 Switzerland Producer & Import Prices, y/y August +0.5% +0.5% +0.2%

09:00 Eurozone ECOFIN Meetings September

09:00 Eurozone Eurogroup Meetings September

Euro rose moderately against the dollar after yesterday analysts from Goldman Sachs Group raised its forecast for the next half a year for the pair eur / usd to $ 1.40 from $ 1.37 previously . According to statements by GS, outlook raised expectations to improve the prospects for economic growth in the euro area , which will lead to an influx of capital into the euro area and help to recover from the financial crisis. Expert Division Goldman Sachs Group, led by the London-based chief currency strategist Thomas Stolper , sees growth in the euro over the next three months to $ 1.38 , against a previous forecast of $ 1.34 .

Of secondary statistics in the region can be noted on the weak data reduction of employment in the euro area. EU statistics agency said Friday that the number of people employed in the 2nd quarter decreased by 0.1 % compared to the first quarter and amounted to 145 million people, which is 1 % less than in the 2 - fourth quarter 2012 . Employment growth has generally lagged behind the growth of production for a few months, so the decline in the second quarter is not surprising. But with the decline in industrial production, which occurred at the beginning of the third quarter, this fact underscores the fragility of the recovery in the euro area.

The yen weakened after his September report to the Cabinet of Japan said that the country is " on the path to economic recovery at a moderate pace ." Recall that at the moment , Japanese Prime Minister Shinzo Abe and the Bank of Japan's attempt to revive the economy and get out of the long-established 15 -year deflation by the unprecedented monetary stimulus programs .

Governor of the Bank of Japan Haruhiko Kuroda on Friday reiterated its support for a sales tax increase , reversing its potentially negative consequences for the economy.

" It is highly probable that the economic growth in Japan will continue to exceed its capacity even after the increase in the sales tax " to 8 % from 5 % in April, Kuroda said at a meeting of the Council on Economic and Fiscal Policy , an advisory body to the Prime Minister Shinzo Abe .

Kuroda stressed that "it is possible to deal with deflation ," and at the same time to rebuild public finances through tax increases.

