Notícias do Mercado

-

23:58

NZD/USD refreshes two-day high at 0.6030 amid an upbeat NZ GDP

- NZD/USD is confidently auctioning above 0.6000 on higher-than-expected NZ GDP data.

- The kiwi economy has grown by 0.4% and 1.7% on an annual and quarterly basis.

- Odd of a full percent rate hike by the Fed has strengthened dramatically.

The NZD/USD pair has established above the psychological resistance of 0.6000 as Statistics New Zealand has reported higher-than-expected Gross Domestic Product (GDP). The economic data has landed higher at 1.7% against the expectations of 1% and the prior contraction of 0.2% on a quarterly basis. Also, the annual reading at 0.4% is higher than the forecasts of 0.2% but remained lower than the former figure of 1.2%.

The kiwi GDP data will have a significant impact on the strategy building of the Reserve Bank of New Zealand (RBNZ) policymakers against the ramping up inflationary pressures. There is no denying the fact that the RBNZ is prepared to sacrifice the growth prospects over containing the red-hot inflation. And, the inflation rate recorded at 7.3% in the second quarter is sufficient to cripple an economy. Well,

This week, investors will also focus on the Business NZ PMI, which indicates the business conditions in the economy. As per the preliminary estimates, the economic data will decline marginally to 52.5 against the prior release of 52.7.

Meanwhile, the US dollar index (DXY) has turned sideways amid the unavailability of any potential trigger, which could provide a decisive move in the counter. After a higher-than-expected reading of the US Consumer Price Index (CPI) data, the commentary from Federal Reserve (Fed) policymakers will be keenly watched by the market participants.

No doubt, the commentary will dictate the continuation of the restrictive stance on monetary policy but unexpectedly increasing core CPI has strengthened the odds of a full 1% rate hike in the September monetary policy meeting.

-

23:50

AUD/JPY Price Analysis: Drops due to Japanese intervention woes

- AUD/JPY edged lower by 0.66% on Wednesday, courtesy of Forex intervention rumors.

- From a daily chart perspective, the pair remains upward biased, but to re-test the YTD high, AUD/JPY buyers need to conquer 97.00.

- Short term, the AUD/JPY is headed south and can fall as low as 95.00, just above the 200-EMA.

The AUD/JPY dropped on Wednesday after the Japanese authorities threatened to intervene in the Forex Markets. So traders, aware of the verbal intervention, bought the yen to the detriment of most G8 currencies. As the Asian Pacific session begins, the AUD/JPY is trading at 96.58, slightly down by 0.02%.

AUD/JPY Price Analysis: Technical outlook

From a daily chart perspective, the AUD/JPY remains upward biased, with the pair bouncing off the daily low at 95.98, just above the 20-day EMA. The good news for AUD/JPY is that the cross-currency stay above the 96.00 figure, keeping risks skewed to the upside, further confirmed by the RSI’s reading at 56.88 in positive territory. If the AUD/JPY tumbles below the 20-day EMA, the pair will slide below the 95.00 figure. Nevertheless, the path of least resistance is to the upside, meaning that a re-test of the YTD high at 98.59 is on the cards.

However, the AUD/JPY bias is neutral-to-downwards in the short term, with immediate resistance at the daily pivot point at 96.74. Break above will expose the 50-day EMA at 96.90, ahead of testing the psychological 97.00 figure, which is also the open of the week. Once it’s cleared, the next supply zone would be the confluence of the 20-EMA and the R1 daily pivot at 97.48.

On the other hand, the AUD/JPY first support would be the 96.00 psychological figure. A breach of the latter will expose the S1 daily pivot at 95.85, followed by the S2 pivot point at 95.12, ahead of the 200-EMA at 94.82.

AUD/JPY Key Technical Levels

-

23:48

New Zealand Gross Domestic Product (QoQ) came in at 1.7%, above forecasts (1%) in 2Q

-

23:48

New Zealand Gross Domestic Product (YoY) above forecasts (0.2%) in 2Q: Actual (0.4%)

-

23:48

New Zealand’s Q2 GDP grew 1.7% QoQ versus 1.0% expected, NZD/USD marches beyond 0.6000

New Zealand’s (NZ) second quarter (Q2) Gross Domestic Product (GDP) grew 1.7% QoQ compared to 1.0% market expectations and a prior contraction of 0.2%, per the latest report from the Statistics New Zealand. The YoY figures came in as 0.4% versus 0.2% expected and 1.2% previous readouts.

Market reaction

Following the data release, the NZD/USD pair extended the previous day’s rebound towards 0.6050.

Also read: NZD/USD remains depressed below 0.6000 mark, lowest since May 2020

About New Zealand GDP

The Gross Domestic Product (GDP), released by Statistics New Zealand, highlights the overall economic performance on a quarterly basis. The gauge has a significant influence on the Reserve Bank of New Zealand’s (RBNZ) monetary policy decision, in turn affecting the New Zealand dollar. A rise in the GDP rate signifies improvement in the economic conditions, which calls for tighter monetary policy, while a drop suggests deterioration in the activity. An above-forecast GDP reading is seen as NZD bullish.

-

23:34

EUR/USD remains lackluster around parity, US Retail Sales, Fed bets eyed

- EUR/USD fails to cheer recently hawkish comments from the ECB policymakers, stays sidelined at weekly low.

- EU announced energy plan but failed to impress Euro buyers.

- Softer US data, mixed concerns surrounding Fed appear to test the traders.

- Risk catalysts, US Retail Sales for August will be important for fresh impulse ahead of next week’s FOMC.

EUR/USD struggles to restore the trader’s confidence while taking rounds to 0.9980-85 during the initial Asian session on Thursday. In doing so, the major currency pair fails to cheer hawkish comments from the European Central Bank (ECB) policymakers, as well as the European Commission’s (EC) release of an energy plan. The reason could be linked to the expectations of more geopolitical tension with Russia and the hawkish Fed hopes.

Recently, ECB policymaker Robert Holzmann has stated that the central bank's rates will be higher in a year but hikes will be data-dependent. Before that, ECB’s Constantinos Herodotou said, “ECB’s latest decision to hike the key rates does not mean there has been a forgone conclusion on the final level of interest rate.” Above all, ECB Chief Economist Philip Lane said on Wednesday that the current transition will require the ECB to continue to raise interest rates over the next several meetings, as reported by Reuters.

Further, the European Commission announced on Wednesday that it proposed a voluntary target for European Union countries to cut overall monthly electricity use by 10% compared to the same period in recent years, as reported by Reuters. “EU proposes windfall levy to claw back surplus profits from fossil fuel companies,” the news also mentioned.

Talking about the data, Eurozone’s Industrial Production fell 2.3% MoM in July versus the 1.0% expected contraction.

On the other hand, US Producer Price Index (PPI) declined to 8.7% YoY in August from 9.8% in July, versus 8.8% market forecasts. Details suggest that the PPI ex Food & Energy, better known as Core PPI, also eased to 7.3% YoY from 7.6% but surpassed the market expectation of 7.1%.

It should be noted that US President Joe Biden’s rejection of US fears and China’s stimulus are some of the key developments that should have favored the risk appetite and the EUR/USD prices. However, the Sino-American tussles and the energy crisis in Europe seemed to have challenged the optimism.

Against this backdrop, the Wall Street benchmarks printed mild gains while the Treasury yields retreated from the multi-day high, posting mild losses at the end.

Looking forward, the US Retail Sales for August, expected to remain unchanged at 0.0%, will be important to watch for clear intraday directions. Also important will be the market bets on the Fed’s next moves.

Also read: Australian Employment Preview: Will labor market upturn save the aussie?

Technical analysis

EUR/USD recovery remains elusive unless crossing the 50-DMA hurdle surrounding 1.0100. However, multiple supports around 0.9950, 0.9900 and the latest multi-year low near 0.9860 could challenge the bears.

-

23:30

When is the NZ Q2 GDP and how could it affect NZD/USD?

NZ Q2 GDP Overview

Thursday's economic docket highlights the release of the second-quarter NZ Gross Domestic Product (GDP) report, scheduled at 10:45 GMT. Having witnessed a 1.2% YoY jump in economic activities during the previous quarter, market players might not get delighted with the estimation of the Q1 GDP figures, an expected 0.2% YoY, as it is insufficient to back the Reserve Bank of New Zealand (RBNZ) for more rate hikes. More interestingly, the QoQ figures are expected to display a significant growth of 1.0% against a contraction of 0.2%.

It is highly observed that RBNZ Governor Adrian Orr is more worried over soaring price pressures rather than saving the economy from a stagnant phase, a meaningful expansion in GDP numbers will trim trouble for the central bank. The RBNZ is consecutively squeezing liquidity from the economy by hiking its Official Cash Rate (OCR), which has reached 3%.

How could it Affect NZD/USD?

The recent carnage in commodity-linked currencies after the release of the US Consumer Price Index (CPI) data is not providing much room for a quick recovery. A release of higher-than-expected headline inflation and core CPI reading has strengthened the odds of a bumper rate hike by the Federal Reserve (Fed) in September. Investors should brace for at least a 75 basis point (bps) rate hike to combat the inflation monster.

Ross J Burland, Editor FXStreet, outlined important technical levels to trade the NZD/USD pair: “the W-formation's support is key. If the bulls commit, then the price will be destined for structure and resistance near the 38.2% Fibonacci level ahead of a 50% retracement thereafter. This is a level that meets the bounce halfway through the sell-off (the green candle) where the 78.6% Fibonacci meets where prices were agreed, so this would be expected to act as the firmest of the resistances.”

Key Notes

NZD/USD remains depressed below 0.6000 mark, lowest since May 2020

NZD/USD Price Analysis: Bulls eye a move to the 38.2% Fibo and beyond

About NZ GDP

The Gross Domestic Product Annualized released by the Statistics New Zealand shows the monetary value of all the goods, services and structures produced within a country in a given period of time. GDP Annualized is a gross measure of market activity because it indicates the pace at which a country's economy is growing or decreasing. Generally speaking, a high reading or a better than expected number is seen as positive for the NZD, while a low reading is negative.

-

23:15

AUD/USD steadies around 0.6750 ahead of Aussie employment data, US Retail Sales

- AUD/USD struggles to extend the previous day’s corrective pullback from weekly low.

- Softer US PPI, mixed concerns surrounding China and Fed test traders.

- Australia’s Consumer Inflation Expectations, employment data for August will be crucial for immediate directions.

- US Retail Sales will be the key ahead of next week’s Fed decision.

AUD/USD treads water around 0.6750 as traders await Australia’s monthly employment numbers during early Thursday in the Asia-Pacific region. The Aussie pair marked a corrective pullback from the weekly low, after witnessing the heaviest daily slump in two years the previous day, but the recovery failed to gain any major fundamental support to prevail ahead of the key data.

On Wednesday, global markets remained sluggish after witnessing heavy volatility, due to the US Consumer Price Index (CPI), the previous day. Even so, the risk appetite improved a bit, or say consolidated, due to the traders’ search for fresh implications.

US Producer Price Index (PPI) declined to 8.7% YoY in August from 9.8% in July, versus 8.8% market forecasts. Details suggest that the PPI ex Food & Energy, better known as Core PPI, also eased to 7.3% YoY from 7.6% but surpassed the market expectation of 7.1%.

With the mixed data for inflation, market players struggled to carry the previous day’s hawkish bias for the Fed, despite expecting either a 0.75% or a full 1.0% rate hike by the US central bank in the next week’s Federal Open Market Committee (FOMC).

Elsewhere, US President Joe Biden’s rejection of US fears and China’s stimulus are some of the key developments that should have favored the risk appetite. However, the Sino-American tussles and the energy crisis in Europe seemed to have challenged the optimism.

Amid these plays, the Wall Street benchmarks printed mild gains while the Treasury yields retreated from the multi-day high, posting mild losses at the end.

Moving on, Australia’s Consumer Inflation Expectations for September, expected 6.7% versus 5.9% prior, will offer immediate directions ahead of the key Aussie jobs report. Forecasts suggest the Aussie Employment Change to increase from -40.9K to 35K while the Unemployment Rate to rise to 66.6% versus 66.4% prior. Even so, the Reserve Bank of Australia’s (RBA) cautious mood might challenge the AUD/USD bulls.

Also read: Australian Employment Preview: Will labor market upturn save the aussie?

Following that, the US Retail Sales for August, expected to remain unchanged at 0.0%, will be important to watch for clear intraday directions.

Also read: US Retail Sales Preview: Can consumers keep up with inflation? A breather could weigh on the dollar

Technical analysis

A two-month-old ascending support line, at 0.6700 by the press time, precedes the yearly low of 0.6680 to restrict short-term downside of the AUD/USD pair. The recovery moves, however, needs validation from the monthly resistance line and the 50-DMA, respectively near 0.6850 and 0.6890 in that order. Overall, AUD/USD is likely to hold lower grounds but could remain range bound.

-

23:07

Silver Price Forecast: XAG/USD advances steadily, eyeing the $20.00 figure

- XAG/USD climbed on a risk-on impulse and lowered US T-bond yields.

- US PPI for August tempered inflationary pressures on the producer side.

- XAG/USD Price Analysis: Break above $20.00 to send silver towards $21.00 mark.

Silver price rebounds at around the 50-day EMA and climbs towards a daily high near $19.69 on Wednesday after the US Labor Department revealed that August PPI was aligned with expectations easing inflationary pressures on the producer side, contrarily to Tuesday’s CPI.

Therefore, the XAG/USD is trading at $19.61, above its opening price by 1.86%.

Before Wall Street opened, US data revealed by the Bureau of Labour Statistics (BLS) showed that the PPI for August shrank by 0.1%, aligned with the consensus, while the year-over-year figure was down at 8.7%, less than July’s 9.8% report. Meanwhile, the so-called core PPI, which excludes volatile items, edged higher, 0.4% MoM, but on an annual reading, edged up by 7.3%.

In the meantime, the US Dollar Index, a measure of the buck’s value against a basket of six currencies, finished Wednesday’s session down by 0.15%, at 109.648, undermined by US Treasury yields, mainly the 10-year benchmark note rate, unmoved during the day at around 3.404%.

The reflection of the abovementioned is the US Dollar Index, losing some traction, down by 0.09%, below the 110.000 mark. At the same time, the US 10-year benchmark note rate shows signs of exhaustion, flat at around 3.414%.

Another tailwind for the white metal prices was that the US 10-year TIPS, a proxy for real yields, gained only one bps, sitting at 0.939%.

On Thursday, the US economic docket will feature unemployment claims, retail sales, and the New York and Philadelphia Fed Manufacturing Indices, a prelude for October’s ISM report.

Silver Price Analysis (XAG/USD): Technical outlook

The XAG/USD daily chart illustrates the white metal as neutral-to-downward biased. However, if silver buyers reclaim the $20.00 mark, that could pave the way for a test of a four-month-old downslope trendline around $20.20 before reaching the 100-day EMA at $20.39. A breach of the latter will expose the August 15 cycle high at $20.87, ahead of the $21.00 psychological level.

-

23:05

Gold Price Forecast: XAU/USD aims to recapture $1,700 as DXY displays momentum loss

- Gold price is attempting a bullish reversal after refreshing its weekly low at $1,693.67.

- The structure of slowing down the pace of hiking interest rates by the Fed is far from over.

- Going forward, the US Retail Sales data will be of utmost importance.

Gold price (XAU/USD) has sensed a buying interest after printing a fresh weekly low of $1,693.67 in the late New York session. The precious metal is required to initially recapture the psychological resistance of $1,700.00 to establish a rebound base and a follow-up recovery extension will be set on autopilot mode. The yellow metal has attempted a recovery as the US dollar index (DXY) is displaying exhaustion signals after a juggernaut rally.

Earlier, gold prices witnessed a bloodbath after a surprise rebound in the US inflation rate. As consensus for the inflation rate was meaningfully lower led by a fall in gasoline prices, investors had started betting that the pace of hiking interest rates by the Federal Reserve (Fed) would slow down now.

The already troublesome job of Fed policymakers is going to be more laborious now as core CPI that excludes food and oil prices has stepped up to 6.3% vs. the expectations of 6.1% and 40 basis points (bps) higher than the prior release.

In today’s session, the US Retail Sales data will be a key trigger. The economic data is not showing any sign of improvement in the overall demand.

Gold technical analysis

The gold prices are attempting to reclaim the prior consolidation area formed in a narrow range of $1,697.12-1,709.62 on an hourly scale. An occurrence of the same will result in a fakeout and the odds of a bullish reversal will get bolstered. However, this is not enough to claim it a bullish reversal as it will require more filters.

The yellow metal is auctioning below the 20-period (High-Low) Exponential Moving Average (EMA) band. The Relative Strength Index (RSI) is oscillating in the 20.00-40.00 range but the downside momentum seems to fade away.

Gold hourly chart

-

22:32

Forex Today: Yen rallies on BoJ verbal intervention, but US dollar bulls perked-up

Here is what you need to know for Thursday, September 15:

The US dollar that fell to a low of 109.257 did not stay down there for long on Wednesday and the index rallied back to test the 109.70s in New York. Technically, the index is on course for the 109.90s again ahead of what is expected to be a hawkish Federal Reserve outcome next week.

Meanwhile, Wednesday's inflation data was more benign, showing producer prices (PPI) declined for a second straight month in August as gasoline prices fell further, but this was not enough for markets to price put the Fed's aggressive stance.