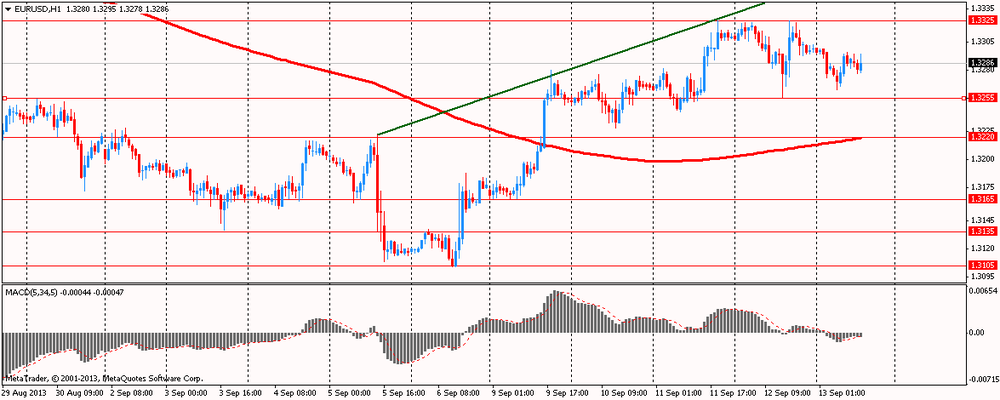

EUR / USD: during the European session, the pair rose to $ 1.3290

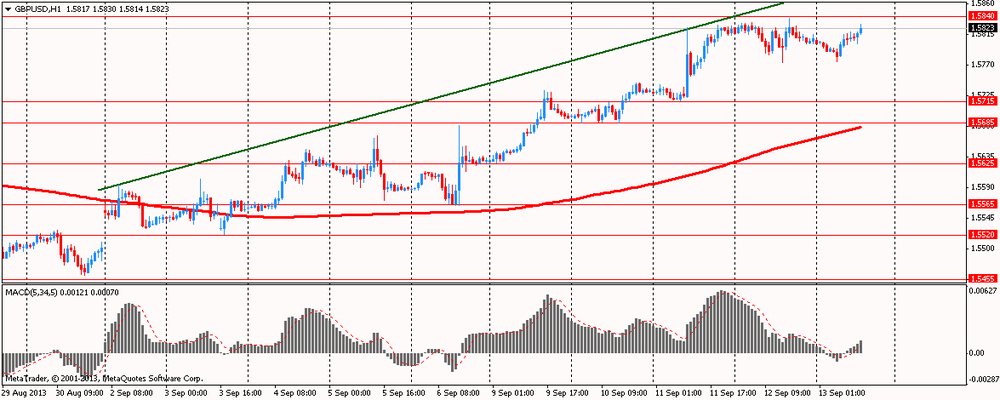

GBP / USD: during the European session, the pair rose to $ 1.5830

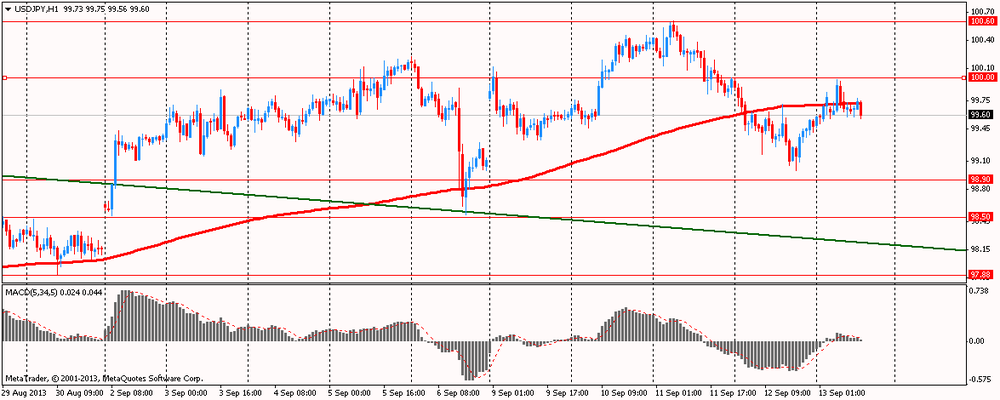

USD / JPY: during the European session, the pair rose to Y99.98

At 12:30 GMT will be released in Canada capacity utilization in Q2 . U.S. at 12:30 GMT will publish the change in retail sales , the change in retail sales excluding auto sales , changes in the volume of retail trade sales , excluding cars and fuel, the producer price index , producer price index excluding prices for food and energy prices in August , at 13:55 GMT - the index of consumer sentiment from the University of Michigan in September, the 14:00 GMT - change in stocks in commercial warehouses in July. At 19:00 GMT the United States will be made by the Treasury report on currency.

-

13:00

Orders

EUR/USD

Offers $1.3350, $1.3325/30, $1.3315

Bids $1.3255/50, $1.3240/30, $1.3210/00, $1.3150/40

GBP/USD

Offers $1.5920/30, $1.5900, $1.5870/80, $1.5840/50

Bids $1.5755/50, $1.5720, $1.5700

AUD/USD

Offers $0.9400, $0.9380/85, $0.9280

Bids $0.9220, $0.9205/00, $0.9155/50

EUR/GBP

Offers stg0.8550/55, stg0.8520, stg0.8460/65, stg0.8440/50, stg0.8425/30

Bids stg0.8380, stg0.8350, stg0.8300

EUR/JPY

Offers Y134.60, Y134.30/40, Y133.80, Y133.50, Y133.00/10, Y132.70

Bids Y132.20, Y132.00, Y131.80/70, Y131.50, Y131.30/20

USD/JPY

Offers Y101.50/55, Y101.00, Y100.80, Y100.60/65, Y100.20/30, Y100.00

Bids Y99.50/40, Y99.00, Y98.60/50

-

11:31

European stocks declined

European stocks declined, paring the Stoxx Europe 600 Index’s second weekly gain, as investors awaited a report on U.S. retail sales, while America and Russia held talks on Syria. U.S. index futures were little changed, while Asian shares also retreated.

The Stoxx 600 fell from its highest level in more than five years yesterday as a report showed the euro area’s industrial output contracted more than forecast. The gauge has still advanced this week amid better-than-expected economic data from China and as U.S. President Barack Obama delayed a decision on military action against Syria.

U.S. Secretary of State John Kerry meets with Russian counterpart Sergei Lavrov in Geneva to discuss a deal to remove Syria’s chemical weapons. Syrian President Bashar al-Assad said that the administration of President Barack Obama must stop its military threats and cease arming rebel groups for the nation to give up its chemical arsenal.