The US Department of Labor reported that August’s Producer Price Index (PPI) moderated, dropping 0.1% MoM, aligned with forecasts, while the annual reading edged lower by a full percentage point to 8.7% vs. 9.8% in the previous month. Core PPI, every month rose by 0.4% but annually exceeded estimations, topping at around 7.3%.

There have been no Federal Reserve speakers this week as the media blackout went into effect at midnight Friday ahead of Chair Jerome Powell’s post-decision press conference on September 21.

Traders expect 75 basis points when its policy committee meets next week and lower market hopes for a smaller increase. However, there is a one-in-five chance that the Fed will raise rates by a full percentage point, up from zero a day before the inflation report according to FEDWATCH. The two-year US Treasury yield, a bellwether for interest rate expectations, rose 3.834% Wednesday.

As for other central banks, the yen rose 1% against the dollar on Wednesday after the Bank of Japan conducted a rate check-in in possible preparation for currency intervention. According to Reuters, central bank officials called up dealers and asked for the price of buying or selling yen. ''However, actually intervening to support the currency would be a larger step.''

At the same time, Japanese Finance Minister Shunichi Suzuki told reporters on Wednesday that recent yen moves have been "rapid and one-sided", adding that yen-buying currency intervention was among the government's options should such moves continue. USD/JPY dropped from a high of 144.96 to a low of 142.55.

The euro was nearly flat against the dollar around 0.9980 but travelled between a high of 1.00236 and 0.99767 on the day.

GBPUSD ranged between 1.1480 and 1.1590 and ended the day higher despite a recovery in the greenback and data that showed that inflation ticked lower in August after breaking the 10% threshold, which was last seen in 40 years.

Ahead of today's labour market data, AUD/USD formed a double bottom near 0.6700 and climbed towards its daily high at 0.6760. It will be a busy day for the antipodeans with New Zealand growth data to start ahead of the Unemployment number later in the session.

New Zealand’s second quarter Gross Domestic Product data are out today. ''We’ve pencilled in a 0.4% quarter-on-quarter expansion, but given data volatility and mixed signals going in, a read plus or minus 1 percentage point of our pick would not surprise,'' analysts at ANZ Bank said.

''And while the RBNZ have growth of 1.8% QoQ pencilled in, we think a disappointment today is unlikely to carry much weight in terms of monetary policy settings. CPI and wage inflation pressures are still way too high, which combined with ongoing fiscal stimulus this fiscal year (the year to 30 June 2023), suggests the RBNZ has little choice but to carry on with OCR hikes to at least 4%. Indeed, in a world of biting capacity limits, weaker than expected activity doesn’t necessarily mean inflation is poised to slow.''

As for the Aussie jobs numbers, ''after the huge disappointment last month, August jobs report may show some modest improvement as indicators of labour demand (e.g., job ads) remain strong,'' analysts at TD Securities argued. ''However, we see downside risk if COVID-related disruptions on the labour market persist. A poor jobs report likely seals the outcome for a 25bps hike (TD: 25bps) in October after the Governor struck a dovish tone last week.''

In crypto, volatility struck as traders positioned in preparation for Ethereum's transition to Proof-of-Stake. Bitcoin and Ethereum have retraced more than 7% over the past 24 hours.

In commodities, gold fell to a low of $1,693.78 from a high of $1,707.07 while WTI came up for air, printing a high of $90.17.

-

21:41

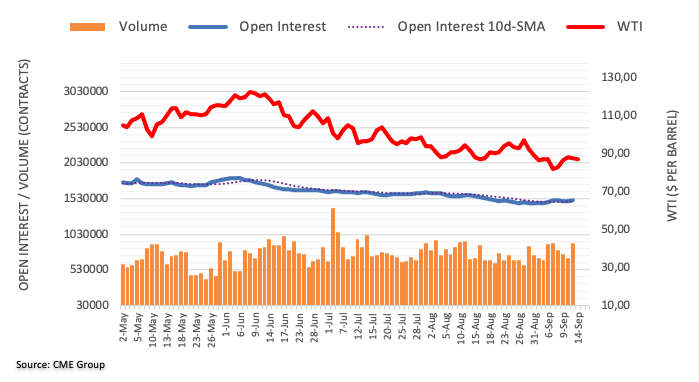

WTI Price Analysis: Bulls come up for air to test key resistance

- WTI is up on the day and testing a key technical level on the 4-hour charts.

- Bulls need a break of the 4-hour resistance or face imminent doom below the weekly countertrend.

WTI oil came up for air on Wednesday and moved in a key area of 4-hour support as the following charts will illustrate. At the time of writing, the black gold is trading 1.5% higher after rallying from a low of $86.20bbls to a high of $90.17bbls on the day so far.

WTI weekly charts

The price recently broke below the weekly trendline support that is in the process of being retested as the above analysis illustrates.

Zooming in, this is made clearer with the price testing the key 89.80s in trade this week.

WTI H4 chart

From a 4-hour perspective, however, the price has formed a W-formation and should the support area hold, there could be a move to test above the resistance which could lead to a break back into the bullish weekly trend.

-

21:35

ECB's Holzmann: Rates will be higher in a year

European Central Bank member Robert Holzmann has stated that the central bank's rates will be higher in a year but hikes will be data-dependent. he adds that they underestimated the pace of inflation gains and that the ECB could have begun hiking sooner.

Key notes

- The Bank has shown its prepared to go beyond expectations.

- There is a possibility of stagflation in the eurozone.

Meanwhile, markets appeared to be returning to normal on Wednesday following the prior day's volatility that came on the back of the US inflation data. The euro regained some composure and is up 0.11% at 0.9977 after recovering from 0.9955 earlier in the day.

-

21:00

Argentina Consumer Price Index (MoM) declined to 7% in August from previous 7.4%

-

20:44

AUD/USD buyers emerged in critical support but are not out of the woods

- Money market futures have fully priced in a 75 bps, though 1 in 4 expect a 100 bps lift.

- The AUD/USD gained some traction bolstered by US dollar weakness.

- AUD/USD Price Analysis: Positive divergence in the daily chart suggests sellers’ exhaustion.

The AUD/USD stopped the bleeding and jumped off weekly lows at around the 0.6700 figure after the US Producer Price Index report for August alleviated some of Tuesday’s CPI worries, which sent most risk assets tumbling, while the greenback rose above the 110.00 thresholds, on renewed inflation fears. Nevertheless, as of writing, sentiment is mixed, though it appears that traders are in wait-and-see mode.

On Wednesday, the major began trading at around 0.6720s and edged toward its weekly lows nearby the 0.6700 figure, forming a double bottom as shown by the AUD/USD hourly chart, and climbed towards its daily high at 0.6760. At the time of writing, the AUD/USD is trading at 0.6737, above its opening price by 0.17%.

US inflation data has been grabbing all the headlines in the last couple of days. On Tuesday, August, core CPI edged above the 7% YoY threshold above estimations, fueling speculations that the Fed might lift rates 100 bps in the September meeting. Nevertheless, August’s Producer Price Index (PPI) has tempered concerns, with figures coming aligned with estimations and flashing positive news regarding supply chain disruptions.

The reflection of the abovementioned is the US Dollar Index, losing some traction, down by 0.09%, below the 110.000 mark. At the same time, the US 10-year benchmark note rate shows signs of exhaustion, flat at around 3.414%.

An absent economic docket left the Aussie adrift to US dollar dynamics. Australian data revealed during the week showed that business confidence improved. Later, Australian employment data would be disclosed. August’s Employment Change is estimated at 35K, while the Unemployment Rate is expected to remain at 3.4%.

On the US front, the US economic calendar will feature Fed’s Regional Manufacturing Indices, alongside unemployment claims and retail sales data for August-

AUD/USD Price Analysis: Technical outlook

The AUD/USD is downward biased, but a doji in the daily chart suggests that selling pressure is evaporating. US dollar positioning is overextended, and with the Relative Strength Index (RSI) printing higher lows, contrarily to price action reaching lower lows, a positive divergence is surging. That said, the major might edge higher ahead of next week’s US FOMC monetary policy decision.

On the upside, resistance lies at 0.6800, which, once cleared, exposes the 20-day EMA at 0.6839, ahead of the 50-day EMA at 0.6890. On the flip side, the AUD/USD first support would be 0.6700, followed by the YTD low at 0.6681 and the 0.6600 figure.

-

20:36

US dollar shows who's boss, rallies back into bullish territory

- DXY bulls are moving back in and 109.72 guards a break to the 109.90s.

- A break of the 109.40s and 109.10s below there opens the risk of a significant downside extension.

The US dollar rallied on Tuesday against the yen, euro and other currencies following stronger-than-expected US inflation data that rocked US stocks, bolstered US yields and sent the greenback towards last week's two-decade peak of 110.79. The price made a high of 110.01 before bears cleaned up across the counterparts for low-hanging fruit in the corrections.

However, while the DXY fell to a low of 109.257, it did not stay down there for long. The index has since rallied back to test the 109.70s which is encouraging for the bulls. Technically, the bulls will want to see 109.90 cleared before the week is out ahead of what is expected to be a hawkish Federal Reserve outcome next week.

There are no Federal Reserve speakers this week as the media blackout went into effect at midnight Friday ahead of Chair Jerome Powell’s post-decision press conference on September 21. Traders expect 75 basis points when its policy committee meets next week and lower market hopes for a smaller increase. However, there is a one-in-five chance that the Fed will raise rates by a full percentage point, up from zero a day before the inflation report according to FEDWATCH.

Yesterday, Consumer Price Index gave the greenback a boost as the headline came at 8.3% YoY vs. 8.1% expected and 8.5% in July, while core came in at 6.3% YoY vs. 6.1% expected and 5.9% in July. ''While this was still the second straight month of deceleration for headline from the 9.1% peak in June to the lowest since April, it’s a huge reminder that the Fed’s fight against inflation is nowhere close to being over,'' analysts at Brown Brothers Harriman explained.

''We think it would be very tempting for the Fed to hike 100 bp in order to underscore its inflation-fighting credentials and surprise the markets,'' the analysts said. ''Equities would tank but that's what the Fed wants. More importantly, the swaps market is now pricing in a terminal rate between 4.25-4.50%.''

Positioning data shows the market is long dollars but not remarkably so by historical standards. Speculators’ net long USD index positions edged slightly higher but remain within the recent range, a little below the levels reached in the run-up to the Fed’s Jackson Hole event. Interest rates have been a major driver of the greenback, as higher rates give dollar bonds and deposits attractive yields. Outside the United States, especially in Asia, major economies' rates trajectories stand in stark contrast which is expected to continue supporting the greenback which is up nearly 15% against a basket of currencies in a rally that has the dollar on course for its best year since 1984.

DXY technical analysis

The four-hour chart above illustrates the market structure and the bulls that are attempting to show who is boss by taking on the M-formation's neckline. 109.72 guards a break to the 109.90s and prospects of a bullish continuation for the days and weeks ahead. A break of the 109.40s and 109.10s below there opens the risk of a significant downside extension.

-

19:34

EUR/USD bounces off weekly lows though stays below parity, amid US dollar weakness

- EUR/USD reached a weekly low at 0.9955, just below the 20-day EMA.

- US economic data fueled expectations of a 100 bps rate hike, with odds lying at 26%.

- Money market futures estimate an ECB 75 bps rate hike in October.

The EUR/USD slightly recovers from yesterday’s losses, advancing almost 0.31%, due to a soft US dollar after August’s US Producer Price Index (PPI) dropped 0.1%, in line with the consensus, though easing fears of inflation becoming entrenched.

On Wednesday, the EUR/USD began trading near the day’s lows at 0.9955 but climbed toward the daily high above 1.0020 before losing the parity again. At the time of writing, the EUR/USD is trading at 0.9985, above its opening price by 0.19%.

Before Wall Street opened, the US Labor Department reported that prices paid by the producer in August contracted as estimated by 0.1%, flashing signs that the supply chain headwinds are easing. In the meantime, the core reading edged up by 0.4%. In the meantime, annual-based numbers in the Producer Price Index (PPI) decelerated from 9.8% in the previous reading to 8.7%, while the core PPI exceeded estimations of 7%, peaking at around 7.3%.

US economic data released during September further cemented the Fed’s case for a 75 bps rate hike. However, the possibility of a 100 bps increase surfaced after Tuesday’s CPI reported that core inflation was stickier than estimated. According to the CME FedWatch Tool, the odds of a 100 bps rate hike lie at 26%.

In the Euro area side, July’s Industrial Production fell 2.3% MoM, vs. a contraction of 1.1% estimated, showing the deterioration in the bloc’s economy. As a result, the annually-based reading fell 2.4%, against expectations of 0%. Weakness in Germany spread toward other larger economies in the Eurozone. Meanwhile, Short Term Interest Rates (STIRs) have priced in an 80% chance of an ECB 75 bps rate hike in October, amidst a 250 bps tightening over the next 12 months.

What to watch

The US economic calendar will feature unemployment claims, the NY and Philly Fed Business Indices, alongside important Retail Sales figures.

EUR/USD Key Technical Levels

-

19:34

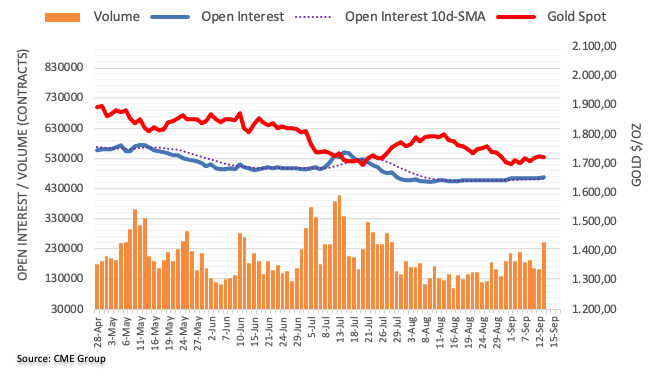

Gold Price Forecast: XAU/USD bears meet critical support, eyes on bullish correction

- Gold is bleeding as the US dollar resurges from the lows of the day.

- Bears need to get below the daily support or face demand into key resistance in the day ahead.

Gold is back under pressure, losing some 0.32% after falling from a high of $1,707.15 to a low of $1,696.51 so far. The US dollar is attempting a comeback and is moving up from the lows of the day down at 109.275 to 109.618 so far, as per DXY.

The DXY is an index that measures the greenback vs a basket of currencies and it has been whipsawed over the US inflation data that was released yesterday which sent markets into a state of higher volatility. Gold has responded with two-way price action and continues to be driven on the back of the market's pricing of the Federal Reserve that meets next week to decide upon its next interest rate hike.

Traders expect 75 basis points when its policy committee meets next week and lower market hopes for a smaller increase. However, there is a one-in-five chance that the Fed will raise rates by a full percentage point, up from zero a day before the inflation report according to FEDWATCH. Inflation in the United States ran at an 8.3% annualized pace in August, ahead of expectations for an 8.0% rise

''Given the persistence of inflation continues to support an aggressive effort by the Fed, we now expect the FOMC to raise the target rate by 75bp at its meeting next week, deliver another 75bp hike in November, and hike a further 50bp in December,'' analysts at TD Securities said.

''We also now expect a higher terminal rate range of 4.25-4.50% by year-end. In this context, while prices are certainly weak, precious metals' price action is still not consistent with their historical performance when hiking cycles enter into a restrictive rates regime. Indeed, gold and silver prices have tended to display a systematic underperformance when markets expect the real level of the Fed funds rate to rise above the neutral rate, as estimated by Laubach-Williams.''

''We expect continued outflows from money managers and ETF holdings to weigh on prices, which will ultimately raise the pressure on a small number of family offices and proprietary trading shops to capitulate on their complacent length in gold.''

Gold technical analysis

In the prior analysis, it was shown that the bulls had been stripped of their moment and the focus was back on the downside while below the neckline of the daily M-formation, as follows:

Zooming out, we could see that the downside target had been a key level for a considerable amount of time:

Gold live update

The daily chart shows that the price is extending the downside with the neckline still vulnerable for a restest, however.

Gold H1 chart

From a much lower time frame basis, hourly and 15 minutes, the price action meeting prior lows and a support structure that needs to be taken into account.

Gold M15 chart

-

18:42

GBP/USD: Renewed downside pressure ahead of the pound – Wells Fargo

Taking into account that the Bank of England’s tightening is set to lag the Federal Reserve and fall short of market expectations, analysts at Wells Fargo expect renewed downside in the pound. They see the GBP/USD pair falling to 1.1200 or below by late 2022/early 2023.

Key Quotes:

“Our outlook for Bank of England rate hikes contrasts with the more aggressive path of tightening expected by the Federal Reserve. It also falls well short of rate hikes currently priced into markets, which anticipate a peak in the Bank of England's policy rate near 4.50% around the middle of 2023. As the Bank of England lags the Fed and falls short of market expectations, we expect the GBP/USD exchange rate to come under renewed pressure, falling to $1.1200 or below by late 2022/early 2023.”

“As the U.S. economy also falls into recession and the Fed reaches the end of its tightening cycle we expect some rebound in the pound, though with the U.K. facing its own economic challenges that rebound should be modest, We forecast a GBP/USD exchange rate of $1.1500 by the end of 2023.”