TDC A/S fell 2.9 percent as a shareholder offered a stake of 11 percent in Denmark’s biggest phone company.

Fresenius SE rose 4.1 percent after the health-care company’s Helios unit agreed to buy 43 hospitals from Rhoen-Klinikum AG.

Carlsberg A/S climbed 1.6 percent after forecasting sustained organic sales growth in China for the rest of the year.

FTSE 100 6,571.69 -17.29 -0.26%

CAC 40 4,100.17 -6.46 -0.16%

DAX 8,481.44 -12.56 -0.15%

-

11:15

Eurozone employment falls at slower pace

The pace of decline in the number of employed persons in euro area eased in the second quarter, according to the latest data released by Eurostat on Friday.

Employment fell 0.1 percent quarter-on-quarter to 145 million in the second quarter, slower than a 0.4 percent drop recorded in the first quarter.

On an annual basis, employment fell 1 percent, at the same pace as in the previous quarter.

The number of employed in EU28, including Croatia which joined the bloc in July, remained unchanged from the first quarter. Employment declined 0.4 percent from second quarter of 2012.

Among the member states, Estonia, Lithuania, Portugal, Luxembourg, the Czech Republic and Ireland recorded the highest growth rates compared with the previous quarter. Meanwhile, Cyprus, Spain, the Netherlands, Slovenia and Slovakia registered the largest decreases.

-

10:25

Option expiries for today's 1400GMT cut

EUR/USD $1.3150, $1.3200, $1.3250, $1.3300, $1.3310, $1.3350

USD/JPY Y98.65, Y99.00, Y99.50, Y99.75, Y99.80, Y100.00, Y100.20, Y100.25, Y101.00

EUR/JPY Y130.70, YY132.50, Y132.75

GBP/USD $1.5800

EUR/GBP stg0.8400, stg0.8480/85

GBP/JPY Y157.50

EUR/CHF Chf1.2355

AUD/USD $0.9100, $0.9180, $0.9200, $0.9205, $0.9210, $0.9220, $0.9230, $0.9300, $0.9330, $0.9350

USD/CAD C$1.0240, C$1.0250, C$1.0335, C$1.0400, C$1.0440

-

09:40

Asia Pacific stocks close

Asian stocks fell, with the regional benchmark index snapping an 11-day rally, as the U.S. and Russia hold talks on Syria and investors await the outcome of a Federal Reserve meeting next week.

Nikkei 225 14,404.67 +17.40 +0.12%

Hang Seng 22,893.88 -59.84 -0.26%

S&P/ASX 200 5,219.63 -22.91 -0.44%

Shanghai Composite 2,236.22 -19.39 -0.86%

BHP Billiton Ltd., the biggest mining company, slipped 1 percent in Sydney as metal futures headed for a weekly decline.

Mitsui OSK Lines Ltd., which has the world’s largest merchant shipping fleet, fell 3.5 percent after a gauge of freight rates halted an eight-day rally.

Sun Hung Kai Properties Ltd., the world’s No. 2 developer by market value, dropped 1.8 percent in Hong Kong after setting a lower sales target this year.

-

08:40

FTSE 100 6,573.67 -15.31 -0.23%, CAC 40 4,101.67 -4.96 -0.12%, Xetra DAХ 8,470.26 -23.74 -0.28%

-

08:15

Switzerland: Producer & Import Prices, y/y, August +0.2% (forecast +0.5%)

-

08:15

Switzerland: Producer & Import Prices, m/m, August +0.2% (forecast +0.2%)

-

07:21

European bourses are initially seen trading narrowly mixed Friday: the FTSE down 2, the DAX down 4 and the CAC up 4.

-

07:01

Asian session: The dollar rose versus the yen

04:30 Japan Industrial Production (MoM) (Finally) July +3.2% +3.2% +3.4%

04:30 Japan Industrial Production (YoY) (Finally) July +1.6% +1.6% +1.8%

The dollar rose versus the yen, poised for a second weekly gain, ahead of a report that may show U.S. retail sales accelerated. Consumer purchases in the U.S. climbed 0.5 percent in August after a 0.2 percent increase in July, according to the median forecast of economists surveyed by Bloomberg News before today’s Commerce Department figures.