-

18:01

USD/CHF Price Analysis: Subdued around 0.9610 due to broad US dollar weakness

- US prices paid by producers show signs of easing, except for the core PPI.

- Core inflation in the US is showing signs of being stickier than estimated.

- USD/CHF Price Analysis: Break above 0.9630 puts the 0.9700 figure in play; otherwise, a fall toward 0.9420 is on the cards.

The USD/CHF is trading sideways after rising 0.82% on Tuesday as a reaction to US inflation data showing signs that it’s easing in plain vanilla CPI. Still, core inflation is edging higher on the consumer and producer side, as the US Department of Labor reported. Therefore, the USD/CHF remained almost unchanged but slightly down 0.01%, trading at 0.9613.

USD/CHF Price Analysis: Technical outlook

On Wednesday, the USD/CHF daily chart depicts the pair as neutral-to-downward biased, and it’s worth noting that earlier, the major tested the weekly high at around 0.9633, but broad US dollar weakness put a lid on higher USD/CHF prices.

Meanwhile, the USD/CHF four-hour scale illustrates the pair consolidating above the 20-EMA and the daily pivot point, each at 0.9576 and 0.9574, respectively. Additionally, the 200-EMA at 0.9612 is acting as resistance, keeping the USD/CHF prices subdued and unable to break the daily high at 0.9630.

A clear break above the 200-EMA would open the door for a test of Wednesday’s high at 0.9630, which, once cleared, the major could rally to the R1 pivot point at 0.9668. The break above would expose the confluence of the 50 and 100-EMAs at 0.9700.

On the flip side, the USD/CHF first support would be the confluence of the 20-EMA and the central pivot at 0.9574-76. A breach of the latter will expose the S1 pivot at 0.9515, followed by the September 13 low at 0.9479, followed by the S2 pivot point at 0.9421.

USD/CHF Key Technical Levels

-

17:06

BoE: A close call between 50bps and 75bps – Danske Bank

Next week, the Bank of England will have its monetary policy decision. Consensus points to a 50 bps rate hike but a 75 bps is not ruled out. Analysts at Danske Bank expect fewer hikes than priced in markets as they emphasise the rising recession risk in the UK.

Key Quotes:

“We expect the Bank of England (BoE) to hike the Bank Rate by another 50bp at its next meeting bringing it to 2.25%. Markets are currently pricing around 65-70bp. We expect 50bp as opposed to 75bp, as we are more negative on the growth outlook. Also BoE has had a tendency to surprise to the dovish side at recent meetings.”

“BoE was the first G10 central bank to forecast a recession by Q4 2022 at its last meeting, while using a far more dovish market pricing as policy input than what is currently priced. We see this as a contributing factor to our base case as the growth outlook looks considerably worse now than back then given current market pricing.”

-

16:52

GBP/USD pares some of Tuesday’s losses, back above 1.1560

- UK inflation underpinned the Sterling, appreciating and recovering some ground vs. the buck.

- US prices paid by producers dropped, flashing signs of easing.

- GBP/USD Price Analysis: Break above 1.1600, to open the door for higher prices; otherwise, it might re-test the YTD lows.

The GBP/USD is trimming some of Tuesday’s losses after UK’s CPI showed signs of decelerating, while the US prices paid by producers for August ticked up, particularly in core PPI, in line with Tuesday’s CPI reading.

During the day, the GBP/USD hit a daily low of 1.1479. but edged higher, following the UK’s report, sending the GBP/USD above the 1.1500 figure towards its daily high at around current exchange rates. At the time of writing, the GBP/USD is trading at 1.1565, above its opening price by 0.65%.

The US Department of Labor reported on Wednesday that August’s Producer Price Index (PPI) moderated, dropping 0.1% MoM, aligned with forecasts, while the annual reading edged lower by a full percentage point to 8.7% vs. 9.8% in the previous month. Regarding core PPI, every month rose by 0.4% but annually exceeded estimations, topping at around 7.3%.

On the UK front, the Office for National Statistics (ONS) revealed that inflation ticked lower in August after breaking the 10% threshold, which was last seen in 40 years. Even though it’s good news for the Bank of England (BoE), it would not deter the central bank from increasing rates. Also, the appointment of a new Prime Minister in the figure of Liz Truss keeps market players at bay, waiting for its energy bill plan to kick in.

Analysts at ING wrote in a note that they expect the Bank of England (BoE) to raise rates by 50 bps next week, despite the environment not favoring the British pound. They added, “Slow growth and weaker equity markets should leave sterling as an underperformer.”

What to watch

An absent UK economic docket would keep traders leaning on US dollar dynamics. The US economic calendar will feature unemployment claims, the NY and Philly Fed Business Indices, alongside important Retail Sales figures.

GBP/USD Price Analysis: Technical outlook

The GBP/USD daily chart depicts the pair recovering from weekly lows under the 1.1500 psychological level. A daily close above the September 12 low at 1.1600 would pave the way towards the 1.1700 figure, but a tranche of US economic data, ahead of the FOMC’s meeting, might refrain traders from opening fresh bets vs. the greenback. On the downside, a break below 1.1500 will re-expose the YTD low at 1.1404.

-

16:46

Fed to keep rolling with another 75 bps hike next week – Wells Fargo

Next week, the Federal Reserve will have its monetary policy meeting. Market participants see a 75 basis points rate hike. Analysts at Wells Fargo, point out the September's increase in rates, will be complemented by the reduction in the Fed's balance sheet hitting its full stride.

Key Quotes:

“Another super-sized 75 bps rate hike at next week's FOMC meetings seems all but assured. Employment growth has been robust over the past two months, averaging 421K new jobs in July and August. Headline inflation has been relatively tame over the same period, but falling gasoline prices have accounted for the bulk of the weakness. Excluding food and energy, core inflation has remained far too high for the Fed's liking. Over the past three months, core inflation has risen at a 6.5% annualized rate, more than triple the central bank's 2% target.”

“Next week's meeting will also include an update to the FOMC's Summary of Economic Projections (SEP). We expect the 2022 median projection for the federal funds rate to be 3.875%, up from 3.375% in the June SEP. We think the 2023 median dot probably will be above the 2022 dot, but only modestly so.”

“Despite the hawkish rhetoric, few Fed officials have publicly advocated for a peak federal funds rate that is well above 4%. Our expectation is that the median projection for the 2023 fed funds rate will be 4.175%. For 2024 and 2025, we think the dots will show a steady easing of policy as inflation moves back to 2%. We expect the changes to the SEP inflation projections will be relatively modest, but weaker GDP growth and higher unemployment projections for 2023 seem likely in our view.”

-

16:29

EUR/GBP falls to one-week lows near 0.8600

- EUR/GBP breaks key short-term support.

- Pound recovers ground from multi-month lows.

- UK August CPI annual rate drops below 10% in August.

The EUR/GBP is falling on Wednesday, extending the correction from the highest level in more than a year it reached on Monday at 0.8721. The cross recently bottomed at 0.8624.

The pound gained momentum after breaking the 0.8650 support area. The very short-term outlook points to the downside, while under 0.8650. Below the daily low, the next support stands at 0.8605.

Inflation eases in the UK, IP declines in EZ

Data released in the UK on Wednesday showed inflation eased in August with the annual CPI rate falling from 10.1% to 9.9%, against expectations of a 10.2% reading. It still remains near 40-year highs. Despite the figures, the Bank of England is still expected to raise key interest rates by 50 basis points next week.

On the economic front, Industrial Production showed a decline of 2.3% in the Eurozone against expectations of a more modest decline. The European Central Bank is seen hiking rates again by 75 basis points.

Regarding the energy crisis, the European Union said today it expects to raise €140 billion from windfall taxes on energy companies. The European Commission wants a target to cut electric use by 10%.

Technical levels

-

16:07

ECB's Villeroy: Could reach neutral rate by end of 2022

European Central Bank (ECB) policymaker Francois Villeroy de Galhau said Wednesday that he estimates the euro area neutral rate at below or close to 2% and added that they could reach it by the end of the year, per Reuters.

Additional takeaways

"Monetary normalisation is fully warranted in the euro area, too early to say what the final interest rates will be."

"Until we reach neutral rate, we definitely have to act, in a determined but orderly way."

"Only beyond the neutral rate would tightening begin if needed."

"Not having a forward guidance does not mean, cannot mean, not having a narrative and a monetary strategy."

Market reaction

The EUR/USD pair showed no immediate reaction to these comments and was last seen trading at 1.0002, where it was up 0.32% on a daily basis.

-

15:40

IMF's Georgieva: Central bankers must be stubborn in fighting broad-based inflation

International Monetary Fund (IMF) Managing Director Kristalina Georgieva said on Wednesday that central bankers must be stubborn in fighting broad-based inflation, as reported by Reuters.

"If fiscal policy is not targeted sufficiently, it may become the enemy of the monetary policy, fueling inflation," Georgieva further added.

Market reaction

These comments don't seem to be having a significant impact on risk mood. As of writing, the S&P 500 Index was up 0.3% and the Nasdaq Composite Index was rising 0.5% on a daily basis.

-

15:30

United States EIA Crude Oil Stocks Change above forecasts (0.833M) in September 9: Actual (2.442M)

-

14:58

USD/TRY finally reaches new all-time highs around 18.26

- USD/TRY surpasses 18.26 and clinches new record high.

- The lira drops to a new all-time low vs. the US dollar near 18.30.

- Next event of note in the calendar will be the End Year CPI Forecast.

The Turkish lira depreciates to fresh record lows vs. the greenback and lifts USD/TRY to new all-time highs past 18.26 on Wednesday.

USD/TRY now looks to… 20?

USD/TRY gives away part of the initial advance amidst some renewed dollar weakness and the most likely presence of FX intervention by Ankara.

The pair, in the meantime, keeps well and sound the multi-week side-lined mood above the 18.00 region and against the backdrop of the utter absence of genuine buyers of the Turkish currency.

TRY, in the meantime, is expected to remain under scrutiny ahead of the release of the End Year CPI Forecast later in the week ahead of the key interest rate decision by the Turkish central bank (CBRT) on September 22.

In the domestic docket so far this week, the Unemployment Rate eased to 10.1% in July, while Industrial Production expanded 2.4% YoY in the same month and Retail Sales contracted 0.3% vs. the previous month.

What to look for around TRY

Finally, USD/TRY made up its mind and advanced to new all-time highs past the 18.26 level on Wednesday.

So far, price action around the Turkish lira is expected to keep gyrating around the performance of energy and commodity prices - which are directly correlated to developments from the war in Ukraine - the broad risk appetite trends and the Fed’s rate path in the next months.

Extra risks facing the Turkish currency also come from the domestic backyard, as inflation gives no signs of abating (despite rising less than forecast in July and August), real interest rates remain entrenched well in negative territory and the political pressure to keep the CBRT biased towards low interest rates remains omnipresent.

In addition, there seems to be no other immediate option to attract foreign currency other than via tourism revenue, in a context where official figures for the country’s FX reserves remain surrounded by increasing skepticism.

Key events in Türkiye this week: Budget Balance (Thursday) – End Year CPI Forecast (Friday).

Eminent issues on the back boiler: FX intervention by the CBRT. Progress of the government’s scheme oriented to support the lira via protected time deposits. Constant government pressure on the CBRT vs. bank’s credibility/independence. Bouts of geopolitical concerns. Structural reforms. Presidential/Parliamentary elections in June 23.

USD/TRY key levels

So far, the pair is losing 0.02% at 18.2409 and a breach of 17.8590 (weekly low August 17) would target 17.7919 (55-day SMA) and finally 17.7586 (monthly low August 9). On the upside, the next hurdle appears at 18.2623 (all-time high September 14) seconded by 19.00 (round level).

-

14:51

Gold Price Forecast: XAU/USD shows resilience below $1,700 mark, not out of the woods yet

- Gold reverses an intraday dip to sub-$1,700 levels, though struggles to gain any meaningful traction.

- A modest USD weakness offers some support; bets for more aggressive Fed rate hikes continue to cap.

- Signs of stability in the equity markets also suggest that the path of least resistance is to the downside.

Gold shows resilience below the $1,700 mark for the second successive day and attracts some dip-buying on Wednesday. The XAU/USD sticks to a mild positive bias through the early North American session, though seems to struggle to capitalize on the move and remains below the $1,710 level.

Following the previous day's stronger US CPI-inspired rally, the US dollar edges lower and turns out to be a key factor offering some support to the dollar-denominated commodity. The modest USD downtick lacks any obvious fundamental catalyst and is more likely to remain limited amid expectations that the Fed will keep raising interest rates at a faster pace to tame inflation.

The implied odds for a full 1% rate hike at the September FOMC meeting stands at 34%. Moreover, the markets have also been pricing in another 75 bps rate hike move in November. This, in turn, lifts the yield on the rate-sensitive two-year US government bond to levels last seen in November 2007 and the benchmark 10-year Treasury note holds steady near the YTD peak touched in June.

The prospects for a more aggressive policy tightening by the Fed, along with elevated US Treasury bond yields, favours the USD bulls and caps the non-yielding gold. Apart from this, a modest recovery in the risk sentiment - as depicted by signs of stability in the equity markets - further contributes to keeping a lid on any meaningful upside for the safe-haven precious metal.

Looking at the broader picture, gold has been oscillating in a familiar band over the past two weeks or so. Given that the XAU/USD, so far, has been struggling to gain any meaningful traction, the range-bound price action might still be categorized as a bearish consolidation phase. This, in turn, suggests that the path of least resistance for the commodity is to the downside.

Technical levels to watch

-

14:09

US Retail Sales Preview: Forecasts from six major banks, can the US consumer remain strong?

The US Census Bureau will release the August Retail Sales report on Thursday, September 15 at 12:30 GMT and as we get closer to the release time, here are the forecasts of economists and researchers of six major banks regarding the upcoming data.

US Retail Sales data are set to show no improvement in the overall demand. But the Control Group is what matters, and here, expectations are high. A 0.5% increase is expected.

Commerzbank

“The drop in gasoline prices is lifting consumer sentiment, which is why the usual sentiment indicators recovered noticeably in August. We expect retail sales to rise by 0.4% this month (consensus +0.3%).”

TDS

“We look for retail sales to lose speed in August (-0.5%), following a flat MoM print in July. Spending was likely dented by a sharp drop in gasoline station sales and another retreat in auto sales. We also look for slowing in control group sales to 0.2% following a string of firm MoM increases. Sales in the eating/drinking segment likely fell for the first time in several months.”

NBF

“Car dealers likely contributed negatively to the headline number, as auto sales cooled during the month. Gasoline station receipts, meanwhile, could have declined steeply judging from a drop in pump prices. All told, headline sales could have edged down 0.1% in the month. Spending on items other than vehicles may have been weaker, retreating 0.3%.”

Deutsche Bank

“We expect a +0.6% MoM reading, up from last month's flat print. As gasoline prices continue their downward trend, whether this assuages the inflationary pressures on consumer spending will be important.”

CIBC

“Lower gasoline prices and unit auto sales will weigh on total retail sales in the US in August, but higher volumes at restaurants could have provided a partial offset, leaving total sales down by 0.2% on the month. While the drop in gas prices will have left money on the table for spending elsewhere, it’s likely that that was directed towards services, rather than other goods, where excesses in spending remain. Moreover, the surge in online sales seen in July is unlikely to have been repeated in August, suggesting that the control group of sales (ex. gasoline, autos, building materials, restaurants) likely posted a lacklustre 0.2% advance, a likely contraction in volume terms.”

Wells Fargo

“Retail sales were flat in July, but after accounting for price changes, we estimate real sales rose 0.6%– the first volume gain in three months. Nominal sales likely dipped 0.2% in August, held down by a double-digit decline in gasoline prices last month and a slight decline in vehicle units sold. Savings at the pump, however, are likely to have supported sales in other categories as back-to-school shopping went into full swing. We look for sales ex-autos and gas to post another decent gain for August. Consumer spending has shown resilience this summer. However, with gas prices falling more slowly, borrowing rates rising and the jobs market cooling, we expect the staying power of the consumer to fade over the remainder of the year. Retail spending is likely to feel the pullback to a disproportionate extent after many goods purchases were pulled forward during the pandemic and spending on experiences was put on hold.”

-

13:50

EU proposes windfall levy to claw back surplus profits from fossil fuel companies

The European Commission announced on Thursday that it proposed a voluntary target for European Union countries to cut overall monthly electricity use by 10% compared to the same period in recent years, as reported by Reuters.

Additional takeaways

"EU Commission proposes 180 euros per megawatt hour revenue cap for non-gas fuelled power generators."

"EU revenue cap would apply to wind, solar, biomass, lignite, nuclear and some hydropower generators."

"EU proposes windfall profit levy to claw back surplus profits from fossil fuel companies."

"EU levy would recoup 33% of oil, gas, coal, refining companies' surplus taxable profits in the fiscal year 2022."

"EU levy would apply to fossil fuels companies that have tax obligations in EU countries."

"EU proposes mandatory target for EU countries to cut electricity use 5% during peak price periods."

Market reaction

The shared currency holds its ground following this development and the EUR/USD pair was last seen rising 0.32% on the day at 1.0002.

-

13:34

US: Annual PPI declines to 8.7% in August vs. 8.8% expected

- Annual PPI in US fell at a stronger pace than expected in August.

- US Dollar Index trades modestly lower on the day at around 109.50.