The yen weakened after Japan’s Cabinet Office said in its September report that the nation is “on the way to recovery at a moderate pace.” Prime Minister Shinzo Abe and the Bank of Japan are trying to revitalize the economy and end 15 years of entrenched deflation through an unprecedented stimulus program.

The euro was near a two-week high after Goldman Sachs Group Inc. upgraded its forecast to $1.40 in six months from $1.37. GS raised its forecast for the euro versus the dollar on the expectation improved growth prospects will boost capital inflows for the region as it recovers from a fiscal crisis. Europe’s common currency will climb to $1.38 in three months compared with a previous forecast for $1.34, analysts led by London-based chief currency strategist Thomas Stolper wrote in a client note on Sept. 12.

EUR / USD: during the Asian session the pair fell to $ 1.3270

GBP / USD: during the Asian session, the pair fell below $ 1.5780

USD / JPY: during the Asian session the pair rose to Y99.85

The calendar quietens down somewhat Friday, although we still have releases on both sides of the Atlantic. French data gets the session underway, with the release of the August Bank of France retail survey. The limited UK data will see the release of the July construction output numbers at 0830GMT. Further eurozone data is set for release at 0900GMT, with the release of the second quarter employment numbers. Also at 0900GMT, the ECOFIN is set to meet in Vilnius, Lithuania. Across the Atlantic, the US calendar gets underway at 1230GMT, when the August retail sales index is released, along with the August producer price index. At 1355GMT, the University of Michigan Sep Consumer Sentiment index is set to be published. At 1400GMT, the July Business Inventories data will cross the wires.

-

06:20

Commodities. Daily history for Sep 12’2013:

GOLD 1,322.40 -41.10 -3.01%

OIL (WTI) 108.64 1.08 1.00%

-

06:20

Stocks. Daily history for Sep 12’2013:

Nikkei 225 -0,26 -37,80 14,387.27%

Hang Seng 22,932.77 -4.37 -0.02%

S & P / ASX 200 5,242.54 8,15 0,16%

Shanghai Composite 2,255.6 14,34 0,64%

FTSE 100 6,588.98 +0.55 +0.01%

CAC 40 4,106.63 -12.48 -0.30%

DAX 8,494 -1.73 -0.02%

Dow -25.96 15,300.64 -0.17%

Nasdaq -9.04 3,715.97 -0.24%

S&P -5.7 1,683.43 -0.34%

-

06:19

Currencies. Daily history for Sep 12'2013:

(pare/closed(00:00 GMT +02:00)/change, %)

EUR/USD $1,3255 -0,41%

GBP/USD $1,5806 -0,10%

USD/CHF Chf0,9303 -0,03%

USD/JPY Y99,49 -0,49%

EUR/JPY Y132,31 -0,57%

GBP/JPY Y157,25 -0,59%

AUD/USD $0,9262 -0,65%

NZD/USD $0,8135 +0,14%

USD/CAD C$1,0326 +0,11%

-

06:00

Schedule for today, Friday, Sep 13’2013:

04:30 Japan Industrial Production (MoM) (Finally) July +3.2% +3.2%

04:30 Japan Industrial Production (YoY) (Finally) July +1.6% +1.6%

07:15 Switzerland Producer & Import Prices, m/m August 0.0% +0.2%

07:15 Switzerland Producer & Import Prices, y/y August +0.5% +0.5%

09:00 Eurozone Trade Balance s.a. July 14.9 15.3

09:00 Eurozone ECOFIN Meetings September

09:00 Eurozone Eurogroup Meetings September

12:30 Canada Capacity Utilization Rate Quarter II 81.1% 81.3%

12:30 U.S. Retail sales August +0.2% +0.5%

12:30 U.S. Retail sales excluding auto August +0.5% +0.3%

12:30 U.S. PPI, m/m August 0.0% +0.2%

12:30 U.S. PPI, y/y August +2.1% +1.3%

12:30 U.S. PPI excluding food and energy, m/m August +0.1% +0.2%

12:30 U.S. PPI excluding food and energy, Y/Y August +1.2% +1.3%

13:55 U.S. Reuters/Michigan Consumer Sentiment Index (Preliminary) September 82.1 82.6

14:00 U.S. Business inventories July 0.0% +0.4%

-

05:32

Japan: Industrial Production (YoY), July +1.8% (forecast +1.6%)

-

05:31

Japan: Industrial Production (MoM) , July +3.4% (forecast +3.2%)

-