The Producer Price Index (PPI) for final demand in the US declined to 8.7% on a yearly basis in August from 9.8% in July, the data published by the US Bureau of Labor Statistics revealed on Wednesday. This print came in lower than the market expectation of 8.8%.

The annual Core PPI edged lower to 7.3% from 7.6% but surpassed the market expectation of 7.1%. On a monthly basis, the Core PPI was up 0.4% following July's increase of 0.3%.

Market reaction

These figures don't seem to be having an immediate impact on the dollar's performance against its rivals. As of writing, the US Dollar Index was down 0.15% on the day at 109.60.

-

13:31

United States Producer Price Index (MoM) meets expectations (-0.1%) in August

-

13:31

Canada Manufacturing Sales (MoM) in line with expectations (-0.9%) in July

-

13:30

United States Producer Price Index ex Food & Energy (MoM) above expectations (0.3%) in August: Actual (0.4%)

-

13:30

United States Producer Price Index (YoY) below expectations (8.8%) in August: Actual (8.7%)

-

13:30

United States Producer Price Index ex Food & Energy (YoY) came in at 7.3%, above forecasts (7.1%) in August

-

13:07

USD strength to persist into early next year – Rabobank

In the view of economists at Rabobank, the US dollar is set to remain well supported for several months with the hawkish position of the Fed underpinning the attraction of the greenback as a safe haven.

Scope for further dips in EUR/USD below parity

“As the Fed still has a lot of work to do in taming price pressures and ensuring that inflation expectations are well anchored into the medium-term, it can be assumed that the FOMC will not be ready to relinquish its hawkish position just yet. Since this will impact risky assets, we see risk that USD strength persists into early next year.”

“We expect the USD to remain the favoured safe haven relative to either the JPY or the CHF in view of higher US short-term interest rates.”

“Given also that the eurozone is facing a difficult winter which includes the possibility of energy rationing for some businesses, we see scope for further dips in EUR/USD below parity.”

-

13:01

EUR/USD, GBP/USD and most of major crosses to see a period of choppy range-trading – SocGen

Almost every measure of US inflation, other than headline CPI, is rising again. Where do we go now? Kit Juckes, Chief Global FX Strategist at Société Générale, believes that investors should get ready for choppy, more than trending, FX markets.

CPI shock, a Fed peak reprice, but not necessarily a huge dollar rally

“The dollar got a lift, but I don’t think this latest surge can take us very far. The market has pushed up pricing of terminal Fed Funds by almost 50 bps in a week, to above 4%, but the US Dollar Index is pretty much here it was a week ago.”

“It still seems more likely that EUR/USD, GBP/USD and most of the major crosses settle for a period of choppy range-trading, with volatility staying elevated, rather than we see the start of a new dollar uptrend.”

“The yen, however, is likely to remain very difficult to trade. A verbal intervention campaign seems to have begun but a change in monetary policy doesn’t seem imminent.”

-

13:00

Brazil Retail Sales (MoM) registered at -0.8%, below expectations (0.3%) in July

-

12:29

ECB's Lane: Rates to continue to rise over next several meetings

European Central Bank (ECB) Chief Economist Philip Lane said on Wednesday that the current transition will require the ECB to continue to raise interest rates over the next several meetings, as reported by Reuters.

Additional takeaways

"Encouraging market intermediation of government deposits remains desirable in the long term."

"Most measures of longer-term inflation expectations currently stand at around 2%."

"If energy costs were to decline or demand were to weaken over the medium term, it would lower pressures on prices."

"Rate hike has been well transmitted to money market rates."

"Eurozone inflation drivers are of a different nature compared to demand-driven overheating dynamics."

"The appropriate monetary policy for the euro area should continue to take into account that the energy shock remains a dominant driving force."

"Inflation dynamics associated with the energy shock component, to which the euro area is particularly exposed, are of a different nature compared to demand-driven overheating dynamics."

Market reaction

EUR/USD is struggling to preserve its recovery momentum after this report and was last seen gaining 0.25% on the day at 0.9995.

-

12:18

EUR/USD Price Analysis: Next target emerges at 1.0180

- EUR/USD reclaims part of the ground lost on Tuesday’s sell-off.

- Further rebound should target the multi-month line near 1.180.

EUR/USD regains some poise and manages to trim part of the weekly pullback following Tuesday’s slump in the wake of the release of US inflation figures.

If the recovery picks up extra pace, then the interim hurdle comes at the 55-day SMA at 1.0125 prior to the key 7-month resistance line, today near 1.0180. A move beyond the latter is needed to mitigate the downside pressure and allow at the same time a visit to the interim 100-day SMA at 1.0325 prior to the more relevant August high at 1.0368 (August 10).

In the longer run, the pair’s bearish view is expected to prevail as long as it trades below the 200-day SMA at 1.0741.

EUR/USD daily chart

-

12:09

US Dollar Index Price Analysis: Next on the upside comes the 2022 high

- DXY trims part of Tuesday’s intense advance above 110.00.

- Further bouts of strength could see the dollar retest yearly highs.

DXY gives away some gains following the post-CPI sharp upside to the 110.00 region on Wednesday.

Despite the ongoing knee-jerk in the dollar, its short-term bullish view remains unchanged while above the 7-month support line around 106.30.

If sellers push harder, then a potential visit to the weekly low at 107.58 (August 26) could start emerging on the horizon just ahead of the interim 55-day SMA at 107.43.

In the longer run, DXY is expected to maintain its constructive stance while above the 200-day SMA at 101.53.

DXY daily chart

-

12:00

South Africa Retail Sales (YoY) above forecasts (8.4%) in July: Actual (8.6%)

-

12:00

United States MBA Mortgage Applications: -1.2% (September 9) vs previous -0.8%

-

11:58

Silver Price Analysis: XAG/USD sticks to gains near daily high, around mid-$19.00s

- Silver regains positive traction on Wednesday and recovers a part of the overnight decline.

- The emergence of dip-buying favours bullish traders and supports prospects for further gains.

- A convincing break through a multi-month descending trend-line will reaffirm the positive bias.

Silver attracts some buying near the $19.25 region, or the 50-day SMA support on Wednesday and reverses a part of the overnight retracement slide from a nearly four-week high. The white metal maintains its bid tone through the first half of the European session and is currently placed just above the mid-$19.00s.

From a technical perspective, the recent recovery from the $17.55 area, or over a two-year low, stalled on Tuesday near a descending trend-line resistance. The said barrier, currently pegged near the $20.00 psychological mark, extends from May monthly swing high and should act as a pivotal point. A convincing breakthrough will be seen as a fresh trigger for bulls and set the stage for additional gains.

Given that technical indicators on the daily chart have just started moving in the bullish territory, the XAG/USD might then climb to test the 100-day SMA, near the $20.45 region. Some follow-through buying should allow spot prices to aim back to reclaiming the $21.00 round-figure mark. The momentum could get further get extended towards the next relevant hurdle, around the $21.50 area.

On the flip side, the 19.25 region (50 DMA) seems to have emerged as an immediate strong support. This is closely followed by the $19.00 mark, which if broken might trigger some technical selling around the XAG/USD. The subsequent downfall, however, could still be seen as a buying opportunity and remain limited near the $18.45-$18.40 support zone, which should act as a strong base for the metal.

Silver daily chart

Key levels to watch

-

11:56

EUR/JPY Price Analysis: Further downside not ruled out

- EUR/JPY adds to Tuesday’s pullback below the 143.00 yardstick.

- The 138.80 region should offer decent support near term.

EUR/JPY extends the corrective downside for the second session in a row and breaches the 143.00 mark on Wednesday.

The ongoing knee-jerk is not surprising considering the bearish divergence in the daily RSI. That said, the continuation of the decline could extend to the 138.80 zone, where the 55- and 100-day SMAs coincide.

In the meantime, while above the 200-day SMA at 135.08, the prospects for the pair should remain constructive.

EUR/JPY daily chart

-

11:27

USD/JPY flirts with daily low, around 143.00 mark amid chances of BoJ intervention

- USD/JPY meets with a fresh supply and retreats sharply from the 145.00 neighbourhood.

- Jawboning by Japanese authorities points to an imminent intervention and boosts the JPY.

- The emergence of some selling around the USD also contributes to the intraday downfall.

The USD/JPY pair faces rejection near the 145.00 psychological mark and retreats from the vicinity of a 24-year high retested earlier this Wednesday. The downward trajectory extends through the first half of the European session, though the pair manages to rebound a few pips from the daily low and is currently placed just above the 143.00 mark.

A combination of factors fails to assist the USD/JPY pair to capitalize on the previous day's post-US CPI strong rally of over 300 pips. The Japanese yen strengthens across the board amid jawboning by Japanese officials and chances that the Bank of Japan (BoJ) may step in to arrest a freefall in the domestic currency. This, along with the emergence of some US dollar selling, exerts downward pressure on the major.

That said, a recovery in the global risk sentiment - as depicted by a generally positive tone around the equity markets - could cap gains for the safe-haven JPY. Apart from this, a big divergence in the monetary policy stance adopted by the Japanese central bank and the Federal Reserve supports prospects for the emergence of some dip-buying around the USD/JPY pair. The BoJ remains committed to continuing with its monetary easing.

In contrast, the US central bank is expected to keep raising interest rates at a faster pace to tame inflation. The bets were reaffirmed by the stronger US CPI report on Tuesday. The markets quickly started pricing in the possibility of a full 1% rate hike at the next FOMC meeting on September 20-21. This is evident from a fresh leg up in the US Treasury bond yields, which favours the USD bulls and should lend support to the USD/JPY pair.

Nevertheless, the fundamental backdrop remains tilted firmly in favour of bullish traders. Hence, any subsequent decline could still be seen as a buying opportunity and remain limited. Market participants now look forward to the US Producer Price Index (PPI), due for release later during the early North American session. Apart from this, the US bond yields and the broader risk sentiment should provide some impetus to the USD/JPY pair.

Technical levels to watch

-

11:15

ECB's Herodotou: No forgone conclusion on final level of interest rate

The European Central Bank's (ECB) latest decision to hike the key rates does not mean there has been a forgone conclusion on the final level of interest rate, ECB policymaker Constantinos Herodotou said on Wednesday, as reported by Reuters.

Market reaction

EUR/USD preserves its recovery momentum following these comments. As of writing, the pair was trading at 1.0015, where it was up 0.5% on a daily basis. Meanwhile, the Euro Stoxx 600 Index is down 0.4% on the day, pointing to a cautious market mood.

-

10:42

USD/CAD retreats from one-week high amid weaker USD, downside seems cushioned

- USD/CAD surrenders modest intraday gains to the 1.3200 neighbourhood, or a one-week high.

- A positive risk tone weighs on the safe-haven greenback and exerts some downward pressure.

- Aggressive Fed rate hike bets and recession fears warrant caution for aggressive bearish traders.

The USD/CAD pair struggles to capitalize on its intraday positive move to a one-week high set earlier this Wednesday and retreats to the 1.3160-1.3165 area during the first half of the European session. The pullback is sponsored by a modest US dollar weakness, though the fundamental backdrop supports prospects for the emergence of some dip-buying.

A recovery in the global risk sentiment - as depicted by a generally positive tone around the equity markets - seems to weigh on the safe-haven greenback. Apart from this, an intraday bounce in crude oil prices underpins the commodity-linked loonie and exerts some downward pressure on the USD/CAD pair. That said, growing acceptance that the Fed will stick to its aggressive policy tightening path to tame inflation should continue to act as a tailwind for the buck.

Investors started pricing in the possibility of a full 1% rate hike at the next FOMC policy meeting on September 20-21 following the release of stronger US consumer inflation data on Tuesday. This is reinforced by a fresh leg up in the US Treasury bond yields. In fact, the yield on rate-sensitive two-year US government bonds climbs to an almost 15-year high and the benchmark 10-year US Treasury note holds steady just below the YTD peak touched in June.

The prospects for faster rate hikes by the US central bank, along with economic headwinds stemming from fresh COVID-19 curbs in China, have raised concerns about a global recession. Concerns that a deeper economic downturn will dent fuel demand should keep a lid on oil prices, which, in turn, should weigh on the Canadian dollar and offer support to the USD/CAD pair.

Hence, it will be prudent to wait for strong follow-through buying before confirming that the previous day's solid recovery of over 200 pips from the vicinity of mid-1.2900s has run out of steam. Market participants now look forward to the US Producer Price Index (PPI), which, along with the US bond yields and the broader risk sentiment, will influence the USD.

Apart from this, traders will also take cues from oil price dynamics to grab short-term opportunities around the USD/CAD pair. Nevertheless, the bias still seems tilted firmly in favour of bullish traders and any intraday downfall is more likely to remain limited. Bulls, however, might wait for sustained strength beyond the 1.3200 mark before positioning for further gains.

Technical levels to watch

-

10:38

Gold Price Forecast: XAU/USD remains poised to test $1,688 key support – Confluence Detector

- Gold price is licking its wounds near $1,700 after Tuesday’s sharp sell off.

- The US dollar retreats amid a USD/JPY slide and a pause in the yields rally.

- XAU/USD looks south amid a wall of powerful resistance levels.

Gold price is consolidating the previous sell off, as bears are taking a breather before resuming the next leg lower. A pause in the US Treasury yields rally combined with a broad US dollar retreat is offering a temporary reprieve to gold buyers. The bright metal remains vulnerable amid the revival of hopes for aggressive Fed tightening in the coming months. The US inflation data outpaced estimates and squashed the ‘peak inflation’ narrative, suggesting that the Fed will continue with bigger and more rapid rate hikes to control inflation. According to the CME FedWatch Tool, markets are now pricing a 36% chance of a full percentage point Fed rate hike next week. Attention now turns towards the US key events in the second half of the week for fresh trading opportunities in the bullion.

Also read: Gold Price Forecast: XAU/USD eyes 2022 low at $1,681 amid aggressive Fed rate hike bets

Gold Price: Key levels to watch

The Technical Confluence Detector shows that the gold price is eyeing a firm break below the SMA5 four-hour at $1,702 to resume the bearish momentum towards the previous day’s low of $1,697.

Bears will then gear up for a test of the previous week’s low of $1,691, below which the convergence of the pivot point one-day S1 and Bollinger Band one-day Lower at $1,688 will be put at risk.

On the flip side, strong resistance is seen around $1,707, the confluence of the Fibonacci 61.8% one-week and the Fibonacci 23.6% one-day. Acceptance above the latter is needed to offer a fresh boost to XAU bulls.

The next relevant upside target is aligned at $1,710, the meeting point of the Fibonacci 38.2% one-day and SMA10 one-day. Further up, the intersection of the SMA5 one-day and the Fibonacci 38.2% one-week at $1,715 will be the level to beat for bulls.

Here is how it looks on the tool

About Technical Confluences Detector

The TCD (Technical Confluences Detector) is a tool to locate and point out those price levels where there is a congestion of indicators, moving averages, Fibonacci levels, Pivot Points, etc. If you are a short-term trader, you will find entry points for counter-trend strategies and hunt a few points at a time. If you are a medium-to-long-term trader, this tool will allow you to know in advance the price levels where a medium-to-long-term trend may stop and rest, where to unwind positions, or where to increase your position size.

-

10:37

Germany 30-y Bond Auction rose from previous 1.1% to 1.79%

-

10:27

Japan’s Suzuki: If Tokyo were to intervene, it will do so swiftly, without pause

Japanese Finance Minister Shunich Suzuki is on the wires now, via Reuters, making some bold statements on a potential forex market intervention.

Key quotes

Recent yen moves have been quite sharp.

Won't rule out any options, when asked about chance of FX intervention.

No comment on whether Japan conducted rate check.

If Tokyo were to intervene, it will do so swiftly.

If Tokyo were to intervene, it will do so without pause.

Govt watching fx moves with high sense of urgency.

If yen continues to make such moves, we will take necessary action without ruling out any options.

Govt, BOJ will coordinate carefully given recent FX moves.

FX moves have been volatile over the past few days.

MOF usually won't confirm whether it intervened in the market, even after it did so.

Market reaction

USD/JPY showed limited reaction to the above comments, as it kept it range around 143.50, losing 0.72% on the day.

-

10:08

Greece Unemployment Rate (MoM) up to 12.6% in July from previous 12.1%

-

10:02

Eurozone Industrial Production drops 2.3% MoM in July vs. -1.0% expected

Eurozone’s Industrial Production fell more than expected in July, the official data published by Eurostat showed on Wednesday, suggesting that the bloc’s manufacturing sector activity is in the doldrums.

The industrial output in the old continent decreased by 2.3% MoM vs. a 1.0% drop expected and 0.7% last.

On an annualized basis, the industrial output declined by 2.4% in July versus a 0.4% rise expected and June’s 2.4%.

FX implications

The shared currency meets fresh supply following the disappointing Eurozone industrial figures. At the time of writing, EUR/USD is trading at 0.9986, back under parity while still adding 0.18% on the day.

About Eurozone Industrial Production

Industrial Production is released by Eurostat. It shows the volume of production of Industries such as factories and manufacturing. Uptrend is regarded as inflationary which may anticipate interest rates to rise. Usually, if high industrial production growth comes out, this may generate a positive sentiment (or bullish) for the EUR, while low industrial production is seen as a negative sentiment (or bearish).

-

10:00

European Monetary Union Industrial Production w.d.a. (YoY) below expectations (0.4%) in July: Actual (-2.4%)

-

10:00